Market Overview

| Study Period | 2020 - 2031 |

|---|---|

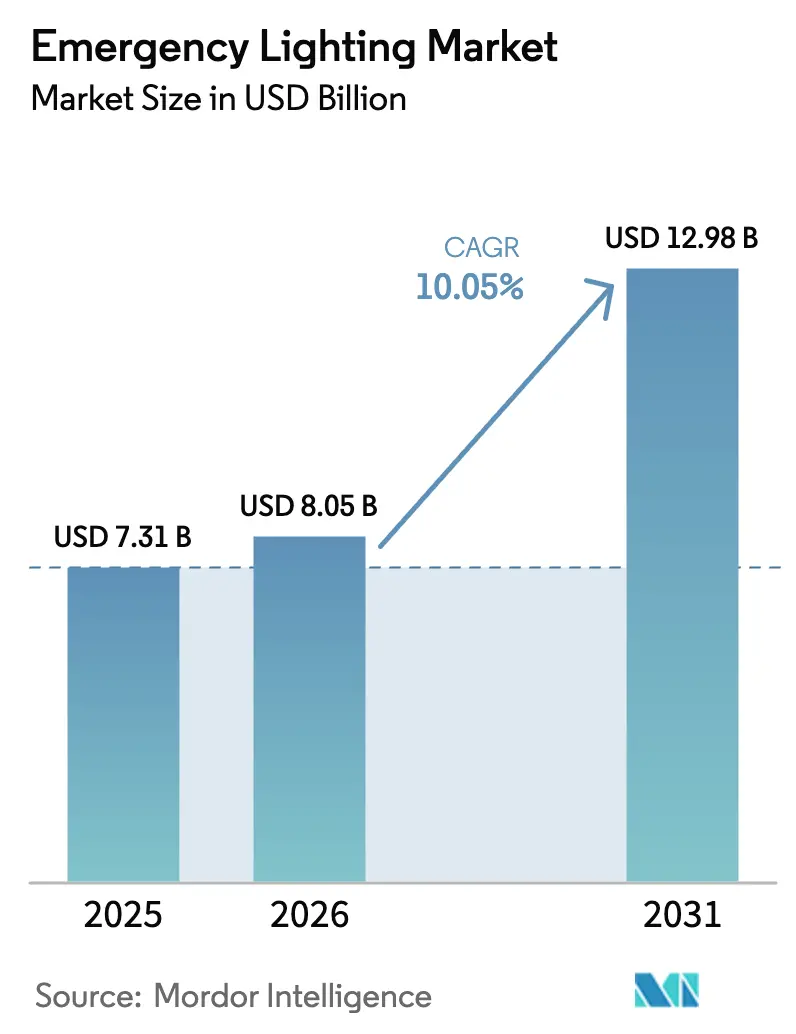

| Market Size (2026) | USD 8.05 Billion |

| Market Size (2031) | USD 12.98 Billion |

| Growth Rate (2026 - 2031) | 10.05% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emergency Lighting Market Analysis by Mordor Intelligence

The emergency lighting market size was valued at USD 7.31 billion in 2025 and estimated to grow from USD 8.05 billion in 2026 to reach USD 12.98 billion by 2031, at a CAGR of 10.05% during the forecast period (2026-2031). The expansion is propelled by stringent life-safety codes, retrofits tied to green-building targets, and smart-lighting technologies that provide automated testing and remote monitoring. LED conversion remains the largest upgrade driver, while wireless connectivity lowers installation costs for existing buildings. Infrastructure investments in tunnels, airports, and data centers further accelerate demand, especially in Asia-Pacific and the Middle East. Competitive dynamics favor brands that pair hardware with cloud-based diagnostics, allowing facility managers to oversee thousands of devices from a single dashboard.[1]International Code Council, “Fire Code, 2024 (IFC 2024),” UpCodes, up.codes

Key Report Takeaways

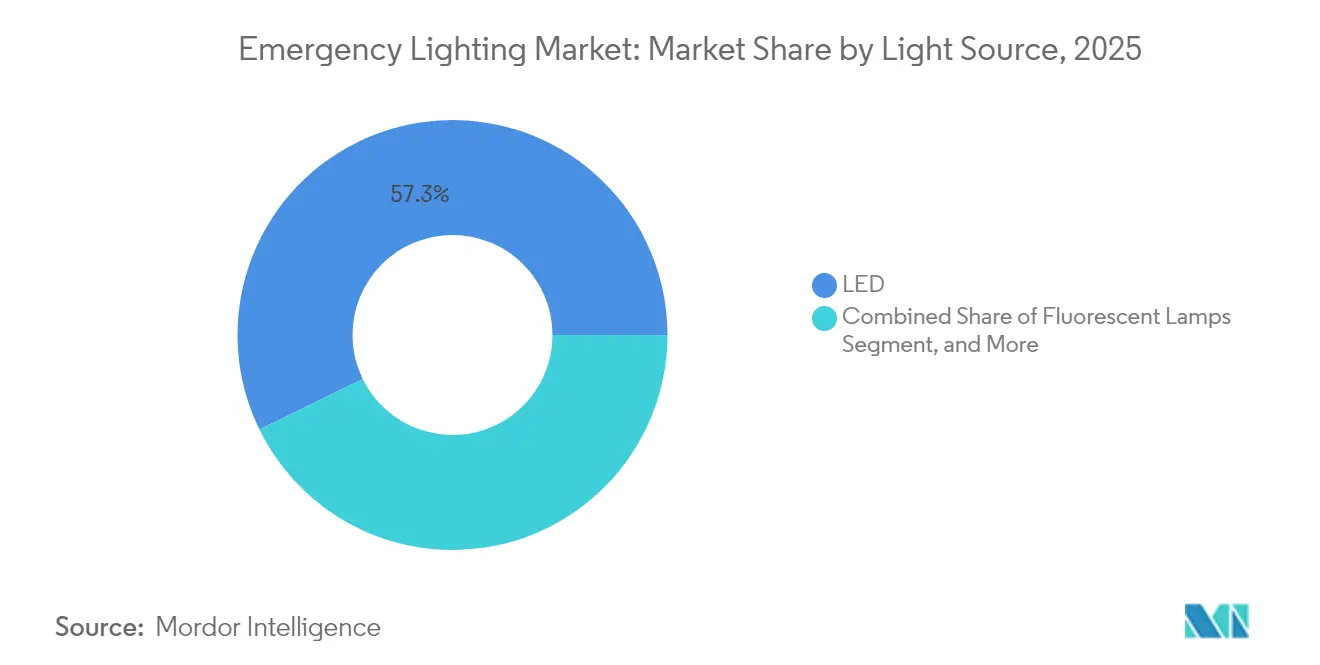

- By light source, LED held 57.25% of emergency lighting market share in 2025; wireless/IoT-enabled systems are expected to expand at a 13.02% CAGR to 2031.

- By power system, self-contained solutions accounted for 65.05% share of the emergency lighting market size in 2025, while centralized battery systems advance at an 11.12% CAGR through 2031.

- By installation type, surface-mounted units dominated with 46.12% revenue share in 2025; recessed fixtures are projected to grow at a 10.18% CAGR to 2031.

- By communication, wired products retained 81.55% share in 2025, but wireless alternatives will record the fastest growth at 13.02% through 2031.

- By end user, commercial offices led with 27.65% of emergency lighting market share in 2025; public infrastructure segments are forecast to post an 11.33% CAGR through 2031.

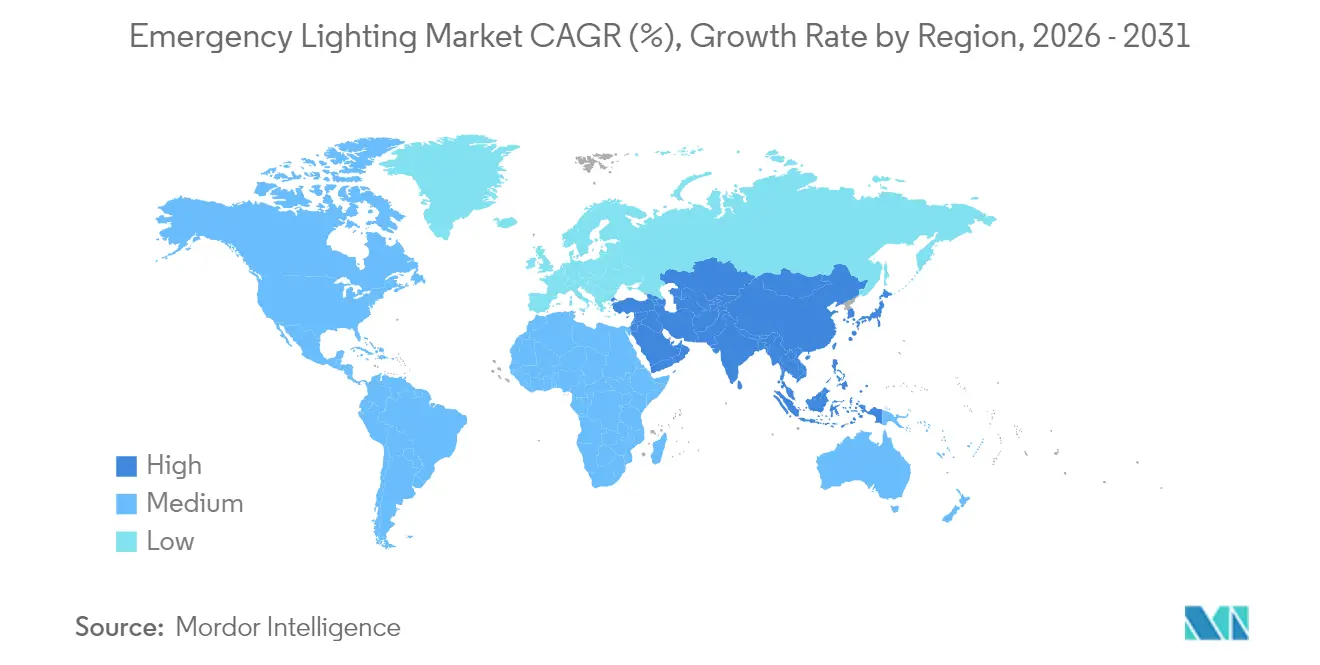

- By geography, Asia-Pacific captured 33.85% of the emergency lighting market in 2025; the Middle East and Africa region is poised for the highest 10.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Emergency Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart LED retrofits across European public infrastructure | +1.8% | Europe → North America | Medium term (2-4 years) |

| Stricter U.S. IBC/NFPA 101 mandates for high-rises | +2.1% | North America → APAC | Short term (≤ 2 years) |

| Urban rail-tunnel build-outs in China and India | +1.5% | Asia-Pacific | Long term (≥ 4 years) |

| Data-center boom adopting centralized battery systems | +1.9% | North America & EU → APAC | Medium term (2-4 years) |

| ESG-linked LED exit-sign upgrades | +1.2% | Global developed markets | Long term (≥ 4 years) |

| Offshore platform investments in the Middle East | +0.7% | Middle East, North Sea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart LED retrofits across European public infrastructure

European municipalities are replacing fluorescent fixtures with networked LED luminaires that cut energy consumption by up to 50% while simplifying compliance reporting. The EU Green Deal pushes public buildings to reach carbon neutrality by 2030, and connected fixtures automatically send test logs to facility dashboards, trimming maintenance labor. Acuity Brands’ STAR Gateway illustrates how automated audits meet EN 50172 requirements, making smart LEDs the default choice for rail stations, schools, and government offices.[2]Acuity Brands, “Emergency Lighting Testing with STAR,” acuitybrands.com

Stricter U.S. IBC/NFPA 101 mandates for high-rises

The 2024 code cycle raises minimum egress illuminance to 1.07 lux for 90 minutes and cuts activation time to 10 seconds. Many legacy nickel-cadmium units cannot pass updated UL 924 tests that now require a “normal-power present” signal, compelling owners to replace equipment ahead of recertification deadlines. Federal facilities add another layer of pressure by specifying LED systems with integrated controls to meet GSA energy targets.[3]U.S. General Services Administration, “LED Lighting and Controls Guidance for Federal Buildings,” gsa.gov

Urban rail-tunnel build-outs in China and India

Metro systems in Beijing, Mumbai, and new Tier-2 cities demand IP67-rated, vibration-resistant luminaires capable of operating during single-point failures. Funding from multilaterals such as the Asian Development Bank underpins dozens of projects, each requiring kilometers of emergency fixtures that interface with SCADA platforms.[4]Asian Development Bank, “ADB to Help Nepal Upgrade Electricity Transmission and Distribution Infrastructure,” adb.org Manufacturers with turnkey tunnel packages and regional testing expertise gain a clear edge.

Data-center boom adopting centralized battery systems

Hyperscale operators favor central inverters tied to the building-wide UPS so that one bank of batteries can serve thousands of heads. Eaton’s acquisition of Fibrebond gives it prefab enclosures that combine power conversion, controls, and fire suppression, shortening deployment schedules for cloud campuses. The trend also spurs interest in lithium-ion alternatives such as hydrogen fuel cells, which demand luminaires that ride through fuel-cell “warm-up” phases.[5]Eaton, “Eaton Emergency Lighting UPS,” eaton.com

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium-ion fire-safety concerns in healthcare | -1.4% | Global developed markets | Short term (≤ 2 years) |

| Supply-chain crunch for IC drivers & optics | -1.1% | Global, notably APAC | Medium term (2-4 years) |

| Fragmented standards across ASEAN | -0.8% | ASEAN emerging | Long term (≥ 4 years) |

| High install/test cost for wireless systems | -0.9% | Global price-sensitive | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lithium-ion fire-safety concerns in healthcare facilities

Hospitals are delaying lithium-ion rollouts after thermal-runaway incidents that led to ward evacuations. NFPA is drafting NFPA 800 to govern on-site storage, but until finalized, many health networks stay with sealed lead-acid or nickel-metal hydride packs despite shorter life. Proposed U.S. legislation to codify national battery safety standards adds further uncertainty.

Supply-chain crunch for IC drivers and optics

Component shortages that began in 2023 still linger, particularly for RF chipsets used in addressable luminaires. Vendors have re-engineered boards to accept multi-source parts, but re-qualification with UL and CE adds cost and delays. Limited availability keeps wireless SKUs on allocation, slowing the highest-growth slice of the emergency lighting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Light Source: LED Dominance Faces Technology Transition

LED devices controlled 57.25% of emergency lighting market share in 2025, and the segment is set to advance at a 9.54% CAGR through 2031. Fluorescent tubes linger in older buildings, yet rising energy tariffs and lamp bans speed replacement schedules. Niche high-intensity discharge units remain in petrochemical zones where 10 kV surge immunity takes precedence over efficacy.

Smart diodes now embed sensors, memory, and selectable color temperatures, exemplified by the Green Creative Universal CCT Select tube, which helps specifiers tailor glare levels without swapping hardware. This convergence of intelligence with illumination keeps LED systems as the anchor of the emergency lighting market, even as wireless protocols reshape product line roadmaps.

By Power System: Centralized Systems Gain Infrastructure Traction

Self-contained packs represented 65.05% of emergency lighting market size in 2025, thanks to straightforward installation and unitized maintenance. Large venues, however, prefer central banks to cut room-by-room battery checks. Data centers exemplify the shift, with centralized racks ensuring all fixtures receive conditioned power and firmware updates from a single hub.

Eaton’s inverter platforms, soon incorporating Exertherm thermal analytics, highlight how predictive monitoring reduces unscheduled downtime. Lithium-ion strings deliver long cycle life, yet hospitals and airports still specify VRLA in critical zones until regulatory clarity improves. The split between autonomy and central command will define procurement choices over the forecast horizon.

By Installation Type: Recessed Systems Drive Aesthetic Integration

Surface-mounted housings remained the go-to retrofit option, but architects increasingly select recessed troffers that sit flush with modern ceiling grids. Growth of 10.18% CAGR stems from high-end offices, hotels, and museums where design language prizes unobtrusive hardware.

Wireless mesh controls allow recessed heads to self-commission, avoiding new conduit pulls. As building owners chase LEED v5 credits tied to lighting power density, recessed LED kits that double as both normal and emergency circuits reduce fixture counts, strengthening their value proposition across the emergency lighting market.

By Product: Combo Units Lead Innovation Integration

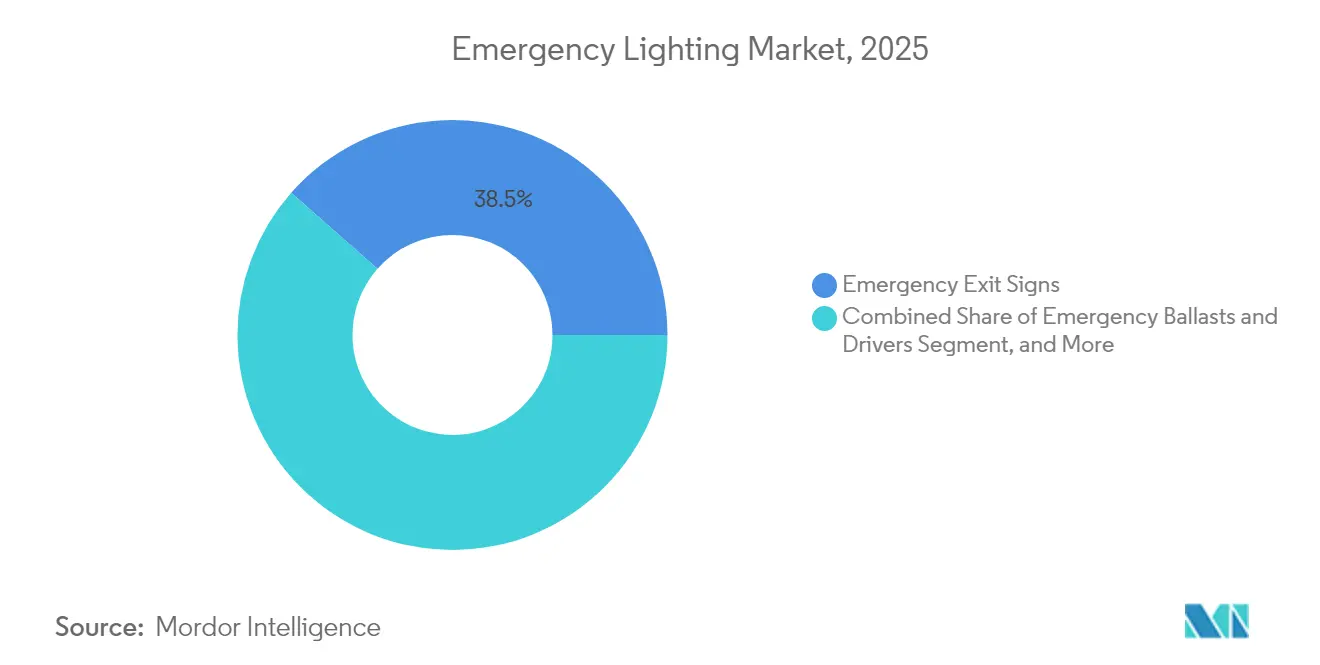

Exit signs alone delivered 38.50% of 2025 revenues, yet combo units-packing both pictograms and twin floodlights-are edging ahead with an 11.22% growth rate. They slash wiring steps and shrink SKU counts for contractors. Addressable variants auto-test each circuit, logging results for inspectors and trimming walkthrough time.

Stand-alone luminaires still shine in warehouses where 1,000 lumen beams must clear tall racks. In contrast, emergency ballasts attract projects that cannot justify fixture swaps, letting owners insert a driver into an existing troffer to meet code. The shift toward “all-in-one” hardware underscores how feature density is becoming the new battleground in the emergency lighting market.

By Communication: Wireless Systems Transform Facility Management

Hard-wired networks made up 81.55% of shipments during 2025, but wireless LoRaWAN, BLE, and proprietary RF are now the focal point for R&D. A 13.02% CAGR through 2031 is forecast as universities, housing authorities, and airports approve RF links that cut labor hours by 30%.

The landmark deployment of 10,000 LoRa-equipped units in Singapore public housing proves long-range, low-power tech can manage life-safety devices at city scale. ABB’s Naveo Pro mobile app lets technicians verify discharge tests from a smartphone, signaling how digital workflows will dominate procurement discussions within the emergency lighting market.

By End User: Public Infrastructure Drives Highest Growth

Commercial offices accounted for 27.65% of global revenues in 2025, driven by dense urban high-rises. Yet airports, tunnels, and rail platforms form the fastest-moving slice, supported by sovereign stimulus across Asia-Pacific. Here, photometric uniformity and vibration resistance weigh more heavily than aesthetics, opening space for ruggedized SKUs.

Healthcare adoption remains tempered by battery-fire fears, while warehouses seek high-candela beams for rack clarity. Residential smart-home packages start to feature micro-inverters feeding ceiling cans, hinting at future consumer interest once code bodies address single-family requirements.

Geography Analysis

Asia-Pacific, with a 33.85% stake in the emergency lighting market, benefits from megaprojects such as Mumbai Metro Line 3 and Beijing Sub-Center Tunnel. Regional governments use concessional loans from institutions like ADB to electrify outlying provinces, ensuring every new substation or rail spur specifies compliant luminaires. Semiconductor shortages make scheduling tricky, but local PCB houses in Shenzhen and Penang shorten lead times for domestic vendors.

The Middle East and Africa will register a 10.74% CAGR through 2031 as Qatar extends LNG export hubs and Saudi Vision 2030 accelerates tourism corridors. Offshore rigs in the Gulf demand copper-free aluminum bodies that survive salt-spray and 60 °C highs. Chalmit-branded Protecta X fixtures in North Sea fields validate 120,000-hour lifespans, encouraging NOCs to budget for premium solutions.

North America and Europe offer steady replacement cycles. U.S. code revisions now force high-rise landlords to upgrade within recertification windows, bolstering retrofit volumes. Europe’s Renovation Wave funnels grants toward public-sector LED swaps, with Germany underwriting smart controls that shave carbon footprints ahead of 2030 targets. Mature buyers favor vendors that bundle analytics dashboards with hardware, elevating software maintenance contracts as a vital slice of the emergency lighting market.

Regulatory Landscape

Emergency lighting demand is anchored in life-safety codes that require minimum egress performance and documented testing. In Europe, the 2024 standards cycle updated core requirements with EN 1838:2024 (approved May 19, 2024) for emergency lighting performance and EN 50172:2024 (approved May 27, 2024) for emergency escape lighting systems, reinforcing photometric and system-level compliance practices used across public buildings and transport infrastructure.

In the United Kingdom, BS 5266-1:2025 came into effect on October 31, 2025, replacing the 2016 edition and tightening expectations around commissioning documentation and periodic verification. This increases the value of self-testing and centrally logged records for large estates. In North America, the ANSI/UL 924 revision dated February 12, 2025 introduced new marking and evaluation provisions, with a mandatory compliance date of February 12, 2027, affecting product redesign, certification scheduling, and portfolio transitions for manufacturers selling into UL-listed channels.

Value Chain Analysis

The emergency lighting value chain spans LED packages and optics, driver ICs and control electronics, batteries and battery management, luminaire mechanicals, and system software for testing, reporting, and monitoring. Component suppliers feed module makers (light engines, drivers, BMS), which then supply OEMs and brand owners that design, assemble, certify, and sell exit signs, luminaires, combo units, and monitoring gateways. Installation is typically executed by electrical contractors, with ongoing inspection and maintenance handled by facility teams or service partners.

Safety-critical certification and electronics availability shape downstream lead times because changes to drivers, wireless chipsets, or battery packs can trigger re-qualification for regulated SKUs. The market context highlights ongoing tightness in specialized IC drivers and optics since 2023, which has encouraged OEMs to pursue multi-sourcing, re-engineered boards, and closer alignment with test houses and standards requirements (for example, UL 924 in North America and EN 50172/EN 1838 in Europe). On the go-to-market side, vendors increasingly pair hardware with cloud or on-premise dashboards for automated test logs and portfolio health, shifting value capture toward software-enabled service contracts and multi-site compliance reporting.

Competitive Landscape

Market rivalry centers on technology layers more than manufacturing scale. Acuity Brands links up to 20,000 heads through its STAR Gateway, providing cloud reporting that eases NFPA audits. Eaton folds Fibrebond’s prefabricated shelters into its offer, giving hyperscale data-center clients a single-vendor path from UPS to luminaire. Signify reorganized into vertical business units, allowing its connected-lighting arm to court transport authorities separately from consumer channels.

Private-equity exits underscore structural shifts: Hubbell sold Progress Lighting to Kingswood Capital and kept only hazardous-area brand Chalmit, reflecting a tilt toward specialized niches. Smaller European firms carve space in tunnel or maritime segments where EN 60598-2-22 tests require custom optics. The top five vendors collectively hold under 30% of global revenue, keeping the emergency lighting market moderately fragmented and innovation-driven.

Emergency Lighting Industry Leaders

Emerson Electric Co.

Schneider Electric

Hubbell Lighting Inc.

Legrand SA

Eaton Corp. plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standards updates are creating a compliance-driven replacement and upgrade pathway that favors automated testing, auditable records, and tighter commissioning verification. BS 5266-1:2025 taking effect on October 31, 2025 in the UK, alongside EN 1838:2024 and EN 50172:2024 approved in May 2024, increases emphasis on documented photometric verification and repeatable inspection outcomes. This aligns with connected gateways and self-test features used to generate digital test logs for facility managers.

Interoperability and data visibility remain a practical whitespace area as emergency lighting systems move beyond standalone luminaires into building-wide monitoring networks. DALI-2 (IEC 62386) and D4i extensions for energy and diagnostics data provide a standards-based route to connect emergency lighting into broader building management workflows, while wireless platforms address retrofit constraints where new wiring is costly or disruptive. Beyond buildings, smart-city programs create adjacent demand signals for networked lighting and multi-function poles, supported by examples such as Seoul districts rolling out smart poles that integrate safety and communications functions and Andhra Pradesh implementing an IoT-enabled smart street lighting project at scale. These programs support opportunities for vendors that can package compliant emergency-capable luminaires with centralized monitoring and maintenance-ready data outputs.

Recent Industry Developments

- July 2026: Schneider Electric announced a definitive agreement to acquire Cognite Holding B.V., an industrial data and AI software provider, to integrate capabilities into its Industrial Automation business. The move strengthens Schneider Electric's software stack that can support data-driven operations across critical infrastructure, aligning with the market shift toward connected, monitored life-safety systems and centralized compliance reporting.

- March 2025: Eaton agreed to acquire Fibrebond Corporation for USD 1.4 billion, adding modular power enclosures aimed at cloud and colocation data centers. The deal supports faster deployment of centralized power and monitored infrastructure, reinforcing demand for emergency lighting architectures that integrate with UPS-backed, facility-wide backup strategies common in hyperscale builds.

- March 2024: Eaton unveiled its Building Safety Management System (BSMS) digital ecosystem and the DualSmart connected emergency lighting system at Light + Building 2024. The launch expanded software-led lifecycle management for emergency luminaires, reinforcing a competitive shift from standalone fixtures toward platforms that automate testing, streamline maintenance, and improve audit readiness.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the emergency lighting market counts revenues from permanently installed luminaires, exit signs, power packs, and monitoring modules that automatically switch to battery or generator supply during a mains failure, across buildings and public infrastructure.

Scope exclusions: Portable flashlights, vehicle-related lighting, and short-term rental or temporary lighting units are not included.

Segmentation Overview

- By Light Source

- LED

- Fluorescent Lamps

- High-Intensity Discharge (HID)

- Induction and Others

- By Power System

- Self-Contained/Battery-Backup

- Central Battery (UPS)

- Hybrid/Distributed

- By Installation Type

- Surface-Mounted

- Recessed

- Suspended

- Portable

- By Product

- Emergency Exit Signs

- Stand-alone Emergency Luminaires

- Combo Units

- Emergency Ballasts and Drivers

- By Communication

- Wired

- Wireless/IoT-Enabled

- By End-user

- Commercial - Offices

- Commercial - Hospitality and Retail

- Industrial -Manufacturing and Warehouses

- Oil and Gas/Mining

- Residential

- Public Infrastructure (Airports, Tunnels, Rail)

- Healthcare Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building a fact base on building activity and safety compliance, since emergency lighting demand is linked to occupancy requirements and retrofit cycles. We leaned on public source types such as International Code Council publications, NFPA code overviews and public notes, IEA lighting and electricity indicators, and UN Comtrade trade statistics for lighting equipment (HS-level cues).

To keep pricing and technology context realistic, we also used sources such as U.S. DOE materials on solid-state lighting, government procurement portals for tender language patterns, and peer-reviewed papers on battery chemistry performance and LED reliability. Company annual reports, investor decks, and reputable press were used to cross-check product mix and regional exposure, and a paid subscription for company financials and news helped verify revenue baselines and ownership changes. This list is illustrative, and many other public documents were reviewed to collect, validate, and clarify the inputs.

Primary Interviews and Surveys

Primary discussions were used to pressure-test adoption drivers such as code enforcement intensity, retrofit versus new-build split, and the pace of LED and self-testing feature upgrades, which then feed into demand assumptions. We spoke with stakeholders across manufacturing, distribution, installation, and facility operations so pricing, channel margins, and replacement cycles could be checked across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 41% |

| Mid tier: 52% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 17% | Managers: 52% | Americas: 26% |

Market-Sizing & Forecasting

The core model uses a top-down build that reconstructs demand from the active building stock and construction pipeline, then adjusts for the portion of floor space and occupancies that must comply with emergency egress and backup-lighting rules. The totals are corroborated with selective bottom-up checks, like sampled average selling price by product type multiplied by implied unit demand, plus channel checks on typical project bill of materials.

Inputs were chosen because they can be refreshed and explained in a repeatable way, even when country-level data quality varies. Key examples include non-residential construction spending and completions, retrofit intensity driven by LED conversion and automated testing requirements, replacement cycles linked to battery life and test frequency, average project density of exit signs and luminaires per facility type, and regional mix shifts driven by infrastructure additions. For forecasting, scenario analysis was used around construction cycles and retrofit catch-up, and the final growth path was aligned with expert consensus on regulation-led upgrades and pricing progression. Where bottom-up visibility was limited for smaller markets, we used proxy installation rates from similar code regimes and then normalized results against trade flows and construction signals.

Data Validation & Update Cycle

Outputs are validated through several checkpoints so the final number is not driven by a single data series. We compare the model against independent signals like lighting-category trade movements, construction indicators, and price direction from public tenders, then investigate outliers before sign-off.

Assumptions are reviewed in steps, and follow-up outreach is triggered when a region shows a sharp shift in mix, pricing, or growth that is not supported by the supporting indicators. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery review is completed so clients receive the latest updated view.

Mordor Intelligence's Emergency Lighting Market Size Measured Against Other Published Estimates

Published market sizes for emergency lighting do not always match because each publisher chooses its own boundaries, year labeling, and pricing basis, and these choices change the final totals. Differences also come from how retrofit demand is treated and whether the model leans more on construction activity or on product shipment and pricing assumptions.

The benchmark table shows a spread that is mainly explained by what is counted as emergency lighting revenue and when it is recognized. In Mordor Intelligence's model, the scope is limited to permanently installed luminaires, exit signs, power packs, and monitoring modules, while portable and vehicle-related lighting are excluded, and values are tracked at manufacturer selling prices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.05 B (2026) | |

| Global Consultancy A | USD 7.82 B (2025) | Uses a different base year and, based on its scope wording, may blend adjacent smart-lighting and component categories, which can shift what is counted as emergency lighting hardware versus related controls or services. |

| Industry Publisher B | USD 8.45 B (2025) | Applies a broader system view with multiple product and battery types, and the higher number can also reflect different pricing points, currency timing, and a more aggressive upgrade curve for LED and central-power deployments. |

Reading the three figures together, the gap is not only about growth expectations, it is also about consistent scoping and year alignment. By tying the estimate to clear building-led demand drivers and then checking it with practical pricing and mix assumptions, we arrive at a market value that can be traced and repeated as new construction and retrofit signals move.

Key Questions Answered in the Report

What is the current size of the emergency lighting market?

The market is valued at USD 8.05 billion in 2026 and is projected to reach USD 12.98 billion by 2031.

Which region dominates the emergency lighting market?

Asia-Pacific holds the largest 33.85% regional share, thanks to aggressive infrastructure development.

What technology segment is growing the fastest?

Wireless/IoT-enabled emergency lighting is forecast to grow at a 13.02% CAGR through 2031, the highest among all segments.

Why are healthcare facilities cautious about lithium-ion batteries?

Documented thermal-runaway incidents and pending NFPA 800 guidelines have raised fire-safety concerns, slowing adoption in hospitals

How do new U.S. building codes affect market demand?

The 2024 IBC and NFPA 101 updates require quicker activation and higher illuminance, prompting immediate retrofits of non-compliant systems.

What role do data centers play in future demand?

Rapid data-center construction favors centralized battery systems with remote diagnostics, adding a positive 1.9% impact to overall CAGR.

Page last updated on: