North America ESIM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

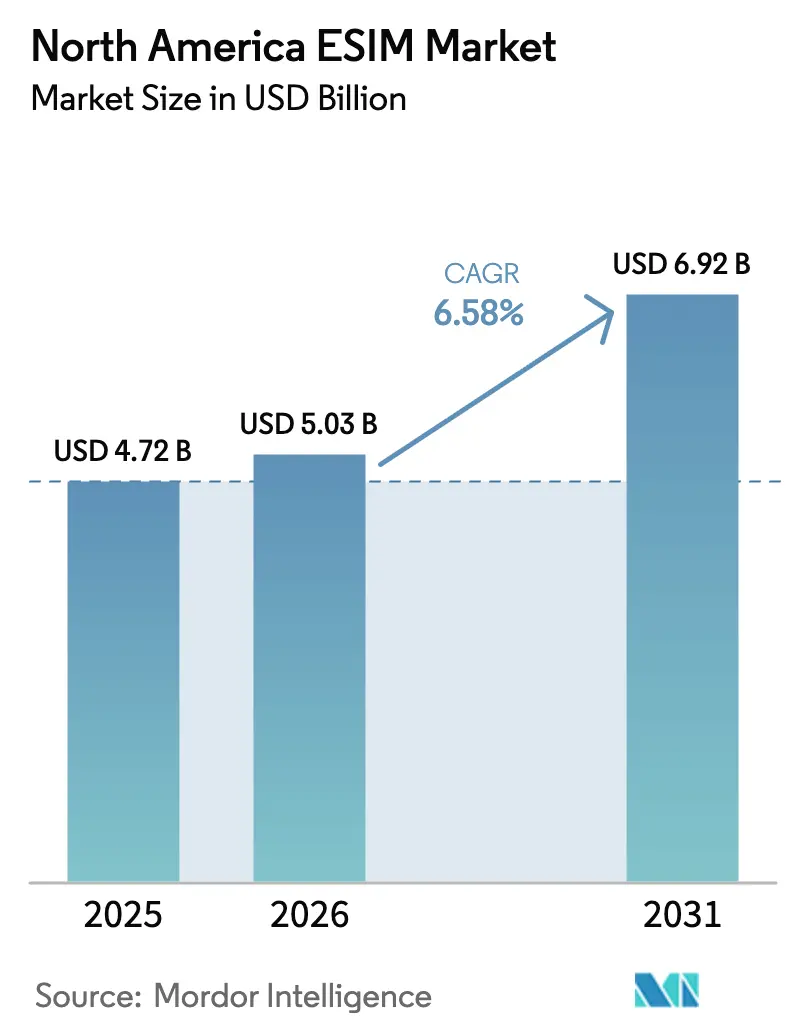

| Base Year Market Size (2025) | USD 4.72 Billion |

| Market Size (2026) | USD 5.03 Billion |

| Market Size (2031) | USD 6.92 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

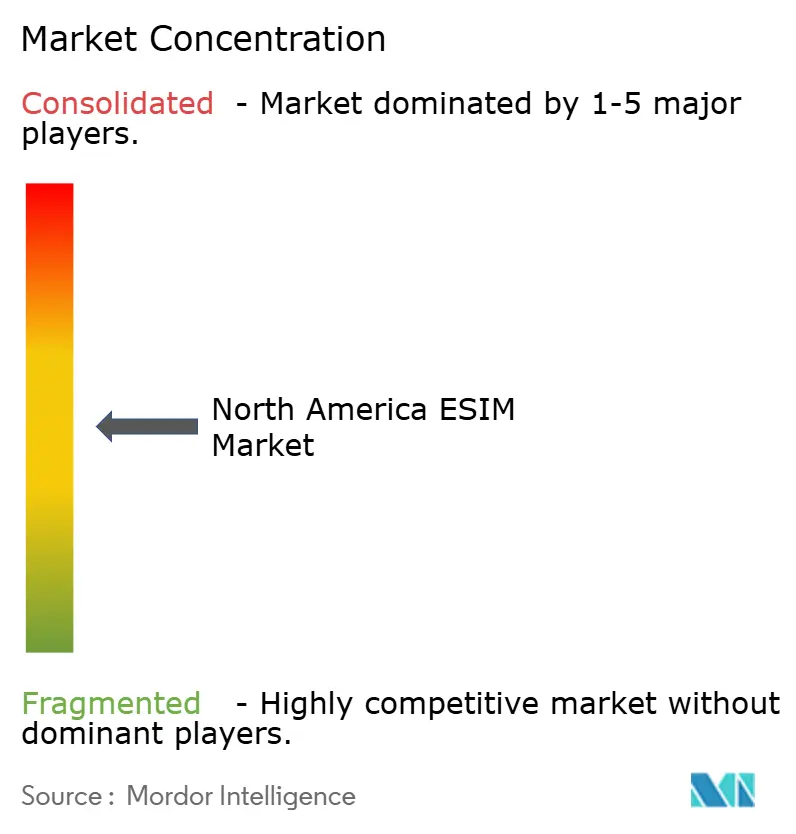

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America ESIM Market Analysis by Mordor Intelligence

The North America eSIM Market size is expected to grow from USD 4.72 billion in 2025 to USD 5.03 billion in 2026 and is forecast to reach USD 6.92 billion by 2031 at 6.58% CAGR over 2026-2031. In terms of shipment volume, the market is expected to grow from 186.79 million units in 2025 to 263.89 million units by 2030, at a CAGR of 7.16% during the forecast period (2025-2030). Accelerated device launches that exclude physical SIM slots, the expansion of enterprise digitization, and supportive US public-safety mandates are collectively reinforcing the region’s first-mover status. A steady migration toward remote SIM provisioning services is reshaping revenue models as carriers favor software-driven activation, while 5G fixed-wireless access (FWA) roll-outs and private networks are broadening the addressable base of industrial and rural users. Industrial IoT, logistics, and asset-tracking use cases are scaling fastest because eSIM minimizes activation costs and supports seamless cross-border connectivity. Competitive intensity is rising as traditional security specialists, chipmakers, and cloud-native start-ups assemble all-in-one offerings that blend hardware, software, and managed services.

Key Report Takeaways

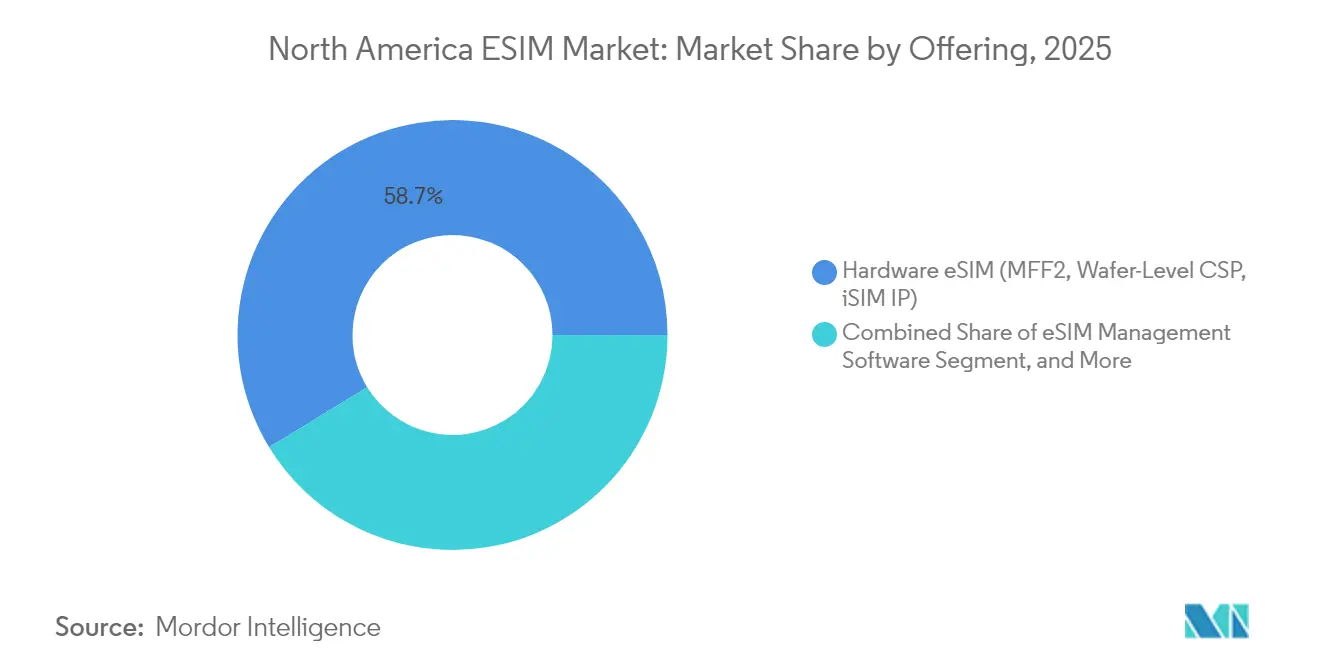

- By offering, the hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) segment led in the North America eSIM market with a 58.74% share in 2025, whereas remote SIM provisioning services are projected to expand at a 10.02% CAGR through 2031.

- By device type, smartphones and feature phones accounted for 54.21% of the North America eSIM market in 2025, whereas M2M/IoT modules are projected to grow at a 10.17% CAGR through 2031.

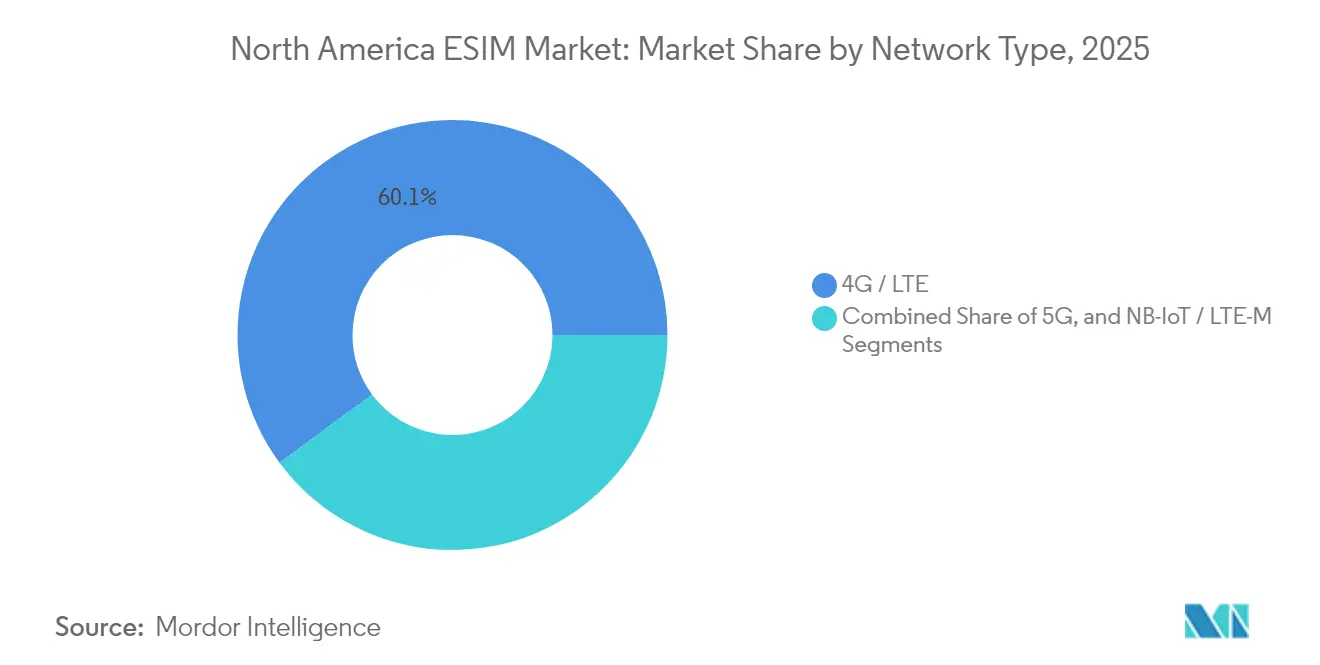

- By network type, 4G/LTE retained 60.12% share of the North America eSIM market in 2025, while 5G is forecast to surge at 15.28% CAGR to 2031.

- By end-user industry, the consumer electronics segment accounted for 61.55% of the North America eSIM market in 2025, while logistics and asset tracking are poised for the fastest growth, with a 14.12% CAGR through 2031.

- By country, the United States captured 81.05% of the North America eSIM market in 2025, while Mexico is projected to register a 9.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America ESIM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sharp Rise in iPhone-Led eSIM-Only Launches | +2.1% | North America-wide, strongest in US urban markets | Short term (≤ 2 years) |

| 5G FWA Rollouts Demanding Remote SIM Provisioning | +1.8% | US rural markets, Canadian remote regions | Medium term (2-4 years) |

| Mandates for Digitized SIM Lifecycle in US FirstNet | +1.2% | United States federal and state agencies | Medium term (2-4 years) |

| Auto-OEM Pivot to Embedded Connectivity for OTA Updates | +0.9% | North America automotive manufacturing hubs | Long term (≥ 4 years) |

| Private-Network Boom in Industry 4.0 Facilities | +0.7% | US manufacturing belt, Canadian industrial zones | Long term (≥ 4 years) |

| Insurance Premium Discounts for eSIM-Enabled Asset Tracking | +0.4% | Cross-border logistics corridors, fleet operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sharp Rise in iPhone-Led eSIM-Only Launches

Removing the physical SIM slot from the iPhone 14 lineup triggered a region-wide rush to upgrade carrier provisioning systems. [1]Apple Inc., “iPhone 14 Pro Launch,” apple.com Service revenues at Apple reached USD 24.2 billion in Q4 2024, underscoring how eSIM unlocks ancillary monetization beyond devices. AT&T shortened in-store activation times by 15%, while T-Mobile accelerated onboarding by 40%. Greater consumer familiarity is now spilling into wearables and tablets, widening attach-rate opportunities for both device makers and operators. Samsung’s decision to extend eSIM to its Galaxy portfolio signals intensified competitive imitation.

5G FWA Rollouts Demanding Remote SIM Provisioning

Verizon’s eSIM-enabled 5G Home now covers more than 70 million U.S. households, demonstrating FWA scalability without truck rolls. [2]Verizon Communications, “5G Private Networks,” verizon.com Eliminating on-site installations reduces deployment costs by nearly 30% compared to fiber alternatives. Canadian operator Rogers has adopted a similar model for northern communities under federal broadband subsidies. [3]Rogers Communications, “Rogers Expands 5G to Rural Communities,” about.rogers.com Dynamic network switching enables gateways to hunt for stronger signals, improving customer retention as rural users gain speeds previously unattainable over copper.

Mandates for Digitized SIM Lifecycle in US FirstNet

The FirstNet Authority compels all public-safety devices to support remote provisioning by 2026, ensuring a captive market for compliant eSIM modules. Requirements also ripple into transport, utilities, and healthcare contractors that interface with emergency responders, spurring wider enterprise adoption. The Department of Homeland Security endorses eSIM for tamper-resistant authentication, aligning federal cybersecurity posture with commercial best practice. [4]Department of Homeland Security, “Critical Infrastructure Security,” cisa.gov Agencies that embrace the technology gain audit-ready visibility over every SIM profile change, a feature lacking in legacy plastic SIM workflows.

Auto-OEM Pivot to Embedded Connectivity for OTA Updates

Ford executed 63 million over-the-air updates across its connected fleet, proving eSIM’s ability to sustain vehicle software life cycles. General Motors and Qualcomm are co-developing platforms that support multiple carrier profiles for global roaming, a step that can reduce connectivity costs by 20-25%. Tesla’s eSIM architecture supports tiered data plans that customers can upgrade on demand, adding post-sale revenue and boosting margins above traditional hardware levels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carrier Reluctance to Cede SIM-Lock Revenue | -1.4% | US postpaid markets, Canadian incumbent carriers | Short term (≤ 2 years) |

| Fragmented Entitlement-Server Standards Among MNOs | -0.8% | Cross-border operations, MVNO ecosystems | Medium term (2-4 years) |

| Limited Hardware PIN-Pad Space in Ultra-Thin Wearables | -0.6% | Premium wearables segment, fashion tech | Long term (≥ 4 years) |

| Cyber-Risk Concerns Over Remote Profile Swaps | -0.5% | Enterprise security-sensitive sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Carrier Reluctance to Cede SIM-Lock Revenue

North American operators net approximately USD 2.3 billion annually from early-termination penalties and unlock requests, revenue lines that are endangered by instant eSIM hopping. Verizon introduced eSIM management surcharges on certain unlimited plans, signaling an attempt to claw back margin. The shift is most acute in postpaid accounts where amortized handset subsidies depend on multi-year loyalty. Canada’s CRTC rule, which forces free device unlocks, amplifies the tension by curbing former lock-in tactics.

Cyber-Risk Concerns Over Remote Profile Swaps

NIST flagged authentication loopholes that could expose corporate networks during profile downloads. A CISA survey showed 68% of Fortune 500 security teams quote eSIM risks as their top IoT hurdle. Multi-profile management increases the attack surface across fleets of phones, gateways, and sensors. Finance and healthcare operators must prove HIPAA and SOX compliance, so they hesitate until zero-trust frameworks mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Services Outpace Hardware Gains

Hardware eSIM modules held a 58.74% share of the North America eSIM market in 2025, owing to enduring demand for soldered MFF2 chips in smartphones and vehicles. Yet remote SIM provisioning services are racing ahead at 10.02% CAGR, indicating that future value pools will come from cloud dashboards, subscription APIs, and lifecycle analytics rather than silicon. The North America eSIM market size tied to management software also gains momentum as enterprises consolidate multi-vendor devices onto single orchestration platforms that ease audit burdens.

Service-centric economics enable carriers to generate new margins from instantaneous profile swaps, cross-border roaming plans, and usage-based IoT bundles. Hardware specialists are responding through joint ventures with cloud providers, as shown by Qualcomm’s pact with IDEMIA to embed iSIM stacks directly into Snapdragon chipsets. The resulting convergence blurs category lines and compresses time-to-market for integrated solutions that preinstall provisioning credentials at the foundry.

By Device Type: IoT Modules Narrow the Gap with Smartphones

Smartphones anchored 54.21% of 2025 revenue, a figure still buoyed by Apple’s aggressive elimination of the SIM tray. However, M2M and IoT boards are projected to post a 10.17% CAGR through 2031, underscoring a shift toward industrial automation, smart logistics, and energy metering. The North America eSIM market share for IoT endpoints is widening as module makers bundle global roaming, tamper-proof security, and compact footprints suitable for harsh environments.

Tablet and laptop shipments continue to profit from the remote-work wave, particularly among field technicians and students who seek out always-on cellular models. Premium wearables face challenges with battery and antenna constraints, yet adoption continues to grow steadily within the fitness, medical alert, and kids’ tracker segments. The GSMA’s SGP.32 standard will further lift constrained-device adoption by lightening memory and processing overhead on sub-100-kilobyte microcontrollers.

By Network Type: 5G Captures Incremental Spend

Although 4G/LTE retained 60.12% of connections in 2025, 5G lines are expanding at a blistering 15.28% CAGR through 2031, propelled by low-latency Industry 4.0, cloud gaming, and edge analytics. The North America eSIM market size allocated to 5G devices accelerates as carriers rely on software provisioning to juggle network slices and private cells inside campuses.

NB-IoT and LTE-M remain relevant for low-throughput sensors requiring decade-long battery life. eSIM permits their remote re-homing across frequency bands when operators re-farm spectrum. Policy-based selection engines embedded in the eSIM profile negotiate optimal bearer services, enhancing resilience for smart utilities and environmental monitoring.

By End-user Industry: Logistics and Asset Tracking Sprint Ahead

Consumer electronics accounted for 61.55% of 2025 revenue, driven by the high shipment volume of phones, tablets, and smartwatches. Yet logistics and asset-tracking lines will chart the fastest 14.12% CAGR to 2031 as insurers slash premiums for fleets that mount eSIM beacons enabling live cargo visibility. North America eSIM market size growth in transport stems from cross-dock orchestration that demands always-on telemetry across U.S.-Mexico trade corridors.

Automotive OEMs embed multiple operator profiles to guarantee roaming resilience for over-the-air updates and emergency call mandates. Industrial conglomerates utilize private 5G and eSIM to authenticate thousands of robots without requiring manual SIM swaps. Healthcare providers cautiously expand the use of telehealth gadgets but must navigate HIPAA encryption requirements, which elevate demand for secure element-grade chipsets.

Geography Analysis

The United States accounted for 81.05% of regional revenue in 2025, underpinned by dense 5G coverage, aggressive handset subsidies, and firm regulatory backing that enforces eSIM support across public-safety networks. Major cities double as living labs where carriers pilot edge compute and network slicing, showcasing eSIM’s fast profile activation for pop-up private networks. Enterprise procurement policies increasingly mandate single-SKU devices that roam globally on dual profiles, driving volume orders.

Canada contributes a stable revenue tranche as Rogers, Bell, and Telus synchronize eSIM roll-outs that pair consumer plans with IoT remote-provisioning portals. Remote communities in Nunavut and Yukon benefit from government funds that support FWA deployments, which require zero-touch activation. Cross-border trucking firms rely on multi-profile eSIM modems to avoid roaming surcharges between Alberta's oil sands and Montana refineries, thereby boosting demand from heavy machinery OEMs.

Mexico, although smaller, registers the fastest 9.42% CAGR through 2031, driven by MVNO entrants that utilize eSIM apps to target prepaid smartphone users without requiring retail kiosks. Maquiladora factories spanning Sonora to Nuevo León prefer eSIM-enabled routers that hop seamlessly onto U.S. networks for cloud backhaul. Rising smartphone adoption, remittance-driven data sharing, and cross-border family plans further accelerate growth.

Competitive Landscape

Incumbent security titans Thales, Giesecke+Devrient, and IDEMIA still ship the bulk of eSIM operating systems; yet, chipmakers like Qualcomm, STMicroelectronics, and Infineon are embedding secure elements directly onto system-on-chip (SoC) dies, squeezing the margins of discrete cards. Cloud-native disruptors, such as Kigen and Amdocs, court operators with API-first provisioning stacks that reduce integration times from months to days. AT&T now bundles Thales’ Adaptive Connect into its global IoT profile manager, expanding its reach across more than 200 territories.

Acquisitions accelerate capability consolidation, as seen in G+D’s purchase of the IoT platform Pod Group, which broadened its service layer, and STMicroelectronics' investment in eSIM firmware start-ups to cement silicon-plus-services bundles. Verizon, Rogers, and América Móvil share entitlement-server standards aimed at frictionless roaming across North America, a move to deter OTT connectivity brokers.

White-space opportunities exist around satellite-cellular hybrid eSIMs, edge gateway attestation, and zero-trust policy engines suited to critical infrastructure. Vendors able to pre-certify against NIST, CISA, and FCC benchmarks are likely to win high-security public-sector deals, as agencies divert budgets toward more secure connectivity.

North America ESIM Industry Leaders

Thales S.A.

Giesecke+Devrient (GmbH)

IDEMIA Group, S.A.S.

STMicroelectronics N.V.

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Evergy partnered with Kigen to deploy secure eSIM OS and eIM solutions combining private LTE with public networks to fortify grid resilience amid rising weather threats.

- October 2025: AT&T and Thales introduced an eSIM driven by Adaptive Connect that integrates into the AT&T Virtual Profile Management for IoT, servicing automotive, smart-city, healthcare, and utility sectors.

North America ESIM Market Report Scope

The North America eSIM Market Report is Segmented by Offering (Hardware eSIM [MFF2, Wafer-Level CSP, iSIM IP], eSIM Management Software, Remote SIM Provisioning Services), Device Type (Smartphones and Feature Phones, Tablets and Laptops, Wearables, M2M/IoT Modules), Network Type (5G, 4G/LTE, NB-IoT/LTE-M), End-user Industry (Consumer Electronics, Automotive and Transportation, Industrial and Manufacturing, Logistics and Asset Tracking, Energy and Utilities, Healthcare and Wearables), and Country (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software |

| Remote SIM Provisioning Services |

| Smartphones and Feature Phones |

| Tablets and Laptops |

| Wearables |

| M2M/IoT Modules |

| 5G |

| 4G/LTE |

| NB-IoT/LTE-M |

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Logistics and Asset Tracking |

| Energy and Utilities |

| Healthcare and Wearables |

| United States |

| Canada |

| Mexico |

| By Offering | Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software | |

| Remote SIM Provisioning Services | |

| By Device Type | Smartphones and Feature Phones |

| Tablets and Laptops | |

| Wearables | |

| M2M/IoT Modules | |

| By Network Type | 5G |

| 4G/LTE | |

| NB-IoT/LTE-M | |

| By End-user Industry | Consumer Electronics |

| Automotive and Transportation | |

| Industrial and Manufacturing | |

| Logistics and Asset Tracking | |

| Energy and Utilities | |

| Healthcare and Wearables | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is driving enterprise demand for the North America eSIM market?

Mandates such as FirstNet, 5G FWA roll-outs, and IoT asset-tracking needs push enterprises to adopt remote provisioning for scalability and security.

How fast will 5G connections grow relative to 4G?

5G eSIM lines are expected to expand at a 15.28% CAGR through 2031, outpacing 4G, which continues to decline in share.

Which device category will post the highest growth?

M2M/IoT modules are projected to see a 10.17% CAGR, reflecting industrial digitization.

Why is Mexico the fastest-growing geography?

MVNO competition, cross-border manufacturing, and supportive regulation elevate Mexico’s forecast CAGR to 9.42%.

What restraint could most hinder adoption?

Carrier reluctance to lose SIM-lock revenue remains the strongest single drag, knocking an estimated 1.4% off CAGR potential.

Which end-user segment offers the richest opportunity beyond consumer phones?

Logistics and asset tracking is forecast to expand at 14.12% CAGR as insurers reward eSIM-enabled visibility.

Page last updated on: