Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

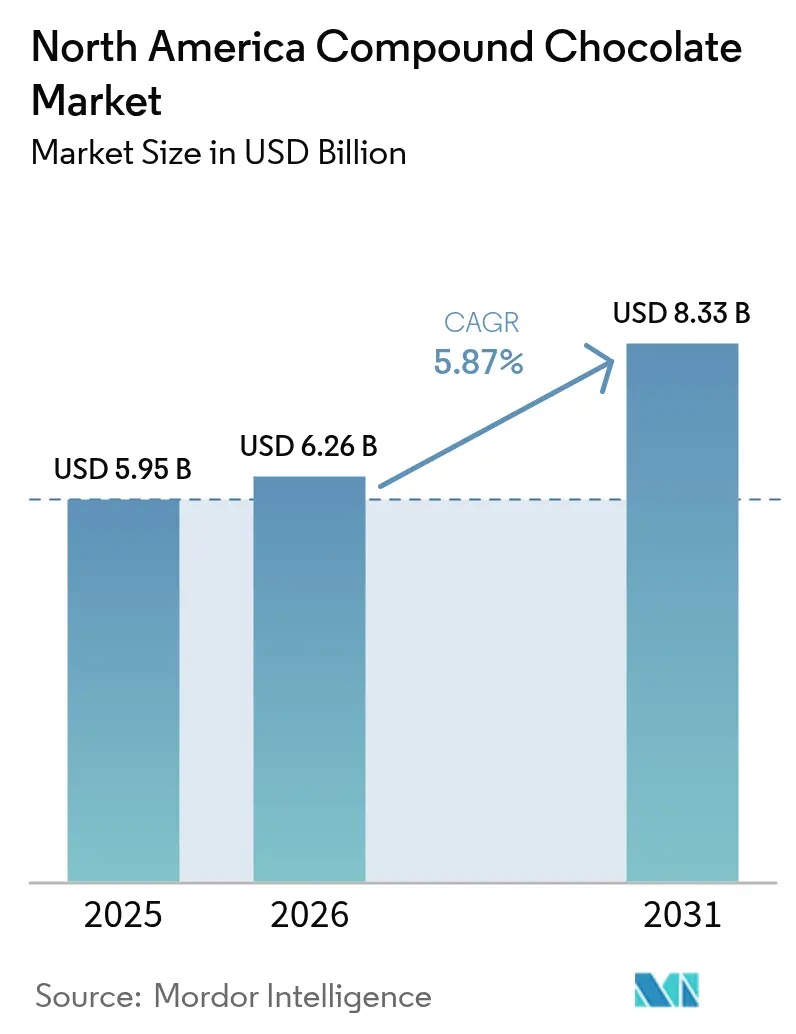

| Base Year Market Size (2025) | USD 5.95 Billion |

| Market Size (2026) | USD 6.26 Billion |

| Market Size (2031) | USD 8.33 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Compound Chocolate Market Analysis by Mordor Intelligence

The North America compound chocolate market size is projected to expand from USD 5.95 billion in 2025 to USD 6.26 billion in 2026 and USD 8.33 billion by 2031, registering a CAGR of 5.87% between 2026 and 2031. This growth trajectory highlights the market's ability to navigate cocoa price fluctuations effectively. The World Bank reported that in 2024, cocoa prices averaged USD 7.33 per kilogram, a significant increase from USD 3.28 [1]Source: World Bank, "World Bank Commodities Price Forecast", thedocs.worldbank.org. Compound chocolate fits that brief, allowing confectioners, bakeries, and ice-cream makers across the region to coat, enrobe, mold, or fill their products without the strict tempering demands of couverture. The scope covers compound chocolate that replaces some or all of the cocoa butter in traditional chocolate with alternate vegetable fats and includes chips, drops, blocks, coatings, spreads, and fillings sold through retail, industrial, and foodservice channels in the United States, Canada, Mexico, and the rest of North America.

Key Report Takeaways

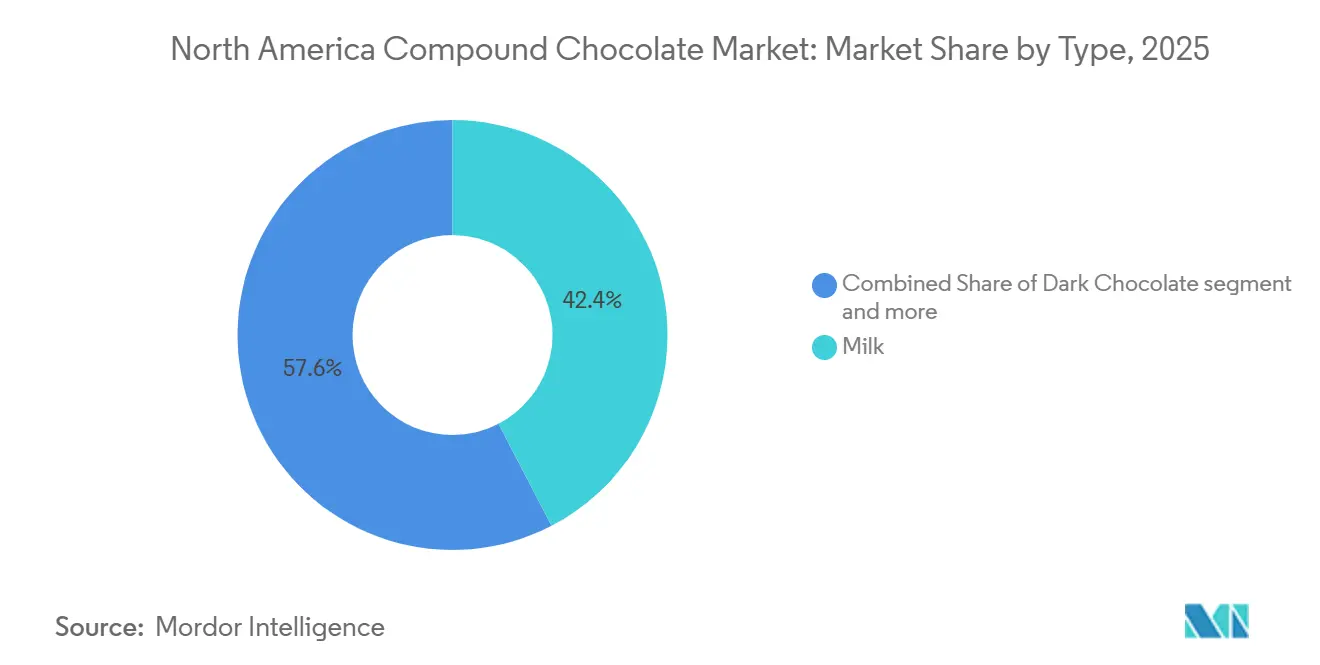

- By type, milk compound chocolate led with 42.38% of the North America compound chocolate market share in 2025, and dark compound chocolate is projected to advance at a 5.92% CAGR through 2031.

- By form, chips, drops, and chunks captured 36.11% of the North America compound chocolate market size in 2025; fillings and spreads are forecast to expand at a 6.03% CAGR from 2026 to 2031.

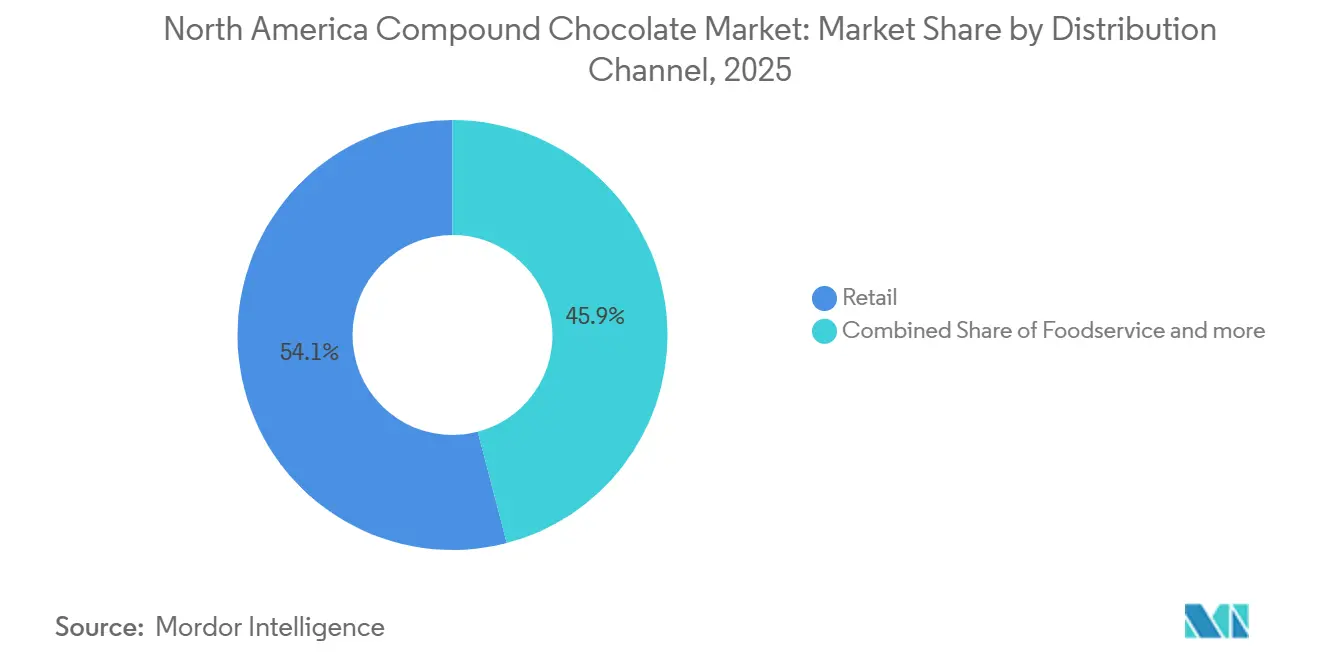

- By distribution channel, retail accounted for 54.04% of the North America compound chocolate market share in 2025, and foodservice is set to record the fastest growth at 6.27% CAGR through 2031.

- By geography, the United States dominated with 78.24% revenue share in 2025, and Mexico is poised to register a 7.04% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Compound Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adaptability and functional advantages for food manufacturers | +1.2% | North America, with the strongest adoption in the United States industrial segments | Medium term (2-4 years) |

| Expansion of the foodservice sector | +0.8% | United States and Canada, concentrated in the QSR and fast casual segments | Short term (≤ 2 years) |

| Increase in home baking and cooking activities | +0.6% | North America, particularly suburban United States and Canadian markets | Short term (≤ 2 years) |

| Developments in flavor innovation and ingredient inclusion | +0.9% | North America, led by premium segments in urban centers | Medium term (2-4 years) |

| Progress in fat crystallization technology | +0.7% | North America, strongest in private label and co-manufacturing | Medium term (2-4 years) |

| Extended Shelf Life Supports Mass Production and Export | +0.5% | North America, concentrated in major manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adaptability and functional advantages for food manufacturers

Food processors are increasingly adopting compound chocolate, driven by the need for manufacturing flexibility. These processors are turning to cost-effective alternatives to traditional chocolate, seeking to eliminate tempering requirements and broaden processing windows. Compound chocolate tolerates temperature fluctuations better than couverture and eliminates the tempering step, cutting production time for molded snacks and enrobed cookies. The lower viscosity of compounds enables thinner yet still glossy coatings that reduce chocolate usage per unit, improving margin without noticeable sensory loss. Manufacturers can also incorporate higher levels of inclusions, such as puffed grains or protein crisps, because the fat phase stabilizes added particulates. That adaptability has become critical as private-label confectioners roll out bite-size pouches across discount chains.

Expansion of the foodservice sector

Despite broader economic pressures, certain segments of the foodservice industry are showing resilience, leading to a targeted demand for compound chocolate applications. The National Restaurant Association reported that in June 2025, the U.S. restaurant industry's performance index reached a score of 100 [2]Source: National Restaurant Association, "Restaurant Performance Index June 2025", restaurant.org. This segmentation is crucial for compound chocolate suppliers. Fast casual operators, for instance, often seek versatile coating and filling solutions. These solutions not only maintain quality over extended hold times but also support the rapid cycles of menu innovation. Data from the US Census Bureau indicate that in 2024, sales from U.S. food service and drinking places reached new heights in 2024 compared to the previous year [3]Source: US Census Bureau, "Food services and drinking place sales in the United States", census.gov. This trend indicates a growing demand for compound chocolate, particularly in the educational foodservice and hospitality sectors.

Increase in home baking and cooking activities

Shifts in consumer baking habits are driving a retail surge in demand for compound chocolate products. These products not only simplify home baking but also promise professional-quality results. What began as a pandemic-driven necessity has evolved into a lasting lifestyle change, with consumers now prioritizing ingredients that streamline the baking process without compromising on quality. During 2025, e-commerce platforms recorded double-digit growth in sales of flavored compound chips as social media tutorials encouraged consumers to marble brownies or decorate cupcakes. Retailers leverage shelf-stable compound chunks in seasonal bake-at-home kits, broadening usage among novice cooks. Flavor houses respond with natural color nano-emulsions that disperse evenly in compound fat matrices, giving hobbyists Instagram-worthy results.

Developments in flavor innovation and ingredient inclusion

Manufacturers are rapidly innovating flavors, using the flexible formulation of compound chocolate to integrate trending ingredients and cater to shifting consumer tastes. Ingredients such as adaptogens, botanicals, and protein enhancements are driving growth in the nutritional balance chocolate sector, with turmeric, reishi, and spirulina at the forefront. The launch of plant-based compound bars by The Functional Chocolate Co., which combines Fair Trade cacao with botanicals supported by clinical research, underscores the market's growing embrace of premium functional formulations. Flavor houses are infusing compound chocolate with botanical extracts, fruit powders, and high-oleic nuts to differentiate bars in premium checkout zones. The neutral base of non-lauric fats supports savory twists such as miso or sea salt, while lauric fats accept high-fat inclusions like peanut butter chips without bloom. R&D teams employ controlled fat crystallization to ensure snap even after inclusions, paving the way for extended product lines through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from pure chocolate products | -1.1% | North America is, strongest in premium retail segments | Medium term (2-4 years) |

| Sustainability and ethical sourcing concerns | -0.8% | North America, concentrated in conscious consumer segments | Long term (≥ 4 years) |

| Volatility in vegetable fat prices | -0.9% | North America, affecting all manufacturing segments | Short term (≤ 2 years) |

| Stringent food labeling regulations | -0.4% | US and Canada, impacting all commercial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from pure chocolate products

As consumers increasingly equate pure chocolate with quality and authenticity, the North America compound chocolate market faces hurdles in its expansion. While premium chocolate segments flourish, everyday chocolate sales remain stagnant, underscoring consumers' readiness to invest in perceived quality. This trend poses challenges for compound chocolate, often viewed as a budget-friendly substitute. Premium retailers highlight bean-to-bar provenance, pushing consumers toward couverture products that feature single-origin cocoa and transparent supply chains. Craft makers fuel perception that compounds are lower quality, forcing mainstream snack brands to defend their formulations. Price gaps narrow whenever cocoa butter prices dip, eroding the compound’s cost edge, and private-label lines may swap back to real chocolate for limited promotional runs.

Fluctuations in vegetable fat prices

In 2024, the World Bank reported an increase in palm oil prices, with the average reaching a nominal USD 963 per metric ton, up from USD 886. This price rise, combined with volatile movements in soybean oil and broader commodity fluctuations, often driven by geopolitical tensions and natural disasters, has created financial challenges for compound chocolate manufacturers. These producers, who depend on palm oil, coconut oil, and other vegetable fats, are facing both margin pressures and supply chain uncertainties. While cocoa butter prices are determined by established futures markets, the pricing of vegetable fats is influenced by various factors, including Indonesia's palm oil export policies, weather conditions in Brazil, and disruptions in sunflower oil production from Ukraine. For example, Cargill's commitment in January 2024 to exclusively use RSPO-certified palm oil not only reduces supply flexibility but may also lead to higher costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Milk Formats Anchor Demand While Dark Records the Fastest Uptick

Milk variants commanded 42.38% of the North America compound chocolate market share in 2025 as mainstream confectionery bars rely on dairy-forward flavor profiles. Manufacturers prefer milk compound for ice-cream toppings because lactose enhances Maillard browning during hardening tunnels, producing an appetizing tan hue without sticking to molds. Meanwhile, the North America compound chocolate market size for dark variants is projected to climb at a 5.92% CAGR from 2026 to 2031, supported by better alignment with plant-based and ketogenic dietary preferences.

Consumers seeking intense cocoa notes gravitate toward sugar-reduced dark compound bites that maintain a melting point near 32°C, convenient for on-the-go snacking. Brand extensions with 70% cocoa solid equivalents employ high-impact cocoa powders, enabling marketers to print “rich dark flavor” claims while keeping ingredient costs predictable. The shift expands the addressable market among health-conscious millennials and boosts volume prospects in specialty retailers. As these trends gain momentum, industry players are keenly observing the evolving preferences, hinting at potential innovations on the horizon. With the growing emphasis on health, the market is poised for further transformations, underscoring the importance of adaptability in brand strategies.

By Form: Chips Dominate Baking Aisles, Fillings Accelerate in Spreads

Chips, drops, and chunks accounted for 36.11% of the North America compound chocolate market size in 2025. This preference is driven by home bakers and commercial cookie plants prioritizing uniform melt and shape retention during baking cycles. Additionally, the rise of gourmet baking at home has led to an increased demand for these specific forms of chocolate. Meanwhile, re-sealable stand-up pouches at mass retailers not only make it easy for consumers to trial new flavors like mint or orange but also ensure the freshness of the product. Furthermore, the convenience of these pouches has led to a surge in impulse purchases, especially among younger consumers. Industrial customers also appreciate the smaller fat bloom risk in chips compared to pure chocolate when stored in unconditioned warehouses, making them a preferred choice for bulk purchases.

Fillings and spreads are projected to log a 6.03% CAGR between 2026 and 2031. This growth is largely attributed to the rising popularity of filled donuts, croissants, and confectionery sandwich cookies on QSR menus. Moreover, as consumers increasingly seek indulgent yet convenient options, the demand for these fillings is set to soar. Producers are also capitalizing on controlled rheology, which enables high-speed injection lines, ensuring efficiency and consistency in production. The North America compound chocolate market share for fillings is poised to widen further. This is due to plant-based pastry chains substituting traditional dairy creams with innovative palm-kernel-based chocolate centers. These centers not only resist syneresis during freezing and thawing but also cater to the growing demand for plant-based alternatives.

By Distribution Channel: Retail Drives Volume, Foodservice Fuels Incremental Growth

In 2025, retail claimed a commanding 54.04% share of North America's compound chocolate market, driven by mass merchandisers and club stores championing family-size baking bags. With a keen focus on at-home experimentation, omni-channel strategies leverage sponsored social media posts, seamlessly guiding shoppers to e-commerce refill packs. Thanks to a shelf-life extending nine months or more, retailers confidently allocate slower-moving flavor SKUs, sidestepping spoilage risks.

Foodservice, on the other hand, is set to experience a vigorous ascent, projected at a 6.27% CAGR through 2031. This growth is fueled by convenience stores adopting high-shear beverage dispensers, effortlessly blending compound flakes into refreshing iced mochas. Meanwhile, fast-casual chains are drizzling compound sauces over breakfast waffles, relishing the cost-effectiveness of these sauces compared to traditional couverture tempering stations. As a result, the compound chocolate market's supply to foodservice distributors in North America is poised to outstrip overall growth, sparking heightened investments from regional fat-processors.

Geography Analysis

The United States accounted for 78.24% of regional revenue in 2025 because national bakery franchises and confectionery multinationals base production domestically. Investment tax credits in several Midwestern states lowered the cost of automated compound molding lines, drawing fresh capacity onshore. Private-label programs at big-box retailers leaned on U.S. suppliers for just-in-time deliveries during holiday peaks, stabilizing demand. As a result, the U.S. solidified its position as the dominant player in North America's confectionery landscape. This trend is expected to continue, with further investments and innovations on the horizon.

Canada remains a steady market where biscuit and snack factories cluster around Ontario and Quebec. Government grants for clean-label product reformulation stimulate trials with sunflower-based compound fats that support allergen-free claims. Although the market is smaller in absolute terms, a favorable product mix of seasonal confectionery gifts pushes average selling prices above the regional mean. With a focus on health-conscious products, Canadian manufacturers are tapping into the growing demand for organic and natural ingredients. This strategic shift not only caters to evolving consumer preferences but also positions Canada as a key player in the North America market.

Mexico is set to register a 7.04% CAGR from 2026 to 2031 as multinational confectioners expand plants in Nuevo León to serve both domestic and export requirements under the United States-Mexico-Canada Agreement. Lower labor and land costs permit manufacturers to run smaller batch sizes, enabling rapid flavor localization. Supermarket chains in central Mexico list value-priced compound bars aimed at working-class households that seek affordable treats in inflationary times. As the middle class expands, there's a noticeable shift towards premium products, indicating a potential market evolution. This duality of catering to both budget-conscious and premium-seeking consumers showcases Mexico's diverse market landscape.

Competitive Landscape

Regional compound chocolate supply is moderately concentrated. Barry Callebaut enhances North America reach by adding a molding line in Illinois that handles ruby-hued compound products tailored for bakery mixes. Cargill introduces a non-hydrogenated palm kernel fraction under its Regal brand that reduces saturated fat by 20% while maintaining gloss, appealing to school snack bidders. Puratos collaborates with Canadian artisanal chocolatiers to launch origin-labeled compound drops for inclusion in bread mixes, reinforcing premium credentials.

Second-tier players such as Blommer Chocolate Company cater to contract manufacturers seeking short lead times on customized color coatings, leveraging proximity to Chicago’s rail hub. Hershey Ingredients and Foodservice rolls out a line of ready-to-use compound fudge bases aimed at doughnut shop chains. Vertical integration across cocoa powder, refinery, and pressing operations helps multinationals stabilize margins against volatile vegetable-fat prices.

Innovation centers in Pennsylvania and Ontario invite bakery customers to test viscosity and chip integrity under actual oven conditions, shortening commercialization cycles. Sustainability commitments around traceable palm supply chains feature prominently in 2026 corporate social-responsibility reports, with Mars and Mondelez publishing dashboards that track progress toward 2027 deforestation-free milestones. Certifications become points of competitive differentiation, especially in Canada’s retail market where front-of-pack eco-labels sway purchase decisions.

North America Compound Chocolate Industry Leaders

-

Fuji Oil Holdings Inc.

-

Puratos Group

-

AAK AB

-

Barry Callebaut

-

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ferrero North America introduced Ferrero Rocher-branded chocolate squares with a crispy chocolate shell, creamy filling, and crunchy hazelnut center. The product was made available in milk hazelnut, dark hazelnut, white hazelnut, caramel hazelnut, and assorted varieties.

- May 2025: Owned by Mondelēz International, Hu introduced new individually wrapped filled chocolate bites. Targeting the on-the-go and post-dinner market, the bites come in three flavors: hazelnut butter, cashew butter, and creamy coconut.

- May 2025: The global chocolate manufacturer, Mars, launched a new selection of Halloween products. The line includes new M&M's milk chocolate, peanut milk chocolate, and peanut butter milk chocolate blends. The seasonal portfolio also featured new variety packs for chocolate and candy brands such as Snickers, Milky Way, and Twix.

- February 2025: Former NFL player Ed McCaffrey and his family launched a line of plant-based, gluten-free, and non-GMO protein bites in the U.S. The company launched with three flavors: Chocolate Chip Cookie Dough, Birthday Cake, and Fudge Brownie, and these protein bites are designed to provide clean energy and are rich in fiber.

North America Compound Chocolate Market Report Scope

The compound chocolate market is defined as cocoa products that incorporate either a cocoa butter substitute (CBS) or a cocoa butter equivalent (CBE). Commonly used vegetable fats include hard fats or semi-solid fats at room temperature, such as coconut oil and palm kernel oil. The North America Compound Chocolate Market is Segmented by Type (Dark, Milk, White, and More), Form (Chips/Drops/Chunks, Slabs and Blocks, Coatings, Fillings and Spreads, and More), Distribution Channel (Retail, Industrial, and Foodservice), and Geography (United States, Canada, and Mexico, and Rest of North America). The Market Forecasts are Given in Terms of Value (USD).

By Type

| Dark |

| Milk |

| White |

| Others |

By Form

| Chips / Drops / Chunks |

| Slabs and Blocks |

| Coatings |

| Fillings and Spreads |

| Others |

By Distribution Channel

| Retail | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Industrial | |

| Foodservice |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Dark | |

| Milk | ||

| White | ||

| Others | ||

| By Form | Chips / Drops / Chunks | |

| Slabs and Blocks | ||

| Coatings | ||

| Fillings and Spreads | ||

| Others | ||

| By Distribution Channel | Retail | Supermarkets / Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Industrial | ||

| Foodservice | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How big will the North America compound chocolate market be by 2031?

It is forecast to reach USD 8.33 billion by 2031, expanding at a 5.87% CAGR from 2026.

Which product type leads sales?

Milk compound chocolate held the largest share at 42.38% of regional revenue in 2025.

Which format is growing fastest?

Fillings and spreads are projected to post a 6.03% CAGR between 2026 and 2031.

Why do foodservice chains prefer compound chocolate?

Compound coatings skip tempering, save prep time and withstand kitchen heat, suiting fast-paced outlets.

Page last updated on: