North America Contract Research Organization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

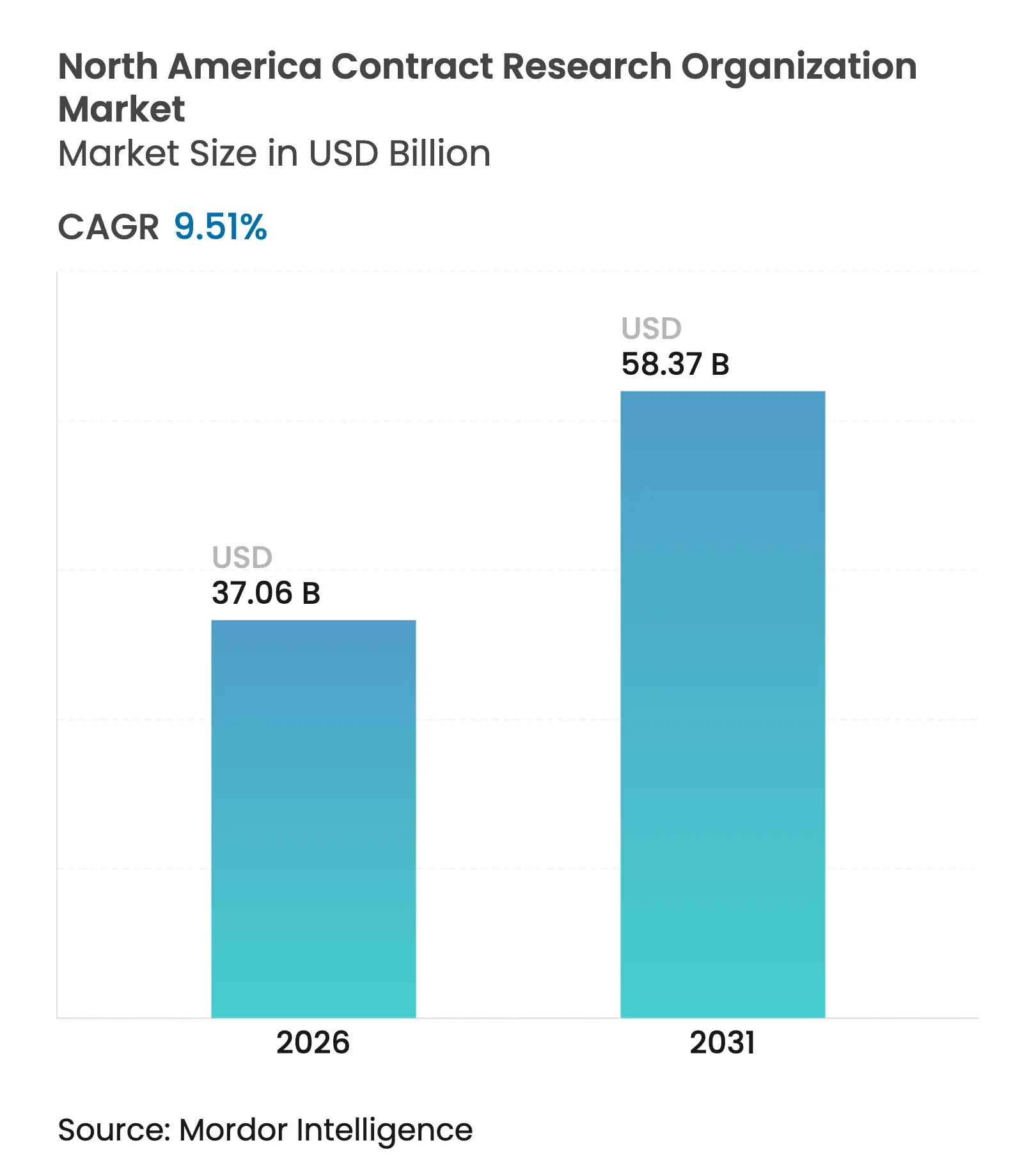

| Market Size (2026) | USD 37.06 Billion |

| Market Size (2031) | USD 58.37 Billion |

| Growth Rate (2026 - 2031) | 9.51 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Contract Research Organization Market Analysis by Mordor Intelligence

The North America Contract Research Organization Market size in 2026 is estimated at USD 37.06 billion, growing from 2025 value of USD 33.84 billion with 2031 projections showing USD 58.37 billion, growing at 9.51% CAGR over 2026-2031. Robust growth is driven by record-high global R&D outlays, a steady pivot toward specialized outsourcing, and rising acceptance of decentralized and hybrid clinical trial models across the region.[1]Source: U.S. Food and Drug Administration, “Conducting Clinical Trials With Decentralized Elements Guidance,” fda.gov Biopharmaceutical sponsors intensify collaboration with CROs to navigate complex regulatory pathways, while technology-enabled patient-recruitment solutions compress enrollment timelines, improving portfolio productivity. Geographic concentration remains pronounced: the United States contributes most of the current revenue, yet Canada’s cost-efficient early-phase ecosystem accelerates faster, creating competitive white space for regional providers. Functional Service Provider (FSP) adoption reshapes commercial models as large sponsors unbundle traditional contracts, suppressing legacy margins but opening niches for high-value specialty service lines.

Key Report Takeaways

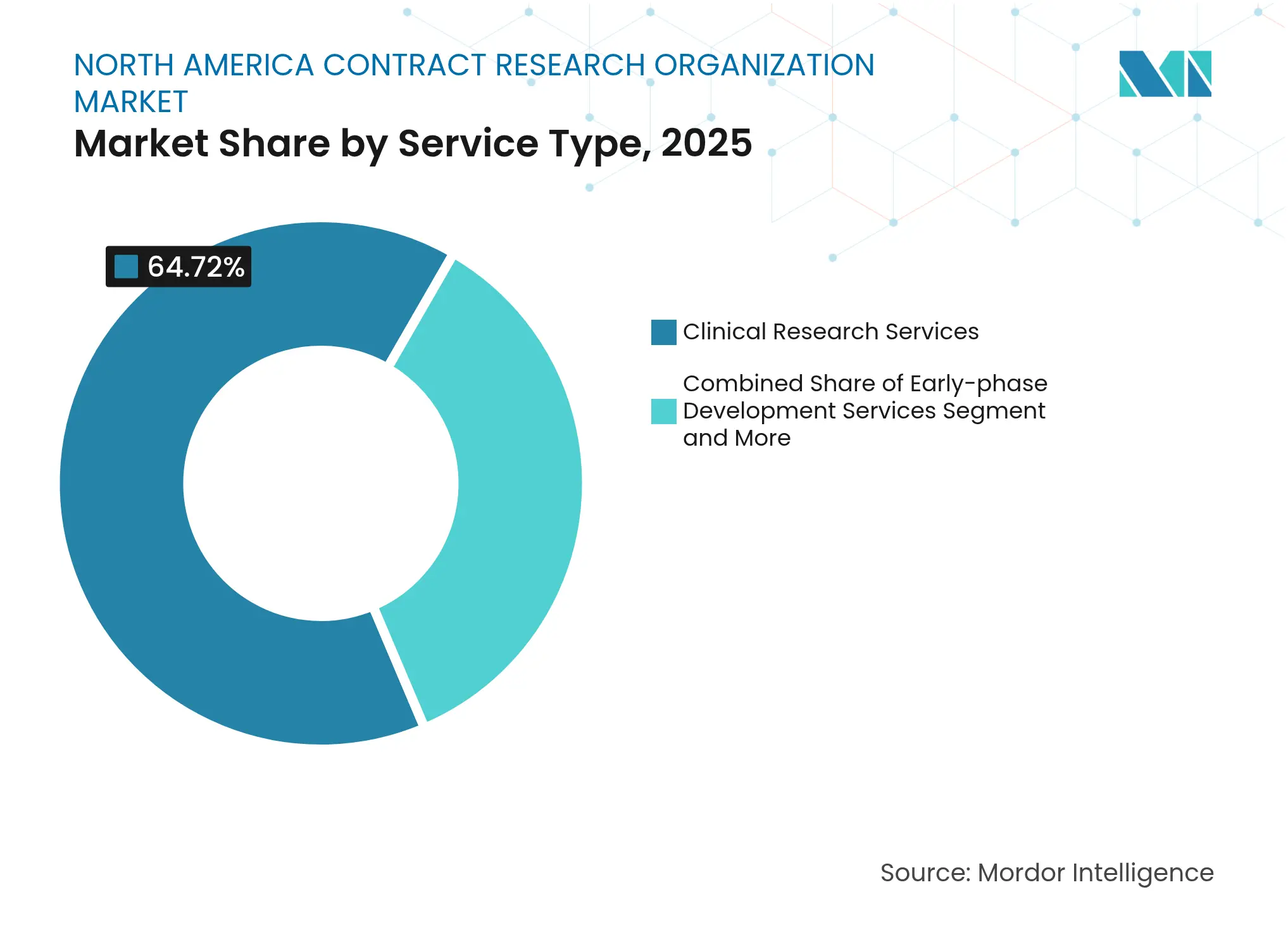

- By service type, Clinical Research Services led with 64.72% of North America Contract Research Organization market share in 2025; Early-phase Development Services record the fastest 10.4% CAGR through 2031

- By therapeutic area, Oncology captured 28.31% revenue share in 2025, while Infectious Diseases is projected to expand at a 9.88% CAGR to 2031

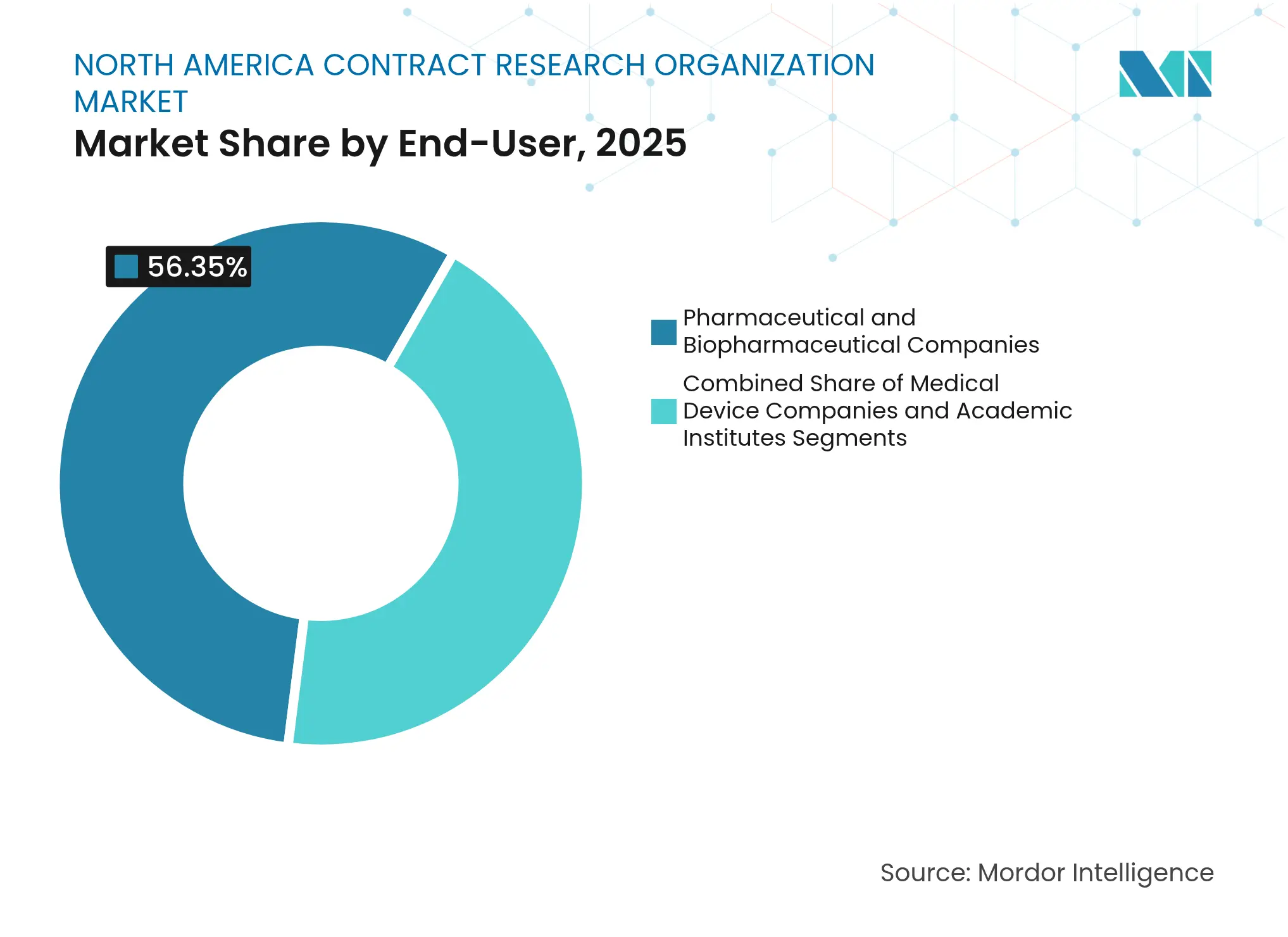

- By end-user, Pharmaceutical and Biopharmaceutical Companies held 56.35% share of the North America Contract Research Organization market size in 2025; Medical Device Companies advance at a 9.79% CAGR through 2031

- By geography, the United States commanded 85.12% share of the North America Contract Research Organization market in 2025, whereas Canada registers the highest 9.63% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Contract Research Organization Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising R&D Expenditure by Pharma & Biotech

Sponsors

Rising R&D Expenditure by Pharma & Biotech

Sponsors

| +1.6% | North America & Global | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.6%

|

Geographic Relevance

:

North America & Global

|

Impact Timeline

:

Medium term (2-4 years)

|

Growing Volume & Complexity of Clinical Trials

Growing Volume & Complexity of Clinical Trials

| +2.1% | Global, concentrated in North America | Long term (≥ 4 years) | |||

Intensifying Outsourcing Trend Across Life-Science Value

Chain

Intensifying Outsourcing Trend Across Life-Science Value

Chain

| +1.8% | North America & EU primary | Medium term (2-4 years) | |||

Regulatory Push for Accelerated Pathways

Regulatory Push for Accelerated Pathways

| +1.5% | US FDA jurisdiction, spillover to Canada | Short term (≤ 2 years) | |||

Expansion Of Decentralized/Hybrid Trial Models Needing CRO

Tech Stacks

Expansion Of Decentralized/Hybrid Trial Models Needing CRO

Tech Stacks

| +0.9% | North America lead, global adoption | Medium term (2-4 years) | |||

AI-Driven Patient-Recruitment Analytics Boosting CRO

Efficiency

AI-Driven Patient-Recruitment Analytics Boosting CRO

Efficiency

| +0.7% | North America tech hubs, selective global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising R&D Expenditure by Pharma & Biotech Sponsors

Big-pharma R&D spending reached USD 161 billion in 2024, marking a structural shift toward externalized development that favors CRO partnerships. Biotech firms added more than USD 50 billion in outsourced contracts, seeking variable cost structures and risk-sharing arrangements. The upcoming USD 350 billion patent-cliff window between 2025 and 2029 further accelerates the need for cost-efficient development pipelines. Surveys show sponsors plan a 4% budget uplift in 2025, with large companies driving premium demand tiers. Collectively, higher R&D allocations enhance the growth trajectory of the North America Contract Research Organization market as CROs transition from vendors to strategic partners.

Growing Volume & Complexity of Clinical Trials

Precision-medicine designs now shrink eligible patient pools by as much as 80%, driving demand for advanced recruitment analytics and global reach. Novel modalities such as antibody-drug conjugates require integrated biomarker, safety, and manufacturing know-how, capabilities that well-funded CROs can monetize through premium service tiers. The FDA’s Center for Clinical Trial Innovation, created in April 2024, underscores regulatory support for sophisticated trial methodologies. Complexity therefore sustains double-digit demand for specialized CRO services across the North America Contract Research Organization market.

Intensifying Outsourcing Trend Across Life-Science Value Chain

Roughly 60% of global clinical-development spend is already externalized, and CRO penetration in North America stands near 40% with ample headroom. Sponsors now outsource not only site operations but also regulatory submissions, manufacturing oversight, and post-market surveillance, shifting revenue pools from transactional tasks to strategic engagements. The North America Contract Research Organization industry benefits from this evolution, as mastery of integrated programs enables providers to lock in multiyear agreements that smooth revenue visibility.

Regulatory Push for Accelerated Pathways

The FDA’s finalized 2024 guidance on decentralized trials, along with fast-track and breakthrough therapy frameworks, reduces development timelines by up to 40%, rewarding CROs that offer deep regulatory science expertise. New draft guidance for multiregional oncology trials requires U.S. patient inclusion, reinforcing domestic trial relevance and buttressing the North America Contract Research Organization market. Providers that combine regulatory insight with technology-enabled monitoring gain a clear competitive edge.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of Skilled Clinical-Research Professionals

Shortage of Skilled Clinical-Research Professionals

| -1.2% | North America acute, global concern | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-1.2%

|

Geographic Relevance

:

North America acute, global concern

|

Impact Timeline

:

Long term (≥ 4 years)

|

Escalating Trial Costs & Budget Constraints for Small

Sponsors

Escalating Trial Costs & Budget Constraints for Small

Sponsors

| -0.8% | Global, concentrated in biotech sector | Medium term (2-4 years) | |||

Complex, Evolving FDA Guidance for Decentralized Trials

Complex, Evolving FDA Guidance for Decentralized Trials

| -0.6% | US primary, regulatory spillover effects | Short term (≤ 2 years) | |||

Shift Toward FSP/Unbundled Sourcing Squeezing CRO Margins

Shift Toward FSP/Unbundled Sourcing Squeezing CRO Margins

| -0.4% | North America & EU large pharma | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Skilled Clinical-Research Professionals

The clinical research workforce crisis reaches critical proportions, with seven job openings for every experienced clinical research coordinator and a 10:1 ratio for clinical research nurses, creating structural capacity constraints that limit CRO growth potential. Seven openings exist for every experienced coordinator, and CRA turnover hovers near 30% in the United States, eroding project delivery capacity.[2]Source: Association of Clinical Research Professionals, “Clinical Trial Workforce Preparedness,” acrpnet.org Oncology and rare-disease domains suffer acutely as expertise commands premium salaries that squeeze provider profitability. CROs respond with internal academies and career-ladder programs, but talent gaps persist, tempering near-term scalability within the North America Contract Research Organization market.

Escalating Trial Costs & Budget Constraints for Small Sponsors

Rising clinical trial costs disproportionately impact smaller biotech sponsors, with Phase III studies now averaging USD 20-30 million, forcing companies to delay or cancel development programs that could otherwise drive CRO demand. Sponsors defer programs or adopt piecemeal FSP engagements, shrinking the addressable pool for full-service providers. CROs focusing on flexible pricing and modular offerings mitigate some revenue risk but still face elongated sales cycles.

Segment Analysis

By Service Type: Clinical Research Services Maintain Dominance Despite Early-Phase Acceleration

Clinical Research Services represented 64.72% of 2025 revenue, anchoring the North America Contract Research Organization market. These late-phase activities remain indispensable to sponsors seeking global regulatory approvals, underpinning a stable revenue core. At the same time, Early-phase Development Services expand at a 10.4% CAGR to 2031 as biotech companies prioritize Phase I partners with dedicated units, adaptive-design expertise, and first-in-human safety infrastructure.

The segment mix evolution favors CROs that balance high-volume Phase III execution with specialty early-phase capabilities. Laboratory and consulting offerings add value through integrated biomarker, companion-diagnostic, and regulatory-science support. Such end-to-end propositions position full-service providers to capture cross-selling synergies and defend market share despite FSP margin pressures, reinforcing leadership across the North America Contract Research Organization market.

Note: Segment shares of all individual segments available upon report purchase

By Therapeutic Area: Oncology Leadership Faces Infectious Diseases Momentum

Oncology controlled 28.31% revenue in 2025, supported by 4,295 completed studies in 2023. Immune-oncology pipelines and complex biomarker strategies maintain steady flow through Phase III, sustaining rich demand for specialized monitoring and safety services. Nonetheless, Infectious Diseases posts the highest 9.88% CAGR as pandemic-preparedness funding institutionalizes vaccine and antiviral R&D.

CROs that scale infectious-disease units, expand BSL-2/3 laboratories, and integrate epidemiology modeling capture outsized growth. CNS and immunology programs require precision-medicine frameworks that few providers master, tightening competition for niche expertise. This therapeutic diversification underpins broader resilience within the North America Contract Research Organization market.

By End-User: Medical Device Acceleration Challenges Pharma Dominance

Pharmaceutical and Biopharmaceutical Companies still generate 56.35% of 2025 revenue, yet Medical Device Companies advance at a 9.79% CAGR on the back of software-as-medical-device and combination-product complexity. Device sponsors now demand robust clinical evidence and post-market surveillance, mirroring drug-development rigor.

Academic institutes form a catalytic yet smaller cohort, often incubating novel modalities before licensing to commercial partners. CROs investing in device-specific regulatory strategy, usability engineering, and real-world performance analytics unlock new fee pools. Cross-training multidisciplinary teams supports converging development pathways and secures incremental revenue throughout the North America Contract Research Organization market size spectrum.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The United States delivered 85.12% of 2025 revenue, leveraging unrivaled sponsor density, trial infrastructure, and FDA proximity to maintain gravitational pull for late-phase programs. Domestic data underpin global marketing submissions, making U.S. patient inclusion mandatory for most pipelines. Major providers such as IQVIA translate deep electronic-health-record assets into competitive site-selection and recruitment advantages that smaller rivals cannot easily match.

Canada contributes a rising share, logging a 9.63% CAGR through 2031 by enabling Phase I studies ahead of U.S. IND filings and offering 15–25% cost savings. Health Canada’s responsive review timelines and ethnically diverse populations appeal to sponsors running rare-disease or early-proof-of-concept studies. CROs with operations on both sides of the border capitalize on complementary regulatory pathways to compress timelines.

Mexico rounds out the regional picture, emerging as a cost-effective location for studies requiring Hispanic-heritage enrollment or chronic-disease prevalence. Infrastructure constraints and variable investigator experience curb scale today, yet cross-border collaboration initiatives promise gradual uplift. The integrated North America Contract Research Organization market therefore reflects a blend of high-value U.S. volume, accelerated Canadian starts, and selectively deployed Mexican cohorts, optimizing both cost and data relevance.

Competitive Landscape

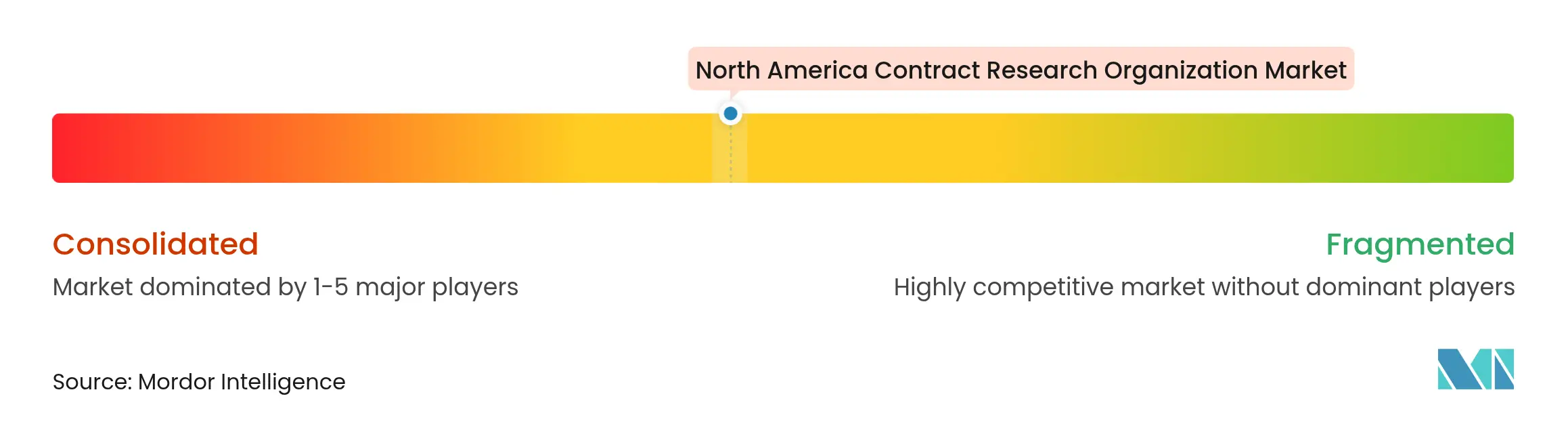

Market Concentration

Competitive dynamics remain moderately consolidated: IQVIA, Fortrea, ICON, Charles River, and Medpace together command sizeable share yet leave room for hundreds of specialist firms. Scale players focus on technology integration—AI-enabled recruitment, eCOA platforms, and real-world evidence—to defend incumbency and win enterprise-wide preferred provider deals.

Niche competitors thrive in rare diseases, cell-gene therapy, and regional site-management, leveraging depth over breadth. Private-equity inflows fund start-ups targeting point solution gaps such as decentralized monitoring or e-consent, raising the innovation bar across the North America Contract Research Organization market. Functional outsourcing trends intensify pricing competition on individual service lines; providers able to demonstrate demonstrable efficiency gains or therapeutic mastery capture premium contracts.

Strategic moves underscore the race for differentiation: Thermo Fisher expanded its Kentucky laboratory to extend integrated lab-to-clinic offerings, Fortrea sharpened therapeutic-area focus post-spin-off, and ICON continued bolt-on acquisitions to deepen infectious-disease capabilities. Success increasingly hinges on blending therapeutic specialization, digital operating models, and workforce development programs that stabilize delivery quality in an otherwise talent-constrained environment.

North America Contract Research Organization Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Thermo Fisher Scientific expanded its clinical research laboratory in Kentucky, adding bioanalytical and central-lab capacity for sponsors targeting accelerated timelines.

- January 2024: Biognosys declared its new proteomics facility in Massachusetts operational. This expansion in the United States allows Biognosys' biopharma clients in the United States to conveniently access specific proteomics contract research organization (CRO) services.

- August 2023: Kohlberg signed a definitive agreement to secure a majority stake in Worldwide Clinical Trials, a comprehensive contract research organization (CRO) and an affiliate of TJC, L.P.

Table of Contents for North America Contract Research Organization Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising R&D Expenditure by Pharma & Biotech Sponsors

- 4.2.2Growing Volume & Complexity of Clinical Trials

- 4.2.3Intensifying Outsourcing Trend Across Life-Science Value Chain

- 4.2.4Regulatory Push for Accelerated Pathways

- 4.2.5Expansion Of Decentralized/Hybrid Trial Models Needing CRO Tech Stacks

- 4.2.6AI-Driven Patient-Recruitment Analytics Boosting CRO Efficiency

- 4.3Market Restraints

- 4.3.1Shortage of Skilled Clinical-Research Professionals

- 4.3.2Escalating Trial Costs & Budget Constraints for Small Sponsors

- 4.3.3Complex, Evolving FDA Guidance for Decentralized Trials

- 4.3.4Shift Toward FSP/Unbundled Sourcing Squeezing CRO Margins

- 4.4Regulatory Landscape

- 4.5Porter’s Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Service Type

- 5.1.1Clinical Research Services

- 5.1.1.1Phase I

- 5.1.1.2Phase II

- 5.1.1.3Phase III

- 5.1.1.4Phase IV

- 5.1.2Early-phase Development Services

- 5.1.3Laboratory Services

- 5.1.4Consulting Services

- 5.2By Therapeutic Area

- 5.2.1Oncology

- 5.2.2Infectious Diseases

- 5.2.3Central Nervous System (CNS) Disorders

- 5.2.4Immunological Disorders

- 5.2.5Cardiovascular Diseases

- 5.2.6Respiratory Disorders

- 5.2.7Diabetes

- 5.2.8Other Therapeutic Areas

- 5.3By End-User

- 5.3.1Pharmaceutical and Biopharmaceutical Companies

- 5.3.2Medical Device Companies

- 5.3.3Academic Institutes

- 5.4By Geography

- 5.4.1United States

- 5.4.2Canada

- 5.4.3Mexico

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1IQVIA Holdings Inc.

- 6.3.2Fortrea

- 6.3.3ICON plc

- 6.3.4Charles River Laboratories

- 6.3.5Medpace Holdings

- 6.3.6Syneos Health

- 6.3.7Parexel International

- 6.3.8Thermo Fisher Scientific Inc. (PPD Inc.)

- 6.3.9PSI CRO

- 6.3.10Premier Research

- 6.3.11Worldwide Clinical Trials

- 6.3.12Inotiv

- 6.3.13Precision for Medicine

- 6.3.14dicentra

- 6.3.15Syreon Corporation

- 6.3.16TFS HealthScience

- 6.3.17Ergomed plc

- 6.3.18Wuxi AppTec

- 6.3.19Covance (by Labcorp)

- 6.3.20ClinChoice

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

North America Contract Research Organization Market Report Scope

As per the scope of this report, a contract research organization is a company that provides clinical trial services for the pharmaceutical, biotechnology, and medical device industries. CROs range from large, international, full-service organizations to small, niche specialty groups.

The North America contract research organization market is segmented into service type, therapeutic areas, end-user, and geography. By service type, the market is segmented into clinical research services, early-phase development services, laboratory services, and consulting services. The clinical research services segment includes phase I clinical research services, phase II clinical research services, phase III clinical research services, and phase IV clinical research services. By therapeutic areas, the market is segmented into oncology, infectious diseases, central nervous system disorders, immunological disorders, cardiovascular diseases, respiratory disorders, diabetes, and other therapeutic areas. Other therapeutic areas include metabolic, musculoskeletal, wound and injuries, eye diseases, and mouth & dental diseases. By end user, the market is segmented into pharmaceutical and biopharmaceutical companies, medical device companies, and academic institutes. By geography, the market is segmented into the United States, Canada, and Mexico. Market sizing and forecasts for each segment have been conducted based on value in USD.