North America B2C Legal Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

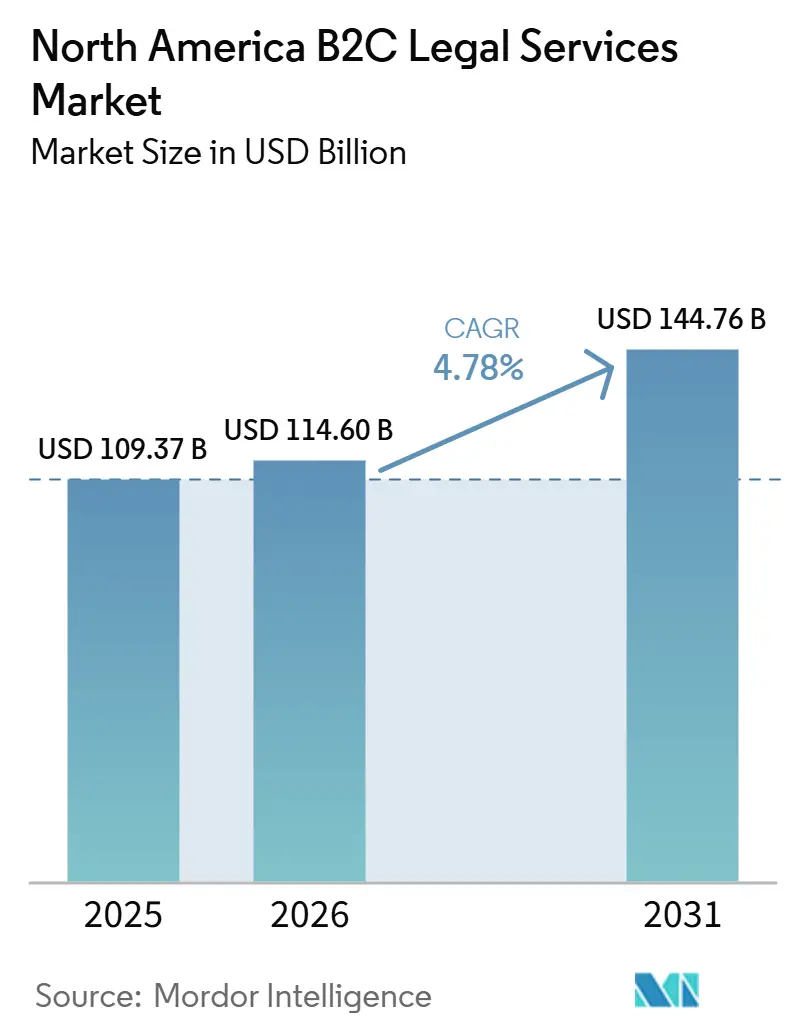

| Base Year Market Size (2025) | USD 109.37 Billion |

| Market Size (2026) | USD 114.60 Billion |

| Market Size (2031) | USD 144.76 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

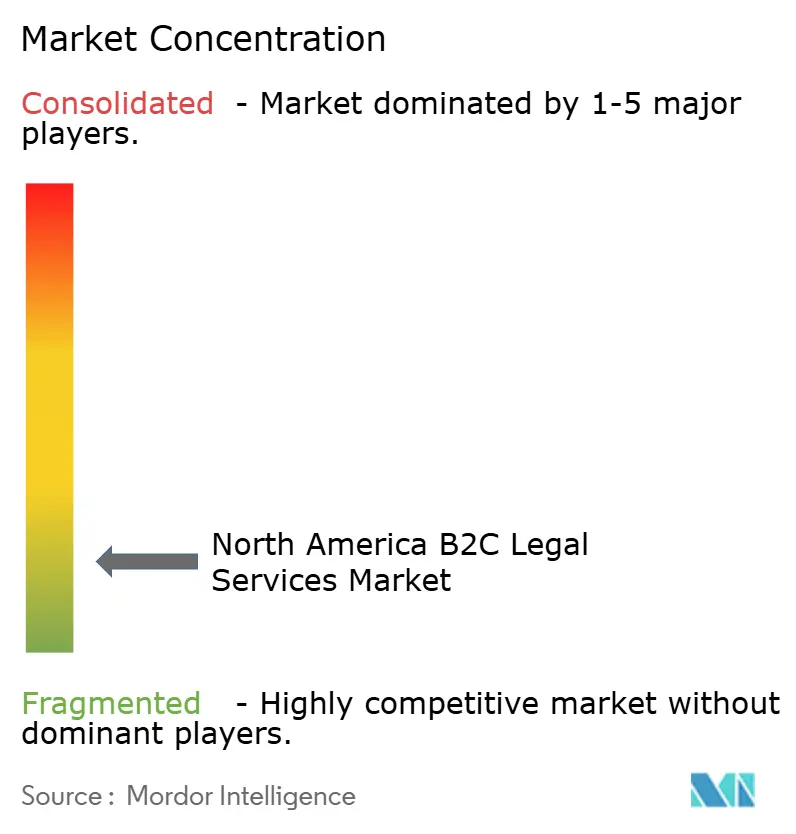

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America B2C Legal Services Market Analysis by Mordor Intelligence

The North America B2C Legal Services Market size is expected to grow from USD 109.37 billion in 2025 to USD 114.60 billion in 2026 and is forecast to reach USD 144.76 billion by 2031 at 4.78% CAGR over 2026-2031.

Structural shifts in how services are delivered and regulated drive this acceleration, not just incremental demand. Ongoing court digitization compresses intake-to-disposition timelines and lowers the friction of client access, which benefits online-first models that can capture and convert demand at scale. Broader acceptance of flat fees, subscriptions, and embedded payments aligns provider economics with consumer expectations while moderating revenue volatility. Regulatory experiments, particularly Arizona’s ABS program, are reshaping ownership and capital models, though multijurisdictional practice rules still limit cross-border scalability. Immigration volumes and an aging population support durable case pipelines in family, humanitarian, and estate planning areas, stabilizing the North America B2C Legal Services market through the cycle.

Key Report Takeaways

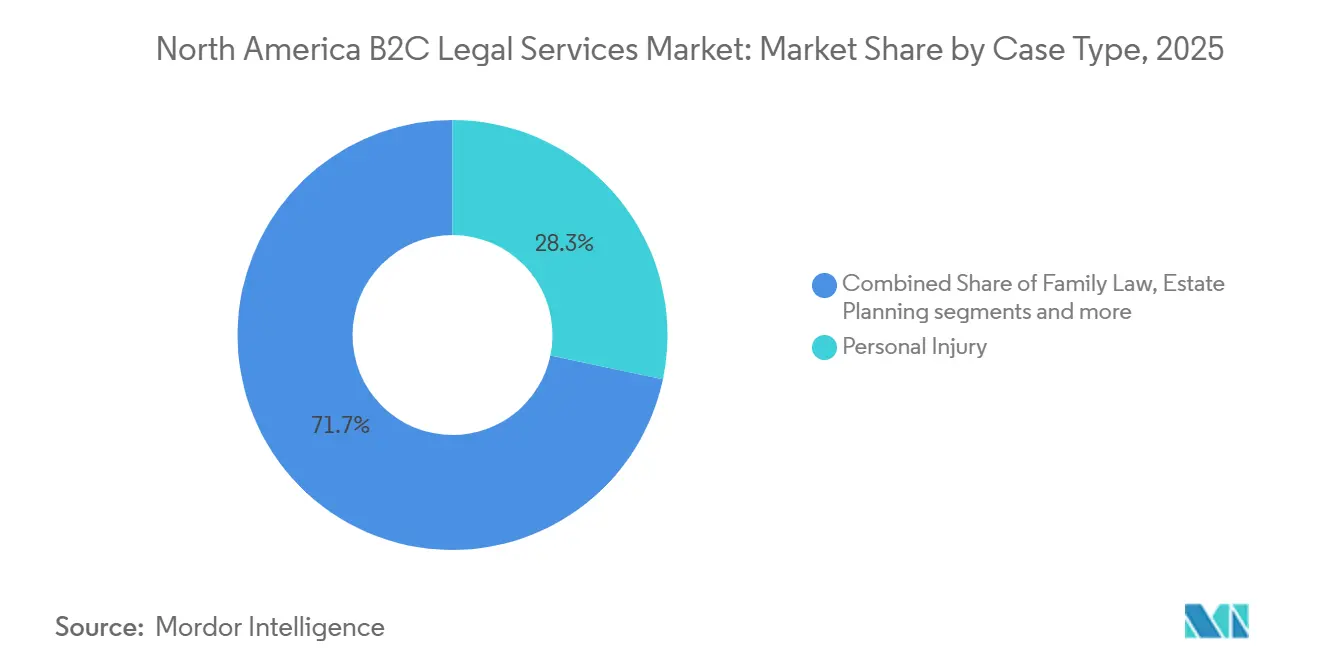

- By case type, Personal Injury led with 28.30% revenue share of the North America B2C legal services market in 2025, while Immigration posted the fastest growth at 7.6% CAGR through 2031.

- By delivery mode, the hybrid channel held 55.50% of the North America B2C legal services market share in 2025; fully virtual platforms are projected to expand at a 12.20% CAGR to 2031.

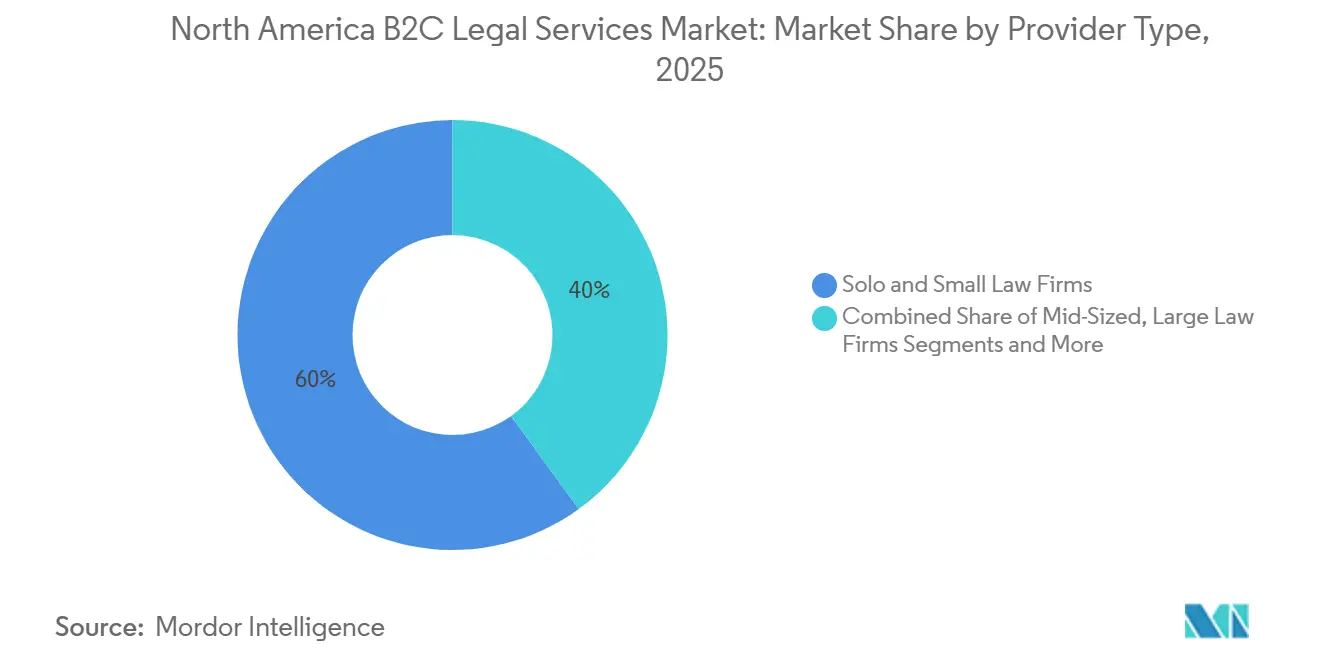

- By provider type, solo and small firms captured a 60.00% share of the North America B2C legal services market in 2025, but online-only platforms are scaling fastest at an 10.40% CAGR to 2031.

- By service type, legal advice represented 40.30% of the North America B2C legal services market size in 2025; legal documentation services are pacing ahead at 9.10% CAGR to 2031.

- By geography, the United States controlled 92.00% of the 2025 revenue of the North America B2C legal services market, whereas Mexico is poised to grow at a 8.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America B2C Legal Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Court digitization and normalized remote hearings reduce access barriers and travel time for consumers | +1.2% | North America-wide, with APAC spill-over in Canada-Asia corridors | Medium term (2-4 years) |

| An aging population accelerates estate planning, probate, and elder law demand | +1.5% | United States & Canada primarily, with minimal Mexico exposure | Long term (≥ 4 years) |

| Immigration inflows and pathway policy shifts sustain family and humanitarian case volumes | +0.9% | United States & Canada, Mexico as origin rather than destination | Short term (≤ 2 years) |

| Consumer preference for flat fees, online payments, and rapid intake boosts conversion in B2C | +1.1% | National, with early gains in major metropolitan areas | Short term (≤ 2 years) |

| ABS and regulatory sandboxes (AZ, UT, DC) catalyze new B2C delivery models and pricing | +0.8% | Arizona, Utah, DC core, indirect influence via competitive pressure nationally | Long term (≥ 4 years) |

| Embedded legal fee financing (BNPL, pay-over-time) increases affordability, and the matter starts | +0.7% | The United States, primarily, is emerging in Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Court digitization and normalized remote hearings reduce access barriers and travel time for consumers

Modernization across courts is shortening case timelines and reshaping client acquisition economics for the North America B2C Legal Services market. The United States judiciary tested new components for the CM/ECF replacement in 2026 with a faster rollout path now expected at district courts, reinforcing the durability of digital-first workflows. California trial courts conduct about 150,000 remote civil proceedings each month, with strong satisfaction among users and court staff, which signals permanence for remote and hybrid hearings. Ontario built out more than 145 courtrooms with virtual-hearing technology and processed over 1.987 million documents electronically in fiscal 2024-2025, while achieving high completion rates for refugee protection matters within 20 months. Mississippi completed statewide e-filing adoption by July 2025, improving docket transparency and real-time access for litigants and attorneys. Utah’s Court Xchange platform lifted digital filings by 42% in the Salt Lake City District Court and doubled pro se initiations in rural San Juan County, illustrating how digital access expands participation beyond urban cores.

An aging population accelerates estate planning, probate, and elder law demand

Demographic change is compressing intergenerational wealth-transfer timelines in Canada and the United States, and low planning penetration creates a clear advisory gap for the North America B2C Legal Services market. By 2030, 22.5% of Canadians are projected to be 65 or older, which lifts demand for wills, powers of attorney, and elder care planning[1]Statistics Canada, “Population Projections for Canada, Provinces and Territories,” Statistics Canada, statcan.gc.ca. Less than a quarter of Canadians over 65 had an estate plan as of 2025, which amplifies the need for accessible planning tools and simple pricing. In the United States, only 32% of adults reported having a will in 2025, even as older cohorts display higher completion rates, underscoring uneven preparation. A USD 105 trillion transfer is expected over 25 years in the United States, with most funds earmarked for heirs and a significant share for charities, which underpins steady growth for estate planning, probate, and related services[2]Anthony Cardillo, “Estate Planning Statistics,” Center on Education and the Workforce, cep-dc.org. Canadian tax changes coming into effect in 2026, including the higher capital gains inclusion rate and a larger Lifetime Capital Gains Exemption, further encourage proactive structuring and trust reviews.

Immigration inflows and pathway policy shifts sustain family and humanitarian case volumes

Immigration continues to support B2C demand across family, humanitarian, and related pathways in the North America B2C Legal Services market. Canada admitted 483,640 permanent residents in 2024, including 105,990 family reunification cases and 76,685 refugees and protected persons, which provided stable work for lawyers and accredited representatives. The Immigration and Refugee Board of Canada finalized a record 102,500 decisions across all divisions in fiscal 2024-2025, even as refugee claim inventory rose, which points to high case volumes and long queues. In the United States, 420,209 asylum applications were processed in fiscal 2024, but the backlog reached 1.347 million cases with a median cycle time above 185 months, which sustains flat-fee advisory and document preparation demand. Family-based I-130 petitions also logged large volumes, reinforcing the pipeline for B2C legal providers focused on reunification and status adjustments. Policy steps like Executive Order 14159 in January 2025 created short-term advisory needs tied to registration and compliance for non-citizens, but broader throughput still depends on administrative capacity and adjudication resources.

Consumer preference for flat fees, online payments, and rapid intake boosts conversion in B2C

Client preference for transparency has shifted revenue models toward flat fees, subscriptions, and embedded payments in the North America B2C Legal Services market. In 2024, 71% of clients preferred flat fees for full cases, and a majority also favored upfront pricing for individual activities, which improves conversion and shortens decision cycles[3]Clio, “Legal Trends for Mid-Sized Law Firms,” Clio, clio.com. Law firms continue to expand alternative fee arrangements, with most United States firms offering AFAs by late 2025, and flat fees are the most common model among AFA users. Embedded payment options such as LawPay’s Pay Later with Affirm and Clio’s Pay Later lower upfront barriers for consumers while providing firms with faster settlement of receivables. Mid-size firms that expand flat-fee use report faster closes and stronger collections, suggesting that pricing clarity compounds with operational gains from intake automation. As AI tools reduce drafting time and automate routine steps, the revenue risk for hourly billing grows, which makes fixed pricing and subscription-based offerings more resilient and consumer-friendly in B2C contexts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State UPL and multijurisdictional licensing rules constrain cross-border virtual scaling | -0.6% | United States state-level fragmentation is less acute in Canada’s provincial system | Medium term (2-4 years) |

| BC’s Enhanced Care no-fault auto regime curtails PI litigation addressable market | -0.3% | British Columbia and Alberta are considering adoption by 2027 | Long term (≥ 4 years) |

| Generative-AI chatbots pose malpractice/UPL risk, tempering automation of front-end advice | -0.4% | Global, with heightened U.S. bar scrutiny | Short term (≤ 2 years) |

| Rising privacy/cyber obligations raise compliance costs for online-only models | -0.2% | North America-wide, stricter enforcement in California and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

State UPL and multijurisdictional licensing rules constrain cross-border virtual scaling

UPL and MJP constraints fragment service delivery models that could otherwise scale with remote hearings and digital filing in the North America B2C Legal Services market. Each U.S. state defines the practice of law independently, and UPL exposure can attach without a showing of consumer harm, which increases risk for national platforms. New York ethics guidance in 2026 set boundaries for participation in out-of-state ABS firms when the predominant effect is in New York, which tightens cross-border fee-sharing conditions[4]New York State Bar Association, “Ethics Opinion 1291,” NYSBA, nysba.org. Multiple courts and bars also set certification or consent requirements for generative AI use, increasing supervisory burdens for multistate practices. In Canada, provincial admissions are still required for cross-provincial representations, which limits national platforms to province-based service footprints. The net effect is higher compliance costs and slower national expansion relative to the potential enabled by court digitization.

BC’s Enhanced Care no-fault auto regime curtails PI litigation

British Columbia’s no-fault auto insurance model has reduced tort-based litigation, which narrows the PI addressable market share in that province within the North America B2C Legal Services market. ICBC reported a 41% year-over-year decline in pending in-province bodily injury claims under the prior legal-based product for fiscal 2024-2025, with about 13,500 litigated claims settled in the year. More than 95% of claims costs now flow directly to customers through benefits rather than litigation outcomes, and the loss adjustment expense ratio is expected to stabilize as legacy legal costs roll off. The legislature appointed a special committee in February 2026 to conduct a comprehensive review of Enhanced Care by May 2026, which may inform future adjustments. Alberta is considering similar changes by 2027, which could extend the PI contraction if adopted. The impact on the overall North America B2C Legal Services market remains modest because the United States accounts for the bulk of consumer PI litigation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Case Type: Personal Injury Incumbents Face Margin Pressure from Virtual Competitors.

Personal injury held 28.30% of the North America B2C Legal Services market share in 2025, and immigration is projected to be the fastest-growing case type at 7.60% CAGR through 2031, reflecting durable demand from pathway shifts and large adjudication backlogs. Estate planning and probate benefit from an aging population and large wealth transfers, while family law and criminal defense track steady demographic baselines rather than policy-sensitive cycles. Bankruptcy and debt relief softened as consumer delinquency patterns normalized from pandemic-era peaks, yet filings remain elevated compared to pre-2020 levels inside many local courts. Large PI firms like Morgan & Morgan expanded in 2025 and 2026, opening new offices and adding attorneys while reporting USD 1.098 billion in verdicts across 295 trials in 2025, which illustrates scale advantages in contingency-fee litigation.

At the same time, virtual competitors pressure traditional PI acquisition models as online-first providers lower lead costs via search, social, and programmatic channels. British Columbia’s Enhanced Care framework materially reduced post-2021 tort litigation, which narrows the provincial PI pool, even as the United States remains the dominant share of the North America B2C Legal Services market. Immigration’s projected 7.60% CAGR is supported by sustained United States asylum volumes, Canadian refugee and protected-person admissions, and large family-based petition flows that generate stable advisory work under flat-fee pricing. Bilingual practices targeting Hispanic communities and cross-border matters stand to gain share as Spanish-language intake grows in the United States metros with high migrant populations.

By Delivery Mode: Fully Virtual Platforms Surge as Hybrid Models Retain Majority Share

Hybrid delivery captured 55.50% share in 2025 as clients combined in-person engagement for critical steps with remote updates and filings for routine events in the North America B2C Legal Services market. Fully virtual platforms are projected to grow at 12.20% CAGR through 2031 on the back of normalized remote hearings and the spread of digital intake and e-filing in high-volume courts. California’s 150,000 monthly remote civil proceedings and Ontario’s substantial document e-filing volumes show how hybrid is now standard operating procedure in the region. Survey evidence from Minnesota indicates most hearing participants prefer remote attendance, which locks in digital access gains.

The North America B2C Legal Services market size for fully virtual models is projected to expand at a 12.20% CAGR between 2026 and 2031, reflecting broad comfort with video consultations and mobile-first workflows among younger cohorts. LegalZoom’s subscription base and rising average order value illustrate how documentation, compliance, and DIFM concierge can scale without bricks-and-mortar buildouts. Hybrid will remain prevalent for complex PI and certain criminal matters where physical presence and rapport building can be decisive, but even these matters benefit from remote discovery and motion practice. Technology investments such as AI-enabled cameras and public participation pods in court innovation labs further reduce the experiential gap between virtual and in-person settings.

By Provider Type: Solo/Small Firms Dominate Share Yet Online-Only Platforms Scale Fastest

Solo and small firms held 60.00% share in 2025 due to local relationships, lower overhead, and community-based referrals in the North America B2C Legal Services market. Online-only platforms are projected to post a 10.40% CAGR through 2031 as they convert scale advantages in intake, document automation, and subscription monetization. Many mid-sized firms are expanding alternative pricing and subscription models, but their slower practice-management adoption limits their ability to fully capture online demand.

The North America B2C Legal Services industry is adopting AI at a rapid rate, which reduces drafting time and threatens revenue under hourly billing, reinforcing the shift to fixed fees and subscriptions. LegalZoom showed rising free cash flow and a strong subscription mix in 2025, proving the scalability of productized services across millions of users. Large PI firms like Morgan & Morgan remain outliers that can scale advertising-driven volume, yet they, too, rely on technology to lift staff productivity and conversion. The net effect is continued share leadership by small firms with faster growth by online-only platforms through 2031.

By Service Type: Legal Advice Leads Share as Documentation Automation Drives Fastest Growth

Legal advice held 40.30% share in 2025 as complex matters still depend on an attorney's judgment within the North America B2C Legal Services market. Legal documentation is projected to be the fastest-growing service type at 9.10% CAGR to 2031 as AI compresses drafting time and consumers embrace fixed-fee packages for standard documents. LegalZoom, Trust & Will, and Rocket Lawyer all expanded documentation-led offerings paired with on-demand human review, which helps balance automation with professionalism.

The North America B2C Legal Services market size for documentation is projected to expand at 9.10% CAGR as fixed-fee bundles make legal access more predictable for DIY and DIFM users. ABA guidance and discipline actions in 2024 and 2025 underscore the need for supervised delivery, which is why leading platforms include attorney consultation or review options for higher-risk documents. With AI adoption now mainstream among legal professionals, providers that integrate automation while preserving ethical compliance will capture the bulk of the documentation growth.

Geography Analysis

The United States held 92.00% of the North America B2C Legal Services market share in 2025, supported by population scale, higher per-capita legal spending, and mature digital infrastructure, while Mexico is projected to grow the fastest at 8.10% CAGR through 2031. Remote-hearing programs and full e-filing rollouts in several U.S. states indicate a lasting shift toward hybrid court operations, which aligns with the scaling model of online-first providers. Arizona’s 136 ABS approvals by April 2025 mark a national leadership position for regulatory experimentation, while Utah’s retrenchment shows how policy design choices steer long-run outcomes. Consumer finance rules, including New York’s BNPL Act, add geographic variation to compliance roadmaps that embedded-payment providers must address.

Canada’s growth corresponds to federal immigration admissions, provincial court digitization, and estate-planning complexity tied to tax changes. The IRB’s 2024-2025 decision volumes and pending inventories highlight high demand that outstrips processing capacity, which sustains case backlogs across refugee protection. British Columbia’s Enhanced Care regime reduces PI litigation and rechannels disputes into benefits administration, which over time stabilizes ICBC’s expense ratios while limiting B2C PI opportunities in the province. Alberta’s evaluation of a similar approach by 2027 will be a key watch point for cross-provincial PI providers.

Mexico’s projected 8.10% CAGR reflects early-stage digitization, expanding middle-class legal needs, and nearshoring dynamics that create cross-border demand for business formation and immigration support in the North America B2C Legal Services market. Regional asylum processing documented sizable application volumes with limited approvals and access challenges, which motivates Spanish-language intake and representation in the United States border states. H-2B visa allocations beyond the annual cap in fiscal 2025 point to ongoing seasonal worker inflows from Mexico and Central America, which support immigration practices that operate across both sides of the border. Bilingual law firms with the United States and Latin America offices continue to expand service footprints for family, humanitarian, and labor pathways.

Competitive Landscape

The North America B2C Legal Services market remains highly fragmented but shows visible concentration among scaled platforms and large contingency-fee firms that can fund mass-market intake. Solo and small firms still hold most provider share, though shrinking moats are evident where virtual competitors reduce acquisition costs and consumer finance tools improve access. Online subscription platforms like LegalZoom report strong subscription revenues and rising average order values, which validate documentation-led and DIFM concierge models for B2C demand. Rocket Lawyer’s AI contract review and Trust & Will’s EstateOS illustrate how product innovation pairs with human review to preserve compliance.

Large PI incumbents continue to invest in office expansion, hiring, and CRM-driven productivity to defend share and lift throughput per staff. Morgan & Morgan’s 2026 announcements detailed a national litigation partnership expansion and reported 2025 trial activity with strong verdict outcomes, which support sustained brand spending and market reach. Mid-sized firms are scaling AFAs and digital payments, yet they lag small firms in practice-management adoption, which opens space for platforms to win on speed, transparency, and price certainty.

Regulatory frameworks are a strategic variable. Arizona’s ABS surge invites nonlawyer ownership and capital, while Utah’s sandbox adjustments narrowed approvals focused on consumer impact and limited certain ABS models. New York and California set explicit boundaries for cross-border fee sharing, which complicates national scaling but provides clarity for compliant structures. BNPL and embedded finance rules introduce state-by-state operational differences, which generally favor integrated vendors with bar approvals and better data-governance tooling.

North America B2C Legal Services Industry Leaders

LegalZoom

Rocket Lawyer

Morgan & Morgan

LegalShield

Trust & Will

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Trust & Will secured USD 4.5 million investment from Curql, bringing total Series C funding to over USD 32 million, to expand estate-planning access for credit union members nationwide via a Credit Union Service Organization (CUSO) structure.

- February 2026: Morgan & Morgan announced alliance with Brodhead Law, LLC, led by Ben C. Brodhead, to expand catastrophic injury and wrongful death litigation across Georgia, New York, Illinois, Nevada, Arizona, and New Mexico.

- January 2026: Clio launched Clio Capital, providing U.S. law firms direct access to working capital via fast, fixed-fee financing based on Clio Payments performance data rather than traditional credit underwriting.

- November 2025: FreeWill raised USD 30 million in Series B funding led by Bain Capital Double Impact to transform nonprofit fundraising via non-cash giving.

North America B2C Legal Services Market Report Scope

Legal services encompass legal advice, representation, notarial activities, and research services. Law firms function as legal arms for large corporations, providing services to corporate entities and individuals.

The North American B2C legal services market is segmented by segment, service, mode, and country. By segment, the market is segmented into criminal law, taxation law, family law, and other segments. By service, the market is segmented into legal assistance, legal documentation, and legal advice. By mode, the market is segmented into online legal services and offline legal services, and by country, the market is segmented into the United States, Canada, and the Rest of North America. The report offers market size and forecasts for the North American B2C legal services market in value (USD) for all the above segments.

| Family Law |

| Personal Injury |

| Estate Planning & Probate |

| Criminal Defense (Misdemeanor & Felony) |

| Immigration |

| Bankruptcy & Debt Relief |

| In-Person Consultations |

| Hybrid (In-Person + Virtual) |

| Fully Virtual / Online Platforms |

| Solo & Small Law Firms (<10 attorneys) |

| Mid-size Law Firms (11-50 attorneys) |

| Large Law Firms (>50 attorneys) |

| Online-only Legal Platforms |

| Legal Assistance |

| Legal Documentation |

| Legal Advice |

| Other Services |

| United States |

| Canada |

| Mexico |

| By Case Type | Family Law |

| Personal Injury | |

| Estate Planning & Probate | |

| Criminal Defense (Misdemeanor & Felony) | |

| Immigration | |

| Bankruptcy & Debt Relief | |

| By Delivery Mode | In-Person Consultations |

| Hybrid (In-Person + Virtual) | |

| Fully Virtual / Online Platforms | |

| By Provider Type | Solo & Small Law Firms (<10 attorneys) |

| Mid-size Law Firms (11-50 attorneys) | |

| Large Law Firms (>50 attorneys) | |

| Online-only Legal Platforms | |

| By Service Type | Legal Assistance |

| Legal Documentation | |

| Legal Advice | |

| Other Services | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected growth for the North America B2C Legal Services market to 2031?

The market is projected to reach USD 144.76 billion by 2031, growing at a 4.78% CAGR from 2026 to 2031.

Which case type is expanding the fastest in North America B2C Legal Services?

Immigration is projected to grow at a 7.60% CAGR through 2031, supported by high asylum volumes, family petitions, and sustained backlogs.

How are ABS and regulatory sandboxes affecting providers in North America?

Arizona’s 136 ABS approvals and New York’s Rule 5.4(a)(4) open new capital and ownership models while setting conditions for cross-border fee sharing, which enables innovation but requires careful compliance.

What delivery mode is gaining the most momentum in consumer-facing legal services?

Fully virtual platforms are projected to grow at a 12.20% CAGR as court digitization normalizes remote hearings, and consumers adopt video consultations and mobile intake.

How do embedded payments and BNPL affect legal accessibility?

BNPL and pay-over-time options reduce upfront barriers and speed firm cash flow, though new rules like New York’s BNPL Act add licensing, pricing, and data-governance requirements.

Which geography currently accounts for the largest share of consumer-facing legal services?

The United States held 92.00% of the region’s value in 2025, supported by scale, higher per-capita spend, and mature digital infrastructure.

Page last updated on: