Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

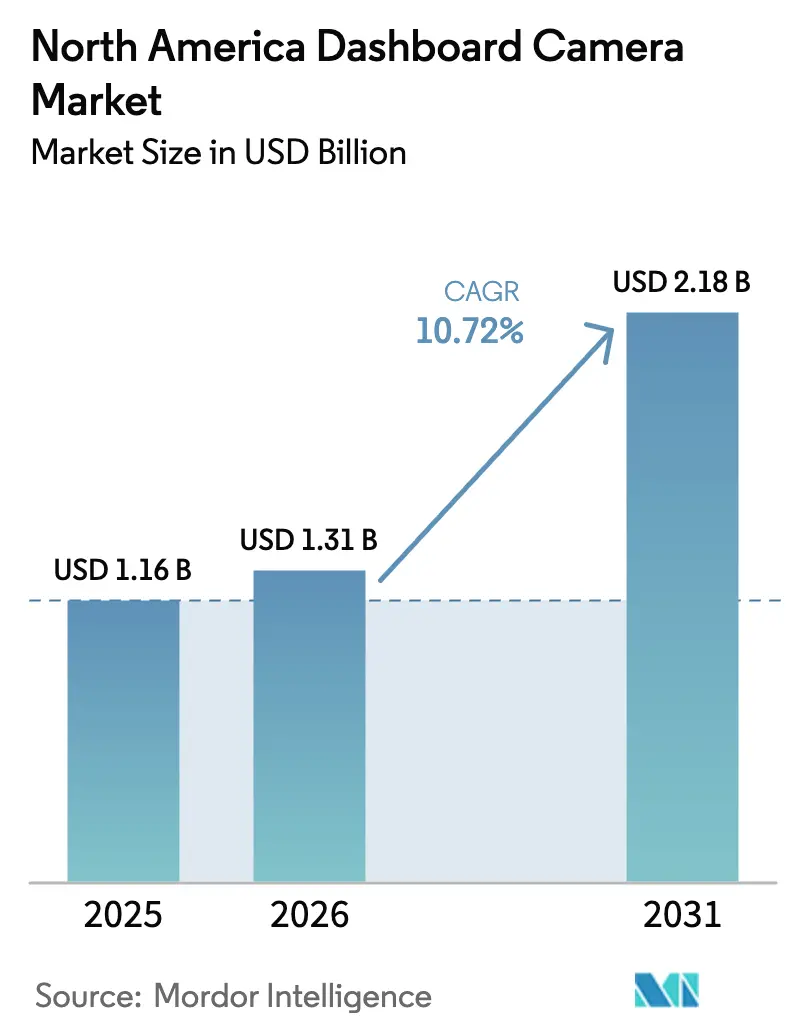

| Base Year Market Size (2025) | USD 1.16 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 10.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Dashboard Camera Market Analysis by Mordor Intelligence

The North America dashboard camera market size is projected to expand from USD 1.16 billion in 2025 and USD 1.31 billion in 2026 to USD 2.18 billion by 2031, registering a CAGR of 10.72% between 2026 to 2031. The growing judicial acceptance of video evidence, insurer telematics incentives, and the declining cost of edge-AI processors are accelerating replacement cycles, while regulatory pilots for autonomous delivery create new demand nodes. Smart devices that pair cloud video with artificial-intelligence event detection already dominate shipments, and subscription add-ons are giving vendors durable revenue beyond hardware margins. Although offline retailers still sell the majority of units, e-commerce platforms are gaining market share by bundling next-day delivery with cloud storage plans. Competitive pressure centers on cybersecurity assurance, as recent research exposed Wi-Fi vulnerabilities in more than twenty dash-cam models.

Key Report Takeaways

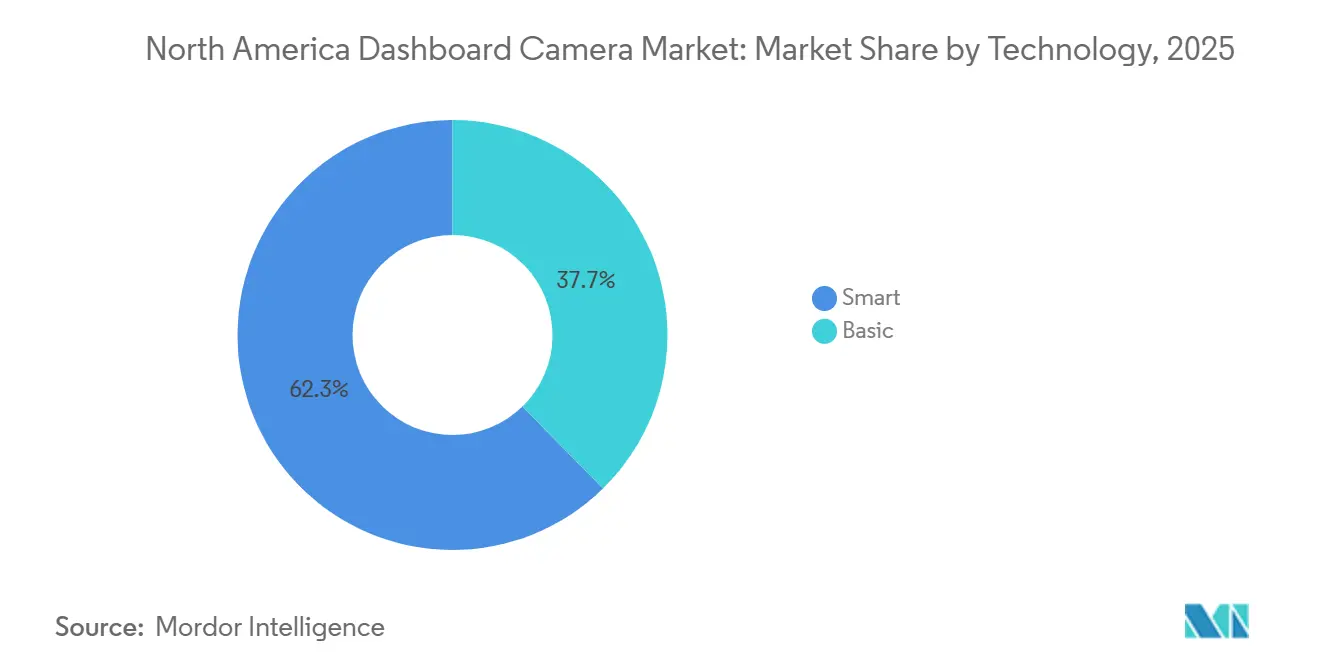

- By technology, smart dash cams are expected to lead with 62.34% of the North America dashboard camera market share in 2025, while basic units are forecast to grow at a 6.1% CAGR through 2031.

- By distribution channel, offline retail accounted for 73.49% of 2025 sales; online is projected to expand at an 11.19% CAGR through 2031.

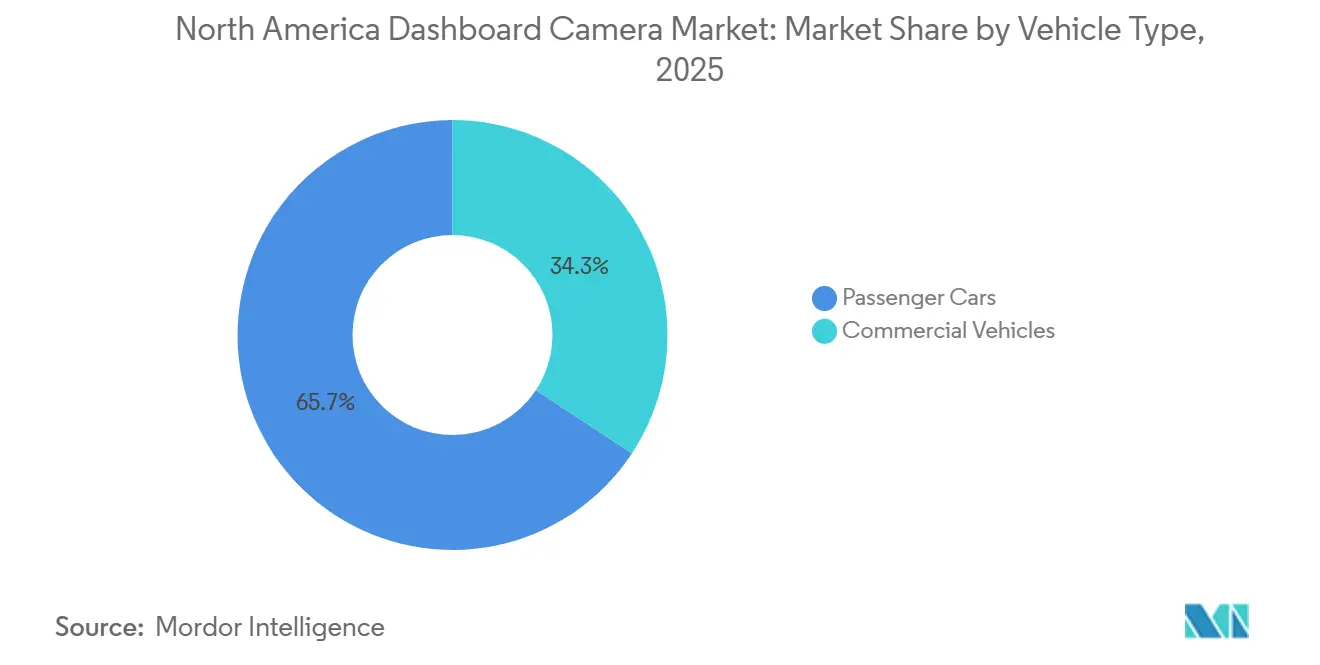

- By vehicle type, passenger cars accounted for 65.71% of shipments in 2025, while commercial vehicles are set to post an 11.15% CAGR through 2031.

- By resolution, HD (1080p) held a 48.19% share in 2025, and full HD and above are expected to grow fastest at an 11.51% CAGR.

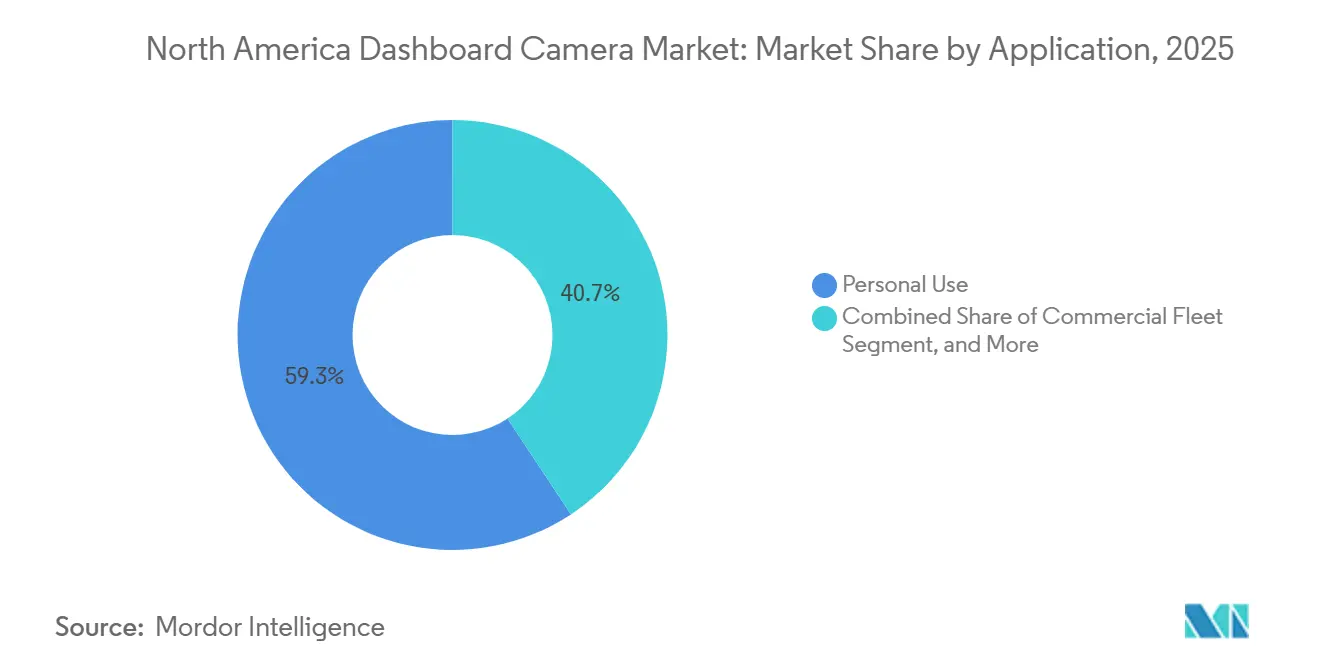

- By application, personal use contributed 59.28% of volumes in 2025; however, fleet deployments are forecast to advance at an 11.57% CAGR.

- By price range, mid-range units commanded 56.77% of the 2025 demand, whereas premium models above USD 200 are expected to rise at an 11.63% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Dashboard Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Emphasis on Driver Safety and Legal Evidence Acceptance | +2.1% | United States and Canada, spillover to Mexico logistics corridors | Medium term (2-4 years) |

| Technological Advancements in Smart and Connected Dash Cams | +2.4% | United States and Canada urban centers, expanding to suburbs | Long term (≥ 4 years) |

| Falling Dash Cam Prices Across Retail Channels | +1.3% | North America-wide, strongest in United States big-box retail | Short term (≤ 2 years) |

| Rising Online Retail Penetration for After-Market Accessories | +1.6% | United States e-commerce concentration, Canada following, Mexico nascent | Medium term (2-4 years) |

| Insurance Telematics Discounts for Dash Cam Users | +1.8% | United States and Canada, limited Mexico penetration | Medium term (2-4 years) |

| Autonomous Delivery Pilots Requiring Video Event Recorders | +1.5% | Ontario, California, Texas pilot zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Emphasis on Driver Safety and Legal Evidence Acceptance

Courts across the region are increasingly accepting dashcam footage, which cuts litigation timelines and settlement costs for insurers and fleets.[1]SambaSafety Research Team, “2024 Commercial Auto Insurance Report,” SambaSafety, sambasafety.com More than four in five commercial insurers now incorporate telematics data into their underwriting processes, and fleets that have used AI-enabled cameras for 30 months have seen a 73% reduction in crash rates. Connecticut’s 2025 requirement of a 90-day minimum retention and four-year archival period for disputed incidents establishes a template that other states are likely to replicate. Together, these factors recast the camera from a discretionary gadget to a standard risk-management tool.

Technological Advancements in Smart and Connected Dash Cams

Five-nanometer system-on-chip designs encode 4K60 video and run neural networks at under 2 watts, shrinking the cost difference between consumer and fleet-grade units.[2]Ambarella Newsroom, “Ambarella Unveils 5 nm AI SoCs,” Ambarella, ambarella.com Recent launches integrate drowsiness alerts, blind-spot detection, and live cloud sync into devices priced below USD 200. Voice control and continuous cloud backup, once premium perks, now appear in mid-range offerings, nudging buyers toward feature-rich subscriptions. Vendors that fuse video, GPS, and vehicle health data deliver deeper insights and retain customers longer.

Falling Dash Cam Prices Across Retail Channels

Volume deals with image-sensor suppliers, and rising competition among Asian contract manufacturers has trimmed bill-of-materials costs, allowing retailers to position 1080p units near the USD 80 threshold without eroding margins.[3]Amazon Listings Data, “AZDOME 3-Channel 4K Dashboard Camera,” amazon.com As smart features migrate to entry tiers, consumers perceive greater value, compressing upgrade cycles. Big-box chains leverage in-store installation and extended warranties to keep traffic, while online platforms offset thin hardware margins with paid cloud plans.

Rising Online Retail Penetration for Aftermarket Accessories

E-commerce bundles that pair hardware with subscription cloud storage lure first-time buyers by simplifying setup. Price-matching policies and free returns reduce perceived risk, while user reviews provide newcomers with confidence in the reliability. Mobile mechanics, by installing devices at customers' homes, have effectively closed the service gap that previously benefited physical stores. This approach not only enhances customer convenience but also eliminates the need for customers to visit physical locations, offering a competitive edge in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy Concerns and Data-Protection Regulations | -1.4% | California, Illinois, Texas leadership, Canada following | Medium term (2-4 years) |

| Lower Penetration versus Incentivized European Markets | -0.9% | United States and Canada, minimal Mexico effect | Long term (≥ 4 years) |

| CMOS Sensor Supply Constraints Limiting 4K Models | -1.2% | North America-wide, tied to Asia-Pacific supply | Short term (≤ 2 years) |

| Cyber-security Risks in Connected Dash Cams | -0.8% | United States and Canada connected-device markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Privacy Concerns and Data-Protection Regulations

California’s Senate Bill 296 requires automakers to obtain explicit consent and localize camera data, thereby increasing compliance costs and slowing factory installations. Illinois and Texas biometric-privacy statutes create uncertainty for vendors offering facial-recognition alerts, forcing firmware variations by state. Advocacy groups continue to press for uniform disclosure standards, and until a federal framework emerges, feature rollouts will remain staggered.

CMOS Sensor Supply Constraints Limiting 4K Models

Three companies control roughly 80% of the global CMOS sensor market, and recent freight disruptions have multiplied shipping rates by almost nine times, thereby inflating landed costs. United States tariffs added another 10-15% to component prices. In the U.S., a lone secure fabrication plant faces challenges meeting demand for premium 4K units, resulting in constrained supply. This limitation continues to drive higher production and availability of entry-level HD products, as manufacturers prioritize these segments to address market needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Smart Devices Embed Fleet-Grade Intelligence

Smart units captured a 62.34% share in 2025, supported by cloud video, AI event detection, and telematics integration. The North America dashboard camera market size for smart models is forecast to grow at an 11.13% CAGR through 2031 as buyers embrace subscription services that automate evidence uploads and enable live-view driver coaching. Recurring fees, such as a USD 9.99 monthly cloud plan, are recasting vendor economics toward software annuities. Nextbase’s 2025 acquisition of a machine-vision startup, which embedded pedestrian detection directly on the device, illustrates how software, not optics, now anchors differentiation.

Price erosion narrows the gap with basic cameras, eroding the latter’s appeal to budget consumers who back up footage locally. Fleet operators are drawn to cameras that integrate video with GPS and vehicle diagnostics, citing reductions in crash rates of up to 80%. Over time, edge-AI silicon will make smart capabilities standard even in entry-level segments, while basic cameras will retreat to niche roles, such as parking surveillance or serving as starter devices for first-time owners.

By Distribution Channel: E-Commerce Gains Despite Offline Dominance

Offline stores accounted for 73.49% of transactions in 2025, driven by on-site installations and immediate availability; however, online sales are expanding at an 11.19% CAGR. The North America dashboard camera market share for online channels benefits from next-day delivery and seamless cloud plan activation, which physical retailers struggle to match. Amazon’s best-seller lists regularly feature 3-channel 4K units at roughly USD 130, backed by tens of thousands of reviews that amplify trust.

Commercial fleets continue to rely on brick-and-mortar distributors for bulk procurement and warranty services. Insurer-led subsidy programs direct customers to certified installers, thereby increasing store traffic. In response, e-commerce players now partner with mobile technicians, narrowing the convenience gap. Even as the channel mix slowly pivots to online platforms, offline retail will maintain its dominance, bolstered by hands-on support, at least until the middle of the decade.

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars represented 65.71% of 2025 volumes; however, commercial vehicles are expected to post an 11.15% CAGR as insurers widen telematics discounts. The North America dashboard camera market size for fleets is expanding because video evidence cuts claim costs and satisfies hours-of-service audits. Some trucking firms report crash reductions of more than 70% after implementing AI cameras for two years. Multichannel designs that pair cab-facing and road-facing lenses are gaining popularity for coaching and fraud prevention.

Personal car adoption, which is highest in California and Texas, is driven by rising litigation risk. Original equipment installations, such as Tesla’s built-in dashcam suite, normalize the feature and reshape consumer expectations. Driven by surging e-commerce shipping volumes and regulatory trials for autonomous couriers, light commercial vans have emerged as a rapidly expanding subsegment in parcel delivery. The increasing demand for faster and more efficient last-mile delivery solutions, coupled with advancements in autonomous vehicle technology, is further fueling growth in this segment.

By Resolution: 4K Adoption Hinges on Sensor Supply

HD 1080p units led with a 48.19% share in 2025, striking a balance between clarity and manageable file size. Full HD and 4K models are expected to expand at an 11.51% CAGR, but the North America dashboard camera market share for 4K remains capped until sensor shortages are alleviated. New 5-nanometer chips encode 4K60 video at low power, enabling extended parking-mode recording. Garmin’s USD 399 premium model pairs 4K optics with a polarizer lens that cuts windshield glare.

Tariffs and freight shocks have driven up the prices of low-end components, prompting several brands to discontinue sub-720p units. Despite clear forensic advantages, the sole domestic image-sensor fab's supply risks keep 4K devices priced out of mainstream budgets. This pricing challenge continues to delay their widespread adoption, as affordability remains a critical factor for mass-market penetration.

By Application: Fleet Deployments Outpace Personal Use

Personal use accounted for 59.28% of 2025 demand; however, fleet deployments are expected to surge at an 11.57% CAGR as insurers subsidize hardware and regulators mandate event data recorders for autonomous pilots. The North America dashboard camera market size for commercial fleets gains from projected USD 10 billion video-telematics revenue by 2030. Fleet managers increasingly require continuous video as part of integrated safety platforms that rank drivers and automate training interventions.

Rideshare and delivery drivers blur the line between personal and commercial categories, opting for dual-facing cameras that deter false claims. Law-enforcement uptake is modest as agencies prioritize body-worn cameras, but emerging state archival rules could revive police demand. Over the forecast horizon, fleets, light commercial vehicles, and gig-economy operators will collectively gradually surpass those used for purely personal purposes.

By Price Range: Premium Segment Gains on Subscription Models

Mid-range units, priced between USD 100 and USD 200, held a 56.77% share in 2025. Premium models priced above USD 200 are expected to grow at an 11.63% CAGR, as enterprises value dual lenses, cellular connectivity, and bundled multi-year cloud storage. The North America dashboard camera market size for premium gear benefits from insurer subsidies that offset purchase prices, effectively shifting cost to subscription services. A single fleet can recoup camera outlay within a year via lower deductibles, reinforcing willingness to spend.

Economic units under USD 100 still attract first-time users but face shrinking margins after tariffs raised component costs. Vendors reposition these models as entry points into larger ecosystems, offering discounted upgrades to cloud plans that smooth revenue volatility. In the future, premium and mid-range devices are set to take the lead, capturing a significant share of the market. This shift is expected to push economy devices into a narrower budget niche, catering primarily to cost-conscious consumers or specific use cases.

Geography Analysis

The United States anchors demand, buoyed by high vehicle ownership, frequent litigation, and state mandates that standardize video retention. California’s privacy law adds compliance cost for factory-installed cameras but leaves aftermarket devices largely untouched, sustaining retail sales. Factory integration, exemplified by GM’s dual-lens system, raises consumer expectations and speeds diffusion. Texas and Florida follow with strong uptake due to dense traffic and no-fault insurance rules.

Canada contributes to outsize fleet growth, thanks in part to insurer telematics discounts and harsh winter driving conditions. Programs offering up to 15% policy savings encourage operators to install AI-enabled cameras. Ontario’s autonomous-vehicle pilot, which is expected to run into the next decade, requires comprehensive video archives, thereby cultivating a parallel demand stream. Domestic telematics providers leverage proximity to fleet customers, shortening service cycles and deepening integration.

Mexico remains a nascent yet strategic market, as cross-border logistics carriers add cameras to comply with U.S. e-Manifest rules. Urban theft concerns in Mexico City also increase demand for personal cars. Currency fluctuations and lower average vehicle prices temper premium adoption, yet discounted hardware bundles tailored for logistics corridors are closing the gap. Over the forecast, the region’s sales mix will remain United States-centric, but Canadian fleet demand and Mexican logistics upgrades will narrow the share disparity.

Regulatory Landscape

North American dashboard camera adoption operates under a patchwork of vehicle-equipment, motor-carrier, and privacy rules rather than a single dashcam-specific federal standard. In the United States, NHTSA does not certify retail dash cameras and has not issued a dedicated FMVSS for them, while it continues research on camera-based visibility systems as alternatives to mirrors (RIN 2127-AM02).

Value Chain Analysis

The value chain spans image sensors, optics, memory, and AI-capable system-on-chip platforms, followed by camera module assembly, firmware/AI feature integration, distribution, installation, and ongoing cloud video storage and analytics. North America remains strongest in upstream design, software, and semiconductor platforms (for example, Ambarella, Qualcomm, and Mobileye-linked ecosystems), while most finished dashcam assembly is concentrated in Asia, with limited U.S. finished-goods manufacturing and more activity in final integration, firmware loading, QA, and support for fleet-grade deployments.

Downstream, consumer sales flow through big-box and specialty retailers and increasingly e-commerce, while fleets source through telematics and safety-platform integrators that bundle hardware with subscriptions, installation, and claims-support workflows. Key fleet-stack integrators such as Samsara, Lytx, Motive, and Netradyne anchor demand through video telematics and coaching software, while OEM embedding is emerging as an adjacent channel that can shift volumes away from aftermarket entry tiers. The chain is sensitive to component availability and landed cost (CMOS sensors and connectivity modules) and to compliance-driven localization and privacy requirements that create firmware variants and data-handling obligations across states and provinces.

Competitive Landscape

Market structure is moderately concentrated. Consumer-electronics leaders Garmin, Nextbase, and Thinkware dominate retail shelves, while Samsara, Lytx, and Netradyne control fleet telematics by embedding cameras into broader safety stacks. Consolidation continues: Gentex agreed to acquire VOXX International, adding to its automotive electronics scale, and Nextbase bought a computer-vision startup to hardwire AI differentiation. Investors validate the video-telematics thesis, as Netradyne raised USD 90 million at a USD 1.35 billion valuation.

Factory-installed solutions show rising momentum. Tesla’s standard multi-camera suite and GM’s dealer-installed dual-lens option illustrate OEM appetite for subscription revenue streams. Yet California’s consent requirements slow broader OEM rollouts, preserving room for aftermarket innovators. Cybersecurity emerges as a key battleground after researchers exploited Wi-Fi vulnerabilities in minutes on multiple models. Vendors that certify encrypted firmware and secure boot processes are gaining enterprise preference, while brands that are slow to patch security gaps risk a rapid decline in market share.

White-label manufacturers still supply economy tiers, but tariff headwinds and brand trust issues restrain their advance. Mid-range and premium segments differentiate through AI-powered analytics, 4K optics, and cloud integration, keeping price competition in check. With the rise in subscription uptake, hardware margins are set to compress, underscoring the growing significance of ecosystem lock-in and customer lifetime value.

North America Dashboard Camera Industry Leaders

Garmin Ltd

Thinkware Corporation

LG Innotek

Panasonic Corporation

Harman International Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial fleets present a clear whitespace where regulation and insurance models formalize the value of video evidence and telematics. British Columbia's Dashboard Cameras in Commercial Vehicles Act (Bill M 217-2025) provides a concrete template for outward-facing camera specs in heavy vehicles over 11,793 kg GVWR, standardizing continuous recording, retention windows, and night-vision features across a major Canadian jurisdiction. In the United States, FMCSA's acceptance of dashcam footage within the Crash Preventability Determination Program expands how video records can be used in safety determinations, shaping demand for secure storage and retrieval of footage.

Opportunities concentrate around subscription-centric smart cameras and integrated telematics bundles that extend beyond device sales into cloud storage, AI event detection, and coaching workflows. State-level programs tying insurance pricing to telematics and camera adoption create room for targeted offerings to mid-sized fleets and owner-operators across cross-border corridors, while ongoing privacy and cybersecurity scrutiny creates product space for encrypted firmware, secure boot, and region-appropriate data handling that keeps total cost of ownership competitive.

Recent Industry Developments

- May 2026: Netradyne announced a major North American capacity expansion to support its fleet safety platform, adding new data center capacity and expanded integrations with partner telematics providers. The expansion strengthens its position in enterprise video telematics and accelerates data processing for video evidence workflows.

- November 2025: Thinkware introduced the ARC 900 dash cam with dual Sony STARVIS 2 sensors, 4K/60fps front recording, and Wi-Fi 6 connectivity, expanding premium connected camera offerings and cloud workflow support.

- September 2024: Garmin launched the Dash Cam X series including Mini 3, X110, X210, and X310, extending its lineup with 4K Ultra HD capture and Clarity lens technology, reinforcing premiumization in consumer channels and emphasizing optics and processing for evidence-quality footage.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from dashboard cameras (dash cams) sold for in-vehicle video recording across the United States, Canada, and Mexico, including consumer and fleet use where the device is purchased for installation in a vehicle.

Scope exclusions: It excludes factory-integrated ADAS camera modules, rear view cameras sold as part of parking systems, and standalone video management services that are not bundled with a dash cam device sale.

Segmentation Overview

- By Technology

- Basic

- Smart

- By Distribution Channel

- Offline

- Online

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- By Resolution

- SD (Below 720p)

- HD (1080p)

- Full HD and Above

- By Application

- Personal Use

- Commercial Fleet

- Law Enforcement

- By Price Range

- Economy (Below USD 100)

- Mid-Range (USD 100–200)

- Premium (Above USD 200)

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand and supply context for dash cams in North America, and then lining it up to what can be observed in public data series. We reference sources such as US DOT and NHTSA publications on road safety and crash trends, Statistics Canada transport indicators, and Mexico transport statistics where available, since these help explain adoption drivers for evidence capture.

We also use materials such as US International Trade Commission data, customs import and export statistics, and patent databases to understand how product features and sourcing patterns are shifting (for example, resolution steps, connectivity, and basic AI features). Company filings, investor presentations, product catalogs, and reputable press were reviewed to build a realistic view on pricing ladders and channel mix, and we used paid subscriptions for company financials and shipment-level import and export checks to cross-verify. These sources are illustrative, and many other public and proprietary references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary conversations were used to pressure-test the desk assumptions that most often move the number, especially average selling price progression, channel discounting, and attach rates by passenger versus commercial vehicles. We spoke with stakeholders across device brands, distributors and retailers, fleet-focused resellers, and end users, and we kept coverage balanced across the United States, Canada, and Mexico so regional pricing constraints and compliance needs did not get averaged out too early.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | |

| Mid tier: 50% | Functional/Unit leaders: 31% | |

| Smaller Players: 15% | Managers: 55% |

Market-Sizing & Forecasting

The core sizing uses a top-down approach where vehicle parc, new vehicle sales, and estimated dash cam penetration are used to reconstruct an addressable demand pool for each country, which is then translated into value using observed price bands. To keep the output realistic, selective bottom-up checks are added using channel checks, sampled unit volumes by category, and an ASP times volume bridge across basic and smart devices.

Inputs that typically matter include passenger car versus commercial vehicle mix, fleet adoption triggers tied to safety policies, the share of online versus offline sales, resolution and connectivity shifts that move ASP, and replacement cycles driven by device failures or feature upgrades. Forecasts are built using scenario analysis with a simple regression layer on the main demand indicators, and then the future path is adjusted based on expert views on pricing pressure, feature premium durability, and expected policy or insurance nudges. Where unit information is incomplete for smaller channels, gaps are filled with conservative ranges and then tightened through interview feedback before being accepted.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between the model output and independent signals such as trade flows, observable price points, and the implied units required to support the value totals. Outliers are reviewed, assumptions are rechecked, and follow-up calls are triggered when a key input changes the result beyond a practical tolerance.

A multi-step internal review is completed before sign-off, and the report is refreshed annually with interim updates when material events occur, such as sharp currency moves, abrupt pricing resets, or policy shifts affecting fleet procurement. Before delivery, a final analyst pass is performed so the published view reflects the latest available data and confirmed assumptions.

Mordor Intelligence's North America Dashboard Camera Market Size Compared With Other Published Estimates

Published market sizes for North America dash cams often do not match, even when the topic sounds identical. The differences usually come from timing choices, how average selling price is treated across price bands, and whether the definition stays limited to dashboard camera devices or expands into adjacent in-vehicle camera categories.

In this study, the refresh timing is treated as a real input because currency conversion windows, promo-heavy retail months, and feature-driven ASP jumps can shift annual value noticeably, which is then validated through repeated channel price checks and fleet purchasing feedback, and this is where Mordor Intelligence lands at a different level than some other published figures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.16 B (2025) | |

| Industry Databook A | USD 0.81 B (2023) | Uses an earlier base year and a shorter outlook, and its revenue capture appears more consumer-weighted, which can undercount higher ASP fleet and law enforcement demand and later smart-device mix shifts. |

| Trade Publisher B | USD 0.53 B (2024) | Uses a narrower interpretation closer to automotive dashboard camera units, with limited clarity on channel coverage and pricing bands, which can compress ASP and exclude parts of the aftermarket dash cam value sold through retail and online. |

Looking across the three figures, the spread is mainly explained by base year choice and how pricing ladders are updated as smart features move from premium to mid-range. Our approach stays traceable because each step is tied back to vehicle demand indicators, country-level adoption logic, and observable price points that can be rechecked when conditions change.

Key Questions Answered in the Report

How large is the North America dashboard camera market in 2026?

It reached USD 1.31 billion and is forecast to grow toward USD 2.18 billion by 2031.

Which dashboard camera technology leads regional sales?

Smart, cloud-connected units held 62.34% of 2025 revenue and continue to outpace basic models.

What is driving commercial-fleet adoption of dash cams?

Insurer premium discounts, regulatory data-logging mandates, and documented crash-rate reductions motivate fleets to install AI-enabled cameras.

Are 4K dashboard cameras gaining traction?

Yes, full HD and 4K models are the fastest-growing resolution segment, though sensor shortages keep prices elevated.

How are privacy regulations affecting factory-installed cameras?

State laws such as California’s Senate Bill 296 mandate explicit consent and data localization, slowing OEM rollouts while leaving aftermarket devices less affected.

Which retailers are capturing online dash-cam demand?

E-commerce leaders like Amazon and other major online marketplaces drive growth by bundling next-day delivery with cloud-storage subscriptions.

Page last updated on: