Nigeria Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

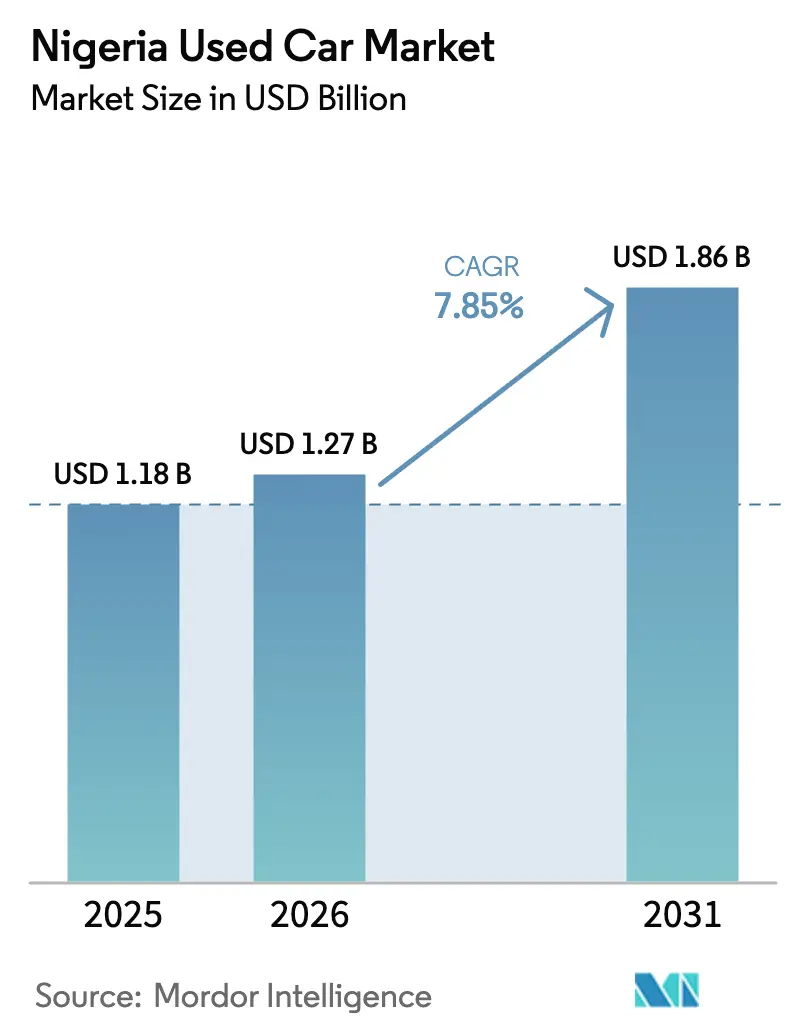

| Base Year Market Size (2025) | USD 1.18 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

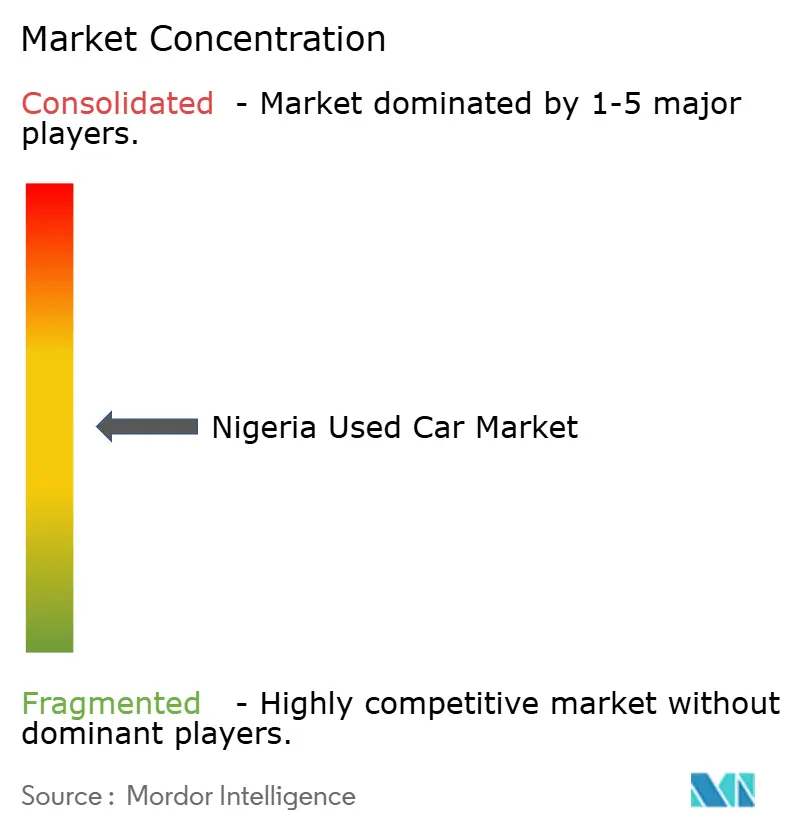

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Used Car Market Analysis by Mordor Intelligence

The Nigerian used car market size is expected to grow from USD 1.18 billion in 2025 to USD 1.27 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at 7.85% CAGR over 2026-2031. A shift drives the market's growth to digital retail channels, fintech innovations improving vehicle financing access, and diaspora remittances enabling near-new vehicle imports that offer better value than new ones. A persistent gap between new car prices and household purchasing power, compounded by inflation, high interest rates, and naira depreciation, has pushed many toward pre-owned vehicles as a more affordable option in a challenging economic environment. Organized online platforms capitalize on the shift through transparent pricing, verified inspection reports, and bundled loans. Meanwhile, customs enforcement of a 12-year age ceiling and higher duties compress import volumes, creating scarcity that supports residual values and accelerates domestic remarketing programs.

Key Report Takeaways

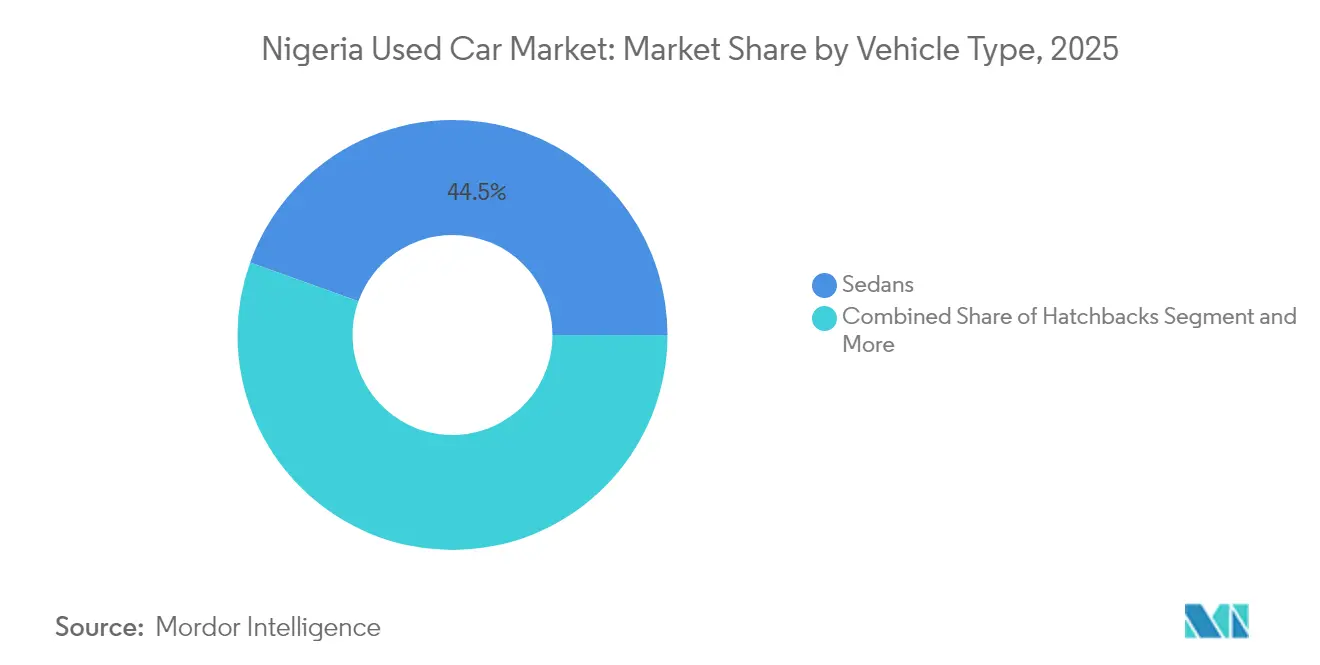

- By vehicle type, sedans held 44.52% of Nigeria's used car market share in 2025, while SUVs and MPVs are on track for a 9.12% CAGR through 2031.

- By vendor type, unorganized dealers controlled 70.49% of Nigeria's used car market share in 2025; organized platforms are poised to compound at a 9.68% CAGR to 2031.

- By fuel type, petrol cars captured 78.88% of Nigeria's used car market share in 2025, but electric vehicles are expected to post an 11.12% CAGR over the forecast horizon.

- By sales channel, offline showrooms accounted for 52.62% of Nigeria's used car market share in 2025, and online channels are accelerating at a 10.05% CAGR through 2031.

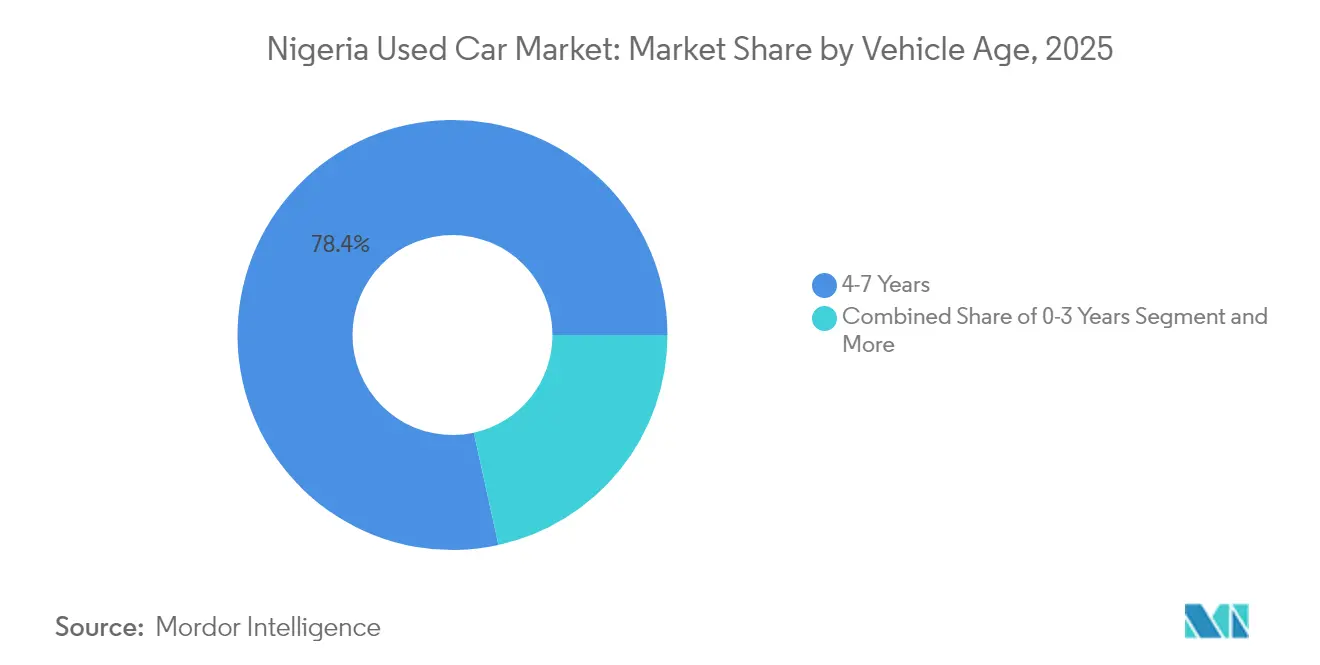

- By vehicle age, the 4–7-year cohort dominated, with 78.43% of Nigeria's used car market share in 2025, while 0–3-year units represent the fastest-growing slice, with a 10.24% CAGR.

- By customer type, individual buyers led with 89.78% of Nigeria's used car market share in 2025, while corporate / fleet purchases accounted for 10.22%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria participates in a competitive field that extends beyond its own borders. The market landscape in the global used car industry outlined by Mordor Intelligence covers that wider structure.

Nigeria Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Vehicle Platforms | +2.1% | National, with concentration in Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Affordable Mobility Demand | +1.8% | National, strongest in urban centers | Long term (≥ 4 years) |

| Fintech Auto-Leasing Growth | +1.4% | National, with early adoption in Lagos, Abuja | Medium term (2-4 years) |

| Diaspora Vehicle Inflows | +1.2% | National, with concentration in diaspora-connected communities | Short term (≤ 2 years) |

| Ride-Hailing Fleet Renewals | +0.9% | Urban centers, primarily Lagos, Abuja, Port Harcourt | Short term (≤ 2 years) |

| State Inspection Expansion | +0.8% | National, phased rollout across states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Digital Platforms for Vehicle Discovery and Price-Transparency

Autochek, Cars45, and similar portals now deploy VIN decoding, fraud analytics, and remote inspection scheduling that shorten search times and narrow information asymmetry. Autochek’s back-end captures device fingerprints and financial SMS patterns to flag suspicious traffic [1]“Privacy Policy,”, Autochek, autochek.africa. Rapid mobile-data uptake underpins a marketplace where buyers confirm service history, access instant loan quotes, and book delivery slots from a single app. Network effects reward compliant sellers with faster inventory turnover and embed smaller traders into digital ecosystems at lower marginal cost.

Growing Middle-Class Demand for Affordable Mobility Solutions

While price pressures are starting to lighten, many households still grapple with a challenging financial landscape. Daily living costs are stretching budgets thin, and borrowing remains tightly constrained. Consequently, most consumers find financing a new vehicle unattainable, further solidifying their inclination towards budget-friendly, pre-owned alternatives. Therefore, the Nigerian used car market absorbs latent demand, especially for fuel-efficient sedans and compact SUVs with established service parts. Naira weakness inflates showroom prices yet magnifies the value of diaspora remittances, allowing families to fund near-new imports with foreign currency support. Structured products such as revenue-share vehicle loans for ride-hailing drivers broaden eligibility beyond salaried borrowers, redirecting traffic to certified pre-owned schemes that bundle warranty protection.

Expansion of Fintech-Enabled Auto-Loans and Micro-Leasing Products

Moove is expanding its vehicle financing operations, using ride-hailing earnings as a repayment method. The company's model integrates insurance, maintenance, and digital tracking into a unified cost structure, simplifying driver vehicle ownership. By partnering with major platforms such as Uber and Bolt, Moove facilitates automated repayments and assists operators, often excluded from traditional banking, in establishing their financial profiles.

In parallel, LagRide's launch of electric taxis via bank-backed leases underscores a rising trend: merging clean energy with novel financing solutions. The concept of micro-leasing is broadening its horizons, now encompassing mini-buses and two-wheelers. This expansion is bolstered by technologies like telematics and remote immobilizers, which are crucial in mitigating default risks. Collectively, these advancements signal a significant shift in mobility finance, where digital innovations and alternative credit avenues enhance access and affordability.

Diaspora Vehicle Remittances Increasing Supply of Near-New Cars

Remittances from abroad increasingly shape Nigeria's automotive landscape. Many expatriates are keen on investing back home, with vehicles topping the list. These imports are often newer, well-maintained cars that align with international safety and emissions standards, carving out a premium niche in the used car market.

Policy proposals, like dedicated investment funds, aim to formalize and streamline these diaspora contributions, potentially boosting import efficiency and broadening financing access. Yet, looming regulatory risks, such as possible levies on outbound remittances from major sending countries, introduce uncertainty to future inflows. This vulnerability in the supply chain highlights the urgent need for adaptive and resilient policy frameworks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import Duty and Port Costs | -2.3% | National, with concentration at Lagos, Port Harcourt ports | Short term (≤ 2 years) |

| Naira Depreciation Impact | -1.9% | National, affecting all import-dependent segments | Medium term (2-4 years) |

| Used EV Battery Concerns | -0.7% | Urban centers with EV adoption, primarily Lagos, Abuja | Long term (≥ 4 years) |

| Odometer and VIN Fraud | -0.6% | National, more prevalent in unorganized dealer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hike in Import Duties and Port Surcharges Raising Landed Cost

Importing vehicles into Nigeria has become both costly and increasingly intricate. Recent, albeit minor, adjustments to duty rates underscore a wider trend of heightened fiscal scrutiny[2]“Monthly Economic Report November 2024,”, Central Bank of Nigeria, cbn.gov.ng. The shift from Fast-Track to Authorised Economic Operator status elevates paperwork requirements and adds compliance spend that smaller importers struggle to absorb. Enforcing 12-year age caps squeezes the supply pool, nudging dealers toward local refurbishing contracts or certified pre-owned sourcing. Rising port service fees in Apapa and Tin Can further widen the cost gap between imported stock and domestically reconditioned vehicles.

Persistent Odometer and VIN Tampering Despite Inspection Apps

Unorganized sellers represent around 70% of the Nigerian used car market, and many transactions occur without digital footprints. State-by-state registration silos limit VIN checks across borders, allowing fraud migration. The Police e-CMR system and FRSC VREG portal enhance traceability but require uniform state adoption to close loopholes[3]“VREG User Guide,”, Federal Road Safety Corps, frsc.gov.ng. Organized marketplaces employ machine-learning outlier detection for mileage consistency, yet cost-sensitive buyers may forego paid reports and remain exposed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Sedans Maintain Leadership as SUV Demand Surges

Sedans controlled 44.52% of Nigeria's used car market share in 2025, thanks to advantageous pricing and broad parts networks. SUVs and MPVs are forecast to realize a 9.12% CAGR through 2031, reflecting ride-height advantages on suburban roads and growing aspirational appeal. The Nigerian used car market size tied to sedans is projected to expand steadily as Corolla and Camry units dominate re-exports from the United States and the Middle East.

In Lagos and Abuja, SUV momentum is evident, where rising disposable income supports larger frames without sacrificing daily usability. Local assembly from Stallion Group and Globe Motors places new-SUV sticker prices within reach of upper-middle-income households, indirectly boosting residual values and improving finance terms in the secondary channel. Taxi-fleet renewals add volume to MPVs such as the Toyota Sienna, feeding downstream remarketing streams.

By Vendor Type: Organized Platforms Narrow the Gap

Unorganized dealerships accounted for 70.49% of 2025 transactions, but online intermediaries and branded showrooms are advancing at a 9.68% CAGR as buyers seek verified history and financing. Embedded credit, warranty, and insurance bundles anchor customer retention and lift gross margin per unit.

Regulatory changes favor scale players: Authorised Economic Operator certification expedites clearance, while digital duty payment trails shield compliant importers from retrospective penalties. Smaller roadside traders risk obsolescence unless integrated into platform partner programs that provide stock-turn guarantees and digital storefronts.

By Fuel Type: Petrol Dominates, Electric Gains Traction

Petrol cars held 78.88% of the 2025 base, mirroring fuel retail coverage and mechanical familiarity among roadside technicians. Electric vehicles, however, post the highest 11.12% CAGR, thanks to policy pledges for 100% zero-emission new-car sales by 2040 and escalating pump prices. The Nigerian used car market size for EVs remains small but highly visible, anchored by corporate taxi schemes and financier-backed driver-ownership contracts.

Battery-swap corridors and solar-powered charge hubs solve grid reliability concerns in pilot zones, trimming range anxiety and sustaining future residual value expectations. Diesel vehicles retain a foothold in commercial logistics and oil-region shuttle services, but their share will likely shrink under tightening emission oversight.

By Sales Channel: Online Platforms Scale Rapidly

Offline lots still represent 52.62% of transactions, reflecting cultural preference for physical inspection. Yet online portals are on course for a 10.05% CAGR through 2031 as virtual reality walk-arounds, escrow services, and no-fault return windows replicate showroom reassurance. The Nigerian used car market share for purely digital transactions widens further when platforms embed trade-in calculators that give instant price discovery, compressing traditional negotiation cycles.

Hybrid dealer models now livestream vehicle walk-throughs from forecourts, extending geographic reach without duplicating inventory. Logistics partners offer 48-hour inter-state delivery with insurance against in-transit damage, erasing a historic barrier to sight-unseen purchases.

By Vehicle Age: Near-New Category Accelerates

Units aged 4–7 years formed 78.43% of turnover in 2025, a sweet spot where depreciation stabilizes while reliability remains attractive. The 0–3-year bracket records a 10.24% CAGR, fueled by diaspora imports of late-model sedans and SUVs and ride-hailing fleet rotations completed within 36 months. Nigeria's used car market size, attached to near-new vehicles, benefits from certified pre-owned programs, adding two-year warranties and service plans, qualifying for bank financing at mid-teens interest.

Import age restrictions and tighter odometer audits constrain inflows of over-aged vehicles, lifting demand for younger inventory and compelling price-sensitive buyers toward installment plans instead of outright cash.

By Customer Type: Individual Purchases Dominate Yet Fleet Demand Shapes Supply

Individual buyers controlled 89.78% of 2025 transactions, underscoring the importance of personal mobility in cities where public transport remains limited. Their dominance reflects widening access to fintech loans, strong diaspora support, and a cultural preference for outright ownership that minimizes recurring payments. This customer tier gravitates toward sedans and compact SUVs with proven parts availability, pushing platforms to emphasize instant credit scoring and warranty bundles that lower perceived risk. As smartphone penetration deepens, individuals increasingly complete end-to-end purchases online, reinforcing the network effects that benefit well-capitalized digital intermediaries.

Corporate and fleet accounts represented a smaller 10.22% slice but exert disproportionate influence through bulk orders and predictable replacement cycles that seed the secondary market with near-new inventory. Ride-hailing operators, logistics start-ups, and government agencies make up the core of this segment, favoring vehicles with extended warranty coverage and telematics packages that optimize uptime. Their standardized specifications create pricing benchmarks that shape residual values for comparable models in the wider retail channel. Fleet managers’ push for lower total cost of ownership accelerates demand for fuel-efficient powertrains and, increasingly, electric taxis financed under revenue-share leases. As these vehicles funnel back into circulation after three to four years, they expand the supply of younger, better-documented units that satisfy rising quality expectations among individual buyers.

Geography Analysis

Lagos underpins roughly one-third of national registrations, housing major ports and the headquarters of Autochek, Cars45, and multiple fintech lenders. High population density, advanced road networks, and concentrated economic activity create a prime catchment for organized marketplaces. Abuja follows, serving federal civil servants and diplomatic communities that favor premium, near-new imports.

Port Harcourt and adjoining oil-producing corridors sustain demand via expatriate compensation packages and higher median wages than non-oil states. Kano and Kaduna illustrate the Nigerian used car market’s inland dynamics: longer supply chains add freight premiums, and limited spare-parts networks bias demand toward ubiquitous Toyota and Honda sedans.

State-level disparities in registration fees, plate issuance backlogs, and inspection protocols influence cross-border vehicle flows, encouraging some traders to route shipments through states with quicker turnaround. Implementing the FRSC VREG portal aims to harmonize processes, but adoption lags in several northern and eastern states, perpetuating inconsistencies that organized platforms must absorb when pricing trade-ins.

Mordor Intelligence provides coverage of the used car market across other key regional markets, including Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Tanzania, South Africa, South Korea, Brazil, Bangladesh, Kuwait, Canada, and Qatar incorporating local coverage and market participation, as required.

Competitive Landscape

The market remains fragmented, yet capital-backed platforms pursue share via technology, financing, and network breadth. Autochek’s AI-driven fraud engine flags mileage anomalies within seconds, reducing arbitration costs and boosting buyer confidence. Moove scales ride-hailing fleet ownership by underwriting revenue-share loans, and its planned USD 1.2 billion debt raise underscores institutional appetite for asset-backed mobility debt.

Shekel Mobility addresses the supply side, extending working capital and inventory software to informal yards, effectively onboarding fragmented stock onto a unified marketplace. Battery-health certification represents an emerging white space; platforms that pioneer standardized reporting can monetize inspection data and unlock lender acceptance for used EVs.

Regulatory shifts award advantage to compliant importers: Authorised Economic Operator status accelerates customs clearance. At the same time, e-CMR integration lowers vehicle theft risk, both valuable datapoints for insurers that bundle cover through marketplace check-out flows. Smaller unorganized traders maintain local trust and flexible cash terms but face margin compression as tech-enabled rivals drive price discovery closer to book values.

Nigeria Used Car Industry Leaders

Jiji (Cars45)

Carmart

OList

Autochek Africa

Betacar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Afreximbank, the African Export-Import Bank, has extended its memorandum of understanding with the African Association of Automotive Manufacturers (AAAM). This collaboration seeks to enhance trade and investment within Africa's automotive sector. Key objectives include the establishment of regional value chains, bolstering financing for the sector, and fortifying associated policies and capabilities.

- February 2025: Stanbic IBTC Bank has teamed up with Autochek, a cutting-edge automotive technology company, to make car ownership more accessible in Nigeria. This partnership aims to streamline the car financing process, providing customers with easier access to loans and a seamless vehicle purchase experience. By leveraging Autochek's innovative platform and Stanbic IBTC Bank's financial expertise, the collaboration seeks to address challenges in the automotive market and enhance affordability for prospective car owners.

Nigeria Used Car Market Report Scope

A used car/pre-owned vehicle, or a secondhand car, is a vehicle that previously had one or more retail owners. A certified pre-owned (CPO) vehicle, on the other hand, is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned. The used car market consists of a wide range of companies involved in the purchasing and selling of pre-owned vehicles through online or offline sales channels.

The Nigeria used car market is segmented by vehicle type, vendor type, fuel type, and sales channel. By vehicle type, the market is segmented into hatchbacks, sedans, and sports utility vehicles (SUVs)/multi-purpose vehicles (MPVs). By vendor type, the market is segmented into organized and unorganized. by fuel type, the market is segmented into petrol, diesel, electric, and other fuel types (liquefied petroleum gas, compressed natural gas, etc.). by sales channel, the market is segmented into online and offline.

The report offers market size and forecast value (USD) for all the above segments.

| Hatchbacks |

| Sedans |

| SUVs/MPVs |

| Organised |

| Unorganised |

| Petrol |

| Diesel |

| Electric |

| Other Fuels (LPG, CNG, etc.) |

| Online |

| Offline |

| 0-3 Years |

| 4-7 Years |

| 8+ Years |

| Individual |

| Corporate / Fleet |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| SUVs/MPVs | |

| By Vendor Type | Organised |

| Unorganised | |

| By Fuel Type | Petrol |

| Diesel | |

| Electric | |

| Other Fuels (LPG, CNG, etc.) | |

| By Sales Channel | Online |

| Offline | |

| By Vehicle Age | 0-3 Years |

| 4-7 Years | |

| 8+ Years | |

| By Customer Type | Individual |

| Corporate / Fleet |

Key Questions Answered in the Report

How large is the Nigeria used car market in 2026?

The Nigeria used car market size stands at USD 1.27 billion in 2026.

What is the projected growth rate for used cars in Nigeria?

Market value is forecast to rise at an 7.85% CAGR between 2026 and 2031.

Which vehicle types dominate Nigerian used-car purchases?

Sedans lead with 44.52% share, followed by fast-growing SUVs and MPVs.

Why are fintech loans important to used-car sales?

Revenue-share and micro-leasing products widen access for ride-hailing drivers and first-time buyers who lack traditional credit history.

Which cities generate the most online used-car activity?

Lagos remains the primary hub, with Abuja and Port Harcourt showing rapid adoption of digital platforms.

Page last updated on: