Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

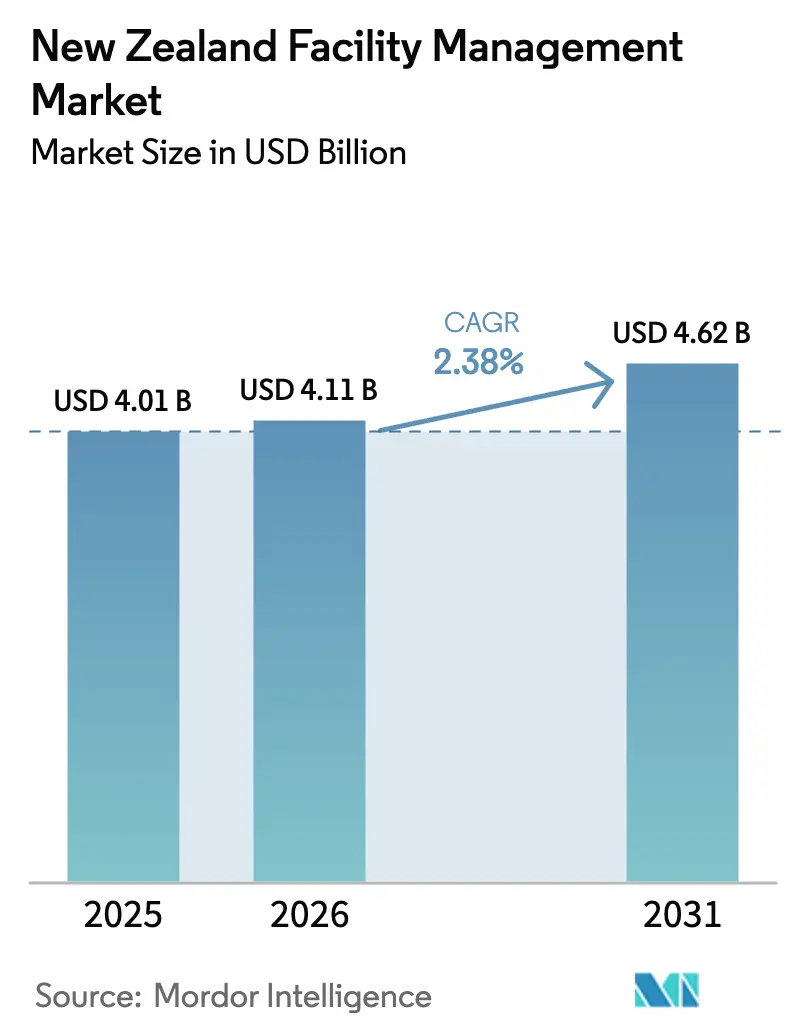

| Base Year Market Size (2025) | USD 4.01 Billion |

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 2.38% CAGR |

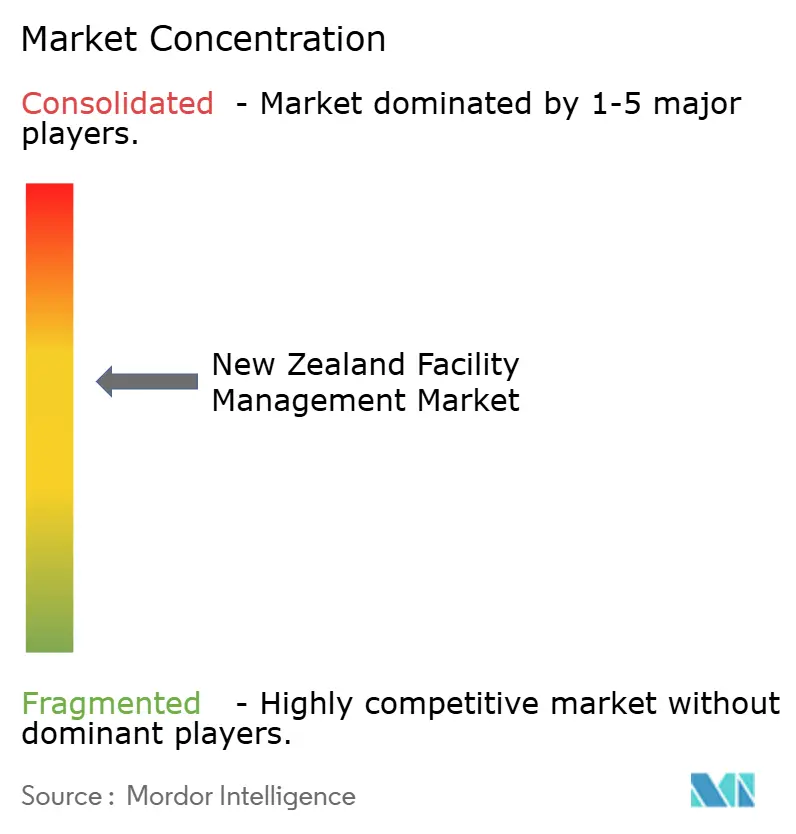

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand Facility Management Market Analysis by Mordor Intelligence

The New Zealand Facility Management Market size in 2026 is estimated at USD 4.11 billion, growing from 2025 value of USD 4.01 billion with 2031 projections showing USD 4.62 billion, growing at 2.38% CAGR over 2026-2031. The measured growth reflects a maturing environment where regulatory compliance, seismic resilience, and digital transformation outweigh pure expansion. Hard services dominate demand, supported by the Building (Earthquake-prone Buildings) Amendment Act 2016, while soft services record the fastest growth as employers outsource non-core functions amid a persistent skills shortage. Outsourced contracts now cover almost two-thirds of the value, and integrated arrangements are replacing single-service deals. Commercial facilities lead spending due to hyperscale data-center builds, whereas institutional and public infrastructure show the strongest growth as Wellington, Auckland, and regional authorities seek better asset stewardship. Escalating insurance premiums, constrained labor availability, and inflationary cost pressures temper momentum yet simultaneously accelerate the adoption of technology-enabled, outcome-based models that promise measurable savings and compliance assurance.

Key Report Takeaways

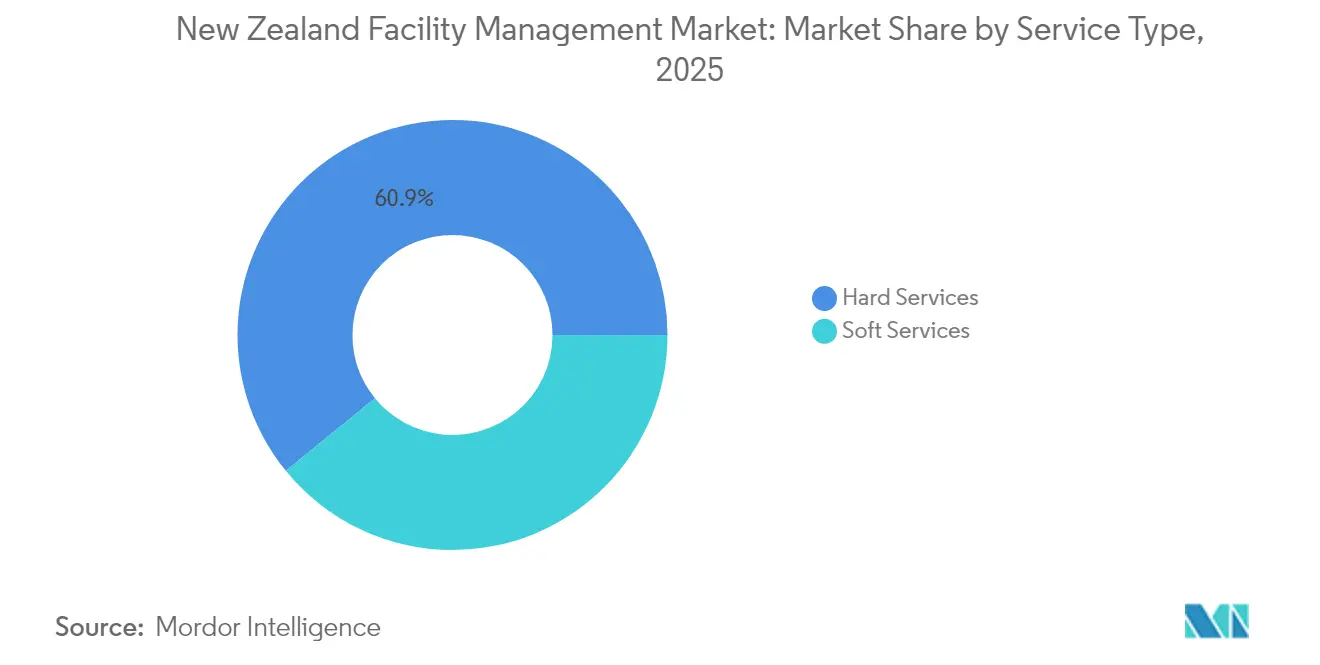

- By service type, hard services held 60.88% of New Zealand's facility management market share in 2025, while soft services are forecast to expand at a 4.08% CAGR to 2031.

- By offering type, outsourced delivery commanded 63.55% share of New Zealand facility management market size in 2025 and is projected to grow at a 3.63% CAGR between 2026-2031.

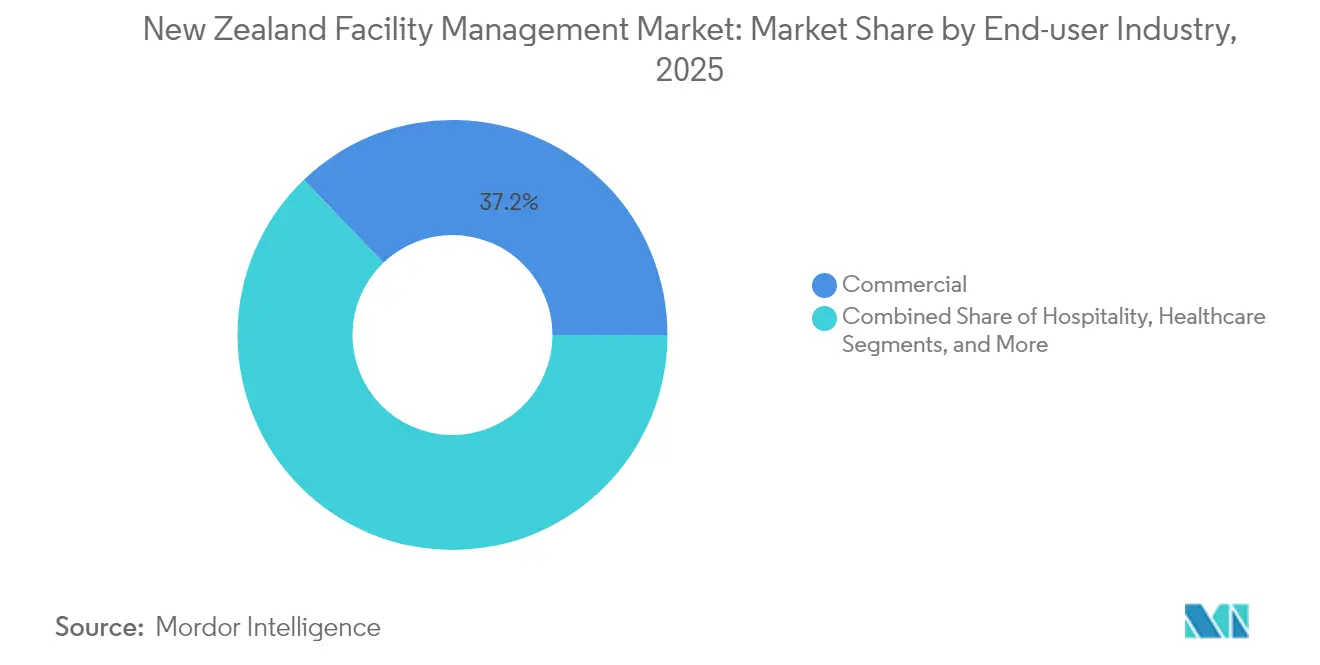

- By end-user industry, commercial facilities captured 37.15% of New Zealand's facility management market share in 2025; institutional and public infrastructure is advancing at a 3.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

New Zealand Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Current occupancy rates | +0.3% | Auckland, Wellington, Christchurch CBDs | Short term (≤ 2 years) |

| Workforce indicators – labour participation | +0.4% | National, concentrated in major metros | Medium term (2-4 years) |

| Urbanization and population growth | +0.5% | Auckland, Hamilton, Tauranga corridors | Long term (≥ 4 years) |

| Infrastructure investment priorities | +0.6% | National focus on transport and utilities | Medium term (2-4 years) |

| Seismic strengthening mandates | +0.7% | High-risk zones (Wellington, Canterbury) | Long term (≥ 4 years) |

| Data-center expansion | +0.8% | Auckland, Wellington, Christchurch, Invercargill | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Current occupancy rates

Hybrid work policies and rising commercial rents push organizations to optimize floorplates, sustaining demand for energy, cleaning, and security services that flex with headcount. Premium Auckland offices such as Fanshawe Street command USD 530 per m², more than double Hamilton averages, prompting multi-site firms to rebalance space portfolios while maintaining uniform service standards. [1]PMG, “Commercial Property For Rent,” PMG.CO.NZ Flexible-workspace operators are consolidating; CBRE’s USD 400 million purchase of Industrious integrates workplace experience with traditional facility offerings. Providers able to match service levels to real-time occupancy and document savings win multi-year outcome-based contracts. IoT-enabled occupancy sensors underpin automated lighting, HVAC, and cleaning rotations, cutting utility and labor hours by double-digit percentages. Over the next two years, occupancy-led optimization is expected to add around 0.3 percentage points to overall market CAGR as more leases shift to variable-cost models.

Workforce indicators – labour participation

A chronic talent deficit touches 40% of New Zealand employers, with trade skills hardest to fill. Construction alone needs 50,000-60,000 extra workers over five years. Average entry-level trade wages have reached USD 30 per hour in Queenstown, inflating the cost base for hard and soft service contracts. To cope, leading vendors deploy cloud-based CMMS and predictive analytics that eliminate 30-50% of routine interventions. [2]Waters Stu, “Guide to Smart Building Technology in 2025,” CORAM.AI MaintainX users such as Ahlstrom slashed mean-time-to-repair by 90%, evidencing tangible ROI. Automation uptake and remote diagnostics are expected to raise service productivity, offset wage inflation, and add 0.4 percentage points to CAGR through 2028.

Urbanization and population growth

Net migration has returned to pre-pandemic highs and concentrates along the Auckland-Hamilton-Tauranga corridor, spurring commercial builds and municipal infrastructure upgrades. Urban sprawl increases the serviced floor area plus ancillary requirements for waste, landscaping, and security. Growth corridors demand resilient utilities; local councils specify minimum green-star ratings that drive higher-value facilities contracts. Over the long term, population inflows are forecast to contribute 0.5 percentage points to market CAGR, particularly benefiting bundled and integrated FM providers capable of regional scale.

Infrastructure investment priorities

The draft National Infrastructure Plan calls for stronger asset management to maximize returns on public spending. Central and local government own roughly 40% of national infrastructure, representing a steady pipeline of road, rail, water, and social-asset maintenance. Auckland Transport alone spends more than USD 250 million annually on road upkeep. Hyperscale data centers built by Microsoft, AWS, and Amazon, totalling USD 8.5 billion, require 24/7 facilities oversight and stringent uptime guarantees. These programs are expected to add 0.6 percentage points to the overall CAGR during the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising operational costs | –0.4% | National, higher in major metros | Short term (≤ 2 years) |

| Skilled labour shortages | –0.6% | National, acute in trades | Medium term (2-4 years) |

| Escalating compliance costs | –0.3% | National, stricter in urban areas | Long term (≥ 4 years) |

| High insurance premiums and natural-disaster risk | –0.5% | Coastal and high seismic areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising operational costs

Construction-cost inflation eased to 1.1% YoY in 2024 after peaking at 10.4% in 2022. Nonetheless, insurance premiums surged 23-76% post-Cyclone Gabrielle, with the Treasury considering a 72% levy hike adding USD 400 annually to policies. Energy tariffs and carbon fees compound the squeeze; commercial buildings generate 3.6 million tons of waste each year and face tighter emissions reporting. Vendors respond with smart-metering, LED retrofits, and waste-to-resource programs that promise double-digit savings, yet near-term profitability remains pressured, trimming about 0.4 percentage points from CAGR.

Skilled labour shortages

Vacancies in HVAC, electrical, and automation trades force overtime rates and reliance on subcontractors, undermining margins. Only 10% of firms run robust apprenticeship schemes, and retirements outpace entrants, widening the competency gap. Instances such as security guards doubling as cleaners at rural hospitals illustrate the strain. Digital twins, AR-assisted maintenance, and centralized help desks alleviate some scarcity, but the constraint still subtracts 0.6 percentage points from growth until training pipelines recover.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Seismic Compliance

Hard services claimed 60.88% share of the New Zealand facility management market size in 2025, underpinned by mandatory structural assessments, MEP upgrades, and fire-safety retrofits across thousands of assets. Engineering consultancies partner with integrated FM firms to deliver turnkey seismic projects, capturing recurring monitoring fees once upgrades finish. Data-center openings intensify demand for mission-critical HVAC maintenance, switchgear testing, and redundancy planning. OEM-backed service contracts guarantee uptime metrics that command premium pricing. Asset-management analytics using AI schedule capital replacements, extend lifecycle, and reduce asset-failure incidents. This predictability grants hard-service providers stable cash flows through 2031.

Soft services, while smaller, grow at 4.08% CAGR as organizations externalize cleaning, security, catering, mailroom, and reception tasks. Wage escalation accelerates automation: cobotic floor-scrubbers, AI-powered rostering, and smart-locker mail solutions proliferate. Healthcare and data-center clients specify higher hygiene and security standards, lifting average contract value. ESG reporting pushes vendors to switch to low-tox chemicals and electrified equipment, differentiating bids. Technology integrators like ESP (rebranding to BraveGen) inject carbon-tracking into cleaning workflows, demonstrating quantitative savings and winning multi-site portfolios. As a result, bundled soft-service contracts increasingly roll into integrated FM deals for holistic value.

By Offering Type: Outsourcing Accelerates Integration

Outsourced delivery held 63.55% of New Zealand's facility management market share in 2025 and maintains a 3.63% CAGR trajectory as enterprises shed non-core operations. Government ministries award long-duration performance contracts that shift risk to suppliers, mirroring Veolia’s 7-25 year template. Integrated FM, the fastest sub-model, knits hard and soft services plus energy advisory into single SLAs backed by digital dashboards. Healthcare boards, universities, and data-center operators favor the arrangement for single-throat accountability and KPI transparency. Cloud-based IWMS platforms enable near-real-time tracking of work orders, compliance, and sustainability metrics.

In-house management still accounts for 36.45% of value, but erodes as skills shortages and technology capex deter boards from retaining full internal teams. Hybrid models emerge: strategic FM oversight remains internal, yet high-specialty activities—chiller overhauls, fire-system testing, facade access—are outsourced. Single service and bundled FM options serve clients unwilling to cede full control but requiring selective expertise, creating a stepping-stone toward integrated deals. Downer’s PPP track record shows bundled FM can lift margins when paired with digital optimization, evidenced by its 34% earnings jump in 2024.

By End-user Industry: Commercial Leads Digital Transformation

Commercial facilities commanded 37.15% of the New Zealand facility management market size in 2025, propelled by hyperscale cloud campuses and omnichannel retail distribution. Microsoft, AWS, and Amazon collectively invest USD 8.5 billion in server farms that expect 99.999% uptime and precise environmental controls. Retailers modernize warehouses with autonomous robots, demanding specialized floor maintenance and electrical support. Sustainability targets push mall owners to deploy smart-meter stacks and LED retrofits, generating shareable utility savings with service partners.

Institutional and public infrastructure exhibits the highest 3.84% CAGR thanks to the government’s asset-management focus and aging hospitals, schools, and transport networks. The healthcare subsector highlights staffing and hygiene complexities; controversies such as dual-role security cleaners underscore service gaps. Education boards install building-management systems for ventilation monitoring, while road-maintenance consortia integrate sensors for predictive pothole repair. Providers with integrated FM capacity and compliance track records capture these portfolios.

Industrial and process plants, hospitality venues, and other sectors round out demand. Fonterra’s Darfield factory processes 4.4 million L of milk daily and contracts advanced automation support. Hotels rebound post-pandemic; Capstone expands to 22 properties, utilizing SiteMinder to optimize occupancy and housekeeping rosters. Each niche requires domain-specific know-how yet increasingly converges around digital dashboards, energy efficiency, and stringent compliance, favoring scale vendors.

Geography Analysis

Auckland dominates the New Zealand facility management market share, reflecting its status as the commercial and population hub, concentration of hyperscale data centers, and large infrastructure builds such as the City Rail Link and airport terminal expansion. Prime CBD office rents exceed USD 530 per m² and drive premium FM rates. Clients prioritize 24/7 support, smart-building solutions, and ESG disclosure. Integrated providers combine help-desk, energy management, and critical-asset maintenance to meet these sophisticated demands.

Wellington ranks second, shaped by seismic risk and a high density of government properties. Over 150 CBD structures await NBS compliance, guaranteeing steady engineering workloads. Public-sector outsourcing continues, illustrated by Te Papa’s cleaning and related services tender awarded to ISS. Vendors must navigate rigorous procurement, unionized workforces, and heightened transparency standards. Demand focuses on seismic monitoring, document management, and lifecycle planning.

Christchurch and the wider Canterbury region remain growth hotspots following post-quake reconstruction and expanding food-processing facilities. Modern building stock integrates IoT controls, requiring technicians versed in BMS analytics. Lower rent—USD 245 per m² in Hamilton as reference—makes bundled FM appealing for cost-sensitive occupants. Regional councils emphasize sustainable waste solutions and water-treatment oversight, opening niches for specialist operators.

Smaller centres such as Invercargill could punch above their weight due to a proposed USD 1 billion data center investment, which will necessitate on-call engineers and strict security regimes. Remote locations encourage cloud-based monitoring and fly-in service crews, representing an emerging use-case for digital twins and AR troubleshooting. Across all geographies, regulatory compliance, resilience, and energy efficiency form common threads, ensuring consistent demand for integrated, technology-driven FM.

Competitive Landscape

The New Zealand facility management market demonstrates moderate fragmentation. Spotless, a Downer subsidiary, leads with more than 1,000 clients and coverage across healthcare, education, and defense. [4]Spotless, “About Us,” SPOTLESS.COM Parent Downer posted USD 38.5 billion work-in-hand and 34% EBITA growth in 2024, underlining the capacity to invest in digital tools and workforce training. Ventia Services Group competes strongly in infrastructure and utilities following its dual NZX/ASX listing and targeted acquisitions.

Global property giants intensify competition. CBRE’s acquisition of Industrious for USD 400 million merges flexible office operations with facilities portfolios, creating a USD 20 billion revenue platform. Cushman & Wakefield and JLL leverage international best practices, particularly in energy optimization and workplace experience analytics. Smaller domestic players focus on niche services—waste, hygiene, or regional contracts—but risk being outbid without scale technologies.

Technology serves as a key differentiator. Downer’s rollout of IBM Envizi halves ESG reporting effort and supports its 50% emissions-cut pledge. Veolia’s long-horizon performance contracts illustrate risk-transfer appetite and integrated energy-service expertise. ESP/BraveGen overlays AI on utility data to deliver carbon insights for cleaning and maintenance workflows. Consolidation is expected as firms seek breadth and digital capability; Ovation Hospitality’s purchase of Downer NZ Catering shows vertical integration in soft services.

White-space lies in outcome-based, data-rich agreements that guarantee energy, uptime, or compliance metrics. Providers that combine asset analytics, mobile workforce tech, and robust HSE governance stand to capture a disproportionate share, especially as public-sector tenders pivot to value-for-money scoring models.

New Zealand Facility Management Industry Leaders

OCS New Zealand

Spotless (Downer Company)

PAE New Zealand

Professional Property and Cleaning Services Ltd

Infratel Networks Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CBRE agreed to acquire Industrious National Management Company for USD 400 million, forming a Building Operations and Experience segment with projected USD 20 billion in 2024 revenue.

- December 2024: AWS announced launch customers for its USD 7.5 billion Auckland cloud region, featuring three availability zones powered by renewable energy.

- November 2024: Amendments to the Earthquake-prone Buildings Act extended remediation deadlines by four years while tightening the warrant-of-fitness regime.

- September 2024: Auckland Airport selected Hawkins (Downer) to build a USD 495 million domestic jet terminal slated to open in 2029.

- August 2024: Downer reported a 34% year-on-year EBITA rise to USD 384.1 million, with facilities margins improving on digital optimization.

New Zealand Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through its responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres.

Both in-house facility management and outsourced FM services are considered in the scope. The integrated facility management service (IFM) market, along with single and bundled services, is included in the outsourced FM services segment.

The NewZealand facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the New Zealand facility management market?

The New Zealand facility management market size is USD 4.11 billion in 2026.

Which service type holds the largest share?

Hard services lead with 60.88% New Zealand facility management market share in 2025.

Why are outsourced contracts growing faster than in-house management?

Organizations pursue cost certainty, regulatory compliance, and access to scarce technical talent, driving outsourced arrangements to a 3.63% CAGR through 2031.

How do seismic regulations influence demand?

The Earthquake-prone Buildings Act mandates assessments and retrofits across commercial stock, ensuring long-term demand for structural and compliance services.

Which end-user segment is expanding the quickest?

Institutional and public infrastructure shows the fastest 3.84% CAGR as government agencies prioritize asset management and maintenance efficiency.

What technologies are reshaping service delivery?

IoT sensors, predictive maintenance analytics, cloud-based CMMS, and ESG reporting platforms cut manual interventions, boost uptime, and support outcome-based contracts.

Page last updated on: