Embedded SIM (eSIM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Volume (2026) | 0.65 Billion units |

| Market Volume (2031) | 2.12 Billion units |

| Growth Rate (2026 - 2031) | 26.67% CAGR |

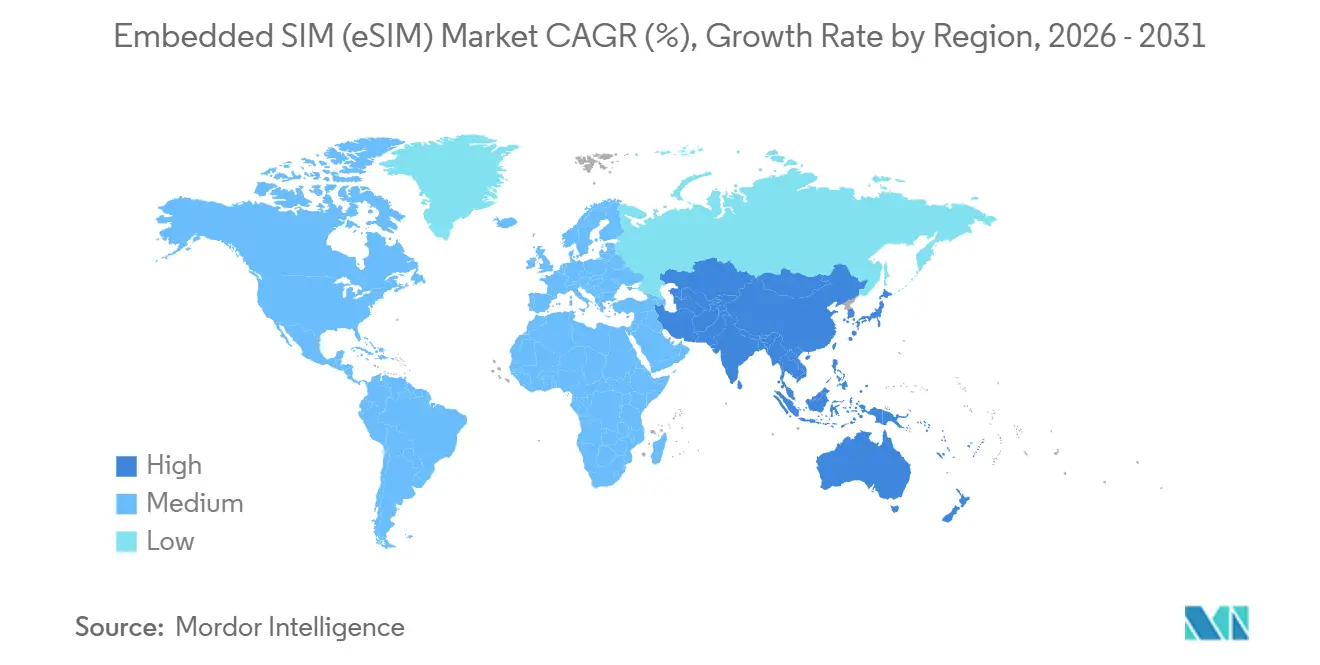

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embedded SIM (eSIM) Market Analysis by Mordor Intelligence

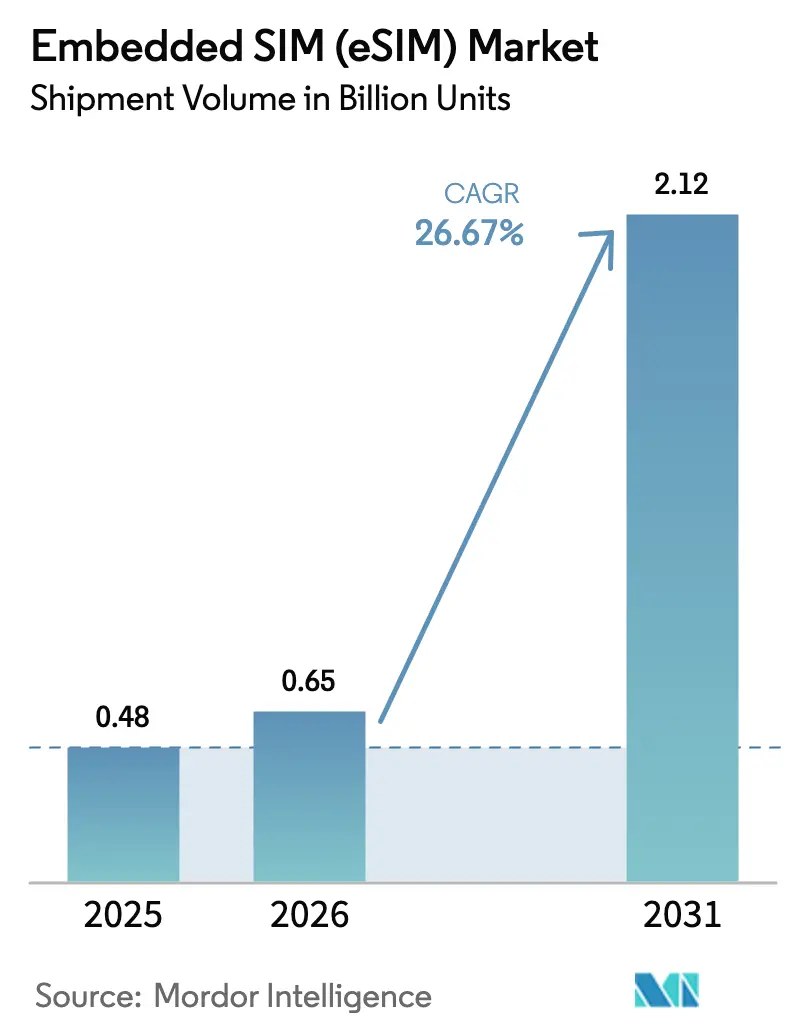

The Embedded SIM Market size in terms of shipment volume is projected to be 0.48 Billion units in 2025, 0.65 Billion units in 2026, and reach 2.12 Billion units by 2031, growing at a CAGR of 26.67% from 2026 to 2031.

The sector is rapidly transitioning away from removable subscriber identity modules toward soldered or integrated alternatives. This growth pattern mirrors three converging shifts: premium-tier smartphones eliminating SIM trays, automotive cybersecurity mandates embedding always-connected telematics, and the June 2024 ratification of the GSMA SGP.32 specification that harmonizes remote provisioning for industrial deployments. Demand is further amplified by nationwide 5G standalone rollouts, which enable low-latency network slicing for use cases ranging from remote surgery to autonomous logistics, and by mobile network operators’ quest to cut operating expenditures tied to plastic card logistics. Competitive dynamics favor semiconductor vendors that integrate secure elements at the wafer level, while traditional SIM card manufacturers confront margin compression. Supply-chain trust concerns, consumer awareness gaps in price-sensitive markets, and dual-stack provisioning costs moderate the momentum but have not derailed adoption trajectories.

Key Report Takeaways

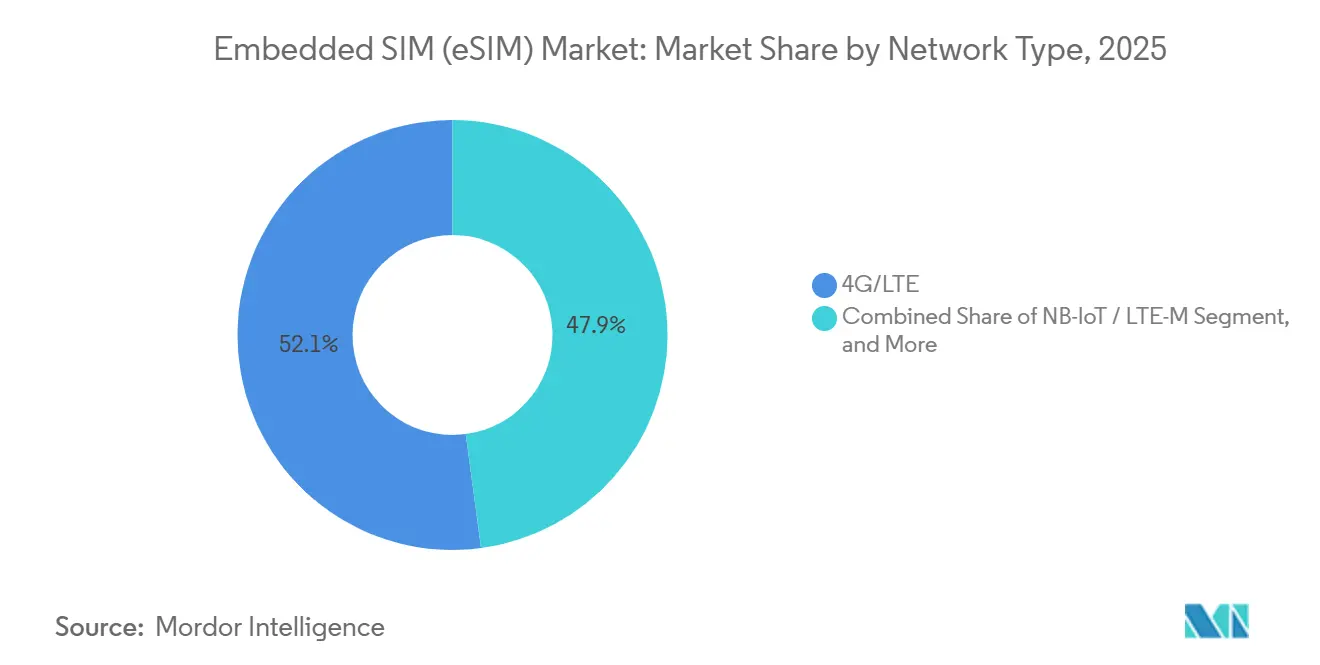

- By network type, 4G/LTE led with 52.11% of the embedded SIM (eSIM) market share in 2025, while 5G is forecast to advance at a 26.89% CAGR through 2031.

- By device type, smartphones commanded 60.29% share of the embedded SIM (eSIM) market size in 2025, whereas wearables are projected to post a 26.76% CAGR during 2026-2031.

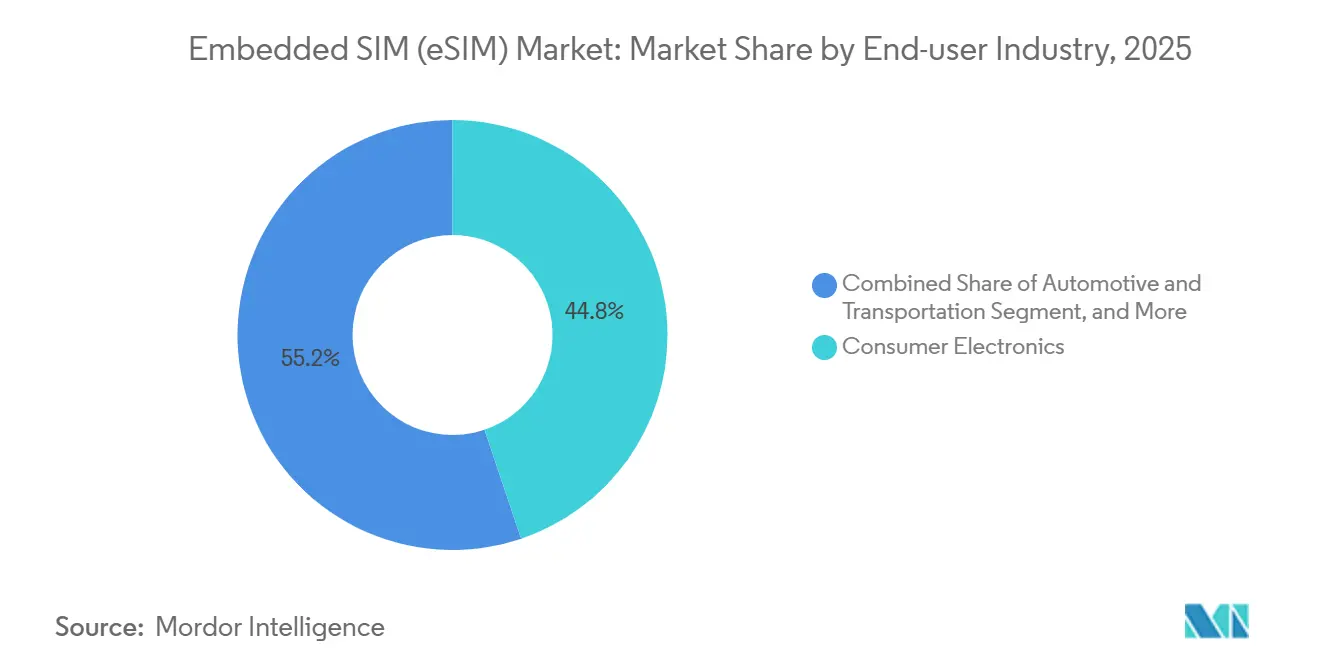

- By end-user industry, consumer electronics accounted for 44.84% of the embedded SIM (eSIM) market size in 2025, but automotive and transportation is expected to record the fastest 27.11% CAGR to 2031.

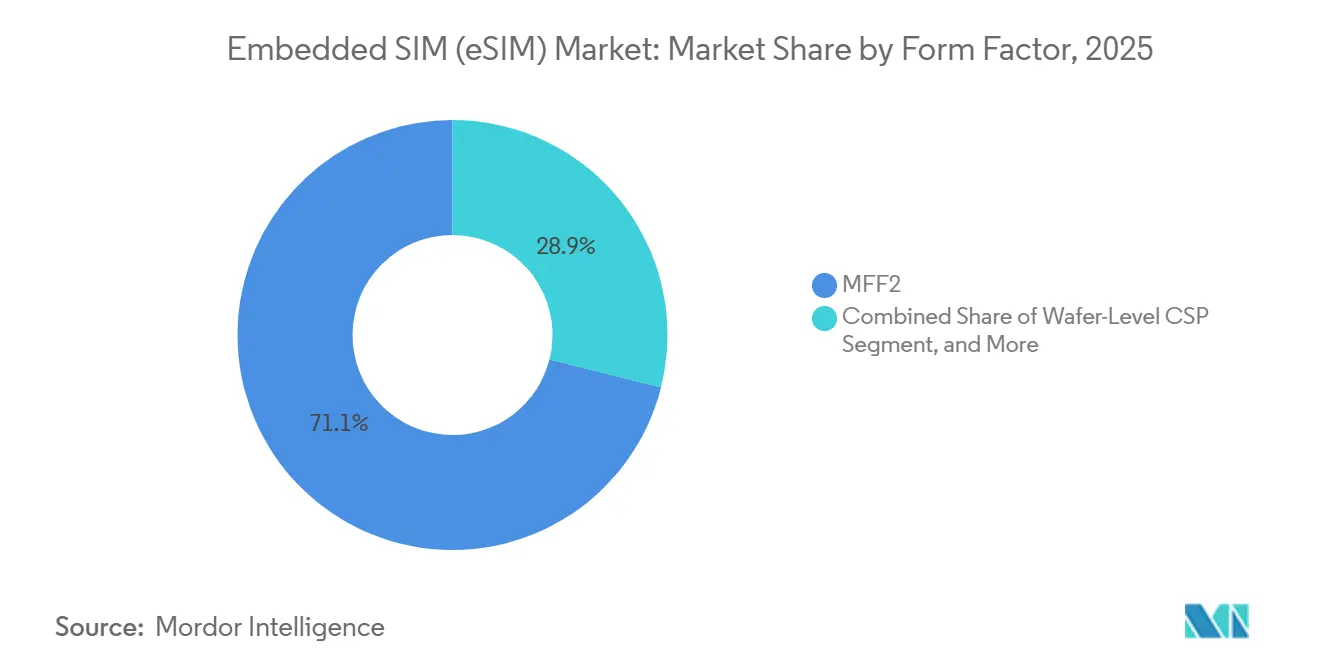

- By form factor, MFF2 modules captured 71.07% share in 2025, yet wafer-level chip-scale packages are set to grow at a 29.38% CAGR over the forecast period.

- By provisioning specification, SGP.02 (M2M) represented 67.22% of 2025 shipments, while SGP.32 (IoT) is on track for a 28.12% CAGR through 2031.

- By geography, North America held 39.39% share in 2025, whereas Asia Pacific is projected to expand at a 27.36% CAGR and emerge as the fastest-growing region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Embedded SIM (eSIM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Roll-Outs Accelerating eSIM Demand | +5.2% | Global, led by Asia Pacific and Middle East | Medium term (2-4 years) |

| Mandates for eCall and UN-R155 Driving Automotive Adoption | +4.8% | Europe and North America, spillover to Asia Pacific | Long term (≥4 years) |

| Apple-Led Smartphone OEM Shift to eSIM-Only Flagships | +6.1% | North America and Europe core, expanding to Asia Pacific | Short term (≤2 years) |

| Telco OPEX Savings Via Remote SIM Provisioning | +3.9% | Global | Medium term (2-4 years) |

| Government IoT Security Regulations Favoring Soldered SIMs | +3.4% | Europe, North America, select Asia Pacific markets | Long term (≥4 years) |

| Emergence of GSMA SGP.32 Specification Unlocking Mass-Scale IoT Deployments | +4.7% | Global, industrial hubs in Europe and Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Roll-Outs Accelerating eSIM Demand

Standalone 5G networks remove latency and throughput constraints that previously limited cellular IoT, enabling devices to switch network slices and roaming partners without physical intervention. China surpassed 1 billion 5G connections in 2024, and carriers there finalized nationwide eSIM enablement by October 2025. Japan achieved 98.4% population coverage in 2024 and targets 99% by 2030, giving enterprises a contiguous national footprint for remote provisioning. In Europe, household coverage reached 94.3% in 2024, creating a launchpad for smart-home and industrial sensors that rely on soldered SIMs.[1]European Commission, “5G Observatory Quarterly Report,” ec.europa.eu Vodafone’s 5G standalone roaming proof-of-concept with A1 and Ericsson in April 2025 showcased frictionless cross-border profile switching.[2]Vodafone Group, “Standalone 5G Roaming Trial Press Release,” vodafone.com As operators commercialize network slicing, enterprises can guarantee quality of service while dynamically selecting carriers, catalyzing shipment growth across industrial gateways and connected vehicles.

Mandates for eCall and UN-R155 Driving Automotive Adoption

The United Nations UN-R155 regulation, compulsory for new vehicle types from July 2024, demands cyber-threat monitoring and secure over-the-air updates, both of which favor tamper-resistant embedded SIM designs. Europe’s eCall directive has already hard-wired cellular emergency connectivity into passenger cars, and new models increasingly adopt soldered eSIMs to meet anti-removal requirements. Continental launched UN-R155-aligned cybersecurity solutions in November 2024 integrating eSIM modules to push security certificates remotely. Thales and Cubic followed in February 2025 with an SGP.32-compliant automotive platform that allows fleet managers to change mobile network operators over the air, lowering roaming charges for cross-border operations thalesgroup.com. As other regions copy the European framework, vehicle production volumes translate directly into multi-year demand for robust eSIM form factors.

Apple-Led Smartphone OEM Shift to eSIM-Only Flagships

Apple removed the SIM tray from iPhone 14-16 U.S. variants, forcing operators to industrialize eSIM activation workflows and signaling to rival brands that premium design now equates to slotless hardware apple.com. Samsung responded by integrating dual-eSIM support in its Galaxy S24 family, while Qualcomm embedded iSIM in Snapdragon 8 Gen 3 to eliminate the discrete secure element qualcomm.com. KPN’s May 2025 one-click eSIM transfer pilot cut iPhone activation steps to a single tap, addressing friction identified by GSMA Intelligence, which found global consumer awareness at only 50% in 2025 kpn.com. The cascading effect is a shorter replacement cycle for legacy SIM cards and accelerated infrastructure upgrades across operator footprints.

Limited Consumer Awareness Outside Premium Handsets

Despite strong traction in affluent regions, GSMA Intelligence reported in March 2025 that only 50 % of global mobile users recognize eSIM terminology, with awareness dropping below 30 % in price-sensitive markets.[3]“Consumer Awareness of eSIM 2025,” gsmaintelligence.com Retail channel incentives still favor plastic SIM card sales, slowing operator marketing in Africa and parts of Asia. Latin America illustrates the gap: 30 carriers launched eSIM by mid-2024, yet only 5 % of smartphone connections used the technology at end-2023. Promotion campaigns such as TIM Brazil’s free trial in late 2023 skewed toward travelers and early adopters, confirming the education challenge. Until low-cost Android devices offer seamless activation and carriers simplify onboarding, mainstream uptake will lag premium tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented M2M Entitlement Specifications | -2.1% | Global, high friction in multi-vendor IoT ecosystems | Medium term (2-4 years) |

| Limited Consumer Awareness Outside Premium Handsets | -3.3% | Emerging markets across Asia Pacific, Africa, South America | Short term (≤2 years) |

| Supply-Chain Trust Concerns (Tamper and Side-Channel Attacks) | -1.8% | Global, heightened scrutiny in Europe and North America | Long term (≥4 years) |

| Operator Lock-In Worries Among Enterprise IoT Buyers | -1.6% | Global, especially multi-national deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented M2M Entitlement Specifications

Enterprises managing long-life industrial assets must juggle legacy SGP.02 provisioning stacks alongside newer SGP.32 workflows, inflating integration budgets and expanding the attack surface. Giesecke and Devrient’s April 2025 attainment of full SGP.32 certification required major server re-architecture and cross-vendor test cycles, illustrating the technical lift.[4]SGP.32 Certification Announcement,” gi-de.com Utilities, logistics, and transportation verticals with 15-year device lifecycles are unwilling to abandon installed SGP.02 fleets, forcing dual-stack operations through at least 2035. The resulting complexity dampens near-term shipment growth for SGP.32 modules and partially offsets the embedded SIM (eSIM) market’s otherwise steep expansion curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Network Type: 5G Standalone Cores Reshape Provisioning

4G/LTE retained 52.11% embedded SIM (eSIM) market share in 2025 as a sizable installed base of smartphones and IoT sensors remained anchored to established networks. The 5G segment is, however, projected to scale at a 26.89% CAGR, reflecting operator migration to standalone cores that permit network slicing, ultra-reliable low-latency communication, and carrier aggregation. China’s three national carriers concluded nationwide eSIM rollouts in October 2025, leveraging 5G architecture to deliver dynamic profile switching for autonomous trucking corridors. In Japan and the European Union, combined 5G population coverage above 94% enables real-time over-the-air provisioning for connected factories and smart-city grids.

As millimeter-wave densification advances, urban private networks will adopt embedded SIM (eSIM) market size modules that can toggle between public and dedicated slices without downtime. Operators in rural markets continue to deploy NB-IoT and LTE-M for low-bandwidth sensors, creating a dual-network strategy that favors multi-mode eSIM chipsets. Over the forecast horizon, 4G will migrate into maintenance mode, while 5G’s contribution to embedded SIM (eSIM) market revenues surges, propelled by industrial automation, remote health care, and immersive media applications that demand deterministic latency guarantees.

By Device Type: Wearables Outpace Smartphones in Growth Velocity

Smartphones accounted for 60.29% of 2025 unit shipments, yet the category’s mid-single-digit growth contrasts with the 26.76% CAGR expected for wearables through 2031. Continuous-glucose monitors, cardiac implants, and fall-detection pendants from Medtronic and Abbott rely on always-on cellular links to cloud dashboards, removing the need for handset tethering. Embedded SIM solutions eliminate ingress points for moisture, dust, and tampering, critical to medical and fitness devices worn 24 hours a day. Laptops and tablets exploit instant-connect financing models that bundle data plans at point of sale, while M2M modules enable asset-tracking beacons and smart-meter retrofits.

Wearables also benefit from wafer-level chip-scale packaging that halves energy draw, extending battery life for thin form factors. Samsung’s eSIM v3.0 specification introduces multiple enabled profiles, supporting personal and corporate lines on a single watch, while Qualcomm-Thales iSIM platforms place the secure element inside the system-on-chip. As health insurers reimburse remote monitoring and enterprises embrace field-force digitization, embedded SIM (eSIM) market size shipments for wearables are set to eclipse tablets by mid-forecast, solidifying the segment as the second-largest contributor after smartphones.

By End-User Industry: Automotive Electrification Drives Connectivity Mandates

Consumer electronics dominated with 44.84% embedded SIM (eSIM) market size share in 2025. Regulatory tailwinds now position automotive and transportation to grow at 27.11% CAGR, fueled by UN-R155 cybersecurity compliance, eCall requirements, and the rise of electric drivetrains that necessitate constant software updates. GSMA SGP.32-compliant platforms from Thales enable fleet managers to switch carriers remotely, optimizing roaming expenses for cross-border logistics. Industrial and manufacturing verticals adopt eSIM to underpin predictive-maintenance sensors and robotic control cells where downtime costs can exceed USD 100,000 per hour.

Logistics and asset tracking lean on ultra-low-power eSIM modules that combine GPS and cellular radios, offering unified visibility across multimodal supply chains. Utilities and energy providers embed secure elements in smart meters to safeguard revenue collection and comply with cyber-resilience legislation. Healthcare deployments span remote diagnostics and medication adherence devices, benefiting from hardware-anchored encryption that meets HIPAA and GDPR mandates. By 2031, automotive is poised to overtake consumer electronics in absolute shipment volumes, making the sector a major force within the embedded SIM (eSIM) market.

By Form Factor: Wafer-Level Integration Compresses Bill of Materials

MFF2 packages secured 71.07% of 2025 volume because their vibration tolerance and extended temperature range suit automotive and industrial use cases. Wafer-level chip-scale packages, however, are forecast to expand at a 29.38% CAGR as smartphones and wearables chase thinner profiles and longer battery life. Infineon’s OPTIGA Connect OC1230 delivers 50% lower power draw through 28 nm CSP construction.

Plug-in accessories target retrofit scenarios; Digi International’s December 2025 SGP.32 dongle offers firmware-based upgrades for legacy field devices, side-stepping complete hardware replacement. iSIM architectures, validated by Qualcomm-Thales on Snapdragon 8 Gen 3, further condense components, freeing board space and reducing per-unit cost by USD 1-2 in mass-market smartphones. Over the forecast window, wafer-level and iSIM formats will capture incremental share in consumer electronics, while MFF2 remains entrenched in safety-critical transport and industrial control installations.

By Provisioning Specification: SGP.32 Resolves IoT Fragmentation

SGP.02 (M2M) held 67.22% of 2025 shipments because installed industrial fleets rely on legacy provisioning servers. SGP.32 (IoT) is projected to grow at a 28.12% CAGR as enterprises seek a unified, multi-operator workflow. IDEMIA’s August 2025 certification spurred more than 40 pilots across utilities and logistics idemia.com. AT&T and Thales launched commercial SGP.32 services in October 2025, allowing zero-touch profile swaps that keep smart-city assets online.

SGP.02 persists in legacy industrial fleets due to multi-year certification cycles, but its lack of multi-operator interoperability drives higher OPEX. T-Mobile’s joint solution with Thales and SIMPL converges SGP.22 and SGP.32 under one platform, simplifying mixed-device estates. As procurement cycles align with depreciated capex schedules, SGP.32-capable shipments will overtake SGP.02 by volume before 2029, anchoring the embedded SIM (eSIM) market to a unified provisioning framework.

Geography Analysis

North America held 39.39% of 2025 unit volumes on the back of Apple’s eSIM-only iPhone lineup and enterprise IoT rollouts in healthcare and logistics. Operators leverage matured 5G standalone cores to monetize premium data plans and remotely provision industrial gateways across oilfields and rail networks. Consumer adoption benefits from widespread carrier marketing that bundles travel eSIM packages into unlimited plans.

Asia Pacific is set to become the fastest-expanding region at a 27.36% CAGR to 2031. China’s October 2025 nationwide rollout covers more than 1 billion 5G connections, enabling low-cost Android makers to eliminate SIM trays and free board space for larger batteries. India followed with Tata Communications and BSNL launching pan-India eSIM in October 2025, targeting both smartphone users and smart-meter deployments in rural electrification programs. Japan and South Korea, already near-saturated in 5G coverage, deploy eSIM in connected cars, wearable payment devices, and smart factories.

Europe enjoys regulatory pull, with 94.3% household 5G coverage and mandates such as eCall and UN-R155 that embed connectivity into vehicle homologation. The Radio Equipment Directive coming into force in August 2025 raises cybersecurity bars, nudging device makers toward soldered eSIM designs. Middle East adoption accelerates, with stc’s national platform in Saudi Arabia cutting SIM logistics and MENA connections forecast to reach 135 million by 2028. Africa remains at a nascent stage except for pilot programs in South Africa and Nigeria, where urban operators test eSIM to serve expatriates and enterprise fleets.

South America shows rising momentum as 30 operators in 14 nations offer eSIM services. Penetration jumps from 5% in 2023 to an expected 75% of smartphone connections by 2030, aided by roaming-friendly tourist markets in Brazil and Argentina. Consumer awareness campaigns, combined with lower-cost eSIM-ready handsets, are expected to unlock latent demand across prepaid segments.

Competitive Landscape

The embedded SIM (eSIM) market is witnessing a competitive tussle among semiconductor suppliers, provisioning-platform vendors, and mobile network operators. Giesecke and Devrient, capitalizing on their early-mover advantage, achieved SGP.32 compliance in April 2025. This strategic move garnered them over 20 design wins and more than 40 pilot projects. Meanwhile, Infineon is carving a niche by emphasizing energy efficiency, utilizing 28 nm wafer-level secure elements to prolong the battery life of wearables. Thales, on the other hand, is banking on a holistic approach, integrating chip fabrication, entitlement servers, and forging alliances with carriers, to achieve a remarkable feat of 23 million installations in connected vehicles.

System-on-chip giants are making waves in the industry: Qualcomm and Thales have successfully validated the inaugural GSMA-certified iSIM on the Snapdragon 8 Gen 3. Juniper Research projects a meteoric rise in iSIM shipments, forecasting an ascent from 800,000 units in 2024 to a staggering 210 million by 2028. This surge is poised to draw volume away from traditional discrete secure element suppliers. As operators increasingly gravitate towards vendor-agnostic entitlement servers, valued for their cost-effectiveness and streamlined audit trails in line with cybersecurity mandates, a wave of platform consolidation appears imminent.

Start-ups are carving out niches in specialized sectors like precision agriculture, cold-chain monitoring, and micro-mobility. However, as the GSMA tightens its certification processes, these newcomers are encountering escalating technical challenges. Looking ahead, the landscape is set for strategic mergers between semiconductor firms and platform vendors, aiming to forge cohesive hardware-software ecosystems. Simultaneously, traditional card manufacturers are at a crossroads, contemplating a shift towards value-added services or a complete exit from the arena.

Embedded SIM (eSIM) Industry Leaders

Giesecke+Devrient GmbH

STMicroelectronics N.V.

Infineon Technologies AG

Thales Group

IDEMIA France SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: 1GLOBAL and Revolut Poland partnered to bundle eSIM mobile plans inside Revolut’s digital wallet for Polish users, enabling frictionless roaming across Europe.

- December 2025: Digi International released an SGP.32 accessory that upgrades legacy modules via firmware, giving enterprises a retrofit path to remote provisioning.

- November 2025: Orange deployed a cloud entitlement server supporting self-service profile transfers, cutting call-center activity for SIM swaps by an estimated 40 %.

- October 2025: China Telecom, China Mobile, and China Unicom completed nationwide eSIM enablement, covering the country’s 1 billion 5G connections.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the embedded SIM (eSIM) market as the worldwide value generated when remotely provisioned, GSMA compliant eUICC chips are sold pre-soldered inside smartphones, wearables, PCs, IoT modules, and connected vehicles, together with the cloud management software that activates and updates profiles over cellular networks. Value from traditional removable SIM cards, proprietary iSIMs still in pilot, and pure connectivity data plans is excluded.

(Scope exclusions: We do not count revenue from legacy plug-in SIM cards, stand-alone M2M connectivity contracts, or proprietary embedded secure elements that lack eUICC support.)

Segmentation Overview

- Overall Market Estimates

- Total Market Value

- By Network Type

- 5G

- 4G/LTE

- NB-IoT / LTE-M

- By Device Type

- Smartphones

- Tablets and Laptops

- Wearables

- M2M/IoT Modules

- By End-User Industry

- Consumer Electronics

- Automotive and Transportation

- Industrial and Manufacturing

- Logistics and Asset Tracking

- Energy and Utilities

- Healthcare and Wearables

- By Form Factor

- MFF2

- Wafer-Level CSP

- Plug-In eSIM

- By Provisioning Specification

- SGP.02 (M2M)

- SGP.22 (Consumer)

- SGP.32 (IoT)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with mobile operators, eUICC design engineers, and automotive connectivity managers across North America, Europe, and Asia-Pacific let us validate activation rates, clarify ASP compression in mid-tier phones, and confirm forecast inflection points such as the planned shift of two leading handset OEMs to eSIM only models in 2027.

Desk Research

Mordor analysts review device production tallies from sources such as UN Comtrade customs data, GSMA Intelligence device adoption dashboards, and national telecom regulator shipment filings, then enrich them with tariff breakouts from Volza import-export data. Industry journals, patent families accessed via Questel, and company 10-Ks help us benchmark average selling prices and upcoming regulation (for instance, eCall mandates in Europe). Selected news feeds on Dow Jones Factiva track quarterly operator eSIM profile downloads. The desk sources named above are illustrative; many additional public and paid references inform our library.

Market-Sizing & Forecasting

A top-down build begins with annual production of cellular capable devices, which are then filtered through eSIM penetration ratios obtained from primary calls. Parallel supplier roll-ups of eUICC wafer shipments provide a selective bottom-up check. Key variables in our model include global 5G handset share, average eSIM attach rate in new passenger cars, monthly consumer profile downloads, IoT module ASPs, and regional smartphone replacement cycles. Multivariate regression, complemented by scenario analysis for regulatory timing, projects each driver to 2030; gaps in device counts are bridged using three-year moving averages.

Data Validation & Update Cycle

Outputs pass an internal variance screener, after which senior reviewers challenge anomalies against third-party indices. Reports refresh every twelve months, with mid-cycle revisions when events such as a major OEM eSIM only launch materially shift baselines. Before publication, an analyst re-pulls the latest shipment datapoints so clients receive our freshest view.

Why Mordor's eSIM Market Baseline Earns Decision-Maker Trust

Published figures vary because firms choose different revenue buckets, profile update assumptions, and refresh cadences.

Key gap drivers include: some studies track only hardware chips, several apply a single global ASP that ignores regional mix, and a few forecast through 2032 without revisiting 5G handset adoption curves each year, unlike Mordor's annual reset.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.29 Bn (2025) | Mordor Intelligence | - |

| USD 1.46 Bn (2024) | Global Consultancy A | Counts smartphones only; excludes IoT, autos |

| USD 11.87 Bn (2025) | Regional Consultancy B | Uses uniform ASP; no profile service revenue |

| USD 11.93 Bn (2024) | Trade Journal C | Projects forward on 2021 device mix; limited refresh cadence |

This comparison shows that by selecting the right scope, blending hardware and service streams, and refreshing inputs yearly, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the projected volume of embedded SIM units by 2031?

Shipments are expected to reach 2.12 billion units by 2031, growing at a 26.27% CAGR from 2026 levels.

Which device category will post the fastest volume growth through 2031?

Wearables are forecast to expand at a 26.76% CAGR, outpacing smartphones, laptops, and tablets.

Why are automotive manufacturers rapidly adopting eSIM?

UN-R155 cybersecurity rules and eCall emergency requirements mandate tamper-resistant, always-connected modules, making embedded SIM the preferred solution.

How does SGP.32 differ from earlier provisioning standards?

SGP.32 unifies IoT remote provisioning, supports multi-operator interoperability, and lowers integration costs compared with legacy SGP.02 machine-to-machine frameworks.

Which regions will contribute most to new eSIM activations?

Asia Pacific will lead growth, driven by China’s nationwide rollout and India’s pan-regional launches, while North America and Europe sustain steady volume additions.

Page last updated on: