Intracranial Pressure Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

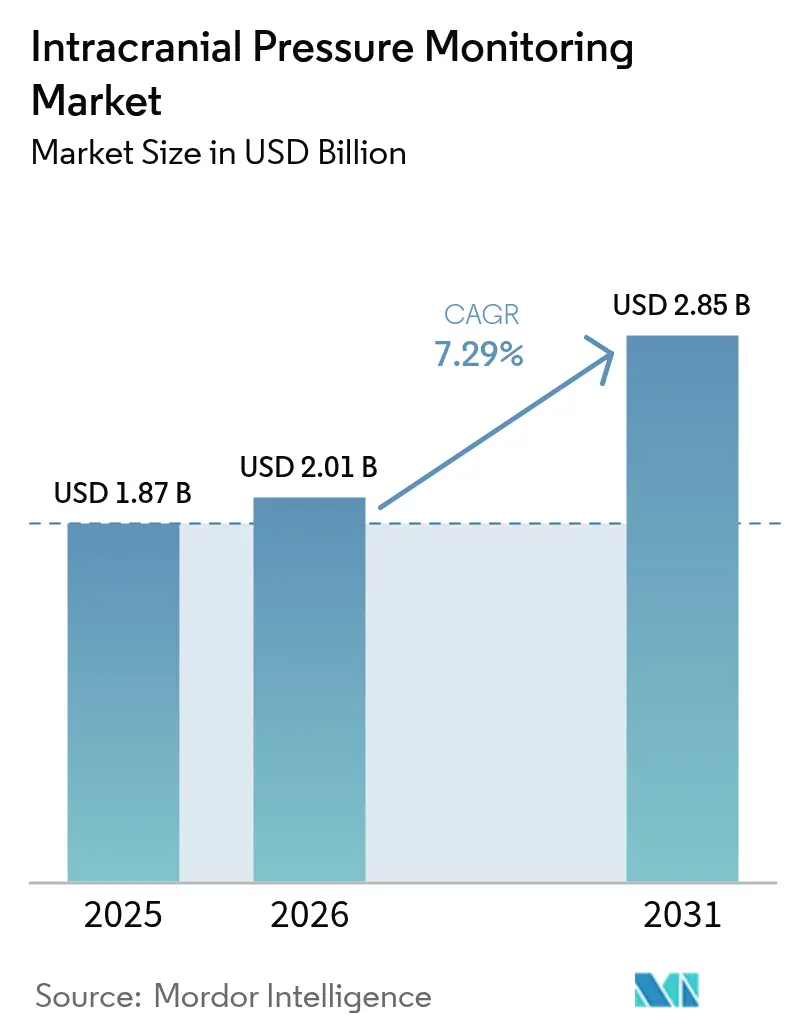

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.85 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

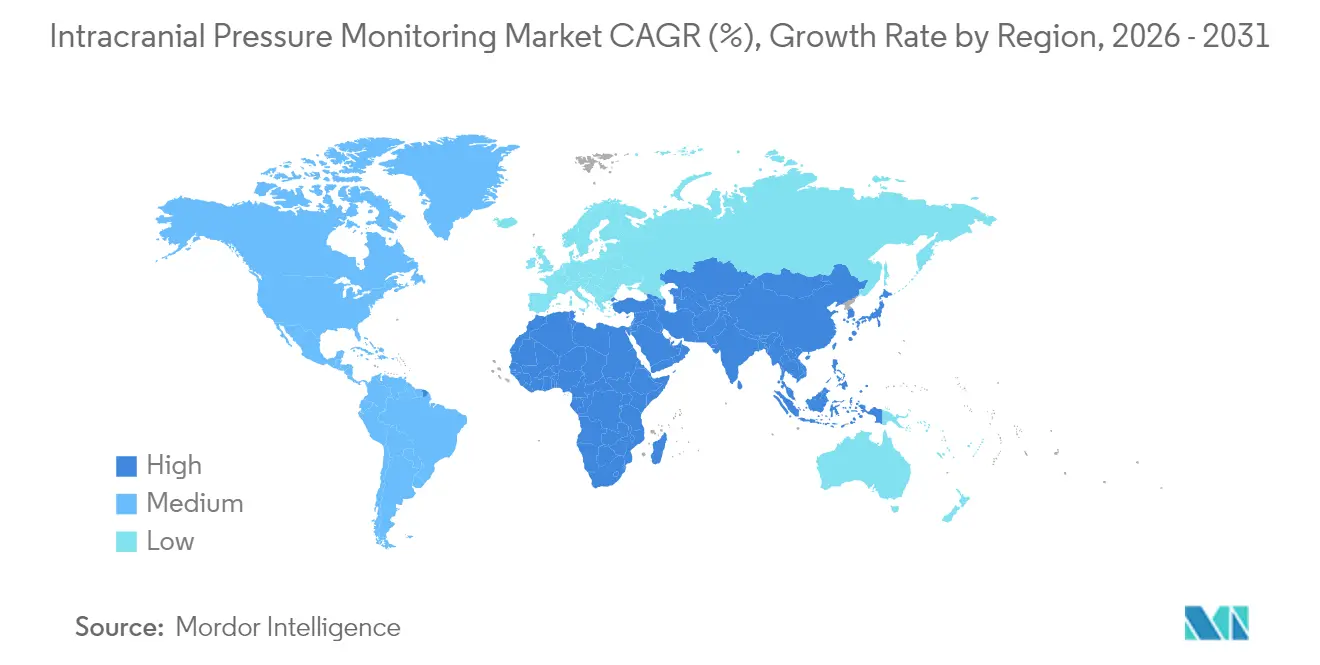

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intracranial Pressure Monitoring Market Analysis by Mordor Intelligence

The intracranial pressure monitoring market size is expected to grow from USD 1.87 billion in 2025 to USD 2.01 billion in 2026 and is forecast to reach USD 2.85 billion by 2031 at 7.29% CAGR over 2026-2031. Growth rests on the pairing of artificial intelligence with conventional neurocritical care, letting clinicians predict pressure surges well before a patient shows clinical decline.[1]Venkatakrishna Rajajee, “Noninvasive Intracranial Pressure Monitoring: Are We There Yet?” Neurocritical Care, springer.com Hospitals are adopting wireless micro-sensors that deliver accuracy within 1.0 mm Hg of invasive systems, while predictive analytics platforms cut intervention time and lower complication rates. Traumatic brain injury keeps demand steady, but infectious conditions and space medicine add fresh revenue streams. Vendors that integrate cybersecurity, data analytics and biocompatible materials now command premium pricing.

Key Report Takeaways

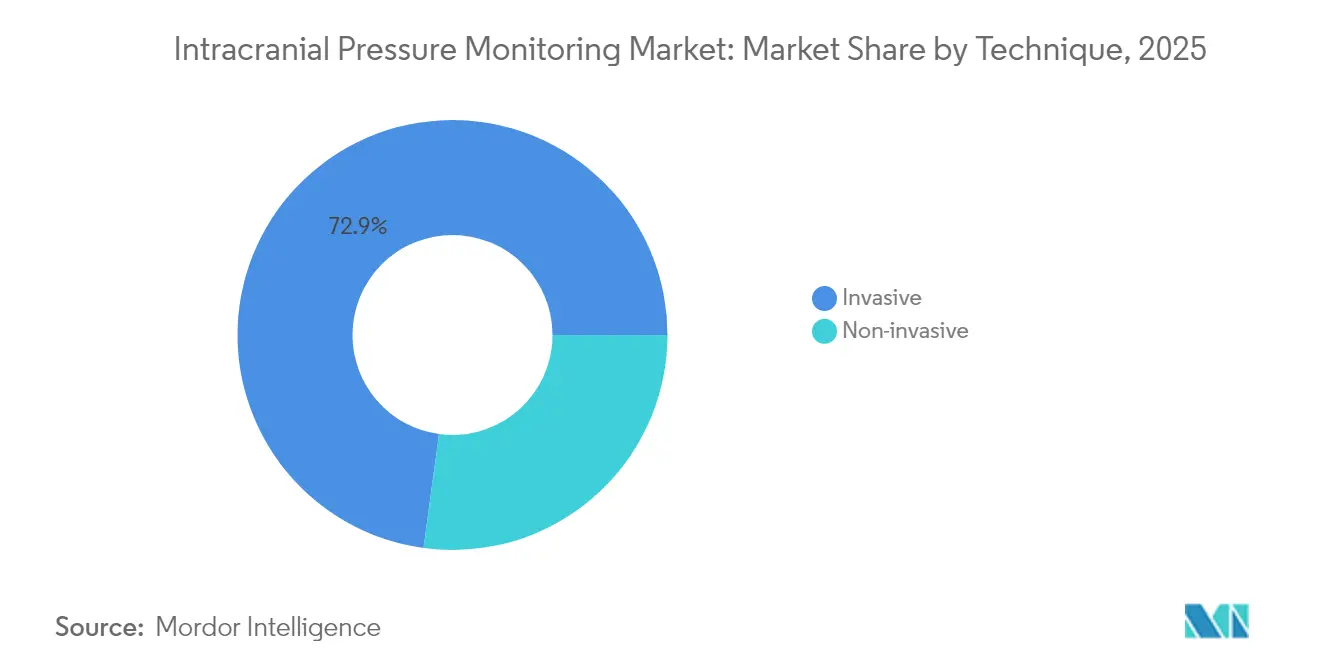

- By technique, invasive devices held 72.85% of intracranial pressure monitoring market share in 2025, whereas non-invasive systems are on track for a 9.78% CAGR to 2031.

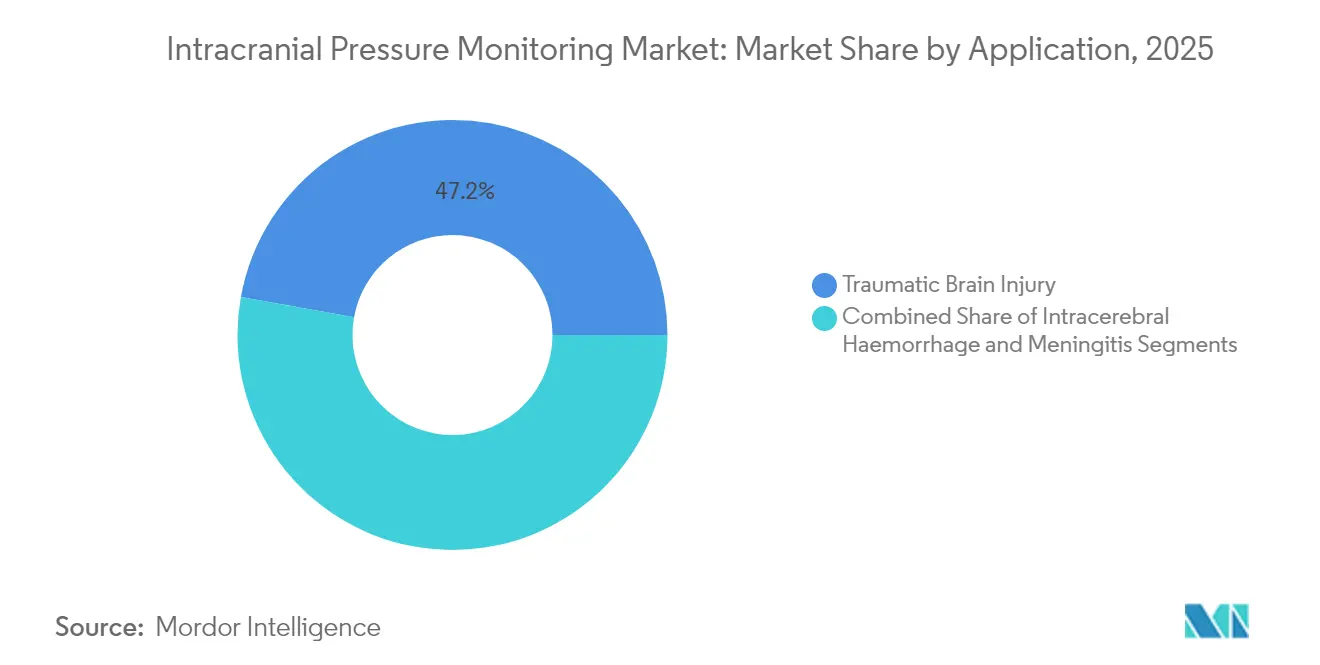

- By application, traumatic brain injury led with 47.18% revenue share in 2025, while meningitis monitoring is projected to grow at 10.76% CAGR through 2031.

- By end-user, hospitals and trauma centres accounted for 50.63% share of the intracranial pressure monitoring market size in 2025; military and space health facilities are expanding at a 9.32% CAGR to 2031.

- By geography, North America dominated with 39.22% share in 2025, yet Asia-Pacific is forecast to post the fastest 9.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intracranial Pressure Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Traumatic Brain Injury (TBI) | +1.2% | Global, with highest impact in North America & APAC | Medium term (2-4 years) |

| Growing Prevalence Of Hydrocephalus & Neuro-Degenerative Disorders | +0.9% | Global, concentrated in aging populations of Europe & North America | Long term (≥ 4 years) |

| Rapid Adoption Of Minimally-Invasive Micro-Sensor Technologies | +1.8% | North America & EU leading, APAC following | Short term (≤ 2 years) |

| AI-Driven Personalised ICP Thresholds & Predictive Analytics | +1.5% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Demand From Space-Medicine & High-Altitude Expeditions | +0.3% | North America, EU, with emerging interest in China & India | Long term (≥ 4 years) |

| Paediatric ICU Protocols Mandating Continuous ICP Monitoring | +0.8% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Traumatic Brain Injury

Traffic collisions, sports mishaps and falls among seniors sustain a high caseload that requires continuous monitoring in intensive care units. Updated Brain Trauma Foundation guidelines recommend pressure tracking for every severe case with a Glasgow Coma Scale below 8, increasing the eligible patient cohort.[2]Nessim Amin and Diana Greene-Chandos, “Intracranial Pressure Monitoring,” Neurocritical Care Monitoring, connect.springerpub.com Military conflicts and adventure sports widen demographic exposure, while value-based care models reward early detection that prevents secondary damage.

Growing Prevalence of Hydrocephalus & Neuro-Degenerative Disorders

Hydrocephalus affects 1 in 1,000 newborns and appears more often among aging adults. Programmable shunt systems now include embedded sensors that fine-tune drainage in real time, trimming revision surgeries.[3]Chenqi He et al., “Intracranial Pressure Monitoring in Neurosurgery: The Present Situation and Prospects,” Chinese Neurosurgical Journal, cnjournal.biomedcentral.com Alzheimer’s and Parkinson’s patients also benefit from sustained monitoring when cerebrospinal dynamics fluctuate.

Rapid Adoption of Minimally Invasive Micro-Sensor Technologies

Next-generation catheters combine pressure, oxygen and temperature sensing through one port, eliminating infection pathways typically seen with external ventricular drains. Wireless variants slash infection rates from 10-15% to near zero and permit patient ambulation. Bioabsorbable versions dissolve post-use, removing the need for extraction.

Demand from Space-Medicine & High-Altitude Expeditions

NASA’s study of spaceflight-associated neuro-ocular syndrome has funded zero-gravity-capable ICP monitors that track fluid shifts during long missions. Portable, non-invasive versions now support mountaineers, soldiers and pilots operating at extreme altitudes where invasive catheters are impractical. China and India are investing in similar technologies for planned lunar and Himalayan missions, accelerating commercial demand. Miniaturised, battery-powered sensors developed for orbit are already migrating into civilian trauma and emergency transport settings, creating downstream market pull.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device & Procedure Cost; Reimbursement Gaps | -1.1% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Shortage Of Trained Neuro-Critical-Care Staff | -0.8% | Global, acute in rural areas and developing countries | Long term (≥ 4 years) |

| Cyber-Security & Data-Privacy Risks With Wireless Systems | -0.5% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Supply-Chain Fragility For Sensor-Grade Piezo Materials | -0.7% | Global, concentrated impact on high-tech manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device and Procedure Cost; Reimbursement Gaps

Capital equipment costs range from USD 15,000 to USD 50,000, and each implantation adds another USD 5,000–15,000 in patient charges. Annual maintenance, single-use sensors and software licences inflate lifetime ownership costs. Reimbursement remains patchy; some insurers cover only invasive systems or demand prior authorization, leaving newer non-invasive options unfunded. Hospitals must compile cost–effectiveness dossiers before purchase, so many low-resource centers postpone adoption despite clinical need.

Shortage of Trained Neuro-Critical-Care Staff

Interpreting multiparameter outputs requires six to twelve months of specialised training, yet many regions lack board-certified neurointensivists. General ICU teams often manage complex cranial data with minimal guidance, raising the risk of delayed intervention. Tele-ICU links ease the gap, but bandwidth limits and time-zone lags can slow urgent decisions. Automated alerts help triage cases, yet bedside expertise remains essential, restraining market growth even where hardware is available.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Invasive Methods Dominate Despite Non-Invasive Innovation

Invasive devices delivered 72.85% of intracranial pressure monitoring market revenue in 2025. External ventricular drains remain indispensable when cerebrospinal fluid diversion is required, while fiber-optic probes offer high fidelity for continuous readings. The segment benefits from standardised clinical protocols and widespread physician familiarity. Non-invasive platforms are growing at 9.78% CAGR, propelled by transcranial Doppler and optic-nerve ultrasonography that achieve clinically acceptable accuracy. Diffuse correlation spectroscopy narrows mean error to 1.0 mm Hg, edging closer to catheter precision.

Continued research funds mobile ultrasound solutions that frontline responders can use before hospital arrival, reinforcing non-invasive momentum. Yet the intracranial pressure monitoring market size for invasive systems is projected to preserve a strong base through 2031 because neurosurgeons still prefer direct readings for complex trauma cases. Hybrid models, where a patient begins with invasive surveillance and shifts to cuff-less optical sensors for step-down care, illustrate convergence across techniques.

By Application: Meningitis Monitoring Emerges as Growth Driver

Traumatic brain injury represented 47.18% of 2025 revenue, reflecting its entrenched protocol status within intensive care units. TBI cases typically mandate monitoring periods of five to seven days, yielding predictable device utilisation. In contrast, the meningitis segment is scaling at 10.76% CAGR, as clinicians recognise that treating pressure early slashes mortality from 30% to 10% and doubles recovery odds. ICP tracking now guides corticosteroid titration and ventricular drainage decisions during infectious flare-ups.

Hydrocephalus and intracerebral haemorrhage round out the portfolio, each benefitting from sensor-equipped shunts and early warning alerts. The intracranial pressure monitoring market size for meningitis is small today yet has outsized growth potential, particularly in regions where bacterial CNS infections remain prevalent. Advancements in multimodal platforms that combine pressure, oxygen and EEG data provide comprehensive oversight across diverse neurological insults.

By End-User: Military and Space Applications Drive Innovation

Hospitals and trauma centres captured 50.63% revenue in 2025 because they possess operating theatres, neurosurgeons and intensive care beds. Continuous monitoring is an expected standard in level-1 trauma institutions, and bundled capital purchases tie sensor demand to renovation cycles. Ambulatory surgical centres are experimenting with short-term postoperative pressure checks, though procedure complexity limits penetration. The military and space health segment is expanding at 9.32% CAGR, reflecting demand from zero-gravity missions, high-altitude deployments and decompression training environments.

Miniaturised, battery-powered implants designed for orbital flight are now transitioning into civilian practice where portability and infection avoidance matter. The intracranial pressure monitoring market share for defence and aerospace remains modest but showcases premium prices and high strategic value. Partnerships between medical device firms and space agencies spur dual-use technology, feeding a virtuous R&D cycle that benefits frontline hospitals.

Geography Analysis

North America held 39.22% of global revenue in 2025 on the back of trauma networks, ample reimbursement and early AI adoption. The United States leads through FDA clearance processes that favour iterative sensor upgrades, while Canada leverages a universal system to implement standardized protocols. Mexico’s device manufacturing clusters add supply resilience, though budget constraints temper hospital uptake. Cyber-security mandates increase compliance costs, yet they also create barriers that protect incumbent vendors.

Asia-Pacific is growing the fastest at 9.11% CAGR thanks to hospital build-outs, rising accident rates and government push for med-tech self-reliance. China subsidises domestic sensor production, and India’s private clinics deploy advanced monitors to serve medical tourists. Japan’s rapidly aging society fuels hydrocephalus applications, whereas South Korea positions trauma facilities as regional centres of excellence. Australia and New Zealand use portable kits to serve mining and remote communities.

Europe shows steady expansion anchored in evidence-based practice and robust data-privacy legislation. Germany and the United Kingdom finance multi-centre trials to validate non-invasive algorithms, while France and Italy refine paediatric protocols. GCC countries invest in neurotrauma capacity, and South Africa pilots tele-neurocritical care to bridge rural gaps. As regulators harmonise rules, market entry becomes simpler yet cyber-security standards tighten, elevating development requirements.

Regulatory Landscape

Intracranial pressure (ICP) monitoring devices are regulated as medical devices with heightened scrutiny due to their use in neurocritical care and, for invasive variants, their implantable or percutaneous nature. In the United States, FDA classifies intracranial pressure monitoring devices under 21 CFR 882.1620 as Class II devices, tying market access to performance and safety controls and to the use of recognized consensus standards during submissions.

In Europe, ICP monitoring systems fall under Regulation (EU) 2017/745 (MDR), where clinical evaluation and technical documentation aligned to Annexes II and III are central to conformity assessment and Notified Body surveillance. MDR transition timing continues to affect commercialization and lifecycle management. Regulation (EU) 2023/607 extends transitional provisions, including a deadline of 31 December 2028 for applicable Class IIb devices, which shapes recertification plans, documentation refresh cycles, and supplier change control.

Value Chain Analysis

The value chain begins with specialized inputs such as MEMS sensor components, medical-grade polymers for catheters and housings, and electronics and firmware that support signal processing and connectivity. Upstream constraints tend to cluster around limited qualified MEMS foundry capacity and sensor-grade materials, while invasive device builds add stringent biocompatibility, cleanroom assembly, and validation steps. Quality systems are reinforced by consensus standards used for design, labeling, safety, and performance (for example ANSI/AAMI NS28 series), which then feed into verification and validation planning.

In the midstream, device OEMs integrate transducers, catheters, and multi-parameter monitors, then carry out sterilization and packaging for invasive consumables, supported by regulatory documentation and post-market surveillance workflows that can slow design changes. Downstream distribution is dominated by hospital procurement and group purchasing channels for neuro-ICU and trauma center use. Service, training, and software updates also contribute to lifecycle value, particularly as wireless and multi-parameter systems increase cybersecurity and compatibility requirements across installed monitoring fleets.

Competitive Landscape

The intracranial pressure monitoring market is moderately fragmented. Medtronic leverages a broad neurosurgical catalogue plus global logistics to hold pole position. Integra LifeSciences targets niche catheters that track oxygen and temperature alongside pressure, appealing to neurointensive units demanding integrated data. Nihon Kohden expanded by acquiring Ad-Tech Medical, pairing EEG platforms with intracranial electrodes to capture long-term epilepsy care.

Younger firms disrupt with diffuse correlation spectroscopy and Doppler-based algorithms that promise catheter-level accuracy without penetration. Wireless, bioabsorbable sensors gain traction as they remove infection concerns and cut operating room time. Cyber-secure firmware becomes a differentiator as hospitals insist on zero-day patching and end-to-end encryption. White-space opportunities span paediatric-specific devices, space-flight solutions and cloud analytics that aggregate signals across entire hospital networks for predictive triage.

Strategic collaborations proliferate. Device makers team with cloud vendors to offer subscription analytics, while aerospace agencies act as test beds for extreme-environment prototypes. Suppliers able to vertically integrate piezo materials hedged against shortages during recent semiconductor disruptions, shielding production schedules.

Intracranial Pressure Monitoring Industry Leaders

Medtronic plc

RAUMEDIC AG

Sophysa Ltd

Integra LifeSciences

Natus Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product whitespace is widening at the intersection of non-invasive sensing and algorithmic inference, where systems reconstruct ICP or waveform surrogates using existing ICU signals (ECG, ABP, PPG) and deep learning, reducing dependence on dedicated invasive hardware. This direction is supported by active clinical validation activity registered on ClinicalTrials.gov and by peer-reviewed first-in-human work, including a February 2026 prospective clinical study of the Archimedes 02 non-invasive ICP pulse waveform monitor. As care teams expand monitoring beyond the ICU, workflow-oriented integration with bedside monitors and alarm systems creates room for vendors that can package software alongside cybersecurity, interoperability, and usable clinical dashboards.

A second opportunity track is chronic and home-adjacent monitoring for hydrocephalus and shunt-managed patients, enabled by implantable micro-sensors that transmit trends for remote follow-up. April 2026 peer-reviewed first-in-human results reported a 0.28 g implantable micro-sensor for remote ICP monitoring in hydrocephalus, supporting longer-duration surveillance and post-discharge management that complements acute trauma use. On commercialization, sustained FDA filing activity under Product Code GWM, alongside longer average 510(k) review times reported at about 197 days, raises the value of regulatory planning, design controls, and submission-ready clinical evidence, favoring manufacturers that can sustain iterative upgrades without disrupting supply continuity.

Recent Industry Developments

- April 2026: Sophysa received FDA 510(k) clearance for the Pressio 3 Multi-parameter Neuromonitoring System (K252241) for intracranial pressure monitoring. The clearance reinforces the shift toward integrated, multi-signal neuromonitoring platforms rather than single-parameter ICP setups, and it strengthens Sophysa's positioning in US hospital procurement cycles.

- November 2025: Sophysa initiated an FDA Class 2 recall for the Pressio 2 ICP Monitoring System (Recall Number Z-1029-2026) tied to software-related issues that could cause unintended monitor reboots. The action highlights how software stability and update management increasingly influence purchasing and replacement decisions for connected neuro-monitoring systems.

- November 2024: Nihon Kohden bought a 71.4% stake in NeuroAdvanced, the parent of Ad-Tech Medical, to deepen its neurological portfolio. The move supports tighter bundling of neuromonitoring modalities in hospital accounts and adds scale for portfolio-driven sales strategies across critical care and neurology.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices and related consumables used to measure and monitor intracranial pressure in clinical settings, including invasive and non-invasive techniques, and the associated device revenues reported across major regions.

Scope exclusions: It excludes neuromonitoring tools that do not produce an intracranial pressure reading, along with general ICU monitors and procedure-only service fees where device revenue is not separately identifiable.

Segmentation Overview

- By Technique

- Invasive

- External Ventricular Drainage (EVD)

- Micro-transducer ICP Monitoring

- Non-invasive

- Transcranial Doppler Ultrasonography

- Tympanic Membrane Displacement

- Optic Nerve Sheath Diameter

- MRI / CT-based ICP Estimation

- Other Non-invasive Techniques

- Invasive

- By Application

- Traumatic Brain Injury

- Intracerebral Haemorrhage

- Meningitis

- Other Applications

- By End-User

- Hospitals & Trauma Centres

- Neuro-intensive Care Units (NICUs)

- Ambulatory Surgical Centres

- Military & Space Health Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the demand side for intracranial pressure monitoring, then aligning it with what is visible on the supply side from public disclosures. We mainly used open sources such as the US CDC for traumatic brain injury context, the WHO for broader neurological and injury burden indicators, and OECD health statistics for hospital activity and critical care capacity signals.

To make sure device and procedure references are not being mixed up, we also reviewed sources such as the US FDA device databases for product clearances, the National Library of Medicine for clinical publications on ICP monitoring practices, and trade and customs statistics from UN Comtrade for directional import and export patterns. Company filings, investor presentations, and reputable medical press were used to cross-check product mix and geographic exposure. A paid subscription focused on company financials, plus a separate patent database, was used to sanity-check timelines and innovation cycles. These examples are not exhaustive, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on hospital-side users and channel-side participants who see actual buying patterns, including clinicians in neuro-ICU and trauma care, biomedical procurement teams, and distributors that supply acute care facilities. Since this is a global device market, inputs were checked across APAC, EMEA, and the Americas so pricing direction, adoption pace for non-invasive techniques, and usage protocols could be compared in a consistent way.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 50% |

| Mid tier: 46% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 19% | Managers: 57% | Americas: 21% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where the treated patient pool and monitoring intensity are reconstructed by region, then converted into device demand using realistic use rates in trauma, neurocritical care, and neurosurgery. Once the demand pool is shaped, revenues are derived using a split between capital equipment and recurring disposables, with price bands reflecting hospital tender behavior and typical replacement cycles.

To keep the model grounded, we used a practical set of inputs, such as traumatic brain injury and hemorrhagic stroke incidence signals, neuro-ICU and trauma center capacity indicators, invasive versus non-invasive adoption mix, average monitoring duration per patient in acute episodes, and the share of cases managed under ICP-guided protocols. Where a direct data point was missing in a country, we carried assumptions from a comparable market after adjusting for hospital density and care pathways, then stress-tested those assumptions using interview feedback.

For forecasting, we ran scenario analysis with a base case anchored to procedure growth and technology substitution, then adjusted using expert views on non-invasive uptake, infection-control preferences, and budget cycles for neurosurgical equipment. Select bottom-up checks, such as sampled ASP time series and estimated unit volumes, were used to corroborate totals and correct any unrealistic jumps.

Data Validation & Update Cycle

Validation is performed through checks that look for mismatches between the modeled totals and independent signals, including regional neuro-ICU expansion, procedure volume direction, and visible pricing movement in hospital buying. When a variance looks too large, we revisit the assumptions, re-check source logic, and re-contact selected experts to confirm whether a real market shift occurred or the model is overreacting.

Before sign-off, the work is reviewed in steps so calculation errors, currency handling, and scope boundaries are caught early. Reports are refreshed annually, and interim updates are triggered when material changes in adoption or pricing occur, followed by a final pass close to publication to reflect the latest available information.

Mordor Intelligence's Intracranial Pressure Monitoring Market Size Versus Other Published Estimates

Published estimates for intracranial pressure monitoring do not always match because the market boundary can shift between monitors only, monitors plus disposables, and broader neurocritical care monitoring bundles. Differences also come from the year used for pricing, how invasive and non-invasive techniques are handled, and whether country coverage is fully built up or partially extrapolated.

By tracking treated neurocritical care demand drivers and refreshing conversion rates from procedure volume to device usage, Mordor Intelligence keeps the estimate tied to ICP-specific monitoring events rather than wider neurology monitoring revenues. In some studies, faster adoption is assumed for non-invasive approaches, or a wider end-user net is applied, which can increase the total even when underlying acute case volumes are similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.01 B (2026) | |

| Global Research Publisher A | USD 1.82 B (2024) | Uses an earlier base year and a different forecast window, which can shift pricing levels and the invasive versus non-invasive mix when converted into revenues. |

| Industry Research Publisher B | USD 1.92 B (2025) | Uses a different base year and may apply alternate product category splits for invasive sensors and non-invasive modalities, which changes how recurring disposables are represented in the total. |

Across the three values, the spread is mainly explained by base-year selection and how each study converts clinical use into revenue across equipment and recurring items. Our approach makes the assumptions easy to trace back to case volumes, monitoring intensity, and realistic pricing bands, which helps keep the final number repeatable when the model is updated.

Key Questions Answered in the Report

What is the current size of the intracranial pressure monitoring market?

The market generated USD 2.01 billion in 2026 and is projected to hit USD 2.85 billion by 2031.

Which technique leads global revenue?

Invasive systems such as external ventricular drains held 72.85% of intracranial pressure monitoring market share in 2025.

What application segment is growing fastest?

Meningitis monitoring shows the highest growth, with a 10.76% CAGR expected through 2031.

Why is Asia-Pacific the fastest-growing region?

Large-scale hospital construction, rising trauma cases and government support for local med-tech production drive the region’s 9.11% CAGR.

How are AI and predictive analytics changing ICP care?

Machine-learning models now forecast pressure spikes up to an hour in advance with about 90% accuracy, enabling proactive treatment and better outcomes.

What is the main restraint limiting adoption?

High device and procedure costs, coupled with uneven reimbursement policies, reduce access in many emerging markets.

Page last updated on: