Air Quality Monitoring Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.62 Billion |

| Market Size (2031) | USD 7.48 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

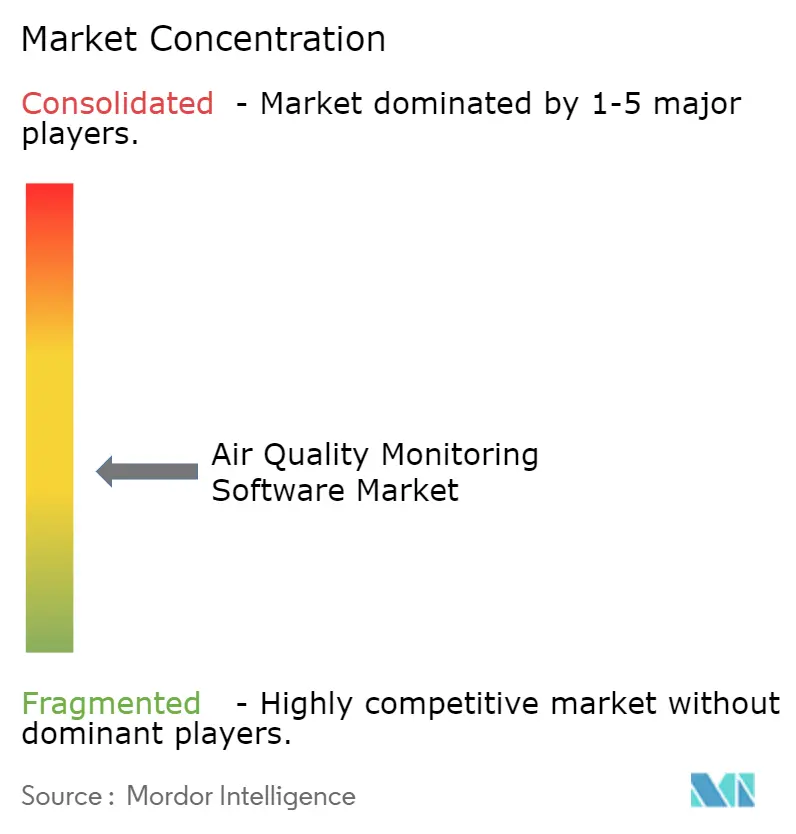

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Quality Monitoring Software Market Analysis by Mordor Intelligence

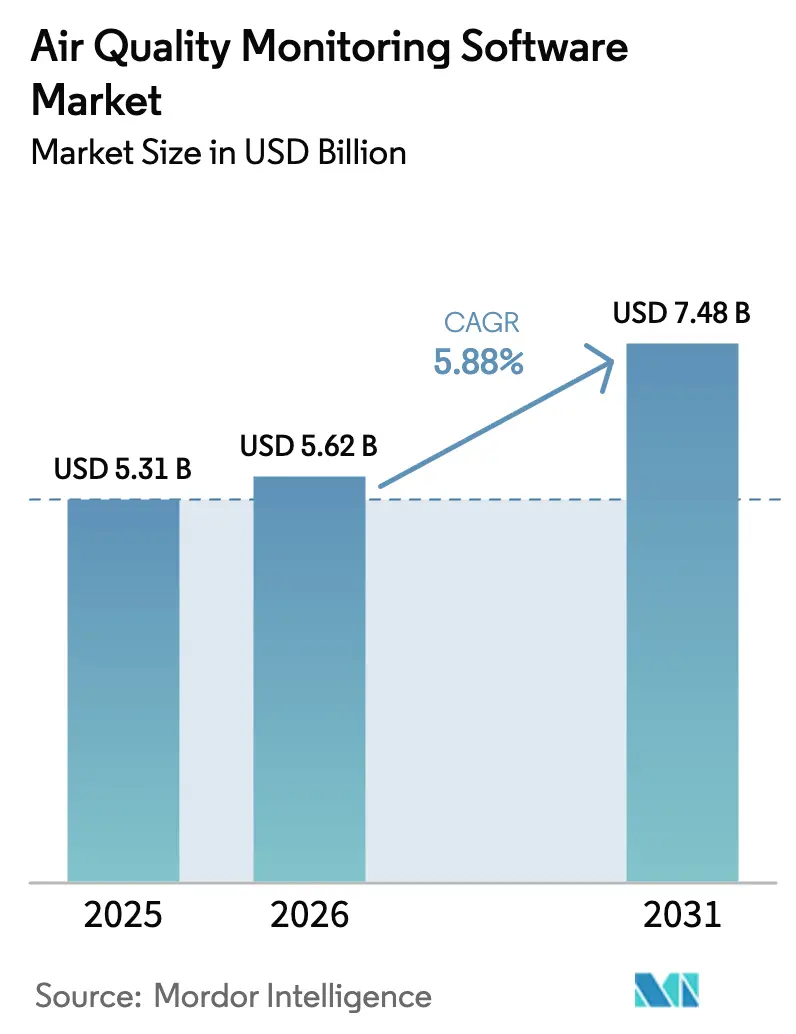

The air quality monitoring software market size is expected to grow from USD 5.31 billion in 2025 to USD 5.62 billion in 2026 and is forecast to reach USD 7.48 billion by 2031 at 5.88% CAGR over 2026-2031. Rising disclosure mandates, smart-city investments, and post-pandemic indoor air quality (IAQ) standards are together enlarging the spending pool for enterprise-grade monitoring platforms. Demand accelerates as publicly listed companies prepare for Scope 3 reporting and as municipal agencies deploy dense sensor networks that require centralised data orchestration. Sensor miniaturisation lowers entry costs, enabling software-as-a-service (SaaS) models that appeal to small and medium enterprises. At the same time, predictive analytics powered by AI allow real-time forecasting and exposure mitigation for mobility and building-automation use cases. Interoperability gaps and GDPR-driven data-localisation requirements temper adoption but also open opportunities for regional vendors with compliant architectures.

Key Report Takeaways

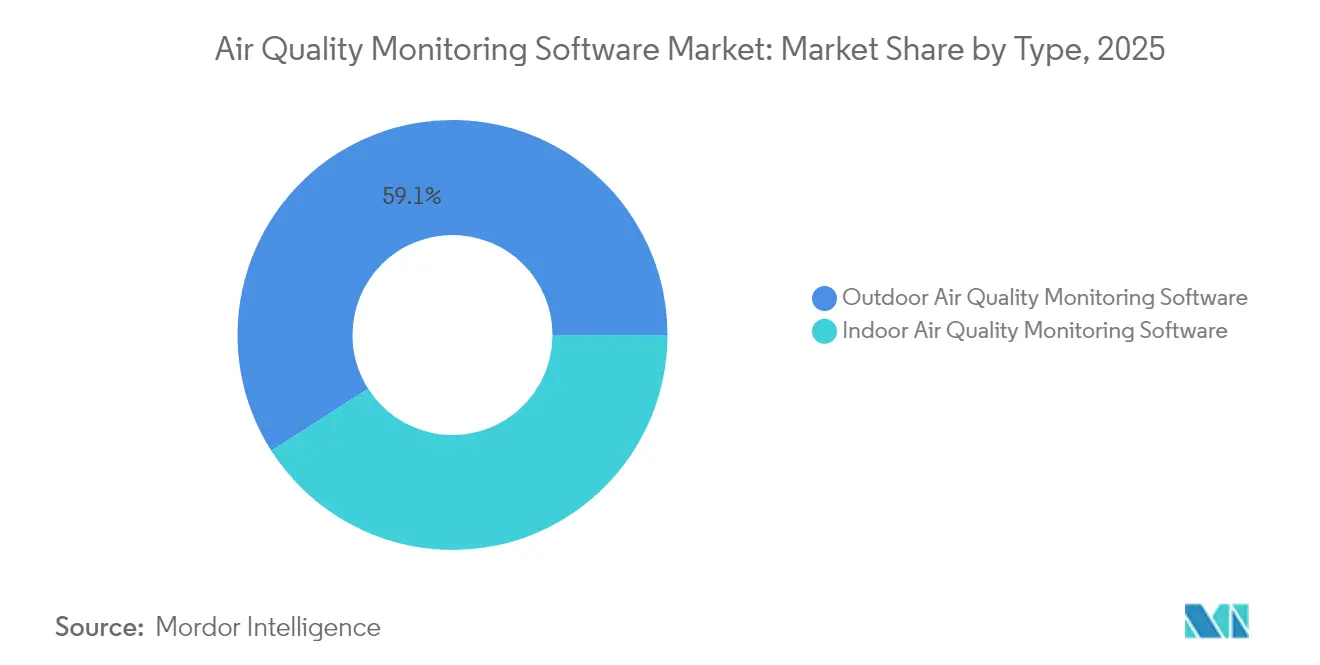

- By product type, outdoor solutions led with 59.05% of air quality monitoring software market share in 2025; indoor platforms are expected to grow at a 9.25% CAGR to 2031.

- By deployment mode, on-premise/hybrid retained 54.05% share of the air quality monitoring software market in 2025, while cloud-based offerings are expanding at an 10.85% CAGR through 2031.

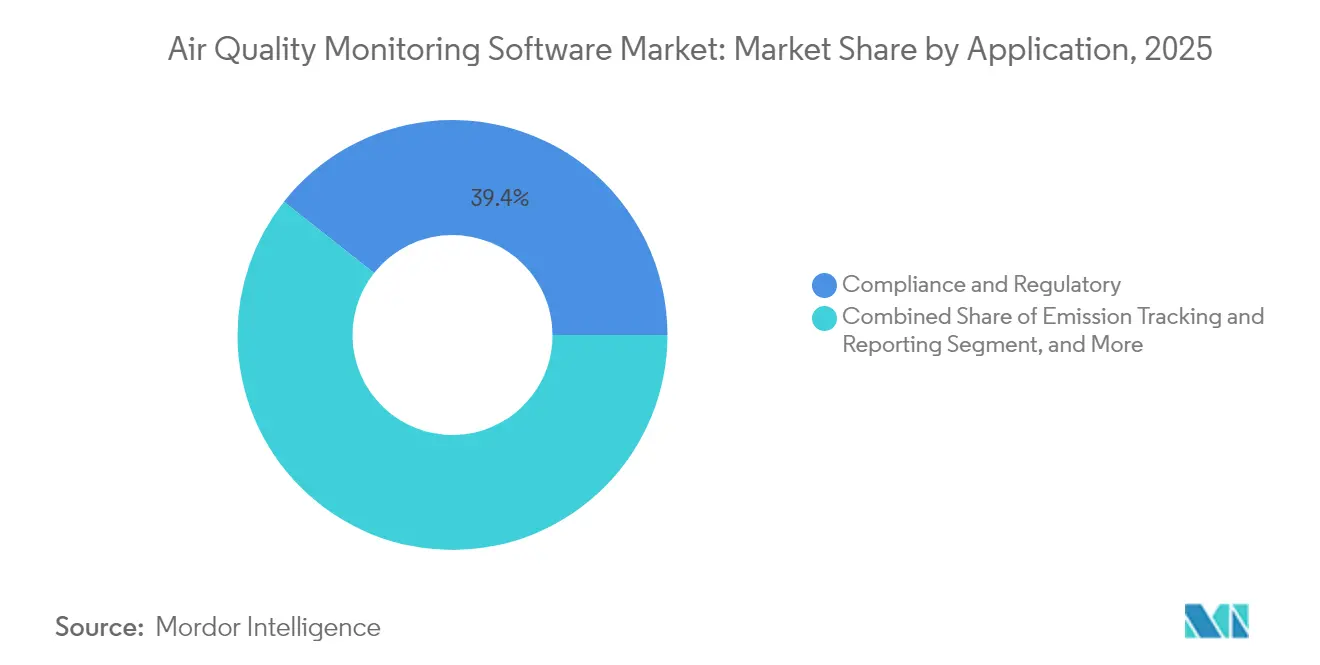

- By application, compliance and regulatory reporting captured 39.35% share of the air quality monitoring software market size in 2025; forecasting and modelling is projected to rise at an 7.85% CAGR by 2031.

- By end-user, government and municipal agencies held 34.15% revenue share in 2025; residential and commercial buildings segment is advancing at a 10.1% CAGR.

- By geography, Asia-Pacific commanded 27.75% revenue share in 2025 and is growing at an 8.05% CAGR on the back of smart-city grants and urbanisation pressures

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Quality Monitoring Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated ESG and Scope-3 disclosure rules | +1.8% | North America & Europe | Medium term (2-4 years) |

| Smart-city funding surge for hyper-local networks | +1.2% | Asia-Pacific, spill-over to MEA | Short term (≤ 2 years) |

| Post-COVID occupational IAQ standards | +0.9% | Global | Medium term (2-4 years) |

| Falling cost of IoT sensors | +0.7% | Global | Long term (≥ 4 years) |

| Carbon-credit platforms needing verifiable baselines | +0.5% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| AI-driven predictive dispersion modelling | +0.4% | Global urban centres | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandated ESG and Scope-3 disclosure rules

Climate-related reporting deadlines in California and forthcoming SEC regulations compel corporations to install continuous monitoring that can satisfy audit-grade traceability.[1]California Air Resources Board, “Mandatory GHG Reporting - Verification,” arb.ca.gov Scope 3 requirements extend visibility into supplier emissions, expanding the addressable customer base for the air quality monitoring software market. European GDPR rules drive demand for platforms with built-in data-localisation and anonymisation, benefiting regional providers able to guarantee compliance.

Smart-city funding surge for hyper-local networks

Asian governments finance dense networks of low-cost particulate-matter sensors to tackle urban pollution hotspots, creating large volumes of real-time data needing scalable analytics. Platforms that integrate multilingual dashboards and citizen-science inputs gain a competitive edge, positioning the air quality monitoring software market for rapid expansion in municipal procurement cycles.

Post-COVID occupational IAQ standards

ASHRAE 241 turned IAQ from a wellness feature into a compliance requirement for commercial buildings, pushing facility managers to embed continuous monitoring within HVAC controls.[2]Source: Trane, “How to Absorb a New Standard: ASHRAE® 241 and More,” trane.com Demand is strongest for software that maps pollutant levels against occupancy analytics, informing ventilation strategies that balance energy use and employee health

Falling cost of IoT sensors

Sensor prices have dropped while machine-learning calibration has lifted accuracy, enabling SaaS models priced for small enterprises. Distributors increasingly bundle hardware, connectivity, and dashboards, widening adoption and fuelling the long-run growth of the air quality monitoring software market.[3]MDPI, “Developing a Cloud-Based Air Quality Monitoring Platform Using Low-Cost Sensors,” mdpi.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy hardware protocol fragmentation | −0.8% | Global, acute in industrial sectors | Medium term (2-4 years) |

| GDPR-linked data-privacy concerns | −0.6% | EU core, expanding globally | Long term (≥ 4 years) |

| Limited broadband in emerging regions | −0.4% | Africa, rural APAC, Latin America | Long term (≥ 4 years) |

| Municipal budget constraints vs open-source tools | −0.3% | Global, concentrated in developing markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy hardware protocol fragmentation

Industrial sites run a mix of decades-old analysers and new IoT sensors that speak incompatible protocols, inflating integration costs and slowing roll-outs.[4]Atmospheric Measurement Techniques, “Long-term evaluation of commercial air quality sensors: an overview from the QUANT study,” amt.copernicus.org Vendors that support multi-protocol gateways or edge-computing adapters are better placed to capture demand within the air quality monitoring software market.

GDPR-linked data-privacy concerns

European rules classify location-specific sensor feeds as potentially personal data, obliging platforms to store or process information in-region and build consent workflows. The resulting architectural complexity raises operating costs and lengthens deployment timelines, particularly for cloud-native providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Outdoor dominance continues while indoor accelerates

Outdoor solutions generated the majority of spending, accounting for 59.05% of air quality monitoring software market share in 2025, driven by regulatory mandates for ambient pollutant tracking around industrial zones and urban corridors. Municipal operators require platforms that visualise data from hundreds of roadside and rooftop stations, pushing suppliers toward high-availability architectures and map-based analytics.

Indoor platforms are advancing at a 9.25% CAGR through 2031. Corporate real-estate portfolios embed sensors into building-management systems to meet ASHRAE 241 and green building certifications, creating a high-growth niche for vendors offering HVAC optimisation algorithms. Growing emphasis on employee well-being and energy performance keeps momentum strong, making indoor monitoring an expanding pillar of the air quality monitoring software market.

By Deployment Mode: Cloud migration gathers pace

On-premise and hybrid installations kept 54.05% of revenue in 2025 as heavy industry and government agencies sought tight control over environmental data. These buyers connect supervisory control and data acquisition (SCADA) systems to local servers before passing selected streams to the cloud, blending low-latency alarms with advanced analytics.

Cloud-native offerings are growing 10.85% a year. Multi-tenant SaaS platforms ingest billions of sensor readings daily and apply machine-learning models that improve with aggregated datasets. Subscription pricing lowers capex and accelerates pilots, pulling new users-especially SMEs-into the air quality monitoring software market

By Application: Compliance dominates, forecasting rises

Compliance and regulatory reporting contributed 39.35% of 2025 spend as organisations sought audit-ready data logs for emissions permitting, ESG filings, and community-right-to-know portals. Software modules that automate chain-of-custody and version control of datasets remain core purchasing criteria.

Forecasting and modelling is climbing at an 7.85% CAGR. Deep-learning ensembles now predict urban PM2.5 and ozone levels with high fidelity, enabling route-planning, health-advisory, and demand-response services. As predictive accuracy improves, this segment widens the functional scope of the air quality monitoring software market.

By End-User: Public sector leadership enables private innovation

Government and municipal agencies held 34.15% share in 2025 after receiving USD 83 million in federal grants for network expansion, including allocations for disadvantaged communities. Public deployments set data standards that shape private-sector tender specifications.

Residential and commercial buildings represent the fastest-growing customer class at a 10.1% CAGR. Prop-tech managers integrate IAQ dashboards into space-utilisation analytics, while insurers start to incorporate indoor air metrics into policy pricing. This momentum diversifies revenue streams across the air quality monitoring software industry.

Geography Analysis

Asia-Pacific accounted for 27.75% of 2025 revenue and is expanding at an 8.05% CAGR as megacity authorities deploy hyper-local networks funded by national smart-city programmes. University-backed initiatives that fill PM2.5 data gaps further catalyse platform adoption across densely populated corridors.

North America leverages strong regulatory drivers, including California’s Scope 3 rules, and sizeable federal grants to modernise state-wide monitoring grids. Enterprise customers take advantage of mature cloud infrastructure, fuelling demand for AI-enabled forecasting modules within the air quality monitoring software market.

Europe records steady uptake as GDPR-compliant platforms carve out a premium niche. Vendors differentiate through in-region hosting and edge-processing capabilities that minimise personal-data exposure. Middle East & Africa adopt explainable-AI models for SO₂ prediction around industrial hubs, though patchy broadband coverage sustains demand for hybrid architectures.

Competitive Landscape

The market remains moderately fragmented. Instrumentation leaders such as Thermo Fisher Scientific retain long-standing regulatory relationships and have secured more than USD 12.9 million in US federal contracts for environmental monitoring equipment. Hardware suppliers are merging analytics capabilities, as seen in the July 2025 SICK–Endress+Hauser joint venture that pools 730 staff to advance emissions monitoring technology.

Start-ups focus on low-cost sensor networks and AI-ready data lakes, while platforms like OpenAQ encourage open-source data sharing, pressuring proprietary vendors on baseline functionality. Cloud hyperscalers demonstrate disruptive potential; Microsoft’s Aurora system performs globe-scale forecasting in less than a minute, setting new performance benchmarks.

Strategic moves underscore rising consolidation. Hitachi Construction Machinery took a stake in Envirosuite to extend monitoring into mining operations. Honeywell launched an emissions suite for offshore platforms, expanding its footprint in the air quality monitoring software market automation.

Air Quality Monitoring Software Industry Leaders

Thermo Fisher Scientific Inc.

Siemens AG

Robert Bosch GmbH.

Honeywell HBT

Aeroqual Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SICK and Endress+Hauser formed a joint venture dedicated to gas analysis and flow-measurement solutions for emissions compliance.

- June 2025: Sensirion and Terabee partnered to integrate advanced indoor IAQ sensors with analytics platforms for health-focused building applications.

- April 2025: EPIC awarded six grants aimed at improving air quality monitoring methodologies and data accessibility in developing regions.

- March 2025: Teledyne introduced ACES®, the first FAA-certified aircraft air quality monitoring system enabling in-flight pollutant tracking.

- January 2025: Honeywell released its Emissions Management Suite for offshore oil and gas platforms, providing near-real-time oversight of emissions performance.

Global Air Quality Monitoring Software Market Report Scope

Air quality monitoring software is an instrument that assists in making long-term strategic decisions regarding air quality. It is an information system that gives people the data for scientifically informed strategic planning and decision-making on air quality in a user-friendly environment in the form of an interactive map.

The Air Quality Monitoring Software Market is segmented by Type (Indoor AQMS and Outdoor AQMS), End-User (Residential and Commercial, Industrial and Public Agencies -Government, Research Institutes, and UAQMA), and Geography (North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Indoor AQ Monitoring Software |

| Outdoor AQ Monitoring Software |

| Cloud-based |

| On-premise/Hybrid |

| Emission Tracking and Reporting |

| Compliance and Regulatory |

| Forecasting and Modeling |

| Data Visualization and Analytics |

| Residential and Commercial Buildings |

| Industrial Facilities (Oil and Gas, Manufacturing, Power Plants) |

| Government and Municipal Agencies |

| Research Institutes and Universities |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Indoor AQ Monitoring Software | ||

| Outdoor AQ Monitoring Software | |||

| By Deployment Mode | Cloud-based | ||

| On-premise/Hybrid | |||

| By Application | Emission Tracking and Reporting | ||

| Compliance and Regulatory | |||

| Forecasting and Modeling | |||

| Data Visualization and Analytics | |||

| By End-User | Residential and Commercial Buildings | ||

| Industrial Facilities (Oil and Gas, Manufacturing, Power Plants) | |||

| Government and Municipal Agencies | |||

| Research Institutes and Universities | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the air quality monitoring software market?

The market generated USD 5.62 billion in 2026 and is projected to reach USD 7.48 billion by 2031 at a 5.88% CAGR.

Which region leads spending on air quality monitoring platforms?

Asia-Pacific held 27.75% of global revenue in 2025 and shows the fastest growth, supported by smart-city initiatives and rapid urbanisation.

Why are indoor monitoring solutions growing faster than outdoor platforms?

Post-COVID health standards (e.g., ASHRAE 241) and green-building certifications have turned continuous IAQ tracking into a core operational requirement for commercial real estate.

How are disclosure regulations influencing demand?

Scope 3 rules in California and upcoming SEC climate disclosures oblige companies to deploy continuous monitoring that generates audit-grade data, directly boosting enterprise adoption.

What role does AI play in modern air quality software?

AI enables high-resolution forecasting, sensor calibration, and anomaly detection; Microsoft’s Aurora model forecasts global pollution in sub-minute times, illustrating the step-change in capability.

Are cloud-based deployments overtaking on-premise systems?

Yes. Although on-premise/hybrid still owns 54.05% share, cloud platforms are expanding at an 10.85% CAGR thanks to scalability and lower up-front costs.

Page last updated on: