Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

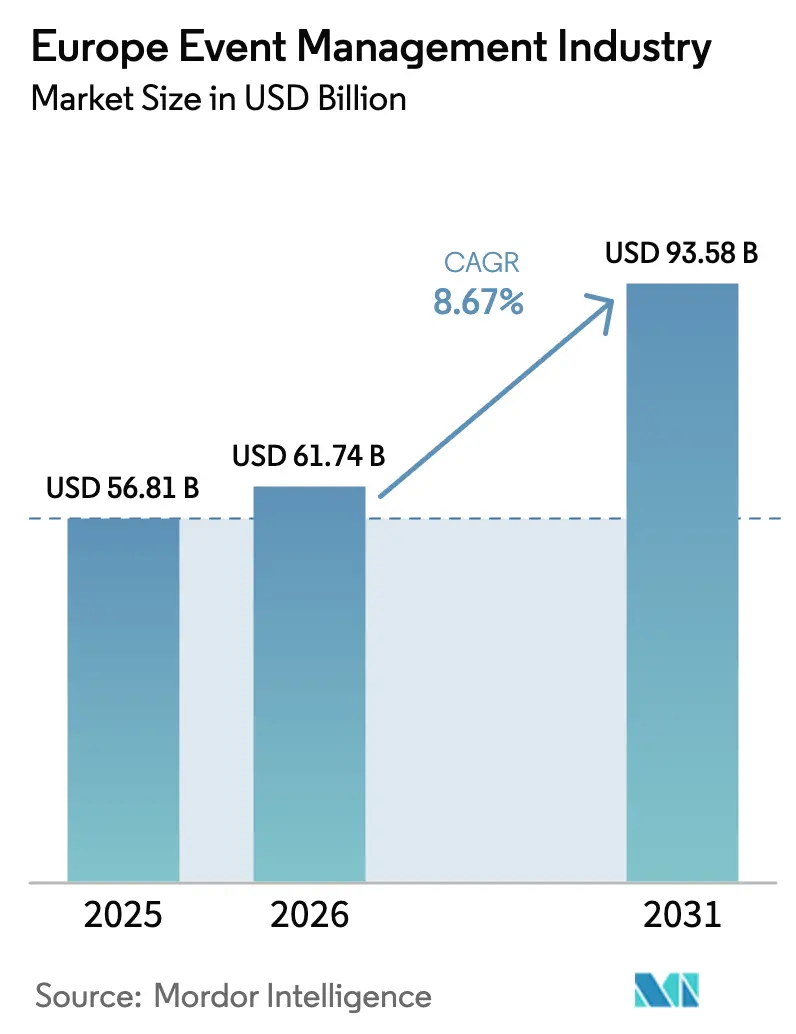

| Base Year Market Size (2025) | USD 56.81 Billion |

| Market Size (2026) | USD 61.74 Billion |

| Market Size (2031) | USD 93.58 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Event Management Industry Analysis by Mordor Intelligence

The Europe event management industry market size was valued at USD 56.81 billion in 2025 and estimated to grow from USD 61.74 billion in 2026 to reach USD 93.58 billion by 2031, at a CAGR of 8.67% during the forecast period (2026-2031). This trajectory affirms a strong rebound underpinned by renewed corporate travel, the normalization of large gatherings, and the widespread integration of hybrid delivery models that blend on-site interaction with digital reach. Upward momentum reflects a balance between pent-up demand for in-person networking and persistent investment in virtual infrastructure that insulates organizers from travel disruptions. Sustained marketing outlays on immersive activations, steady government backing for sustainable practices, and improving data analytics capabilities further raise the growth ceiling of the Europe event management industry market. Meanwhile, mid-sized agencies exploit flexible cost bases to win niche mandates, and venue operators pursue premium pricing to recoup inflation-linked overheads.

Key Report Takeaways

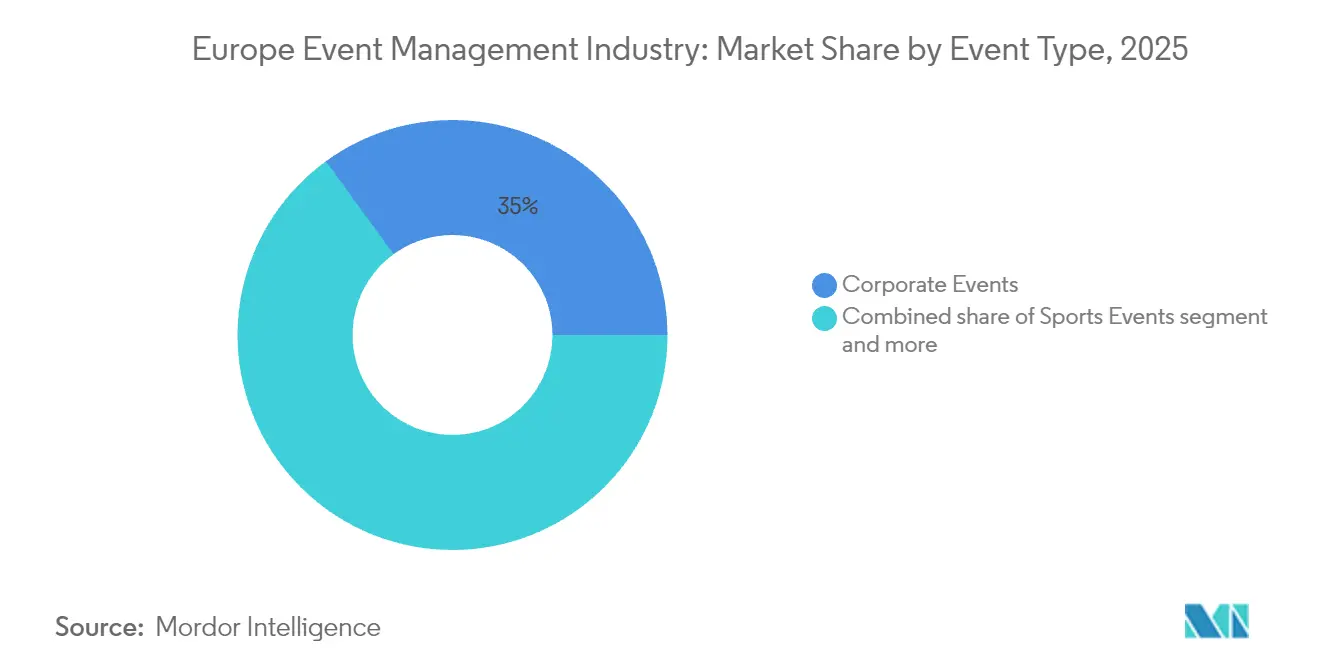

- By event type, Corporate Events led with 35.02% revenue share in 2025; Incentive Events are forecast to expand at a 9.88% CAGR through 2031.

- By mode, in-person gatherings captured 62.76% of the Europe event management industry market share in 2025, while hybrid formats are projected to advance at a 12.27% CAGR to 2031.

- By service, Venue / Location Rental accounted for 30.92% of the Europe event management industry market size in 2025, and Virtual / Hybrid Enablement is growing at a 9.96% CAGR through 2031.

- By end user, SMEs controlled a 71.62% share in 2025; large enterprises are set to post the highest 8.81% CAGR over 2026-2031.

- By geography, the United Kingdom retained 27.63% revenue share in 2025; the Nordics region is projected to grow at a 9.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Event Management Industry Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resurgence of in-person MICE events post-pandemic | +2.1% | Global, strongest in UK, Germany, France | Short term (≤ 2 years) |

| Digitalization & adoption of event-management platforms | +1.8% | NORDICS, BENELUX, with spillover to Central Europe | Medium term (2-4 years) |

| Experiential marketing spend by corporates | +1.5% | UK, Germany, France, with expansion to NORDICS | Medium term (2-4 years) |

| EU & government push for sustainable, inclusive events | +1.2% | EU-wide, early adoption in NORDICS, Netherlands | Long term (≥ 4 years) |

| AI-driven matchmaking & ROI analytics | +0.9% | NORDICS, UK, Germany, gradual adoption elsewhere | Medium term (2-4 years) |

| EU Digital Product Passport spurring data-sharing services | +0.7% | EU-wide, initial focus on manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Resurgence of In-Person MICE Gatherings

Face-to-face meetings re-emerged as a strategic priority when European business-travel outlays started climbing toward USD 450 billion for 2027. Corporations cite higher deal-conversion rates, quicker product-validation cycles, and deeper client trust as the principal benefits of convening onsite. Trade-show organizers report that AI-powered matchmaking lifted scheduled meetings by 44% compared with the 2023 editions. Convention-center occupancy recovered to 74.8% in 2024, yet venue operators still wrestle with margin compression caused by cost inflation. Enterprise willingness to pay premium day-rates despite inflation underscores the revived importance of physical interaction inside the Europe event management industry market[1]Suzanne Neufang, “BTI Outlook 2025: Europe Business Travel Forecast,” Global Business Travel Association, gbta.org.

Digitalization and Platform Adoption

Event technology now spans registration, content streaming, CRM integration, and real-time analytics in one unified stack. Sweden-based InvitePeople posted 95% retention and 48% higher attendee interactions after embedding AI-driven personalization. Across Europe, 73% of planners deem hybrid capability non-negotiable, while privacy-by-design architecture remains a gating factor for procurement. Nordic leadership in broadband quality and cashless payments accelerates experimentation, which then diffuses into Central Europe. These dynamics add fresh tailwinds to the Europe event management industry market.

Rising Experiential Marketing Budgets

Experiential events outperformed traditional media on customer-loyalty metrics in the 2024 Bellwether survey, prompting agencies to scale immersive stages and interactive installations. Automotive, tech, and luxury brands now earmark larger budget shares for live activations that combine education with entertainment. Post-event analytics show that 69% of enterprises tie events directly to revenue generation, while 75% observe productivity gains from corporate gatherings. As spending pivots toward high-engagement formats, the Europe event management industry market secures an expanding marketing wallet share.

EU Drive for Sustainable and Inclusive Events

The Corporate Sustainability Reporting Directive obliges large companies to disclose event-related emissions from 2025. Organizers increasingly adopt ISO 20121 frameworks that mandate objective-setting, supply-chain audits, and stakeholder reporting. Nordic venues already run on renewable energy and furnish real-time carbon dashboards to planners. Demand for carbon-accounting software and accessibility audits broadens service scope, bolstering premium pricing opportunities within the Europe event management industry market[2]Margrethe Vestager, “Corporate Sustainability Reporting Directive—Full Text,” Official Journal of the European Union, eur-lex.europa.eu.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven venue & staffing cost surge | -1.4% | EU-wide, most severe in Netherlands, Germany, UK | Short term (≤ 2 years) |

| GDPR / cyber-security compliance burdens | -0.8% | EU-wide, highest impact in Germany, France | Medium term (2-4 years) |

| Mandatory carbon-foot-print reporting raises costs | -0.6% | EU-wide, early implementation in NORDICS, Netherlands | Long term (≥ 4 years) |

| Virtual alternatives dent demand in Tier-2 cities | -0.5% | Central and Eastern Europe, smaller German cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Venue and Staffing Costs

Average daily venue rates in the Netherlands climbed 38% over 2019 levels, yet profit margins fell to 35.3% as wage expenses surged. Staff shortages across catering and production disciplines hamper service quality and inflate overtime payments. Elevated energy tariffs oblige venues to implement dynamic pricing and minimum-spend clauses, squeezing corporate budgets. Smaller agencies face liquidity strain, driving consolidation that marginally tempers the Europe event management industry market expansion[3]Annette Weisbach, “Hospitality Cost Inflation and Venue Margins in the EU,” European Hotel Managers Association Journal, ehma.com.

GDPR and Cybersecurity Compliance Burden

Non-compliance fines can reach 4% of turnover, prompting rigorous consent workflows, data-residency checks, and ISO 27001 certification of event-tech stacks. The complexity multiplies for hybrid formats that process personal data across streaming, polling, and matchmaking modules. Vendor due diligence cycles extend bid lead times for SME organizers, raising transaction costs and constraining agility. This drag modestly offsets growth prospects in the Europe event management industry market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Event Type: Corporate Dominance Drives Recovery

Corporate Events commanded 35.02% of the Europe event management industry market in 2025, a lead reinforced by executives eager to rebuild culture and client rapport post-remote work. Incentive gatherings, albeit smaller in baseline volume, grow at a brisk 9.88% CAGR as companies use travel and experiences to differentiate retention packages. Association conferences returned to large auditoriums, adding hybrid layers to serve remote professionals. Charity organizers pair live galas with online auctions to widen donor funnels. Festivals and entertainment productions trail the pre-2020 peak because of insurance premiums and crowd-control mandates, but open-air formats draw steady footfall. Meanwhile, sports events reboot hospitality suites, capitalizing on pent-up fan appetite. Hybrid-first events crystallize as a durable niche, granting risk-hedged reach to cautious planners. This diversified mix anchors recurring revenue streams across the Europe event management industry market.

The Europe event management industry market size for Corporate Events climbed alongside board-approved experiential budgets, while the Europe event management industry market share of Incentive Events still sits below 10%, leaving white space for providers fluent in curated travel logistics. Vendors that fuse carbon tracking with experiential storytelling win mid-decade bids from sustainability-minded multinational clients.

By Mode: In-Person Leadership with Hybrid Acceleration

In-person formats retained 62.76% market share in 2025 because trust-building and complex negotiation favor physical presence. Hybrid models, advancing at 12.27% CAGR, extend content to global users and hedge against travel uncertainties. Virtual sessions stabilize near 15% share, serving internal trainings and onboarding. Organizers designing multi-touchpoint journeys observe higher conversion from pre-event webinars into on-site attendance. AV suppliers and cloud-streaming integrators profit from elevated technical specifications that accompany simultaneous live and digital audiences. This segmentation underscores how the Europe event management industry market adopts a portfolio approach rather than a zero-sum substitution path.

Hybrid’s ascent expands the Europe event management industry market size for platform vendors, while the incremental Europe event management industry market share gain for virtual-only providers plateaus due to audience fatigue. Execution complexity encourages large enterprises to outsource end-to-end production, widening the service revenue pool.

By Service: Venue Rental Anchors Growth amid Digital Innovation

Venue / Location Rental represented 30.92% of the Europe event management industry market size in 2025 and retains pricing power given the finite supply in major hubs. Smart-building retrofits that show real-time occupancy and carbon data enhance appeal. Virtual / Hybrid Enablement services, rising at 9.96% CAGR, encompass studios, extended-reality sets, and backend cloud orchestration. Communication and logistics migrate toward omnichannel marketing and mobile app way-finding, reinforcing attendee engagement. AI-driven matchmaking underpins attendee management, with data privacy modules embedded from inception. Catering embraces plant-forward menus to align with ESG mandates. Team-building experiences pivot to outdoor and wellness-oriented concepts. Integrated providers bundle these components to deepen wallet share in the Europe event management industry market.

The Europe event management industry market share gains in enablement offset margin pressure in commodity services such as basic logistics. Agencies that control both venue brokerage and hybrid production capture outsized value.

By End User: SME Dominance Reflects Market Fragmentation

SMEs commanded 71.62% revenue in 2025, demonstrating that Europe’s economic fabric remains heavily decentralized. These clients seek modular packages that cap exposure yet deliver polished brand touchpoints. Large enterprises, projected to post an 8.81% CAGR, require multi-disciplinary teams capable of global compliance reporting and multi-language delivery. Public-sector events proliferate due to stakeholder-consultation mandates embedded in EU directives, adding predictable calendar cycles. Non-profits leverage peer-to-peer fundraising tools inside hybrid builds. Individual professionals consume micro-conferences and career fairs that monetize personal upskilling. Providers that segment by client scale and compliance complexity outperform generic rivals across the Europe event management industry market.

Tailored bundles grow the Europe event management industry market size in the SME tier, while enterprise frameworks with sustainability scorecards bolster the Europe event management industry market share of full-service consultancies.

Geography Analysis

The United Kingdom held a 27.63% share in 2025, sustained by London’s diverse venue stock, multilingual talent, and global air links. Brexit added customs paperwork, yet the mature supplier base blunted friction for cross-border exhibitors. Government incentives for creative-industry apprenticeships enlarge the future workforce. Germany ranks second, drawing industrial expos that orbit its manufacturing clusters. France leverages Parisian cultural cachet and luxury brand patronage. Italy and Spain accelerate as airlines reopen capacity and southern climates appeal for outdoor networking. Benelux punches above its GDP weight by hosting regulatory forums near EU institutions.

Nordic nations deliver the fastest 9.03% CAGR, powered by proactive green-event subsidies and unmatched digital readiness. Local operators integrate cash-free transactions and circular-economy supply chains, winning ESG-oriented briefs. Baltic capitals pilot paperless accreditation that slashes queue times and emissions. Central and Eastern European cities offer competitive price points, though infrastructure gaps and skill shortages temper immediate upside. The European Travel Commission logged 6% visitor arrivals versus 2019, confirming a wider tourism uplift that indirectly supports delegate flows. Currency stability against the USD lowers budget volatility for multinationals planning multi-year rotations. Collectively, these nuances shape a patchwork of opportunities that define the Europe event management industry market.

Competitive Landscape

Market fragmentation characterizes the Europe event management industry: the top five suppliers account for under 15% combined revenue. Scale players concentrate on multinational briefs, bundling venue contracting, creative design, and hybrid technology. Mid-tier agencies differentiate through vertical specialization, such as pharma congresses or fintech roadshows. Technology disruptors like Grip deploy machine-learning algorithms that elevate networking ROI and squeeze manual curation models. White-label SaaS platforms empower micro-agencies to punch above headcount, reinforcing fragmentation.

M&A activity intensified as Impact XM bought Touch Associates to expand its European footprint, while Weezevent merged with Eventix to create a trans-regional ticketing backbone. Strategic stakes target data analytics, GDPR compliance, and sustainability scoring to augment premium value propositions. Venue groups invest in on-site broadcast studios, capturing hybrid revenue streams. Supplier pricing gravitates to dynamic tiering tied to occupancy, bandwidth, and carbon offsets. The Europe event management industry market rewards firms that integrate privacy-safe data, sustainable operations, and immersive tech in one seamless offer.

Europe Event Management Market Leaders

GL events

Reed Exhibitions

ASM Global

CWT Meetings & Events

BCD Meetings & Events

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Impact XM acquired Touch Associates to deepen experiential production capacity across Europe.

- March 2025: Weezevent purchased Eventix, creating the unified but dual-brand ticketing alliance “Weeztix.”

- February 2025: Association of Event Organizers renewed its insurance partnership with InEvexco, enhancing member risk-cover options.

- January 2025: See Tickets Group forged an exclusive integration with Eventication to extend digital ticketing reach.

Europe Event Management Industry Report Scope

Event Management is a platform that coordinates all tasks and activities for events as small as a marathon to as large as the Olympics. These tasks include sales and marketing, logistics, accounting, and travel management. A complete background analysis of the Europe Event Management Market, including an assessment of the national accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and the market overview, is covered in the report. The Europe event management industry is segmented by Type (Corporate Events, Association Events, Non-Profit Events), by Application (Individual User, Corporate Organization, Public Organization, Others), by Geography (Germany, United Kingdom, Spain, Italy, France, Rest of Europe). The report offers market size and forecasts for Europe Event Management Industry in value (USD Million) for all the above segments.

By Event Type

| Corporate Events |

| Association & Conference Events |

| Non-profit & Charity Events |

| Festivals & Entertainment |

| Sports Events |

| Hybrid / Virtual-First Events |

| Others |

By Mode

| In-person |

| Hybrid |

| Virtual |

By Service

| Strategy & Planning |

| Communication & Logistics |

| Venue / Location Rental |

| Attendee Management & Engagement |

| Virtual / Hybrid Enablement |

| Catering & Hospitality |

| Team-building & Experiences |

By End User

| Corporate Organisations |

| SMEs |

| Public Sector / Government |

| Individual Consumers |

| Non-profits & Associations |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Event Type | Corporate Events |

| Association & Conference Events | |

| Non-profit & Charity Events | |

| Festivals & Entertainment | |

| Sports Events | |

| Hybrid / Virtual-First Events | |

| Others | |

| By Mode | In-person |

| Hybrid | |

| Virtual | |

| By Service | Strategy & Planning |

| Communication & Logistics | |

| Venue / Location Rental | |

| Attendee Management & Engagement | |

| Virtual / Hybrid Enablement | |

| Catering & Hospitality | |

| Team-building & Experiences | |

| By End User | Corporate Organisations |

| SMEs | |

| Public Sector / Government | |

| Individual Consumers | |

| Non-profits & Associations | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe event management industry market in 2026?

It reached USD 61.74 billion in 2026 and is projected to hit USD 93.58 billion by 2031.

What CAGR does the market expect through 2031?

The forecast CAGR stands at 8.67% over the 2026–2031 period.

Which event type currently dominates spending?

Corporate Events account for 35.02% of 2025 revenue owing to renewed emphasis on face-to-face collaboration.

Which geographic bloc is growing fastest?

Nordic countries lead with a 9.03% CAGR thanks to advanced digital infrastructure and strong sustainability credentials.

Page last updated on: