Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

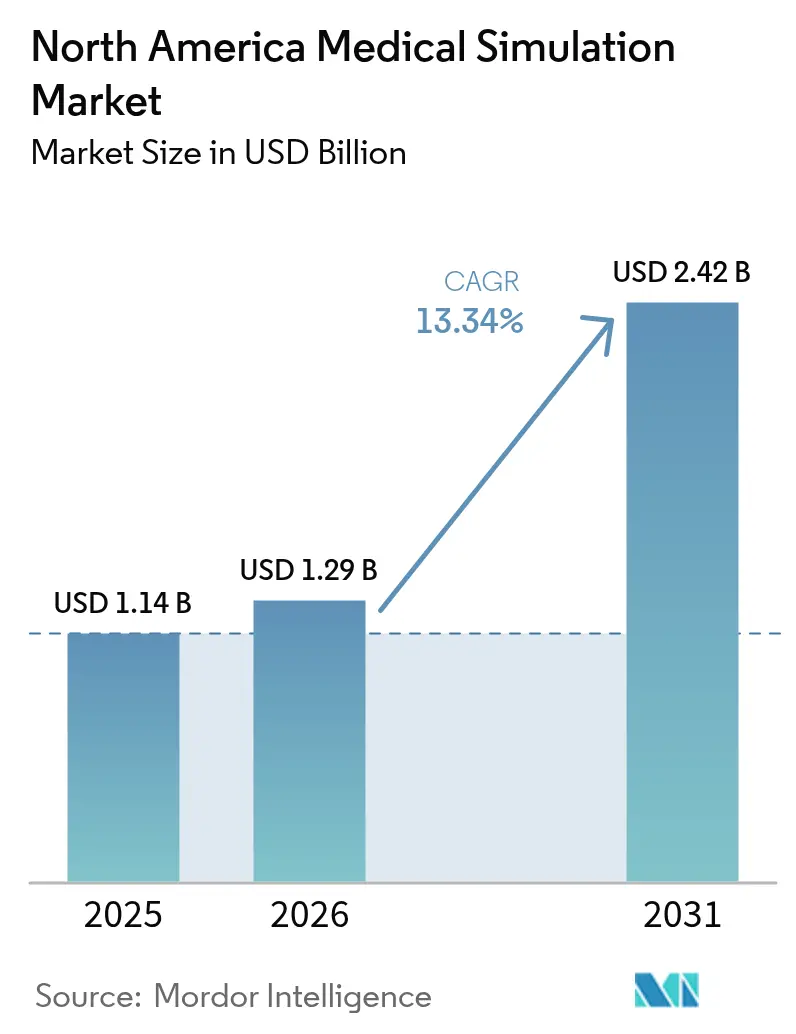

| Base Year Market Size (2025) | USD 1.14 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 2.42 Billion |

| Growth Rate (2026 - 2031) | 13.34% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Medical Simulation Market Analysis by Mordor Intelligence

North American medical simulation market size in 2026 is estimated at USD 1.29 billion, growing from 2025 value of USD 1.14 billion with 2031 projections showing USD 2.42 billion, growing at 13.34% CAGR over 2026-2031. This headline figure represents the current medical simulation market size and highlights the brisk growth trajectory being fueled by faculty shortages, patient-safety mandates, and rapid advances in extended-reality hardware. Demand pressure is strongest where medical schools face limited clerkship slots, regulatory bodies insist on measurable competency proof, and virtual-reality head-mounted displays finally deliver clinical-grade visual fidelity. As a result, the medical simulation market is shifting from discretionary spending toward critical infrastructure investment as educators and hospitals chase scalable, repeatable, and data-rich training models. Regulatory emphasis on computational modeling in FDA submissions, rising adoption of AI-driven adaptive analytics, and cost-effective service contracting all reinforce the market’s growth momentum.

Key Report Takeaways

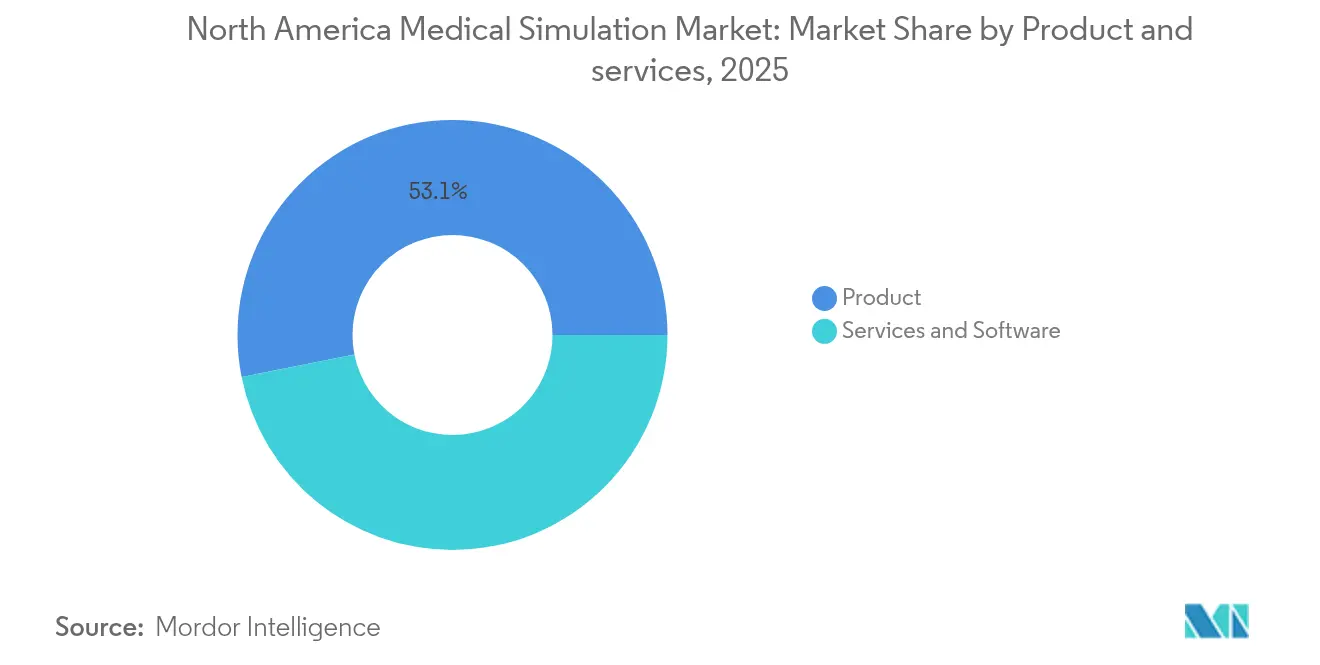

- By products and services, products led with a 53.12% revenue share in 2025; services are expanding at a 13.41% CAGR through 2031.

- By fidelity, low-fidelity systems captured 46.92% of medical simulation market share in 2025, while high-fidelity platforms are projected to grow at 13.68% CAGR to 2031.

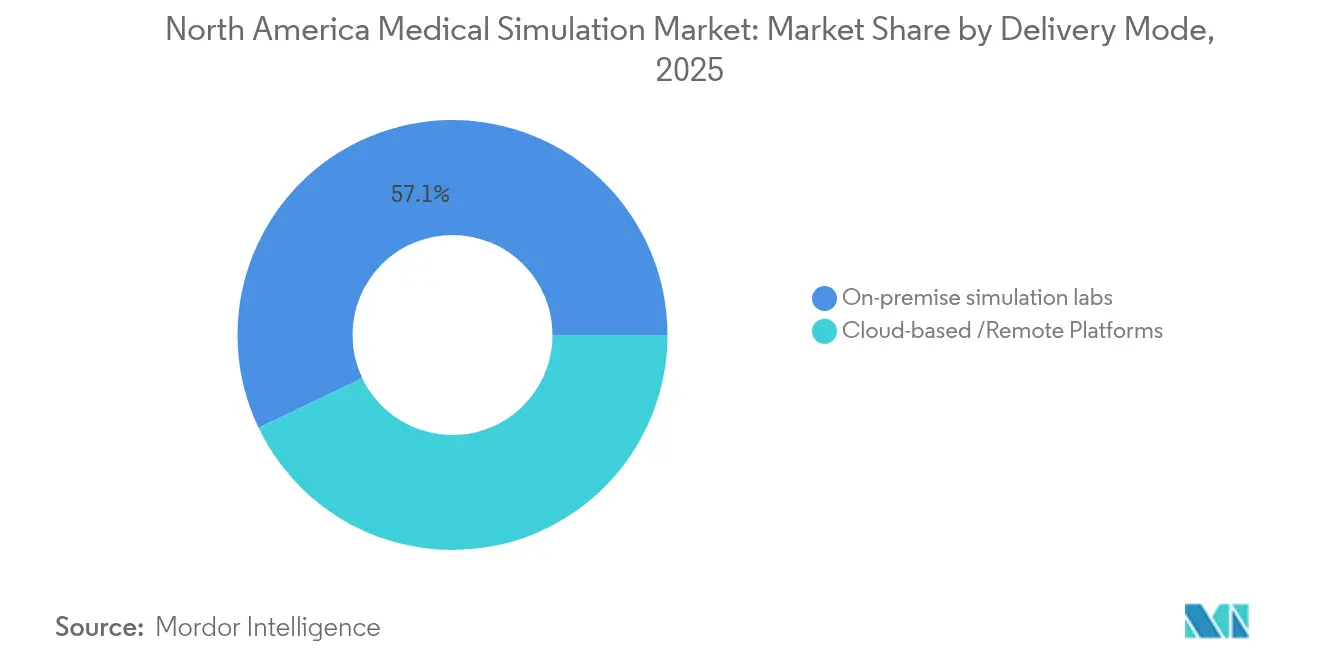

- By delivery mode, on-premise simulation labs accounted for 57.10% of the medical simulation market size in 2025 and cloud-based solutions are advancing at a 14.05% CAGR through 2031.

- By end user, academic and research institutes held 50.20% of revenue in 2025; hospitals and surgical centers are forecast to post the highest CAGR at 14.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Medical Simulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for minimally-invasive-procedure training | +2.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising focus on patient-safety & error-reduction mandates | +2.1% | Global, with strongest enforcement in North America | Short term (≤ 2 years) |

| Adoption of VR/AR hardware breakthroughs in simulators | +1.9% | North America core, spill-over to developed markets | Medium term (2-4 years) |

| Shortage of clinical faculty driving simulation hours | +2.3% | North America & EU primarily | Long term (≥ 4 years) |

| AI-driven adaptive simulation analytics | +1.2% | North America tech hubs, selective global adoption | Long term (≥ 4 years) |

| ESG-linked "zero-harm" corporate training targets | +0.8% | North America & EU corporate healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Minimally-Invasive-Procedure Training

Laparoscopic, robotic, and endoscopic techniques demand psychomotor skills that traditional apprenticeship models cannot deliver at scale. Affordable robotic-surgery interfaces priced near USD 8,400 have widened access to advanced skills practice for resource-constrained schools. Haptic-enabled virtual reality fosters muscle memory and boosts procedural confidence before trainees enter live theaters, and programs using these tools record significant declines in intra-operative error rates. Growth of robotic platforms to offset surgeon shortages further cements simulation as a frontline training modality. The driver adds 2.8 percentage points to forecast CAGR as curricula embed high-repetition, risk-free practice sessions into core learning.

Rising Focus on Patient-Safety & Error-Reduction Mandates

Simulation-based catheter insertion curricula cut 9.95 bloodstream infections per facility each year, saving more than USD 700,000 and delivering a seven-to-one ROI. Such proof reframes simulation from educational overhead to financial imperative. Accrediting bodies like the Joint Commission now require documented competency metrics, which simulation uniquely provides through standardized scenarios and automated scoring. Hospitals leverage these metrics to satisfy value-based reimbursement schemes, shrinking malpractice exposure while elevating care quality.

Adoption of VR/AR Hardware Breakthroughs in Simulators

Apple’s Vision Pro enables mixed-reality overlays that blend virtual patients and real clinical tools, marking a watershed moment for immersive training. Higher-resolution screens, lower latency, and enhanced haptics remove prior fidelity barriers and dampen cybersickness incidence. Collaborations such as GE HealthCare’s alliance with NVIDIA illustrate how AI-enhanced imaging is embedding into simulators to reproduce true-to-life disease variants. The resulting uptick in device purchases and software licensing directly lifts the medical simulation market.

Shortage of Clinical Faculty Driving Simulation Hours

Eighty-four percent of deans cite clerkship shortages, forcing schools to raise simulation quotas. Modern centers let one instructor oversee multiple learners via adaptive scenarios and analytics dashboards, multiplying teaching reach. The COVID-19 disruption validated simulation’s role as curricular backbone rather than ancillary tool. Long-term faculty gaps therefore sustain elevated demand well beyond pandemic pressures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital & maintenance cost of high-fidelity units | -1.8% | Global, particularly affecting smaller institutions | Short term (≤ 2 years) |

| Lack of interoperability standards across simulation platforms | -1.2% | North America & EU primarily | Medium term (2-4 years) |

| Limited faculty training & change-management bandwidth | -0.9% | Global, with varying intensity by region | Long term (≥ 4 years) |

| VR-induced cybersickness impacting learner acceptance | -0.7% | Global, with higher impact in VR-intensive programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital & Maintenance Cost of High-Fidelity Units

Premium patient simulators frequently exceed USD 100,000 per unit, with lifecycle support costs often matching the original purchase price. Community hospitals and small colleges struggle to clear such hurdles when competing priorities include core equipment and staff salaries. Shared regional centers and simulation-as-a-service contracts partially offset the capital pain, but budget sign-offs remain a gating factor and subtract 1.8 percentage points from forecast CAGR.

VR-Induced Cybersickness Impacting Learner Acceptance

Nausea, dizziness, and visual discomfort still affect 45% of VR learners, undermining satisfaction and limiting session lengths. Studies show pre-exposure routines cut nausea by 47% and oculomotor strain by 34%, yet widespread implementation lags. As hardware latency improves and design guidelines mature, the restraint’s impact is expected to fade, but in the near term it trims 0.7 percentage points from overall growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products & Services: Services Accelerate Despite Product Dominance

Products commanded 53.12% of 2025 revenue as the physical backbone of academic and hospital labs. Within that total, interventional and surgical simulators remain the cornerstone, supplemented by task trainers and physiologic manikins. Yet the services category is expanding at a 13.41% CAGR, propelled by institutions favoring turnkey subscriptions over capital outlay. Cloud licensing, curriculum design, and managed-lab services convert episodic purchases into predictable operating budgets, a pivotal shift for the medical simulation market.

Interventional simulator demand mirrors the growth of robotic and laparoscopic procedures, while patient simulators evolve toward wireless, physiology-rich models that integrate with real monitoring devices. Services momentum is most evident in SaaS ultrasound platforms such as 3B Scientific’s e Sono, which illustrates how pay-as-you-go access democratizes advanced training. As recurring revenue rises, the medical simulation industry expands its addressable audience to smaller institutions once priced out of the high-fidelity hardware segment.

By Fidelity: High-Fidelity Solutions Gain Momentum

Low-fidelity tools hold 46.92% of 2025 spend thanks to affordability and quick deployment. Nevertheless, high-fidelity simulators are logging a 13.68% CAGR as empirical studies tie realism to measurable learning gains. The high-fidelity cohort now includes manikins like Gaumard’s HAL S3201 with dynamic lung compliance and drug recognition, bridging the gap between simulation suites and real ICU beds. Institutions justify higher outlays by quantifying error-reduction savings, thereby growing this share of the medical simulation market size.

Medium-fidelity systems remain important for core skills drills, but advanced programs are fast-tracking toward high-immersion experiences that synchronize vitals, imaging, and electronic records. That migration signals a long-run pivot of procurement budgets toward ultra-realism that better prepares clinicians for increasingly complex patient populations.

By Delivery Mode: Cloud Platforms Transform Access Models

On-premise labs still produce 57.10% of 2025 expenditure, yet cloud-delivered content is rising at a 14.05% CAGR. Pandemic disruptions showcased how web-native portals keep curricula uninterrupted, and cloud hosting now underpins adaptive analytics, cohort benchmarking, and cross-campus content sharing. The Scientific World Journal describes architectures like Usalpharma that let quality-assurance trainees access virtual-world exercises from any device, erasing geography as a limiting factor.

Scalability also spares institutions from perpetual hardware refresh cycles, making cloud adoption a central storyline in the medical simulation market. Vendors respond with subscription bundles that package content, analytics, and support into single per-user fees, turning capital planning into operating-expense forecasting.

By End User: Hospitals Accelerate Training Internalization

Academic and research institutes controlled 50.20% of 2025 revenue, reflecting long-standing reliance on simulation for undergraduate and postgraduate programs. Hospitals and surgical centers, however, are growing at 14.27% CAGR as staffing shortages and quality mandates force bedside-level upskilling. Integrated delivery networks embed simulation labs near critical-care units so clinicians can cycle through micro-learning sessions between shifts, weaving practice into daily routines.

Military and defense organizations leverage hyper-realistic casualty models and AI-enhanced incident documentation tools like AutoDoc, underscoring the field’s importance for combat readiness. Device and pharmaceutical firms employ simulation to fast-track product adoption and investigator training, adding further volume to the medical simulation market.

Geography Analysis

The United States remains the engine of regional demand, supported by more than 150 medical schools, extensive residency structures, and federal funding streams. Joint Commission accreditation rules and Veterans Affairs adoption of 40+ VR applications both reinforce simulation’s regulatory anchor. Canada contributes meaningful incremental growth as provincial systems deploy simulation to serve dispersed populations, while Mexico’s private hospitals and medical-tourism hubs adopt high-fidelity suites to attract global patients.

Spill-over effects include cross-border faculty exchanges and shared simulation centers in metropolitan corridors spanning international boundaries. These patterns widen the customer base and lift the overall medical simulation market

Competitive Landscape

Incumbents like CAE Healthcare recently changed ownership as part of Madison Industries’ CAD 311 million acquisition, highlighting a market in realignment. Partnerships—GigXR linking with CAE, GE HealthCare purchasing Intelligent Ultrasound’s AI assets, and Laerdal aligning with the American Hospital Association—signal a shift toward solution ecosystems rather than isolated products. Cloud-native and VR-first entrants challenge hardware heavyweights on agility and price, while established vendors answer with service bundles and AI integration. The market therefore balances fragmentation with consolidation impulses, generating competitive churn that stimulates product innovation without allowing any single firm to dominate the medical simulation market.

North America Medical Simulation Industry Leaders

3D Systems

Canadian Aviation Electronics (CAE) Inc.

Gaumard Scientific

Kyoto Kagaku Co. Ltd

Laerdal Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare partnered with NVIDIA to build AI-driven autonomous X-ray and ultrasound systems for virtual training prior to live deployment

- December 2024: Surgical Science Sweden AB announced plans to acquire Intelligent Ultrasound Group plc, reinforcing its ultrasound simulator portfolio

North America Medical Simulation Market Report Scope

As per the scope of the report, medical simulation is the modern-day methodology for training healthcare professionals through the use of advanced educational technology. Medical simulation is experiential learning that every healthcare professional may need, but cannot be always engaged in during real-life patient care. The market for medical simulation is growing with increasing healthcare facilities. The North America Medical Simulation Market is Segmented by Product and Services (Products (Interventional/Surgical Simulators (Laparoscopic Surgical Simulators, Gynecology Surgical Simulators, Cardiac Surgical Simulators, Arthroscopic Surgical Simulators, and Other Products), Task Trainers, Other Products and Services), Services and Software (Web-based Simulation, Medical Simulation Software, Simulation Training Services, and Other Services and Software)), Technology (High-fidelity, Medium-fidelity, and Low-fidelity Simulators), End User (Academic and Research Institutes and Hospitals), and Geography (United States, Canada, and Mexico). The report offers the value (in USD million) for the above segments.

By Products & Services

| Products | Interventional/Surgical Simulators | Laparoscopic |

| Robotic & Endoscopic | ||

| Orthopaedic | ||

| Patient Simulators | ||

| Task Trainers | ||

| Other Products | ||

| Services & Software | Web-based Simulation | |

| Simulation Software Licences | ||

| Training & Consulting Services |

By Fidelity

| High-fidelity |

| Medium-fidelity |

| Low-fidelity |

By End User

| Academic & Research Institutes |

| Hospitals & Surgical Centres |

| Military & Defence Organisations |

| Medical-device & Pharma Companies |

By Delivery Mode

| On-premise Simulation Labs |

| Cloud-based /Remote Platforms |

By Country

| United States |

| Canada |

| Mexico |

| By Products & Services | Products | Interventional/Surgical Simulators | Laparoscopic |

| Robotic & Endoscopic | |||

| Orthopaedic | |||

| Patient Simulators | |||

| Task Trainers | |||

| Other Products | |||

| Services & Software | Web-based Simulation | ||

| Simulation Software Licences | |||

| Training & Consulting Services | |||

| By Fidelity | High-fidelity | ||

| Medium-fidelity | |||

| Low-fidelity | |||

| By End User | Academic & Research Institutes | ||

| Hospitals & Surgical Centres | |||

| Military & Defence Organisations | |||

| Medical-device & Pharma Companies | |||

| By Delivery Mode | On-premise Simulation Labs | ||

| Cloud-based /Remote Platforms | |||

| By Country | United States | ||

| Canada | |||

| Mexico | |||

Key Questions Answered in the Report

How fast are cloud platforms expanding in the medical simulation market?

Cloud delivery is rising at a 14.05% CAGR as institutions value lower capital burden and pandemic-validated remote access.

What is the typical return on investment for high-fidelity simulation?

A simulation program preventing catheter infections saved over USD 700,000 annually, equating to a 7:1 ROI.

How prevalent is cybersickness in immersive training?

Around 45% of learners report symptoms, though graded exposure protocols reduce nausea by 47% and eye strain by 34%.

Which segment shows the strongest growth momentum?

Services post the steepest 13.41% CAGR, reflecting a shift toward turnkey subscription models.

Why are hospitals ramping up internal simulation centers?

Hospitals aim to offset staffing shortages and comply with competency mandates, driving a 14.27% CAGR within the segment.

What technologies underpin next-generation simulators?

Mixed-reality headsets, AI-driven adaptive analytics, and high-fidelity haptic mannequins form the core of emerging platforms.

Page last updated on: