Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

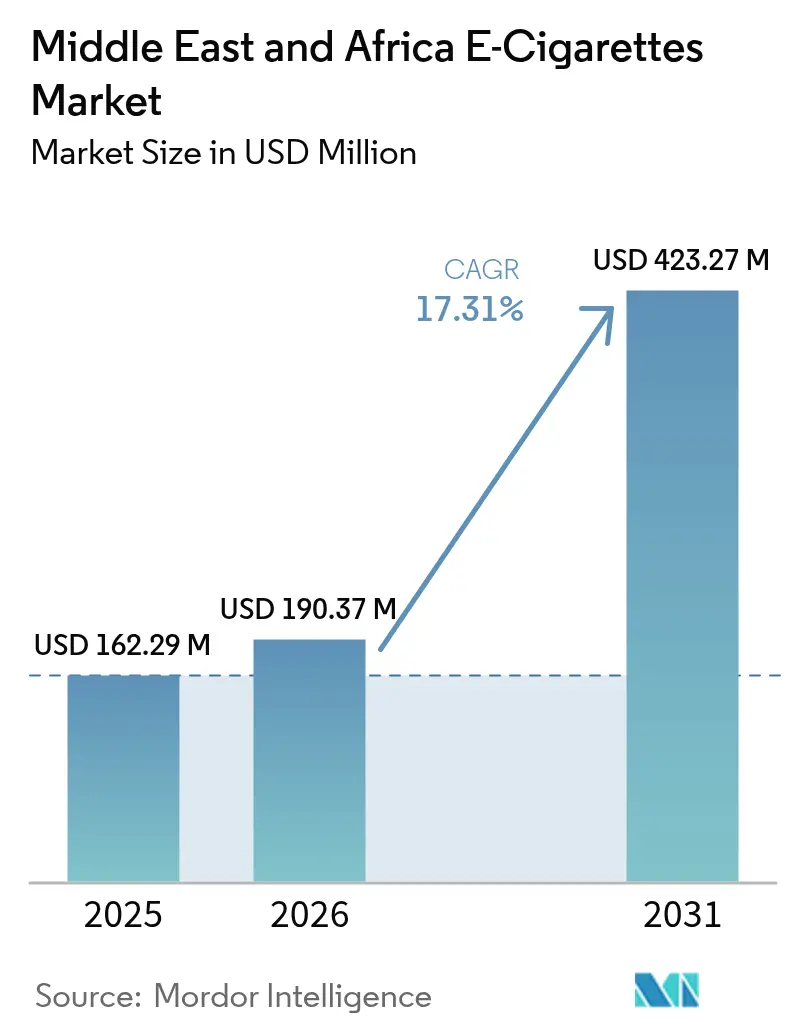

| Base Year Market Size (2025) | USD 162.29 Million |

| Market Size (2026) | USD 190.37 Million |

| Market Size (2031) | USD 423.27 Million |

| Growth Rate (2026 - 2031) | 17.31% CAGR |

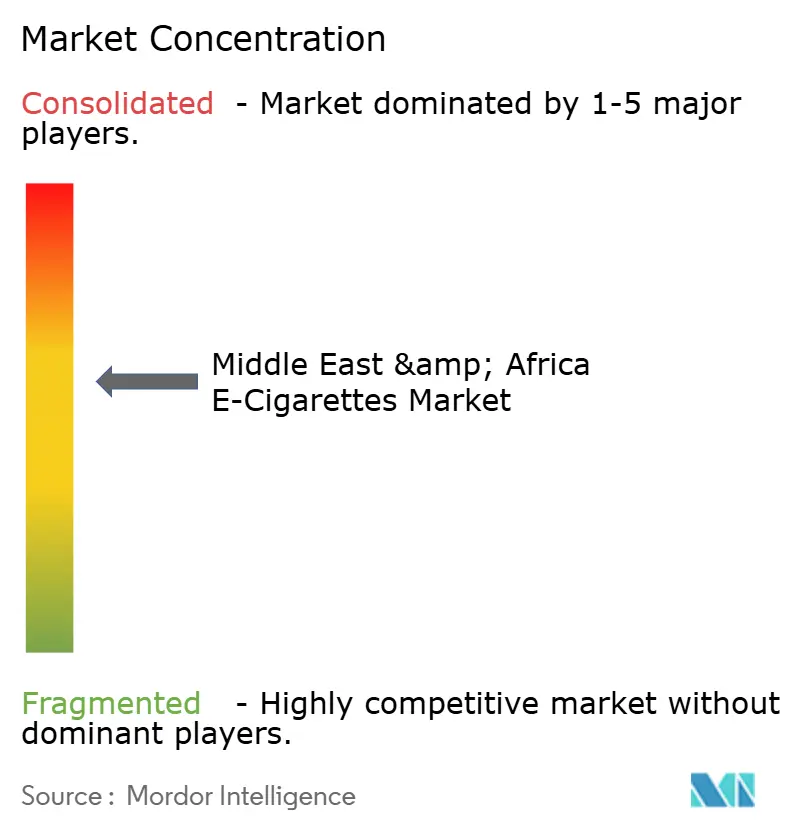

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa E-Cigarettes Market Analysis by Mordor Intelligence

The Middle East and Africa e-cigarette market size is expected to grow from USD 162.29 million in 2025 to USD 190.37 million in 2026 and is forecast to reach USD 423.27 million by 2031 at 17.31% CAGR over 2026-2031. Driven by diverse tobacco-control policies, heightened health awareness, and a pivot to lower-risk nicotine products, the region witnesses a robust double-digit growth. In the Gulf Cooperation Council (GCC) countries, clear regulations, swift flavor innovations, and the allure of high-puff disposables draw in new adult users. Meanwhile, premium product positioning aids in counterbalancing significant excise taxes. Across Africa, however, the landscape is more fragmented. Stricter enforcement on youth access and growing environmental concerns over single-use devices are reshaping strategies for both global and regional players. Companies that swiftly adapt to compliance, innovate in sustainable design, and boast a broad distribution reach stand to gain in this evolving market.

Key Report Takeaways

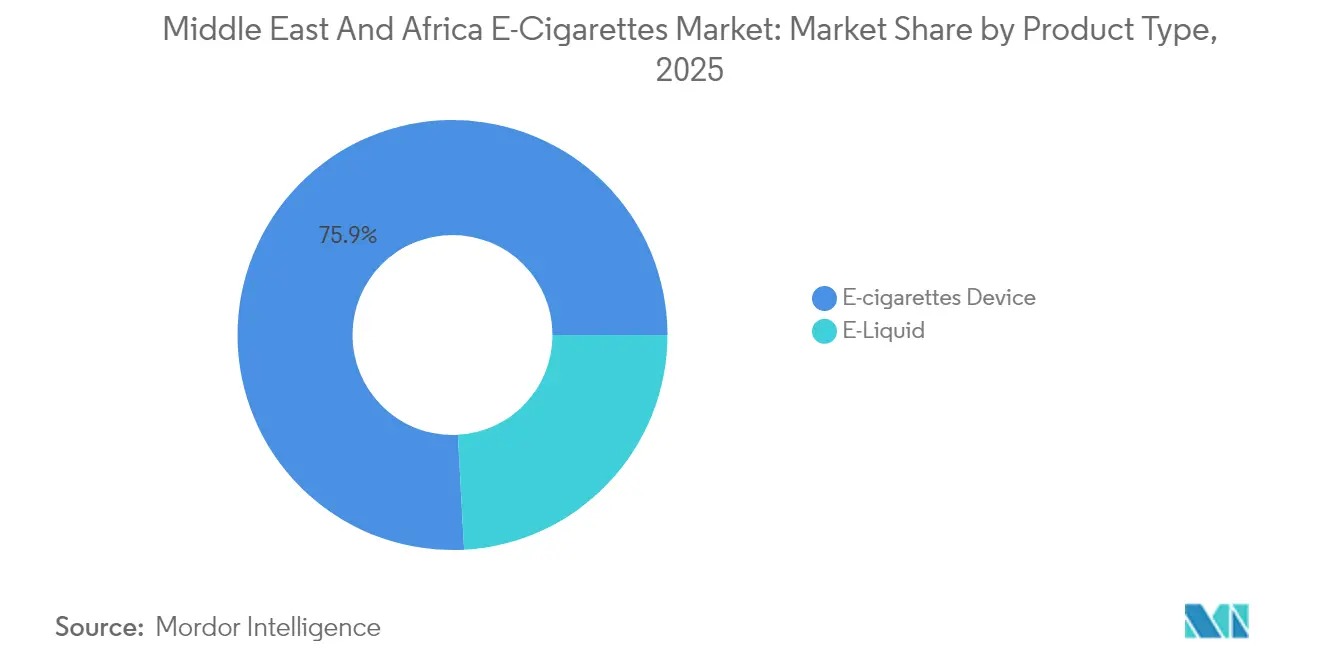

- By product type, devices captured 75.86% of the Middle East and Africa e-cigarette market size in 2025; e-liquids are projected to grow at an 18.26% CAGR through 2031.

- By category, closed systems accounted for 68.10% share of the Middle East and Africa e-cigarette market size in 2025, whereas open systems are expected to advance at an 18.56% CAGR through 2031.

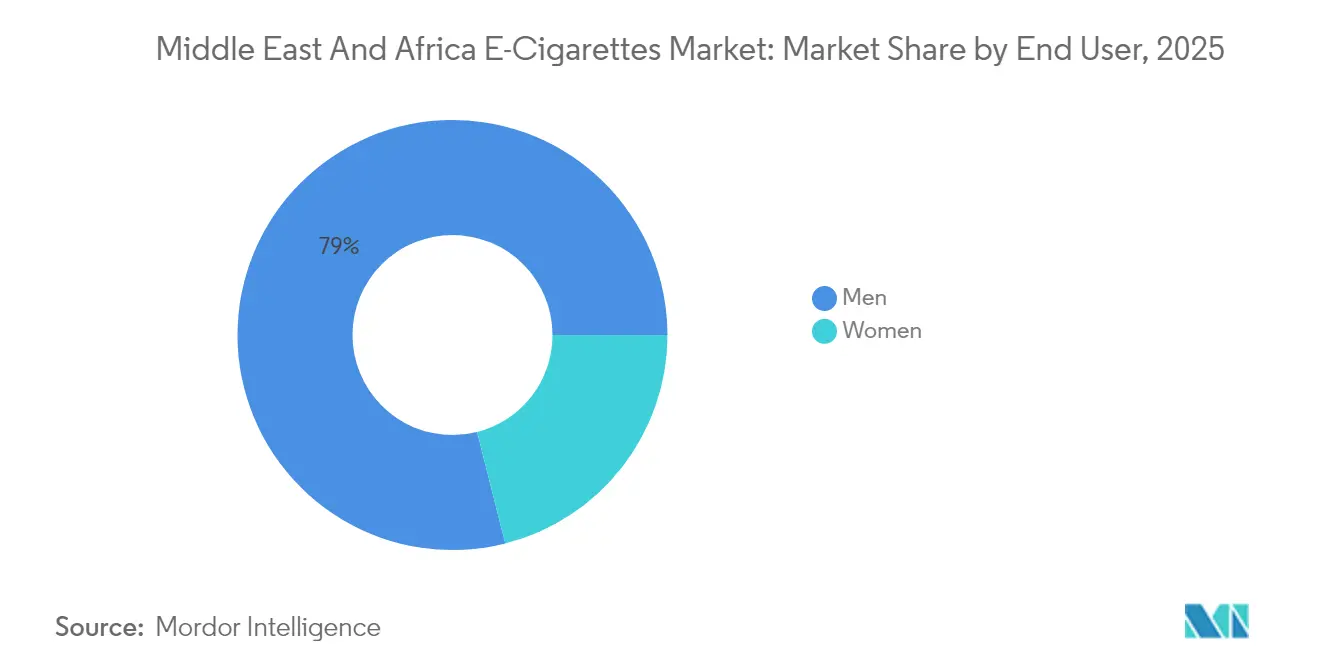

- By end user, men commanded 78.95% share of the Middle East and Africa e-cigarette market size in 2025; women represent the fastest-growing segment with an expected 17.54% CAGR through 2031.

- By distribution channel, offline stores held a 61.82% revenue share in 2025, and online outlets are forecasted to grow at a 19.35% CAGR through 2031.

- By geography, the United Arab Emirates led the Middle East and Africa e-cigarette market with 28.64% of the market share in 2025, while Saudi Arabia is projected to expand at a 18.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa E-Cigarettes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-puff disposable vapes | +3.2% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Growing health consciousness and cessation | +2.8% | GCC focus, expanding to Africa | Medium term (2-4 years) |

| Youth-oriented flavor innovation | +2.1% | Saudi Arabia, UAE, Turkey | Short term (≤ 2 years) |

| Customizable nicotine levels | +1.7% | UAE, South Africa, Morocco | Medium term (2-4 years) |

| Convenience and user-friendly design | +1.4% | Urban centers region-wide | Long term (≥ 4 years) |

| Manufacturing technology advances | +0.9% | UAE, South Africa hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid shift toward high-puff disposable vapes

In the Middle East and Africa, the e-cigarette market is witnessing a surge in the adoption of high-puff disposable devices. This shift is not only altering consumer behavior but also changing distribution strategies. As manufacturers navigate this trend, they're feeling the pinch in their supply chains. They grapple with the need to balance production capacity against the backdrop of regulatory compliance. This is especially pronounced in markets like Egypt, where a 14% VAT, specifically targeting disposable e-cigarettes, adds another layer of complexity, as highlighted by OKK Vapes. However, the pivot towards disposable e-cigarettes isn't without its challenges. These devices produce a notably higher waste output per nicotine delivery unit than their refillable counterparts, raising significant environmental concerns. In response, industry players are pivoting towards biodegradable materials and are championing recycling programs. Yet, they are keen on preserving the convenience that has fueled the rapid consumer adoption of these products. Adding to the complexities, the Emirates Authority for Standardisation and Metrology mandates thorough product certification for these disposable devices. This requirement acts as a gatekeeper, creating hurdles that predominantly benefit established players, armed with both regulatory know-how and the necessary financial clout.

Growing health consciousness and smoking cessation

In the Middle East and Africa, health consciousness is driving the market, with many consumers viewing e-cigarettes as tools for harm reduction, despite mixed scientific evidence and regulatory warnings. Data from the WHO's Eastern Mediterranean Regional Office indicate that in 2022, 92.5 million adults, or 19% of the region's population, used tobacco products. This statistic underscores a significant market for cessation products, as highlighted by the World Health Organization[1]Source: World Health Organization, “Tobacco: E-cigarettes – Q&A,” who.int. Yet, research from sub-Saharan Africa contests the harm reduction narrative. It suggests that, due to limited healthcare infrastructure and patterns of dual use, e-cigarettes may not be effective cessation tools and could even heighten overall nicotine dependence, as reported by Tobacco Control. In December 2023, the Saudi Public Investment Fund launched Badael Company and its DZRT brand, signaling institutional acknowledgment of the cessation market's potential. By positioning nicotine alternatives as public health instruments rather than mere recreational items, they open up marketing avenues. However, this approach demands meticulous adherence to medical claims regulations and the WHO's Tobacco Control guidelines, which stress the importance of safeguarding public health policy from industry sway.

Youth-oriented flavour innovation driving trial

In the Middle East and Africa, flavor innovation aimed at younger audiences is driving notable trial rates, even as regulators strive to limit youth access and the availability of certain flavors. According to the Global State of Tobacco Harm Reduction, there are over 16,000 flavors worldwide, with the World Health Organization noting that fruit and sweet profiles are particularly favored in the region. Yet, as flavor accessibility comes under scrutiny, GCC member states are enacting regulations that prohibit specific named additives, including certain flavoring agents, as highlighted by Tobacco Control. This regulatory landscape opens avenues for flavor accessories and enhancement products that sidestep direct flavor bans yet still resonate with consumers. Manufacturers face the dual challenge of pushing flavor innovation while adhering to compliance mandates, all the while steering clear of marketing strategies that might attract further regulatory scrutiny.

Customizable nicotine levels

Customizable nicotine delivery systems are driving the market, catering to both consumers aiming to quit and those seeking a tailored experience. Regulations in the UAE cap e-liquid nicotine concentrations at 20 mg/ml. This sets the stage for gradual nicotine reduction programs, ensuring products remain appealing, as highlighted by Hangsen International Group`[2]Source: Emirates Authority for Standardisation and Metrology, “UAE Technical Regulations for Electronic Nicotine Delivery Systems,” hangsen.com. Such regulations empower manufacturers to craft product lines that aid in cessation through controlled nicotine tapering, a significant advancement over traditional tobacco products. Philip Morris International's launch of the IQOS ILUMA i underscores this trend, showcasing FlexPuff systems that let users dictate their nicotine intake per session. The push for customization isn't limited to nicotine levels; it spans device features like temperature control, battery optimization, and smartphone connectivity, all amplifying user control. As a result, market players are ramping up R&D investments, aiming to design advanced delivery systems that cater to varied consumer tastes while adhering to regulations across different regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and operational costs | -2.4% | UAE, South Africa | Medium term (2-4 years) |

| Anti-disposable environmental campaigns | -1.8% | Advanced GCC markets | Long term (≥ 4 years) |

| Age and access restrictions | -1.5% | Regional, enforcement uneven | Short term (≤ 2 years) |

| Stringent and fragmented regulations | -2.1% | Turkey ban, varying African policies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production and operational costs

Market expansion in the Middle East and Africa faces significant constraints due to manufacturing and operational cost pressures, with smaller players and new entrants feeling the brunt. In the UAE, regulatory mandates require thorough product testing at ISO/IEC 17025 accredited labs. Conformity certification fees, as highlighted by Hangsen International Group, amount to AED 1,760 (USD 480) per SKU. This is in addition to costs for RoHS compliance and annual renewals. These compliance costs are further exacerbated by excise taxes. Notably, GCC countries levy a hefty 100% excise tax on electronic smoking devices, on top of standard VAT rates that vary between 5% and 15%. International manufacturers grapple with rising operational costs and complex inventory management, especially after disruptions like the Red Sea shipping delays in the first half of 2024. Such cost challenges hit price-sensitive consumers the hardest, curtailing market penetration in lower-income groups. However, this scenario opens doors for local manufacturers, who, due to their proximity to key markets and lighter regulatory burdens, can carve out cost advantages.

Growing anti-disposable environmental campaigns

As the disposable e-cigarette segment fuels much of the region's market growth, it faces mounting challenges from environmental sustainability concerns. This creates a tug-of-war between consumer convenience and ecological responsibility. The WHO Framework Convention on Tobacco Control, underscoring the importance of environmental protection, is increasingly spotlighting the environmental lifecycle impacts of nicotine delivery systems. Notably, disposable vapes produce far more electronic waste per nicotine unit than their refillable counterparts. This disparity has led to heightened regulatory pressures, advocating for extended producer responsibility programs and stringent waste management protocols. In response to these environmental challenges, Imperial Brands, recognizing sustainability as a cornerstone of consumer health, is integrating renewable energy-sourced aluminum and recycled materials into its device components. While these innovations present lucrative market opportunities for manufacturers to pioneer biodegradable or highly recyclable products, they often come with a premium price tag, potentially hindering widespread market adoption. Furthermore, potential regulatory measures addressing these environmental concerns could reshape market dynamics and influence consumer behaviors. Such measures might encompass deposit systems, mandatory recycling initiatives, or even curbs on single-use devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Device Dominance Drives Market Structure

In 2025, e-cigarette devices captured a commanding 75.86% share of the market, underscoring a consumer tilt towards integrated hardware solutions. This trend is further bolstered by regulatory frameworks, particularly in the UAE, where the Emirates Authority for Standardisation and Metrology mandates distinct conformity certificates for both hardware and e-liquids. Such regulations bestow a competitive edge upon manufacturers adept at bundling compliance across these categories, a sentiment echoed by Hangsen International Group. Within the e-cigarette realm, disposable devices reign supreme, largely due to their convenience and allure to younger demographics. Yet, a 14% VAT in Egypt, specifically targeting these disposables, hints at potential market recalibrations, as noted by OKK Vapes. Meanwhile, non-disposable devices are carving out a niche, appealing to both budget-conscious consumers and environmental advocates. This shift is further fueled by technological advancements, like the induction heating and smartphone connectivity features of Philip Morris International's IQOS ILUMA i.

E-liquids are on a rapid ascent, boasting an 18.26% CAGR projected through 2031. This surge is largely attributed to innovative flavors and customizable nicotine levels that resonate with a broad spectrum of consumers. Regulatory frameworks, such as the UAE's adherence to European Pharmacopoeia standards and GSO flavor regulations, bolster the segment by ensuring quality benchmarks, as highlighted by Hangsen International Group. Yet, challenges loom. Flavor restrictions in GCC states, which prohibit specific named additives, not only complicate the market landscape but also amplify the demand for flavor accessories. These accessories cleverly sidestep direct restrictions while still captivating consumers. Additionally, the e-liquid segment's growth trajectory is tempered by regulations on container sizes — with the UAE capping tanks at 10ml and refill packages at 50ml — a limitation that significantly shapes packaging strategies and consumer buying behaviors.

By Category: Closed Systems Lead Despite Open System Growth

In 2025, closed vaping systems commanded a dominant 68.10% market share, underscoring a clear consumer preference for their simplicity and the manufacturers' comprehensive control over the user experience. These systems not only cater to consumer desires but also align with regulatory mandates, ensuring controlled nicotine delivery and minimizing the risk of tampering. This alignment is crucial for adhering to stringent nicotine concentration limits, such as the 20 mg/ml cap set in markets like the UAE, as highlighted by Hangsen International Group. Furthermore, closed systems bolster brand loyalty through their proprietary cartridge ecosystems. However, this strategy is under the regulatory microscope, raising questions about consumer choice and market competition. Technological advancements, such as authentication systems, play a pivotal role in this segment, preventing counterfeit cartridge usage and ensuring quality control throughout the user's journey.

Open vaping systems are rapidly gaining traction, boasting an impressive 18.56% CAGR projected through 2031. Their appeal lies in catering to enthusiasts who crave customization and cost savings through refillable designs. These systems resonate with seasoned users, emphasizing flavor diversity and precise nicotine strength control. This is further validated by the World Health Organization's data, showcasing a global palette of over 16,000 flavor options. However, open systems navigate a labyrinth of regulatory challenges, grappling with fluctuating nicotine concentrations and the intricacies of third-party e-liquid compatibility. This complexity underscores the need for robust compliance frameworks to guarantee product safety and quality. The segment's growth hinges on two pivotal factors: regulatory endorsement of user-customizable systems and the establishment of safety standards that mitigate misuse risks while championing consumer choice.

By End User: Male Dominance with Female Growth Acceleration

In 2025, men commanded a dominant 78.95% share of the market, a trend deeply rooted in traditional tobacco consumption and cultural nuances across the Middle East and Africa. This male predominance resonates with data from the WHO's Eastern Mediterranean Regional Office, which highlights a pronounced tobacco prevalence among men. Such insights underscore a significant market potential for harm reduction products, as noted by the World Health Organization. Male consumers are gravitating towards high-nicotine, tobacco-flavored products, mirroring traditional smoking experiences. This preference is bolstering the market for closed systems and disposable devices. Furthermore, established distribution channels via traditional tobacco retail networks, coupled with male-centric marketing that underscores performance and convenience, are amplifying this segment's growth.

Women, on the other hand, are emerging as the segment with the most rapid growth, boasting a 17.54% CAGR projected through 2031. This surge is largely attributed to heightened health consciousness and flavor innovations that resonate with female tastes. Such a trajectory not only mirrors shifting tobacco consumption patterns but also aligns with WHO findings of increasing tobacco use among adolescent girls in Africa. Female consumers are leaning towards products with lower nicotine levels, favoring fruit and dessert flavors, and opting for discreet device designs that enhance social acceptability. While the segment's growth is met with cultural and regulatory hurdles in conservative markets, the rising participation of women in the workforce and evolving social norms present ripe opportunities for tailored product development and marketing initiatives.

By Distribution Channel: Offline Dominance with Digital Acceleration

In 2025, offline stores held a 61.82% market share, underscoring consumer preference for hands-on product examination and immediate availability, particularly in regions where e-commerce is still in its early stages of development. Traditional tobacco retail networks not only offer established distribution channels for market entry but also play a pivotal role in consumer education. However, these networks face regulatory pressures, particularly regarding age verification and product display. For instance, in the UAE, retailers are required to prominently display age restriction signage and verify customers' ages before making e-cigarette sales. This regulatory landscape creates compliance challenges, inadvertently favoring established retail chains over their independent counterparts. Moreover, offline distribution capitalizes on impulse buying and offers immediate customer support and product education, a crucial aspect for consumers shifting from traditional tobacco products.

Online stores, on the other hand, are the rising stars, boasting a robust 19.35% CAGR. Their growth is fueled by the allure of convenience, a diverse product range, and advanced age verification technologies that ensure adherence to regulations. These digital platforms empower manufacturers, allowing them to connect with consumers in areas where physical retail presence is sparse. They also offer comprehensive product information, aiding consumers in making informed choices. Yet, this growth isn't without hurdles. Regulatory challenges loom, especially concerning cross-border sales and tax compliance. Markets like the GCC present unique challenges, with stringent requirements like digital tax stamps and e-invoicing. Furthermore, while online distribution fosters market growth in areas where cultural norms restrict traditional retail, challenges like delivery restrictions and payment processing issues temper this expansion in certain regions.

Geography Analysis

In 2025, the United Arab Emirates (UAE) commanded a dominant 28.64% share of the e-cigarette market in the Middle East and Africa. The UAE has solidified its position as the regional hub, thanks to its comprehensive regulatory frameworks and advanced distribution infrastructure. Since April 2019, the Emirates Authority for Standardisation and Metrology has been at the helm of the UAE's regulatory approach, fostering market certainty. This, in turn, has drawn international investments and spurred product innovation. Highlighting the UAE's strategic significance, Philip Morris International chose Dubai as the base for its regional headquarters, overseeing operations in South and Southeast Asia, the Commonwealth of Independent States, the Middle East, and Africa. The market thrives on the UAE's high disposable incomes, which cushion the impact of a steep 100% excise tax, and a refined retail infrastructure adept at catering to both premium and mass-market strategies.

Saudi Arabia stands out as the region's fastest-growing market, boasting a 18.79% CAGR projected through 2031. This surge is largely attributed to the nation's youth increasingly adopting e-cigarettes and a rising health consciousness among its traditional smokers. The Saudi Public Investment Fund's December 2023 launch of the DZRT nicotine pouch brand, via its newly established Badael Company, underscores institutional backing for harm reduction strategies and hints at a burgeoning domestic market. Yet, challenges loom with regulatory ambiguities surrounding flavor restrictions and controls on youth access, potentially hindacing growth. The market also reaps benefits from the Vision 2030 initiative, which aims to diversify the economy beyond oil and modernize the healthcare sector. Countries like South Africa, Nigeria, Egypt, Morocco, and Turkey present a mixed bag of regulatory landscapes, each offering unique opportunities and hurdles. For instance, while Turkey's blanket e-cigarette bans have spurred an illicit market and muddied official market assessments, high levels of tobacco smuggling hint at a significant underground demand, as noted by Tobacco Prevention & Cessation. In 2024, Egypt introduced a 14% VAT on disposable e-cigarettes, reflecting a nuanced regulatory stance that seeks to balance revenue needs with public health goals, according to OKK Vapes. Meanwhile, Morocco's February 2025 green light for Japan Tobacco International's production facilities signals a warming market climate and hints at the potential for local manufacturing growth, as reported by Africa Intelligence. South Africa grapples with regulatory ambiguities; draft legislation, which lapsed before the May 2024 elections, might see a comeback, potentially introducing plain packaging mandates and advertising curbs, per Chambers Practice Guides. The broader Middle East & Africa region, while marked by regulatory uncertainties, holds promise. As the WHO Framework Convention on Tobacco Control takes root, it paves the way for standardized regulations on novel nicotine products.

Competitive Landscape

The Middle East and Africa e-cigarette market demonstrates moderate concentration with established tobacco multinationals competing against emerging regional players and technology-focused manufacturers. Established tobacco multinationals in the Middle East and Africa e-cigarette market face competition from emerging regional players and tech-focused manufacturers. Philip Morris International, leveraging its IQOS heated tobacco platform and a robust regional infrastructure, reported a 15.6% growth in heated tobacco unit sales in 2024 across the SSEA, CIS & MEA region. Meanwhile, Imperial Brands, with a disciplined approach prioritizing consumer demand and distribution, achieved a staggering 136.4% growth in revenues from next-generation products, aggressively expanding in Africa, Asia, Australasia, and Central & Eastern Europe.

Companies with regulatory expertise and deep financial pockets are increasingly favored in the competitive landscape, especially when navigating intricate compliance mandates. For instance, the UAE's conformity certification processes demand hefty upfront investments and continuous renewal fees. Markets with shifting regulatory landscapes and neglected consumer segments present white-space opportunities. This is especially true in African nations, where the WHO's tobacco control framework is standardizing nicotine product regulations. The Saudi Public Investment Fund's foray into the market via Badael Company and the DZRT brand underscores institutional confidence in these opportunities, intensifying competition for global players.

Manufacturers are adopting technology integration as a pivotal differentiation strategy. Investments in smartphone connectivity, IoT features, and anti-counterfeiting measures not only elevate user experience but also bolster adherence to regulations. However, the competitive arena is being reshaped by environmental sustainability mandates. These favor manufacturers who can innovate biodegradable or easily recyclable products. Yet, such advancements often come with a premium price tag, restricting their appeal to the broader market.

Middle East And Africa E-Cigarettes Industry Leaders

British American Tobacco

Aspire Global

Philip Morris International

Japan Tobacco International

Imperial Brands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Japan Tobacco International received authorization to commence cigarette production operations in Morocco, enabling direct competition with incumbent Imperial Brands' Société Marocaine des Tabacs and establishing local manufacturing capabilities that could extend to next generation products.

- December 2023: Saudi Arabia's Badael Company, founded by the Public Investment Fund, launched the DZRT brand of nicotine pouches and e-cigarette alternatives, positioning the products as harm reduction tools with availability through online channels and selected retail outlets.

Middle East And Africa E-Cigarettes Market Report Scope

E-cigarettes are sometimes called "e-cigs," "vapes," "e-hookahs," "vape pens," and "electronic nicotine delivery systems (ENDS). E-cigarettes are also called vaping devices. They could contain e-liquids and a miscellaneous group of devices that allow users to inhale an aerosol containing nicotine, flavorings, and other spices. Various flavors, including mint, menthol, chocolate, cola, bubble gum, and fusions of other fruits, as well as flavoring ingredients, are attracting many consumers to adopt them. The Middle East and Africa E-cigarette Market is segmented by Product into E-cigarette Devices and E-liquid Devices. Based on the distribution Channel, the market is segmented into offline and online channels. Based on Geography, the market is segmented into South Africa, Nigeria, Kenya, Egypt, the United Arab Emirates, and the Rest of the Middle East and Africa. The report offers market size and forecasts for the e-cigarette market in value (USD million) for all the above segments.

By Product Type

| E-cigarettes Device | Disposable E-cigarette |

| Non-Disposable E-cigarette | |

| E-Liquid |

By Category

| Open Vaping Systems |

| Closed Vaping Systems |

By End User

| Men |

| Women |

By Distribution Channel

| Offline Stores |

| Online Stores |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East & Africa |

| By Product Type | E-cigarettes Device | Disposable E-cigarette |

| Non-Disposable E-cigarette | ||

| E-Liquid | ||

| By Category | Open Vaping Systems | |

| Closed Vaping Systems | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | Offline Stores | |

| Online Stores | ||

| By Geography | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East & Africa |

Key Questions Answered in the Report

How big is the Middle East & Africa E-Cigarettes Market in 2026?

The market stands at USD 190.37 million in 2026 and is set to exceed USD 423.27 million by 2031

Which country leads regional sales in 2025?

The United Arab Emirates held 28.64% of 2025 revenue, supported by clear regulations and high spending power.

What product format is most popular today in 2025?

Closed-pod disposable devices dominate, accounting for 68.10% of 2025 market value.

What growth rate is expected for online sales through 2031?

Online channels are forecast to expand at 19.35% CAGR through 2031 as ID-verified e-commerce gains trust.

Which segment is growing fastest by end user through 2031?

Sales to women are projected to rise at a 17.54% CAGR, outpacing the overall market.

Page last updated on: