Market Overview

| Study Period | 2021 - 2031 |

|---|---|

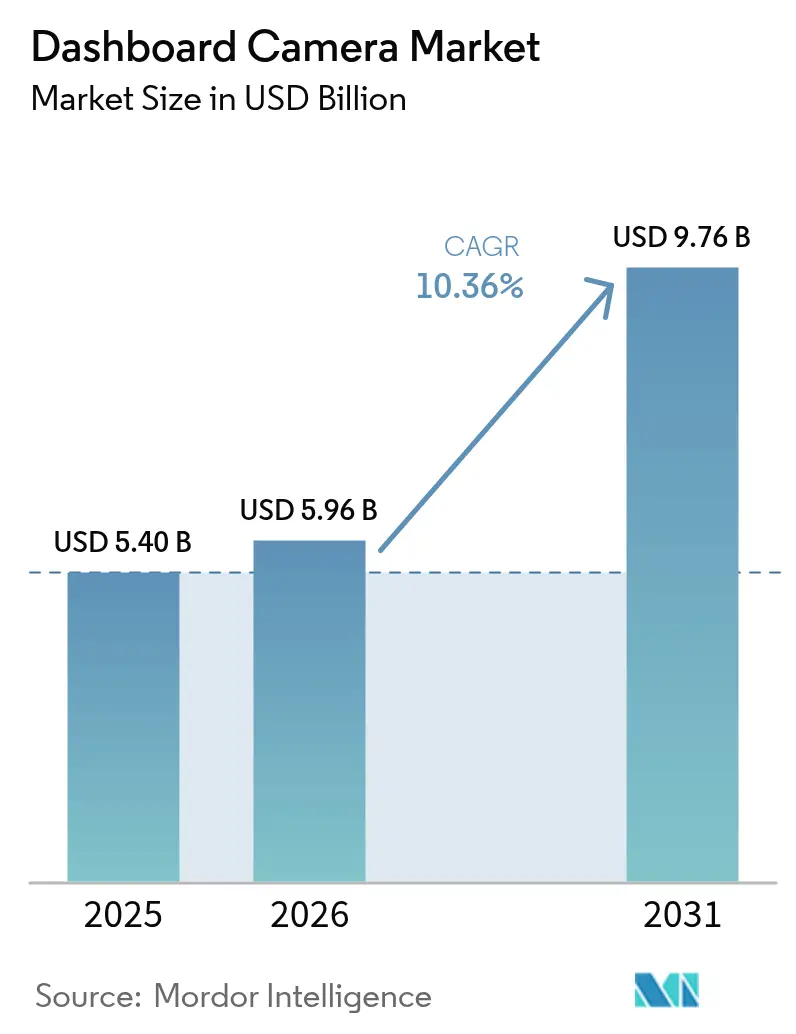

| Market Size (2026) | USD 5.96 Billion |

| Market Size (2031) | USD 9.76 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

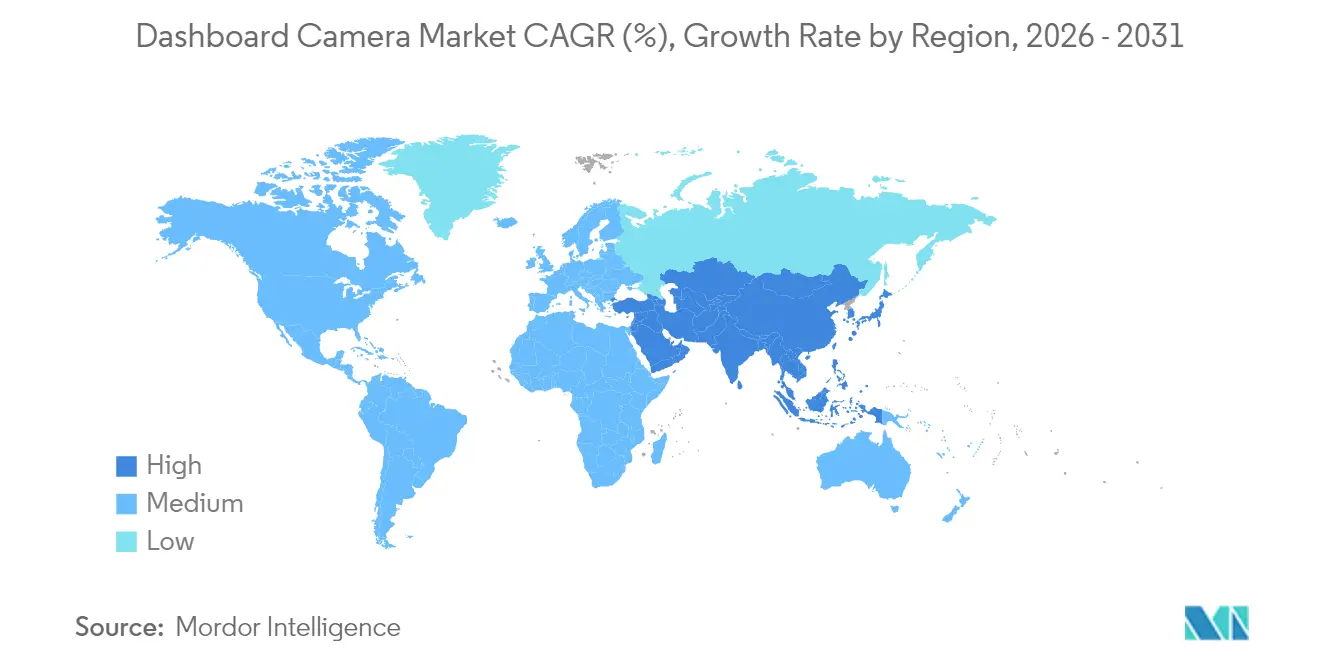

| Fastest Growing Market | Asia |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dashboard Camera Market Analysis by Mordor Intelligence

The dashboard camera market size was valued at USD 5.40 billion in 2025 and estimated to grow from USD 5.96 billion in 2026 to reach USD 9.76 billion by 2031, at a CAGR of 10.36% during the forecast period (2026-2031). This expansion stems from compulsory in-vehicle data recorders in Europe, expanding insurance telematics programs in North America, and rapid AI integration that raises perceived value among fleet operators. Europe’s firm regulatory stance has positioned factory-fit units as the new norm, while Asia’s thriving automotive production base and telematics-friendly insurers underpin the fastest regional growth momentum. Technological differentiation has pivoted from hardware to software; cloud-connected analytics, GDPR-compliant storage, and heat-resistant designs now determine brand preference. Competition is intensifying as aftermarket specialists, fleet telematics vendors, and OEMs converge on the same connected-video opportunity, prompting new partnerships and white-label supply models.

Key Report Takeaways

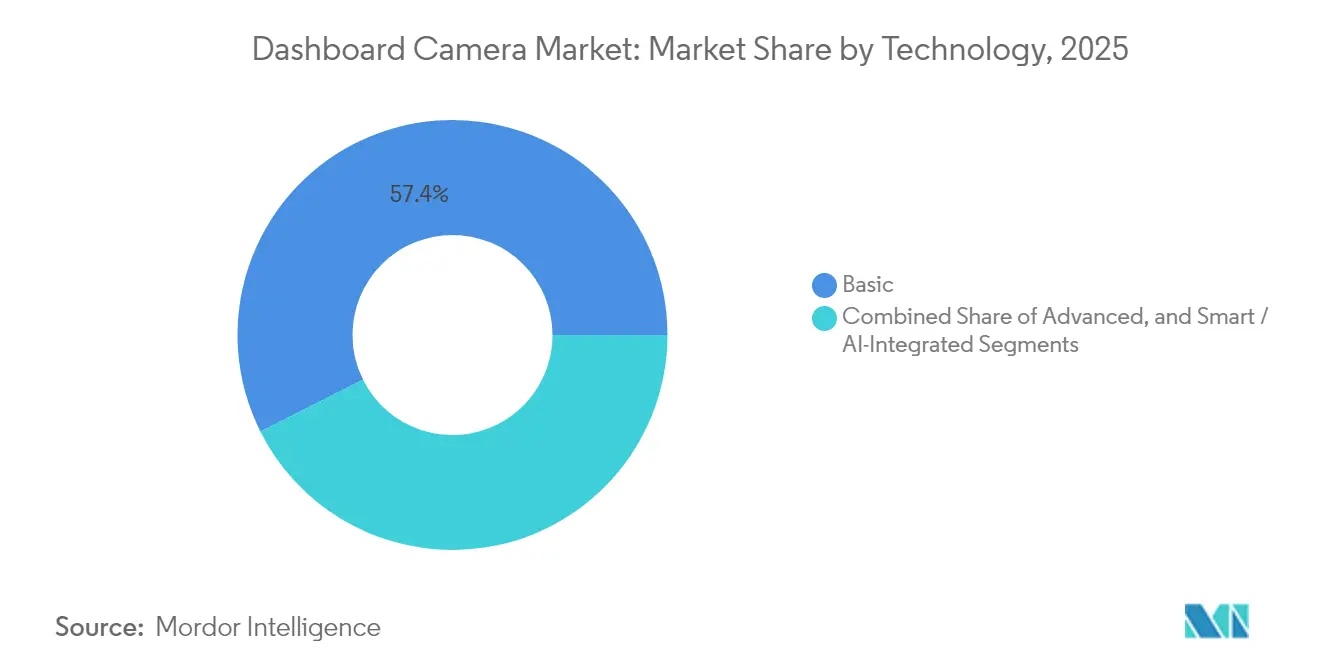

- By technology, basic models retained 57.40% of the dashboard camera market share in 2025; smart/AI-integrated units are projected to expand at a 11.83% CAGR to 2031.

- By product architecture, single-channel systems led with 71.30% revenue share in 2025, whereas dual-channel configurations are growing at 10.78% CAGR through 2031.

- By video quality, SD and HD accounted for 60.20% of the dashboard camera market size in 2025; 4K/UHD formats are advancing at a 12.74% CAGR.

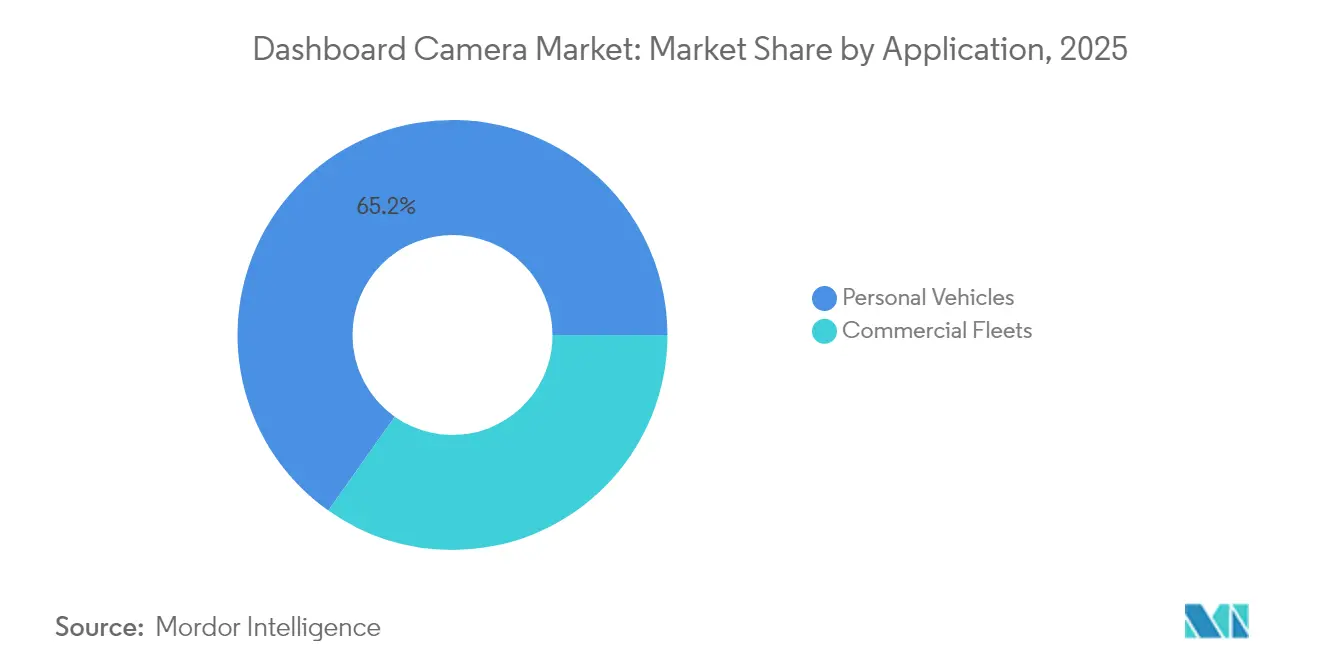

- By application, personal vehicles represented 65.20% of the dashboard camera market size in 2025, while commercial fleets exhibit the highest projected CAGR at 10.92% to 2031.

- By distribution channel, in-store retail held 59.10% share in 2025; online sales are rising at 11.60% CAGR.

- By geography, Europe commanded 34.60% share in 2025; Asia is the fastest-growing region with an 11.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dashboard Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European eCall-Event Data Recorder Mandate Driving Factory-Fit Dashcams | +2.10% | Europe, spill-over to North America | Short term (≤ 2 years) |

| AI-Enabled Fleet Video Telematics Adoption in US and UK Logistics | +1.80% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| OEM-Installed Dashcams by Tesla, BMW and Hyundai Accelerating APAC Uptake | +1.50% | APAC core, spill-over to global markets | Medium term (2-4 years) |

| Insurance Telematics Discounts in Canada and South Korea | +1.20% | North America and APAC, selective EU adoption | Long term (≥ 4 years) |

| Government Commercial Fleet Video Evidence Regulation (e.g. India 2026 Regulation) | +0.90% | India, expanding to Southeast Asia | Long term (≥ 4 years) |

| Insurer-driven 4K/UHD video-quality adoption for claim clarity | +0.60% | Global commercial fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

European eCall-Event Data Recorder mandate driving factory-fit dashcams

The July 2024 regulation obliges every new passenger vehicle in the EU to store crash-related data, making video capture a logical extension that OEMs are embedding at the production line [1]European Commission, “Mandatory drivers assistance systems expected to help save over 25,000 lives by 2038,” single-market-economy.ec.europa.eu . Manufacturers gain a compliance differentiator, suppliers secure long-term platform volume, and aftermarket brands must pivot toward dealer accessories and fleet retrofits. German Tier-1 electronics firms have moved quickly with GDPR-ready firmware and encrypted storage, giving them an edge as global platforms export EU-validated technology to other markets.

AI-enabled fleet video telematics adoption in US and UK logistics

Large carriers have transitioned from incident review to predictive coaching. AI analytics automatically flag tail-gating, distraction, or fatigue, enabling safety managers to intervene early, cut claims, and negotiate lower premiums [2]FleetOwner, “How fleets are leveraging AI to boost operations,” fleetowner.com . Scalable cloud review reduces manual footage trawling and makes enterprise deployments feasible across thousands of tractors and vans. Vendors that own proprietary computer-vision stacks now command strategic partnerships with telematics integrators eager for video-first differentiation.

OEM-installed dashcams by global automakers accelerating APAC uptake

Mainstream brands are standardizing integrated dashcams on high-trim variants, bundling over-the-air upgrades that improve features post-sale. The strategy secures subscription revenue for cloud storage, limits aftermarket cannibalization, and heightens customer loyalty. Asian consumers, accustomed to factory infotainment and ADAS packages, are particularly receptive, pushing regional suppliers into white-label manufacturing for vehicle platforms launching from 2025.

Insurance telematics discounts in Canada and selected APAC markets

Usage-based insurers are rolling out 5-10% premium reductions for vehicles equipped with certified video units. Canadian pilots show lower fraud incidence and quicker claim settlement when footage is available, encouraging wider carrier adoption. The incentive underscores a cost–benefit narrative that accelerates household uptake beyond core tech-savvy drivers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven Recording Restrictions in Germany and Austria | -1.40% | Europe, potential expansion to other privacy-focused regions | Short term (≤ 2 years) |

| Cyber-Vulnerability Disclosures in Connected Dashcams | -1.10% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Heat-Induced Device Failures (e.g., Middle-East >15% RMA) | -0.80% | Middle East and Africa, expanding to other hot climates | Medium term (2-4 years) |

| Installation complexity and privacy hesitancy for dual/in-cabin cameras | -0.50% | Global retail consumers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GDPR-driven recording restrictions in Germany and Austria

Loop recording, anonymization, and minimal retention periods are compulsory, raising firmware complexity and cost. The Austrian traffic authority enforces fines up to EUR 20 million (USD 21.8 million) for non-compliance. Legal clarity improved after Germany’s Federal Court allowed dashcam evidence in lawsuits, but hardware vendors still need region-specific SKUs, eroding economies of scale.

Heat-induced device failures in Middle East markets

Ambient temperatures above 50°C accelerate component ageing; failure rates in pilot studies have topped 15%. Firms now design heat-dissipating housings, higher-temperature NAND, and capacitor-based power backups, yet these add material cost and delay feature parity with temperate-climate models. Fleets in the Gulf countries defer deployment until proven ruggedized solutions reach scale, moderating near-term volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: AI migration redefines product value

Basic dashcam technology retained the largest 57.40% market share in 2025, while smart/AI-integrated units register the fastest 11.83% CAGR through 2031. Smart models convert video into coaching alerts, helping fleets cut claims and negotiate lower premiums. Personal users still buy basic units for cost-effective evidence, yet upscale buyers increasingly choose app-linked devices with cloud uploads. Suppliers that control computer-vision IP secure recurring subscription revenue, buffering hardware commoditization within the dashboard camera market.

Concurrently, insurers cite AI-generated risk profiles when negotiating premiums, reinforcing demand from both carriers and self-insured corporates. Personal vehicle owners remain price-focused, yet upscale buyers gravitate to app-enhanced devices offering emergency upload and remote-viewing peace of mind. As over-the-air updates become commonplace, firmware road-maps rather than optics will anchor brand stickiness within the dashboard camera market.

By Product Architecture: dual-channel momentum in liability-sensitive fleets

Single-channel designs led with 71.30% revenue share in 2025, but dual-channel systems are growing at an 10.78% CAGR on the strength of fleet demand for forward-plus-cabin evidence. Logistics firms report 30% faster dispute resolution when interior footage is available, validating higher capital spend. Ride-hailing drivers and parents form a niche retail audience for multi-view kits, whereas OEMs integrate existing park-assist sensors to trigger selective cabin recording, merging privacy compliance with expanded coverage.

Consumer adoption of rear-plus-cabin views is slower; installation complexity and privacy hesitancy dampen uptake. Nonetheless, ride-hailing drivers and parents are niche segments willing to pay for 360° coverage. OEMs are experimenting with leveraging existing park-assist sensors to trigger selective interior recording, blending safety with privacy compliance.

By Video Quality: 4K becomes the fleet evidence benchmark

SD and HD formats held the largest 60.20% share of shipments in 2025, yet 4K/UHD units post the top 12.74% CAGR as insurers stipulate high-resolution proof for plate legibility. Falling storage costs and better compression unlock broader adoption, though higher bit-rates still strain mobile data budgets. Vendors add AI frame selection that discards redundant scenery to keep file sizes manageable while meeting evidentiary standards.

Yet, higher bit-rates strain mobile data budgets. Providers now bundle AI compression that retains evidentiary frames, discarding redundant scenery to halve file sizes. Regulatory bodies may codify minimum resolution requirements, mirroring aircraft black-box standards, further institutionalizing 4K as the commercial default.

By Application: fleet telematics unlocks enterprise ROI

Personal vehicles accounted for the greatest 65.20% share of units in 2025, whereas commercial fleets deliver the steepest 10.92% CAGR to 2031. Carriers integrate video with ELD data to diagnose root causes of accidents and fuel waste, merging safety with efficiency. India’s 2026 ADAS rule accelerates multi-camera demand in heavy trucks . Passenger-car growth steadies as early adopters saturate, but insurer rebates could extend penetration to mainstream drivers.

Personal vehicle penetration remains a volume bulwark, lifted by word-of-mouth sharing of incident exonerations. Subsidies from insurers and ride-share platforms could nudge uptake further, though the growth curve flattens after early-adopter saturation. Long replacement cycles in passenger cars maintain steady but modest refresh demand.

By Distribution Channel: e-commerce scales direct engagement

In-store retail captured the leading 59.10% share in 2025, but online sales expand at a 11.60% CAGR as brands bundle cloud storage and firmware updates at checkout. Physical outlets retain relevance through professional installation services and same-day swaps. Hybrid click-and-collect models combine digital discovery with local fitment, ensuring broad reach across distinct buyer personas in the evolving dashboard camera market.

Subscription renewals, firmware updates, and accessories like thermal housings generate continuous online interactions post-sale. Traditional car-audio shops diversify into fleet retrofits, leveraging installation expertise to offset traffic lost to virtual storefronts. This omnichannel convergence ensures broad reach across divergent buyer personas in the dashboard camera market.

Geography Analysis

Europe led with 34.60% share in 2025, anchored by the eCall-Event Data Recorder mandate that institutionalized video evidence. Northern markets exhibit above-average attach rates as insurers embrace footage for claims triage. Privacy safeguards such as automatic face blurring are now baseline specifications, adding development complexity yet raising consumer trust.

Asia posts the fastest 11.25% CAGR to 2031. China benefits from scale manufacturing economies and municipal smart-city grants that endorse connected cameras. South Korea’s insurers offer structured telematics credits, accelerating household adoption. India’s 2026 commercial ADAS requirement positions the country as a major demand catalyst; localized suppliers already pilot rugged units tuned for monsoon humidity under guidelines from the Ministry of Road Transport and Highways.

North America shows robust fleet momentum. Carriers integrate video with existing ELD and route-optimization stacks, while progressive insurers and risk-management pools endorse camera evidence to curb litigation costs. Extreme-heat regions of the Southwest, alongside Middle-Eastern and African climates, remain constrained by hardware reliability issues; vendors investing in thermal-resistant designs stand to unlock latent potential as validated field data emerges.

Competitive Landscape

The field remains moderately fragmented: the top five vendors collectively command under 35% revenue, giving new entrants headroom. Garmin and Thinkware capitalise on brand equity and installed service networks. Fleet-centric vision-analytics specialists partner with telematics majors to penetrate enterprise accounts. Component makers such as Gentex leverage automotive OEM relationships to embed cameras into mirror assemblies, shifting revenue upstream.

Strategic thrusts cluster around three themes. First, AI algorithm ownership becomes a moat as inference accuracy drives insurance acceptance. Second, cloud ecosystems convert one-time hardware sales into recurring revenue; companies now quote annualised run-rate metrics to investors. Third, region-specific compliance solutions—from GDPR filters to desert-grade cooling—create defensible niches. M&A activity is set to rise as firms seek end-to-end stacks spanning optics, silicon, and SaaS in the expanding dashboard camera market.

Dashboard Camera Industry Leaders

Garmin Ltd

Nextbase Ltd.

Thinkware Corporation

Panasonic Corporation

Xiaomi Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Gentex launched a next-generation HomeLink platform that links in-vehicle systems to smart-home devices, signaling intent to position dashcams as nodes within wider IoT ecosystems.

- January 2025: Garmin unveiled the Dash Cam X series, targeting professional evidence capture with premium optics, reinforcing its shift toward high-margin fleet and enthusiast segments.

- December 2024: Vueroid announced the S1 Infinite 4K model with AI-powered license-plate restoration, illustrating a premium-tier feature race among challenger brands.

- July 2024: The EU formally enforced Event Data Recorder rules across all new cars, cementing the regulatory pathway for integrated dashcam adoption.

Global Dashboard Camera Market Report Scope

The Global Dashboard Camera Market is segmented by Technology (Basic, Smart), Product Type (Single-channel, Dual-channel, Rear-view), and Geography. Dashboard cameras are onboard cameras that continuously record the view through a vehicle's front windscreen and sometimes rear or other windows. The essential benefits of vehicle dashboard cameras are their accident recording capabilities. They help to capture vehicle collations on video, which ensures that there is always a witness around. Dashcams are also placed on truck dashboards, which help to record front-facing videos.

By Technology

| Basic |

| Advanced |

| Smart / AI-Integrated |

By Product Type

| Single-Channel |

| Dual-Channel |

| Rear-View/Surround |

By Video Quality

| SD and HD |

| Full-HD |

| 4K / UHD |

By Application

| Personal Vehicles |

| Commercial Fleets |

By Distribution Channel

| In-store |

| Online |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Sweden, Norway, Denmark, Finland) | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Malaysia, Vietnam, Philippines) | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Basic | ||

| Advanced | |||

| Smart / AI-Integrated | |||

| By Product Type | Single-Channel | ||

| Dual-Channel | |||

| Rear-View/Surround | |||

| By Video Quality | SD and HD | ||

| Full-HD | |||

| 4K / UHD | |||

| By Application | Personal Vehicles | ||

| Commercial Fleets | |||

| By Distribution Channel | In-store | ||

| Online | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics (Sweden, Norway, Denmark, Finland) | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN (Indonesia, Thailand, Malaysia, Vietnam, Philippines) | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the dashboard camera market?

The dashboard camera market is valued at USD 5.96 billion in 2026.

How fast is the dashboard camera market expected to grow?

The market is forecast to expand at a 10.36% CAGR, reaching USD 9.76 billion by 2031.

Which region is growing the fastest?

Asia is projected to advance at an 11.25% CAGR through 2031, driven by expanding vehicle production and supportive insurance programs.

Why are fleets adopting AI-enabled dashcams?

AI analytics cut review time, flag risky behaviour in real time, and enable insurers to offer premium reductions, delivering measurable ROI.

Page last updated on: