Professional and Commercial Services

12th MayDriving Growth in Hong Kong’s Auditing & Accounting Market

4 Min Read

The Newspaper Industry is Segmented by Platform (Print and Digital), Business Model (Advertising Revenue, Subscription / Circulation Revenue, and Others), and Publication Frequency (Daily, Weekly, and More), Format (Broadsheet, Tabloid, Berliner), Language (English, Chinese and More), Distribution Channel (Home Delivery, Newsstands / Retail, and More), End-User Sector – Advertisers (Retail & FMCG, BFSI, and More), Geography.

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

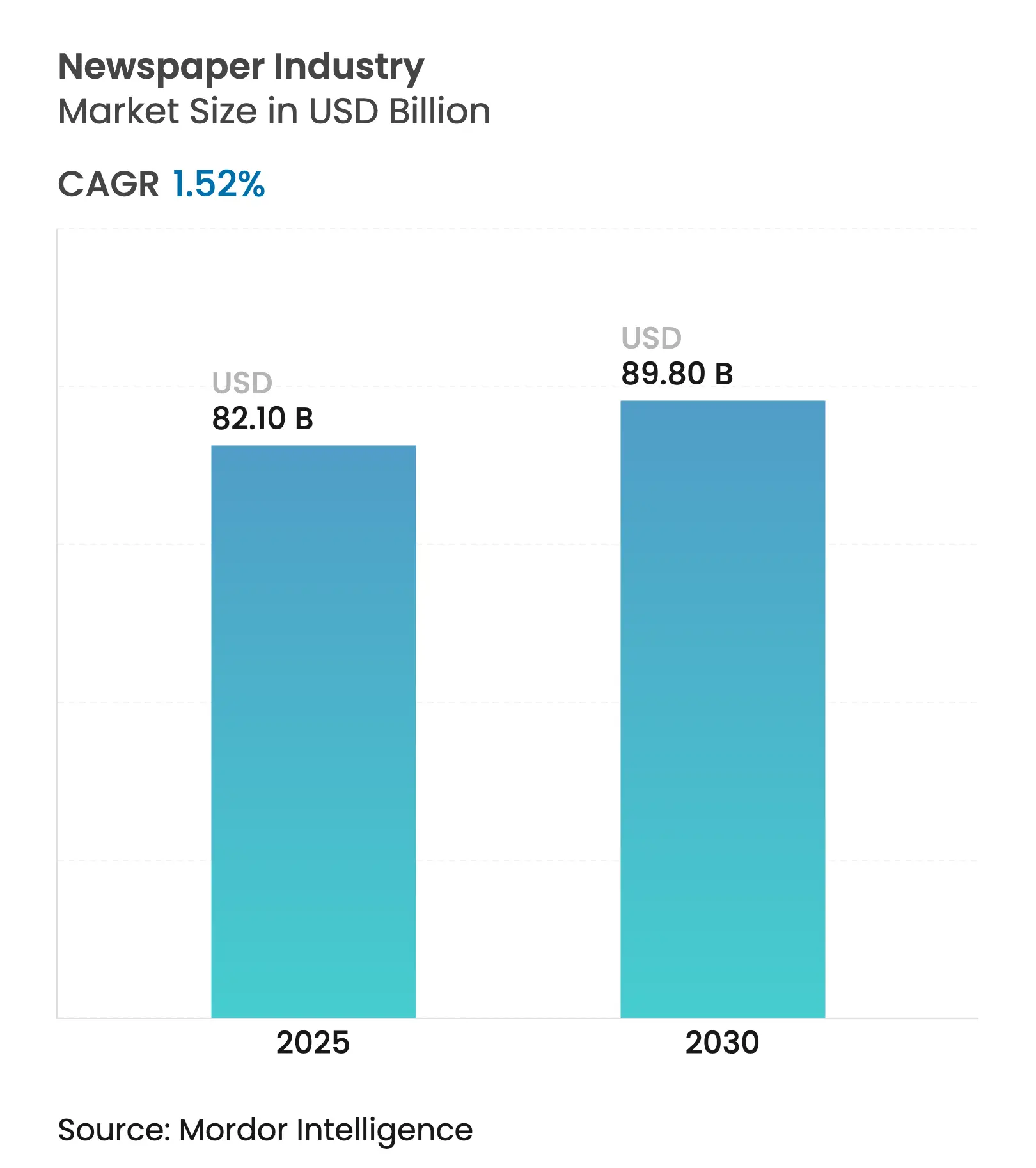

| Market Size (2025) | USD 82.10 Billion |

| Market Size (2030) | USD 89.80 Billion |

| Growth Rate (2025 - 2030) | 1.52 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The newspaper Industry size stood at USD 82.17 billion in 2025 and is forecast to reach USD 89.85 billion by 2030, reflecting a 1.52% CAGR for the period. Demand stabilizes because print editions still command 83% of revenue while digital subscriptions rise fastest, supported by improving paywall conversion and mobile news habits. Advertisers continue to allocate 56% of total spending to print and digital newspaper pages, yet reader revenue grows faster as publishers shift toward predictable cash flows. Global smartphone adoption, especially across Asia-Pacific, expands reach and underpins the strongest growth geography. Consolidation remains moderate: the five largest companies held only 12% of 2024 revenue, so competitive intensity stays manageable and allows regional publishers to survive.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge

in Digital Subscription Revenue Fueled by Successful Paywall Strategies

Surge

in Digital Subscription Revenue Fueled by Successful Paywall Strategies

| + 0.2% | Global, with strongest impact in North America and Western Europe | Medium term (2-4 years) | (~) %

Impact on CAGR Forecast:+ 0.2% |

Geographic

Relevance

:

Global,

with strongest impact in North America and Western Europe

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Rapid

Smartphone Penetration Expanding Readership in Tier-2 & Tier-3 Cities

Across Asia-Pacific

Rapid

Smartphone Penetration Expanding Readership in Tier-2 & Tier-3 Cities

Across Asia-Pacific

| + 0.2% | Asia-Pacific, particularly India, China, and Southeast Asia | Medium term (2-4 years) | |||

Hyper-local

Advertising Demand Boosting Community Newspapers

Hyper-local

Advertising Demand Boosting Community Newspapers

| + 0.1% | North America, Europe, and emerging markets in Asia | Short term (≤ 2 years) | |||

Print

Newspaper Credibility Advantage Driving Premium B2B Advertising in

Financial Dailies

Print

Newspaper Credibility Advantage Driving Premium B2B Advertising in

Financial Dailies

| + 0.2% | Global, with concentration in financial centers | Short term (≤ 2 years) | |||

Government

Subsidies & VAT Exemptions Sustaining Print Circulation

Government

Subsidies & VAT Exemptions Sustaining Print Circulation

| + 0.2% | Europe, parts of Asia, and select North American regions | Medium term (2-4 years) | |||

AI-Driven

Newsroom Automation Lowering Operational Costs & Enabling Real-time

Content Delivery

AI-Driven

Newsroom Automation Lowering Operational Costs & Enabling Real-time

Content Delivery

| + 0.3% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in Digital Subscription Revenue Fueled by Successful Paywall Strategies

Publishers increasingly rely on flexible paywalls that release enough content to hook casual readers then lock specialized coverage behind a subscription page. Readers value investigative journalism, exclusive analysis, and expert commentary, so conversion rates keep climbing. Direct reader relationships also yield richer first-party data that improves targeting and retention. This revenue stream buffers the newspaper market against volatile ad cycles because recurring payments improve cash-flow visibility. The strategy is most advanced in North America and Western Europe where consumers already spend heavily on digital media.

Rapid Smartphone Penetration Expanding Readership in Tier-2 & Tier-3 Cities Across Asia-Pacific

Affordable Android handsets combined with expanding 4G/5G networks pull millions of new users online for the first time. Rising literacy and aspirational middle-class demand intensify appetite for credible news content, helping publishers leapfrog legacy logistics and reach remote readers at minimal marginal cost. Tailored language editions and lighter-weight app designs improve engagement. For the newspaper market, these new audiences represent incremental growth rather than substitution because print penetration in many of these districts was historically low.

Hyper-local Advertising Demand Boosting Community Newspapers

Small and medium enterprises now seek neighborhood-specific reach that broad digital platforms struggle to deliver, so community titles reclaim relevance. Print inserts and bundled digital–print packages allow precise postcode or township targeting. Local readers tend to trust long-standing community publications, creating a premium environment for advertisers in sectors such as retail, real estate, and professional services. Revenue from classifieds and service directories rebounds as publishers refine CRM databases to prove campaign performance.

Investment banks, asset managers, and corporate advisers still favor the gravitas of reputable print titles that reach decision-makers in boardrooms and trading floors. The tactile permanence of a printed page coupled with fact-checked reporting underpins brand safety. As a result, full-page or multi-page spreads in leading financial dailies command premium rates that offset shrinking run volumes. This adds resilience to the newspaper market in cities such as New York, London, Singapore, and Frankfurt.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating Newsprint Costs Due to Supply-Chain Disruptions & Carbon-Pricing Escalating Newsprint Costs Due to Supply-Chain Disruptions & Carbon-Pricing | -0.2% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) | (~) %

Impact on CAGR Forecast:-0.2% |

Geographic

Relevance

:Global, with highest impact in North America and Europe |

Impact

Timeline

:Short term (≤ 2 years) |

Revenue Cannibalization from Social Platforms Capturing 70%+ of Digital Ad Spend Revenue Cannibalization from Social Platforms Capturing 70%+ of Digital Ad Spend | -0.2% | Global, with highest impact in mature digital markets | Medium term (2-4 years) | |||

Declining Reader Trust & News Avoidance Among Gen-Z Audiences Globally Declining Reader Trust & News Avoidance Among Gen-Z Audiences Globally | -0.2% | Global, with pronounced effect in Western markets | Long term (≥ 4 years) | |||

Consolidation of Retail Distribution Channels Increasing Last-Mile Costs for Print Consolidation of Retail Distribution Channels Increasing Last-Mile Costs for Print | -0.1% | North America, Europe, and developed Asian markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Newsprint Costs Due to Supply-Chain Disruptions & Carbon Pricing

Industrial paper production faces tightened capacity after mill closures and stricter environmental policies. Energy-intensive processes mean carbon taxes inflate input costs while shipping bottlenecks raise freight rates. Because paper can account for up to 30% of a publisher’s operating budget, cost spikes erode print margins, especially for regional titles without scale economies. Many publishers respond by trimming page counts or accelerating digital migration, yet smaller rural papers risk closure, which would shrink overall reach of the newspaper market.

Revenue Cannibalization from Social Platforms Capturing 70%+ of Digital Ad Spend

Google, Meta, and emerging short-form video apps combine user-level data tracking, automated buying, and global scale, diverting spend once destined for newspaper inventory. Publishers experience a decoupling between traffic growth and ad yield because the platforms collect the bulk of revenue on referral clicks. Dependency on algorithmic distribution also increases volatility and undermines bargaining power. Without stronger alternative monetization or negotiated data-sharing frameworks, the newspaper market faces a structural headwind on its traditional two-sided model.

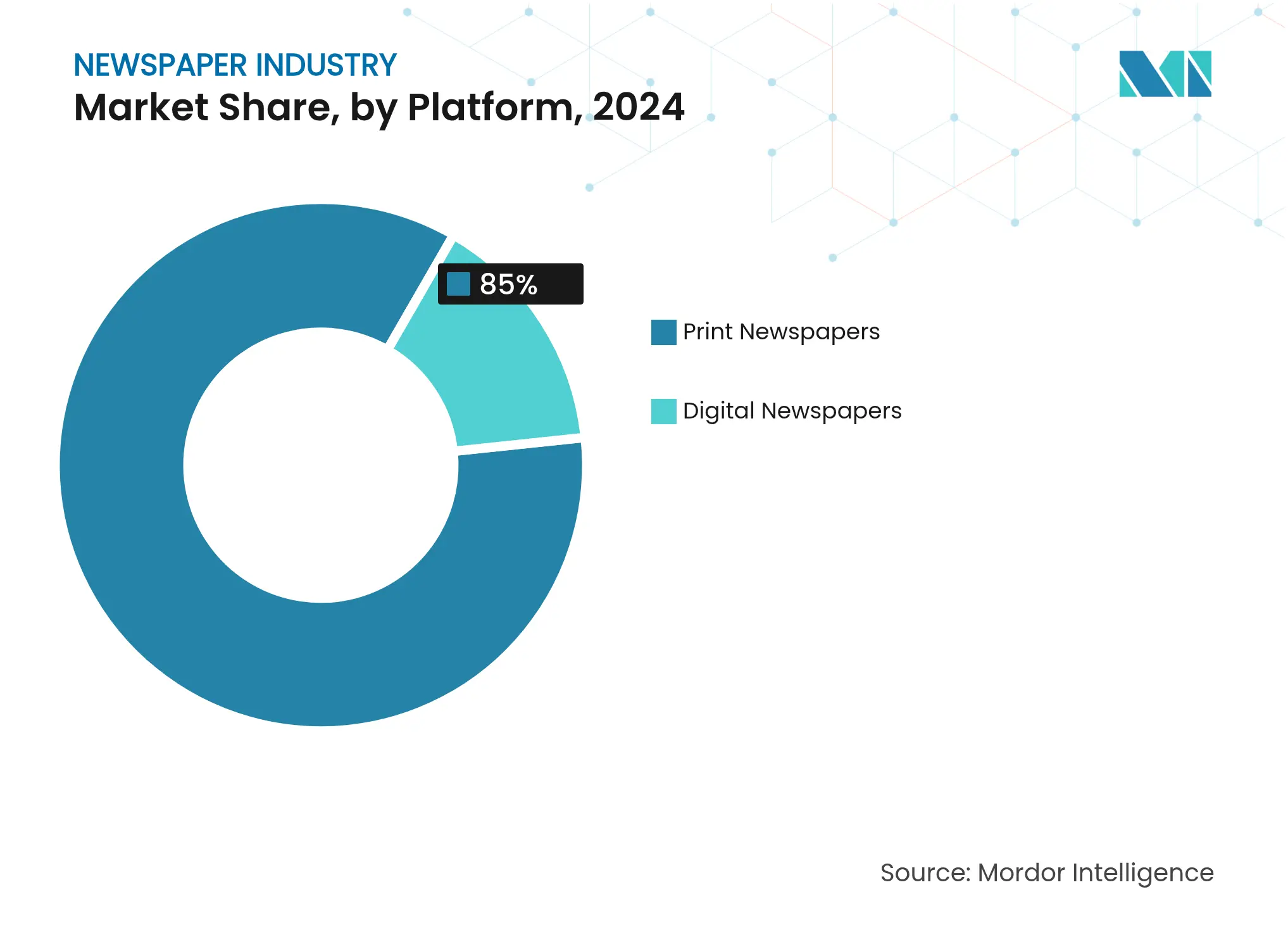

By Platform: Persistent Print Leadership Amid Digital Acceleration

Print continues to deliver 85% of 2025 revenue within the newspaper market and remains profitable in regions where daily rituals and credible commentary sustain loyalty. Readership among seniors and commuters underpins high average spend per copy, and advertisers still value the brand-safe environment. The format’s tactile experience, more relaxed reading pace, and absence of push notifications maintain differentiation from screen-based media.

By Business Model: Reader Revenue Outpaces Advertising Dependence

Advertising retained a 56% contribution to 2025 turnover but slowed due to structural migration toward platform-controlled ecosystems. Cross-media packages that mix print display, digital banners, and sponsored content remain integral for categories like autos and finance. High-impact placements around investigative exclusives boost brand recall and maintain premium CPMs, ensuring the newspaper market still monetizes attention effectively.

Subscriptions and single-copy circulation now expand faster, posting a 1.6% CAGR as consumers place greater value on reliable, ad-light content. Dynamic metered paywalls, tiered article allowances, and membership perks such as podcasts or events push average revenue per user higher. Enhanced analytics enable precise churn predictions and personalized win-back offers. This pivot to a reader-centric model stabilizes cash flows and reduces exposure to macro advertising cycles.

By Publication Frequency: Daily Editions Retain Scale, Weeklies Advance on Depth

Daily papers preserved a 71.5% slice of 2025 revenue because they fulfill the public’s appetite for continuous updates and serve as a ritual for morning commutes. Their tight production cadence supports real-time coverage that drives website sessions and keeps print subscribers engaged. High insertion frequency sustains advertiser demand for recurring exposure within the newspaper market.

Weekly editions accelerate at a 1.5% CAGR as cost pressures push small-town publishers toward fewer print days. These editions balance in-depth features, lifestyle pages, and investigative series that benefit from longer lead times. Weekend bundles integrate crossword booklets and magazine supplements, improving per-copy yields. The slower rhythm also aligns with consumers seeking reflective analysis that complements instant digital alerts.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

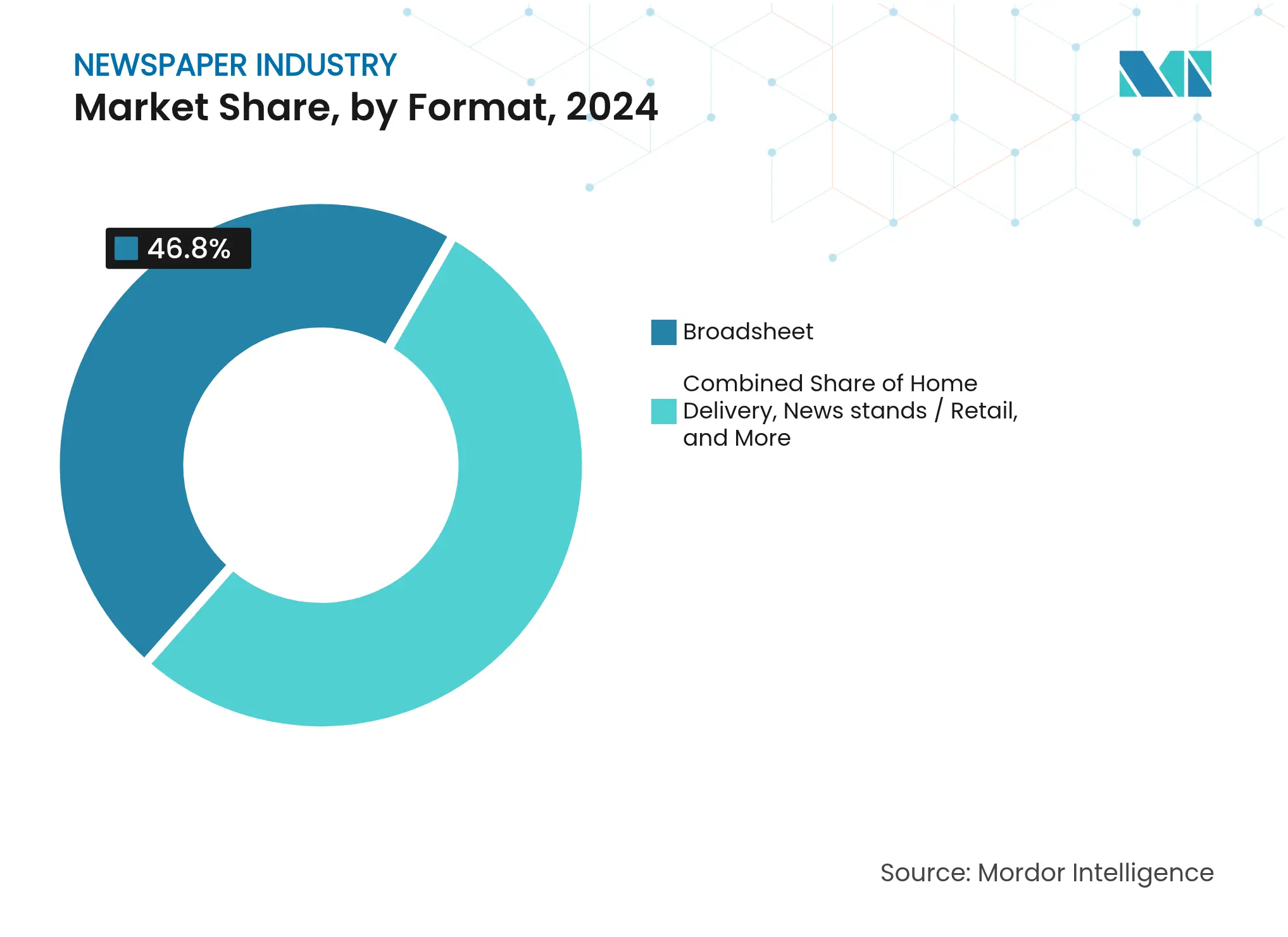

By Format: Broadsheet Stability Meets Tabloid Convenience

Broadsheets held 46.8% of 2025 revenue and remain the reference point for quality dailies and global business coverage. The expansive layout accommodates complex infographics, large photos, and nuanced op-eds, underpinning perceived authority. Corporate advertisers endorse the format for thought-leadership placements, sustaining a premium within the newspaper market size hierarchy.

Tabloids grow at a 1.7% CAGR by offering commuter-friendly dimensions and lower paper costs. Compact folds fit public-transport seating and integrate seamlessly with retail checkout racks. Modern tabloids increasingly balance sensational front pages with credible reporting, broadening appeal. Economically, the reduced newsprint consumption mitigates inflation risk and improves contribution margins at moderate print runs.

By Distribution Channel: Direct Delivery Dominates, Apps Take Flight

Home delivery remained the foremost route with 55.3% of 2025 distribution value. Subscription management systems, early-morning logistics, and loyalty benefits such as vouchers or event invitations reinforce retention. The channel fosters strong brand intimacy, making it hard for aggregators to disintermediate publisher-to-reader relationships within the newspaper market.

Online portals and mobile apps are the runaway growth leaders, advancing at a 2.3% CAGR. Push notifications, adaptive article formats, and one-click payments underpin rising engagement. Real-time analytics inform editors which headlines resonate, refining topical focus. Publishers deploy progressive web apps for low-bandwidth markets, while native apps integrate audio briefings and personalized newsletters, creating daily touchpoints that build habit.

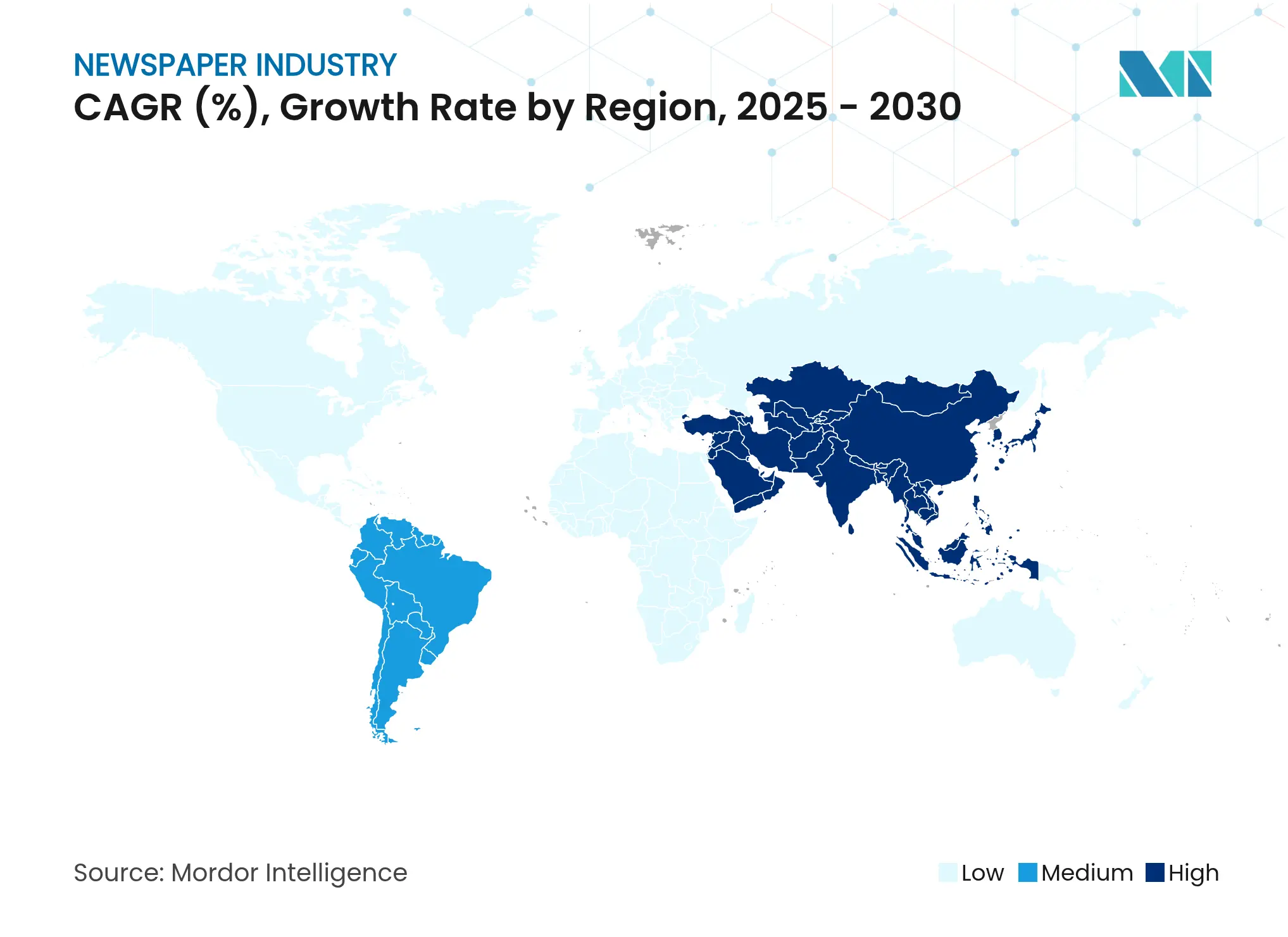

North America generated 36.8% of 2025 revenue, representing the largest share of the newspaper market. Consumer willingness to pay for trusted reportage supports robust subscription stacks that offset soft advertising yields. The New York Times grew digital-only subscribers by 250,000 in Q1 2025, pushing total subscriptions beyond 11.6 million and lifting revenue 7.1% to USD 635.9 million. Consolidation persists: a December 2024 merger between McClatchy and a national magazine publisher created an entity that reaches more than 100 million monthly uniques.

Asia-Pacific is the fastest-growing region with a forecast 1.8% CAGR. Smartphone penetration tops 80% in key urban clusters, enabling leapfrog adoption of digital news. Dentsu projects regional ad spend to rise 5.8% in 2025, outpacing global trends. India’s pulp and paper sector expects a 6.3% capacity CAGR by end-2024, ensuring adequate print supply. GroupM estimates China will secure 51.2% of global DOOH revenue in 2025, creating synergies for publishers investing in outdoor and branded content channels.

Europe shows mixed momentum. The European Commission forecasts 2025 EU GDP growth at 1.1%, edging up to 1.5% by 2026 [1]Source: European Commission, “European Economic Forecast Spring 2025,” ec.europa.eu. Government VAT relief and targeted subsidies temper print erosion, while local M&A heats up: RedBird’s agreement to acquire The Telegraph in May 2025 signals investor confidence in premium titles. Regulatory frameworks around data privacy and platform negotiations shape monetization strategies, nudging publishers toward diversified revenue portfolios.

Market Concentration

News Corp disclosed USD 8.32 billion in fiscal-year 2024 revenue, buoyed by its Digital Real Estate Services and Dow Jones units, even as News Media advertising slipped 3%. Gannett sharpened operational efficiency through centralized printing hubs and AI-assisted page layout, while Axel Springer expanded Politico Europe’s paywall footprint.

Technology deployment differentiates performance. Surveys indicate 70% of newsroom staff now rely on generative AI for headline tests, social snippets, or translation tasks. The Guardian’s adoption of The Trade Desk OpenPath yielded programmatic revenue growth above 25% year-on-year. Legal pushback also shapes strategy: The New York Times filed suit against OpenAI in late 2024 to protect proprietary archives.

Local news niches offer white-space for emergent players. Tamedia runs 27 weekly hyper-local newsletters serving 700 Swiss municipalities, confirming appetite for micro-community engagement [2]Source: IMNA, "International News Media Association",https://www.inma.org/. Meanwhile, digital-native brands leverage low overheads and multimedia storytelling to court under-35 readers who prefer mobile-first formats. Cost pressures, ad-revenue migration, and print logistics encourage further consolidation, yet the dispersed ownership structure preserves plural voices within the global newspaper market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Market Definitions and Key Coverage

Our study defines the global newspaper industry as the combined revenue generated by publishers that create, print, and digitally distribute general-interest daily or weekly newspapers, together with the sale of in-house advertising and circulation packages.

Scope exclusion: Magazines, newsletter services, and book publishing activities sit outside this sizing.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews and short surveys with newsroom executives, regional printer associations, advertising agencies, and distribution partners across North America, Europe, and Asia-Pacific. These conversations confirmed cost structures, realistic average selling prices, and the adoption curve for metered paywalls, plugging gaps left by published statistics.

Desk Research

We first gathered baseline data from open, authoritative outlets such as UNESCO Institute for Statistics, the World Association of News Publishers (WAN-IFRA), Pew Research Center, national statistics offices, and OECD Media Outlook reports. Macroeconomic indicators, print-run disclosures, and household broadband adoption rates provided essential context, while company filings, investor presentations, and trusted news portals clarified publisher revenue splits. Where deeper firm-level detail was required, D&B Hoovers supplied cross-checked financials. The desk findings underpin platform share, pricing bands, and historic demand shifts.

Additional directional signals, such as import-export records for newsprint, postal delivery volumes, and patent filings around automated layout tools, helped verify consumption trends. The sources listed illustrate the type of material referenced; many other public records supported data cleaning and sense-checks.

Market-Sizing & Forecasting

A top-down approach begins with national newspaper revenue totals reconstructed from production and trade data, which are then adjusted for publisher yield and advertising load. Results are corroborated through selective bottom-up checks, such as sampled publisher roll-ups and circulation × ASP comparisons, to fine-tune regional totals. Key variables feeding the model include household print readership rates, digital subscription penetration, ad-page yield, newsprint price volatility, and device ownership trends. Forecasts draw on multivariate regression that aligns these drivers with GDP and demographic projections, before scenario analysis adjusts for policy or technology shocks. Where granular publisher data were incomplete, plausible ranges derived from peer benchmarks bridged the gap.

Data Validation & Update Cycle

Outputs pass a two-step peer review, variance checks against external meters such as WAN-IFRA press-run audits, and anomaly flags in our proprietary dashboards. We refresh each model annually and trigger interim updates when mergers, material price swings, or regulatory changes arise.

Why Mordor's Newspaper Industry Size & Share Analysis Baseline Commands Reliability

Benchmark comparison

Published estimates often diverge because firms select differing product mixes, revenue definitions, and forecast cadences. We openly declare inclusions, exclude magazines, and keep currency conversions locked to IMF yearly averages, ensuring consistency.

Key gap drivers typically stem from bundling magazines with newspapers, assuming uniform cover-price escalation, or projecting either highly pessimistic print decline or an overly aggressive digital surge without regional nuance. Our balanced mix of print and digital cohorts, plus annual refreshes, reduces such drift.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 82.17 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 90.00 B (2024) | Global Consultancy A | Uses historical five-year average ASP, limited primary validation | ||

USD 214.34 B (2024) | Industry Association B | Combines newspaper and magazine revenues, inflating total | ||

USD 95.60 B (2024) | Regional Consultancy C | Applies single global growth rate, minimal currency normalization |

Driving Growth in Hong Kong’s Auditing & Accounting Market

4 Min Read

Strategic Entry into Latin America’s HR Market

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.