Pharmaceutical Contract Sales Organizations (CSO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

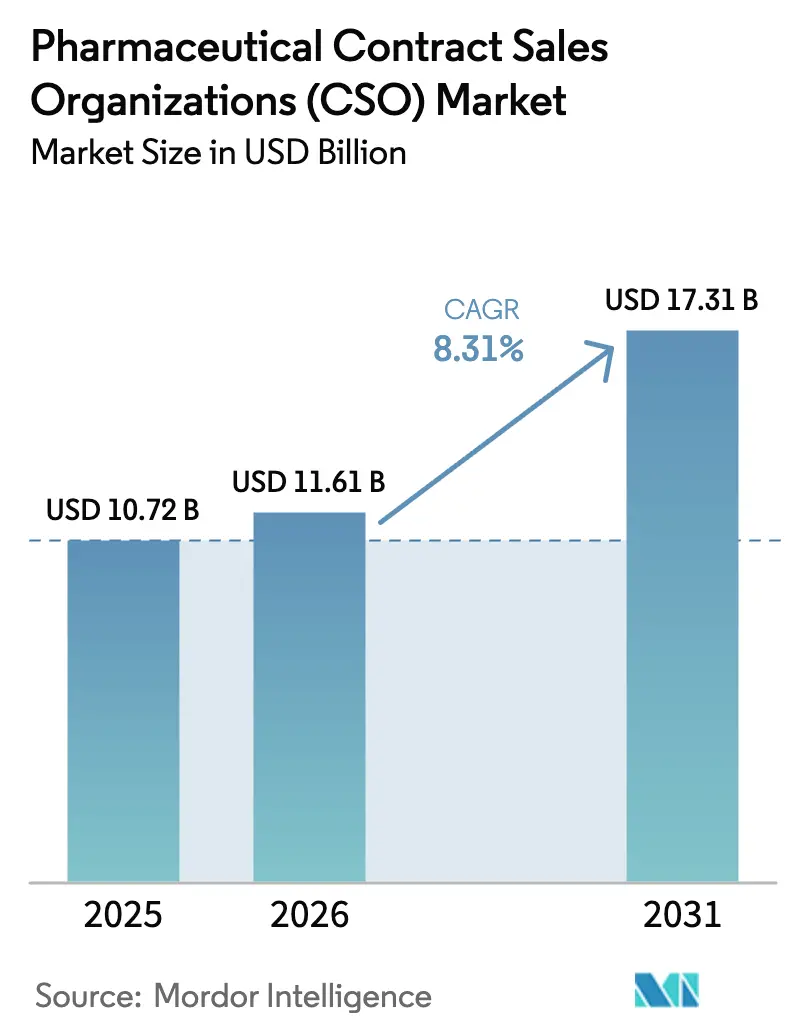

| Market Size (2026) | USD 11.61 Billion |

| Market Size (2031) | USD 17.31 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

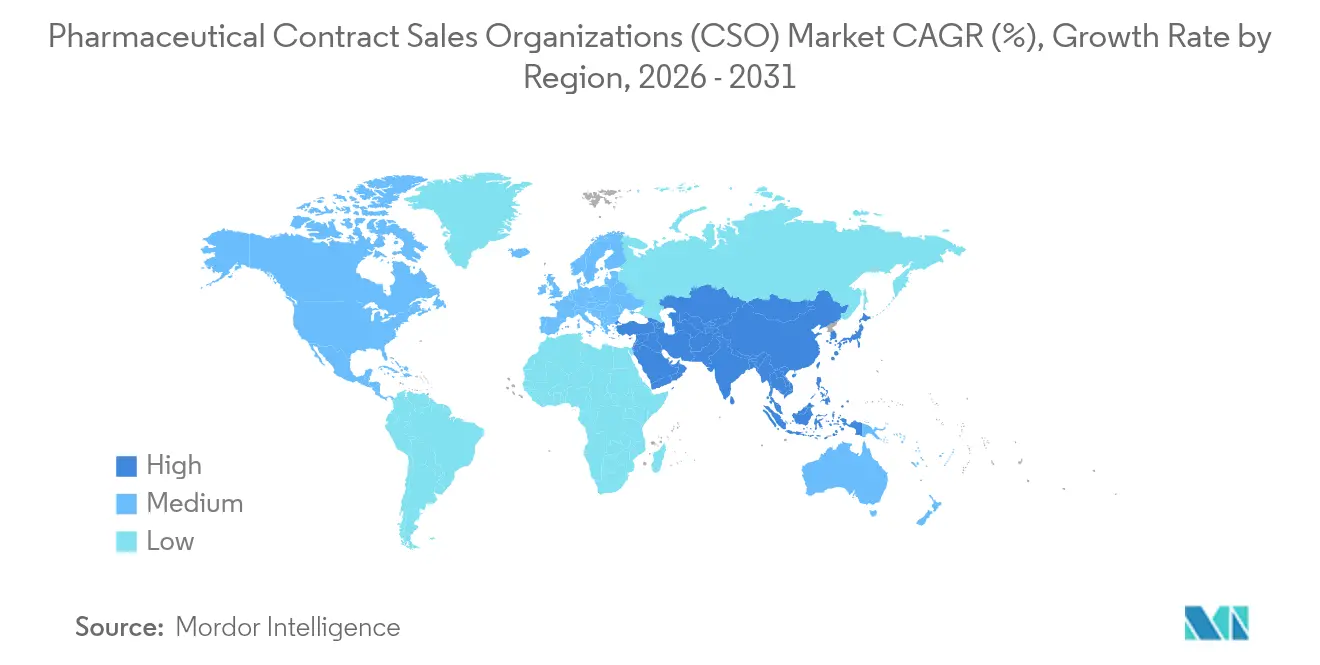

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

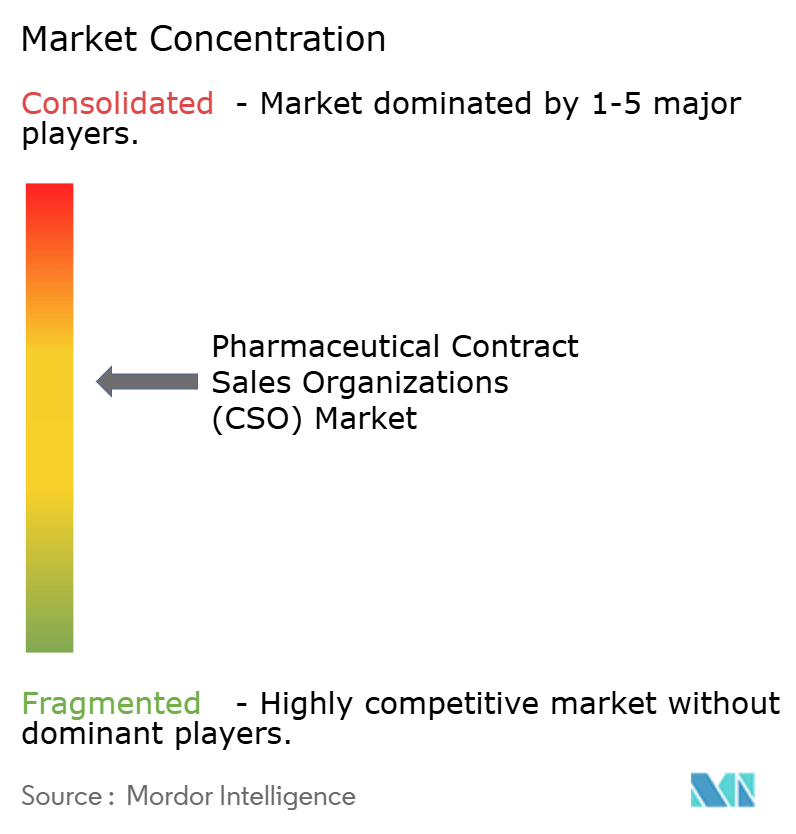

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Contract Sales Organizations (CSO) Market Analysis by Mordor Intelligence

The contract sales organization market size in 2026 is estimated at USD 11.61 billion, growing from 2025 value of USD 10.72 billion with 2031 projections showing USD 17.31 billion, growing at 8.31% CAGR over 2026-2031. Higher patent-cliff exposure, intensifying regulatory demands, and biopharma’s shift toward flexible operating models keep outsourced commercial execution in strong demand. Mid-sized biotechnology firms that completed public offerings between 2019 and 2023 now face aggressive launch timelines yet lack field infrastructure, prompting rapid CSO adoption. Large pharmaceutical companies continue to turn to CSOs as hospital network consolidation raises the bar for account-based selling. Meanwhile, AI-guided territory design and predictive engagement lift return on investment and reinforce the value of outsourcing partners. Strong growth in Asia-Pacific, where clinical trial and commercial costs run 30-40% below Western averages, further propels global expansion.

Key Report Takeaways

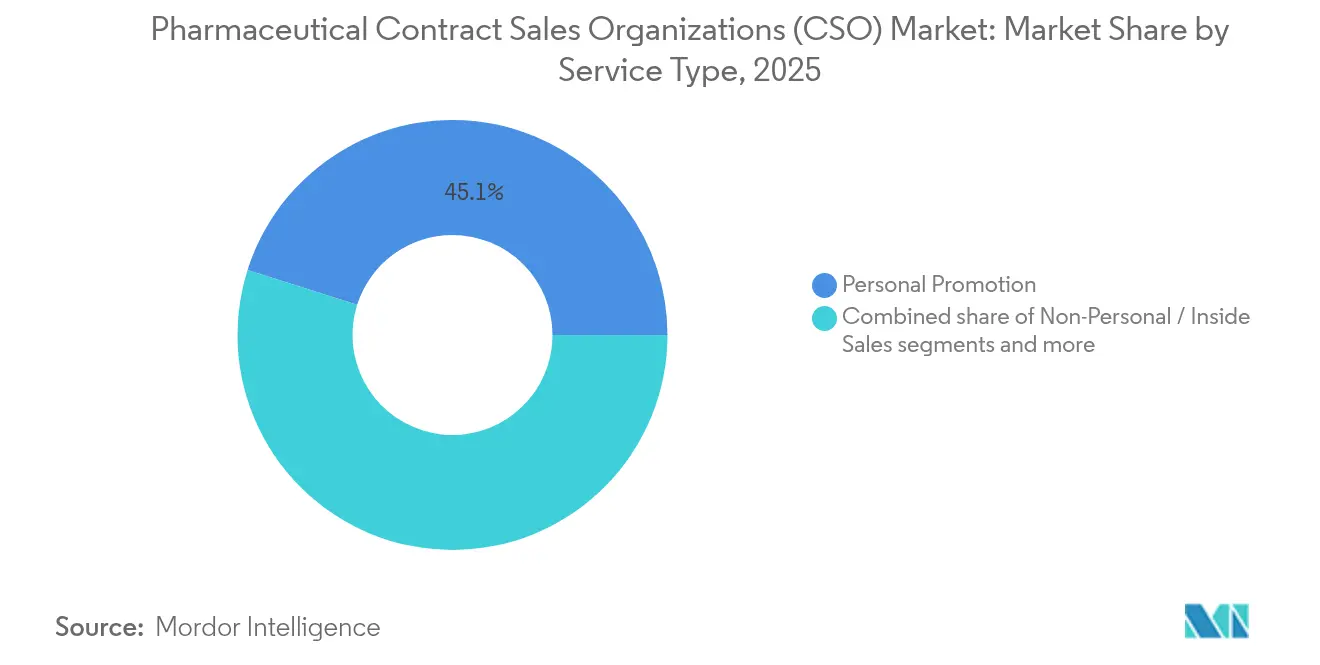

- By service type, personal promotion retained 45.12% of contract sales organization market share in 2025, while hybrid omnichannel engagement is projected to post the fastest 8.60% CAGR through 2031.

- By therapeutic area, oncology led with 32.55% revenue share in 2025; rare diseases are advancing at a 9.05% CAGR to 2031.

- By client type, large pharmaceutical firms held 56.41% of the contract sales organization market share in 2025, whereas emerging biotech companies are forecast to expand at 10.62% CAGR by 2031.

- By geography, North America commanded 43.10% share of the contract sales organization market size in 2025, yet Asia-Pacific is expected to log a 10.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Contract Sales Organizations (CSO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widening patent-cliff pipelines | +2.1% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Cost-containment pressures among big pharma | +1.8% | Global | Long term (≥ 4 years) |

| Shift toward specialty & biologics portfolios | +1.5% | Global, led by North America | Long term (≥ 4 years) |

| Rapid hospital-channel consolidation raises need for turnkey account-based teams | +1.2% | North America & Europe | Short term (≤ 2 years) |

| AI-guided rep-targeting improves CSO ROI, boosting outsourcing appetite | +0.9% | Global, early adoption in North America | Medium term (2-4 years) |

| Mid-sized biopharma IPO class lacks field infrastructure but faces launch deadlines | +0.8% | Global, concentrated in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Widening Patent-Cliff Pipelines

Loss of exclusivity on 190 drugs is expected to strip more than USD 236 billion in branded revenue by 2030, forcing pharmaceutical firms to accelerate launches of pipeline assets and preserve cash-flow streams. CSOs provide ready-deploy field teams in weeks, versus the 12–18-month window needed for internal hiring. Oncology and rare-disease launches rely on deeply trained clinical representatives that most sponsors lack, making CSOs essential for bridging the revenue gap. Biosimilar entrants quicken the erosion, heightening urgency for immediate commercialization support. As a result, CSO outsourcing is increasingly embedded in brand-defense playbooks.

Cost-Containment Pressures Among Big Pharma

Margin compression from the Inflation Reduction Act, global reference pricing, and rising launch costs forces manufacturers to treat commercial spending as a variable cost. CSOs let sponsors flex headcount in or out as brands move through life-cycle stages. Variable models also shift recruitment, training, and retention overhead to the vendor while performance guarantees cap risk. Tier-one pharma sees outsourced selling capacity as a strategic hedge that allows faster geographic entry or exit, especially when payer dynamics change suddenly.

Shift Toward Specialty & Biologics Portfolios

Biologics dominate late-stage pipelines, accounting for the fastest growing class of approvals, and involve meticulous cold-chain and reimbursement navigation. CSOs invest in therapeutic centers of excellence that train multi-client field forces on complex infusion protocols, specialty pharmacy workflows, and rare-disease patient services. Individual sponsors cannot match these economies of scale, so they lean on CSOs for depth and speed. The expertise proves critical when value-based contracting or outcomes-based payment schemes underpin access.

Rapid Hospital-Channel Consolidation

Integrated delivery networks and group purchasing organizations now control a rising share of drug purchasing decisions in the United States and Europe. Building the sophisticated account management skill set needed to navigate multi-stakeholder committees is expensive and time intensive. CSOs already maintain dedicated institutional teams familiar with formulary reviews, quality metrics, and population-health economics. Heightened GPO leverage therefore pushes sponsors to outsource institutional engagement to trusted partners who can speak the language of hospital finance and bundled payments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing HCP access barriers for face-to-face promotion | -1.4% | Global, most severe in North America | Short term (≤ 2 years) |

| Stringent compliance requirements on third-party reps | -0.8% | Global, with varying regional intensity | Medium term (2-4 years) |

| Rising preference for modular omnichannel "inside-out" models dilutes pure-play CSO demand | -0.6% | North America & Europe, early adoption markets | Medium term (2-4 years) |

| Data-privacy laws limit real-time rep performance analytics | -0.4% | Global, with highest impact in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing HCP Access Barriers

Face-to-face access rates for U.S. prescribers slid from 60% in 2022 to 45% in 2024, reflecting tighter health-system gatekeeping and clinician workload. CSOs must pivot to omnichannel engagement, yet digital investments compress margins when clients still benchmark pricing on legacy field models. The rise of institutional formulary committees further weakens individual physician influence, undermining the classic rep playbook. Regional variation in access policies adds complexity and escalates operational costs for vendors that must master different credentialing workflows.

Stringent Compliance Requirements on Third-Party Reps

Regulators intensified scrutiny on speaker programs and field conduct, illustrated by recent multi-million-dollar settlements under the Anti-Kickback Statute. CSOs must expand audit trails, ramp up training, and deploy monitoring platforms to stay ahead. These investments raise overhead and deter smaller entrants. Data-privacy rules in Europe and parts of Asia restrict granular performance analytics, limiting visibility that sponsors increasingly demand. Consequently, risk-averse manufacturers sometimes favor in-house teams for high-risk brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hybrid Models Gain Ground

Personal promotion remained the largest slice of the contract sales organization market size with USD — corresponding to 45.12% of 2025 revenue. The conventional field-rep model persists because many prescribers still value human interaction for complex treatments. Yet hybrid omnichannel solutions that knit digital pushes with curated in-person calls are growing at 8.60% CAGR, the fastest among service categories. This expansion reflects falling HCP access and the need for content that can be consumed asynchronously on clinicians’ terms.

CSOs now embed data scientists, content strategists, and medical writers alongside territory managers to orchestrate channel mix. AI-driven “augmented rep” programs push next-best-action insights directly to representatives’ tablets, allowing dynamic call plans and personalized follow-ups. Sponsors judge success not by call volume but by customer experience scores and pull-through metrics, rewarding vendors that offer closed-loop analytics. As a result, hybrid engagement is reshaping pricing models toward outcome-based fees that favor technology-rich providers.

By Therapeutic Area: Oncology Dominance Meets Rare-Disease Momentum

Oncology generated 32.55% of 2025 revenue, the single largest therapeutic slice of the contract sales organization market share, as immuno-oncology combinations and precision diagnostics demand deep clinical fluency. Complex care pathways, multidisciplinary tumor boards, and biomarker testing protocols require reps who can articulate evolving standards. These needs align with CSO scale economics that let multiple sponsors tap into a common pool of hematology-oncology educators.

Rare diseases clock a 9.05% CAGR to 2031, outpacing every other therapeutic area as gene and cell therapies reach commercialization. Orphan launches entail patient identification through novel diagnostic algorithms, close liaison with advocacy groups, and high-touch distribution logistics. CSOs have responded by building rare-disease centers of excellence staffed with genetic counselors and reimbursement experts. Sponsors value seamless coordination across hub services, payers, and specialty pharmacies—a capability that young biotech firms seldom possess internally.

By Client Type: Biotech Surge Redefines Demand

Large pharmaceutical companies still supply 56.41% of 2025 revenue for the contract sales organization market and typically maintain multi-year master service agreements that span portfolios. They rely on CSOs to surge capacity during launch peaks, test new geographies, or fill therapeutic expertise gaps. Mid-tier firms tap vendors for ad-hoc regional coverage or for brands outside core therapeutic focus.

Emerging biotech represents the most dynamic client cohort with a 10.62% CAGR to 2031, reflecting relentless venture investment and IPO momentum. Many lack brand-building experience, so they outsource everything from key-opinion-leader mapping to patient-services hotlines. CSOs sweeten value propositions with risk-sharing models tied to milestone payments or profit splits, which align well with biotech cash-flow realities. Consequently, vendor-biotech collaborations now incubate novel go-to-market tactics that later migrate to larger sponsors.

Geography Analysis

North America’s 43.10% share stems from entrenched pharmaceutical headquarters, intricate reimbursement systems, and rising hospital consolidation that demands sophisticated account coverage. CSOs specialize in navigating GPO formularies, value-based contracts, and state-level policy nuances. U.S. sponsors lean on vendors that supply AI-enabled territory planning to balance direct hospital access with remote engagement. Canada and Mexico augment regional growth through generics expansion and accelerating biologics uptake.

Europe holds the second-largest revenue stream, though growth is tempered by single-payer cost controls and heterogeneous country regulations. CSOs create value by harmonizing multi-country launches, ensuring cultural adaptation, language compliance, and local market-access dossiers. Germany and the United Kingdom host robust pipelines that feed outsourcing demand, while France, Italy, and Spain require nuanced navigation of reference pricing and centralized tendering.

Asia-Pacific tops the growth charts with 10.23% CAGR through 2031. China leads thanks to streamlined drug-approval reforms and government incentives for innovative therapies. India offers world-scale manufacturing and expanding middle-class demand, intensifying competition for skilled representatives. Japan rewards rapid market entries by granting early post-marketing price revisions, making CSO support invaluable. South Korea’s digital-health leadership pushes vendors to master omnichannel, whereas Australia’s HTA process necessitates specialized pharmaco-economic negotiation skills.

Competitive Landscape

The contract sales organization market remains moderately fragmented, with the top five providers controlling significant global revenue. Leaders differentiate through AI analytics, therapeutic specialization, and integrated commercial-services portfolios. IQVIA’s alliance with Salesforce infuses its Orchestrated Customer Engagement suite into Life Sciences Cloud, blending CRM data with predictive insights for multi-tenant client delivery. Syneos Health leverages CRO synergies to cross-sell commercialization, notably winning new oncology trials that transition smoothly into launch support. EVERSANA invests in pharmacovigilance and patient hub assets, broadening its risk-sharing models that tie fees to script lift.

White-space entrants focus on rare-disease navigation or cell-therapy logistics where clinical and distribution demands are unique. Private-equity capital fuels consolidation plays that roll smaller regional CSOs into scalable platforms with standardized compliance systems. Competitive intensity pivots around proof of ROI; vendors showcase AI-based territory adjustments that yield double-digit call-productivity gains. Rising compliance scrutiny raises the cost of entry, creating barriers for niche firms that cannot absorb audit and training overhead.

Pharmaceutical Contract Sales Organizations (CSO) Industry Leaders

Ashfield Medcomms.

IQVIA Inc.

Syneos Health

ICON plc

CMIC HOLDINGS Co., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Pfizer settled with the Office of Inspector General in a USD 60 million agreement over speaker-program practices, prompting CSOs to tighten promotional oversight

- December 2024: Novo Holdings completed a USD 16.5 billion acquisition of Catalent, expanding end-to-end outsourcing scope across manufacturing and commercial services.

Global Pharmaceutical Contract Sales Organizations (CSO) Market Report Scope

As per the scope of the report, pharmaceutical contract sales outsourcing (CSO) refers to the practice of pharmaceutical companies hiring external service providers to manage and execute their sales functions rather than maintaining an in-house sales team. This can include tasks such as marketing, sales force management, and territory development. CSO offers flexibility, cost-efficiency, and access to specialized expertise to pharmaceutical companies without the overhead of maintaining a large sales department.

The market is segmented by services, sales type, therapeutic area, and geography. By service, the market is segmented into personal promotion, non-personal promotion, and others. By sales type, the market is segmented into a dedicated sales model and a syndicated sales model. By therapeutic area, the market is segmented as cardiovascular disorders, oncology, metabolic disorders, neurology, and others. The other therapeutic areas include orthopedic diseases and infectious diseases, among others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecasts were made on the basis of value (in USD).

| Personal Promotion (Dedicated Field Teams) |

| Non-Personal / Inside Sales |

| Hybrid Omnichannel Engagement |

| Oncology |

| Cardiovascular & Metabolic |

| CNS & Psychiatry |

| Infectious Diseases |

| Rare Diseases |

| Large Pharma (More than USD 10 billion Sales) |

| Mid-Sized Pharma (USD 1-10 B billion) |

| Emerging Biotech (Less than USD 1 B billion) |

| Medical Device & Diagnostics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Personal Promotion (Dedicated Field Teams) | |

| Non-Personal / Inside Sales | ||

| Hybrid Omnichannel Engagement | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular & Metabolic | ||

| CNS & Psychiatry | ||

| Infectious Diseases | ||

| Rare Diseases | ||

| By Client Type | Large Pharma (More than USD 10 billion Sales) | |

| Mid-Sized Pharma (USD 1-10 B billion) | ||

| Emerging Biotech (Less than USD 1 B billion) | ||

| Medical Device & Diagnostics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the contract sales organization market in 2026?

The contract sales organization market size is USD 11.61 billion in 2026.

What is the forecast CAGR for contract sales outsourcing through 2031?

The market is projected to grow at an 8.31% CAGR between 2026 and 2031.

Which service segment is expanding fastest?

Hybrid omnichannel engagement shows the fastest growth at 8.60% CAGR to 2031.

Why is Asia-Pacific attracting CSO investment?

Lower operating costs, larger patient pools, and regulatory reforms support a 10.23% regional CAGR.

What client group is driving new CSO contracts?

Emerging biotech companies are growing at 10.62% CAGR as they rush to commercialize launches.

How does AI improve CSO effectiveness?

Predictive targeting reduces low-value calls by up to 50% and optimizes channel mix for higher ROI.

Page last updated on: