Netherlands Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 39.71 Billion |

| Market Size (2026) | USD 41.46 Billion |

| Market Size (2031) | USD 51.45 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

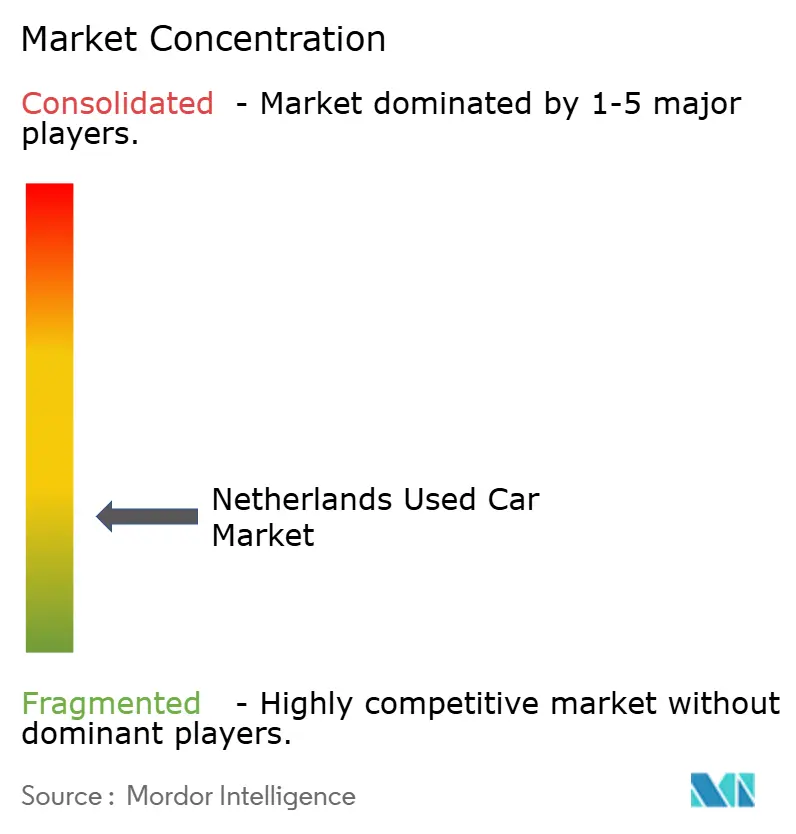

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Used Car Market Analysis by Mordor Intelligence

The Netherlands' used car market size in 2026 is estimated at USD 41.46 billion, growing from 2025 value of USD 39.71 billion with 2031 projections showing USD 51.45 billion, growing at 4.41% CAGR over 2026-2031. Sustained demand for affordable mobility, a steady influx of nearly-new corporate fleet vehicles, and robust digital retail infrastructure form the core growth engine. Regulatory milestones such as zero-emission zones across 29 municipalities reshape replacement cycles while WLTP-driven fleet tax changes expand late-model supply. Hatchbacks anchor volume, yet the SUV cohort expands faster due to lifestyle preferences and electric-ready platforms. Dealer consolidation, the rise of omnichannel storefronts, and embedded-finance APIs compress transaction friction, allowing vendors to tap broader audiences without geographic limits. Market risks include high financing costs, odometer fraud in parallel imports, and technological obsolescence in older models.

Key Report Takeaways

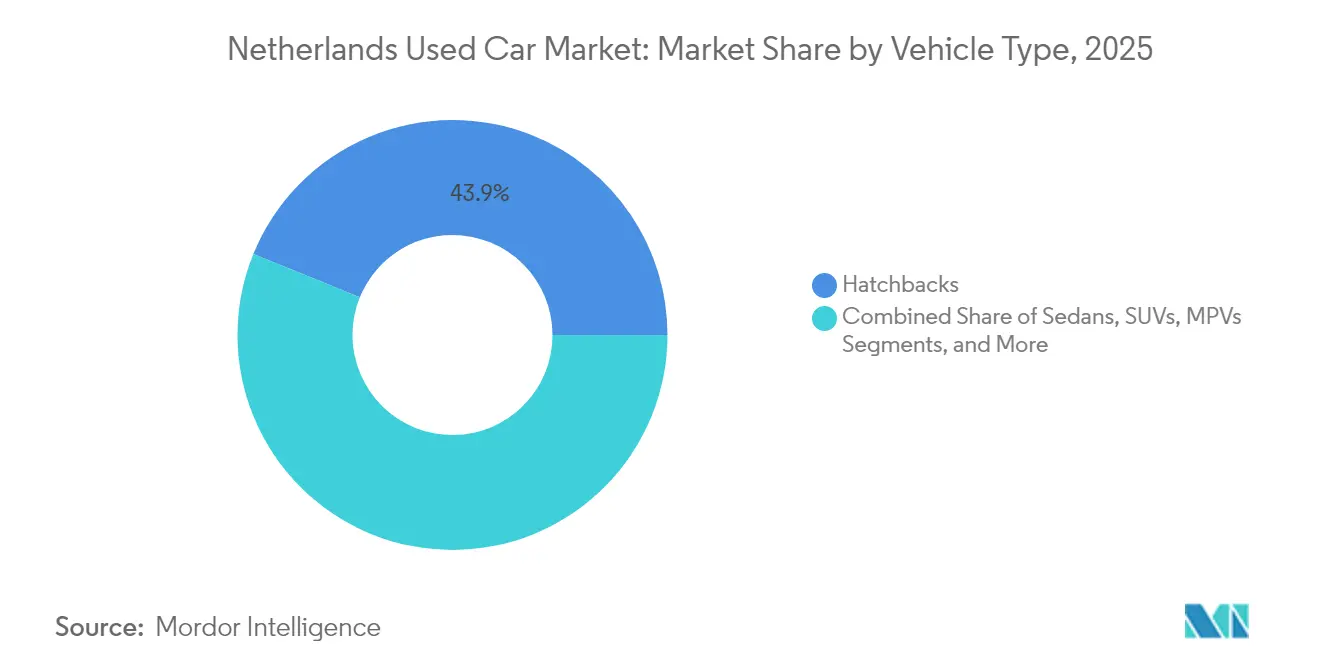

- By vehicle type, hatchbacks led with 43.85% of the Netherlands' used car market share in 2025, whereas SUVs are projected to log the fastest 8.78% CAGR to 2031.

- By vendor type, the organized dealer channel held 58.74% share of the Netherlands used car market size in 2025 and is expanding at a 6.83% CAGR through 2031.

- By fuel type, petrol cars accounted for 52.66% share of the Netherlands' used car market size in 2025, while battery electric vehicles are climbing at a 10.25% CAGR to 2031.

- By vehicle age, the 3-5 year bracket captured 31.44% of the Netherlands' used car market share in 2025, and the 0-2 year segment is forecast to widen at a 9.05% CAGR through 2031.

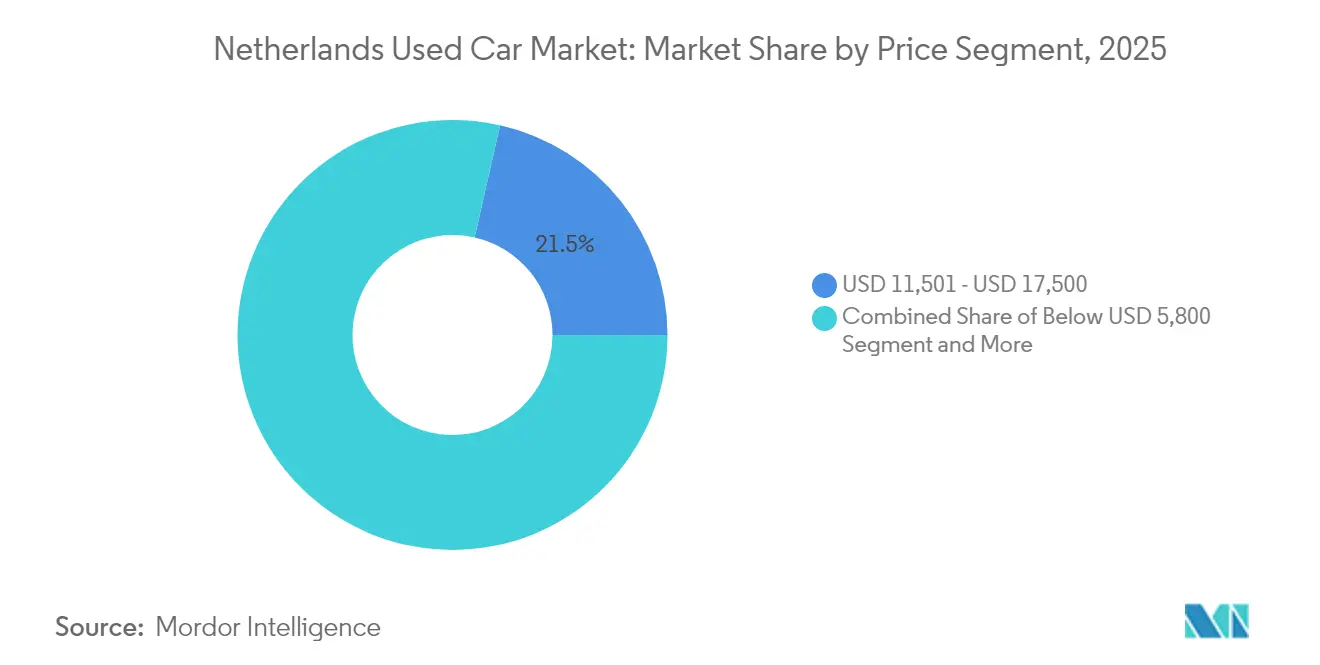

- By price segment, the USD 11,501-17,500 band commanded 21.45% share of the Netherlands used car market size in 2025, whereas cars priced above USD 35,000 are set to rise at an 7.74% CAGR.

- By sales channel, online platforms contributed 43.02% to the Netherlands' used car market size in 2025, and pure-play e-retailers are scaling at a 9.36% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands forms part of a network that extends across countries and regions, each contributing to a shared international environment. The global used car market outlook by Mordor Intelligence consolidates those connections.

Netherlands Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Demand for Affordable Mobility Amidst Inflation | +1.2% | Netherlands, spillover to Belgium and Germany | Short term (≤ 2 years) |

| Rapid Digitalization and Omnichannel Retail Models | +1.1% | Netherlands, leading EU digital transformation | Medium term (2-4 years) |

| Expansion of OEM-Backed Certified-Pre-Owned (CPO) Programs | +0.8% | Netherlands, with early adoption in Randstad region | Medium term (2-4 years) |

| Zero-Emission-Zone (2025) Policy Accelerating ICE Replacement | +0.8% | Netherlands, 29 municipalities with ZE-zones | Short term (≤ 2 years) |

| Corporate-Fleet Churn From WLTP Tax Changes Boosting Nearly-New Supply | +0.7% | Netherlands, with secondary effects in EU markets | Short term (≤ 2 years) |

| Embedded-Finance APIs Enabling Instant Credit and Insurance Bundling | +0.6% | Netherlands, early fintech adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Affordable Mobility Amidst Inflation

Inflation pushes new-car prices beyond reach for many households, steering purchasers toward quality used cars that trim the total cost of ownership. Fleet operators are offloading internal-combustion assets ahead of tighter environmental rules, swelling nearly-new supply at compelling price points. Dutch BPM tax revisions scheduled for 2025 further accelerate this rotation by erasing key exemptions for commercial vehicles. Financing patterns adjust in tandem, with lenders stretching terms so customers can hold monthly payments steady while stepping into higher-spec models.

Expansion of OEM-Backed Certified Pre-Owned Programs

Automakers strengthen brand affinity and margin control through warranties and refurbishment standards that lift consumer trust. Organized dealers gain momentum because CPO inventory sits within their partner network. The ten largest dealer groups, which own new-car throughput, deploy centralized reconditioning hubs and real-time inventory tools that small independents cannot replicate. Connected-car telematics adds another layer of transparency by confirming mileage and maintenance history, a key antidote to odometer fraud.

Rapid Digitalization and Omnichannel Retail Models

Online platforms accounted for more unit transfers in 2024, and pure-play e-retailers are scaling at double-digit speed. Dutch broadband penetration and high digital literacy clear the path for end-to-end online journeys that combine virtual showrooms with home delivery. Dealers introduce artificial-intelligence pricing engines and image-based condition scans to keep pace with 24-hour consumer research cycles. Many buyers consult the web before any physical lot visit, forcing legacy franchises to invest in CRM, live chat, and embedded-finance widgets that approve credit within minutes. These integrated systems widen the Netherlands' used car market to time-pressed urbanites and semi-urban buyers.

Zero-Emission-Zone 2025 Policy Accelerating ICE Replacement

Since January 2025, municipalities in the Netherlands have been extended the privilege to designate urban areas where only zero-emission vehicles can operate. These zones restrict access to ICE-driven commercial vans and trucks, allowing only electric vehicles (EVs) and hydrogen-powered vehicles for business purposes. Fleets and small businesses retire non-compliant vehicles early to avoid penalties, releasing fresh stock into secondary channels. Amsterdam and several other municipalities mandate that newly registered taxis be zero-emission by 2025, creating predictable disposal waves that benefit 0-2 year inventory.[1]“Uitstootvrije Zone 2025,” Gemeente Amsterdam, amsterdam.nlRegional price gaps emerge as restricted vehicles migrate to provinces without zone coverage, embedding arbitrage opportunities for data-savvy wholesalers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interest-Rate Environment Raising Financing Costs | -1.1% | Netherlands, synchronized with ECB monetary policy | Short term (≤ 2 years) |

| Odometer-Tampering Risk in Parallel Imports Eroding Buyer Trust | -0.9% | Netherlands, cross-border transactions with Germany/Belgium | Short term (≤ 2 years) |

| Older Vehicles Lack Advanced ADAS / Connectivity Features | -0.8% | Netherlands, affecting vehicles over 5 years old | Long term (≥ 4 years) |

| Stricter EU End-of-Life-Vehicle Directive Increasing Dealer Compliance Costs | -0.6% | Netherlands, EU-wide regulatory harmonization | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Older Vehicles Lack Advanced ADAS and Connectivity Features

Cars over five years old often miss driver-assistance systems and smartphone integration. Dutch drivers do not get ADAS briefings at purchase, while 40% of sellers feel under-informed, and knowledge gaps widen, blunting the demand for older stock.[2]J. Doornbos et al., “Consumer Knowledge Gaps on ADAS Functions,” Accident Analysis & Prevention, sciencedirect.com Insurance discounts and safety incentives increasingly tilt toward tech-rich cars, reducing price elasticity for the 6-8 and 9-12 age brackets. Technology-light vehicles drift to budget niches as automakers standardize over-the-air updates and semi-autonomous functions.

High Interest-Rate Environment Raising Financing Costs

Sub-EUR 15,000 shoppers must now extend loan terms to match pre-rate-hike monthly outlays. Cash deals inch upward, slowing turnover for dealers reliant on captive-finance penetration. Fleet buyers face similar headwinds as corporate borrowing costs climb, triggering longer retention cycles. The Netherlands carries high household debt, so rising mortgage payments squeeze discretionary vehicle budgets first.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Hatchbacks Dominate but SUVs Set the Pace

Hatchbacks secured 43.85% of the Netherlands' used car market share in 2025, cementing their role as price-efficient urban transport. Yet, growth tilts toward SUVs, which are projected to register a 8.78% CAGR to 2031. The Netherlands' used car market size for SUVs expands as consumers prioritize elevated seating, perceived safety, and compatibility with electric powertrains. Fleet disposals historically favored compact body styles, but the zero-emission-zone rules make higher-roof BEV crossovers attractive replacements. Residual value resilience further lifts SUV uptake, balancing higher purchase prices with predictable exit prices.

The "others" category, convertibles, coupes, niche sports cars, and crossovers, captures a moderate share in the market, propelled by crossover sub-segments that blur hatchback and SUV cues. MPVs keep a steady share, appealing to larger families seeking cabin versatility. Corporate tax changes encourage businesses to pivot from sedan company cars to compact crossovers that meet new WLTP brackets, thus reshaping future feedstock for retail channels.

By Vendor Type: Organized Dealers Leverage Digital Scale

Organized dealerships controlled 58.74% of the Netherlands' used car market size in 2025 and are slated to grow 6.83% annually to 2031. Digital storefronts, warranty extensions, and integrated financing solidify their edge. The Netherlands used car market size handled by the top 10 groups climbs as they pool refurbishment centers, lowering per-unit reconditioning cost and shortening days-to-sale. Certified pre-owned lines further differentiate stock, granting these sellers a pricing premium while shielding buyers from fraud risk.

Unorganized vendors remain relevant in rural provinces and for older, low-price inventory. Yet regulatory compliance layers such as the tightened End-of-Life Vehicle directive raise overhead, prompting smaller outfits to outsource recycling and documentation. Digital marketplaces give independents national visibility but cannot fully bridge the gap in warranty, logistics, and finance facilitation that large dealer networks deliver.

By Fuel Type: Electrics Accelerate Transformation

Petrol cars retained 52.66% of the Netherlands' used car market share in 2025, but their expansion slowed as environmental policy intensified. Battery electric vehicles enjoy a 10.25% CAGR forecast as corporate leases expire into retail pools. The Netherlands' used car market size for BEVs is expected to strengthen, due to an increase in BEV share in new-vehicle registrations in 2024, half of which were corporate, guaranteeing a sizeable rollout to secondary buyers within typical three-to-four-year cycles. Diesel demand fades under zone restrictions and negative sentiment, while hybrids serve as a transitional bridge for consumers wary of charging limitations.

Range confidence is buttressed by more than 120,000 public charging points nationwide. The high initial cost of battery electric vehicles produces short-term uncertainty, yet leaves the long-run cost equation favorable relative to petrol.

By Vehicle Age: Nearly-New Cars Gain Traction

Vehicles aged 3-5 years own 31.44% of the Netherlands' used car market size in 2025, balancing modern tech with moderate depreciation. The 0-2 year niche, fed by corporate fleet churn, is the fastest climber with a 9.05% CAGR through 2031. Companies dispose of cars sooner to sidestep zero-emission penalties, so nearly-new volumes and trim levels improve. Warranty overlap and lower mileage enhance buyer confidence, cutting time-to-sale across digital channels.

Older slices, 6-8 years and 9-12 years, remain viable for budget seekers but face value drag from missing ADAS. Vehicles over 12 years old contend with insurance surcharges and zone restrictions that limit city access. Financing mirrors the risk curve: lenders offer favorable rates on under-five-year cars, whereas loans for older inventory demand higher down-payments and shorter maturities, constraining affordability.

By Price Segment: Middle Market Anchors Volume

The USD 11,501-17,500 accounted for 21.45% of the Netherlands' used car market share in 2025 as households seek a balance of features and manageable debt loads. In contrast, the Netherlands' used car market share above USD 35,000 shows the sharpest value growth, riding an 7.74% CAGR propelled by wealth concentration and accelerated luxury depreciation. Sub-USD 5,800 lots cater to cash-constrained buyers and last-mile service providers.

Mid-tier brackets (USD 17,501-23,100 and USD 23,101-35,000) will have more transactions as purchasers stretch budgets for infotainment upgrades or electrified powertrains. Interest-rate sensitivity is acute in these zones because term extensions directly affect affordability metrics.

By Sales Channel: Digital Platforms Reshape Access

Online outlets captured 43.02% of the Netherlands' used car market share in 2025, and their prevalence in the Netherlands' used car market will climb as omni-journeys normalize. Pure-play e-retailers record a 9.36% CAGR by combining nationwide inventory, algorithmic pricing, and logistics networks that offer doorstep delivery within 48 hours. Offline OEM franchise dealers retain a sizeable footprint through showroom test drives and same-day service packages, but increasingly plug into centralized digital marketplaces for lead generation.

Multi-brand independents leverage localized trust and after-sales proximity, yet now mirror the digital toolsets of broader rivals. Physical auctions lose share to online auction rooms where wholesalers bid in real time. Augmented-reality walk-arounds and 360-degree imaging temper buyer hesitation around remote purchases.

Geography Analysis

The Randstad arc—Amsterdam, Rotterdam, The Hague, and Utrecht—concentrated the Netherlands' used car market value in 2024, owing to its dense population, higher disposable income, and above-national digital adoption rates. Zero-emission zones in these cities intensify the turnover of older ICE cars, pushing compliant supply into secondary towns. Their buyers prize utility over prestige, so hatchbacks and light vans dominate inventory mixes.

Southern regions Noord-Brabant and Limburg benefit from proximity to Belgian and German borders. Although odometer fraud is common among incoming German imports, cross-border arbitrage thrives, prompting countermeasures such as mandatory mileage verification at transfer. Charging density remains a differentiator. Urban areas host most of the nation's charging public points, whereas rural drivers cite range anxiety as a barrier to BEV acquisition. Embedded-finance penetration also skews urban, where fintech lenders approve credit on mobile, while rural residents rely on traditional bank networks. Dutch tax policy, digital literacy, and reliable logistics make the country a net exporter of lightly used BEVs, especially toward Germany, where incentives remain stronger. Consequently, domestic sellers monitor foreign exchange and policy shifts to time cross-border listings for maximum margin.

Mordor Intelligence delivers a comprehensive view of the used car market across all major regions such as Africa, alongside country-level analysis for Finland, Norway, Nigeria, Ethiopia, Hong Kong, New Zealand, Myanmar, and Switzerland, each offering a view of the local market realities.

Competitive Landscape

Dealer concentration tightens each year. The 100 largest groups sell nearly all new cars and redirect their procurement muscle into used operations. They acquire smaller independents to pool inventory, negotiate financing kickbacks, and invest in AI-driven repricing engines. The Netherlands' used car market consequently sees unit margins stabilize, even as price transparency increases through comparison portals.

Pure-play digital retailers raise capital to establish inspection hubs that reassure consumers through certified condition reports and return windows. Some expand into strategic partnerships with charging station operators to bundle energy subscriptions with electric-vehicle purchases. Traditional franchises respond by embedding same-day delivery and live video walk-throughs, blurring the line between online and offline propositions.

White-space entrants specialize in niche services: battery-health certification, ADAS retrofitting, and high-end vehicle authentication. EU scrutiny over anti-recycling collusion, underscored by the EUR 458 million (USD 540 million) fine in April 2025, nudges OEMs to outsource end-of-life compliance to transparent recyclers. Dealers that align early with certified dismantlers gain reputational leverage and smoother inventory rotation.

Netherlands Used Car Industry Leaders

Marktplaats

AutoScout24

AutoTrack

ViaBOVAG

Gaspedaal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The price of used Dutch electric vehicles (EVs) decreased by 30% since 2023, with the average cost of a second-hand EV priced at €18,427 (USD ~21,736), according to an internal analysis conducted by the Looping platform. This decline stems from reduced government subsidies, lower new model prices, and an increased supply of post-lease vehicles in the used market.

- February 2025: Lizy, a Belgian-based used car leasing company, announced its plan to expand into the Netherlands. Lizy provides digital leasing solutions for used vehicles to SMEs and self-employed individuals, enabling them to secure and receive vehicles within short timeframes.

Netherlands Used Car Market Report Scope

A used car, a pre-owned vehicle, or a second-hand car is a vehicle that has previously had one or more retail owners. On the other hand, a certified pre-owned (CPO) vehicle is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned. The term ''used'' refers to the fact that the car has been driven and may have accumulated some wear and tear over its lifetime.

The scope of the Netherlands used car market is segmented by vehicle type and vendor. By vehicle type, the market is segmented into hatchbacks, sedans, sport utility vehicles, and multi-purpose vehicles. By vendor, the market is segmented into Organized and Unorganized.

For each segment, market sizing and forecast have been done based on value (USD billion).

| Hatchbacks |

| Sedans |

| Sports Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Others (Convertibles, Coupes, Crossovers, Sports Cars) |

| Organised |

| Unorganised |

| Petrol |

| Diesel |

| Hybrid (HEV & PHEV) |

| Battery-Electric (BEV) |

| LPG / CNG / Others |

| 0 - 2 Years |

| 3 - 5 Years |

| 6 - 8 Years |

| 9 - 12 Years |

| Above 12 Years |

| Below 5,800 |

| 5,800 - 11,500 |

| 11,501 - 17,500 |

| 17,501 - 23,100 |

| 23,101 - 35,000 |

| Above 35,000 |

| Online Digital Classified Portals |

| Pure-Play E-Retailers |

| OEM-Certified Online Stores |

| Offline OEM-Franchised Dealers |

| Multi-brand Independent Dealers |

| Physical Auction Houses |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| Sports Utility Vehicles (SUVs) | |

| Multi-Purpose Vehicles (MPVs) | |

| Others (Convertibles, Coupes, Crossovers, Sports Cars) | |

| By Vendor Type | Organised |

| Unorganised | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid (HEV & PHEV) | |

| Battery-Electric (BEV) | |

| LPG / CNG / Others | |

| By Vehicle Age | 0 - 2 Years |

| 3 - 5 Years | |

| 6 - 8 Years | |

| 9 - 12 Years | |

| Above 12 Years | |

| By Price Segment (USD) | Below 5,800 |

| 5,800 - 11,500 | |

| 11,501 - 17,500 | |

| 17,501 - 23,100 | |

| 23,101 - 35,000 | |

| Above 35,000 | |

| By Sales Channel | Online Digital Classified Portals |

| Pure-Play E-Retailers | |

| OEM-Certified Online Stores | |

| Offline OEM-Franchised Dealers | |

| Multi-brand Independent Dealers | |

| Physical Auction Houses |

Key Questions Answered in the Report

What is the current value of the Netherlands used car market?

The market is worth USD 41.46 billion in 2026 and is projected to climb to USD 51.45 billion by 2031.

Which vehicle type is growing the fastest in Dutch used-car sales?

SUVs lead growth with a 8.78% CAGR forecast to 2031, driven by lifestyle shifts and electric-ready chassis designs.

Why are battery electric vehicles gaining ground in the secondary market?

Corporate fleets register nearly half of new BEVs, and these low-mileage cars enter the market after lease expiry, while robust public charging network boost buyer confidence.

What impact will zero-emission zones have on used-car prices?

Zones make older Euro 4 and Euro 5 ICE models less desirable in affected cities, encouraging accelerated disposal and producing regional price differentials favoring compliant vehicles.

How does the high interest-rate environment affect buyers?

Higher ECB rates raise monthly loan costs, prompting longer terms for mid-priced cars and greater reliance on cash deals in budget segments, which can slow overall transaction velocity.

Page last updated on: