Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

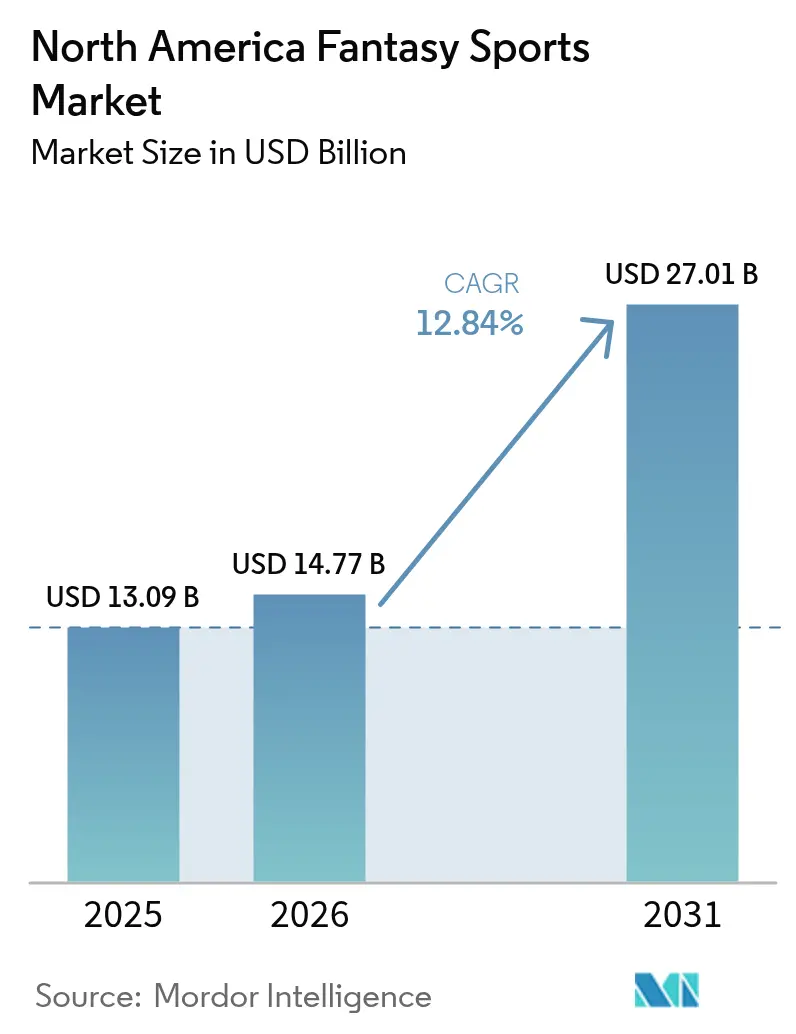

| Base Year Market Size (2025) | USD 13.09 Billion |

| Market Size (2026) | USD 14.77 Billion |

| Market Size (2031) | USD 27.01 Billion |

| Growth Rate (2026 - 2031) | 12.84% CAGR |

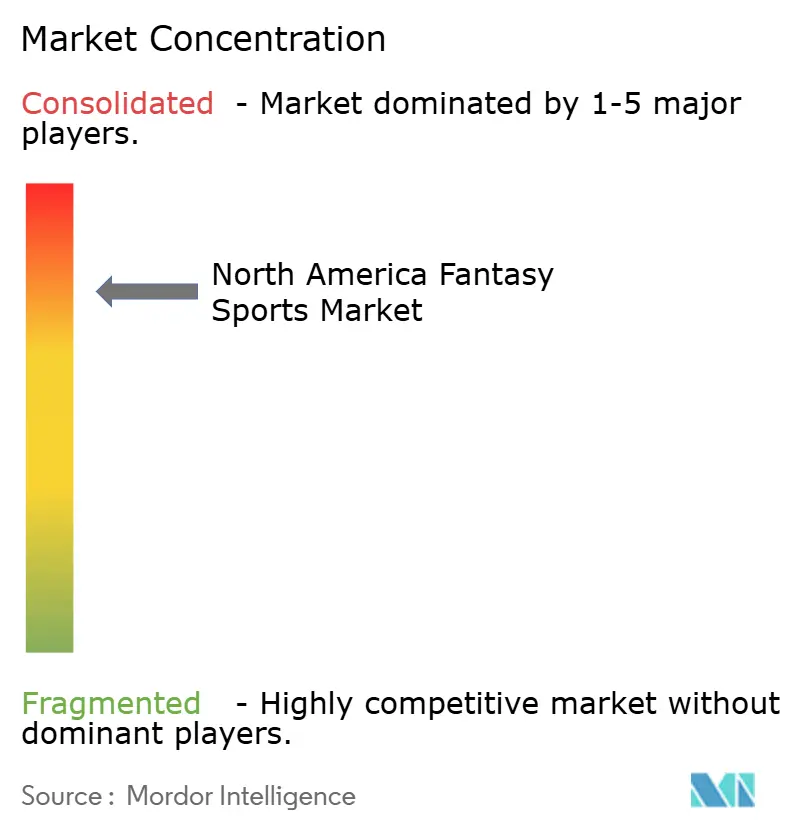

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Fantasy Sports Market Analysis by Mordor Intelligence

The North America fantasy sports market size was valued at USD 13.09 billion in 2025 and estimated to grow from USD 14.77 billion in 2026 to reach USD 27.01 billion by 2031, at a CAGR of 12.84% during the forecast period (2026-2031). The market’s momentum is rooted in regulatory liberalization that now covers more than 90% of the population, in 5G-enabled mobile usage that raises session length, and in product hybrids that merge skill-based contests with real-time wagering.[1]FanDuel Press Team, “FanDuel TV Launches New FAST Channel ‘FanDuel TV Extra,’” press.fanduel.com Emerging ancillary formats, intense duopoly marketing, and rising Gen Z participation continue to expand total addressable demand while compressing margins for smaller operators. Operators are investing in AI-driven personalization, blockchain payments, and cross-media partnerships to widen monetization pathways and reduce customer acquisition cost pressure. Regulatory clarity is also encouraging alliances with leagues and broadcasters, allowing unified data feeds that heighten in-game engagement.

Key Report Takeaways

- By fantasy sports type, Daily/Weekly Fantasy and Ancillaries held 60.55% of the 2025 revenue of the North America fantasy sports market, while the same category is projected to expand at a 13.82% CAGR through 2031.

- By sporting type, American Football commanded 58.25% of the 2025 value of the North America fantasy sports market; Ice Hockey is forecast to post the fastest ascent at a 14.38% CAGR to 2031.

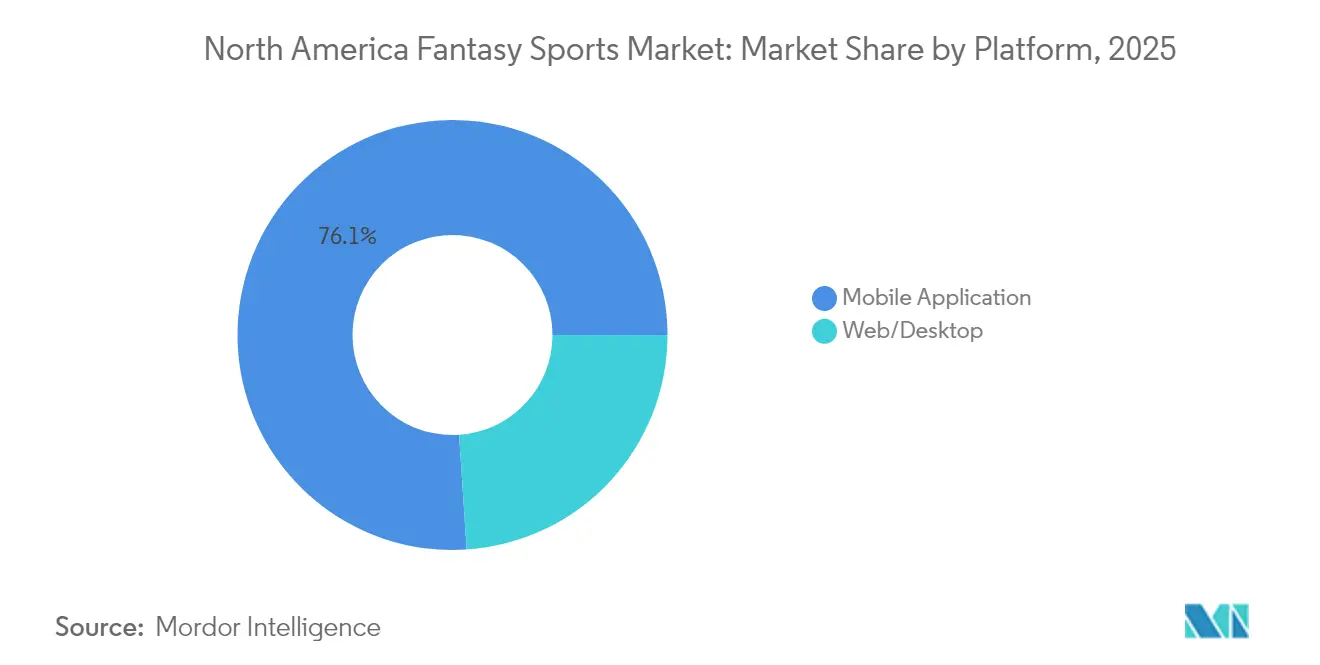

- By platform, mobile applications accounted for 76.05% of user activity in 2025 of the North America fantasy sports market, and also led future growth with a 13.9% CAGR.

- By revenue model, entry-fee rake contests generated 60.95% of the 2025 turnover of the North America fantasy sports market, whereas Hybrid/Ancillary Micro-Betting is advancing at a 14.2% CAGR through 2031.

- By user demographic, the 25-34 age group held 58.10% share of the North America fantasy sports market in 2025, while the 18-24 cohort is expanding most rapidly at a 14.58% CAGR.

- By geography, the United States represented 84.10% of the 2025 market value of the North America fantasy sports market, whereas Canada is projected to grow at a 14.05% CAGR over the forecast horizon the led.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Fantasy Sports Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory expansion to >90% population | +3.2% | United States, Canada | Medium term (2-4 years) |

| Smart-phone and 5G penetration | +2.8% | Urban North America | Short term (≤ 2 years) |

| Major-league schedule growth | +2.1% | United States, Canada | Long term (≥ 4 years) |

| AI-driven personalization | +1.9% | North America early adoption | Medium term (2-4 years) |

| Micro-bet “pick-em” formats | +1.6% | Urban United States, Canada | Short term (≤ 2 years) |

| Streaming of Sunday-Ticket and NHL/MLB packages | +1.4% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Expansion to >90% of North American Population by 2027

State-level legalization is accelerating network effects that lower marginal compliance cost and unlock broader ad inventory on search and social channels. Newly enabled states increase lifetime value because operators can standardize product features across a larger contiguous user base. Unified compliance modules let leading platforms redirect spending from legal vetting to high-yield marketing and product R&D. The trend also encourages strategic partnerships with payment gateways, reducing friction in onboarding. Altogether, wider legality contributes a 3.2% additive lift to forecast CAGR as remaining holdout jurisdictions move toward enabling frameworks.[2]Lexology, “A Safe Bet: FanDuel and DraftKings Are Stifling Competition,” lexology.com

Smart-phone and 5G Penetration Lifts Mobile DFS Traffic

5G networks bring sub-20 millisecond latency, enabling push-based player-prop updates that were impractical on 4G. Real-time data improves lineup optimization and reinforces the daily engagement loop. Operators report a 40% gain in average session length once users migrate to 5G-capable devices. The technology also facilitates biometric login and instant withdrawals, lowering abandonment at key friction points. In parallel, device manufacturers preload sports-betting widgets, shortening the funnel between media consumption and fantasy entry. These shifts collectively add 2.8% to the expected CAGR across the North America fantasy sports market.[3]Qualcomm Technologies, “5G Gaming Insights,” qualcomm.com

Major-League Schedule Growth and Cross-Media Tie-ins

Expanded NBA and MLB game calendars inject more fantasy-eligible events, driving higher contest frequency. League-owned media arms are embedding contest prompts inside live streams, converting passive viewers into active contestants. FanDuel TV Extra, for example, offers over 12 hours of integrated programming that funnels viewers straight into contests through clickable overlays. These tie-ins improve acquisition efficiency by 20% relative to traditional advertising. They also extend user engagement into shoulder seasons, smoothing revenue volatility.

AI-Driven Personalization Raises Session Length and ARPU

Machine-learning models ingest user history to recommend contests, upsell premium data, and time push notifications at peak receptivity. Operators tracking 2024 pilots noted a 15-point improvement in retention after six months, alongside a 12% uplift in ARPU. Real-time personalization also reduces customer support tickets because suggested lineups lower new-user cognitive load. During live play, AI offers micro-bet prompts calibrated to individual risk tolerance, lifting in-game turnover. Over the forecast horizon, personalization accounts for a 1.9% additive CAGR impact, especially as Gen Z usage deepens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-by-state regulatory fragmentation | -2.1% | United States, Canada | Long term (≥ 4 years) |

| Rising CAC amid duopoly-scale ad spend | -1.8% | Competitive North America | Short term (≤ 2 years) |

| KYC/AML compliance and payment surcharges | -1.3% | North America | Medium term (2-4 years) |

| User shift to straight sports-betting | -1.1% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

State-by-state Regulatory Fragmentation and Fee Burden

Each jurisdiction sets unique fee structures ranging from USD 50,000 up to USD 600,000 per license forcing operators to replicate compliance workflows. Maintaining discrete reporting systems elevates fixed costs, curbing smaller entrants’ ability to reach scale. Spot audits and sudden rule reinterpretations have already removed ten operators from Massachusetts in 2024, underscoring headline risk. Capital tied up in bonding requirements and legal contingencies delays feature rollouts, slowing innovation cadence and shaving 2.1% off long-run CAGR.

Rising CAC Amid Duopoly-scale Ad Spend

DraftKings and FanDuel collectively spent more than USD 1.2 billion on marketing in 2024. Their saturation of broadcast and social channels elevated average CAC to USD 300–350, up from USD 200–250 within 18 months. Smaller operators struggle to generate brand recall, driving consolidation as Colorado’s active licensees fell from 26 to 13. To maintain profitability, platforms must extend average customer lifespan by at least four months or introduce higher-margin subscription tiers. The cost headwind reduces forecast CAGR by 1.8%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fantasy Sports Type: Daily Formats Drive Market Evolution

Daily/Weekly Fantasy and Ancillaries captured 60.55% of 2025 revenue, underscoring the shift to instant-gratification experiences that sync with mobile alerts and social feeds. The format’s 13.82% CAGR outpaces season-long contests as operators embed micro-bet props inside lineups, further widening engagement. Transaction frequency aligns earnings with media moments, letting platforms monetize peaks in live viewership. High fill rates also enhance liquidity, supporting larger guaranteed prize pools that attract casual and high-volume users alike. These dynamics cement the daily segment as the cornerstone of the North America fantasy sports market.

Season-long formats still retain legacy users who prize community leagues and deeper research cycles. However, younger cohorts gravitate toward dynamic payout structures and lower commitment windows. Operators reply by automating draft assistance, adding weekly cash-based challenges, and cross-selling season subscribers into daily contests mid-year. The convergence widens average user value, though it increases classification scrutiny as regulatory bodies debate the line between skill and chance.

By Sporting Type: Football Dominance with Hockey Acceleration

American Football delivered 58.25% of 2025 revenue and benefits from a compact weekly cadence that drives concentrated user activity. Statistical depth and cultural ubiquity ensure top-of-mind positioning every fall weekend. Operators lock in user retention through cross-promotions that roll football players into basketball or baseball slates once the Super Bowl concludes. Baseball remains steady due to its near-daily schedule, offering volume traders multiple entries and consistent ARPU. Basketball enjoys both college and pro seasons, extending contest availability into spring.

Ice Hockey is the fastest-growing sub-segment at 14.38% CAGR as streaming reach improves and younger Canadian audiences adopt daily formats. Operators leverage real-time shift data and player tracking to develop premium stat feeds that mirror football’s depth. Growth in niche sports such as golf, soccer, and eSports diversifies revenue, protecting platforms from over-reliance on a single league cycle. Genius Sports’ BetVision expansion into global soccer underscores the wider opportunity set beyond the core four U.S. leagues.

By Platform: Mobile Supremacy with Desktop Persistence

Mobile apps commanded a 76.05% share in 2025 and are projected to grow at a 13.9% CAGR through 2031. Push notifications, location-based offers, and biometric sign-in drive conversion, while 5G low latency supports synchronized in-stream wagering. APIs pull live video synchronized to contest dashboards, helping users manage lineups mid-play. Camera-enabled social sharing turns highlight reels into viral acquisition assets.

Desktop maintains a niche for research-intensive and multi-lineup users. Screen real estate suits advanced optimizer tools and third-party plug-ins. Cohorts alternating between devices generate higher total handle, prompting operators to maintain cross-platform parity. Responsive design and single sign-on ensure state-level compliance while preserving UX consistency.

By Revenue Model: Rake Dominance with Hybrid Innovation

Entry-fee rake contests produced 60.95% of 2025 turnover, giving operators predictable percentage earnings that scale with pool size. Subscription and premium analytics tiers deepen monetization among power users, offering advanced projections and ownership data. Free-to-play ad-supported pools drive funnel top-ups, later converting to paid entries via loyalty mechanics.

Hybrid/Ancillary Micro-Betting is advancing at 14.2% CAGR, layering live player props atop existing contest structures. In-game prompts raise the velocity of wagers, shifting revenue from pre-match peaks to sustained in-event streams. Blockchain payments shrink transaction fees beneath 2%, widening margin on micro wagers originally uneconomic on card rails. Operators see favorable elasticity; average ticket size falls, but volume gains lift gross gaming revenue.

By User Demographic: Millennial Core with Gen Z Expansion

Users aged 25-34 generated 58.10% of 2025 stakes and present the highest lifetime value due to disposable income and deep sports literacy. They gravitate toward higher-buy-in contests and premium data subscriptions. The 35-44 and 45+ bands prefer season-long leagues, showing higher retention yet lower contest frequency.

Gen Z (18-24) is the fastest-growing cohort at 14.58% CAGR. They favor pick-em props, social feeds, and instant withdrawals via digital wallets. Gamified loyalty ladders and referral bonuses resonate strongly, leveraging peer networks for organic growth. Operators localize content with meme-style graphics and short-form video to meet the expectations of this mobile-native audience.

Geography Analysis

The United States accounted for 84.10% of the 2025 value and remains the anchor of the North America fantasy sports market. State-by-state legalization lets operators leverage contiguous marketing, while NFL, NBA, and MLB partnerships secure proprietary data feeds that enhance scoring accuracy and in-app engagement. Tax rate disparities encourage corporate domiciling in favorable jurisdictions, but platform access remains nationwide via geofenced apps.

Canada is accelerating at a 14.05% CAGR as provinces adopt Ontario’s regulatory blueprint. Higher tax burdens prompt operators to emphasize premium tools and subscription bundles to protect margin. NHL coverage offers cultural resonance, while cross-border campaigns leverage brand equity built in the U.S. Localization includes French-language interfaces and debit-first payment options to capture Quebec and Atlantic users.

Mexico is in an early development phase. SEGOB licensing focuses on sportsbook frameworks, leaving fantasy classifications ambiguous. Operators studying entry must integrate OXXO cash deposits and Spanish-language UI, plus soccer-first contest menus. Growth potential is significant, yet dependent on clearer rules and localized marketing that educates consumers on skill-based formats.

Competitive Landscape

The North America fantasy sports market exhibits a duopoly where DraftKings and FanDuel jointly control a roughly 80% share. Both firms carry robust compliance infrastructure and first-mover brand equity, letting them outspend rivals in media and secure exclusive league data. DraftKings’ 2024 acquisition of Simplebet bolstered in-play micro-betting, while FanDuel’s integration of FanDuel TV Extra amplifies cross-media funneling. The companies also lobby collectively through trade associations, shaping favorable regulatory standards.[4]Mogin Law LLP, “A Safe Bet: FanDuel and DraftKings Are Stifling Competition,” moginlaw.com

Mid-tier challengers such as PrizePicks and Underdog Sports target Gen Z with simplified pick-em formats and influencer alliances. They differentiate via low-stakes contests and streamlined UX, though rising CAC pressures profitability. Niche operators focus on individual sports or single states, using local partnerships to build brand presence before expanding.

Technology suppliers like White Hat Studios and Genius Sports monetize data, video, and content tools that power both incumbents and disruptors. Their modular offerings lower build-time for new entrants but deepen dependence on shared infrastructure, reinforcing switching costs. As antitrust scrutiny grows, regulators may revisit data access terms, potentially opening room for alternative providers.

North America Fantasy Sports Industry Leaders

DraftKings Inc.

Flutter Entertainment plc (FanDuel)

Yahoo Inc. (Yahoo Fantasy)

Paramount Global (CBS Sports Digital)

ESPN Enterprises, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Genius Sports rolled out BetVision for more than 120 soccer competitions, introducing touch-to-bet overlays.

- March 2025: White Hat Studios expanded its DraftKings partnership into Pennsylvania.

- March 2025: MetaBet signed a content deal with DraftKings Network, embedding contextual betting widgets.

- January 2025: DraftKings launched a paid subscription tier offering boosted odds and exclusive analytics to enhance retention.

- December 2024: DraftKings completed its Simplebet acquisition, integrating micro-betting APIs into the flagship app.

North America Fantasy Sports Market Report Scope

A fantasy sport (known less commonly as rotisserie or roto) is a kind of game usually played utilizing the Internet, where participants assemble imaginary or virtual teams of actual players of a professional sport. These teams play based on the statistical performance of those members in actual games.

The North America Fantasy Sports Market is segmented by Fantasy Sports Type (Traditional Fantasy Sports, Daily Fantasy Sports & Ancillaries), Sporting Type (Football, Baseball, Basketball, Others), and Country.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Fantasy Sports Type

| Traditional Season-long |

| Daily/Weekly Fantasy and Ancillaries |

By Sporting Type

| American Football |

| Baseball |

| Basketball |

| Ice Hockey |

| Other Sports (Golf, Soccer, eSports) |

By Platform

| Mobile Application |

| Web/Desktop |

By Revenue Model

| Entry-fee Rake Contests |

| Subscription/Premium Tools |

| Advertising-supported Free Play |

| Hybrid/Ancillary Micro-Betting |

By User Demographic

| Age 18-24 |

| Age 25-34 |

| Age 35-44 |

| Age 45+ |

By Country

| United States |

| Canada |

| Mexico |

| By Fantasy Sports Type | Traditional Season-long |

| Daily/Weekly Fantasy and Ancillaries | |

| By Sporting Type | American Football |

| Baseball | |

| Basketball | |

| Ice Hockey | |

| Other Sports (Golf, Soccer, eSports) | |

| By Platform | Mobile Application |

| Web/Desktop | |

| By Revenue Model | Entry-fee Rake Contests |

| Subscription/Premium Tools | |

| Advertising-supported Free Play | |

| Hybrid/Ancillary Micro-Betting | |

| By User Demographic | Age 18-24 |

| Age 25-34 | |

| Age 35-44 | |

| Age 45+ | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America fantasy sports market in 2026?

The market stands at USD 14.77 billion in 2026 and is forecast to reach USD 27.01 billion by 2031.

Which fantasy sports type grows the fastest?

Daily/Weekly Fantasy and Ancillaries expand at 13.82% CAGR, outpacing season-long formats.

Why are customer acquisition costs rising?

A duopoly marketing spend surpassing USD 1.2 billion annually has pushed average CAC to USD 300–350 per user.

Which platform holds the majority of user activity?

Mobile applications account for 76.05% of 2025 usage and are projected to grow at 13.9% CAGR.

What geographic area presents the highest growth rate?

Canada is set to expand at 14.05% CAGR through 2031, driven by provincial regulatory openings.

How will micro-betting influence revenue models?

Hybrid micro-betting grows at 14.2% CAGR, adding live, low-value wagers that deepen ARPU without cannibalizing entry fees.

Page last updated on: