Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

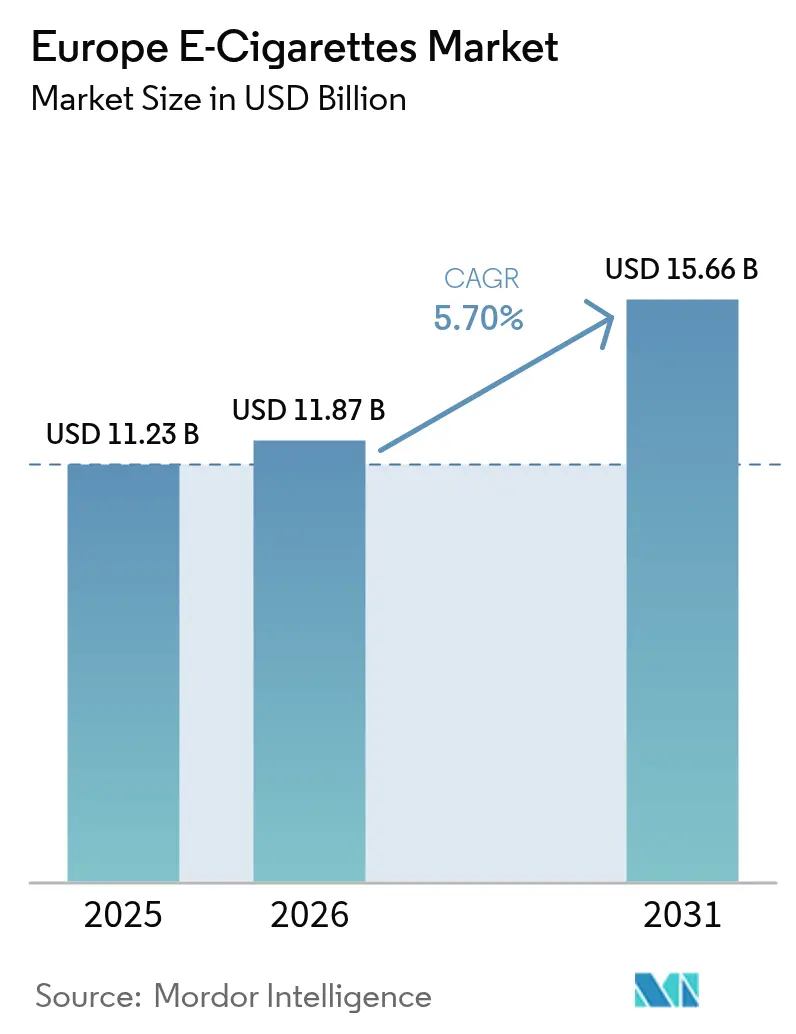

| Base Year Market Size (2025) | USD 11.23 Billion |

| Market Size (2026) | USD 11.87 Billion |

| Market Size (2031) | USD 15.66 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe E-Cigarettes Market Analysis by Mordor Intelligence

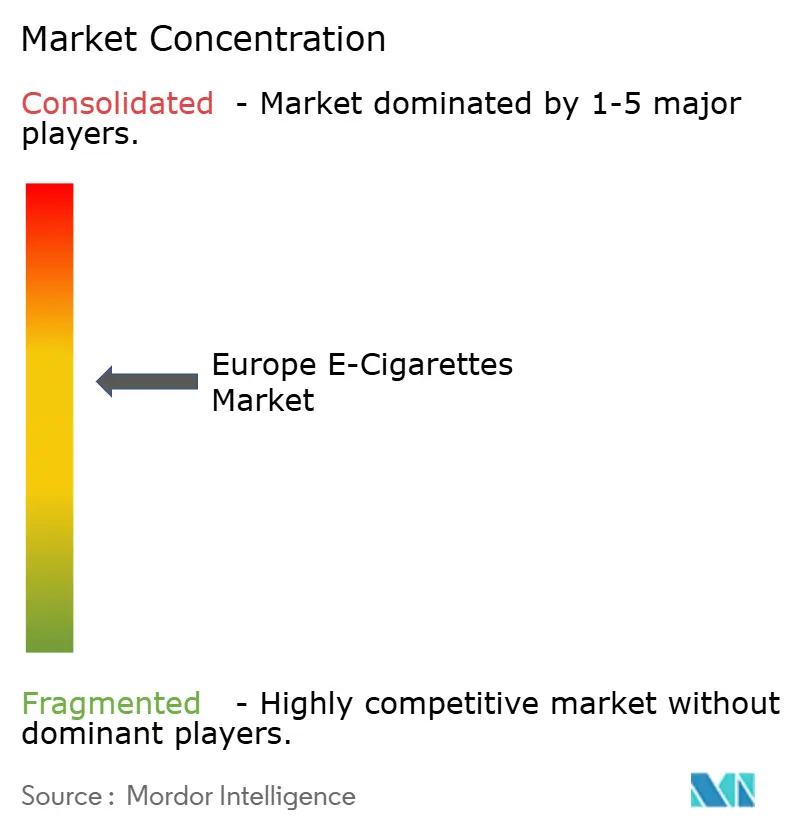

The European e-cigarettes market size was valued at USD 11.23 billion in 2025 and estimated to grow from USD 11.87 billion in 2026 to reach USD 15.66 billion by 2031, at a CAGR of 5.70% during the forecast period (2026-2031). This growth highlights the shift of vaping from being a niche alternative to becoming a widely accepted category, supported by endorsements from several public health authorities across Europe. The increasing demand is driven by factors such as harm-reduction evidence, improved product availability, and supportive regulations in countries like the United Kingdom and some Central and Eastern European nations. However, the market faces challenges, including inconsistent regulations across the European Union, higher excise taxes, and the proliferation of illegal disposable vaping products. These issues make it more complex for companies to navigate the market and emphasize the importance of adhering to strict compliance measures. The competition in the market is intensifying as established tobacco companies and emerging technology-driven players compete to stand out. Companies are focusing on innovations such as scientifically backed product claims, advanced coil technologies, and measures to prevent youth access to vaping products. The European e-cigarettes market is moderately consolidated, with global tobacco giants, hardware innovators, and regional players competing for market share and shelf space.

Key Report Takeaways

- By geography, the United Kingdom led with 43.23% of the European e-cigarettes market share in 2025; Spain is projected to post the fastest 5.76% CAGR to 2031.

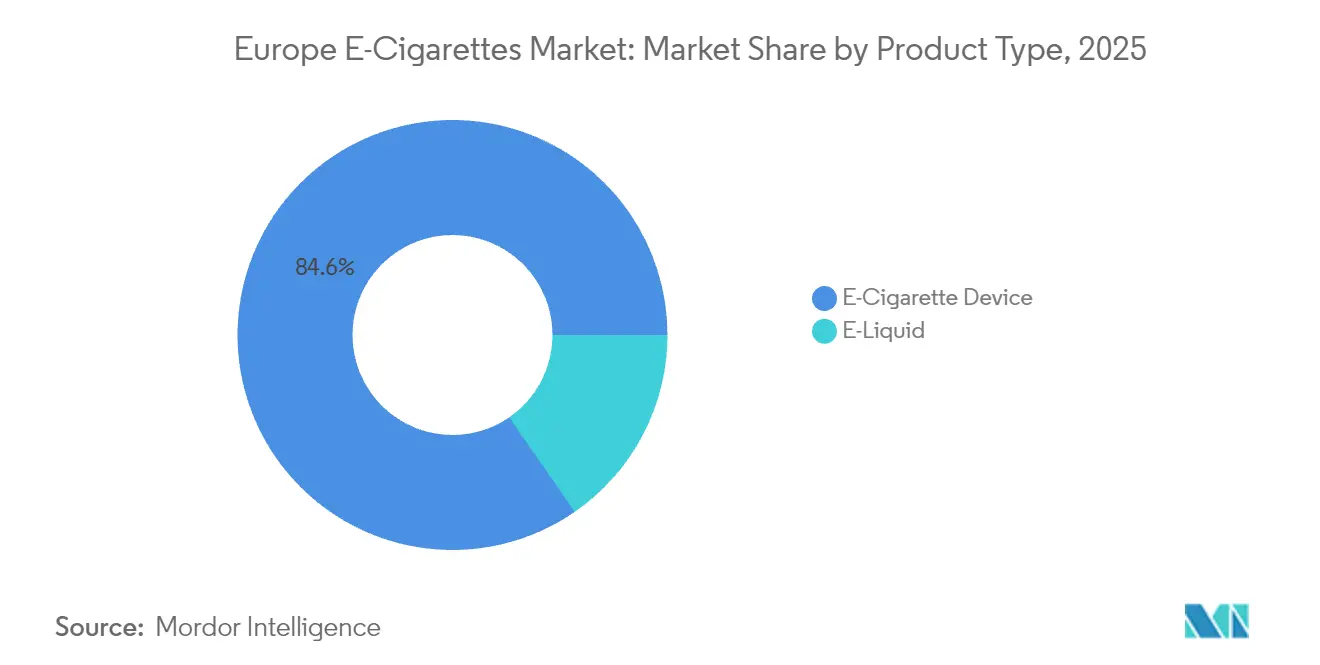

- By product type, e-cigarette devices accounted for 84.62% of revenue in 2025, while e-liquids are poised to grow at a 5.22% CAGR through 2031.

- By category, closed systems controlled 76.10% of sales in 2025; open systems are forecast to expand at a 5.18% CAGR to 2031.

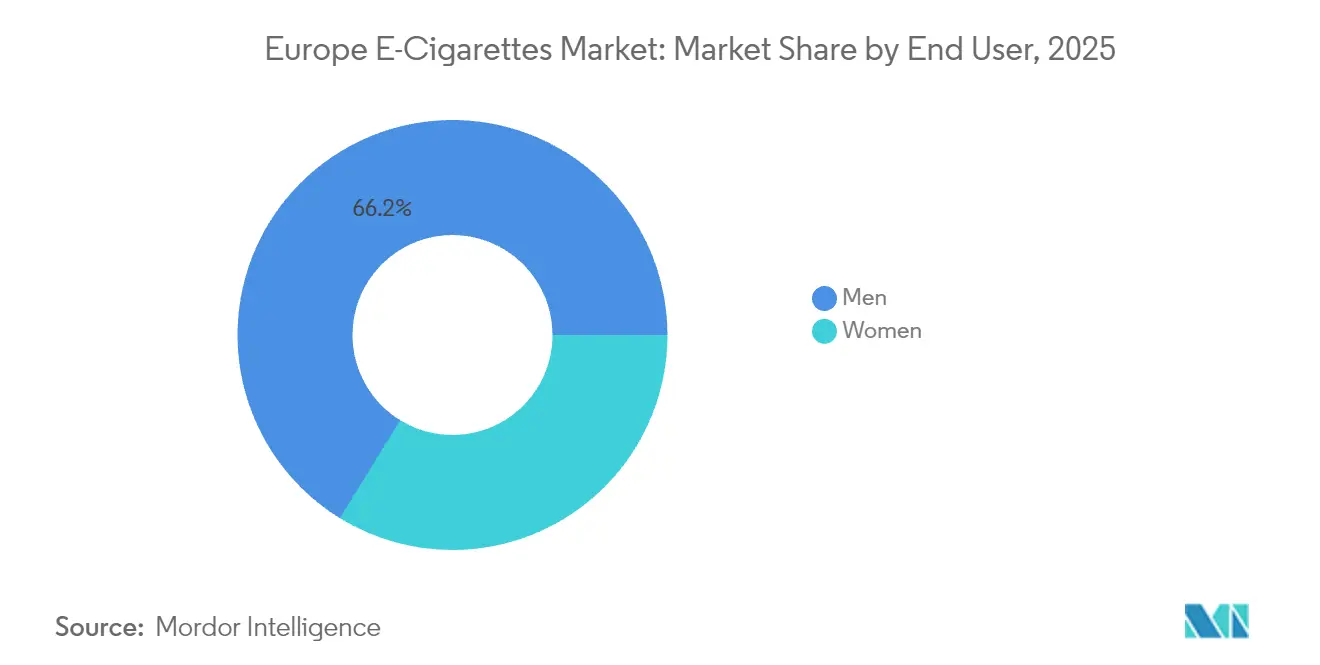

- By end user, men represented 66.22% of the user base in 2025, yet women constitute the fastest-growing cohort at a 5.42% CAGR to 2031.

- By distribution channel, offline retail generated 68.40% of revenue in 2025, whereas online sales are expected to rise at a 6.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe E-Cigarettes Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Availability and diversity of flavors | +1.2% | Strongest in United Kingdom, Netherlands, Germany | Medium term (2-4 years) |

| Supportive regulatory stances in key markets | +0.9% | United Kingdom, Czech Republic, emerging in Greece, Hungary | Long term (≥ 4 years) |

| Public health campaigns and awareness programs | +0.7% | United Kingdom, France, Sweden, expanding Europe-wide | Medium term (2-4 years) |

| Increasing health consciousness and harm reduction awareness | +0.8% | Particularly strong in Northern Europe | Long term (≥ 4 years) |

| Technological advancements and product innovation | +0.6% | Led by United Kingdom, Germany, Netherlands | Short term (≤ 2 years) |

| Social media and influencer marketing | +0.4% | Strongest impact in younger demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing health consciousness and harm reduction awareness

Health awareness and the growing focus on harm reduction are driving the increasing use of e-cigarettes across Europe. Consumers are moving away from traditional tobacco products and opting for less harmful alternatives. In the first quarter of 2025, Philip Morris International reported that 42% of its total revenue came from smoke-free products, with a strong presence in Europe. This growth was supported by the launch of products like IQOS Iluma in several EU markets in late 2024. Scandinavia, known for its low smoking rates, continues to set an example for effective and balanced tobacco regulation. In France, a 2024 survey conducted by Kumulus Vape, in collaboration with the French Institute of Public Opinion (IFOP), revealed that 83% of vapers experienced improved well-being and cost savings compared to smoking traditional cigarettes[1]Source: Kumulus Vape, " The IFOP 2025 survey for Kumulus Vape highlights the effectiveness of vaping," kumulusvape.fr. Adding to this momentum, British American Tobacco introduced its Vuse Pro in early 2025 across several European countries.

Public health campaigns and awareness programs

Governments across Europe are increasingly supporting vaping as a safer alternative to help adults quit smoking, while also taking steps to prevent its misuse among young people. The WHO European Region has the highest adult smoking rate globally, at 28%, which highlights the need for effective alternatives[2]Source: World Health Organization, "Globally, the WHO European Region has the highest prevalence of tobacco smoking among adults (28%)," who.int. To address this, the UK government launched the “Swap to Stop” program in 2023, providing one million adult smokers with free vape starter kits and behavioral support. The Government of the UK reports that vaping helps an additional 50,000–70,000 people quit smoking each year. Among exclusive vapers, this confidence rises to 85%, showing growing trust in vaping as a solution. However, youth experimentation with vaping is also increasing. For example, in England, 1 in 4 teens aged 11–15 have tried vaping, which highlights the need for better education and awareness, according to the National Health Service (NHS), England, as of 2024[3]Source: National Health Service, "Almost 1 in 10 secondary school pupils currently vape, new NHS survey shows," england.nhs.uk. Moving forward, public health campaigns must focus on clear messaging emphasizing vaping’s benefits for adult smokers while educating young people about its appropriate use.

Supportive regulatory stances in key markets

European regulators are increasingly creating policies that support the use of e-cigarettes as effective tools to help people quit smoking, while also ensuring proper safety measures are in place. In the UK, a report by the Royal College of Physicians in April 2024 highlighted that vaping products are more effective in helping people quit smoking compared to traditional nicotine replacement therapies. This reinforces the UK’s approach of using evidence to promote harm reduction. Similarly, Greece has included harm reduction in its national tobacco strategy. Since 2020, the country has allowed companies to share science-based information about reduced-risk tobacco products, creating a more favorable environment for vaping businesses. Hungary has also adopted a supportive stance by classifying e-cigarettes as consumer goods under the EU Tobacco Products Directive (TPD), which has relaxed rules on advertising and product notifications. These flexible policies allow vaping companies to grow in markets with fewer restrictions before entering stricter ones.

Availability and diversity of flavors

Flavor options play a significant role in helping adults stick to vaping and quit smoking in Europe. In France, a 2024 survey conducted by Kumulus Vape, in collaboration with the French Institute of Public Opinion (IFOP) revealed that 66% of French vapers believe having a variety of flavors is crucial for staying with vaping and successfully quitting smoking. To meet this demand, companies are introducing innovative products with advanced features. For instance, CFU’s UP2U multi-layer pod system offers staggered flavor release, allowing users to enjoy multiple flavors in one device. Similarly, the Voopoo Drag Bar Z700 SE, launched in France and Germany in late 2024, provides a compact design with dual-flavor capability, enabling users to switch flavors during use for a more personalized experience. However, stricter regulations across Europe, such as flavor bans in countries like Slovenia, Finland, and Hungary, along with the Netherlands’ 2024 rule restricting e-liquids to tobacco flavors, are pushing companies to adapt.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Availability of illegal and unauthorized products | -1.4% | Particularly severe in Germany, United Kingdom, France | Short term (≤ 2 years) |

| Youth vaping concerns and related restrictions | -0.8% | Europe-wide, strongest impact in Belgium, Ireland, France | Medium term (2-4 years) |

| Taxation on vaping products | -0.6% | 20 European countries, expanding coverage | Medium term (2-4 years) |

| Health concerns and uncertainty over long-term effects | -0.5% | Varying intensity by country | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of illegal and unauthorized products

The increasing availability of illegal and unauthorized vaping products is creating significant challenges for the regulated vaping market in Europe, both financially and in terms of public health. Major manufacturers are feeling the strain. For example, British American Tobacco highlighted in its 2024 earnings call that the rise of illicit single-use vapes has been a major factor in declining sales volumes. The company pointed out that weak enforcement is shifting consumer demand to the illegal market rather than reducing overall consumption. Regulatory measures, such as flavor bans, can unintentionally worsen this issue. In Quebec, for instance, flavor restrictions led to a noticeable increase in illegal sales as consumers sought alternatives outside the legal market. This situation highlights the need for stronger and more coordinated enforcement efforts. Customs agencies, trading standards authorities, and e-commerce platforms must work together to close enforcement gaps. Without such collaboration, regulatory goals may remain unachieved, and the illegal market will continue to grow.

Youth vaping concerns and related restrictions

Concerns about youth vaping are growing across Europe, leading to stricter regulations that are changing how vaping products are designed, marketed, and sold. Data from the European Parliament shows that nearly one-third of 15-year-olds have tried e-cigarettes, which has increased pressure on governments to act[4]Source: European Parliament, "EU-wide ban on flavoured and disposable vapes," europarl.europa.eu. In response, Belgium has banned disposable vapes starting January 2025, and Ireland is working on similar laws. This has resulted in inconsistent product availability across the region. The UK is also introducing the Tobacco and Vapes Bill, which proposes stricter rules on flavor names, packaging designs, and retailer licensing. These changes are forcing manufacturers to focus on branding that supports adult smoking cessation while also discouraging youth usage. While these regulations increase costs for compliance and frequent product adjustments, they also create opportunities for companies that adopt responsible practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Drive Market Dominance

In 2025, devices dominated the European e-cigarettes market, making up 84.62% of total sales. Their allure lies in features like temperature control and biometric locking, offering long-term value to a diverse consumer base. These customizable features cater to both novice and experienced users, enhancing the overall vaping experience. Meanwhile, e-liquids surged with a 5.22% CAGR, fueled by the rising trend of refillable vaping systems, especially as regulations clamp down on disposables. The shift toward refillable systems not only aligns with sustainability goals but also provides consumers with a wider variety of flavors and nicotine strengths. Projections for 2031 indicate that while device revenue will stay above USD 12 billion, e-liquids will play a pivotal role in bolstering customer retention and lifetime value for businesses.

Technological strides, including enhanced power chips, quick-charge batteries, and leak-proof pods, have lengthened the lifespan of vaping devices, curbing the frequency of replacements. These advancements not only improve device reliability but also enhance user convenience, making vaping more accessible and appealing. Yet, this evolution has paved the way for firms to pivot towards higher-margin accessories and premium components, such as advanced coils. Brands delving into modular systems stand to gain from both hardware sales and the recurring revenue stream from e-liquid purchases. However, they face the intricate challenge of regulatory compliance, as any design updates under the Tobacco Products Directive necessitate re-certification, complicating operations and inflating costs.

By Category: Closed Systems Maintain Control

In 2025, closed pods captured a dominant 76.10% share of the revenue, underscoring their widespread appeal, thanks to their user-friendly nature and reliable performance. These systems have taken the lead in Europe's e-cigarette landscape, catering to users who favor the convenience of pre-filled cartridges. With the integration of cartridge-lock technology, closed-pod systems not only safeguard the quality of e-liquids but also thwart unauthorized refills. This safeguard has gained prominence amid heightened regulatory scrutiny, especially in light of flavor bans reshaping the market. The blend of convenience and dependability has cemented closed pods as a top choice for consumers, reinforcing their status as a primary revenue generator.

Conversely, open tanks are carving out a niche, especially among seasoned users who value cost-effectiveness and flavor customization. With a growth rate of 5.18% CAGR, these systems resonate with a more discerning market segment. Open tanks empower users to refill with diverse e-liquids, enhancing flexibility and personalizing the vaping journey. In response to this trend, leading brands are broadening their offerings, introducing open-system devices to complement their established closed pods. A case in point is Hangsen, whose BAR range of salt-nicotine e-liquids is tailored for refillable pods, nudging users towards sustainable choices over disposable ones.

By End User: Women Drive Growth Acceleration

In 2025, men accounted for 66.22% of adult vapers, continuing to dominate the vaping demographic. However, the growth rate among male users has started to slow down. On the other hand, women are emerging as the fastest-growing group of vapers, with a compound annual growth rate (CAGR) of 5.42%. This shift is influencing product designs, with companies focusing on creating lighter, more portable devices, subtle color options, and reduced vapor output to appeal to female consumers. The European e-cigarettes market size linked to female users is projected to double between 2026 and 2031, presenting a significant opportunity for brands that cater to this segment with targeted products and marketing strategies. Features like flavored zero-nicotine options and wellness-focused messaging are particularly appealing to this growing demographic.

The increasing number of female vapers is also prompting retailers to rethink their approach to product displays and customer engagement. Stores are incorporating lifestyle-oriented displays and training staff to address female-specific concerns, such as nicotine dependency, pregnancy-related risks, and compatibility with cosmetics. Marketing campaigns that emphasize stress relief, odor-free vaping, and social acceptance are resonating well with women who are new to vaping. This shift in the gender mix is not only reshaping product offerings but also creating new opportunities for brands to expand their customer base by addressing the unique preferences and needs of female consumers.

By Distribution Channel: Digital Transformation Accelerates

In 2025, physical stores, including vape shops and convenience outlets, accounted for 68.40% of all vaping-related expenditures. This significant share underscores the value of hands-on experiences, allowing customers to test devices, sample flavors, and obtain tailored advice. Notably, vape shops play a pivotal role, acting as support centers for those aiming to quit smoking, thereby nurturing customer loyalty and fostering a community spirit. These establishments offer essential guidance, particularly beneficial for newcomers navigating the diverse product landscape. Additionally, physical stores provide an opportunity for customers to build trust with knowledgeable staff, who can offer insights into product safety and usage. Yet, despite their robust foothold, these physical outlets are increasingly challenged by the rising prominence of online platforms.

Online sales are witnessing a 6.02% CAGR, buoyed by features such as age-verification tools and subscription services that enhance convenience and offer savings. E-commerce platforms not only boast a broader product range but also facilitate swift cross-border transactions, a boon given the varying regulations across countries. However, the online segment faces challenges, including stricter digital marketing regulations and the removal of certain products from platforms, which can limit consumer access. In response, many retailers are pivoting towards hybrid retail strategies, incorporating solutions like click-and-collect services or in-store kiosks. These models allow customers to place digital orders while still benefiting from in-person assistance, bridging the gap between convenience and personalized support.

Geography Analysis

The United Kingdom held the largest share of the European e-cigarettes market in 2025, accounting for 43.23% of the total market. This dominance is largely due to supportive policies that promote e-cigarettes as effective tools for quitting smoking. The National Health Service provides clear guidance on vaping, and streamlined product-notification processes make it easier for companies to bring products to market. Additionally, the upcoming ban on single-use devices in June 2025 is expected to shift consumer preferences toward refillable pod systems and multi-pack e-liquid options, creating new opportunities for growth in the market.

Spain is projected to experience the fastest growth in the European e-cigarettes market, with a compound annual growth rate (CAGR) of 5.76% through 2031. This growth is driven by increasing awareness of harm-reduction benefits and rising tobacco taxes, which encourage smokers to switch to vaping. Companies like Philip Morris International have seen significant success with smoke-free products such as IQOS Iluma and VEEV, establishing a strong distribution network that other brands can utilize. Retailers in Spain are also adapting to this trend by introducing dedicated sections for heat-not-burn and vaping products.

Other major markets, including Germany, France, and Italy, contribute significantly to the region's revenue but face unique challenges. Meanwhile, a tax of EUR 0.08 per milliliter on nicotine-containing liquids puts pressure on price-sensitive consumers. Nordic countries like Sweden demonstrate the benefits of balanced regulations, achieving the lowest smoking rates in Europe. Similarly, Eastern European nations such as Greece, the Czech Republic, and Hungary are gradually relaxing their rules, creating new growth opportunities as disposable bans in Western Europe shift market focus to these regions.

Competitive Landscape

In the European e-cigarettes market, a moderately consolidated landscape sees global tobacco giants, hardware innovators, and regional specialists competing for dominance. British American Tobacco has emerged as a frontrunner, capitalizing on its broad presence across various sales channels and emphasizing clinical testing to back its product claims. Companies are now strategically differentiating themselves through scientific validation, flavor innovation, and nimbleness in navigating regulations. Their goal is twofold: to stay in sync with shifting EU directives and to attract both smokers seeking alternatives and lifestyle-focused vapers. Similarly, Philip Morris International has shifted its focus toward smoke-free products. This trend highlights the growing importance of reduced-risk products as companies adapt to changing consumer preferences and stricter regulations across Europe.

Imperial Brands is expanding its product offerings with Blu bar disposables and Blu 2.0 pod kits, incorporating environmentally friendly practices to address potential regulatory challenges. Technology-focused companies like RELX and Smoore are driving innovation by improving atomizer technology and streamlining contract manufacturing processes. These advancements allow them to cater to both branded and white-label markets across Europe. Meanwhile, regional players like Norse Impact have achieved notable success in specific markets, such as Sweden, where they hold a 27% market share. This success demonstrates how smaller companies can effectively compete with larger players by focusing on localized strategies and leveraging e-commerce expertise.

Illicit trade remains a significant challenge for the legal e-cigarette market, as it creates downward pressure on prices and forces compliant companies to bear additional costs for testing and regulatory compliance. To address these challenges, companies are focusing on ensuring supply chain transparency and introducing unique features such as child-resistant pods, authentication technology, and sustainable packaging. These innovations not only help brands stand out in a competitive market but also position them to better navigate increasing regulatory scrutiny. As the market continues to evolve, such strategies will be crucial for maintaining profitability and building consumer trust.

Europe E-Cigarettes Industry Leaders

-

British American Tobacco PLC

-

Philip Morris International, Inc.

-

Imperial Tobacco Group plc

-

Japan Tobacco International

-

Altria Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Upends Company introduced its latest open-system vaping device, which has received TPD certification. This innovative product features a 10mL e-liquid pod designed for extended usage and is powered by a high-capacity 1000mAh battery, ensuring reliable performance and convenience for users.

- May 2025: ELFBAR unveiled a disposable waterpipe-style e-cigarette, while DOJO introduced the BLAST 10K “2+8” pod system in the United Kingdom, signposting ongoing experimentation within regulatory limits.

- August 2024: Philip Morris introduced Veev One, a recyclable ceramic-heated closed-pod system, to the UK market. The product is now available through various UK retailers and online platforms, emphasizing the company's commitment to innovative and sustainable solutions in the vaping industry.

- June 2024: Arcus Compliance has acquired vape industry data platform VapeClick. VapeClick is a comprehensive online directory of UK Medicines and Healthcare products.

Europe E-Cigarettes Market Report Scope

An electronic cigarette or e-cigarette is a handheld device that vaporizes a flavored liquid.

The Europe e-cigarette Market is segmented by product type, battery mode, and geography. Based on product type, the market is segmented into the completely disposable model, rechargeable but disposable cartomizers, and personalized vaporizers. Based on battery mode, the market is segmented into automatic e-cigarettes and manual e-cigarettes. Based on geography, the market is studied for the United Kingdom, France, Germany, Italy, Russia, Spain, and the Rest of Europe.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| E-Cigarette Device | Disposable E-Cigarette |

| Non-Disposable E-Cigarette | |

| E-Liquid |

By Category

| Open Vaping Systems |

| Closed Vaping Systems |

By End User

| Men |

| Women |

By Distribution Channel

| Offline Stores |

| Online Stores |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | E-Cigarette Device | Disposable E-Cigarette |

| Non-Disposable E-Cigarette | ||

| E-Liquid | ||

| By Category | Open Vaping Systems | |

| Closed Vaping Systems | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the current Europe vaping market size?

The Europe vaping market size stood at USD 11.87 billion in 2026 and is projected to reach USD 15.66 billion by 2031.

Which country holds the largest Europe vaping market share?

The United Kingdom leads with 43.23% of regional revenue, thanks to an evidence-based regulatory stance that encourages adult smokers to switch.

Which product segment is expanding fastest?

E-liquids are growing at a 5.22% CAGR, driven by the transition from disposables to refillable systems and rising demand for customized flavors.

Who are the leading companies in the Europe vaping industry?

British American Tobacco, Philip Morris International, and Imperial Brands dominate, while technology-focused players such as RELX compete on innovation and manufacturing scale.

Page last updated on: