Public Sector Consulting And Advisory Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

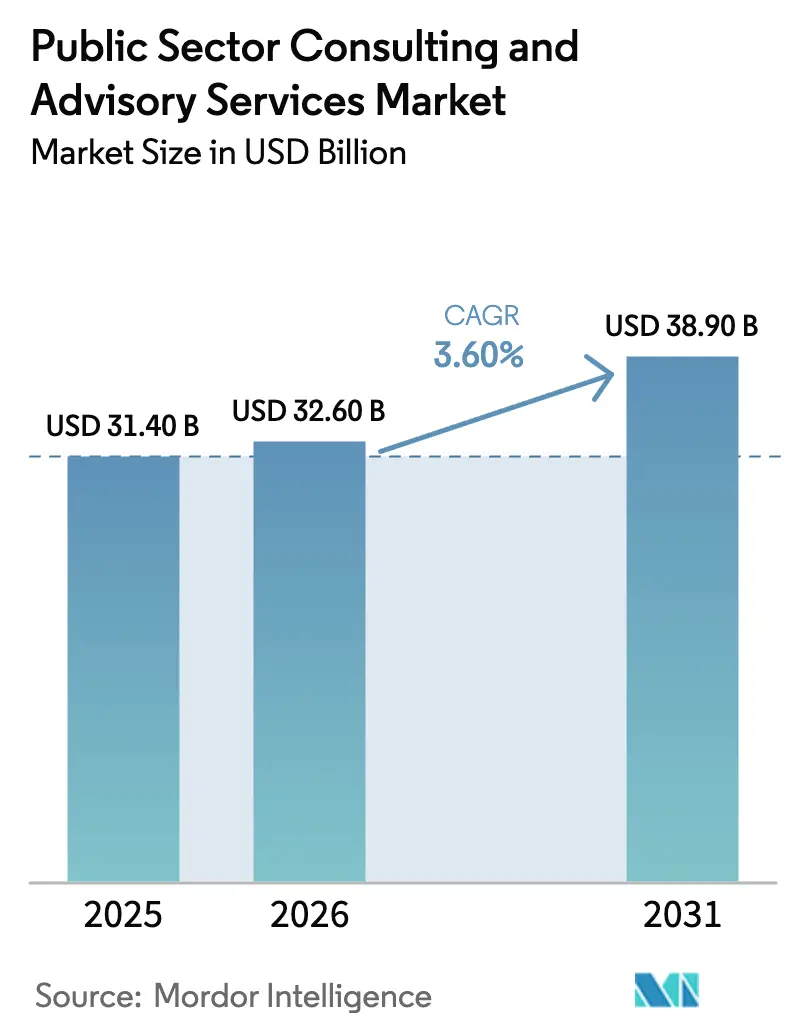

| Market Size (2026) | USD 32.60 Billion |

| Market Size (2031) | USD 38.90 Billion |

| Growth Rate (2026 - 2031) | 3.60% CAGR |

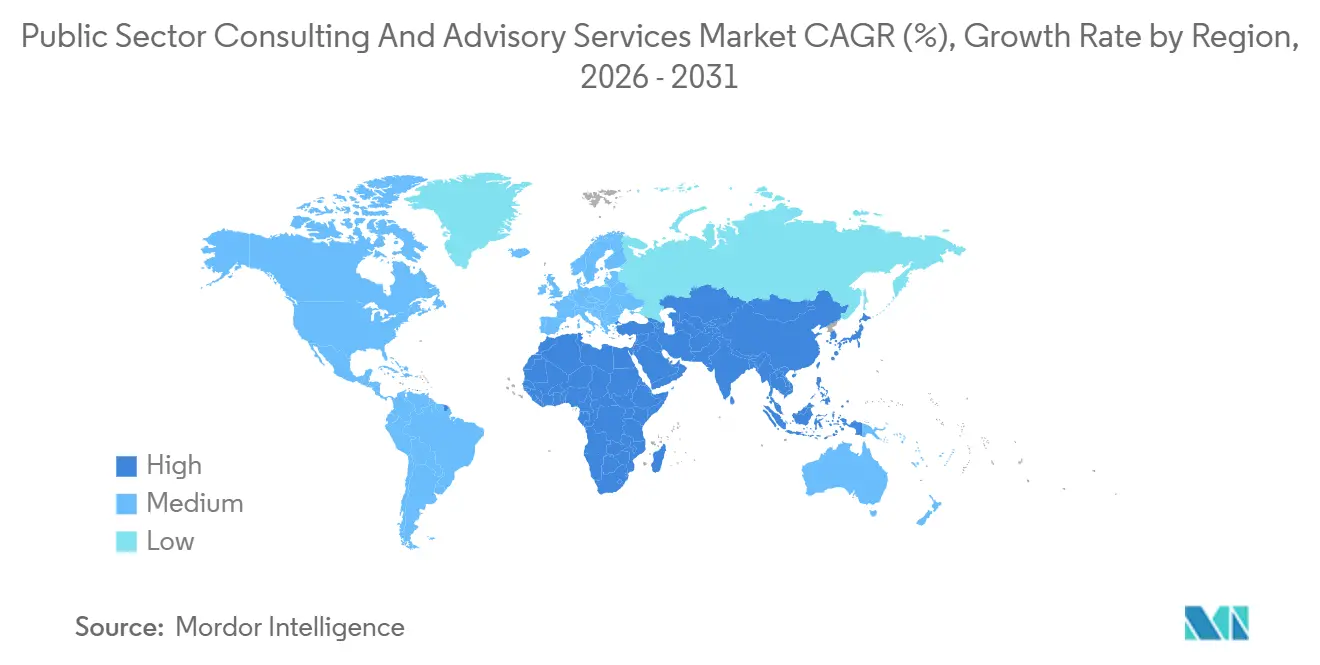

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

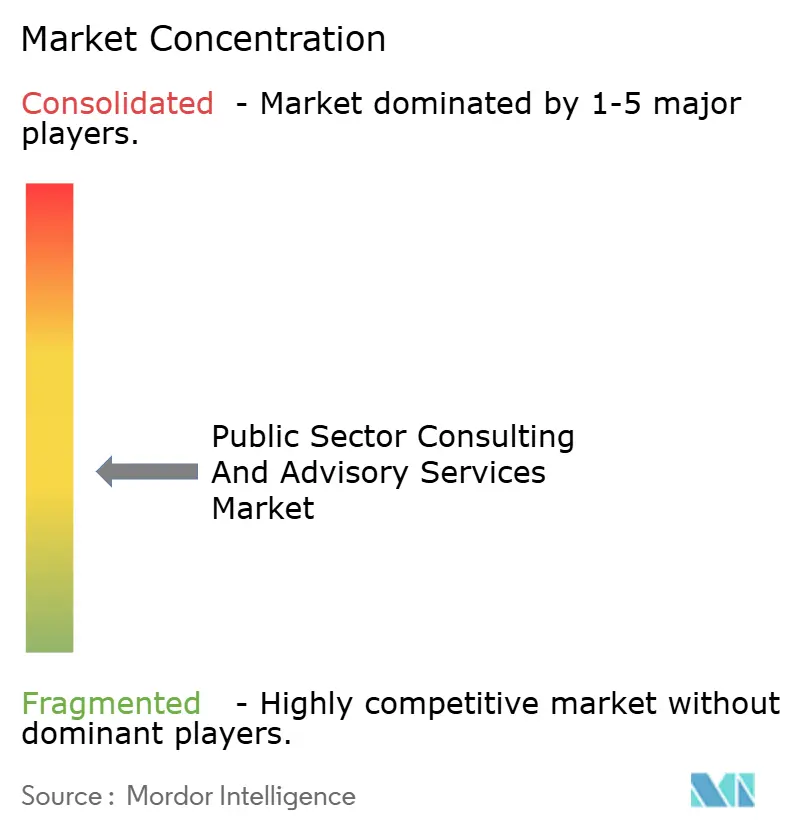

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Public Sector Consulting And Advisory Services Market Analysis by Mordor Intelligence

The Public Sector Consulting And Advisory Services Market size is expected to grow from USD 31.40 billion in 2025 to USD 32.60 billion in 2026 and is forecast to reach USD 38.90 billion by 2031 at 3.60% CAGR over 2026-2031.

Agencies are channeling spend from staff augmentation to architected transformation in zero-trust cybersecurity, AI governance, and digital public infrastructure, which raises demand for outcome-linked delivery and narrows the field to firms with technical depth and implementation scale[1]U.S. Office of Management and Budget, “M-25-21: Implementation of Artificial Intelligence Executive Order Requirements,” The White House, whitehouse.gov. The Office of Management and Budget’s April 2025 mandates to appoint Chief AI Officers and catalog high-impact AI systems are creating a new compliance layer that most agencies cannot address with in-house capacity, which expands technology consulting scopes and accelerates the shift to solutions-led engagements. In North America, infrastructure delivery remains a central growth engine as funding under the Infrastructure Investment and Jobs Act continues to convert to projects, which sustains multiyear advisory and program delivery needs across transportation, water, broadband, and energy. In Europe, eIDAS 2.0 compresses digital identity modernization into tight deadlines that compel rapid cross-border coordination and increase reliance on consultants for interoperability, wallet readiness, and acceptance pathways in regulated sectors. Asia-Pacific’s digital public infrastructure wave, exemplified by India’s UPI transaction growth in 2026 and Aadhaar’s population-scale coverage, is transforming point projects into replicable platforms, expanding advisory opportunities in architecture, standards, and capacity building across multiple regions.

Key Report Takeaways

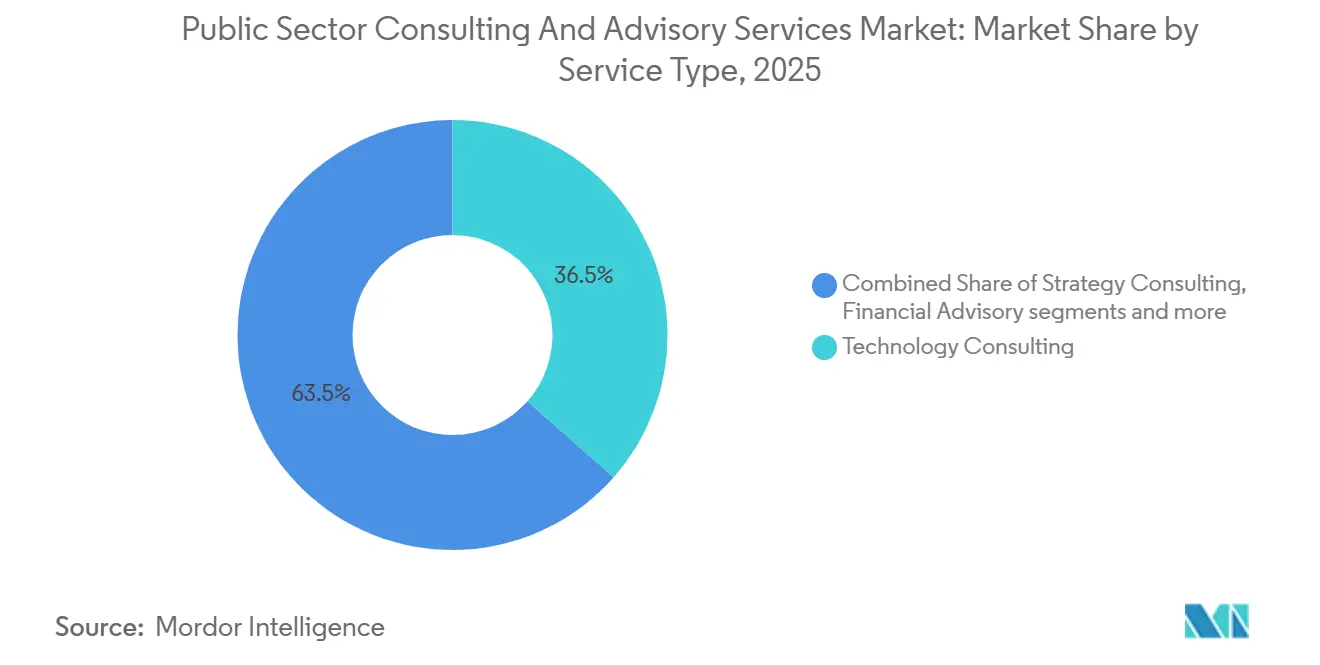

- By service type, technology consulting led the Public Sector Consulting and Advisory Services market with 36.5% revenue share in 2025 and is projected to grow at a 9.0% CAGR through 2031.

- By end user, the central government segment accounted for 52.0% of the Public Sector Consulting and Advisory Services market in 2025, while state and local government is forecast to record the highest growth at a 7.0% CAGR through 2031.

- By geography, North America held 64.5% of the Public Sector Consulting and Advisory Services market in 2025, while Asia-Pacific is expected to deliver the fastest expansion at a 17.9% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Public Sector Consulting And Advisory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-trust and AI-ready cybersecurity mandates across agencies | +1.2% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| eIDAS 2.0/EUDI wallets driving cross-border digital identity build-outs | +0.8% | Europe primary, spill-over to APAC and Latin America | Short term (≤ 2 years) |

| Infrastructure stimulus delivery and resilience programs | +1.1% | North America core, with secondary impact in APAC | Medium term (2-4 years) |

| Outcome-based procurement and results-driven contracting | +0.9% | Global, with North America and Europe leading | Long term (≥ 4 years) |

| Digital Public Infrastructure replication and GovTech platforms | +1.5% | APAC core, with replication in MEA and Latin America | Medium term (2-4 years) |

| Algorithmic accountability and AI-governance requirements | +0.7% | North America and EU primary, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Zero-Trust and AI-Ready Cybersecurity Mandates Across Agencies

Agencies are under pressure to mature zero-trust controls and secure AI deployments, which sustains demand for cleared firms that can deliver cyber architecture, tooling, and governance at enterprise scale. NASA’s Office of Inspector General projected USD 211 million in cybersecurity infrastructure spending for fiscal 2024 through 2029, signaling persistent federal investment into defensive modernization that consultancies help implement and operationalize[2]NASA Office of Inspector General, “NASA Cybersecurity Infrastructure Investment Plan, IG-24-012,” NASA OIG, oig.nasa.gov. CISA reported broad uptake of endpoint detection and response and protective DNS among Federal Civilian Executive Branch agencies by September 2025, which sets a baseline for advisory scope focused on integration, monitoring, and continuous improvement rather than first-time deployment. The April 2025 OMB memoranda formalized responsibilities for AI safety and oversight, prompting agencies to define roles, inventories, and review processes that most do not yet have in place. Clearance system modernization has experienced multi-year implementation delays, which prolong adjudications and complicate staffing of sensitive programs, thereby favoring incumbent consultants with benches of adjudicated personnel. Together, these factors concentrate spend on firms that can combine cyber engineering, AI risk frameworks, and cleared delivery teams, which reinforces a premium tier in the Public Sector Consulting and Advisory Services market.

eIDAS 2.0/EUDI Wallets Driving Cross-Border Digital Identity Build-Outs

The eIDAS 2.0 Regulation sets binding deadlines for government-issued digital identity wallets to be available by December 2026 and widely accepted in regulated sectors by December 2027, compressing a multi-year roadmap into a short window that grows advisory demand for architecture, conformance, and interoperability solutions. The European Commission funded pilots to accelerate EUDI wallet use cases across public and private services, which increases the near-term volume of work on standards alignment, certification, and cross-border acceptance pathways. Governments need legal, technical, and change-management capacity to replatform identity into wallet ecosystems while preserving privacy and security, which many agencies source from external consultants to meet deadlines. The Public Sector Consulting and Advisory Services market stands to benefit as ministries and agencies procure multi-domain expertise to integrate wallets with legacy services and enable mutual recognition across borders. Consulting firms with prior large-scale identity experience and cross-jurisdictional teams gain an advantage because they can combine policy and engineering in service of regulatory conformance and user experience.

Infrastructure Stimulus Delivery and Resilience Programs

The Infrastructure Investment and Jobs Act continues to drive program-management, grants administration, and delivery oversight as funds convert into thousands of projects across transportation, broadband, water, and energy. States and municipalities often lack program offices sized to manage multi-year, multi-stakeholder capital programs, which leads them to retain consultancies for schedule controls, risk management, and federal compliance. Advisory work expands when agencies must align permitting, community engagement, and resilience standards with federal grant requirements across many parallel projects. The Public Sector Consulting and Advisory Services market benefits as agencies integrate capital planning with climate resilience and digital operations, which lengthens engagement scopes from discrete deliverables to broader portfolio support. Delivery complexity elevates the value of firms that can combine engineering, program controls, and compliance under one roof while meeting public accountability standards[3]U.S. Department of Transportation, “Infrastructure Investment and Jobs Act Implementation,” U.S. Department of Transportation, transportation.gov.

Outcome-Based Procurement and Results-Driven Contracting

Jurisdictions are moving from input-based consulting contracts to outcome-based models that tie payments to measurable results, which shifts risk onto vendors and elevates the importance of verifiable performance metrics. Washington State’s Department of Children, Youth, and Families expanded performance-based agreements, creating a structured demand for advisory support in metric design, baselines, and verification processes. GSA’s OneGov Strategy launched in April 2025 with explicit emphasis on results-driven shared services, reinforcing outcome orientation at the federal level and shaping how agencies scope and award transformation work. For consultants, this means investing in measurement capabilities and readiness to underwrite delivery risk, which differentiates integrated technology providers from diagnostic-only advisors. The Public Sector Consulting and Advisory Services market increasingly rewards firms that can pair strategy with accountable implementation under fixed or incentive-aligned structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data localization and sovereign cloud constraints | -0.6% | Global, with acute impact in EU and emerging in APAC | Medium term (2-4 years) |

| Procurement reform scrutiny and consulting spend rationalization | -0.9% | North America primary, with secondary impact in Europe | Short term (≤ 2 years) |

| Complex grants, FAR, and Uniform Guidance compliance burdens | -0.5% | North America core, particularly U.S. federal and state | Long term (≥ 4 years) |

| Scarcity of cleared and specialist public-sector talent | -1.1% | Global, with acute impact in North America and UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Localization/Sovereign Cloud Constraints and Schrems II Risk

Governments are tightening controls on the movement and processing of sensitive data, which compels agencies and vendors to localize workloads and create sovereign environments. The U.S. Department of Justice issued a rule in April 2025 restricting access to bulk sensitive personal data by countries of concern, which increases compliance complexity for cross-border engagements and solution hosting. In Europe, hyperscalers are committing significant investment to European-controlled environments, signaling a durable shift toward sovereignty that reshapes cost structures and deployment strategies for public programs. For consultancies, these rules require parallel architectures and segregated delivery teams to satisfy residency and access controls across jurisdictions. The Public Sector Consulting and Advisory Services market must adapt to layered compliance and potential duplication of infrastructure, which can compress margins and slow implementation timelines.

Procurement Reform Scrutiny and Consulting Spend Rationalization

Reform efforts are reshaping federal procurement in 2026, with a focus on streamlined rules, threshold adjustments, and enhanced competition. An April 2025 executive order initiated a broad Federal Acquisition Regulation update, including the removal of many prescriptive clauses and higher thresholds that can change how and when agencies use external providers[4]Executive Office of the President, “Executive Order 14275: Reforming Federal Procurement to Promote Small Business Participation and Fair Competition,” Federal Register, federalregister.gov. FAR case 2024-016 operationalizes elements of streamlining, which may shift agencies toward smaller task orders, different pricing structures, and new competition patterns that raise bid costs and affect win rates for vendors. The Public Sector Consulting and Advisory Services market adjusts to longer deliberation, more granular scoping, and a stronger requirement to demonstrate measurable outcomes per dollar spent. Firms that quantify impact and align incentives to results are better positioned to sustain growth under tighter oversight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Technology Consulting Commands Premium in AI and Cyber Transformation

Technology consulting captured 36.5% of the Public Sector Consulting and Advisory Services market share in 2025 and is expanding at 9.0% CAGR from 2026 to 2031, driven by cloud modernization, zero-trust controls, AI governance, and enterprise-scale system integration. The Public Sector Consulting and Advisory Services market size for technology consulting is projected to expand at 9.0% CAGR between 2026 and 2031 as agencies operationalize AI and tighten cybersecurity baselines under evolving rules and program oversight. Recent large-scale wins highlight the scope of enterprise integration and transformation work, including a 4.5-year engagement supporting the Veterans Affairs EHR modernization program that centers on system integration and AI-enabled clinical workflows across a national footprint. This demand concentrates on providers that can fuse architecture, delivery, and compliance for mission-critical systems operating under strict privacy, security, and resiliency requirements. Within the Public Sector Consulting and Advisory Services industry, management consulting remains important for organization design and operating models but faces pricing and scope pressures as buyers favor implementation-ready solutions that can demonstrate measurable outcomes. Operations and HR consulting play targeted roles in continuous-vetting readiness, cleared talent pipelines, and workflow automation for administrative functions, which agencies often source as adjunct capabilities to technology-led programs.

Market dynamics favor firms with codified delivery assets, including AI risk frameworks, compliance accelerators, and proprietary architectures that reduce time to value and de-risk outcomes. The Public Sector Consulting and Advisory Services industry sees larger players expand through program factories and solution accelerators tailored to federal and state procurement models, while boutiques differentiate through deep expertise in algorithmic auditing, privacy engineering, or sovereign cloud. Engagement models shift from time and materials to fixed or incentive structures aligned to results, which reward providers that can measure impact and absorb delivery risk through governance and automation. Technology consulting is anchored by cyber and data platforms, EHR and case systems, and digital identity initiatives tied to wallet adoption in Europe and DPI replication in Asia, which ensures multi-year scopes beyond initial launches. Where agencies anticipate persistent regulation and high assurance demands, they tend to prefer integrators with cleared benches, compliance certifications, and reference architectures that have passed audit and authorization in similar environments.

By End User: State and Local Government Accelerates Digital Modernization

Central government accounted for 52.0% of consulting expenditures in 2025, reflecting the scale and complexity of federal missions in defense, intelligence, healthcare, and infrastructure that rely on cleared delivery and program controls. The Public Sector Consulting and Advisory Services market size for state and local government is projected to expand at a 7.0% CAGR between 2026 and 2031 as jurisdictions adopt performance-based contracting and invest in digital service upgrades to improve outcomes and resilience. Outcome-based procurement at the state level, such as Washington’s portfolio of performance-based agreements, introduces technical needs in indicator design, baselines, and data governance that many procurement teams procure from external specialists. Infrastructure delivery at the subnational level also drives program management and compliance work as federal funds convert to multi-year capital projects that require detailed grants administration and controls under Uniform Guidance. Education and healthcare end users source cybersecurity, interoperability, and analytics modernization as they address resilience, enrollment, and care coordination priorities with limited internal teams.

Across the Public Sector Consulting and Advisory Services industry, end-user maturity and budget structures shape engagement patterns. Federal buyers tend to award larger, multi-year contracts to firms with clearances and relevant past performance, while state and local buyers fragment scopes into phased task orders to manage thresholds and risk. This fragmentation raises transaction costs for vendors yet expands addressable opportunities for firms with regional delivery models and repeatable offerings that fit mid-market budgets. Education and healthcare segments participate through targeted modernization initiatives and compliance efforts that focus on value-based care, identity and access management, and privacy-preserving data exchange. Law enforcement and judiciary modernization creates niche advisory needs in case systems, digital evidence management, and AI governance in sensitive applications, which require careful alignment to policy, transparency, and civil liberties considerations. Overall, federal concentration drives scale and complexity, while state and local growth sustains volume as outcome orientation and digital services move from pilots to standard operating models.

Geography Analysis

North America retained 64.5% of the Public Sector Consulting and Advisory Services market share in 2025 as federal and subnational programs translated funding into active portfolios and as agencies advanced cybersecurity and AI governance under evolving mandates. Funding under the Infrastructure Investment and Jobs Act was authorized into tens of thousands of projects by mid-2024, which sustains advisory scopes across planning, compliance, and delivery. Procurement reforms and streamlining efforts influence award structures and competition, which can extend timelines and shift pricing preferences toward fixed or incentive-aligned models. Clearance-system delays highlighted in congressional oversight continue to constrain staffing for classified programs, which tends to reinforce incumbency and limit overall growth velocity in sensitive domains. Canada and Mexico contribute selectively through national digital and energy transition programs, but the breadth and depth of U.S. federal and state portfolios keep North America at the center of the Public Sector Consulting and Advisory Services market.

Asia-Pacific is the fastest-growing region with a projected 17.9% CAGR over 2026-2031 as countries replicate digital public infrastructure patterns in identity, payments, and data exchange. India’s UPI transaction scale and Aadhaar identity coverage form reference models that other governments adapt through collaborative pilots, technical assistance, and staged operationalization. The Philippines’ national ID rollout and Kenya’s digital ID enrollment reflect momentum that often extends to neighboring countries through capacity-building partnerships and donor-supported programs. Japan and South Korea emphasize high-assurance public platforms and integrated digital services, which generate consulting demand for architecture modernization, interoperability, and privacy-preserving analytics. Australia and New Zealand focus on climate adaptation and Indigenous data sovereignty, which shape advisory requirements toward co-design and culturally sensitive governance. The region’s growth comes through modular engagements that scale with institutional capacity, which suits consultancies with repeatable templates and training programs tailored to public-sector teams.

Europe combines supranational regulation with national delivery constraints, which creates sustained demand for conformance, testing, and interoperability advisory. The eIDAS 2.0 schedule drives country-by-country wallet readiness and cross-border acceptance work that requires both legal and technical capabilities within tight timelines. Sovereign cloud initiatives are galvanizing public markets as jurisdictions require European-controlled data environments for sensitive workloads, prompting consulting requirements in architecture, portability, and compliance-by-design. Markets with strong in-house digital capabilities focus on niche consulting for high-risk AI classification, accessibility, and privacy engineering, while others rely on external providers to guide holistic modernization. The Public Sector Consulting and Advisory Services market size in Europe is closely tied to regulatory timelines and funding cycles, which shape engagement volumes and the mix of conformance versus build work. Latin America and the Middle East and Africa contribute episodically through infrastructure, smart city, and administrative modernization programs supported by sovereign budgets and multilateral financing, which often require program controls, compliance frameworks, and capability transfer components.

Competitive Landscape

The market combines global integrators, Big Four practices, and specialist consultancies, each competing for technology-heavy and compliance-intensive transformations. Large integrators and federal practices frequently anchor complex programs with security, compliance, and delivery scale, as seen in enterprise EHR modernization engagements and defense training initiatives awarded in early 2026. Strategy-led firms are increasing the share of implementation-ready work through technology partnerships that seek to collapse the gap between advisory design and on-the-ground delivery, which aligns with outcome-driven procurement trends. Hyperscalers are deepening public-sector offerings and managed services in sovereign environments, which introduces co-opetition as consultancies integrate cloud-native tools while defending margins on commodity workloads.

Firms that convert delivery know-how into platforms and accelerators are building a durable advantage. Solution factories for AI governance, privacy engineering, and zero-trust patterns shorten time to value and strengthen proposals under performance-based structures. Corporate venture investments and ecosystem programs link consultancies with startups in simulation, AI assurance, and domain analytics, which broadens capability portfolios without the slower timelines of organic development. The Public Sector Consulting and Advisory Services market favors providers that can quantify impact, handle shared risk, and navigate regulated environments with audit-ready methods that hold up to scrutiny. Procurement streamlining and threshold changes also invite more vendors into competitions, which increases recompete frequency and encourages agencies to test smaller, outcome-tied task orders.

Defense and national security work remains a differentiator due to clearances and mission sensitivity. Providers with deep, cleared benches retain an advantage in intelligence analysis, secure systems integration, and training simulation where staffing constraints limit substitution. In 2026, multiple defense-related awards and partnerships underscored the appetite for AI-enabled training, domain awareness, and cyber hardening, reinforcing the premium commanded by firms with scalable, cleared delivery. As agencies expand AI oversight and digital identity programs, competitive pressure intensifies in audits, conformance assessments, and cross-border interoperability, where a small set of consultancies can meet both regulatory and technical depth at scale.

Public Sector Consulting And Advisory Services Industry Leaders

Boston Consulting Group

McKinsey & Company

Accenture

EY

Deloitte

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Booz Allen Ventures invested in Hadean, a UK-based provider of AI-powered digital wargaming and command and control capabilities, to help establish Hadean’s U.S. presence for U.S., NATO, and allied missions, reflecting an acceleration of venture partnerships to extend mission-focused capabilities.

- February 2026: Accenture Federal Services secured a 4.5-year contract supporting the Veterans Affairs EHR modernization with system integration and AI-enabled clinical workflows across the enterprise, positioning the firm in one of the government’s most complex health IT transformations.

- February 2026: Booz Allen Hamilton received the largest share of a USD 391.6 million multiple-award IDIQ to support U.S. Southern Command’s enhanced domain awareness mission, providing strategic and technical services across information operations and domain awareness.

- May 2025: Bain & Company formed a global partnership with Palantir to deliver end-to-end AI transformations that combine Palantir’s platforms with Bain’s sector expertise, targeting faster performance impact on complex transformation programs in public and regulated domains.

Global Public Sector Consulting And Advisory Services Market Report Scope

The global public sector consulting and advisory services market refers to the industry that provides consulting and advisory services to governments, public organizations, and agencies at various levels (local, regional, national, and international). These services aim to assist public sector entities in improving their performance, efficiency, effectiveness, and service delivery to citizens.

The global public sector consulting advisory services market is segmented by service type (strategy consulting, management consulting, technology consulting, human resource consulting, financial advisory, and other service types (risk & compliance advisory & operations consulting)), end user (central government, state and local government, educational institutions, healthcare organizations, law enforcement and judiciary services, and other end users (transportation services & utilities and environmental projects)), and geography (North America (United States, Canada, Mexico, and Rest of North America), Europe (France, United Kingdom, Russia, Rest of Europe), Asia-Pacific (India, China, Japan, Rest of Asia-Pacific), Latin America (Brazil, Argentina, Uruguay, and Rest of Latin America), and Middle East and Africa( United Arab Emirates, Saudi, Qatar, and Rest of Middle East and Africa.))

| Strategy Consulting |

| Management Consulting |

| Technology Consulting |

| Human Resource Consulting |

| Financial Advisory |

| Other Service Types (Risk & Compliance Advisory & Operations Consulting) |

| Central Government |

| State and Local Government |

| Educational Institutions |

| Healthcare Organizations |

| Law Enforcement and Judiciary Services |

| Other End Users (Transportation Services & Utilities And Environmental Projects) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | France |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Argentina | |

| Uruguay | |

| Rest of Latin America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East and Africa |

| By Service Type | Strategy Consulting | |

| Management Consulting | ||

| Technology Consulting | ||

| Human Resource Consulting | ||

| Financial Advisory | ||

| Other Service Types (Risk & Compliance Advisory & Operations Consulting) | ||

| By End User | Central Government | |

| State and Local Government | ||

| Educational Institutions | ||

| Healthcare Organizations | ||

| Law Enforcement and Judiciary Services | ||

| Other End Users (Transportation Services & Utilities And Environmental Projects) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | France | |

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Latin America | Brazil | |

| Argentina | ||

| Uruguay | ||

| Rest of Latin America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Public Sector Consulting and Advisory Services market?

The Public Sector Consulting and Advisory Services market size is projected to expand from USD 31.4 billion in 2025 to USD 38.9 billion by 2031 at a 3.6% CAGR over 2026-2031.

Which service type is leading growth in the Public Sector Consulting and Advisory Services market?

Technology consulting leads with 36.5% share in 2025 and a 9.0% CAGR through 2031, driven by cybersecurity, cloud, digital identity, and AI governance mandates.

Which regions are the largest and fastest growing in this market?

North America held 64.5% in 2025, while Asia-Pacific is the fastest growing at 17.9% CAGR on digital public infrastructure replication.

What regulatory shifts are shaping demand in 2026?

OMB’s AI governance memoranda, eIDAS 2.0 wallet deadlines, and procurement streamlining are increasing demand for conformance, interoperability, and outcome-tied delivery.

What are the main constraints on execution?

Data localization requirements and sovereign cloud shifts, procurement scrutiny, complex grants compliance, and scarcity of cleared talent are slowing delivery and elevating costs.

Which buyers are growing spend the fastest?

State and local government buyers are expected to record a 7.0% CAGR to 2031 as they scale outcome-based procurement and modernize digital services.

Page last updated on: