North America Photographic Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

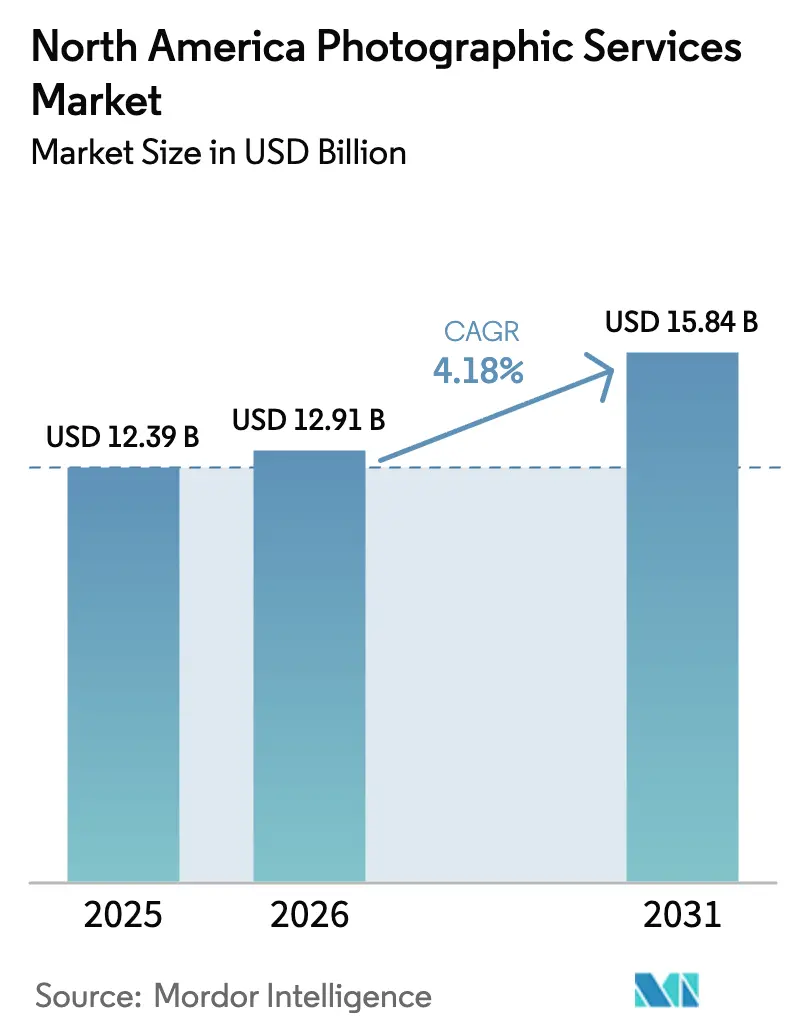

| Base Year Market Size (2025) | USD 12.39 Billion |

| Market Size (2026) | USD 12.91 Billion |

| Market Size (2031) | USD 15.84 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

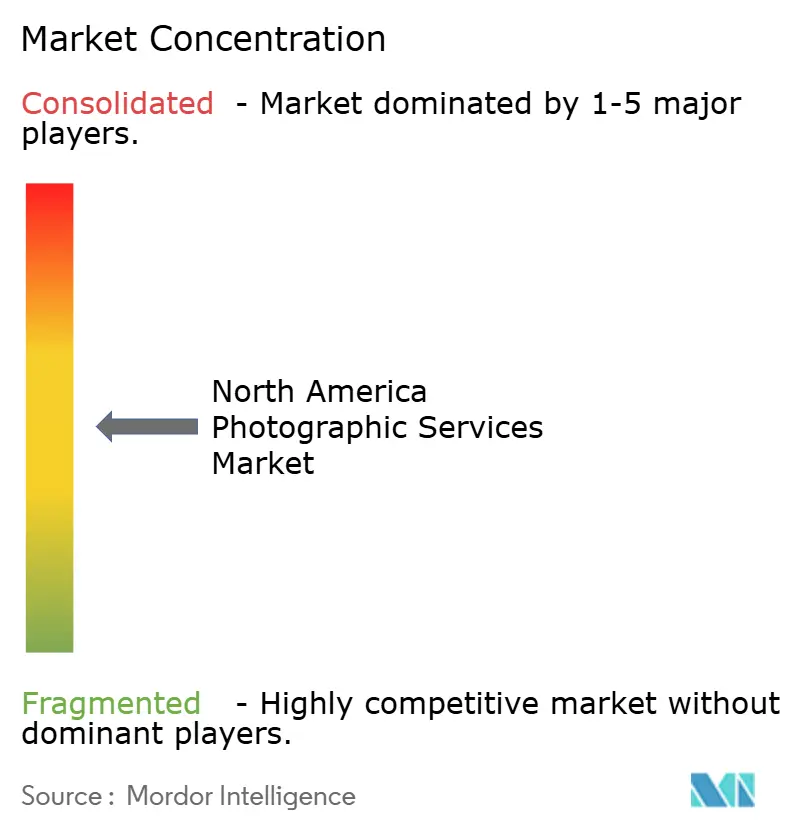

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Photographic Services Market Analysis by Mordor Intelligence

The North America photographic services market size was valued at USD 12.39 billion in 2025 and estimated to grow from USD 12.91 billion in 2026 to reach USD 15.84 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). Steady expansion is supported by rising visual-commerce spending, corporate brand storytelling, and demand for immersive 360° content, even as smartphone cameras and AI automation reshape traditional workflows. Large-scale consolidators are pursuing mergers to build multi-format libraries and AI capabilities, while nimble specialists focus on niche segments such as AI-assisted editing or virtual studio shoots. Individual consumers continue to prioritize professional imagery for social media and milestone events, but e-commerce retailers are emerging as a powerful growth engine as image quality directly links to conversion rates. Technological change, therefore, acts as both competitive pressure and catalyst, compelling providers to refine value propositions around speed, authenticity, and cross-platform consistency.

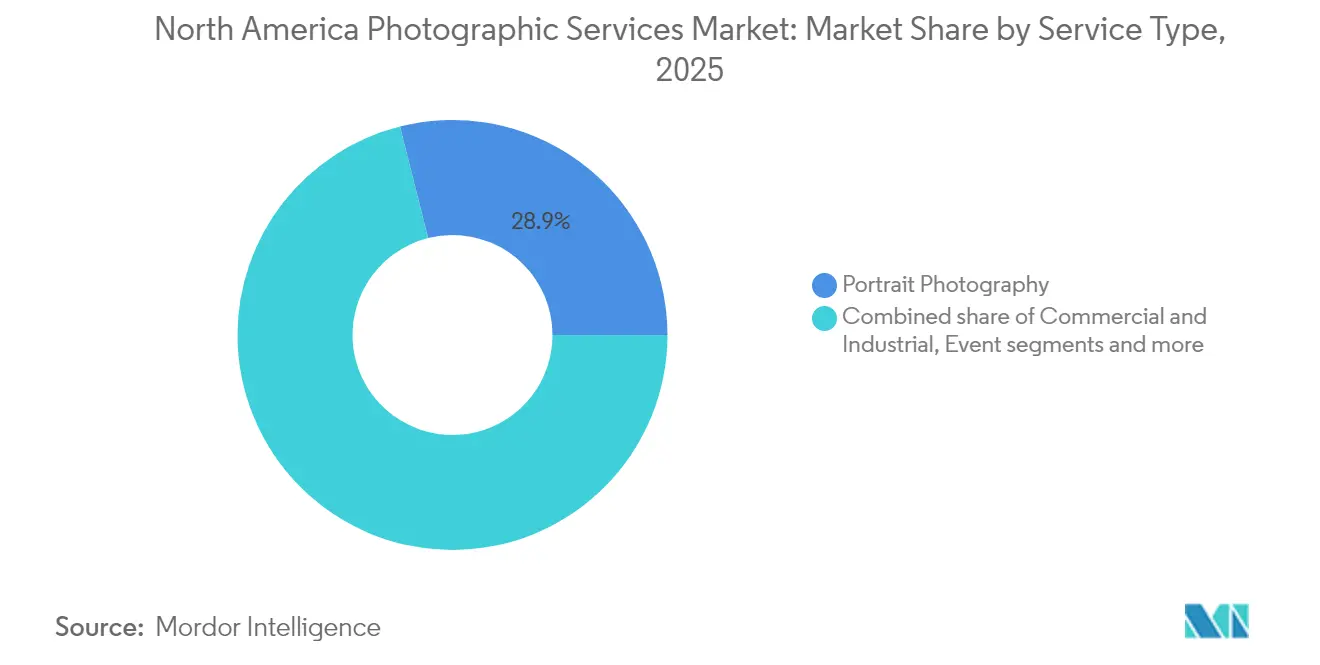

- By service type, Portrait Photography led with 28.93% revenue share of the North America photographic services market in 2025, whereas 360°/VR Photography is forecast to expand at a 6.41% CAGR to 2031.

- By end-user, Individual Consumers held 60.74% of the North America photographic services market share in 2025, while E-commerce & Online Retailers recorded the highest projected CAGR at 7.12% through 2031.

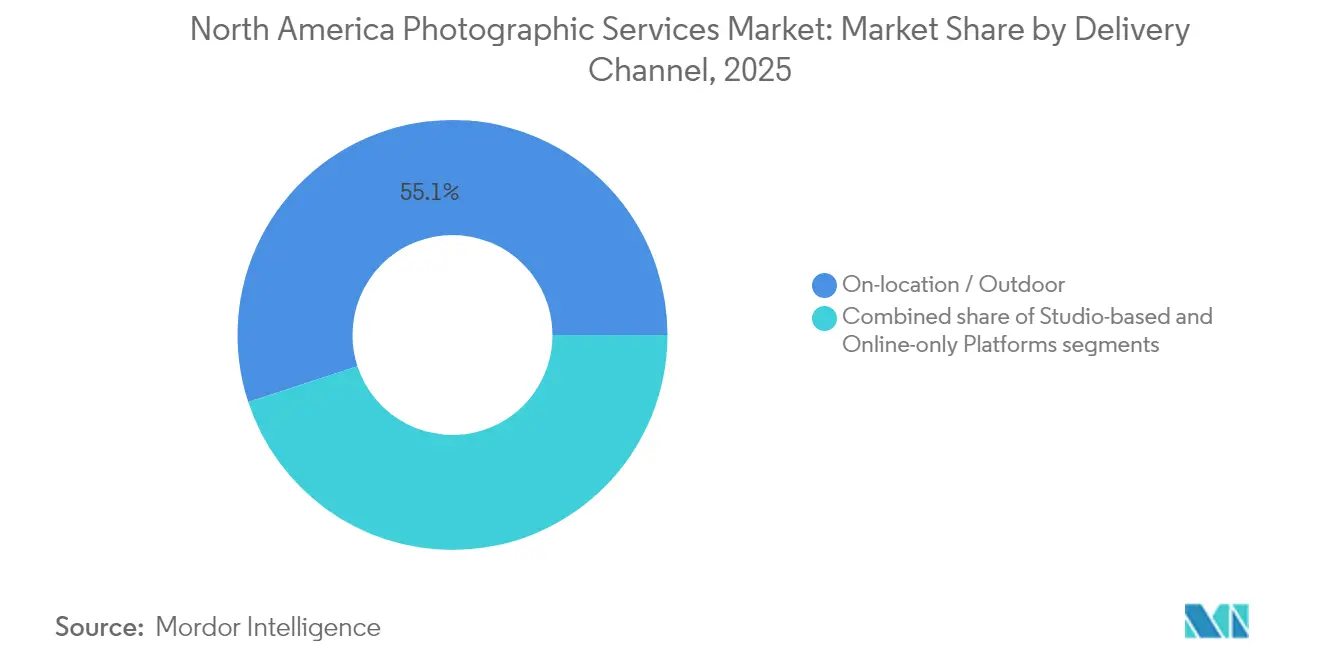

- By delivery channel, On-location/Outdoor shooting accounted for 55.05% of the North America photographic services market size in 2025; Online-only Platforms are advancing at a 6.84% CAGR through 2031.

- By country, the United States commanded 81.86% revenue share in 2025 and retains scale advantages, whereas Mexico is set to grow the fastest at 5.05% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on photographic services market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Photographic Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social media and user-generated content | +0.8% | Global, strongest in US urban markets | Short term (≤ 2 years) |

| High-quality product imagery for e-commerce | +0.9% | North America, spill-over to Mexico | Medium term (2-4 years) |

| Rebound in corporate branding spend | +0.7% | US & Canada | Medium term (2-4 years) |

| AI-enabled automated editing workflows | +0.6% | Technology hubs across North America | Long term (≥ 4 years) |

| Immersive 360° and VR imaging | +0.5% | US enterprise markets, early Canada adoption | Long term (≥ 4 years) |

| Personalised photo merchandise via POD | +0.6% | Consumer markets across North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Social Media & UGC

Brands and influencers depend on visually cohesive feeds to engage their audiences, driving a constant demand for professional-grade imagery on social platforms. Although smartphone cameras enable spontaneous captures, adhering to brand guidelines necessitates professional editing, lighting consultations, and multi-format deliveries. These services ensure consistency and quality, which are critical for maintaining audience trust and brand identity. As a result, hybrid practices broaden the market for professional services by combining the convenience of smartphone photography with the expertise of professionals. Trends emphasizing content authenticity have heightened the demand for candid portraits, allowing photographers to capitalize on advisory roles focused on stylistic consistency. Additionally, the growing need for personalized and relatable content has created opportunities for photographers to guide clients in aligning their visual strategies with audience preferences. Agencies that combine quick editing with optimizations tailored to specific platforms see a boost in repeat business from clients prioritizing social media, as these services help them stay competitive in a fast-paced digital environment.

E-commerce Demand for High-Quality Product Imagery

Conversion analytics confirm that professionally shot images lower product return rates and build buyer confidence, prompting digital retailers to outsource photography at scale. The North America photographic services market benefits from the acceleration in cross-border e-commerce between the United States and Mexico, which pushes demand for culturally adapted visuals. Retailers increasingly request 360° spins and AR-ready assets, widening revenue streams for studios that invest in automated turntables and interactive imaging software. Improved logistics networks reduce delivery windows, so merchants expect same-week photoshoot cycles; suppliers meeting such timelines gain contractual stickiness. The trajectory reinforces product-specific micro-specializations such as fashion flat-lays, electronics macro shots, and food stylization.

Corporate Branding & Marketing Spend Rebound

Post-pandemic reopening stimulated corporate campaigns centered on employee experience, ESG storytelling, and hybrid workplace culture. Public company investor relations departments now schedule continual photo shoots to refresh leadership images across environmental, web, and social channels. Sectoral mergers and live-event recoveries, highlighted by the 2025 Getty-Shutterstock combination, underline renewed confidence in content assets[1]Leigh McGowran, “Getty Images, Shutterstock confirm USD 3.7 billion merger,” reuters.com . As executive visibility widens across webinars and in-person conferences, demand for consistent headshot libraries grows. Providers are able to coordinate multi-city sessions through shared style guides and secure framework agreements. Marketing agencies concurrently outsource behind-the-scenes production stills to integrate with video storytelling, sustaining average project values.

AI-Enabled Automated Editing Workflows

Machine-learning tools now execute color balancing, background removal, and batch tagging in minutes, cutting delivery cycles by up to more than half for early adopters. The merged Getty Images-Shutterstock entity is scaling proprietary AI to counter generative-art competition. Studios deploying cloud-based editors serve geographically dispersed clients without file-size bottlenecks, enabling subscription models for recurring corporate work. Training investment acts as a barrier to entry, but once absorbed, variable costs fall sharply, letting providers price aggressively against traditional shops. Opportunities also surface in AI-quality assurance, where algorithms flag focus issues before field crews leave a location, reducing reshoot risk.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced smartphone cameras are cannibalising demand | -0.4% | Consumer segments across North America | Short term (≤ 2 years) |

| Event seasonality & cancellations | -0.3% | Wedding and corporate event markets | Medium term (2-4 years) |

| Data-privacy regulations limiting candid photography | -0.2% | Regulatory compliance markets | Long term (≥ 4 years) |

| Sustainability scrutiny on chemical photofinishing | -0.1% | Traditional photo processing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Smartphone Cameras Cannibalising Demand

The advancements in computational photography have positioned it as a viable alternative to entry-level DSLRs for well-lit scenarios, leading to a decline in demand for professional portrait services. This trend has intensified margin pressures on mid-tier studios as cost-conscious consumers increasingly adopt DIY approaches. However, high-value services such as controlled lighting setups, large-format printing, and advanced post-production remain reliant on professional expertise. Studios that integrate smartphone-centric workshops and rapid mobile editing solutions are effectively mitigating the risks of disintermediation. By leveraging these strategies, providers are unlocking new revenue opportunities while adapting to evolving consumer preferences.

Event Seasonality & Cancellations

Weddings and corporate events often crowd into tight schedules, creating lulls during off-peak months. These capacity gaps can significantly impact revenue streams for businesses reliant on consistent bookings. Sudden weather changes or health advisories can wipe out bookings for entire weekends, leaving operators with little time to adapt. The rise of hybrid and virtual events has led to a dip in demand for onsite photos, subsequently lowering average order values and reducing profitability. While branching out into corporate portraits or e-commerce shoots can stabilize cash flow, it demands distinct equipment, specialized skills, and tailored marketing approaches, which may require additional investment. Additionally, insurance premiums for unforeseen cancellations become an added expense, compelling smaller operators to adjust their pricing during peak seasons to offset these costs and maintain financial stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Portrait Dominance and Immersive Upswing

Portrait Photography controls 28.93% of 2025 revenues, underscoring the steady pull of headshots, family portraits, and personal-branding imagery within the North America photographic services market. The rise of professional networking and online schooling intensifies the demand for polished profile pictures across age groups. Studios differentiate through express delivery and retouching tiers, enabling price segmentation without diluting perceived quality. Commercial & Industrial Photography remains resilient as firms prioritize product-centric storylines for omnichannel marketing assets. Meanwhile, the 360°/VR sub-segment grows at a 6.41% CAGR, signaling that immersive formats are maturing from novelty to mainstream requirements in real estate and experiential retail. Providers investing in multi-sensor rigs, stitching software, and AR integrations position themselves for outsized share capture once mass adoption accelerates.

A broader mix of specialty offerings—including school photography, stock licensing, and AI-enhanced editing—fills out the North America photographic services market, cushioning operators against single-segment volatility. School & Academic sessions produce predictable yearly revenue but face procurement scrutiny as districts explore cost-saving digital alternatives. Stock and licensing gained new momentum from the Getty-Shutterstock merger, which enlarged searchable archives for global creatives. Continuous expansion of 360°/VR assets is forecast to push the segment’s contribution beyond 10% of the North America photographic services market size within the next decade, reshaping studio investment priorities toward immersive capture hardware.

By End-user: Consumer Anchor and Retailer Surge

Individual Consumers accounted for 60.74% of market demand in 2025, reaffirming the cultural value placed on professional documentation of life events within the North America photographic services market. Milestone celebrations, personal branding, and social-media-ready portraits underpin repeat spending. Enhanced smartphone optics have lowered entry barriers for casual snapshots, yet clients still commission experts for lighting mastery, print-resolution output, and time efficiency. Corporates & SMEs sustain steady budgets for leadership photography and employer-branding content as labor markets remain competitive. Media & Entertainment houses demand highly specialized shoots, licensing, and on-set stills that command premium day rates.

E-commerce & Online Retailers represent the fastest-growing end-user group with a 7.12% CAGR, as conversion science correlates multiple image angles and consistent styling with higher cart completion. The North America photographic services market size for this segment is projected to expand markedly through 2031, propelled by interactive 360° views and AR overlays that shorten consideration time. Educational Institutions maintain a smaller yet stable slice of demand through graduation and yearbook contracts, though pricing pressure intensifies as budgets tighten. Providers able to cross-sell product photography, corporate packages, and event coverage create multi-layered revenue pipelines that hedge economic swings.

By Delivery Channel: On-location Strength and Digital-first Momentum

In 2025, on-location and outdoor shoots accounted for 55.05% of total revenues, underscoring a clear client preference for authentic settings in North America's photographic services market. The allure of natural lighting, contextual backdrops, and immersive narratives justifies travel surcharges and extended sessions and helps maintain the average revenue per job. While studio-based services are crucial for controlled lighting, consistent backgrounds, and high-volume product shoots, the rise of mobile pop-up sets is challenging the advantages of traditional fixed locations. Online-only platforms are experiencing a robust 6.84% CAGR, driven by cloud-based editing suites and collaborative proofing that diminish geographical constraints. These remote workflows empower photographers to cater to clients nationwide without incurring additional travel costs, effectively broadening their audience reach. Services like AI-driven bulk retouching, brand-asset management portals, and subscription content packages are flourishing in this digital landscape. However, the tangible experience of being physically present at events or during environmental portrait sessions remains unmatched in fully digital delivery. Hybrid providers, blending online consultations with on-site execution, are harnessing cross-channel advantages, fostering deeper client loyalty, and solidifying their position in the premium segments of North America's photographic services market.

Geography Analysis

In 2025, the United States is set to dominate the market, accounting for a substantial 81.86% of total revenue. This dominance is fueled by the nation's robust disposable incomes, a well-established e-commerce framework, and a pervasive culture of visual storytelling, both personally and professionally. Major cities like New York, Los Angeles, and Chicago serve as bustling hubs, hosting a dense network of photographers, agencies, and equipment suppliers. While Canadian demand mirrors these trends, it's at a smaller scale. It presents a golden opportunity for U.S. studios eyeing cross-border expansion, especially in the Vancouver and Toronto corridors. Meanwhile, Mexico is on a growth trajectory, boasting the fastest expansion rate at a 5.05% CAGR through 2031 due to consistent GDP growth and a burgeoning middle class with increased spending power.

While the bulk of photographic spending in North America is centered in the U.S., it's the emerging urban centers in Mexico that are witnessing the steepest growth rates. The swift digitization of retail in Mexico has streamlined payments and logistics and empowered SMEs to invest more in high-quality product catalogs. In Canada, businesses are placing a premium on employer-branding imagery. It is especially evident in tech hubs like Toronto and Montréal, where the rise of hybrid work models has heightened the demand for consistent imagery of remote staff. Moreover, cross-border trade agreements are harmonizing standards, compelling studios to ensure multilingual metadata, navigate diverse privacy regulations, and expedite customs processes for physical deliveries.

Coastal states in the U.S. generate higher volumes due to dense populations and brand headquarters, while interior markets thrive on event photography and personalized merchandise. Festivals and sports franchises in Texas and Florida sustain year-round assignments, balancing slower winter periods. Rural areas increasingly use remote proofing portals, enabling clients to select edits without in-person consultations. Image licensing platforms optimize discoverability by segmenting catalogs with regional keywords. In Canada, government policies favor diverse, inclusive imagery, creating opportunities for photographers with aligned portfolios. Mexico’s infrastructural projects and tourism initiatives drive demand for drone mapping and immersive 360° experiences, though currency fluctuations impact equipment costs.

Competitive Landscape

In North America, the photographic services market remains fragmented, with the top players accounting for a moderate share of the total revenue. This scenario opens the door for mid-tier and niche entrants to carve out their space. A significant consolidation took place in January 2025, when Getty Images and Shutterstock merged in a deal valued at USD 3.7 billion. This merger not only combines their vast libraries but also enables cross-licensing of advanced AI tools. Furthermore, the merger is projected to yield annual cost benefits between USD 150 million and USD 200 million[2]“Getty Images and Shutterstock to Merge, Creating a Premier Visual Content Company,” investors.gettyimages.com . With this heightened scale, the newly formed entity is poised to make substantial investments in generative image research and development, a move aimed at countering the trend of content commoditization. In response, independent specialists are carving out their niche by focusing on personalized creative direction, quicker iteration cycles, and a boutique-level experience for their clients.

Technology adoption forms the primary competitive battleground. Studios deploying AI-assisted culling and cloud-based approval portals reduce turnaround drastically, winning recurring corporate contracts. Niche operators such as school portrait houses leverage localized brand equity and year-over-year client retention to maintain defensible niches despite macro-fragmentation. Equipment retailers like B&H Photo Video support ecosystem resilience by offering rapid lens-rental programs and firmware clinics, ensuring professionals can keep pace with hardware evolution. Mobile-first platforms integrate instant booking, dynamic pricing, and gig-economy staffing models to match consumer expectations of convenience.

Pricing pressure intensifies at the low-complexity end of the spectrum, where smartphone cameras substitute for entry-level demand. Providers respond by diversifying into value-added verticals such as wall-art printing, data-driven visual audits for e-commerce compliance, and hybrid event coverage, combining stills with highlight reels. Combined, these differentiated services sustain margin profiles even as commoditized segments thin. The market’s service-oriented nature and regional preference for local talent ensure small businesses remain viable alongside global platforms, maintaining an inherently diverse competitive field.

North America Photographic Services Industry Leaders

Shutterfly LLC

Lifetouch Inc.

Getty Images Holdings Inc.

Shutterstock Inc.

Snappr Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ShootProof released its State of the Photography Industry 2025 report, highlighting workflow shifts toward cloud collaboration among North American professionals.

- January 2025: Getty Images unveiled a USD 3.7 billion merger with Shutterstock, projecting annual benefits of USD 150 million–USD 200 million by the third year while also ramping up R&D efforts in AI-driven content creation.

- May 2025: Getty Images posted Q1 results showing 262,000 active annual subscribers, a 79% rise year-on-year, and acquired Motorsport Images to widen its sports archive.

- March 2025: Shutterstock Strengthens Collaboration with OpenAI to Advance Generative AI Solutions. This enhanced partnership demonstrates Shutterstock's strategic focus on innovation and its commitment to adapting to the rapidly evolving AI-driven content creation landscape.

North America Photographic Services Market Report Scope

The photography industry encompasses companies and individuals that offer a range of photographic services, including still photography and videography for private events. Commercial and portrait photography studios are also included in this industry. A complete background analysis of the North American photographic services market, which includes an assessment of the photography industry, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, is covered in the report. The North American photographic services market is segmented by type (shooting service and after-sales service), application (portrait studio services and commercial studios), and country (USA, Canada, and Rest of North America). The report offers market size and forecasts for the North American photographic services market in terms of value (USD million) for all the above segments.

| Portrait Photography |

| Commercial & Industrial Photography |

| Event & Wedding Photography |

| School & Academic Photography |

| Stock / Licensing Services |

| Individual Consumers |

| Corporates & SMEs |

| Media & Entertainment |

| Educational Institutions |

| E-commerce & Online Retailers |

| On-location / Outdoor |

| Studio-based |

| Online-only Platforms |

| United States |

| Canada |

| Mexico |

| By Service Type | Portrait Photography |

| Commercial & Industrial Photography | |

| Event & Wedding Photography | |

| School & Academic Photography | |

| Stock / Licensing Services | |

| By End-user | Individual Consumers |

| Corporates & SMEs | |

| Media & Entertainment | |

| Educational Institutions | |

| E-commerce & Online Retailers | |

| By Delivery Channel | On-location / Outdoor |

| Studio-based | |

| Online-only Platforms | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North America photographic services market?

The market is valued at USD 12.91 billion in 2026 and is on track to reach USD 15.84 billion by 2031, growing at a 4.18% CAGR.

Which service segment holds the largest share?

Portrait Photography leads with 28.93% of 2025 revenue, driven by headshots, family portraits, and personal branding needs.

Why is e-commerce important for market growth?

Online retailers depend on high-quality product imagery to reduce returns and lift conversion rates, pushing the e-commerce end-user segment to a 7.12% CAGR through 2031.

How will the Getty Images-Shutterstock merger affect competition?

The combination pools extensive content libraries and AI R&D budgets, enhancing scale advantages while intensifying pressure on smaller stock-image providers.

Which country is growing the fastest within the region?

Mexico is forecast to grow at a 5.05% CAGR between 2026 and 2031, buoyed by rising disposable incomes and expanding digital commerce.

What technologies are reshaping photographic services?

AI-powered editing, immersive 360° capture, and cloud-based collaboration tools are shortening delivery cycles and creating new service categories across North America.

Page last updated on: