Distributed Acoustic Sensing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

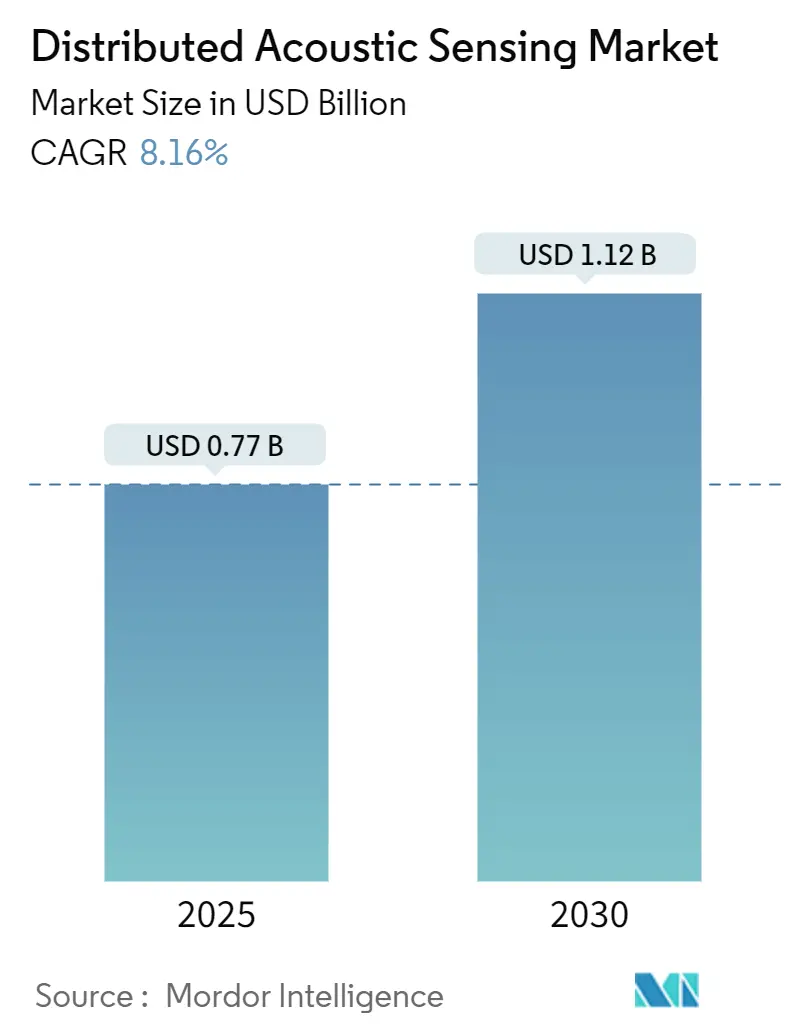

| Market Size (2025) | USD 0.77 Billion |

| Market Size (2030) | USD 1.12 Billion |

| Growth Rate (2025 - 2030) | 8.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Distributed Acoustic Sensing Market Analysis by Mordor Intelligence

The distributed acoustic sensing market is valued at USD 0.77 billion in 2025 and is forecast to reach USD 1.12 billion by 2030, reflecting an 8.16% CAGR. Rising deployments of single-mode and multi-mode fiber along pipelines, rail corridors, and power cables are enlarging the addressable base for interrogator hardware and analytics software. Operators are adopting the technology to detect leaks, third-party interference, micro-seismicity, and structural anomalies across assets that stretch for hundreds of kilometers, eliminating the need for thousands of discrete point sensors. Artificial-intelligence–enhanced algorithms now classify acoustic signatures with more than 91% accuracy, enabling actionable insights to be delivered in near real time. Hardware innovation is also reducing total cost of ownership, with silicon-photonic interrogators achieving sub-meter spatial resolution at lower power budgets.[1]Zhicheng Jin et al., “Silicon Photonic Integrated Interrogator for Fiber-Optic Distributed Acoustic Sensing,” Photon. Res., optica.orgGrowth is further supported by regulations mandating continuous pipeline monitoring in the United States and European Union, along with Asia Pacific infrastructure expansions, particularly China’s high-speed rail network.

Key Report Takeaways

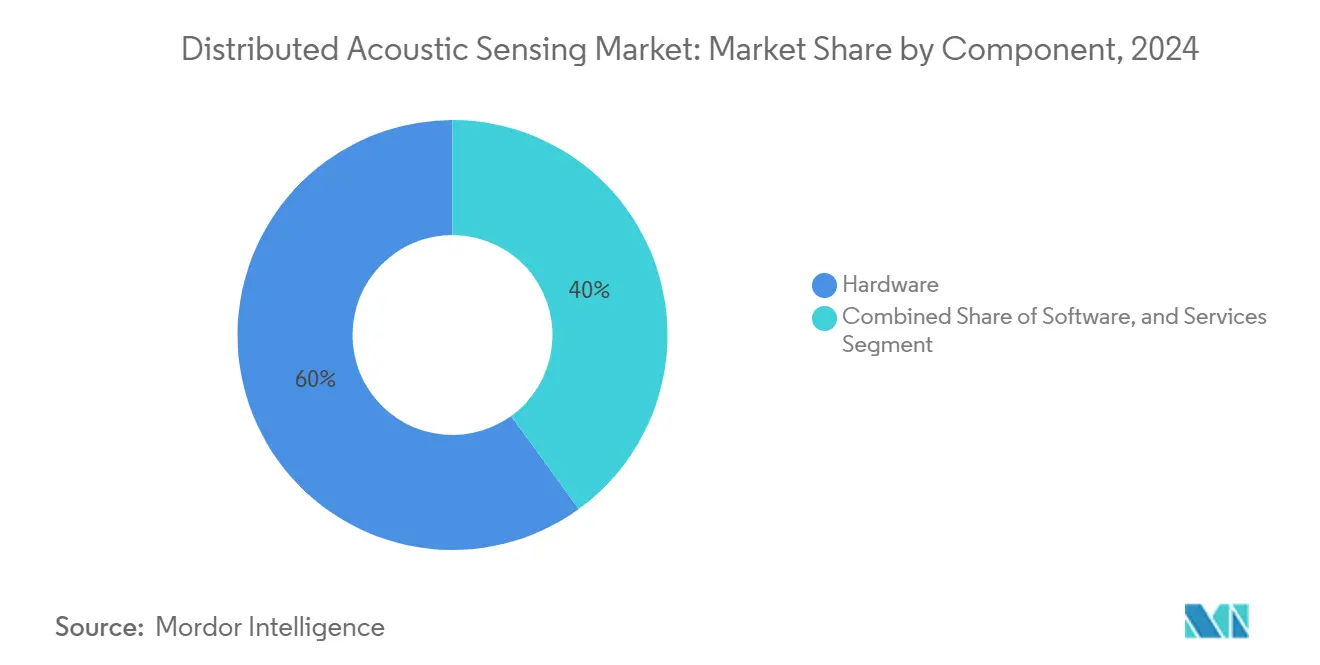

- By component, hardware led with 60% revenue share in 2024, while services are advancing at an 11.1% CAGR through 2030.

- By fiber type, single-mode held 71% of the distributed acoustic sensing market share in 2024; multi-mode is poised for the fastest 12.4% CAGR to 2030.

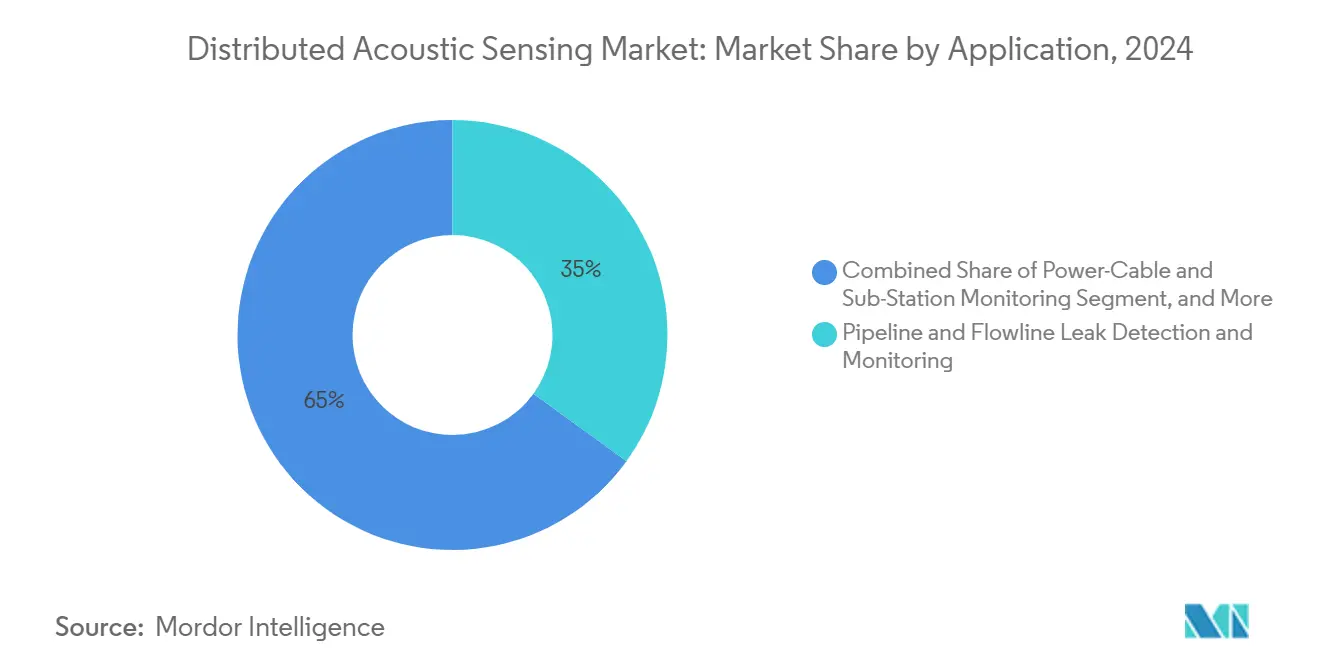

- By application, pipeline and flowline monitoring commanded 35% share of the distributed acoustic sensing market size in 2024, whereas perimeter security is projected to expand at a 10.3% CAGR.

- By end-use industry, oil and gas accounted for 46% of the distributed acoustic sensing market size in 2024, with utilities predicted to grow at a 9.7% CAGR.

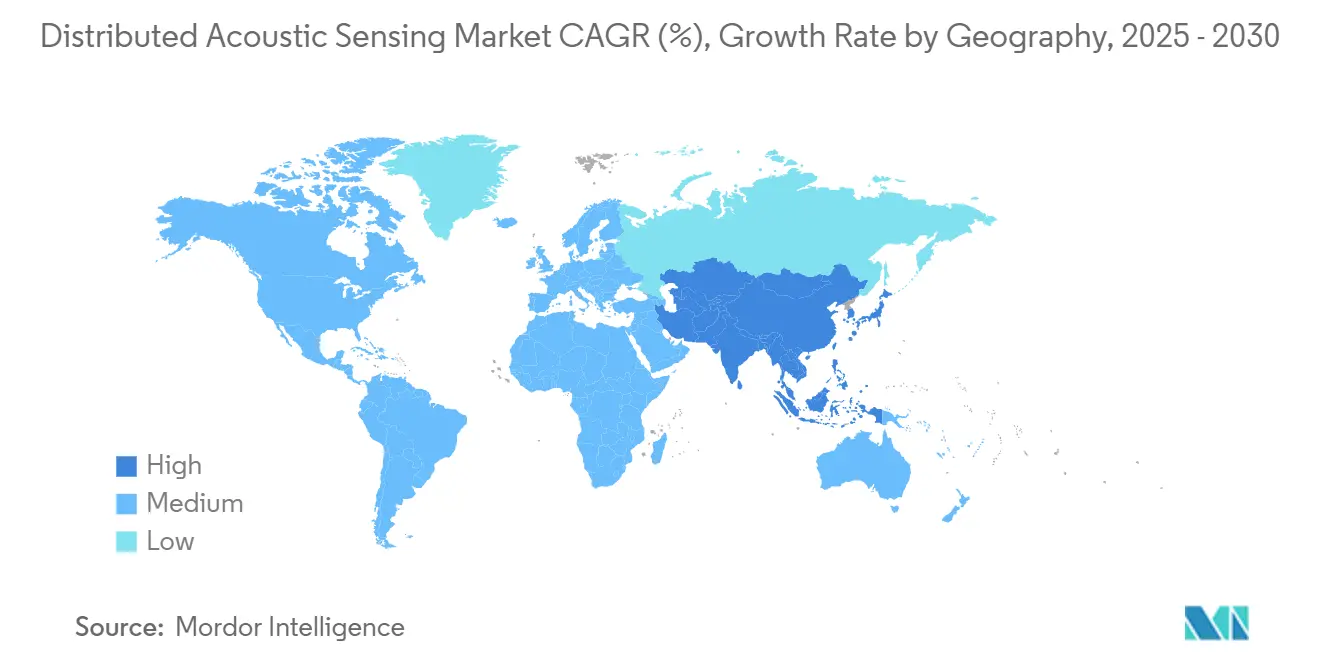

- By geography, North America led with a 35.7% share in 2024, but Asia Pacific is expected to post the highest 10.1% CAGR between 2025-2030.

Global Distributed Acoustic Sensing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Wellbore-Intervention Volumes in North American Shale Plays | +1.8% | North America | Medium term (2-4 years) |

| Mandatory Pipeline Integrity Regulations in US and EU Driving Continuous Acoustic Monitoring | +1.5% | North America & Europe | Short term (≤ 2 years) |

| Deployment of Fiber-based Train Speed Enforcement in China's High-Speed Rail Network | +1.2% | Asia Pacific | Medium term (2-4 years) |

| UK's OFTO Model Fueling Sub-Sea Power-Cable DAS Adoption | +0.9% | Europe | Medium term (2-4 years) |

| Carbon-Capture & Storage (CCS) Projects Requiring Permanent Downhole DAS Arrays | +1.1% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Saudi Aramco's iDAS-Enabled Mega-Fields Boosting Middle-East Demand | +0.7% | Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising wellbore-intervention volumes in North American shale plays

Elevated refracturing and workover activity-exceeding 12,000 interventions in 2024-demands continuous downhole monitoring that only DAS can deliver. Halliburton’s FiberVSP service combines vertical-seismic profiling with coiled-tubing operations, shortening rig time by up to 60%.[2]Halliburton, “FiberVSP Service Acquires Quality VSP Data in Less Time,” halliburton.comOperators use DAS to pinpoint micro-seismic events during fracturing, optimize stage spacing, and mitigate well interference, directly enhancing recovery factors and lowering lift costs.

Mandatory pipeline integrity regulations in the United States and European Union

PHMSA rules now require detection of leaks as small as 1% of flow within 15 minutes, thresholds that distributed acoustic sensing market solutions meet by monitoring entire line lengths in real time. Cross-correlation algorithms have reduced localization error from 7.96 m to 0.11 m.[3]Bob Paap et al., “Leveraging Distributed Acoustic Sensing for Monitoring Vessels Using Submarine Fiber-Optic Cables,” Applied Ocean Research, sciencedirect.comEurope’s revised Gas Directive imposes similar mandates, accelerating urgent upgrades on trans-border corridors.

Deployment of fiber-based train-speed enforcement in China’s high-speed rail network

China’s network surpassed 45,000 km in 2024 and will exceed 70,000 km by 2030. DAS is now mandatory along new corridors, achieving 95% defect-detection accuracy at 350 km/h and providing seismic-event early warning in earthquake-prone areas.[4]Hong-Hu Zhu et al., “Distributed Acoustic Sensing for Monitoring Linear Infrastructures: Current Status and Trends,” Sensors, mdpi.comThe resulting demand underpins the fastest regional growth outlook in Asia Pacific.

Carbon-capture and storage projects requiring permanent downhole arrays

Global CCS capacity is projected to quintuple to 200 million t by 2030. DAS arrays detect micro-seismicity up to 5 km from injection wells, confirming CO₂ plume confinement and satisfying regulatory oversight.[5]Bob Paap et al., “Leveraging Distributed Acoustic Sensing for Monitoring Vessels Using Submarine Fiber-Optic Cables,” Applied Ocean Research, sciencedirect.com Lifetime monitoring obligations create a multidecade revenue stream for service providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Trained Interrogator-Unit Field Engineers in Latin America | -0.8% | Latin America | Medium term (2-4 years) |

| DAS Signal-to-Noise Degradation in Sub-Sea Umbilicals | -0.6% | Global, with concentration in regions with offshore operations | Short term (≤ 2 years) |

| Cap-Ex Inflation for Armoured Fiber in Arctic & Desert Pipelines | -0.5% | Middle East, Russia, Canada | Medium term (2-4 years) |

| Data-Lake Storage Costs for 100 kHz-Rate Distributed Sensing Streams | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Trained Interrogator-Unit Field Engineers in Latin America

Vacancy rates for DAS specialists exceeded 70% in 2024, extending average commissioning delays to 4.3 months in Brazil’s presalt fields.Training a field engineer to proficiency with DAS systems typically requires 12-18 months of specialized education and hands-on experience, creating a significant lag between market demand and available expertise. Although service majors are opening training centers, the talent pipeline lags regional demand, elevating project costs through expatriate staffing

DAS Signal-to-Noise Degradation in Sub-Sea Umbilicals

At depths beyond 1,000 m, ambient and electromagnetic interference can cut signal quality by 40%, masking small leaks or anchor drags. Specialized marine fibers add 35-40% to material costs, hampering adoption in brownfield retrofits despite algorithmic advances in noise filtering. The problem is particularly acute in umbilicals that combine power cables and fiber optics, where electromagnetic interference from power transmission creates additional noise sources that conventional filtering struggles to eliminate. While advanced signal processing algorithms and machine learning approaches are showing promise in distinguishing signals from noise, these solutions require substantial computational resources and specialized expertise to implement effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Leadership Faces Services Upswing

Hardware holds the largest distributed acoustic sensing market share at 60% in 2024. Interrogator units now achieve strain resolutions of 59 pε/√Hz with 1.14 m spatial resolution over 12.1 km. The distributed acoustic sensing market size for hardware segment was USD 0.46 billion in 2024 and is expanding at 6.5% CAGR as silicon-photonic chips shrink footprints for offshore and urban deployments.

Services form the fastest-growing revenue pool, projected at an 11.1% CAGR through 2030. Operators require data-science consulting to interpret daily data volumes exceeding 2 TB per kilometer. Training, commissioning, and analytics contracts are outpacing pure equipment sales, pushing vendors to bundle lifetime service agreements. The distributed acoustic sensing industry increasingly regards data-analytics intellectual property as a competitive moat, prompting cross-licensing deals between photonics manufacturers and AI software specialists.

By Fiber Type: Single-Mode Predominance Meets Multi-Mode Momentum

Single-mode fiber accounted for 71% of 2024 revenues thanks to lower attenuation across >100 km backbones. The distributed acoustic sensing market size attributed to single-mode deployments is forecast to climb at 7.2% CAGR as operators retrofit existing telecom dark fiber for sensing functions. Precision localization at 1.14 m enables leak detection in high-consequence pipeline corridors, safeguarding community and environmental health.

Multi-mode fiber enjoys a 12.4% CAGR outlook. New coherent-averaging methods cut noise by threefold, unlocking dual DTS-and-DAS use in temperature-sensitive wells. The distributed acoustic sensing industry is adopting hybrid cable designs that house both core types, allowing operators to optimize range and temperature response without multiple fiber strings.

By Application: Pipeline Monitoring Dominance Amid Security Surge

Pipeline and flowline surveillance captured 35% of 2024 revenues, underpinned by regulations that demand leak detection within minutes. Advanced cross-correlation pinpoints pinhole leaks at 0.11 m accuracy. The distributed acoustic sensing market share for this segment will remain the largest through 2030 as aging infrastructure and stricter ESG audits intensify monitoring needs.

Perimeter and border security adoption is accelerating at a 10.3% CAGR. DAS turns fences, rail beds, and buried conduits into linear microphones that identify footsteps, digging, or vehicular approach, closing blind spots in conventional camera networks. Urban pilots classify vehicles with 85% accuracy using existing telecom cables, creating cost-effective smart-city traffic management solutions.

By End-use Industry: Oil & Gas Core with Utility Upside

Oil and gas remain the anchor vertical with 46% of 2024 expenditures. Upstream operators deploy DAS for hydraulic-fracture diagnostics and production logging; midstream companies use the technology for pig tracking and integrity management; downstream refineries monitor pipe racks and storage tanks to spot steam-hammer events. Strain-rate resolution in the nanostrain domain allows fracture-propagation monitoring in unconventional reservoirs.

Utilities lead future upside with a 9.7% CAGR forecast. Grid owners are rolling out fiber along overhead lines and underground ducts to detect conductor slap, ice loading, and third-party excavation before failures occur. Yokogawa’s Hyper-Scan deployment in winter grids now provides real-time icing alerts for dispatch centers.[6]Yokogawa Electric Corp., “Hyper-Scan Fiber-Sensing for Power-Line Health,” yokogawa.comEarly fault localization shrinks restoration time and mitigates wildfire risk, reinforcing the distributed acoustic sensing market as an integral layer in modern grid-resilience strategies.

Geography Analysis

North America generated 35.7% of global revenue in 2024. The United States’ shale sector, with 12,000 interventions in 2024, integrates DAS in live coiled-tubing operations to curtail non-productive time and safeguard well integrity. PHMSA compliance deadlines sustain hardware demand along crude and refined-product corridors, while DOE-backed CCS pilots require permanent arrays for plume migration tracking. Existing telecom dark fiber along interstate rights-of-way further lowers deployment costs, maintaining regional leadership in the distributed acoustic sensing market.

Asia Pacific is the fastest-expanding territory at a 10.1% CAGR through 2030. China’s mandate for fiber-optic train-speed enforcement spans the world’s largest 45,000-km high-speed rail grid and underpins metro-scale deployments in seismic early-warning networks. India’s 18,000-km national gas grid and Southeast Asia’s offshore wind cables offer additional momentum. Governments endorse local fiber-manufacturing capacity, ensuring supply-chain resilience for rapid rollouts.

Europe commands a significant share anchored by offshore-wind expansion and the OFTO framework that penalizes cable downtime. North Sea projects now specify DAS monitoring for all export cables, achieving 98% accuracy in detecting anchor drags. EU directives on cross-border pipeline monitoring and CO₂ transport intensify adoption, while high-speed rail operators across France, Spain, and Italy embed DAS for intrusion detection.

The Middle East and Africa demonstrate rising uptake as national oil companies pursue digital-oilfield blueprints. Saudi Aramco’s intelligent DAS roll-out boosted fracture efficiency by 23% in unconventional gas assets, catalyzing deployments across ADNOC and QatarEnergy programs. Harsh-desert armored-cable innovations are now exported globally.

Latin America remains nascent but promising. Brazil’s offshore presalt operators integrate DAS into subsea flowlines, albeit slowed by an engineer skills gap that delays commissioning by 4.3 months. Mexico’s pipeline-security initiatives and Argentina’s real-time pig-tracking pilots illustrate growing recognition of DAS value in safeguarding high-risk assets.

Competitive Landscape

The distributed acoustic sensing market is moderately concentrated, with a blend of oilfield service majors, photonics specialists, and emerging telecom equipment vendors. Silixa, OptaSense (Luna Innovations), AP Sensing, Halliburton, and Bandweaver command notable installed bases. Vendors differentiate on interrogator sensitivity, spatial resolution, and embedded analytics. Silixa’s registred Carina system enhances subsurface monitoring by amplifying backscatter without increasing laser power, a critical advantage for deep wells. OptaSense filed patents for low-cost component stacks that could democratize entry-level systems.

Partnerships between hardware and AI software firms are reshaping the value chain. Service companies bundle lifetime data-analytics contracts, creating annuity income streams and customer lock-in. Open-architecture APIs are emerging as procurement criteria, allowing operators to integrate DAS feeds with enterprise historians and digital-twin platforms.

Segmented competition is intensifying. High-performance subsea and CCS applications remain the province of premium vendors offering ruggedized interrogators and marine cables. Conversely, perimeter-security and smart-city deployments attract lower-cost entrants leveraging commoditized photonics. Cross-industry collaborations-such as telecom carriers leasing dark fiber to sensing service providers-are expanding addressable markets and blurring traditional industry boundaries.

Distributed Acoustic Sensing Industry Leaders

Halliburton Company

Schlumberger Limited

Baker Hughes Company

OptaSense

Silixa Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AP Sensing upgraded its qDoBS Method for power-cable monitoring, earning Fiber Optic Sensing Association recognition for enhancing fault localization in subsea and underground grids.

- April 2025: Silixa introduced a DAS platform tailored for CCS, detecting micro-seismicity beyond 5 km from injection wells, enabling regulatory-compliant long-term monitoring.

- March 2025: OptaSense (Luna Innovations) filed a patent for low-cost component DAS interrogators aimed at cost-sensitive perimeter security.

- February 2025: Bandweaver debuted picoDAS, delivering distance-independent sensitivity for downhole and pipeline application.

- January 2025: Yokogawa launched Hyper-Scan fiber sensing for winter power-line health monitoring, detecting icing events in real time.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the distributed acoustic sensing (DAS) market as revenues generated from fiber-optic interrogator units and associated software that convert back-scattered light into continuous vibration profiles for asset-monitoring tasks across oil and gas, power and utility, transportation, security, and environmental infrastructure. According to Mordor Intelligence, sales of new DAS hardware plus bundled analytics and basic services reached USD 0.77 billion in 2025, with data tracked globally across all deployment environments.

Standalone perimeter-security packages that use fiber sensing but do not provide end-user access to raw or processed acoustic data are outside the study's scope.

Segmentation Overview

- By Component

- Hardware (Interrogator Units)

- Software (Visualization/Analytics)

- Services

- Installation and Commissioning

- Training and Data-Science Services

- By Fiber Type

- Single-Mode Fiber

- Multi-Mode Fiber

- By Application

- Oilfield Services - Hydraulic Fracture Monitoring

- Pipeline and Flowline Leak Detection

- Perimeter and Border Security

- Rail-Track Integrity and Train Speed Enforcement

- Power-Cable and Sub-Station Monitoring

- Seismic and Micro-Earthquake Monitoring

- Structural Health in Smart Cities

- Environmental and Wildlife Monitoring

- By End-use Industry

- Oil and Gas

- Upstream

- Midstream

- Downstream

- Utilities and Power

- Transportation and Logistics

- Military and Homeland Security

- Mining and Geothermal

- Construction and Infrastructure

- Oil and Gas

- By Geography

- North America

- Europe

- Asia-Pacific

- South America

- Middle East

- Africa

Detailed Research Methodology and Data Validation

Primary Research

Multiple conversations with fiber-optic interrogator manufacturers, oilfield service engineers in North America and the Middle East, rail-safety integrators in Europe, and Asian-based utilities helped us validate penetration assumptions, price dispersion, lifecycle replacement rates, and regional regulatory triggers that secondary data only hinted at.

Desk Research

We began with public statistics from bodies such as the US Pipeline and Hazardous Materials Safety Administration, the International Association of Oil and Gas Producers, and the International Union of Railways, which quantify pipeline lengths, well counts, and track kilometers. Trade associations like the Fiber Optic Sensing Association, patent archives on Questel, and incident databases from the European Union Agency for Railways added technology adoption clues and failure rates. Corporate 10-Ks, investor decks, and regional tender portals then helped us benchmark average selling prices and contract sizes. Dow Jones Factiva supplied deal flow and competitive activity. The sources listed are illustrative; many additional datasets fed our desk review and cross-checks.

Market-Sizing and Forecasting

A top-down build starts with installed pipeline, wellbore, rail, and power-cable kilometers by region; these asset pools are then matched with empirically observed DAS penetration ratios that our interviews refined. Bottom-up roll-ups of sampled vendor shipments and service contracts check the totals. Key variables include well-intervention counts, new pipeline kilometers, fiber cost curves, regulatory inspection intervals, typical interrogator unit life, and average service attach rates. Multivariate regression with lagged macro indicators and asset additions underpins the 2025-2030 forecast, while scenario analysis cushions for oil price swings and infrastructure stimulus programs. Data gaps in vendor volumes are bridged through weighted ASP times volume proxies using Hoovers financials and selective channel checks.

Data Validation and Update Cycle

Mordor analysts subject every model iteration to variance and anomaly screens versus independent benchmarks, re-engage experts when deviations exceed set thresholds, and escalate for senior review before sign-off. Reports refresh each year, and material events such as a major pipeline safety directive trigger interim updates; a final sense-check is performed immediately prior to client delivery.

Why Mordor's Distributed Acoustic Sensing Baseline Stands Up to Scrutiny

Published DAS estimates vary because firms choose different asset pools, bundle services inconsistently, or apply divergent price pathways.

Key gap drivers include rival studies counting bundled perimeter-security kits, assuming uniform double-digit ASP erosion, or projecting aggressive oilfield recovery scenarios without reconciling with actual well-intervention budgets. Mordor's scope aligns revenue strictly with stand-alone DAS solutions, applies asset-specific penetration ramps, and benefits from an annual refresh cadence that removes obsolete COVID-era assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.77 B (2025) | Mordor Intelligence | - |

| USD 2.66 B (2024) | Global Consultancy A | Includes turnkey perimeter kits and assumes 20 percent annual ASP increase, inflating totals |

| USD 0.70 B (2024) | Industry Journal B | Excludes transportation deployments and uses static oil-price scenario, understating growth |

| USD 0.98 B (2025) | Research Boutique C | Applies uniform global penetration without region-specific asset baselines |

In short, the disciplined asset-based scoping, blended top-down and bottom-up modeling, and yearly refresh cycle mean Mordor's baseline offers decision-makers a balanced, transparent view they can readily trace back to tangible variables and repeatable steps.

Key Questions Answered in the Report

What is driving current demand in the distributed acoustic sensing market?

Pipeline-integrity regulations in the United States and European Union, along with China’s high-speed rail expansion, are prompting operators to adopt DAS for continuous leak detection, intrusion monitoring, and train-speed enforcement.

Which segment of the distributed acoustic sensing market is growing fastest?

Services, particularly data-analytics and training, are expanding at an 11.1% CAGR because operators need expertise to interpret multi-terabyte daily data streams.

Why is multi-mode fiber gaining ground in distributed acoustic sensing systems?

Advances in coherent-averaging have reduced noise, making multi-mode fibers attractive for applications requiring temperature sensing alongside acoustic monitoring.

How does DAS benefit carbon-capture and storage projects?

Permanent downhole DAS arrays detect micro-seismic events up to 5 km from injection wells, verifying CO₂ plume confinement and supporting regulatory compliance.

What technical challenge limits DAS adoption offshore?

Signal-to-noise degradation in subsea umbilicals can cut detection sensitivity by 40% at depths beyond 1,000 m, although specialized marine fibers and improved algorithms are mitigating the issue.

Which region will grow fastest through 2030?

Asia Pacific, led by China’s mandatory fiber-optic sensing on high-speed rail corridors, is projected to register a 10.1% CAGR in distributed acoustic sensing market revenues.

Page last updated on: