Non-Invasive Intracranial Pressure Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

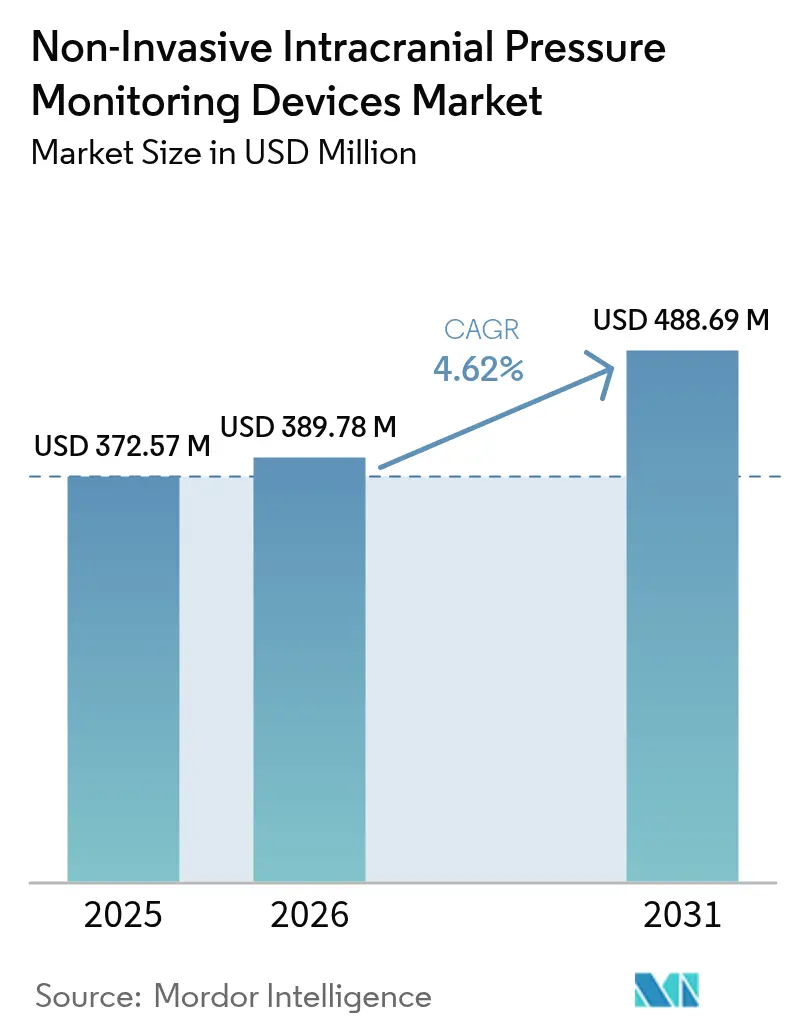

| Market Size (2026) | USD 389.78 Million |

| Market Size (2031) | USD 488.69 Million |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

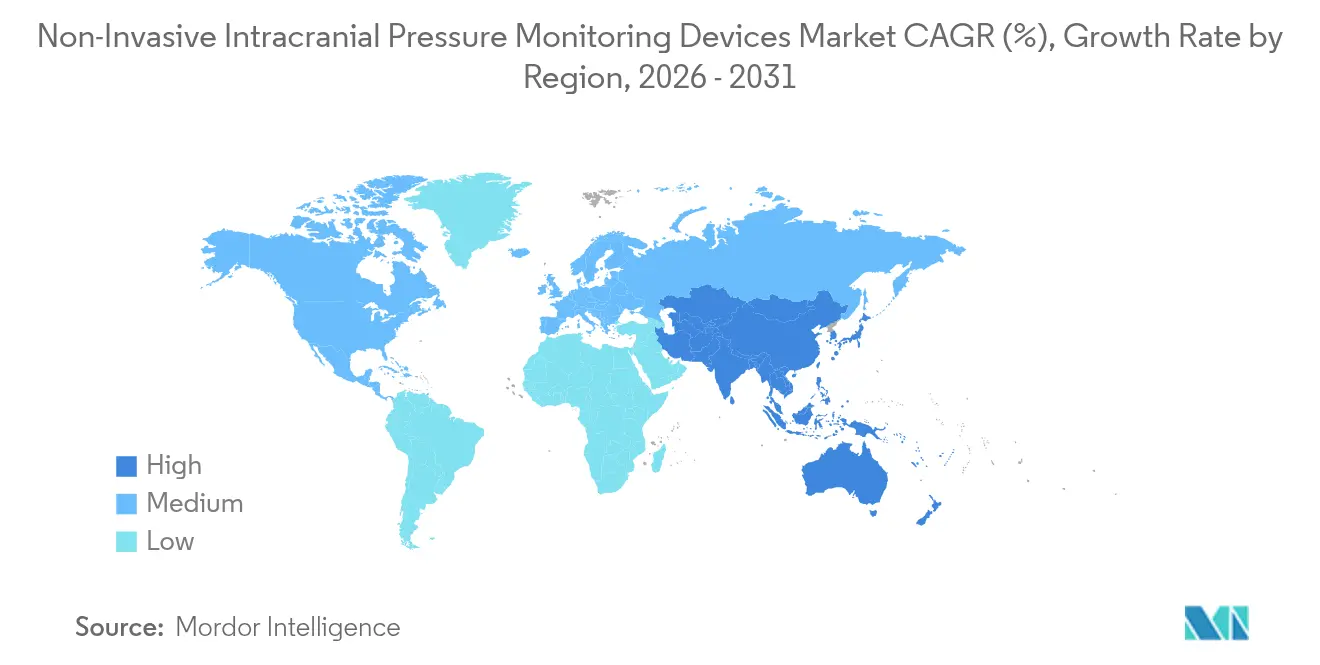

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Invasive Intracranial Pressure Monitoring Devices Market Analysis by Mordor Intelligence

The non-invasive intracranial pressure monitoring devices market size was valued at USD 372.57 million in 2025 and estimated to grow from USD 389.78 million in 2026 to reach USD 488.69 million by 2031, at a CAGR of 4.62% during the forecast period (2026-2031). Incremental expansion reflects the shift from exploratory prototypes to clinically validated solutions that match invasive accuracy while avoiding surgical risks, lowering infection rates and shortening hospital stays. Military research grants, FDA breakthrough-device designations and expanding evidence for AI-enabled waveform analytics are accelerating clinical adoption. Hospitals remain the chief customers, yet rapid uptake in emergency departments, ambulatory centers and home-care programs signals a move toward decentralized monitoring. Asia-Pacific’s demographic pressure and infrastructure build-out underpin the fastest regional CAGR, whereas North America leverages reimbursement frameworks and defense spending to protect its leadership position.

Key Report Takeaways

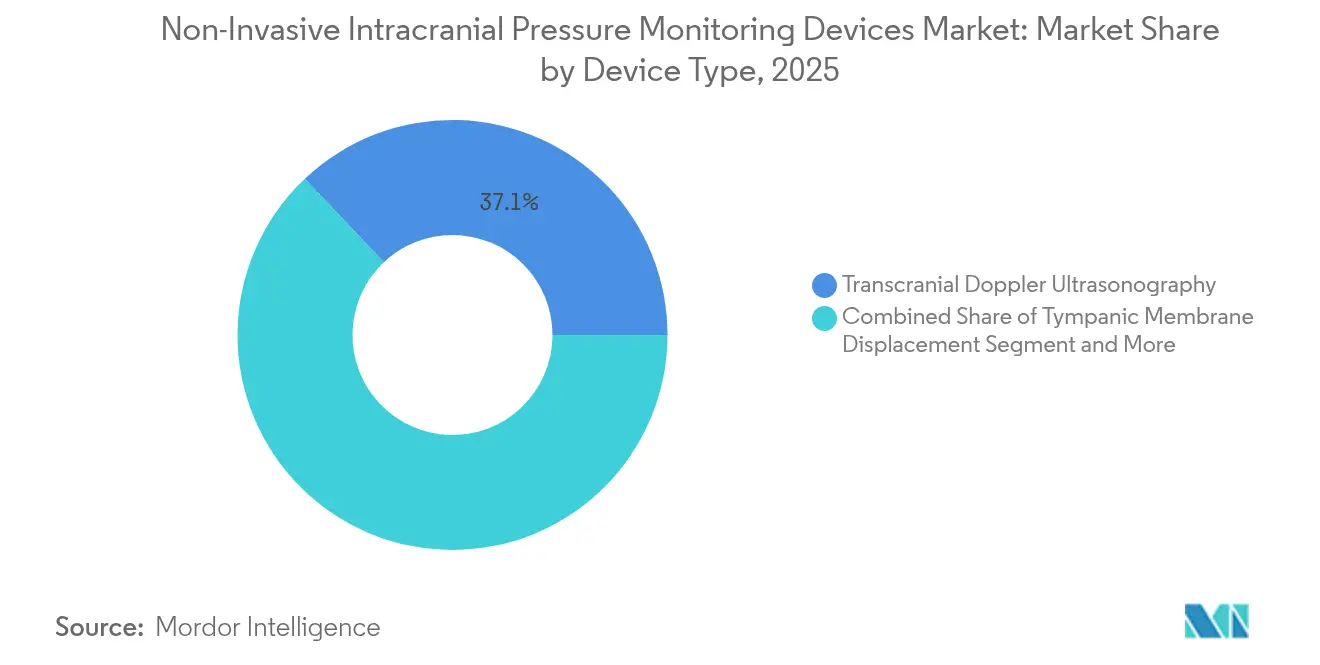

- By device type, transcranial Doppler ultrasonography led with 37.05% of the non-invasive intracranial pressure monitoring devices market share in 2025; infrared pupillometry is projected to advance at an 11.05% CAGR through 2031.

- By application, traumatic brain injury accounted for a 39.93% slice of the non-invasive intracranial pressure monitoring devices market size in 2025; stroke monitoring is expanding at a 9.37% CAGR to 2031.

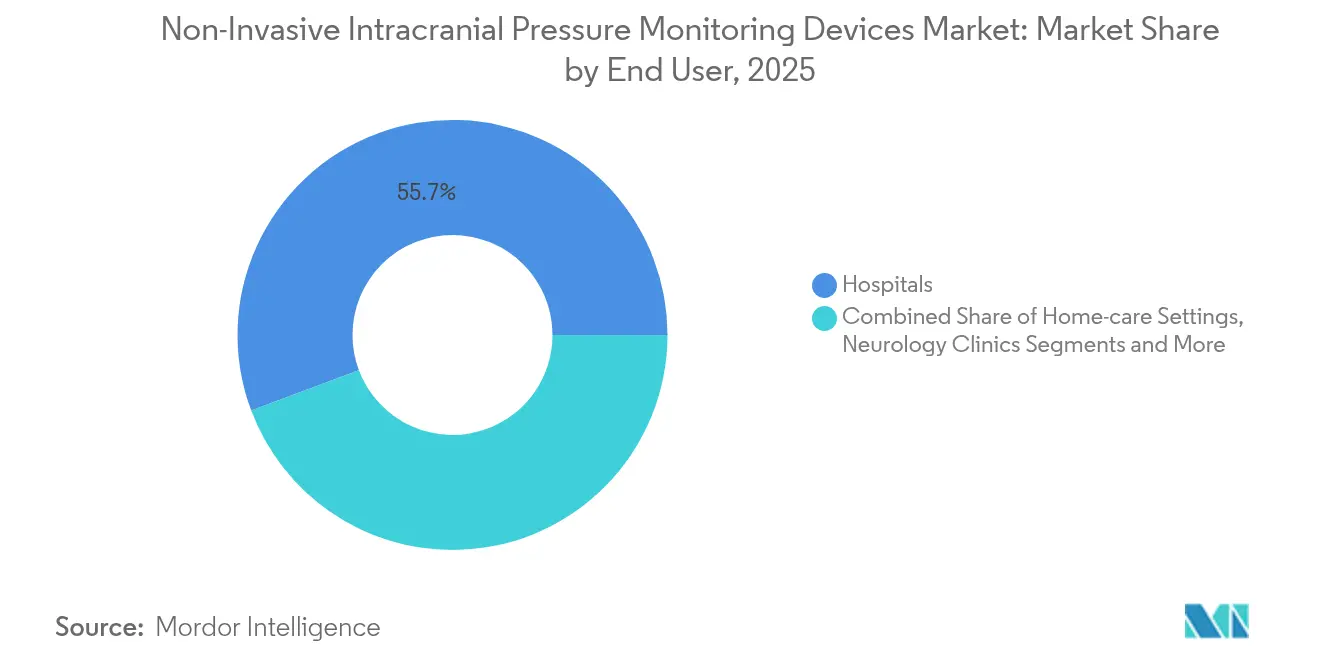

- By end user, hospitals held 55.72% revenue share in 2025, while home healthcare is set to post a 9.12% CAGR between 2026-2031.

- By geography, North America controlled 37.90% of the non-invasive intracranial pressure monitoring devices market size in 2025; Asia-Pacific is the fastest-growing region with an 8.11% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-Invasive Intracranial Pressure Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidences of neurological disorders | +1.2% | Global; greatest in aging North America & Europe | Long term (≥ 4 years) |

| Preference for minimally & non-invasive procedures | +0.8% | Global; strongest in developed systems | Medium term (2-4 years) |

| Wider adoption of point-of-care ultrasound in ED/ICU | +0.6% | North America & Europe lead; Asia-Pacific rising | Short term (≤ 2 years) |

| Growing use of multimodal neuromonitoring bundles | +0.5% | Global; tertiary and trauma centers | Medium term (2-4 years) |

| AI-enabled waveform analytics | +0.7% | Tech-advanced markets first, then emerging | Medium term (2-4 years) |

| Military R&D funding for blast-TBI screening | +0.3% | United States; allies benefitting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidences of Neurological Disorders

More than 70 million people experience traumatic brain injury each year, and overall stroke rates are climbing in younger cohorts, creating sustained demand for continuous, non-invasive monitoring across acute, rehabilitation and home settings[1]Center for Neuroscience and Regenerative Medicine, “Traumatic Brain Injury Statistics,” cdmrp.health.mil. Baseline cognitive testing for every new U.S. Army recruit since June 2024 highlights how military populations now require lifelong brain-health surveillance. The convergence of longer life expectancy with improved survival after severe events is enlarging the patient pool needing serial intracranial pressure checks without added surgical risk. Health systems consequently channel capital into devices that travel with patients across care environments, reinforcing volume growth for the non-invasive intracranial pressure monitoring devices market.

Rising Preference for Minimally & Non-Invasive Procedures

FDA clearance of the i-STAT TBI cartridge in 2024 exemplifies a regulatory tilt toward bedside diagnostics that bypass surgery while delivering rapid, reliable readings. Studies on Brain4care and similar platforms report mean absolute intracranial pressure errors around 3 mmHg, aligning closely with invasive probes and validating the technology in neurosurgical units. Economically, non-invasive pathways trim infection-related costs and reduce ICU length of stay, forming a persuasive value proposition for payers and clinicians alike. Patient advocacy groups amplify this momentum by challenging invasive use when harm-free substitutes exist. Collectively, these forces enlarge the non-invasive intracranial pressure monitoring devices market well beyond tertiary centers.

Wider Adoption of Point-of-Care Ultrasound in ED/ICU

Emergency physicians now deploy optic-nerve diameter and cerebral blood-flow metrics through handheld scanners, posting almost 80% agreement with in-hospital findings and cutting time to intervention. AI-integrated transducers that auto-calculate optic nerve sheath width remove operator bias, a critical gain in crowded trauma bays. Structured credentialing is closing the skills gap, enabling even junior doctors to gather accurate neurologic ultrasound data. Reduced CT usage and shorter door-to-treatment windows underpin hospital return-on-investment cases. In parallel, portable ultrasound enlarges the non-invasive intracranial pressure monitoring devices market within ambulance networks and rural clinics previously beyond reach.

AI-Enabled Waveform Analytics Improving Diagnostic Accuracy

Johns Hopkins algorithms distill arterial pressure, photoplethysmography and ECG waveforms into precise intracranial pressure estimates that match invasive catheter accuracy, all via equipment already present in standard monitors. Continuous analytics flag dangerous pressure trends sooner than manual charting, letting clinicians intervene before herniation risk spikes. Scalability permits simultaneous surveillance of multiple beds with consistent interpretation, mitigating the global neuro-sonographer shortage. Early deployment shows fewer false alarms and quicker therapy adjustments, strengthening the adoption case across high-acuity settings. These gains cement AI as a cornerstone driver for the non-invasive intracranial pressure monitoring devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of trained neuro-sonographers | -0.9% | Global; severe in emerging & rural zones | Medium term (2-4 years) |

| High device acquisition & maintenance costs | -0.7% | Mostly emerging markets | Short term (≤ 2 years) |

| Variability in non-invasive algorithm accuracy | -0.5% | Markets with strict validation rules | Medium term (2-4 years) |

| Slow reimbursement code expansion | -0.6% | United States & complex payor systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Trained Neuro-Sonographers

Effective transcranial Doppler demands mastery of cerebrovascular anatomy, optimal scale settings and nuanced waveform interpretation, skill sets still scarce outside academic centers. Certification pipelines remain thin, and sustained competence requires exposure to diverse pathologies. Workforce gaps translate into delayed studies, unequal access and, in turn, slower install-base growth for the non-invasive intracranial pressure monitoring devices market. Professional societies have launched standardized curricula, yet emerging economies continue to struggle with limited faculty pools and training equipment shortages[2]Journal of Neurosonology, “Transcranial Doppler Technique,” j-nn.org.

High Device Acquisition & Maintenance Costs

AI-enabled multimodal monitors command premium prices, often exceeding capital budgets in low- and middle-income facilities. Beyond purchase, calibration and software-update schedules impose recurring expenditure that strains operating funds. Administrators weigh these outlays against competing needs such as ventilators or imaging scanners. Rapid technology turnover further clouds return-on-investment calculations, prompting cautious rollouts. Consequently, price sensitivity tempers the near-term expansion of the non-invasive intracranial pressure monitoring devices market in cost-constrained health systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Transcranial Doppler Leads Despite Infrared Innovation

Transcranial Doppler held a 37.05% non-invasive intracranial pressure monitoring devices market share in 2025 owing to its established role in vasospasm detection, stroke risk screening and bedside cerebral hemodynamics assessment. Automated waveform storage, portable form factors and protocol standardization have kept adoption robust. The segment benefits from extensive reimbursement coverage and clinician familiarity, anchoring the non-invasive intracranial pressure monitoring devices market size on a solid installed base.

Infrared pupillometry is set for an 11.05% CAGR through 2031 as short-wave infrared cameras deliver touchless readings through closed eyelids, expanding monitoring to sedated or intubated patients. Devices that calculate the Neurological Pupil Index provide objective early warnings of intracranial hypertension, reducing reliance on subjective light-reflex checks. Tympanic membrane displacement and optic-nerve diameter tools serve niche applications where specific anatomic windows or pediatric use dictate alternate approaches. MRI/CT-based estimates remain constrained by cost, radiation exposure and limited repeatability, but may support complex cases requiring multimodal confirmation. Continuous improvements in algorithmic fusion of Doppler and pupillometry promise hybrid platforms that elevate diagnostic confidence while trimming operator training demands.

By Application: Traumatic Brain Injury Dominance Challenged by Stroke Acceleration

Traumatic brain injury represented 39.93% of the non-invasive intracranial pressure monitoring devices market in 2025, driven by defense-sector funding, sports-medicine protocols and motor-vehicle trauma prevalence. Surgeons rely on continuous pressure readings to forestall secondary injury from uncontrolled edema. Military mandates for baseline cognitive testing ensure early deployment of monitoring technology throughout active duty and veteran care pathways.

Stroke monitoring is advancing at a 9.37% CAGR as guidelines now recommend continuous intracranial pressure tracking to guide hyperosmolar therapy and blood-pressure titration in both ischemic and hemorrhagic events. Early-warning algorithms detect subtle pressure elevations that herald neurologic decline, enabling faster intervention. Intracerebral hemorrhage, meningitis and hydrocephalus collectively comprise a meaningful share, each benefitting from non-invasive options that circumvent infection risks in fragile patients. New clinical trials exploring multimodal bundles—combining intracranial pressure, cerebral perfusion and oxygenation—signal further expansion opportunities over the forecast.

By End User: Hospital Dominance Faces Home Healthcare Disruption

Hospitals controlled 55.72% of the non-invasive intracranial pressure monitoring devices market size in 2025 as neuro-ICUs standardize advanced monitoring for complex cases. Integration into electronic records and established purchasing frameworks protect incumbent sales channels. Academic centers also conduct validation studies, reinforcing hospital influence on purchasing standards and clinical protocols.

Home healthcare is forecast to register a 9.12% CAGR through 2031 due to FDA guidance that now facilitates remote neuro-monitoring platforms. Elderly and chronic-care patients benefit from wearable sensors that transmit secure data to central dashboards, curbing readmissions and enhancing quality of life. Neurology clinics and ambulatory centers occupy a middle ground, leveraging non-invasive solutions for same-day procedures and outpatient follow-up. As payors bolster reimbursement for remote physiologic monitoring, home-based deployments will chip away at hospital dominance, reshaping long-term revenue distribution within the non-invasive intracranial pressure monitoring devices market.

Geography Analysis

North America accounted for 37.90% of the non-invasive intracranial pressure monitoring devices market in 2025 amid sizable research budgets, robust reimbursement and the Department of Defense’s USD 3.2 million grant to refine blast-TBI screening. FDA breakthrough-device pathways shorten time-to-market for innovators, while Level 1 trauma centers set clinical standards that ripple across community hospitals. Canada’s single-payer environment supports steady device procurement, and Mexico’s public-health expansions are adding advanced neuromonitoring units in select tertiary hubs.

Asia-Pacific is the fastest-growing region with an 8.11% CAGR to 2031, supported by rising traumatic injury rates, aging demographics and expanding critical-care capacity. China’s revision of the National Medical Products Administration (NMPA) approval process is creating clearer on-ramps for imported and locally produced monitors. Japan and South Korea drive early adoption of AI-enhanced platforms, while India demonstrates high receptivity to cost-effective handheld Doppler solutions capable of operating in resource-sparse districts. Government health-tech incentives and local manufacturing tie-ups are expected to amplify installed bases.

Europe maintains a steady position, anchored by rigorous evidence-based guidelines and cross-border collaboration on multicenter trials exploring multimodal neuromonitoring. Germany, the United Kingdom and France lead acquisitions, whereas Southern and Eastern European systems embrace shared-service networks to pool capital expenditure. Medical Device Regulation (MDR) compliance has lengthened certification timelines yet boosts clinician confidence once devices clear review. Constrained budgets remain a headwind, but pan-EU research grants and vendor financing schemes help sustain device turnover.

Competitive Landscape

The non-invasive intracranial pressure monitoring devices market shows moderate concentration, with the top five manufacturers estimated to hold a significant share in 2025. Integra LifeSciences promotes its CereLink system while rectifying manufacturing observations cited in an FDA warning letter in December 2024. Nihon Kohden’s November 2024 purchase of a controlling stake in NeuroAdvanced expands its EEG and intracranial electrode offerings, underscoring a push toward multimodal neurological platforms.

Start-ups focus on AI algorithms that retrofit to existing bedside monitors, reducing capital hurdles for hospitals and accelerating revenue capture. Military R&D programs continue to seed early-stage ventures targeting blast-related trauma, which often migrate into civilian trauma-unit use. Device makers are also forging distribution alliances in Asia-Pacific to navigate local regulatory pathways and cut time-to-launch.

Strategically, vendors differentiate through software capabilities, cloud-integrated dashboards and training packages that counter the neuro-sonographer shortage. Subscription-based analytics models shift revenue from one-off hardware sales to recurring fees, smoothing cash flow and encouraging continual software upgrades. Litigation risk remains moderate because devices do not pierce the dura, but quality-system rigor is increasingly scrutinized: manufacturing lapses can result in stern FDA action, as evidenced in 2024. Long-term, players able to bundle intracranial pressure, EEG and cerebral oximetry within a single interface should command premium pricing.

Non-Invasive Intracranial Pressure Monitoring Devices Industry Leaders

RAUMEDIC AG

Nisonic

Natus Medical

Integra LifeSciences

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Researchers at the Icahn School of Medicine at Mount Sinai unveiled a non-invasive approach to monitor intracranial hypertension, promising earlier detection of stroke and hemorrhage risk.

- August 2024: FDA granted breakthrough-device status to the M.scio telemetric pressure measurement system for non-invasive intracranial pressure monitoring.

Global Non-Invasive Intracranial Pressure Monitoring Devices Market Report Scope

Non-invasive intracranial pressure monitoring devices are used to measure the pressure within the skull caused by trauma or medical conditions, such as intracranial hypertension, hydrocephalus, subarachnoid hemorrhages, inflammatory diseases, and cerebrospinal space diseases. These devices thus help monitor the pressure, as increased Intracranial Pressure (ICP) can result in serious or life-threatening medical problems. The Non-Invasive Intracranial Pressure Monitoring Devices Market is Segmented by Type (Transcranial Doppler Ultrasonography, Tympanic Membrane Displacement (TMD), Optic Nerve Sheath Diameter, MRI/CT, and Others), Application (Traumatic Brain Injury, Intracerebral Hemorrhage, Meningitis, and Others), and Geography ((North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Transcranial Doppler Ultrasonography |

| Tympanic Membrane Displacement |

| Optic Nerve Sheath Diameter |

| MRI / CT-based Estimation |

| Infrared Pupillometry |

| Others |

| Traumatic Brain Injury |

| Intracerebral Hemorrhage |

| Meningitis |

| Hydrocephalus |

| Stroke |

| Others |

| Hospitals |

| Neurology Clinics |

| Ambulatory Surgical Centers |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Transcranial Doppler Ultrasonography | |

| Tympanic Membrane Displacement | ||

| Optic Nerve Sheath Diameter | ||

| MRI / CT-based Estimation | ||

| Infrared Pupillometry | ||

| Others | ||

| By Application | Traumatic Brain Injury | |

| Intracerebral Hemorrhage | ||

| Meningitis | ||

| Hydrocephalus | ||

| Stroke | ||

| Others | ||

| By End User | Hospitals | |

| Neurology Clinics | ||

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the non-invasive intracranial pressure monitoring devices market in 2026?

The market stands at USD 389.78 million and is projected to reach USD 488.69 million by 2031, implying a 4.62% CAGR.

Which device type currently dominates sales?

Transcranial Doppler ultrasonography leads with a 37.05% share thanks to broad clinical validation and reimbursement support.

What is the fastest-growing application segment?

Continuous stroke monitoring shows the highest forecast growth at a 9.37% CAGR through 2031.

Which region offers the highest growth potential?

Asia-Pacific is set to expand at an 8.11% CAGR due to demographic shifts and expanding critical-care capacity.

How is artificial intelligence influencing adoption?

AI-enabled waveform analytics deliver invasive-level accuracy via standard monitors, reducing operator dependency and widening clinical uptake.

What restrains faster market penetration?

A global shortage of trained neuro-sonographers and high upfront equipment costs remain primary barriers despite rising demand.

Page last updated on: