Cranial Clamps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

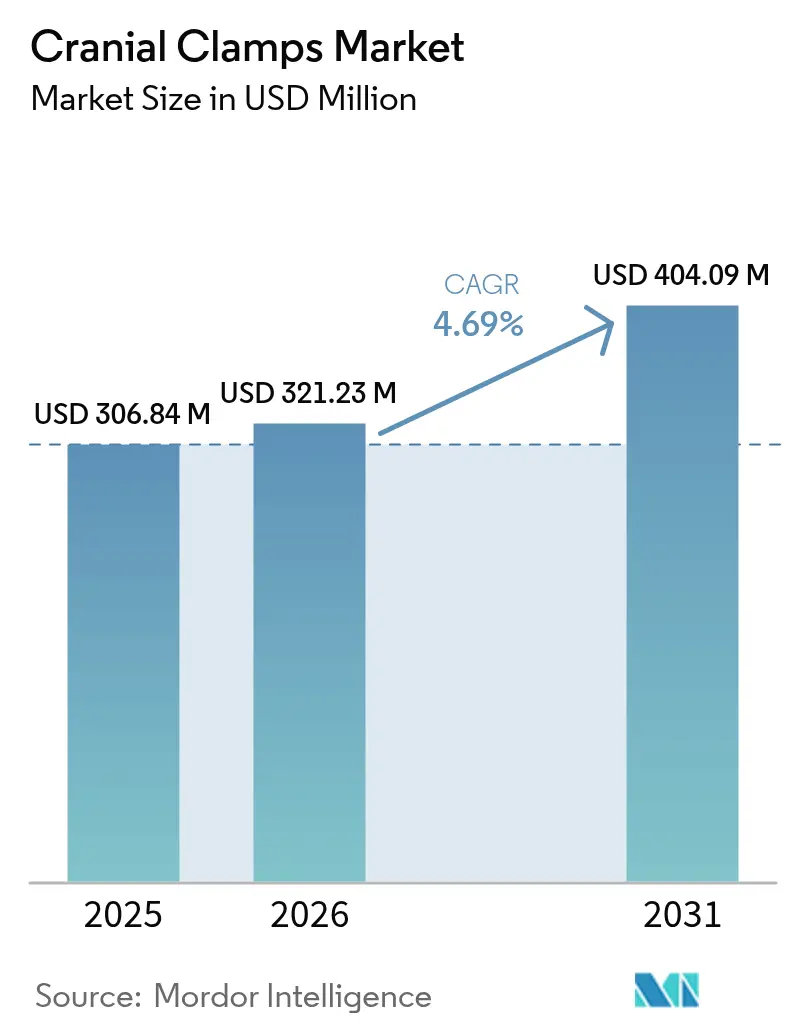

| Market Size (2026) | USD 321.23 Million |

| Market Size (2031) | USD 404.09 Million |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cranial Clamps Market Analysis by Mordor Intelligence

The cranial clamps market size is expected to grow from USD 306.84 million in 2025 to USD 321.23 million in 2026 and is forecast to reach USD 404.09 million by 2031 at 4.69% CAGR over 2026-2031. An upsurge in traumatic brain injury (TBI) cases, a rapidly aging population, and steady migration toward MRI-compatible radiolucent materials collectively sustain demand. Early adoption of same-day discharge protocols at high-volume neurosurgical centers accelerates turnover, while titanium-supply uncertainty prompts manufacturers to diversify alloys and incorporate polymers with lower magnetic susceptibility. Competitive focus tilts toward four-pin designs that distribute force more evenly and comply with stringent post-market surveillance. Simultaneously, ambulatory settings leverage lighter, disposable fixation components to curb infection risk and reduce re-processing overheads. Across growth regions, Asia-Pacific stands out as hospital construction programs in China and India boost neurosurgeon density and spur equipment procurement.

Key Report Takeaways

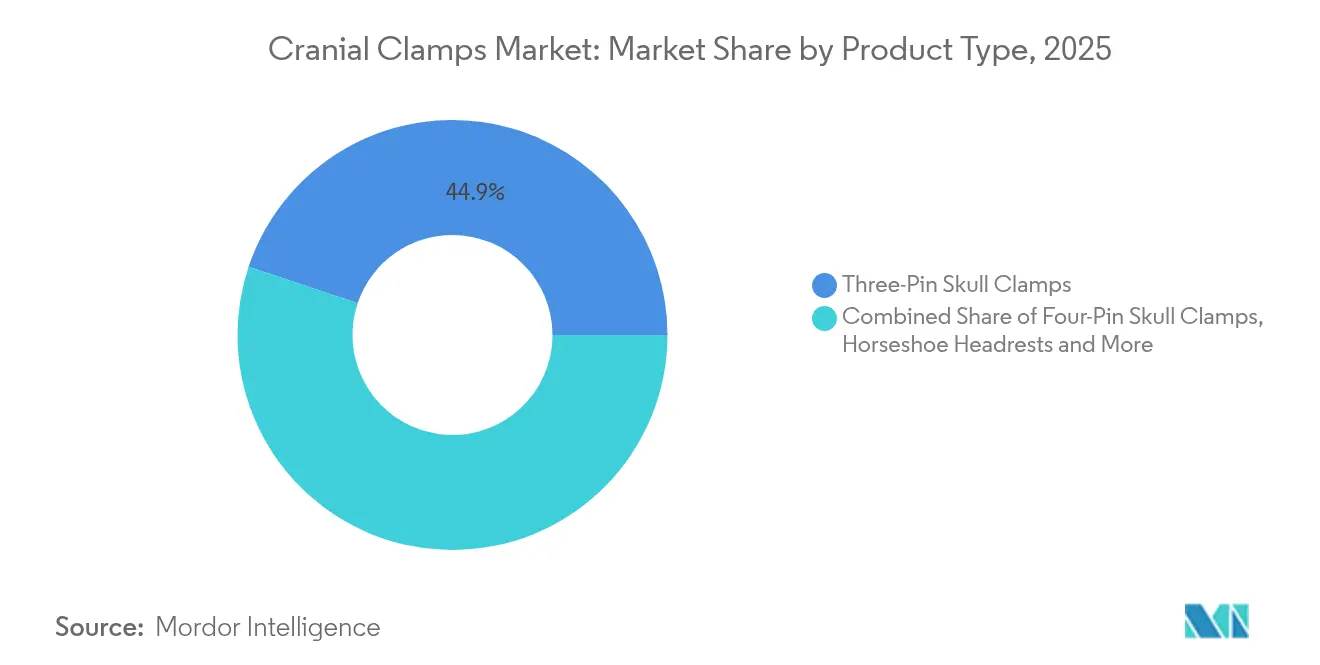

- By product type, three-pin clamps led with 44.86% of cranial clamps market share in 2025, whereas four-pin systems are projected to rise at a 6.98% CAGR through 2031.

- By application, surgical use commanded 60.05% of the cranial clamps market size in 2025; imaging applications are advancing at a 7.08% CAGR to 2031.

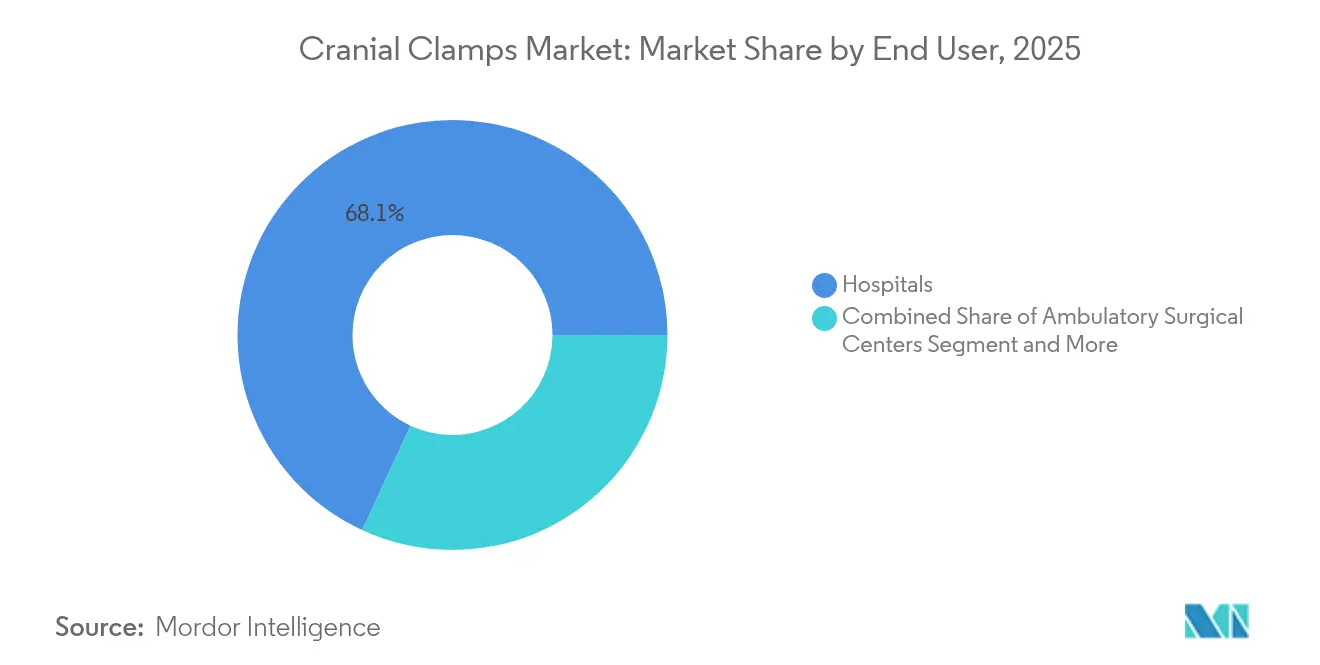

- By end user, hospitals controlled 68.10% of the cranial clamps market size in 2025, while ambulatory surgical centers are expanding at a 7.85% CAGR.

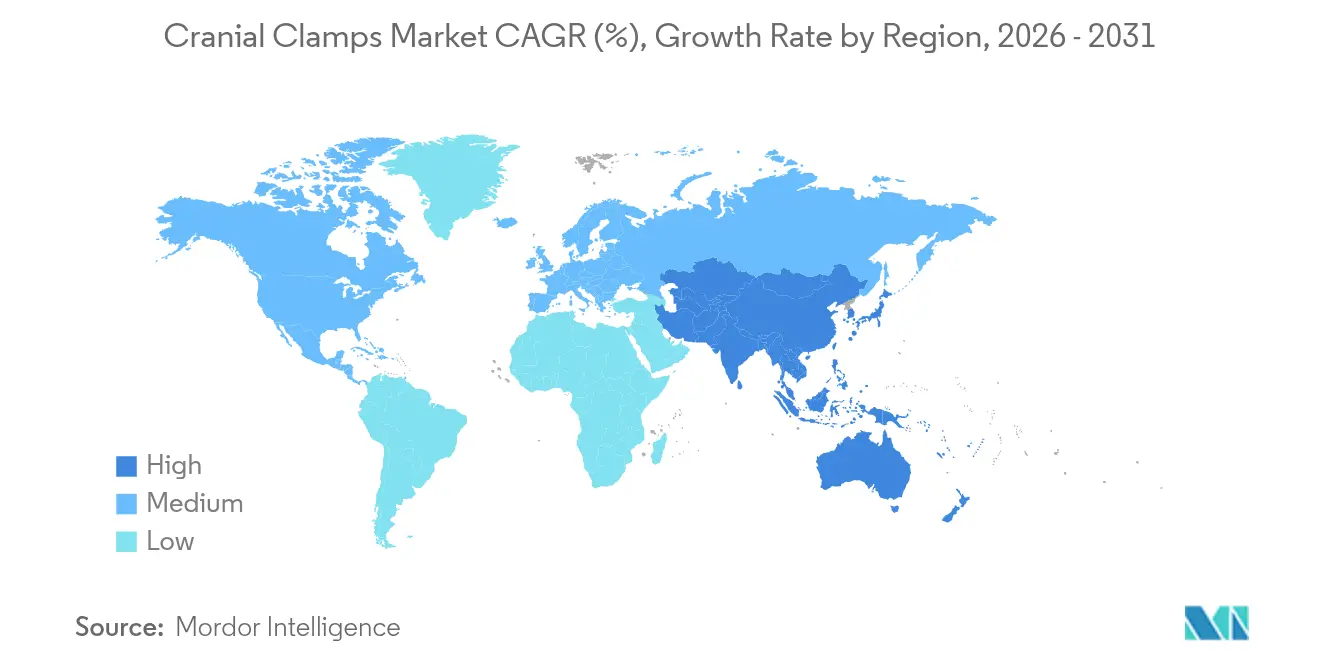

- By geography, North America captured 38.55% revenue share in 2025, yet Asia-Pacific is forecast to grow at a 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cranial Clamps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of traumatic brain injuries | +1.2% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Growing volume of neuro & spine surgeries | +0.9% | Asia-Pacific & North America | Long term (≥ 4 years) |

| Expansion of neurosurgical capacity in emerging economies | +0.8% | Asia-Pacific core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Aging population-induced case growth | +0.7% | Most pronounced in developed markets | Long term (≥ 4 years) |

| Adoption of MRI-compatible radiolucent clamps | +0.5% | Early uptake in North America & Europe | Medium term (2-4 years) |

| Shift toward ambulatory neurosurgery | +0.4% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Traumatic Brain Injuries

Higher TBI detection rates under newer CBI-M criteria have widened the treated population, especially for mild injuries often missed in emergency settings[1]Centers for Disease Control and Prevention, “TBI Data,” cdc.gov. The enlarged patient pool feeds directly into operating-room volume, demanding reliable fixation across emergency craniotomies and reconstructive follow-ups. Pediatric and geriatric subgroups show distinct anatomical needs that steer manufacturers toward age-tuned pin depths and torque limits. Health-economic pressure from escalating TBI treatment costs further incentivizes hospitals to adopt stable, reusable head restraints that shorten procedure time and reduce revision risk. As survivorship improves, this continual inflow of cases reinforces a long-tail revenue stream for the cranial clamps market.

Growing Volume of Neuro & Spine Surgeries

Population-level data confirm steady gains in intracranial tumor resections, spine fusions, and catheter-based interventions. Same-day discharge for selected craniotomy patients now exceeds 88% success at specialized centers[2]Journal of Neurosurgery, “Optimizing outpatient neurosurgery,” thejns.org. Lightweight, MRI-safe clamps support this workflow by streamlining intraoperative imaging and post-anesthesia mobilization. Robotic navigation and AI-driven planning demand precision head positioning within sub-millimetric tolerances, pushing vendors to integrate digital calibration into clamp bases. Coupled with lower outpatient reimbursement differentials, procedure growth cements long-term momentum for the cranial clamps market.

Rapid Expansion of Neurosurgical Capacity in Emerging Economies

China’s 25,438-patient aneurysm trial underscores the scale of new clinical infrastructure under construction. In India, a major multinational has doubled engineering staff at its Global Technology Centre, accelerating locally adapted clamp designs. Regional shortages in trained neurosurgeons spur inter-institutional partnerships, ensuring that standardized fixation systems are specified during procurement. Lower import duties for devices assembled domestically incentivize global manufacturers to establish regional finishing plants, embedding the cranial clamps market deeper into emerging-economy supply chains.

Aging Population-Induced Case Growth

Adults older than 65 increasingly present with chronic subdural hemorrhage that often mandates surgical evacuation. Outcome parity between octogenarians and younger elderly cohorts encourages surgical intervention when frailty scoring is favorable. Because geriatric bone is thinner and more brittle, engineers refine pin angulation and threading to prevent depressed fractures. Parallel growth in aneurysm clipping among patients whose mean age now approaches 55 also sustains demand for adaptable fixation. Collectively, population aging delivers a sizable, predictable case load that anchors revenue visibility in the cranial clamps market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pressure-injury & infection complications | -0.8% | North America & Europe | Short term (≤ 2 years) |

| High device & operating-room integration cost | -0.6% | Emerging markets most affected | Medium term (2-4 years) |

| Stringent post-market surveillance | -0.4% | North America & European Union | Medium term (2-4 years) |

| Titanium & specialty-alloy supply volatility | -0.3% | Global, with regional sourcing dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pressure-Injury & Infection Complications

Device-induced skull fractures and pressure ulcers, although infrequent, drive protocol revisions and may prompt legal scrutiny. Japanese registry data cite a 0.558% annual complication rate for cranial implants, with infections forming 63% of cases. Risk mitigation now includes pre-calibrated spring-loaded pins and routine torque verification. Some hospitals incorporate intraoperative ultrasound to confirm bone integrity before fixation, trading higher procedural cost for increased safety. While these measures temper adoption speed, they also stimulate innovation—benefitting long-term quality within the cranial clamps market.

High Device & Operating-Room Integration Cost

Robot-compatible head frames command premium pricing, and full robotic systems can cost USD 0.5–2.5 million. Coupled with declining inflation-adjusted reimbursements for head trauma procedures, the capital burden deters smaller hospitals from upgrading. Emerging-market import taxes compound the challenge. Vendors counter with modular platforms and pay-per-use service models, yet integration complexity still narrows purchaser pools, restraining the cranial clamps market in budget-sensitive regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Four-Pin Configurations Drive Innovation

Three-pin clamps accounted for 44.86% of cranial clamps market share in 2025 due to decades of clinical familiarity. The four-pin segment, however, is advancing at a 6.98% CAGR and is projected to contribute an additional USD 20.5 million to cranial clamps market size by 2031. Enhanced force distribution lowers localized pressure points, proven by laboratory data showing 50°/25° pin arrangements achieve uniform penetration depths. Manufacturers such as Aesculap deliver sub-two-minute fixation kits certified for magnetic resonance environments, while resorbable molybdenum frames target pediatric skull growth. Horseshoe headrests retain niche value for posterior fossa access, yet disposable pin conversions and color-coded torque sleeves are now standard on flagship lines, reflecting broader innovation cycles within the cranial clamps market.

The development pipeline emphasizes polymer composites, adjustable pin trajectories, and integrated force sensors that relay real-time feedback to surgical dashboards. These advances support robotic re-registration and AI-driven navigation, improving first-pass accuracy. Supply-chain diversification away from titanium mitigates metal price volatility and aligns with environmental stewardship targets. Collectively, these trends reinforce growth while preserving clinical safety benchmarks for the cranial clamps market.

By Application: Imaging Segment Accelerates Growth

Surgery remained dominant with 60.05% of the cranial clamps market size in 2025 because tumor resections and trauma procedures depend on rigid fixation for periods surpassing 4 hours. The imaging application, while smaller, is expanding at a 7.08% CAGR as intraoperative MRI suites proliferate worldwide. Polymer-based clamps that eliminate ferromagnetic artifact enable surgeons to acquire real-time volumetric updates without repositioning. Brain-computer interface trials further boost imaging-centered case volumes, elevating clamp demand in hybrid ORs. Vendors integrate single-use carbon pin sets that conform to MRI safety protocols and reduce contamination risk, reinforcing value propositions amid strict infection-control standards.

The convergence with navigation platforms prompts clamp designs featuring fiducial markers readable by optical or electromagnetic trackers. As AI algorithms segment cranial anatomy automatically, clamp baseplates now incorporate reference frames readable by software, allowing seamless recalibration after intraoperative scans. This synergy cements the imaging sub-segment as a durable growth engine within the cranial clamps market.

By End User: Ambulatory Centers Transform Care Delivery

Hospitals sustained 68.10% of cranial clamps market size in 2025, yet ambulatory surgical centers are scaling fastest at an 7.85% CAGR. Outpatient craniotomy protocols that rely on ultra-short-acting anesthetics and rapid-closure techniques shift purchase decisions toward lightweight, user-friendly fixtures. Disposable accessories minimize turnover time and align with sterilization-free workflows. Specialty neuro clinics add incremental demand for miniaturized, pediatric-ready kits. In response, manufacturers offer modular racks that fit constrained ambulatory storage while preserving high clamping force. This user-mix evolution introduces fresh competitive dynamics and underscores the adaptability of the cranial clamps market.

Parallel adoption of bundled payment models drives centers to favor devices that reduce perioperative complications and readmissions. Clamp systems with real-time force indicators and automatic release mechanisms appeal to risk-averse administrators. Consequently, end-user preferences steer R&D budgets toward intuitive safety features that could become standard across the cranial clamps market.

Geography Analysis

North America controlled 38.55% revenue in 2025, buoyed by high procedural volumes and advanced outpatient pathways that rely on premium fixation devices. Robust reimbursement and rigorous FDA oversight ensure steady upgrade cycles, yet warning letters such as the 2024 Integra LifeSciences citation illustrate the penalties for quality lapses. Post-market surveillance findings feed directly into design iterates, reinforcing a virtuous cycle of compliance and innovation across the cranial clamps market.

Asia-Pacific is the fastest-growing territory, advancing at a 9.18% CAGR through 2031. Large-scale trials like China’s ChTUIA signal massive procedure throughput, and public-private initiatives expand neurosurgeon training pipelines. Government incentives to localize device assembly reduce import dependency, while R&D centers in Singapore and India support design tweaks tailored to regional anatomy and price sensitivity. Japanese hospitals pioneer AI-assisted safety frameworks that elevate equipment specification, raising baseline requirements for market entry.

Europe posts steady gains as regulatory harmonization under the Medical Device Regulation tightens post-market vigilance. Hospitals in Germany and France integrate digital traceability for clamp sterilization cycles, an emerging procurement criterion. Latin America, the Middle East, and Africa benefit from donor-funded theater upgrades and tele-mentoring programs that widen access. Persistent neurosurgeon scarcity—0.93 per 100,000 globally—creates latent demand that activates once infrastructure matures. This map of opportunities underscores both mature and nascent revenue pockets for the cranial clamps market.

Competitive Landscape

The cranial clamps market is moderately concentrated, with three multinationals accounting for most branded revenue yet facing nimble entrants in polymer composites and pediatric-specific systems. Integra LifeSciences’ 16% slide in neurosurgery sales following FDA quality citations underlines the operational cost of compliance failures. Johnson & Johnson’s DePuy Synthes leverages its VELYS robotics ecosystem to cross-sell integrated head fixation that communicates with navigation software. Stryker pairs 3D-printed PEEK cranial implants with custom clamp fittings, strengthening its pre-operative planning suite.

Specialists fill white spaces: KLS Martin reports faster-than-industry revenue on modular pediatric frames, while ClearPoint Neuro secures 510(k) for navigation software that auto-registers clamp geometry. Material innovation accelerates, with ceramic clips and molybdenum resorbables vying for MRI-friendliness and post-operative bone remodeling, respectively. Supply-chain hedging sees vendors dual-source titanium or adopt carbon-fiber composites. Intensifying regulatory scrutiny and customer push for digital integration remain the twin vectors shaping strategy across the cranial clamps market.

Cranial Clamps Industry Leaders

pro med instruments GmbH

Integra LifeSciences

IMRIS (Deerfield Imaging)

Johnson & Johnson (DePuy Synthes)

B. Braun SE (Aesculap)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Johnson & Johnson unified Ethicon, DePuy Synthes, Biosense Webster, Abiomed, and CERENOVUS under its MedTech brand identity to reinforce a cohesive technology portfolio.

- August 2024: Stryker secured FDA clearance for the Pangea Plating System, offering 33 variable-angle plates for trauma stabilization.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the cranial clamps market as the worldwide sales of reusable or single-use three, four, or multi-pin head-holding devices and compatible horseshoe headrests that secure a patient's skull during neurosurgical or imaging procedures.

Scope exclusion: veterinary skull-fixation devices lie outside this definition.

Segmentation Overview

- By Product Type

- Three-Pin Skull Clamps

- Four-Pin Skull Clamps

- Horseshoe Headrests

- Ancillary Accessories

- By Application

- Imaging

- Surgery

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty/Neuro Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and online surveys with neurosurgeons, biomedical engineers, purchasing managers, and regulatory consultants across North America, Europe, Asia-Pacific, and the Middle East validated use-pattern ratios, ASP ranges, and emerging adoption of radiolucent clamps. Feedback also closed data gaps on ambulatory surgery center penetration and typical clamp refurbishment cycles.

Desk Research

Analysts began with open datasets from bodies such as the WHO's Global Health Observatory, the OECD Health Statistics portal, United States CDC's NIS, Eurostat surgical discharge files, and India's MoHFW, which together map neurosurgical procedure volumes and traumatic brain injury incidence. Trade flow snapshots from UN Comtrade and FDA 510(k) listings helped us size cross-border supply as well as new product approvals, while peer-reviewed articles in journals like Neurosurgery clarified complication rates that trigger replacement demand. Where public data were sparse, we turned to D&B Hoovers for company revenue splits and Dow Jones Factiva for device pricing news. Company 10-Ks, hospital procurement dashboards, selected neurosurgery association white papers, and patent abstracts accessed through Questel further enriched average selling price (ASP) assumptions and material innovation timelines. This list is illustrative; many additional secondary sources were consulted to cross-check figures and definitions.

Market-Sizing & Forecasting

A top-down model starts by reconstructing the global neurosurgery pool from procedure counts, head-injury prevalence, and imaging-only case volumes; these are paired with weighted clamp-per-case ratios to derive unit demand, which is then multiplied by regional ASPs. Supplier roll-ups and sampled tender prices provide a selective bottom-up sense-check before totals are finalized. Key variables include TBI incidence, elective neuro-oncology surgery growth, hospital bed expansion, clamp refurbishment interval, and radiolucent upgrade premiums. Forecasts employ a multivariate regression that links those drivers to historical sales, with scenario analysis overlaying regulatory or reimbursement shocks. Gaps in country-level data are bridged by proxy indicators such as neurosurgeon density and GDP-per-capita health spend.

Data Validation & Update Cycle

Outputs pass variance checks against independent import data and prior-year sales; anomalies trigger re-contact with experts before senior review. Mordor refreshes models annually and issues interim revisions when material events, such as product recalls and reimbursement changes, arise, ensuring clients always receive our latest view.

Why Mordor's Cranial Clamps Baseline Earns Clinical Confidence

Published estimates vary because firms choose different device mixes, base years, and refresh cadences.

Typical gaps stem from whether accessories are counted, how refurbished units are treated, and how ASP erosion is modeled.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 306.84 mn (2025) | Mordor Intelligence | - |

| USD 290.20 mn (2024) | Global Consultancy A | excludes ancillary headrests and uses static ASPs that ignore alloy price inflation |

| USD 272.38 mn (2024) | Industry Association B | hospital-only sampling and limited country coverage reduce captured demand |

The comparison shows that figures shrink when accessory sales or emerging-market facilities are left out, and they expand when refurbished units are double-counted. By calibrating scope, refreshing inputs yearly, and balancing top-down incidence logic with bottom-up supplier checks, Mordor Intelligence delivers a dependable, transparent baseline that decision-makers can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current global value of the cranial clamps market?

The market stands at USD 321.23 million in 2026 and is projected to grow to USD 404.09 million by 2031.

Which region is expanding fastest in the cranial clamps market?

Asia-Pacific is growing at a 9.18% CAGR thanks to new neurosurgical centers and localized device production.

Why are four-pin skull clamps gaining traction?

Four-pin designs distribute pressure more evenly, reduce tissue trauma, and support complex robotic-assisted procedures.

How do ambulatory surgical centers influence demand?

Outpatient craniotomy protocols rely on lightweight, disposable clamps that shorten turnover, boosting device orders from these centers.

What are the primary complications linked to cranial clamps?

Documented issues include pressure injuries, skull fractures, and infections, prompting stricter torque controls and surveillance.

Page last updated on: