Ethylene Oxide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

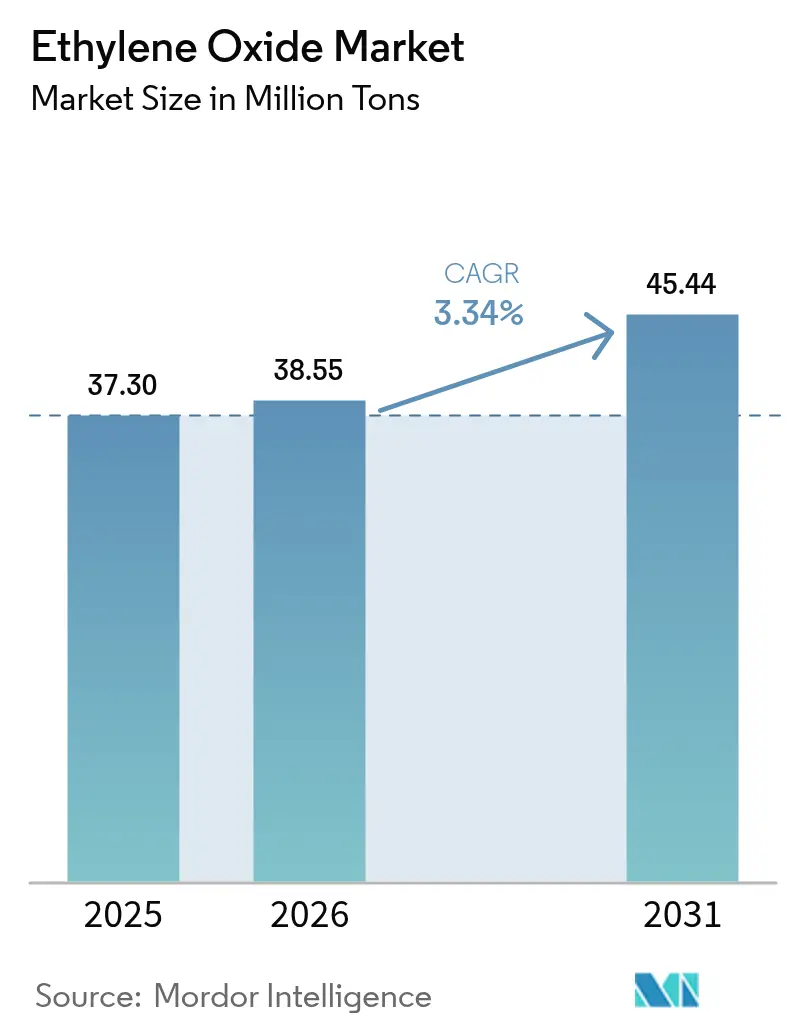

| Market Volume (2026) | 38.55 Million tons |

| Market Volume (2031) | 45.44 Million tons |

| Growth Rate (2026 - 2031) | 3.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethylene Oxide Market Analysis by Mordor Intelligence

The Ethylene Oxide market size is expected to grow from 37.30 Million tons in 2025 to 38.55 Million tons in 2026 and is forecast to reach 45.44 Million tons by 2031 at 3.34% CAGR over 2026-2031. Demand stems from its versatility as a chemical intermediate, with polyester fibers, PET resins, surfactants, ethanolamines, and sterilants underpinning consumption growth. Expansion of polyester-based textiles, wider adoption of PET for lightweight food and beverage packaging, and regulatory-driven investments in medical device sterilization facilities remain the core drivers. Rapid uptake of bio-ethylene feedstock, rising investment in emission-control technology, and the spread of circular-economy initiatives are reshaping sourcing strategies and opening new revenue pools. Competitive dynamics favor vertically integrated producers that can balance feedstock volatility, comply with tightening emission limits, and develop specialty derivatives.

Key Report Takeaways

- By derivative type, ethylene glycols held 75.02% of the ethylene oxide market share in 2025; ethanolamines record the fastest forecast growth at a 3.55% CAGR through 2031.

- By application, Polyester Fiber and PET Resins led with 27.86% revenue share in 2025, while sterilization and fumigation are poised for the highest 3.67% CAGR to 2031.

- By end-user industry, the textile sector commanded 29.74% of the 2025 total, whereas the “other industries” category shows the quickest 3.91% CAGR outlook.

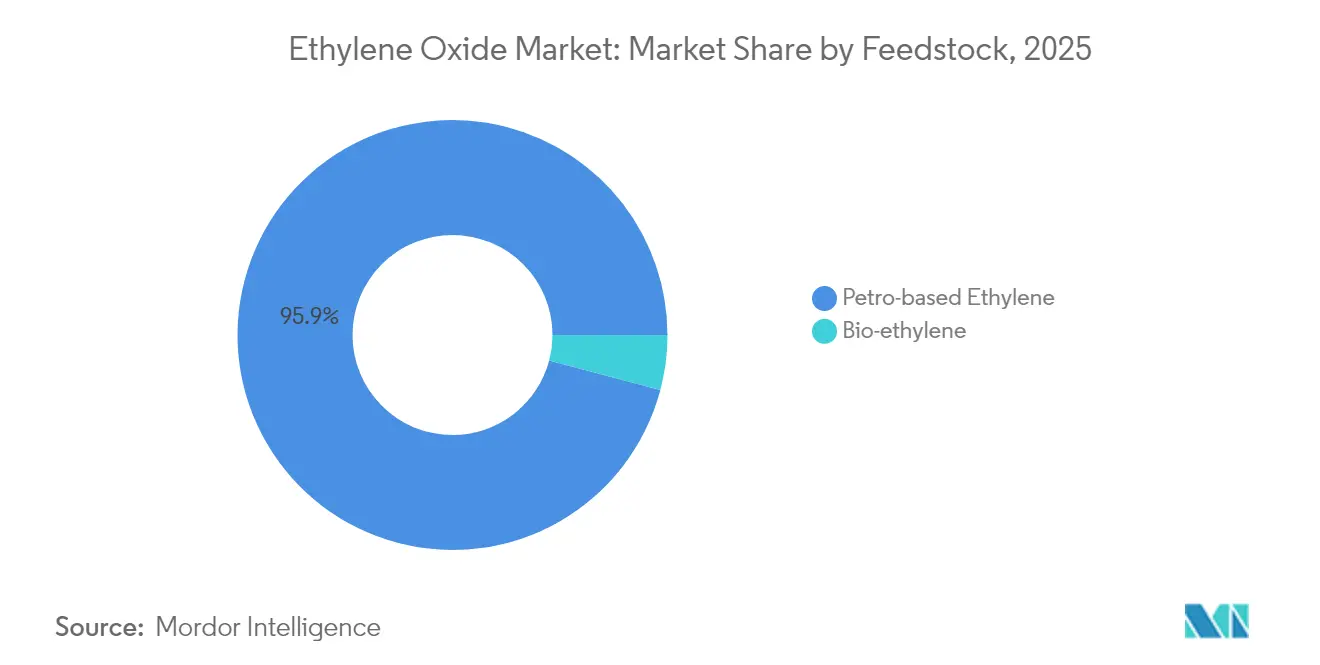

- By feedstock, petro-based ethylene represented 95.88% of volumes in 2025, but bio-ethylene exhibits the fastest 4.72% CAGR to 2031.

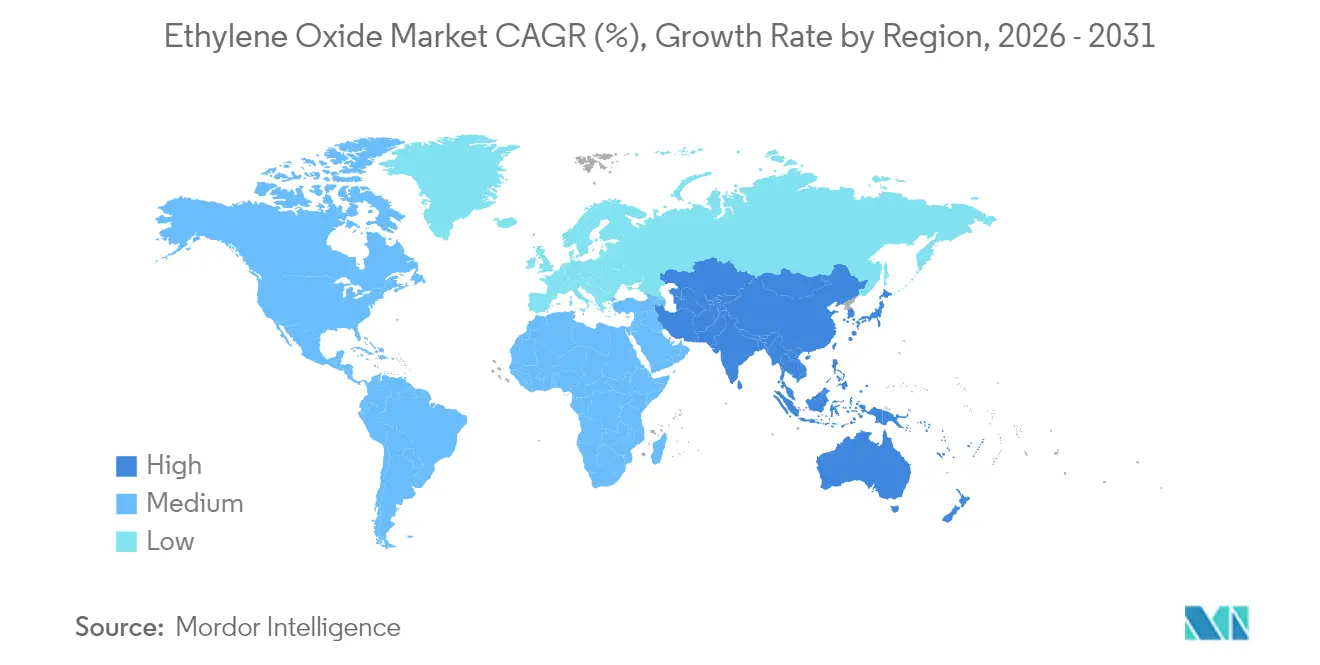

- By geography, Asia-Pacific contributed 50.72% of 2025 demand and is set to grow at 3.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ethylene Oxide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Usage of PET in the Food and Beverage Industry | +0.80% | Global, highest in Asia-Pacific | Medium term (2-4 years) |

| Increasing Demand for Household and Personal Care Products | +0.50% | North America and Europe | Medium term (2-4 years) |

| Increasing Utilziation in Medical Device Sterilization | +0.70% | North America, global supply chains | Short term (≤ 2 years) |

| Growing Demand from Textile and Apparel Industry | +0.90% | Asia-Pacific | Medium term (2-4 years) |

| Increasing Utilization from the Agriculture Sector | +0.40% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Usage of PET in the Food and Beverage Industry

PET packaging adoption is accelerating because brand owners favor lightweight, recyclable solutions that preserve product integrity. Monoethylene glycol derived from ethylene oxide constitutes nearly 90% of the ethylene glycol pool used for PET polymerization, causing direct pull-through on upstream demand. Large resin producers are backing chemical-recycling platforms that depolymerize post-consumer PET into monomers with yields above 90%, enabling circular supply chains while keeping ethylene oxide volumes steady. Companies such as Dow have earmarked multi-million-metric-ton programs to deliver circular and renewable plastics annually by 2030. These initiatives strengthen long-term demand visibility even as the product mix shifts toward recycled grades.

Increasing Demand for Household and Personal Care Products

Surfactants and detergents formulated with ethoxylates and ethanolamines deliver superior cleaning efficiency, especially in hard-water regions. Consumer preference for eco-friendly ingredients is prompting producers such as Nouryon to certify green ethylene oxide derivatives under the ISCC PLUS scheme[1]Nouryon, “Nouryon obtains ISCC PLUS certification for green ethylene oxide,” nouryon.com . Switching from alkylphenol to fatty-alcohol ethoxylates aligns with forthcoming biodegradability regulations while sustaining performance. Capacity additions in Europe and North America are timed to capture this demand uptick as private-label cleaning brands gain retail shelf space.

Increasing Utilization in Medical Device Sterilization

Roughly 50% of the 20 billion sterile medical devices sold annually in the United States depend on ethylene oxide because it penetrates complex geometries without degrading polymers. The EPA’s 2024 emission rule requires a 99.9% removal efficiency from facilities using 10-30 tons per year, spurring investments in advanced catalytic scrubbers and continuous monitoring systems. Transitional FDA guidance issued in late 2024 provides compliance flexibility, thereby preventing supply disruptions while innovations scale. Market participants with proprietary abatement technologies gain a competitive edge under these tighter rules.

Growing Demand from Textile and Apparel Industry

Polyester fibers dominate global apparel due to durability and cost advantages, with Asia-Pacific mills accounting for the majority of new capacity. Chemical recycling processes such as microwave-assisted glycolysis can return polyester and spandex textiles to monomers within 15 minutes and achieve an 88% circularity rate. Although circular flows may displace a fraction of virgin monoethylene glycol, regional fiber demand still outpaces recycling supply, maintaining positive volume growth for the ethylene oxide market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and Environmental Effects over High Exposure | -0.70% | North America and Europe | Short term (≤ 2 years) |

| Volatility of Ethylene Feedstock Prices | -0.50% | Europe highest, global effect | Short term (≤ 2 years) |

| High Production Cost | -0.30% | High energy-price regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health and Environmental Effects over High Exposure

Ethylene oxide is classified as carcinogenic, prompting the EPA’s January 2025 interim decision that cuts worker exposure limits from 0.5 ppm by 2028 down to 0.1 ppm by 2035. Compliance demands costly engineering controls, personal monitoring, and capital upgrades. Some healthcare device makers are accelerating the qualification of alternative sterilization methods, including gamma radiation, vaporized hydrogen peroxide, and nitrogen dioxide. While these substitutes will erode specific volumes, ethylene oxide remains indispensable for heat-sensitive devices with intricate lumens.

Volatility of Ethylene Feedstock Prices

Global ethylene spot prices fluctuate with crude oil swings, logistics bottlenecks, and regional feedstock spreads. In July 2024, US ethylene prices spiked amid scheduled cracker turnarounds, expanding the advantage of low-cost shale-based producers over naphtha-dependent European peers. Freight rates climbed due to security issues in Middle-East shipping lanes and Panama Canal water shortages, heightening delivered-cost dispersion. Producers with integrated steam crackers and geographic diversification can better absorb this volatility than merchant ethylene oxide buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derivative: Glycols Dominate While Ethanolamines Accelerate

Ethylene glycols formed the bedrock of the ethylene oxide market in 2025, capturing 75.02% share as polyester fiber and PET resin output scaled in Asia-Pacific. Price volatility has returned following upstream supply disruptions, pushing Asia-based buyers to secure long-term contracts with integrated producers. In parallel, bio-MEG pilots are gaining traction as brand owners seek lower-carbon packaging options.

Ethanolamines contribute a smaller volume but post the highest 3.55% CAGR to 2031, driven by agrochemicals, gas treatment, and personal-care demand. BASF’s Antwerp debottlenecking raised global alkyl ethanolamine capacity by nearly 30% to more than 140,000 t per year, underscoring the segment’s strategic value. Rising glyphosate herbicide volumes in Latin America and Asia sustain monoethanolamine pull-through, while triethanolamine sees new opportunities in CO₂ capture solvents. Strong downstream diversification shields this derivative class from single-industry cyclicality.

By Application: PET Resins Lead Amid Sterilization Growth

PET resins and polyester fibers absorbed 27.86% of ethylene oxide demand in 2025. The ethylene oxide market size linked to PET is expected to grow steadily as beverage companies transition from glass and metal to lightweight PET bottles. Innovative depolymerization pathways such as dimethyl-carbonate-aided methanolysis enable greater than 90% dimethyl terephthalate yields, opening high-purity recycled PET streams. Over the forecast horizon, virgin demand moderates in developed regions yet expands in fast-growing economies where recycling infrastructure remains nascent.

Sterilization and fumigation ranked as the fastest-growing application at 3.67% CAGR. Approximately 50,000 distinct medical devices rely on ethylene oxide sterilization, preserving thermolabile polymers that cannot withstand gamma or electron-beam radiation. Even with stringent emissions limits, demand persists because alternative modalities often fail to penetrate complex packaging or achieve required sterility assurance levels. Investment in catalytic oxidation units and continuous emissions monitoring allows compliant operations, sustaining growth in this niche.

By End-user Industry: Textile Sector Maintains Leadership

The textile industry consumed 29.74% of 2025 volumes as polyester remained the dominant fiber category. The ethylene oxide market share for textiles reflects strong Asian production bases where blended fabrics and fast fashion drive continuous polymer demand. Advanced chemical-recycling lines are being integrated into large Chinese mills, enabling recovery of monoethylene glycol and terephthalic acid at scale. This circular approach moderates virgin demand growth in the long term but enhances supply security in closed-loop ecosystems.

“Other industries” represent the fastest growth at 3.91% CAGR, reflecting the broad utility of ethylene oxide derivatives in lubricants, coolants, construction chemicals, and specialty pharmaceuticals. The pharmaceutical sector benefits doubly from ethylene oxide’s function as both a sterilant and a precursor for excipients such as polyethylene glycol. Personal-care manufacturers are reformulating toward certified sustainable derivatives, accentuating demand resilience.

By Feedstock: Bio-ethylene Emerges as a Growth Driver

Petro-based ethylene held 95.88% of feedstock share in 2025, leveraging efficient steam crackers tied to low-cost natural-gas liquids in North America and the Middle East. Despite dominance, the segment faces carbon-pricing and energy-cost headwinds in Europe, triggering rationalization of older naphtha units. Diversified producers hedge exposure by co-processing renewable feedstocks or using mass-balance certification systems.

Bio-ethylene grows at 4.72% CAGR through 2031, driven by Brazilian sugarcane ethanol routes that can generate negative cradle-to-gate carbon footprints when biogenic carbon storage is credited. Academic breakthroughs demonstrate two-step dehydration-epoxidation cycles delivering 57% ethylene oxide selectivity at 15% conversion under chemical-looping conditions, hinting at future on-demand small-scale production. Commercial viability hinges on feedstock availability and downstream certification incentives.

Geography Analysis

Asia-Pacific remained the largest ethylene oxide market in 2025, supplying 50.72% of global demand and expanding at a region-leading 3.68% CAGR to 2031. China anchors capacity additions with BASF’s Zhanjiang Verbund complex slated for start-up in 2025. India’s production grows alongside local polyester fiber expansion, supported by government manufacturing incentives. Regional governments tighten environmental norms, but integrated complexes with advanced abatement maintain competitiveness.

North America benefits from shale-based ethane economics that yield some of the world’s lowest ethylene cash costs. Medical device sterilization concentration elevates domestic consumption, and INEOS’s 2024 acquisition of LyondellBasell’s Bayport unit consolidates supply in the largest single market. Compliance with EPA emission rules accelerates investment in catalytic scrubbers and real-time monitoring, setting a global technology benchmark.

Europe confronts high energy prices and more stringent CO₂ targets, prompting 11 million tons of regional chemical capacity closures during 2023-2024. Collaborations such as the 2024 Clariant-OMV agreement to supply lower-carbon ethylene and ethylene oxide derivatives aim to defend market share against imports. Eastern Europe retains selective competitiveness through access to pipeline gas and established downstream polyester assets.

The Middle East leverages advantaged feedstock at integrated complexes, with Saudi-based producers targeting export markets in Asia. Africa sees limited local production but steady imports for detergent and agrochemical formulations. South America advances bio-ethylene projects in Brazil, positioning the subcontinent as a potential net exporter of low-carbon derivatives over the next decade.

Competitive Landscape

The ethylene oxide market features vertically integrated multinationals such as BASF, Dow, SABIC, and INEOS, each controlling feedstock, oxide, and downstream derivatives. INEOS’s USD 700 million purchase of the Bayport plant expands its North American footprint and downstream surfactant presence. BASF raised Antwerp oxide capacity in 2024 and continues to integrate derivatives into high-margin specialties. Dow prioritizes circular polymers development that supports the monoethylene glycol and PET recycling demand growth.

Sustainability differentiation is rising. Dow disclosed plans to commercialize 3 million metric tons of renewable and circular solutions annually by 2030, aiming to lock key consumer-goods customers into long-term supply frameworks. Technology providers compete on advanced silver catalysts that enable higher selectivity and longer run lengths, reducing energy use and by-product formation.

Market entrants explore small-scale oxidative coupling or bio-route projects that promise modular deployment near biomass sources. Established producers counter by offering low-carbon grades under mass-balance accounting systems and investing in closed-loop take-back programs with PET recyclers. Intellectual-property barriers and economies of scale keep the industry moderately consolidated, yet regional regulatory shifts can redraw competitive positions rapidly.

Ethylene Oxide Industry Leaders

BASF SE

China Petrochemical Corporation

Dow

SABIC

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: INEOS has successfully completed the acquisition of LyondellBasell's (LYB) Ethylene Oxide & Derivatives (EO&D) business, including its production facilities in Bayport, Texas, United States. This strategic move is expected to strengthen INEOS's position in the ethylene oxide market, enhancing its production capabilities and market share.

- June 2024: Nouryon has achieved ISCC PLUS certification for its green ethylene oxide and ethanolamines, highlighting its commitment to sustainable production practices. This milestone is expected to positively influence the ethylene oxide market by driving demand for environmentally friendly and certified products.

Global Ethylene Oxide Market Report Scope

Ethylene oxide is produced from ethylene, majorly by direct oxidation. Ethylene is primarily produced from petrochemical-based raw materials, such as naptha, ethane, and propane, which are obtained from the distillation of crude oil. The market is segmented on the basis of derivative, end-user industry, and geography. By derivative, the market is segmented into ethylene glycols, ethoxylates, ethanolamines, glycol ethers, polyethylene glycol, and other derivatives. By end-user industry, the market is segmented into automotive, agrochemicals, food and beverage, textile, personal care, pharmaceuticals, detergents, and other end-user industries. The report also covers the market size and forecasts for ethylene oxide in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Ethylene Glycols | Monoethylene Glycol (MEG) |

| Diethylene Glycol (DEG) | |

| Triethylene Glycol (TEG) | |

| Ethoxylates | |

| Ethanolamines | |

| Glycol Ethers | |

| Polyethylene Glycol | |

| Other Derivatives |

| Polyester Fiber and PET Resins |

| Surfactants and Detergents |

| Sterilization and Fumigation |

| Coolant and Antifreeze |

| Pharmaceuticals Excipients |

| Other Applications |

| Automotive |

| Agrochemicals |

| Food and Beverage |

| Textile |

| Personal Care |

| Pharmaceuticals |

| Detergents |

| Others End user Industries |

| Petro-based Ethylene |

| Bio-ethylene |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Derivative | Ethylene Glycols | Monoethylene Glycol (MEG) |

| Diethylene Glycol (DEG) | ||

| Triethylene Glycol (TEG) | ||

| Ethoxylates | ||

| Ethanolamines | ||

| Glycol Ethers | ||

| Polyethylene Glycol | ||

| Other Derivatives | ||

| By Application | Polyester Fiber and PET Resins | |

| Surfactants and Detergents | ||

| Sterilization and Fumigation | ||

| Coolant and Antifreeze | ||

| Pharmaceuticals Excipients | ||

| Other Applications | ||

| By End-user Industry | Automotive | |

| Agrochemicals | ||

| Food and Beverage | ||

| Textile | ||

| Personal Care | ||

| Pharmaceuticals | ||

| Detergents | ||

| Others End user Industries | ||

| By Feedstock | Petro-based Ethylene | |

| Bio-ethylene | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in the ethylene oxide market?

Demand for polyester fibers, PET packaging, medical device sterilization, and sustainable surfactants is expected to keep volumes rising at a 3.34% CAGR through 2031.

Why is Asia-Pacific the leading region?

Strong textile manufacturing, expanding PET resin plants, and large integrated chemical complexes give Asia-Pacific a 50.72% share and the fastest 3.68% CAGR outlook.

Which derivative segment is growing fastest?

Ethanolamines, supported by agrochemicals and personal-care demand, post a 3.55% CAGR from 2026-2031.

How are tightening EPA regulations affecting the market?

Facilities must cut ethylene oxide emissions by up to 99.9%, prompting heavy investment in catalytic scrubbers yet preserving sterilization demand due to lack of full substitutes.

What is the current volume of the global ethylene oxide market?

The ethylene oxide market size was 38.55 million tons in 2026.

Page last updated on: