Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

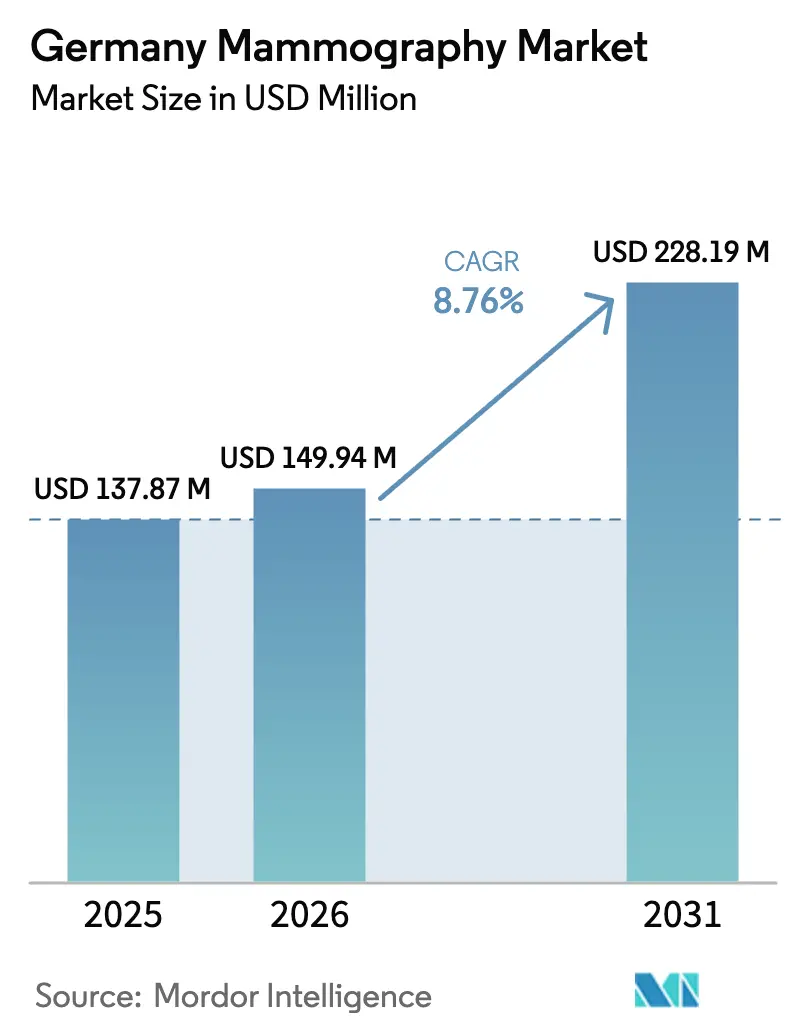

| Base Year Market Size (2025) | USD 137.87 Million |

| Market Size (2026) | USD 149.94 Million |

| Market Size (2031) | USD 228.19 Million |

| Growth Rate (2026 - 2031) | 8.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Mammography Market Analysis by Mordor Intelligence

Germany mammography market size in 2026 is estimated at USD 149.94 million, growing from 2025 value of USD 137.87 million with 2031 projections showing USD 228.19 million, growing at 8.76% CAGR over 2026-2031. Stable public reimbursement, rapid hospital digitization through the Krankenhauszukunftsgesetz (KHZG) fund, and the national rollout of AI-supported screening workflows are driving sustained equipment upgrades across the country. Expanded eligibility that now includes women aged 70-75 adds roughly 2 million potential participants to the biennial screening pool, bolstering procedure volumes and equipment utilization. Clinical evidence from the PRAIM study shows a 17.6% boost in cancer detection when AI is layered onto digital mammography, accelerating demand for software-integrated systems . Meanwhile, he Hybrid-DRG reimbursement framework effective January 2024 is improving economic justification for premium modalities—particularly 3-D digital breast tomosynthesis (DBT)—in both hospital and outpatient settings.

Key Report Takeaways

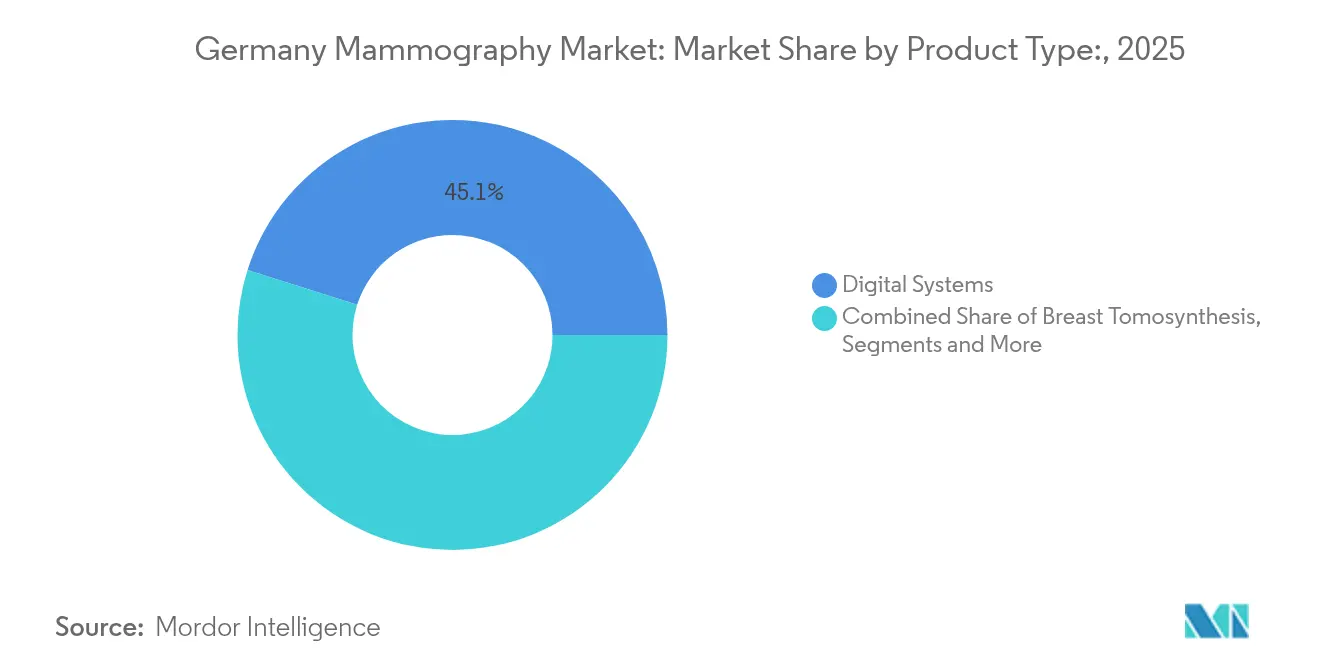

- By product type, digital systems led with 45.12% revenue share in 2025; breast tomosynthesis is forecast to expand at a 9.02% CAGR to 2031.

- By end user, hospitals accounted for 54.10% of the Germany mammography market share in 2025, while diagnostic imaging centres are advancing at a 9.19% CAGR through 2031.

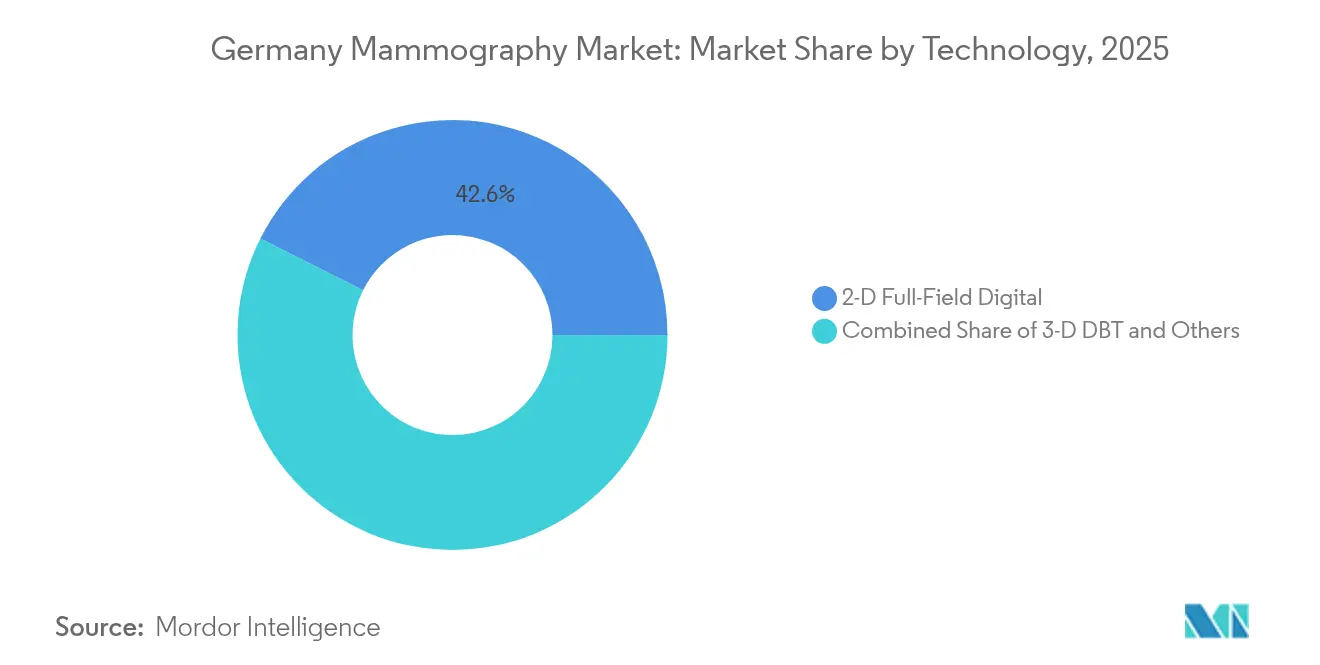

- By technology, 2-D full-field digital systems captured 42.60% share of the Germany mammography market size in 2025 and 3-D DBT is projected to grow at a 9.32% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of breast cancer | +1.8% | National, higher incidence in urban centers | Medium term (2-4 years) |

| National roll-out of AI-enabled screening programs | +2.1% | National, early adoption in tier-1 cities | Short term (≤ 2 years) |

| Increased reimbursement for digital breast tomosynthesis | +1.5% | National, varies by Länder | Medium term (2-4 years) |

| Rapid hospital digitization through KHZG funding | +2.3% | National, priority to rural and smaller hospitals | Short term (≤ 2 years) |

| Venture-backed fem-tech start-ups promoting self-referral | +0.9% | Urban centers, expanding to suburbs | Long term (≥ 4 years) |

| Expansion of mobile screening vans in rural Länder | +0.4% | Brandenburg, Sachsen, eastern states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Breast Cancer

Germany recorded 74,500 new breast cancer cases in 2022, making the disease the most common malignancy among German women [1]Robert Koch Institute, “Krebs – Brustkrebs,” krebsdaten.de. The 2024 extension of the national screening program to women aged 70-75 enlarges the eligible cohort by about 2 million, intensifying demand for mammography appointments across both urban and rural regions. Organized screening has already delivered up to a 40% mortality reduction among regularly screened participants. Yet participation still hovers at 51%, leaving a sizeable untapped market that vendors can address through outreach, mobile units, and AI-powered risk stratification tools. Hospitals and imaging centres that invest in patient-centric digital scheduling and educational campaigns are well positioned to capture this latent demand.

National Roll-Out of AI-Enabled Screening Programs

The PRAIM multicenter study covering 463,094 women demonstrated that AI support increased detection rates by 17.6% without inflating recall rates. As of 2025, at least a dozen screening sites nationwide have embedded AI triage into routine workflow, freeing radiologists to focus on complex reads while maintaining quality benchmarks. Berlin-based Vara now processes more than 80,000 studies each month, underscoring domestic capability to scale AI solutions quickly. Regulatory backing from the Federal Office for Radiation Protection further paves the way for AI applications in younger age brackets, suggesting that adoption curves could steepen beyond current forecasts. Vendors bundling AI with hardware upgrades are therefore able to offer a compelling total-solution narrative to both hospitals and outpatient centres.

Increased Reimbursement for Digital Breast Tomosynthesis

The Hybrid-DRG model introduced in January 2024 simplifies billing for advanced imaging, yielding clearer economics for DBT purchases. Coupled with the European Commission’s 2023 endorsement of DBT for organized screening, payers now view the modality as clinically justified and financially rational. Clinical studies show DBT can uncover up to 65% more invasive cancers than 2-D mammography, improving cost-effectiveness metrics over the long term. Nonetheless, the mandatory 30% state co-financing attached to KHZG grants can stretch the capital budgets of smaller hospitals, slowing uptake outside well-funded facilities. Vendors that offer flexible financing or service-as-a-subscription models can mitigate this barrier.

Rapid Hospital Digitization Through KHZG Funding

KHZG earmarks EUR 4 billion for hospital digitization, with strict 2025 milestones forcing providers to modernize imaging fleets quickly. Siemens Healthineers, through its Teamplay Digital Health Platform, already links more than 560 German clinics, offering plug-and-play integration for new breast imaging equipment. Hospitals must dedicate at least 15% of KHZG grants to cybersecurity, ensuring that new modalities meet stringent data-protection rules. Rural facilities receive prioritized funding, enabling a more balanced geographic deployment of advanced systems and narrowing diagnostic quality gaps between urban and rural regions. The compressed timeline keeps procurement pipelines active through 2025, supporting healthy order books for manufacturers.

Venture-Backed German Fem-Tech Start-Ups Promoting Self-Referral

AI-first start-ups such as Vara and Lunit-backed initiatives encourage women to self-refer for mammography by simplifying risk assessment and appointment booking, particularly in metropolitan areas. Their mobile-friendly portals and personalized reminders address the 49% of eligible women who currently skip biennial screening. Over time, these digital touchpoints are expected to expand into suburban clinics, lifting throughput at diagnostic imaging centres. While still early-stage, venture capital inflows ensure ongoing product refinements and marketing campaigns that could sustainably increase screening compliance.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-dose related patient apprehension | -1.2% | National, higher sensitivity in educated groups | Medium term (2-4 years) |

| Declining private insurance coverage for opportunistic screening | -0.8% | Urban centers with higher private insurance penetration | Short term (≤ 2 years) |

| Shortage of sub-specialized breast radiologists in tier-2 cities | -1.6% | Tier-2 cities and rural areas | Long term (≥ 4 years) |

| High capital cost versus DR-capable general X-ray alternatives | -1.1% | Smaller hospitals and diagnostic centres | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Radiation-Dose Related Patient Apprehension

Despite modern devices lowering mean glandular dose to between 1-10 mGy, over-estimation of radiation risk keeps some women from attending screening exams. Younger, university-educated cohorts are especially cautious, demanding detailed dose disclosures and safety assurances. Vendors are responding with low-dose protocols and dose-tracking dashboards that clinicians can share during consultations. Educational campaigns anchored in transparent risk-benefit messaging have proven effective in closing the perception gap, but they require sustained funding from insurers and public-health agencies to maintain momentum.

Declining Private Insurance Coverage for Opportunistic Screening

Several private insurers tightened reimbursement criteria in late 2024, reducing coverage for women outside the organized screening age band. This policy shift is most visible in affluent urban districts where private insurance penetration is highest. As a result, opportunistic screening volumes have softened, pressuring imaging centres that relied on self-paid mammography. Centres are pivoting toward corporate wellness contracts and bundled DBT packages to offset revenue loss, yet near-term headwinds remain.

Shortage of Sub-Specialised Breast Radiologists in Tier-2 Cities

A 2025 EU-REST survey confirmed that Germany faces critical shortages of breast-trained radiologists outside tier-1 cities, limiting advanced modality uptake in those regions [2]Andreas Böckler, “Current status of radiologist staffing, education and training in the 27 EU Member States,” PMC, pmc.ncbi.nlm.nih.gov . Without sufficient specialists, hospitals delay DBT adoption because the technology’s diagnostic gains rely on nuanced interpretation. Teleradiology could bridge the gap, but only 20% of referring physicians currently leverage it due to workflow and IT hurdles. Unless training pipelines and tele-imaging infrastructure improve, equipment vendors may see uneven order patterns across the country.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Leadership Drives Market Evolution

Digital systems contributed USD 62.21 million to revenue in 2025 and captured 45.12% of the Germany mammography market share, underscoring the wholesale transition away from film-screen and CR platforms. Breast tomosynthesis, while still a smaller category, is projected to clock a 9.02% CAGR through 2031 thanks to guidelines that place DBT on par with 2-D mammography for organized screening reimbursement. Analog systems continue to phase out as KHZG grants encourage IT-connected modalities that feed directly into electronic health records.

Manufacturers now bundle AI computer-aided detection (CAD) suites with hardware sales, increasing deal sizes and differentiating offerings in competitive tenders. Siemens Healthineers’ MAMMOMAT B.brilliant, cleared by the FDA in 2024, showcases titanium contrast-enhanced mammography and wide-angle tomosynthesis for dense-breast visualization. As payers reward better sensitivity and specificity metrics, providers see stronger ROI in premium systems. The Germany mammography market continues to favor platforms that integrate seamlessly with hospital RIS-PACS environments, comply with MDR 2017/745, and deliver cybersecurity measures aligned with KHZG rules.

By End User: Hospital Dominance Faces Outpatient Challenge

Hospitals generated more than half of modality revenues in 2025, leveraging KHZG capital budgets and comprehensive care pathways to maintain leadership. Diagnostic imaging centres, however, are expanding at a 9.19% CAGR as patients gravitate toward shorter wait times, boutique environments, and flexible evening appointments. The Germany mammography market size for outpatient providers is rising as corporate wellness contracts and self-referral apps funnel new clientele into specialized centres.

Mobile screening units and tele-imaging platforms form the “Others” category and represent a strategic lever for reaching rural populations where hospital density is low. Rigorous certification by the German Cancer Society ensures that quality remains uniform across all settings, compelling imaging centres to adopt the same dose-reduction and reporting standards as university hospitals. Competitive differentiation therefore hinges on patient-experience enhancements such as same-day results, personalized risk reports, and AI-curated follow-up schedules.

By Technology: 3-D DBT Transforms Imaging Standards

2-D full-field digital systems still own 42.60% of installed base units, but their leadership is likely to erode as 3-D DBT accelerates at a 9.32% CAGR through 2031. DBT’s ability to reduce recall rates while detecting smaller invasive lesions in dense breasts delivers tangible clinical gains, meeting both payer and provider objectives. Reading-time reductions of up to 30% when AI-enabled slabbing is applied make DBT financially attractive even in resource-constrained settings.

Emerging modalities such as contrast-enhanced mammography and molecular breast imaging reside in the “Others” segment and are beginning to secure MDR approvals. Although their current penetration is small, these technologies offer future pathways for centres seeking to differentiate services further. Vendors that deliver a modular upgrade path—allowing customers to toggle between 2-D, DBT, and contrast modes—stand to capture multiyear replacement cycles while preserving installed-base loyalty within the Germany mammography industry.

Geography Analysis

Germany’s national mammography program now serves an eligible cohort of 13 million women aged 50-75, reflecting the July 2024 inclusion of those aged 70-75 and reinforcing procedure volume across the Germany mammography market. Urban regions such as Berlin, Munich, and Hamburg account for more than 55% of screening appointments, mirroring population density and proximity to academic cancer centers. The Germany mammography market size linked to these tier-1 cities is expected to expand at 8.78% CAGR through 2031 as hospitals automate scheduling and integrate AI triage to manage rising throughput. Screening participation stands at 58% in Bavaria—Germany’s highest—while Berlin records 47%, underscoring the need for targeted outreach programs that harmonize uptake across Länder. The expansion of diagnostic capacity in metropolitan hubs sets the technology adoption tempo for the entire Germany mammography market.

Rural Länder receive priority access to KHZG grants, channeling capital toward digitized equipment and mobile screening units that close the urban-rural quality gap. Brandenburg and Sachsen together added 11 mobile DBT vans in 2025, lifting rural coverage and adding roughly 120,000 annual exams to the Germany mammography market. Eastern states still trail national averages in specialist density, but tele-imaging hubs in Leipzig and Dresden now route 30% of reads to university radiologists, alleviating workforce shortages. These developments illustrate how localized funding and telemedicine can lift the Germany mammography market, particularly where physical infrastructure was historically limited.

Innovation clusters in Bavaria and Baden-Württemberg attract both start-ups and multinational vendors, generating a feedback loop of piloting, regulatory feedback, and early adoption that diffuses nationwide. Berlin-based fem-tech firms leverage the capital’s digital-health community to promote self-referral apps, pushing incremental procedure growth into neighboring Brandenburg and Mecklenburg-Vorpommern. The Germany mammography market size derived from AI-enabled reads reached USD 21.84 million in 2025 and is forecast to cross USD 63.75 million by 2031, with half of that growth attributable to software subscriptions deployed first in these innovation hubs. Geography therefore shapes procurement priorities, reimbursement negotiations, and patient-engagement strategies that collectively steer the Germany mammography market toward uniform standards of care.

Competitive Landscape

The Germany mammography market features a quartet of multinationals—Siemens Healthineers, Hologic, GE HealthCare, and Philips—collectively controlling an estimated 72% of installed modalities in 2025 [3]Siemens Healthineers, “Siemens Healthineers off to a strong start in fiscal year 2025,” siemens-healthineers.com. Siemens Healthineers leverages its domestic footprint and Teamplay Digital Health Platform to bundle equipment, AI, and cybersecurity services, an approach aligned with KHZG funding criteria. Hologic differentiates through contrast-guided biopsy add-ons that integrate with its DBT scanners, while GE HealthCare’s collaboration with RadNet accelerates SmartTechnology rollouts that embed AI risk scoring at the console. Philips focuses on cloud-hosted enterprise imaging that eases data sharing across hospital networks, appealing to providers consolidating radiology services.

Domestic innovators are reshaping competitive dynamics within the Germany mammography market. Vara processes 80,000 mammograms per month on its cloud-native AI platform and secured USD 8.9 million in Series A funding to target new European sites. Lunit signed a 2025 framework agreement with Starvision Service GmbH to deploy AI decision support across the network’s 60 radiology practices, signaling that software-only entrants can achieve rapid scaling without hardware dependencies. These strategic moves illustrate how agile fem-tech and AI specialists carve out share in the Germany mammography market by lowering the adoption barrier for advanced analytics.

Merger-and-acquisition activity intensifies as incumbents seek to own end-to-end workflows. RadNet’s USD 103 million acquisition of iCAD expands AI intellectual property that can be integrated into GE or Hologic scanner fleets. Siemens Healthineers gained FDA clearance for the MAMMOMAT B.brilliant system that features titanium contrast and 50° wide-angle tomosynthesis, enhancing premium product positioning. Collectively, these maneuvers ensure that the Germany mammography market remains innovation-driven, forcing both large and small vendors to update portfolios in cadence with AI performance benchmarks and reimbursement shifts.

Germany Mammography Industry Leaders

Canon Inc. (Canon Medical Systems Corporation)

GE Healthcare

Koninklijke Philips NV

Fujifilm Holdings Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lunit entered a strategic partnership with Starvision Service GmbH to roll out its AI imaging suite across Germany’s largest private radiology network.

- January 2025: The PRAIM study led by Vara and the University of Lübeck confirmed a 17.6% cancer-detection uplift from AI-integrated screening workflows.

- November 2024: Vara raised USD 8.9 million to fund European and Indian expansion of its AI mammography platform.

Germany Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. Germany Mammography Market is Segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End User (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Breast Tomosynthesis |

| Analog Systems |

| Computer-Aided Detection (CAD) Software |

By End User

| Hospitals |

| Diagnostic Imaging Centres |

| Others |

By Technology

| 2-D Full-Field Digital |

| 3-D DBT |

| Others |

| By Product Type | Digital Systems |

| Breast Tomosynthesis | |

| Analog Systems | |

| Computer-Aided Detection (CAD) Software | |

| By End User | Hospitals |

| Diagnostic Imaging Centres | |

| Others | |

| By Technology | 2-D Full-Field Digital |

| 3-D DBT | |

| Others |

Key Questions Answered in the Report

How big is the Germany Mammography Market?

The Germany Mammography Market size is expected to reach USD 149.94 million in 2026 and grow at a CAGR of 8.76% to reach USD 228.19 million by 2031.

What CAGR is forecast for breast imaging equipment sales in Germany to 2031?

Revenue across the German breast imaging market is projected to rise at an 8.76% CAGR through 2031.

Who are the key players in Germany Mammography Market?

Canon Inc. (Canon Medical Systems Corporation), GE Healthcare, Koninklijke Philips NV, Fujifilm Holdings Corporation and Siemens Healthineers AG are the major companies operating in the Germany Mammography Market.

Which product category is growing fastest within Germany?

Breast tomosynthesis systems are expected to post a 9.02% CAGR, outpacing all other modalities.

Page last updated on: