Niobium Pentoxide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

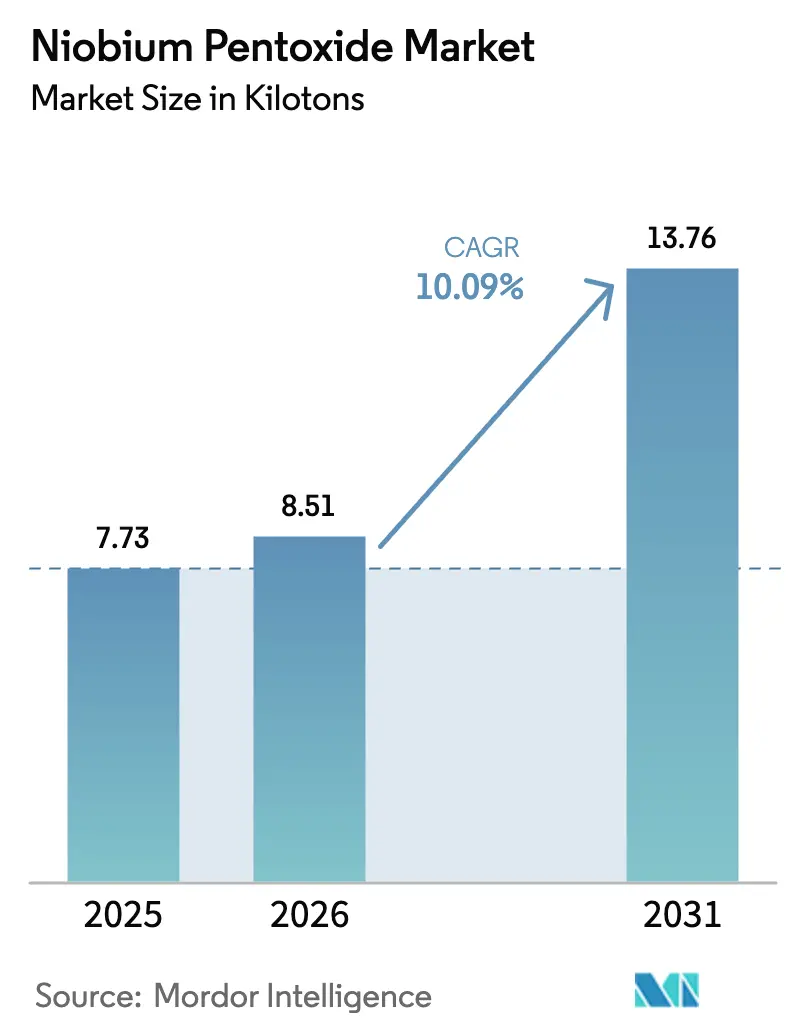

| Market Volume (2026) | 8.51 kilotons |

| Market Volume (2031) | 13.76 kilotons |

| Growth Rate (2026 - 2031) | 10.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Niobium Pentoxide Market Analysis by Mordor Intelligence

The Niobium Pentoxide Market size is projected to expand from 7.73 kilotons in 2025 and 8.51 kilotons in 2026 to 13.76 kilotons by 2031, registering a CAGR of 10.09% between 2026 to 2031. Robust infrastructure spending in Asia, a steady aerospace-fleet renewal cycle in North America, and rapid adoption of ultra-fast-charging battery chemistries are sustaining double-digit demand growth. Bulk consumption in high-strength steels continues to anchor volumes, yet rapidly scaling niche uses in optical glass, additive-manufacturing powders, and 5G radio-frequency sputtering targets are improving the overall value mix. Supply-chain diversification initiatives outside Brazil have gathered pace since 2024, but CBMM’s dominant ore reserve still underpins price discovery. Forward-looking procurement teams are therefore tying up long-term offtake contracts and investing in closed-loop recycling to hedge volatility.

Key Report Takeaways

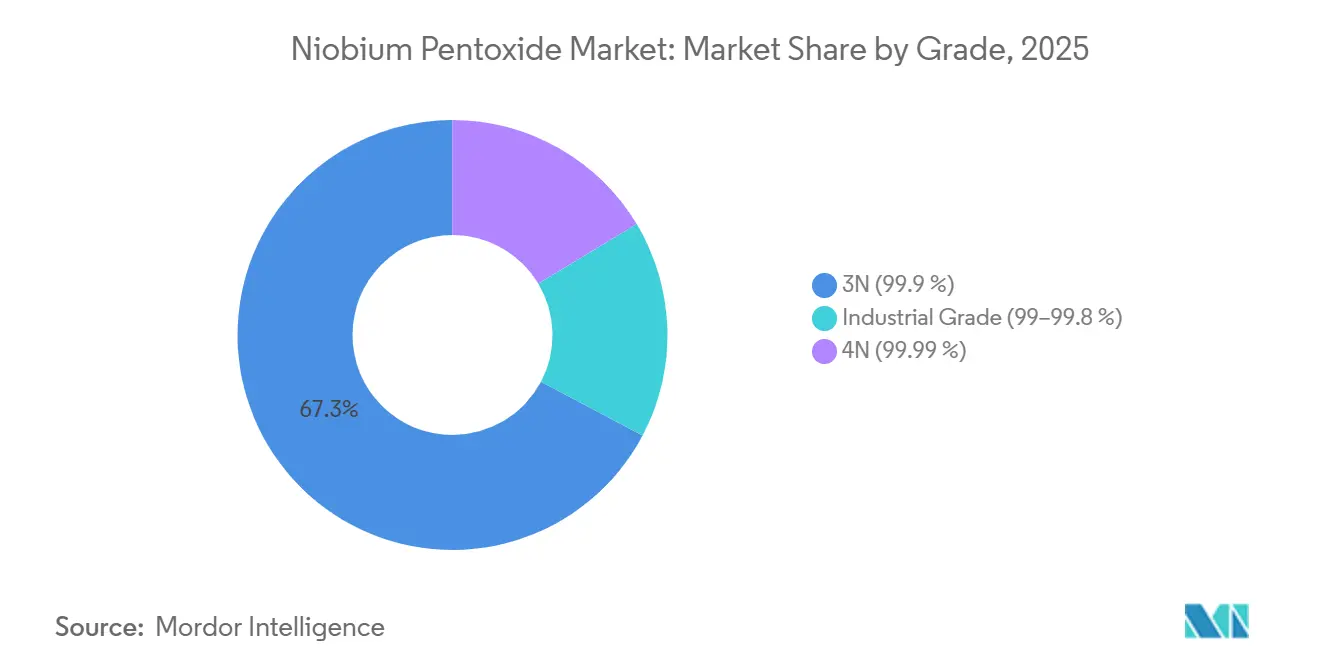

- By grade, the 3N purity segment captured 67.26% niobium pentoxide market share in 2025 and is advancing at a 10.77% CAGR through 2031.

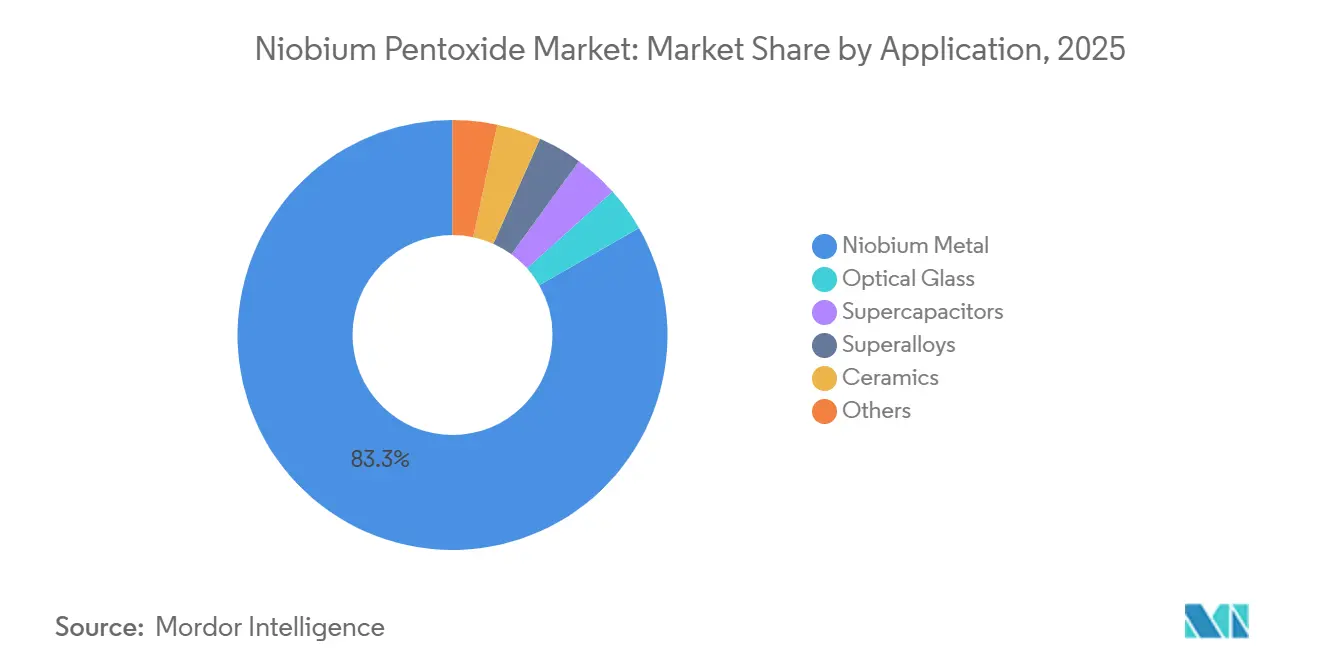

- By application, niobium metal production accounted for 83.30% of the niobium pentoxide market size in 2025 and is growing at a 10.41% CAGR to 2031.

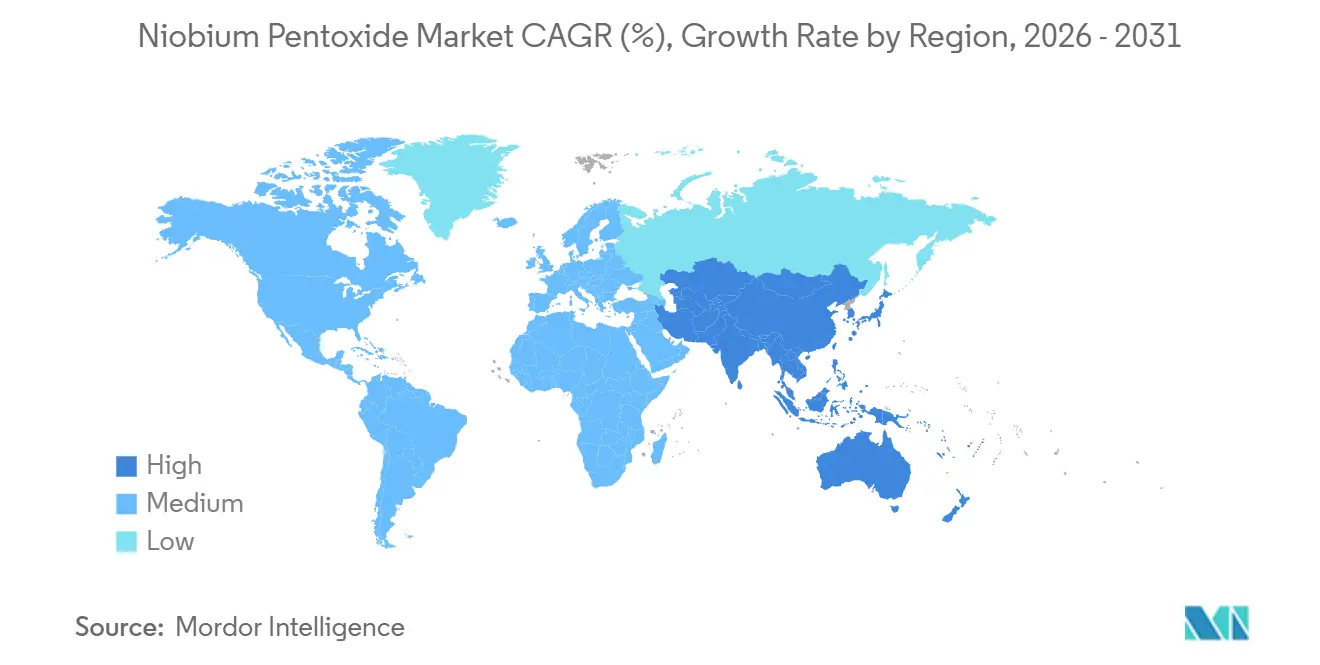

- By geography, Asia-Pacific led with 46.72% of global volume in 2025; the region is projected to expand at a 12.59% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Niobium Pentoxide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-refractive-index optical glass | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Rising adoption in high-strength steels and superalloys | +3.8% | Global | Long term (≥ 4 years) |

| Expansion of Nb₂O₅-based fast-charging batteries and supercapacitors | +2.5% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Emerging use in 5G / AR sputtering targets | +1.1% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Lead-free high-k dielectric ceramics replacing PbO | +1.3% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Refractive-Index Optical Glass

Japanese glassmakers ramped Nb₂O₅-doped blank output in 2024 to satisfy smartphone and augmented-reality lens programs, achieving refractive indices above 1.9 without lead additions. Aspherical camera elements now contain up to 20 weight percent niobium pentoxide, enabling thinner modules in premium handsets and lighter optics in head-mounted displays. Automakers are also specifying niobium-doped silica in solid-state lidar waveguides to reduce scattering losses. Optical uses consume less than 2% of global volume, yet their margin premium supports incremental capacity for 4N refining. Producers, therefore, balance allocations between high-value glass and bulk steel channels to maximize asset utilization.

Rising Adoption in High-Strength Steels and Superalloys

Pipeline builders rely on 0.02–0.05% niobium additions to hit API 5L X80 grade without post-weld heat treatment, a benefit that speeds Arctic and deepwater projects[1]American Petroleum Institute, “API 5L: 2024 Edition,” api.org. China laid nearly 8,000 kilometers of transmission pipe annually between 2024 and 2025, keeping ferroniobium demand resilient even as rebar growth slowed. In aviation, niobium-bearing superalloys such as Inconel 718 deliver creep resistance above 650 °C, a prerequisite for geared turbofan disks certified in 2024. The dual pull from infrastructure and aerospace secures a long-run foundation for bulk oxide consumption.

Expansion of Nb₂O₅-Based Fast-Charging Batteries and Supercapacitors

Nb₂O₅ anodes charge to 80% in six minutes because their pseudocapacitive lithium insertion sidesteps dendrite growth. Chinese cell makers are piloting composite anodes that support 4C rates, positioning electric-bus fleets for turn-around charging in depot schedules. Toshiba’s earlier titanate chemistry proved 20,000 cycles; niobium pentoxide now delivers 30% higher energy density at similar lifetimes. Although Nb₂O₅ costs eight to ten times more than synthetic graphite, system-level economics improve when chargers and fleets are co-optimized, potentially lifting battery demand to 7% of global oxide volume by 2030.

Emerging Use in 5G / AR Sputtering Targets

Radio-frequency filters rely on niobium pentoxide’s high-k dielectric to shrink footprint without adding insertion loss[2]IEEE Microwave Symposium Proceedings, “High-k Dielectric Layers,” ieee.org. Materion and Kurt J. Lesker expanded the 4N target capacity in 2024 to feed Samsung’s front-end modules. Augmented-reality waveguides exploit Nb₂O₅’s refractive index of 2.3 at 550 nm, allowing thinner diffractive stacks in consumer headsets. Sputtering targets account for less than 1% of tonnage yet command a threefold price premium, motivating refiners to carve out dedicated ultra-pure streams.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and safety concerns from Nb₂O₅ dust exposure | -0.8% | North America, Europe | Short term (≤ 2 years) |

| Supply-chain concentration in Brazil | -1.5% | Global | Long term (≥ 4 years) |

| High energy and carbon footprint of ultra-pure refining | -1.2% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health and Safety Concerns from Nb₂O₅ Dust Exposure

OSHA caps respirable niobium-compound dust at 5 mg/m³, pushing refiners to install enclosed handling and real-time monitors. Europe’s REACH regime demands downstream exposure assessments for volumes over one tonne, adding compliance engineering costs of 8–12% on new lines. Smaller North American converters have merged to amortize these expenses, leaving seven suppliers in 2025 versus eleven in 2020. Automation and inert-gas transfers relieve litigation risk, yet margin erosion of one to two points persists, tempering near-term investment appetites.

Supply-Chain Concentration in Brazil

CBMM’s Araxá mine holds 842 million tonnes grading 2.5% Nb₂O₅, equal to about 85% of economically recoverable ore. A single labor strike or permit freeze could scramble global supply within weeks, as seen after the Brumadinho tailings failure in 2024 that triggered a six-month state-wide mining review. Defense agencies now treat niobium as critical; the U.S. Department of Defense awarded USD 26.4 million in 2024 to reboot domestic oxide output in Pennsylvania. Yet new mines typically need a decade to reach steady state, so buyers continue to carry six to nine months of safety stock, constraining spot liquidity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Ultra-Pure 3N Dominates Metallurgical Feedstock

The 3N grade captured 67.26% of global volume in 2025, underscoring its status as preferred feedstock for ferroniobium and master-alloy chains. This segment is forecast to post a 10.77% CAGR to 2031, keeping pace with overall niobium pentoxide market expansion. Industrial-grade oxide trails because pigment and glass uses tolerate wider impurity windows, allowing partial substitution by lower-cost zirconium or cerium compounds. Meanwhile, the 4N segment serves semiconductor sputtering targets and single-crystal growth, and is expanding quickly as radio-frequency filter demand rises. JX Advanced Metals lifted 4N capacity by 40% in 2024 to supply Korean fabs, a sign that ultra-pure streams can justify premium pricing when underpinned by multiyear volume commitments.

Long-standing quarterly ferroniobium benchmarks shield metallurgical-grade buyers from spot volatility, fostering predictable cash flow across the niobium pentoxide market. By contrast, 4N refiners must ride semiconductor capital-expenditure cycles that swing as much as 30% year over year. ISO 11135:2024 now defines an intermediate “medical-device” grade that caps tantalum and titanium below 500 ppm, effectively splitting the spectrum between bulk 3N and ultra-pure 4N. Converters that certify to both ISO 9001 and the new medical standard are poised to capture emerging sterilization and imaging niches.

By Application: Niobium Metal Production Anchors Demand

Niobium metal absorbed 83.30% of niobium pentoxide volume in 2025 because microalloyed steels dominate global construction and energy pipelines. The segment is projected to grow at 10.41% through 2031, mirroring forecast pipeline mileage and turbine build rates. Optical glass demand is driven by camera-module shipments and early lidar adoption. Supercapacitors and superalloys each expand faster than headline growth due to electric-vehicle duty cycles and hotter gas-turbine firing temperatures. Ceramics could scale quickly once KNN capacitors replace PZT in automotive control units mandated after the 2027 RoHS deadlines.

By 2030, higher-value electronics and battery segments may trim niobium metal’s dominance to 78–80% as additive-manufacturing powders and battery-grade oxide gain traction. TANIOBIS patented a spray-pyrolysis route in 2024 that lowers process energy by 30%, a potential tipping point for cost-competitive battery precursors. Closed-loop superalloy recycling remains underdeveloped, with less than 10% of niobium recovered from retired turbine disks, yet hydrometallurgical advances could unlock a secondary feedstock that dovetails with circular-economy targets.

Geography Analysis

Asia-Pacific accounted for 46.72% of the niobium pentoxide market volume in 2025 and is projected to grow at 12.59% through 2031, the fastest regional growth. China’s 54% share of global crude-steel output anchors ferroniobium pull, while Japan and South Korea command ultra-pure niches tied to semiconductor and optics value chains. India’s highway build-out and oil-and-gas pipeline expansions are boosting demand for niobium-microalloyed steels, supported by policy targets that aim for 25,000 kilometers of new highways by 2026. Vietnam and Indonesia are emerging as secondary hubs as they commission integrated mills specifying ferroniobium for high-rise construction.

North American and European consumption of niobium pentoxide is affected by mature steel demand. The United States restarted domestic oxide production in 2025 at Boyertown under a USD 26.4 million Title III award, insulating aerospace and defense flows from single-source risk. Europe tilts toward 4N purity for semiconductor equipment, yet carbon-pricing under the EU ETS inflates refining costs, prompting some converters to relocate ultra-pure steps to Asia. The EU Critical Raw Materials Act of 2024 streamlines permits for niobium projects, but price parity with Asian supply remains elusive.

South America, the Middle East, and Africa together are witnessing rising demand for niobium pentoxide. Globe Metals’ Kanyika project in Malawi, finalized in 2024, targets first production by 2027 at 3,267 tpa, which could supply 4% of global demand and diversify the upstream base. Middle-East uptake centers on niobium-stabilized stainless steels for sour-gas pipelines, an example being Saudi Aramco’s Jafurah field that broke ground in 2024. These niche regional drivers provide a modest but strategically important buffer against any Brazilian disruption.

Competitive Landscape

The niobium pentoxide market is characterized by a high level of consolidation, with major players leveraging vertical integration and technological advancements to maintain a competitive advantage. These companies are heavily investing in research and development to enhance production efficiency and explore innovative applications, particularly in emerging areas such as electric vehicles and energy storage. To ensure operational efficiency, businesses are expanding production capacities and forming strategic partnerships across the value chain, securing raw material supplies and optimizing distribution networks. Collaboration between manufacturers and end-users is increasing, focusing on the development of customized, high-performance solutions. Additionally, market leaders are integrating sustainability initiatives and adopting green manufacturing practices while strengthening their global presence through regional production facilities and strategic distribution alliances.

Niobium Pentoxide Industry Leaders

CBMM

CMOC

JX Advanced Metals Corporation

AMG

XIMEI Resources Holding Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: AMG Advanced Metallurgical Group disclosed site scouting in Pennsylvania and Ohio for U.S. niobium metal production aligned with aerospace and energy demand.

- November 2024: JX Advanced Metals raised 4N oxide capacity 40% at Kurami, serving Samsung’s radio-frequency filter lines.

- June 2024: Materion launched sputtering targets certified to SEMI MF1188 for sub-5 nm semiconductor nodes.

Global Niobium Pentoxide Market Report Scope

Niobium pentoxide, or niobium(V) oxide, is a chemical compound represented by the formula Nb₂O₅. This white, odorless crystalline powder is insoluble in water. Due to its unique properties, niobium pentoxide finds applications across diverse industries, including electronics, optics, aerospace, and biomedicine.

The niobium pentoxide market is segmented by grade, application, and geography. By grade, the market is categorized into industrial grade, 3N, and 4N. By application, the market is segmented into niobium metal, optical glass, supercapacitors, superalloys, ceramics, and others. The report also covers the market sizes and forecasts for the global niobium pentoxide market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Industrial Grade (99–99.8 %) |

| 3N (99.9 %) |

| 4N (99.99 %) |

| Niobium Metal |

| Optical Glass |

| Supercapacitors |

| Superalloys |

| Ceramics |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Industrial Grade (99–99.8 %) | |

| 3N (99.9 %) | ||

| 4N (99.99 %) | ||

| By Application | Niobium Metal | |

| Optical Glass | ||

| Supercapacitors | ||

| Superalloys | ||

| Ceramics | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the niobium pentoxide market size in 2026 and what CAGR is expected through 2031?

The niobium pentoxide market is estimated at 8.51 kilotons in 2026 and is projected to rise to 13.76 kilotons by 2031, reflecting a 10.09% CAGR.

Which purity grade currently dominates demand for niobium pentoxide?

The 3N grade holds 67.26% of 2025 volume and is forecast to grow at a 10.77% CAGR through 2031.

What share of niobium pentoxide consumption goes into niobium metal production?

Niobium metal production—including ferroniobium and master alloys—absorbed 83.30% of total oxide volume in 2025.

Which region leads in niobium pentoxide demand and how fast is it growing?

Asia-Pacific commanded 46.72% of 2025 volume and is expanding at a 12.59% CAGR to 2031.

Why is supply-chain concentration considered a major risk factor?

About 85% of global economically recoverable ore reserves sit in Brazil’s Araxá mine, so any disruption there could squeeze worldwide availability and spike prices.

What emerging application is poised to lift high-purity niobium pentoxide demand?

Fast-charging battery anodes that reach 80% state of charge in six minutes are expected to push battery-grade oxide toward 7% of total demand by 2030.

Page last updated on: