Nerve Repair And Regeneration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

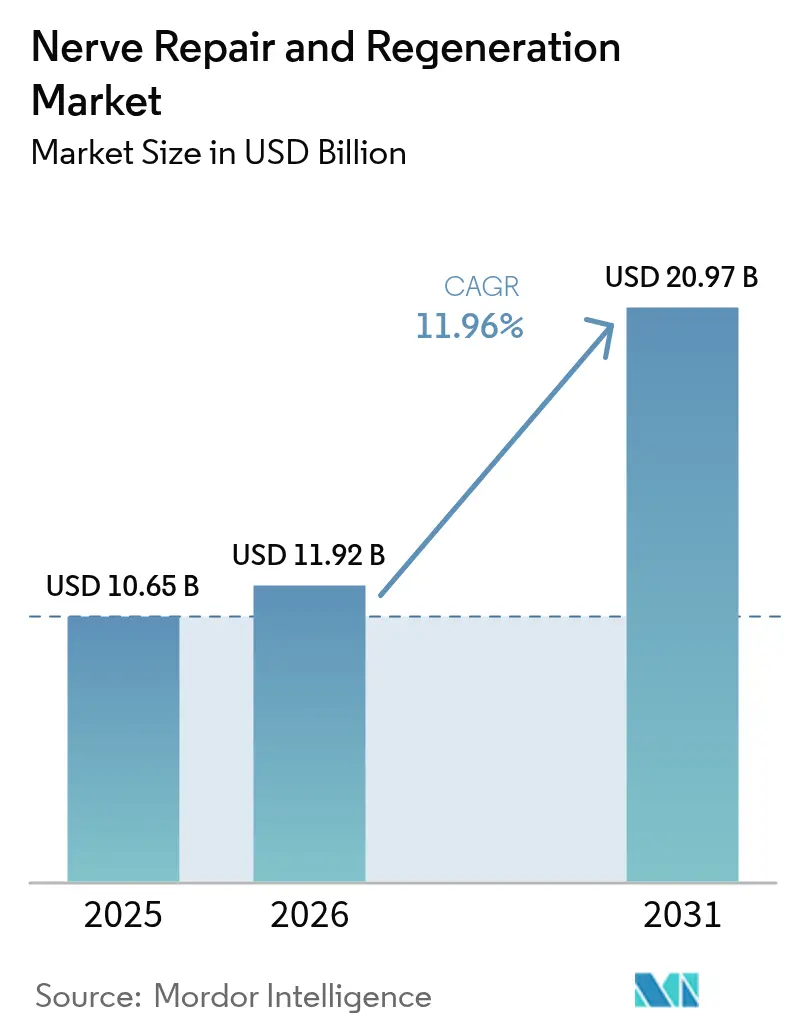

| Market Size (2026) | USD 11.92 Billion |

| Market Size (2031) | USD 20.97 Billion |

| Growth Rate (2026 - 2031) | 11.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nerve Repair And Regeneration Market Analysis by Mordor Intelligence

The nerve repair and regeneration market size is expected to grow from USD 10.65 billion in 2025 to USD 11.92 billion in 2026 and is forecast to reach USD 20.97 billion by 2031 at 11.96% CAGR over 2026-2031. Continued progress in bioelectronic medicine, the growing burden of neurological disorders, and supportive public funding anchor this expansion. AI-enabled closed-loop neurostimulation, 3D-bioprinted patient-specific nerve grafts, and real-time brain-signal monitoring systems are reshaping clinical practice from reactive procedures to precision-guided regeneration. Intensifying adoption of these innovations reveals fresh opportunities across both device and biomaterial categories inside the nerve repair and regeneration market. Demand is reinforced by a demographic shift toward aging populations that experience more diabetes-linked peripheral neuropathies and by increasing battlefield and industrial traumas that require advanced reconstruction therapies. Robust reimbursement in North America, large untapped patient pools in Asia-Pacific, and deep venture funding for emerging biotechnology firms together underpin the global growth outlook.

Key Report Takeaways

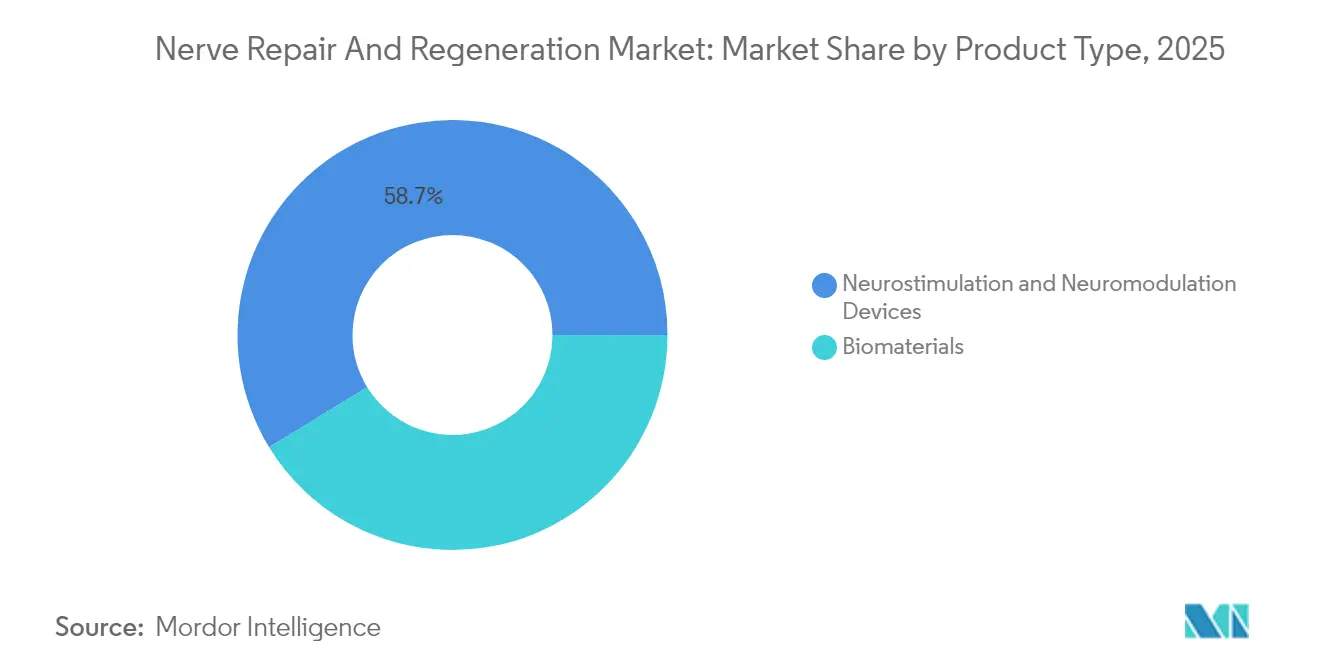

- By product type, neurostimulation and neuromodulation devices held 58.74% of nerve repair and regeneration market share in 2025, while biomaterials are forecast to grow at 14.01% CAGR through 2031.

- By application, traditional neuro-stimulation surgeries captured 42.98% revenue in 2025; stem-cell therapy is projected to expand at an 18.54% CAGR to 2031.

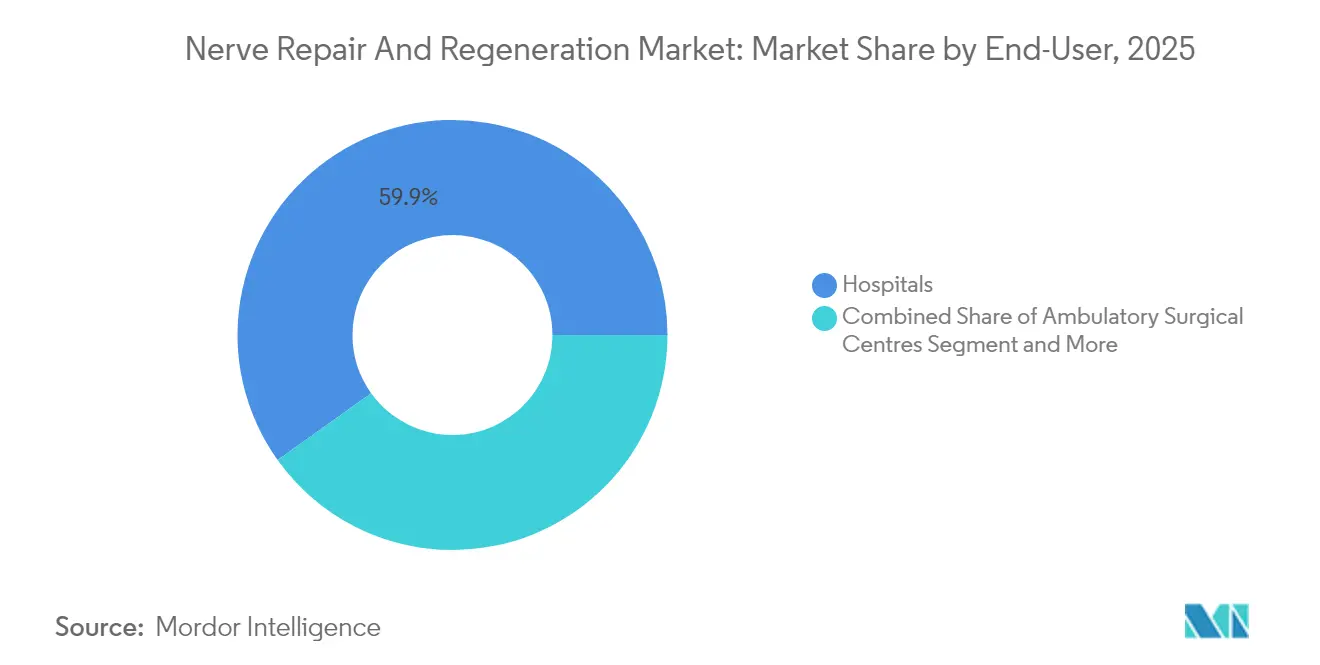

- By end-user, hospitals commanded 59.88% of the nerve repair and regeneration market size in 2025, while ambulatory surgical centers are advancing at 14.29% CAGR through 2031.

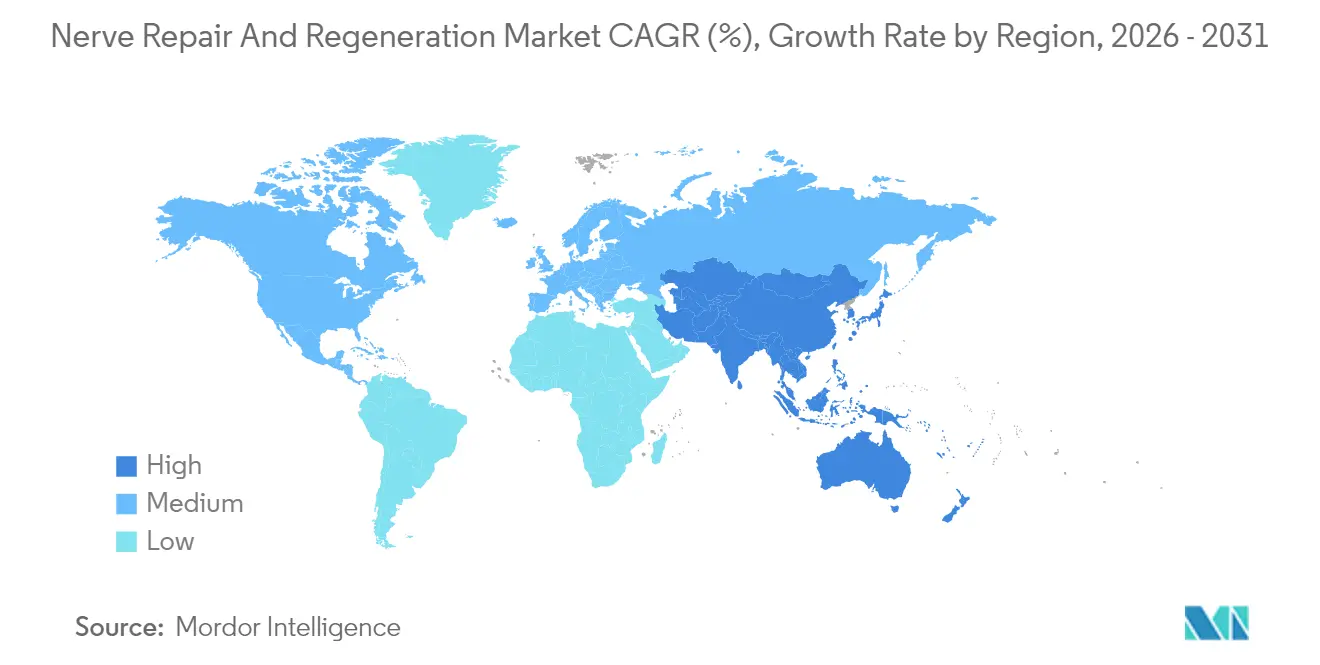

- By geography, North America led with 41.35% revenue share in 2025; Asia-Pacific posts the fastest regional CAGR at 12.45% during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nerve Repair And Regeneration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Incidence Of Nerve Injuries & Neurological Disorders | +2.8% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Technological Advances In Neuro-Modulation & Biomaterials | +3.2% | Global, led by North America & Asia-Pacific | Long term (≥ 4 years) |

| Rising Healthcare Expenditure & Favourable Reimbursement | +2.1% | North America & Europe primarily | Short term (≤ 2 years) |

| AI-Enabled Closed-Loop Bio-Electronic Medicine Adoption | +1.9% | North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Military & Elite-Sports Funding For Peripheral-Nerve Repair | +0.8% | North America, with spillover to allied nations | Medium term (2-4 years) |

| 3-D Bioprinted, Patient-Specific Nerve Graft Breakthroughs | +1.4% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence Of Nerve Injuries & Neurological Disorders

Upper-extremity nerve injuries affect 43.8 per million people annually in the United States, with average charges of USD 47,004 per case. Diabetes-linked peripheral neuropathy and age-related neurodegeneration further enlarge the candidate pool for regenerative interventions. The burden extends beyond acute trauma to long-term disability, pushing health systems to embrace earlier nerve reconstruction. Military conflicts and industrial accidents keep peripheral nerve trauma on policy agendas, while better understanding of nerve pathophysiology broadens eligibility for advanced therapies. Collectively these patterns expand the addressable population in the nerve repair and regeneration market.

Technological Advances In Neuro-Modulation & Biomaterials

Medtronic’s Percept RC neurostimulator captures real-time brain signals and personalizes therapy delivery[1]Medtronic plc, “FDA approves Medtronic Percept RC neurostimulator with BrainSense technology,” medtronic.com. Closed-loop control represents a shift from static to dynamic intervention, potentially improving outcomes and lowering adverse events. Concurrently, 3D-bioprinted chitosan conduits embedded with neurotrophin-3 create bionic microenvironments for peripheral repair. Conductive silk-fibroin scaffolds combined with electrical stimulation have surpassed traditional guides in preclinical recovery metrics. These breakthroughs position biomaterials as a regeneration-first alternative, signalling a major product-mix shift inside the nerve repair and regeneration market.

Rising Healthcare Expenditure & Favourable Reimbursement

Direct outlays on brain disorders reached USD 1.14 trillion worldwide and USD 409 billion in the United States in 2025[2]Aj Mitchell et al., “Economic Impact of Brain Disorders,” Neurology, neurology.org. Medicare and private payers now cover spinal cord stimulation for conditions such as diabetic peripheral neuropathy, broadening patient access. The National Institute of Neurological Disorders and Stroke budgeted USD 2.833 billion in 2025 for gene-based and device research. Enhanced coverage, coupled with rising per-capita spending, immediately accelerates revenue realization in the nerve repair and regeneration market.

AI-Enabled Closed-Loop Bio-Electronic Medicine Adoption

Adaptive systems adjust stimulation up to 50 times per second based on biologic feedback, improving precision therapy. Wireless optogenetic microsystems link artificial intelligence with real-time circuit modulation to speed research translation. Integration with multimodal large language models under development could refine algorithmic adjustment for complex conditions such as post-traumatic stress disorder. These digital therapies signal a future in which personalized neuro-regeneration becomes a routine care pathway in the nerve repair and regeneration market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Implants & Procedures | -1.8% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Dearth Of Trained Neurosurgeons & Rehab Specialists | -1.2% | Global, acute in Asia-Pacific & developing regions | Medium term (2-4 years) |

| Medical-Grade Polymer (Chitosan, PTFE) Supply Constraints | -0.7% | Global, supply chain dependent regions | Short term (≤ 2 years) |

| Cyber-Security & Data-Privacy Risks In Connected Implants | -0.9% | Developed markets with high connectivity adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost Of Implants & Procedures

Spinal cord stimulators range from USD 20,000 to USD 50,000 per implant, excluding surgical expenses, and lifetime costs can surpass USD 100,000 even in insured regions. Supply chain shortages in medical-grade components have inflated prices and elongated lead times. High up-front costs dampen early adoption in low-resource settings and slow diffusion of advanced technologies in the nerve repair and regeneration market.

Cyber-Security & Data-Privacy Risks In Connected Implants

Section 524B of the Federal Food, Drug and Cosmetic Act requires premarket cyber risk mitigation strategies for implantable devices[3]Food and Drug Administration, “Premarket Cybersecurity Guidance,” federalregister.gov. Potential malicious manipulation of stimulation parameters or patient data exposure can undermine clinician and consumer confidence. Manufacturers must invest in encryption, firmware updates, and secure over-the-air communication. These requirements add cost and delay product launches, imposing a structural restraint on the nerve repair and regeneration market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biomaterials Accelerate Despite Device Dominance

Neurostimulation and neuromodulation devices accounted for 58.74% of the nerve repair and regeneration market share in 2025, powered by extensive clinical evidence, surgeon familiarity, and established reimbursement channels. Within the same year, biomaterials began reshaping demand patterns through scaffold-free conduits derived from autologous fibroblasts that passed early human safety benchmarks. The nerve repair and regeneration market size tied to biomaterials is expected to grow at 14.01% CAGR, riding on 3D-printing that fabricates patient-specific grafts and chitosan conduits delivering controlled neurotrophic factors.

Internal neurostimulators dominate revenue with higher average selling prices and preferred indications like chronic neuropathic pain, Parkinson’s disease, and spinal injury. External stimulators, including transcranial magnetic and trans-cutaneous electrical devices, post steady uptake in rehabilitation therapy. Conductive silk-fibroin scaffolds loaded with gold nanoparticles are yielding superior axonal growth in preclinical work, hinting at future substitution potential for traditional leads. As cost curves of biofabrication decline and clinical data matures, biomaterials are poised to transform long-term product mix inside the nerve repair and regeneration market.

By Application: Stem-Cell Therapy Disrupts Traditional Paradigms

Conventional neuro-stimulation surgeries held 42.98% of 2025 revenue, underscoring their entrenched role as the workhorse intervention for chronic pain and movement disorders. Direct neurorrhaphy and nerve grafting continue as standards for acute gaps yet face donor-site morbidity and limited graft length. In contrast, stem-cell therapy posts the fastest 18.54% CAGR, reflecting mounting trial successes such as mesenchymal stem cells delivering one-grade motor improvements in 60% of cervical spinal injury cases.

The nerve repair and regeneration market size attributable to stem-cell therapy is expected to expand exponentially as long-term safety data accumulate. Olfactory ensheathing cell transplantation has moved into first-in-human trials with USD 8.5 million funding and regulatory support in Australia. Neural stem cell infusions for chronic spinal lesions showed sustained benefits over five years without serious adverse events. These findings support a rising shift away from implantable hardware toward biologic reconstruction, rewriting competitive playbooks within the nerve repair and regeneration market.

By End-User: Ambulatory Centers Challenge Hospital Dominance

Hospitals captured 59.88% of 2025 revenue owing to integrated operating theaters, imaging, and specialist teams that manage complex neurosurgical cases. Ambulatory surgical centers, however, are the fastest-growing venue at 14.29% CAGR as minimally invasive devices allow same-day discharge and lower facility fees. Medicare and commercial insurers increasingly reimburse spinal cord stimulation in outpatient settings, encouraging shift of volume outside tertiary centers.

Closed-loop stimulators with longer battery life and wireless programming reduce follow-up visits, a key driver for ambulatory adoption. Stand-alone pain clinics are also expanding implantation capabilities, capturing referrals with quicker scheduling and transparent cost packages. The nerve repair and regeneration market is therefore recalibrating across the care continuum, with hospitals focusing on complex revisions while ambulatory centers build critical mass in routine procedures.

Geography Analysis

North America retained 41.35% revenue share in 2025 on the back of advanced insurance coverage, deep clinical trial density, and continuous public R&D investment such as the USD 2.833 billion NINDS budget. Military research through DARPA’s Bridging the Gap Plus program and the USD 650 million Military Burn Research Program further accelerates innovation in peripheral nerve repair. Canada adds incremental growth via universal health benefits that support equitable access, and Mexico improves cross-border procedure volumes through medical tourism packages. Cybersecurity regulation from the FDA shapes device certification standards and influences global export success.

Asia-Pacific is forecast to deliver a 12.45% CAGR, the highest regional pace, propelled by large patient pools and active government promotion of brain-computer interfaces. China’s National Healthcare Security Administration formally recognized neural care services, paving the way for scaled reimbursement. Japan contributes sophisticated engineering and an aging demographic with high neurological disease prevalence. India advances through private hospital expansion and lower-cost procedural pricing that attract regional medical tourism. Australia’s world-first olfactory ensheathing cell trial positions the country as a translational research hub.

Europe maintains solid share through coordinated healthcare systems and device adoption. Germany leverages industrial design strengths, while the United Kingdom spearheads early-stage stem-cell studies. Regulatory harmonization under the Medical Device Regulation streamlines continental approvals, speeding dissemination of next-gen implants. Middle East and Africa begin scaling high-acuity centers in urban corridors, though limited specialist availability caps penetration. South America exhibits steady improvements as Brazil and Argentina allocate more budget to neurological care, ensuring that the nerve repair and regeneration market continues its global diffusion.

Competitive Landscape

The nerve repair and regeneration industry shows moderate consolidation as legacy multinationals guard neurostimulation franchises while nimble biotechs pursue regenerative breakthroughs. Medtronic, Boston Scientific, and Abbott hold entrenched portfolios, exclusive distribution, and large sales forces that underpin global reach. These leaders invest heavily in adaptive algorithms and cloud-based monitoring that wrap hardware into data-rich care platforms. Boston Scientific’s entry-level cordless products target outpatient centers, while Medtronic’s adaptive brain pacemaker for Parkinson’s delivers on closed-loop promise.

Scaling opportunities emerge in patient-specific biomaterials and stem-cell processing. Axogen’s Avance Nerve Graft pursued FDA biologics licensure and posted 17.4% revenue growth in Q1 2025. Auxilium Biotechnologies enrolled its first patient in the NeuroSpan Bridge trial, indicating momentum for scaffold-based solutions. Partnerships between material scientists, software engineers, and device manufacturers proliferate, aiming to provide end-to-end regeneration ecosystems rather than single components.

Competitive advantage is shifting toward integrated platforms that align implantable stimulators, AI analytics, and regenerative adjuvants. Players lacking software expertise risk commoditization as reimbursement increasingly links payment to functional outcomes and data transparency. Supply chain resilience and cybersecurity compliance now weigh heavily in procurement decisions. Consequently, the nerve repair and regeneration market rewards companies that blend regulatory mastery, cross-disciplinary R&D, and robust digital infrastructure.

Nerve Repair And Regeneration Industry Leaders

Abbott Laboratories

Axogen Corporation

Boston Scientific Corporation

Integra LifeSciences Corporation

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Auxilium Biotechnologies enrolled the first patient in its NeuroSpan Bridge trial evaluating scaffold-based peripheral nerve regeneration.

- February 2025: The FDA approved Medtronic’s adaptive brain pacemaker for Parkinson’s featuring real-time adjustment that cut involuntary movements by 50% in trials.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the nerve repair and regeneration market as all approved devices and biomaterials that restore, replace, or electrically stimulate injured peripheral or central nerves, including internal and external neurostimulation systems, nerve conduits, wraps, protectors, and connectors, as well as autograft-substitute biomaterials and adjunct regenerative therapies.

Scope exclusion: spinal fusion biologics, pure pain-management drugs, and basic wound dressings are outside our number set.

Segmentation Overview

- By Product Type

- Neurostimulation & Neuromodulation Devices

- Internal Neurostimulation Devices

- Spinal Cord Stimulation (SCS)

- Deep Brain Stimulation (DBS)

- Vagus Nerve Stimulation (VNS)

- Sacral Nerve Stimulation (SNS)

- Gastric Electrical Stimulation (GES)

- External Neurostimulation Devices

- Trans-cutaneous Electrical Nerve Stimulation (TENS)

- Trans-cranial Magnetic Stimulation (TMS)

- Internal Neurostimulation Devices

- Biomaterials

- Nerve Conduits

- Nerve Protectors

- Nerve Connectors

- Other Biomaterials

- Neurostimulation & Neuromodulation Devices

- By Application

- Neuro-stimulation & Neuro-modulation Surgeries

- Direct Nerve Repair / Neurorrhaphy

- Nerve Grafting

- Stem-Cell Therapy

- Other Applications

- By End-User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Neurology & Orthopaedic Clinics

- Rehabilitation Centres

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed neurosurgeons, trauma orthopedists, bio-engineers, and procurement managers across North America, Europe, and key Asia-Pacific hubs. These discussions verified real-world ASP dispersion, uptake lags after approvals, and emerging stem-cell protocol penetration, which in turn refined our model multipliers and scenario weights.

Desk Research

We begin by collating publicly available datasets such as U.S. FDA 510(k) clearances, European MDR notified-body listings, UN Comtrade code 902190 import-export lines, and procedure volumes from the Agency for Healthcare Research & Quality. Association portals, for example, the American Association of Neurological Surgeons and EFORT, provide incidence curves that ground our addressable patient pool. Company 10-Ks and device registries then supply selling price corridors, while paid files from D&B Hoovers and Dow Jones Factiva help us gauge vendor-level revenue splits.

Patent family trends on Questel, peer-reviewed outcome studies, and national ministries of health tariff books sharpen unit counts and reimbursement ceilings. The sources cited above are illustrative; many additional outlets were reviewed for corroboration and clarity.

Market-Sizing & Forecasting

A top-down incidence-to-treatment build starts with regional nerve-injury prevalence, surgery rates, and neuromodulation candidacy, which are then multiplied by validated ASP corridors. Results are cross-checked with a bottom-up roll-up of leading supplier revenues and sampled hospital purchase orders before final adjustment. Critical variables in our workbook include diabetes-linked neuropathy prevalence, trauma admissions, neuromodulation reimbursement policies, median device replacement cycles, and biomaterial adoption curves. Five-year forecasts employ multivariate regression blended with ARIMA smoothing, and coefficients are stress-tested through expert consensus workshops. Data gaps where supplier granularity is thin are bridged by cautiously interpolating shipment records and price bands from customs data.

Data Validation & Update Cycle

Outputs undergo variance screens versus historical series and independent trackers; anomalies trigger re-interviews and senior review. Reports refresh each year, with mid-cycle amendments when recalls, major approvals, or reimbursement shocks occur. A last-mile analyst pass ensures clients receive the latest view.

Why Mordor's Nerve Repair And Regeneration Baseline commands reliability

Published values often diverge because firms pick dissimilar product mixes, base years, and refresh cadences.

Key gap drivers here include exclusion of external stimulators by some publishers, unadjusted 2022 currency bases, and optimistic biomaterial penetration assumed without hospital-level checks, whereas Mordor's scope, live primary inputs, and yearly recalibration keep our figure balanced.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.65 B (2025) | Mordor Intelligence | |

| USD 6.5 B (2022) | Global Consultancy A | older base year, narrower product basket, no currency update to 2025 |

| USD 9.1 B (2023) | Industry Journal B | revenue sample lacking biomaterials ASP validation, limited primary checks |

The comparison shows that while other publishers offer useful snapshots, their totals swing widely once scope, timing, and validation rigor are equalized. By anchoring estimates to transparent variables, live expert feedback, and annual refreshes, Mordor provides decision-makers with a dependable starting point for strategy.

Key Questions Answered in the Report

What is the projected value of the nerve repair and regeneration market in 2031?

The market is forecast to reach USD 20.97 billion by 2031 driven by a 11.96% CAGR.

Which product category currently leads global revenue?

Neurostimulation and neuromodulation devices held 58.74% share in 2025.

Why are biomaterials growing faster than devices?

Patient-specific 3D-printed conduits and conductive scaffolds foster true tissue regeneration, pushing biomaterials at a 14.01% CAGR.

Which region promises the fastest growth?

Asia-Pacific is projected to expand at 12.45% CAGR through 2031 due to large patient populations and proactive government programs.

How is reimbursement influencing market adoption?

Expanded Medicare and private insurance coverage for spinal cord stimulation and outpatient implants supports faster utilization in high-income countries.

What emerging therapy shows the highest CAGR?

Stem-cell therapy leads with an 18.54% CAGR, supported by improving safety and efficacy data.

Page last updated on: