Nitrous Oxide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

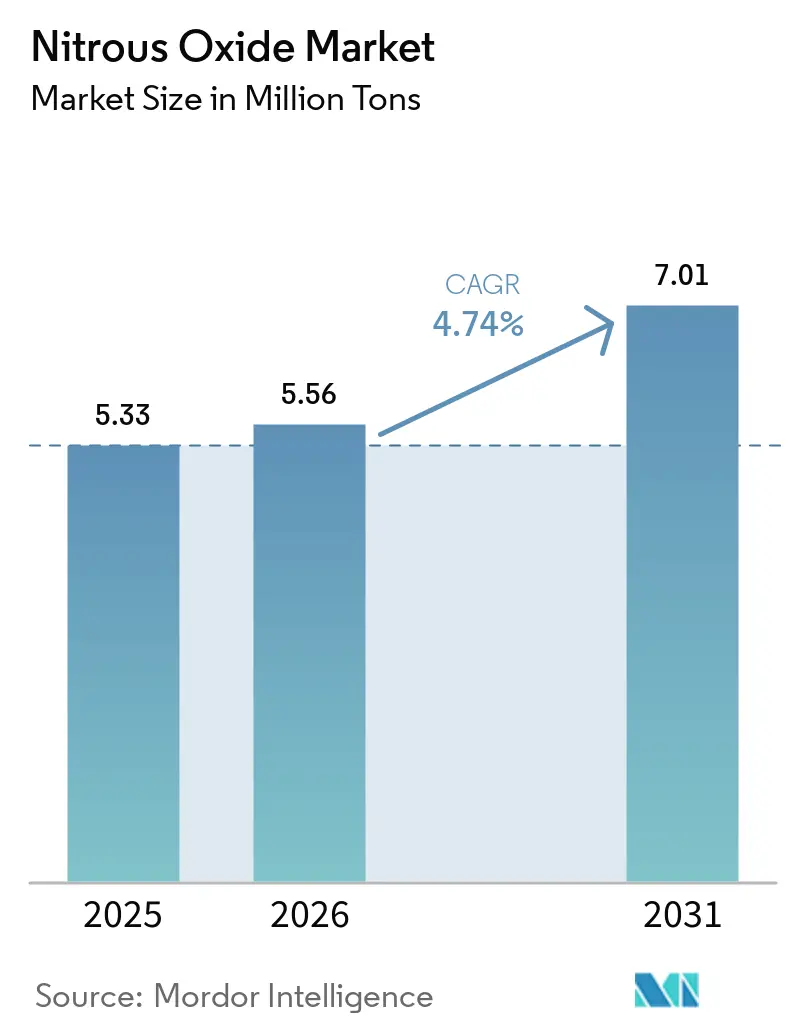

| Market Volume (2026) | 5.56 Million tons |

| Market Volume (2031) | 7.01 Million tons |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nitrous Oxide Market Analysis by Mordor Intelligence

The Nitrous Oxide Market size is projected to expand from 5.33 Million tons in 2025 and 5.56 Million tons in 2026 to 7.01 Million tons by 2031, registering a CAGR of 4.74% between 2026 to 2031. While medical-grade volumes currently dominate trade, demand profiles are shifting due to tightening global greenhouse-gas regulations, an expanding semiconductor industry, and emerging aerospace monopropellant applications. Regional dynamics are split: Asia-Pacific is capitalizing on its semiconductor prowess and swiftly modernizing clinical infrastructure, whereas the Middle East & Africa is experiencing the fastest growth, with hospitals and packaged-gas distributors expanding from a modest starting point. The competitive landscape is moderately intense, with five multinational industrial-gas giants holding sway over most air-separation and logistics assets. However, only a handful have ventured into dedicated high-purity nitrous oxide production, leaving a gap for specialty-gas entrants. Additionally, contrasting regulations, such as the EU's strict climate and recreational-abuse policies versus the U.S.'s lenient vehicle standards, are poised to influence supply flows, tighten margins in certain areas, and create opportunities for more lucrative ultra-high-purity contracts.

Key Report Takeaways

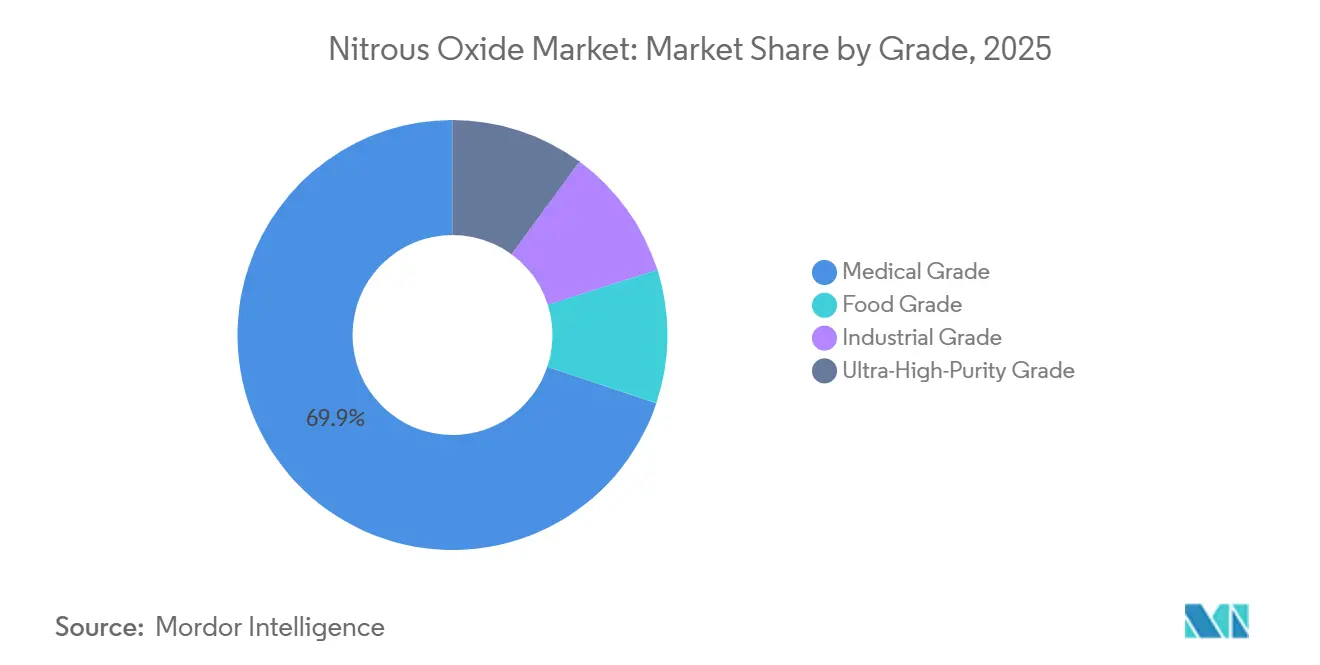

- By grade, Medical Grade captured 69.85% of the Nitrous Oxide market share in 2025, while Industrial Grade is forecast to expand at a 5.41% CAGR from 2026 to 2031.

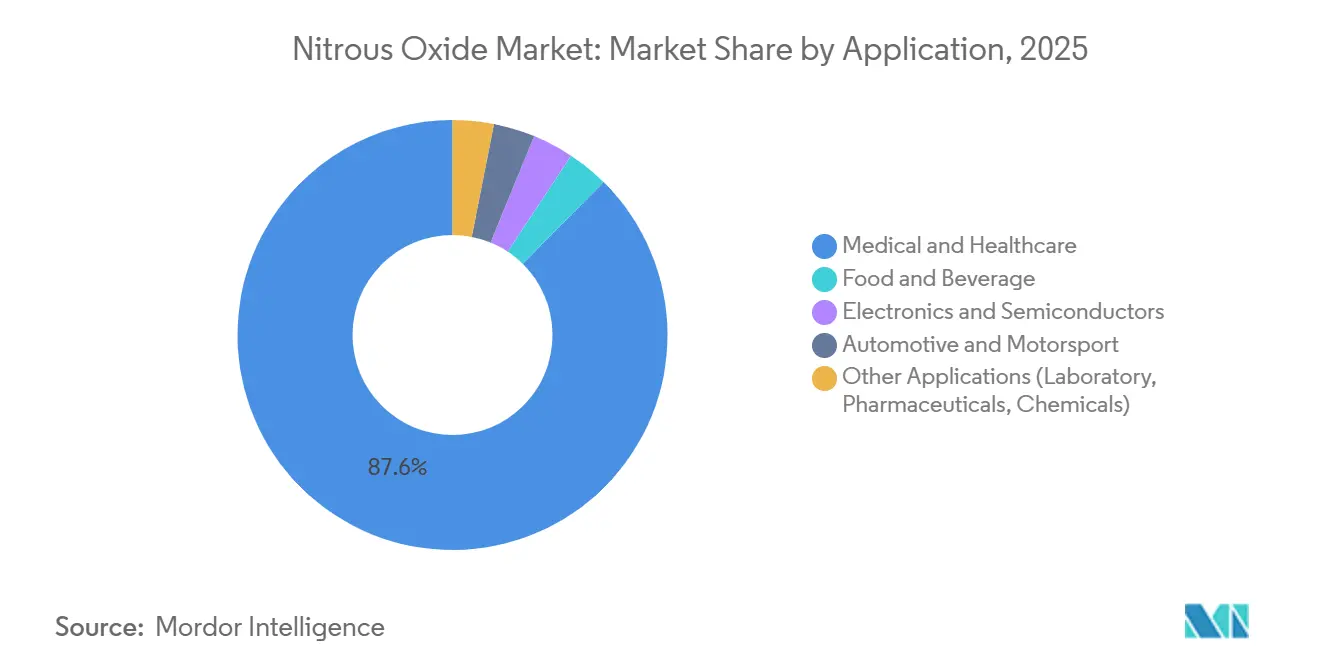

- By application, Electronics & Semiconductors registered the highest projected growth at 5.63% from 2026 to 2031; in 2025, Medical & Healthcare retained 87.60% of the Nitrous Oxide market size.

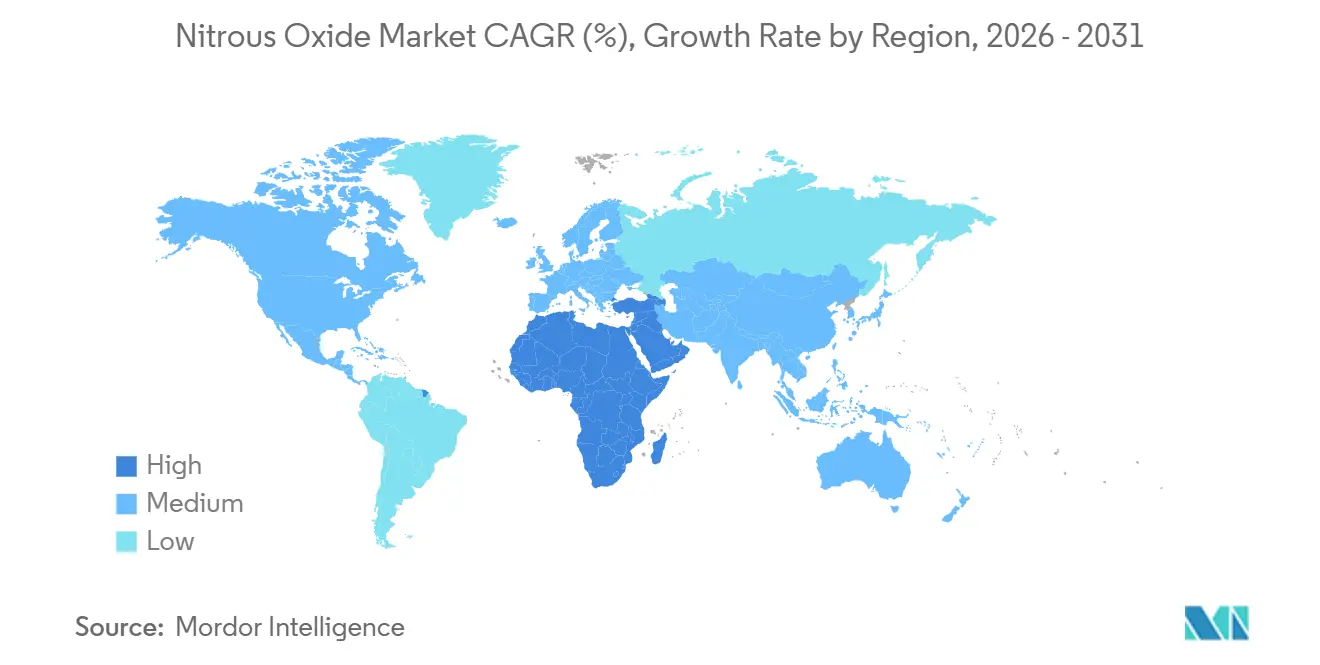

- By geography, Asia-Pacific held 35.17% of the 2025 volume, and the Middle East & Africa is advancing at a 5.56% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nitrous Oxide Market Trends and Insights

Driver Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use as an anesthetic in healthcare | +1.2% | Global, with early gains in Greece, India, China | Medium term (2-4 years) |

| Expansion of food and beverage propellant demand | +0.8% | North America & EU, APAC emerging | Short term (≤ 2 years) |

| Rising semiconductor and electronics etching volumes | +1.5% | APAC core (Taiwan, South Korea, China), spill-over to North America | Long term (≥ 4 years) |

| Shift toward high-purity N₂O in advanced nodes | +0.9% | Global semiconductor hubs (Taiwan, South Korea, Japan, Arizona) | Long term (≥ 4 years) |

| Emerging aerospace micro-thruster applications | +0.3% | Global, concentrated in US, Europe, Japan smallsat clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Use as an Anesthetic in Healthcare

In 2024, Greece lifted a long-standing ban on nitrous oxide sedation, introducing new national guidelines that broaden access in dental, obstetric, and minor-surgery settings. While Greece now mandates certified training for dentists and anesthetists, India and China, with over 300,000 active dentists each, predominantly lean on injectable analgesia. To assuage regulatory concerns, hospitals are now equipping central manifolds with infrared leak detection and ISO 22000-style batch-tracking, ensuring diverted cylinders do not fuel illicit markets. However, these same regions grapple with recreational misuse: from 2010 to 2023, U.S. deaths linked to nitrous oxide rose nearly six-fold, sparking demands for stricter point-of-sale controls that might momentarily hinder legitimate deliveries[1]Centers for Disease Control and Prevention, “Vital Statistics Rapid Release 2025,” cdc.gov. As a result, suppliers are caught in a bind, striving to meet the rising clinical demand while simultaneously investing in tamper-evident valves, smaller pack sizes, and ensuring end-user traceability.

Expansion of Food and Beverage Propellant Demand

Nitrous oxide, recognized as safe under 21 CFR 184.1545, has become the preferred propellant for whipped-cream cartridges and modified-atmosphere packaging. Trials using a mixture of 60% N₂O, 30% CO₂, and 10% N₂ have extended the shelf life of dairy products by up to 50%. This development allows food brands to eliminate the need for additives like carrageenan. However, in the UK and the Netherlands, where non-culinary possession was criminalized in 2023, single-use 8-gram steel chargers remain the primary means for recreational inhalation. In response, retailers have instituted age verification and purchase logging, a move that, while increasing compliance costs, reinforces the integrity of legitimate food-service supply chains. Meanwhile, China's GB 2760-2024 regulation restricts nitrous oxide's application solely to cream-whipping, banning its use as a preservative for canned foods. This mandate compels multinational brands to adjust their formulations based on regional markets.

Rising Semiconductor and Electronics Etching Volumes

At the 3-nm and 2-nm nodes, the gate-all-around (GAA) nanosheet FET architecture requires tighter side-wall selectivity and reduced defectivity. Chipmakers, aligning with sustainability commitments, are using plasma etch steps with nitrous oxide. This approach increases silicon-oxide growth rates and reduces the consumption of fluorinated gases. Fabs, facing heightened purity demands of sub-parts-per-billion for oxygen, moisture, and hydrocarbons, are now installing on-site cryogenic purification systems. They are also utilizing VIM-VAR 316L stainless tubing and real-time residual-gas analyzers. In 2025, Taiyo Nippon Sanso collaborated with imec’s Sustainable Semiconductor program, working on abatement systems. These systems aim to decompose residual N₂O before its release, addressing the gas’s 273 GWP factor.

Emerging Aerospace Micro-Thruster Applications

New-space operators are turning to nitrous oxide monopropellant thrusters. These thrusters self-pressurize at 50 bar, close to room temperature, which means operators can forgo separate helium tanks. Ground tests have achieved a vacuum-specific impulse of 148 seconds. When hybrid engines are combined with polyethylene grains, they can exceed 300 seconds. Currently, small-satellite constellations make up 70% of all orbital launches. Meanwhile, propulsion vendors are testing Nytrox oxidizer blends. These blends increase ignition energy, improving safety for rideshare missions. However, catalyst beds, which are plated with iridium on alumina, face a challenge. They must endure reaction temperatures of 1,600 °C, which restricts flight frequency until more affordable high-temperature alloys become available.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent greenhouse-gas emission regulations | -0.7% | Global, with EU and California leading | Medium term (2-4 years) |

| Health-safety issues from recreational abuse | -0.5% | UK, Netherlands, Australia, US states | Short term (≤ 2 years) |

| High purification cost for electronic-grade gas | -0.4% | Global semiconductor hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Greenhouse-Gas Emission Regulations

Under Regulation (EU) 2024/573, the European Union has set a default Global Warming Potential (GWP) of 273 for nitrous oxide mixtures[2]European Union, “Regulation (EU) 2024/573 on Fluorinated Greenhouse Gases,” eur-lex.europa.eu . This mandates equipment labeling, annual reporting, and accounting in CO₂-equivalents. Meanwhile, California is hinting at the potential inclusion of nitrous oxide in its cap-and-trade program post-2027. Such regulations increase compliance costs for gas suppliers and may drive downstream users to seek out substitutes with a lesser environmental impact or invest in abatement technologies. In a contrasting move, the U.S. Environmental Protection Agency, in February 2026, lifted restrictions on nitrous oxide for motor vehicles. This decision highlights a fragmented regulatory landscape, which not only skews trade flows but also adds layers of complexity to long-term investment strategies.

Health-Safety Issues from Recreational Abuse

Due to the inactivation of vitamin B12 and the resulting neurotoxicity, chronic inhalation of nitrous oxide has led to fatalities. This has prompted several jurisdictions to criminalize possession of the substance, except in medical, industrial, or culinary contexts. In 2023, the UK elevated nitrous oxide to a Class C controlled status, with personal possession now carrying a penalty of up to two years’ imprisonment. Although there was a temporary decline in incidents, 2024 saw a resurgence in poisoning reports in the Netherlands, highlighting the challenges of enforcement. Now, legitimate wholesalers face added costs and supply chain friction as they are mandated to install age-verification systems, limit cylinder sizes, and monitor serial numbers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Medical Dominance Masks Industrial Acceleration

In 2025, shipments of medical-grade nitrous oxide accounted for a dominant 69.85% share, primarily fueled by demand in anesthetics and obstetrics. However, this segment faces regulatory challenges, such as mandatory serialization, tamper-proof valves, and abuse-deterrent packaging, which not only inflate distribution costs but also temper its growth, keeping it below the overall CAGR of the nitrous oxide market. On the other hand, industrial-grade nitrous oxide, growing at a rate of 5.41%, finds its buoyancy in applications like semiconductor etching and emerging satellite thrusters. These applications sidestep the stringent pharmacopeia specifications that typically drive up medical pricing. Ultra-high-purity offerings, while occupying a niche, command a significant premium: the ability to minimize contaminants to sub-ppb levels translates to enhanced process yields. This dynamic was notably highlighted when a Taiwanese foundry inked a five-year take-or-pay contract for on-site generation in 2025. Thus, while medical-grade nitrous oxide continues to dominate in bulk volumes, it is the industrial and ultra-high-purity grades that are poised to reshape market size allocations in the coming five years.

Medical distributors are enhancing their offerings by bundling services like ISO 22000-style batch tracking and infrared manifold monitoring, effectively raising switching costs for hospitals. In contrast, industrial suppliers are channeling investments into cryogenic purification skids and VIM-VAR 316L pipeline networks, strategically positioned near leading-edge fabs. This strategic divergence mandates producers to establish segregated production lines to prevent cross-contamination. Major chipmakers, during plant audits, emphasize the need for dedicated vaporizers and particulate-free loading bays. Companies adept at safeguarding ultra-high-purity flows while simultaneously managing high-volume medical trades stand to seize the majority of the nitrous oxide market's incremental opportunities through 2031.

By Application: Electronics Surge Challenges Medical Hegemony

In 2025, medical and healthcare applications dominated the nitrous oxide market, accounting for 87.60% of the market. However, in mature economies, where anesthesia use is nearing saturation, volume growth has plateaued. While electronics and semiconductors are currently the fastest-growing segment, boasting a 5.63% CAGR. Advanced nodes below 5 nm are increasingly utilizing nitrous oxide in selective oxide-nitride etch steps. This move not only minimizes the use of fluorinated greenhouse gases but also aligns with corporate net-zero commitments. Furthermore, these fabs frequently secure multi-year supply agreements tied to electricity costs, providing margin stability that is not found in the spot-driven medical channels.

In the food and beverage sector, the GRAS classification of nitrous oxide allows for the elimination of synthetic stabilizers, ensuring a consistent micro-foam. This has led to modest growth, even amidst stricter abuse regulations. While automotive performance kits are a niche in regulated markets, they enjoy robust aftermarket demand in regions with lenient enforcement. Aerospace micro-thrusters, though low in volume, offer high margins. Their flight heritage is expanding, especially after the successful small-satellite demonstrations in 2025. Overall, as the nitrous oxide market shifts from a healthcare focus to more lucrative technology segments, we can expect a notable recalibration in market share distribution by the decade's close.

Geography Analysis

In 2025, Asia-Pacific accounted for 35.17% of the volume, driven by robust semiconductor ecosystems in Taiwan, South Korea, and Japan, alongside a growing dental infrastructure in China and India. Chip fabs in the region fuel the demand for ultra-high-purity gas pipelines. Meanwhile, as national health insurance schemes in India and Indonesia start covering nitrous oxide sedation, they unveil a previously untapped clinical demand. Unlike Europe, where regulatory crackdowns on recreational cartridges are stringent, Asia-Pacific sees a more lenient approach, allowing culinary volumes to grow. Yet, export restrictions on advanced process equipment could hinder China's shift to sub-5-nm nodes, moderating the surge in purity-driven demand.

North America benefits from entrenched hospital usage, with over 200,000 dentists in the U.S. routinely prescribing N₂O. The region also hosts the world's largest R&D cluster for small-satellite propulsion. While the February 2026 repeal of vehicle nitrous-oxide tailpipe limits stifled a budding abatement market, it had little impact on upstream consumption. Looking ahead, Canada’s Environment & Climate Change review of industrial process-gas emissions, anticipated in 2027, might roll out reporting mandates similar to those in the EU.

Europe faces the most stringent compliance measures. Regulation (EU) 2024/573 imposes labelling and CO₂-equivalent duties, while the UK’s Class C reclassification makes personal possession without a valid purpose a criminal offense. Though these regulations heighten documentation demands, they also eliminate grey-market wholesalers, channeling volumes to licensed distributors. Meanwhile, Eastern Europe and Turkey are witnessing gradual growth as their healthcare systems enhance maternity services.

Middle East & Africa, starting from a modest base, project the highest forecast growth at a 5.56% CAGR. States within the Gulf Cooperation Council are channeling investments into new air-separation capacities for ammonia and steel, inadvertently producing co-product N₂O streams. In Africa, while private-hospital chains are beginning to use nitrous oxide for short-stay surgeries, challenges like a limited fleet of cryogenic tankers and fragmented regulatory oversight are hindering swift expansion. South America mirrors this pattern: while Brazil sees a rise in clinical nitrous oxide use, a lack of semiconductor demand limits the potential for high-purity applications.

Competitive Landscape

In 2025, five major players, Air Liquide, Linde, Air Products, Messer, and Taiyo Nippon Sanso, held a majority share of the nitrous oxide market, indicating the market is moderately consolidated. These companies utilize vast networks for air separation, pipelines, and cylinder distribution. However, most of their new projects are focusing on outputs of oxygen or nitrogen, rather than on dedicated nitrous oxide (N₂O) purification. For instance, Linde's USD 400 million air separation unit (ASU) in Louisiana, set to be operational by 2029, and Messer's USD 65 million unit in Texas, due in 2027, exemplify this trend. As a result, the capacity for high-purity nitrous oxide is constrained, creating opportunities for specialty gas companies. These newcomers are often ready to invest in on-site generators at semiconductor fabrication plants.

These companies are adopting a strategy that emphasizes long-term, take-or-pay agreements with bulk clients. They also offer enhanced services, such as real-time gas monitoring, purity assurances, and leak-detection analytics, especially for their semiconductor fabrication customers. In a notable move, Baker Hughes acquired Chart Industries for USD 13.6 billion in 2025. This acquisition brings cryogenic storage and heat-exchange capabilities into Baker Hughes' energy-technology suite, enabling them to offer comprehensive nitrous oxide solutions from production to storage. Meanwhile, Air Products is branching out into membrane-based nitrogen skids tailored for aerospace and marine fuels, hinting at potential future applications in N₂O purification.

Some niche players are making waves by focusing on small-satellite propulsion. They provide complete services, from filling nitrous oxide to supplying 3D-printed thruster blocks. However, their volume remains modest when compared to traditional medical cylinder usage. Challenges for new entrants include establishing a cylinder retest infrastructure, adhering to ISO 11120 standards for larger tubes, and managing the increasing capital expenditure for ultra-pure (sub-ppb) purification. The industry landscape shows moderate competition, with a clear emphasis on differentiators like purity, logistical reliability, and compliance services, rather than just pricing.

Nitrous Oxide Industry Leaders

Air Liquide

Air Products and Chemicals Inc.

Linde plc

Messer SE and Co. KGaA

Taiyo Nippon Sanso Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Messer approved a USD 65.4 million liquid air-separation facility in Bryan, Texas, slated for summer 2027 service, expanding nitrogen, oxygen, and hydrogen supply to healthcare and manufacturing customers.

- March 2026: Linde began construction of a new ASU in Oshkosh, Wisconsin, targeting H2 2028 start-up to supply liquid oxygen, nitrogen, and argon across the upper Midwest.

Global Nitrous Oxide Market Report Scope

Nitrous oxide, commonly known as "laughing gas," is a colorless, non-flammable gas with a slightly sweet scent and taste. It is widely used as a sedative and pain reliever in medical and dental procedures, often mixed with oxygen. Additionally, it is used as a propellant in high-performance engines and has recognized psychoactive, dissociative effects.

The market is segmented by grade and application. By grade, the market is segmented into medical grade, food grade, industrial grade, and ultra-high-purity grade. By application, the market is segmented into medical and healthcare, food and beverage, electronics and semiconductors, automotive and motorsport, and other applications (including laboratory, pharmaceuticals, and chemicals). The report also covers the market size and forecasts for Nitrous Oxide in 17 countries across the world. For each segemnt market sizing and forecasts are provided in terms of volume (tons).

| Medical Grade |

| Food Grade |

| Industrial Grade |

| Ultra-High-Purity Grade |

| Medical and Healthcare |

| Food and Beverage |

| Electronics and Semiconductors |

| Automotive and Motorsport |

| Other Applications (Laboratory, Pharmaceuticals, Chemicals) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Grade | Medical Grade | |

| Food Grade | ||

| Industrial Grade | ||

| Ultra-High-Purity Grade | ||

| By Application | Medical and Healthcare | |

| Food and Beverage | ||

| Electronics and Semiconductors | ||

| Automotive and Motorsport | ||

| Other Applications (Laboratory, Pharmaceuticals, Chemicals) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global demand for nitrous oxide by 2031?

Volumes are expected to reach 7.01 million tons, reflecting a 4.74% CAGR from 2026.

Which end-use will add the most incremental demand for nitrous oxide during the forecast period?

Electronics and semiconductor fabs, driven by ultra-high-purity etching needs at 3-nm and 2-nm nodes, post the fastest 5.63% CAGR through 2031.

Why is Asia-Pacific the largest regional consumer of nitrous oxide?

The region combines the world’s densest advanced-node chip capacity with rapidly expanding medical and dental infrastructure, giving it 35.17% of 2025 global volume.

What makes ultra-high-purity nitrous oxide more expensive than medical or industrial grades?

Sub-ppb impurity targets demand multi-stage cryogenic purification, electropolished 316L stainless systems, and real-time gas monitoring, all of which raise capital and operating costs.

Page last updated on: