Nebulizer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

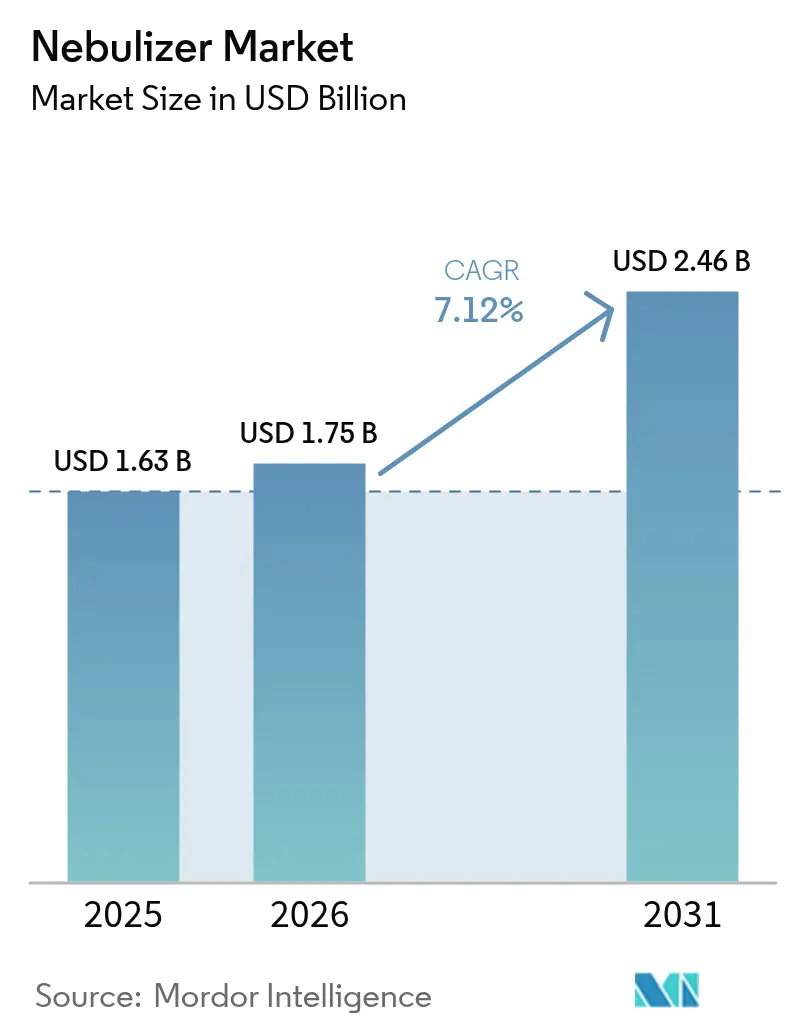

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nebulizer Market Analysis by Mordor Intelligence

The nebulizer market size was valued at USD 1.63 billion in 2025 and estimated to grow from USD 1.75 billion in 2026 to reach USD 2.46 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Robust demand stems from the steady rise in chronic respiratory cases, rapid uptake of home-care respiratory devices, and continued breakthroughs in mesh technology that shrink drug waste and accelerate treatment cycles. Manufacturers are expanding connected-care offerings that pair nebulizers with cloud dashboards, giving providers real-time adherence data that help curb costly hospital readmissions. Competitive intensity is rising as device makers race to secure patents around MEMS-based mesh plates, yet the market rewards firms that wrap robust drug-delivery performance into user-friendly, portable form factors. Geographically, North America anchors revenue, while Asia-Pacific supplies the strongest incremental growth on the back of pollution-driven disease incidence and government investment in primary care infrastructure.

Key Report Takeaways

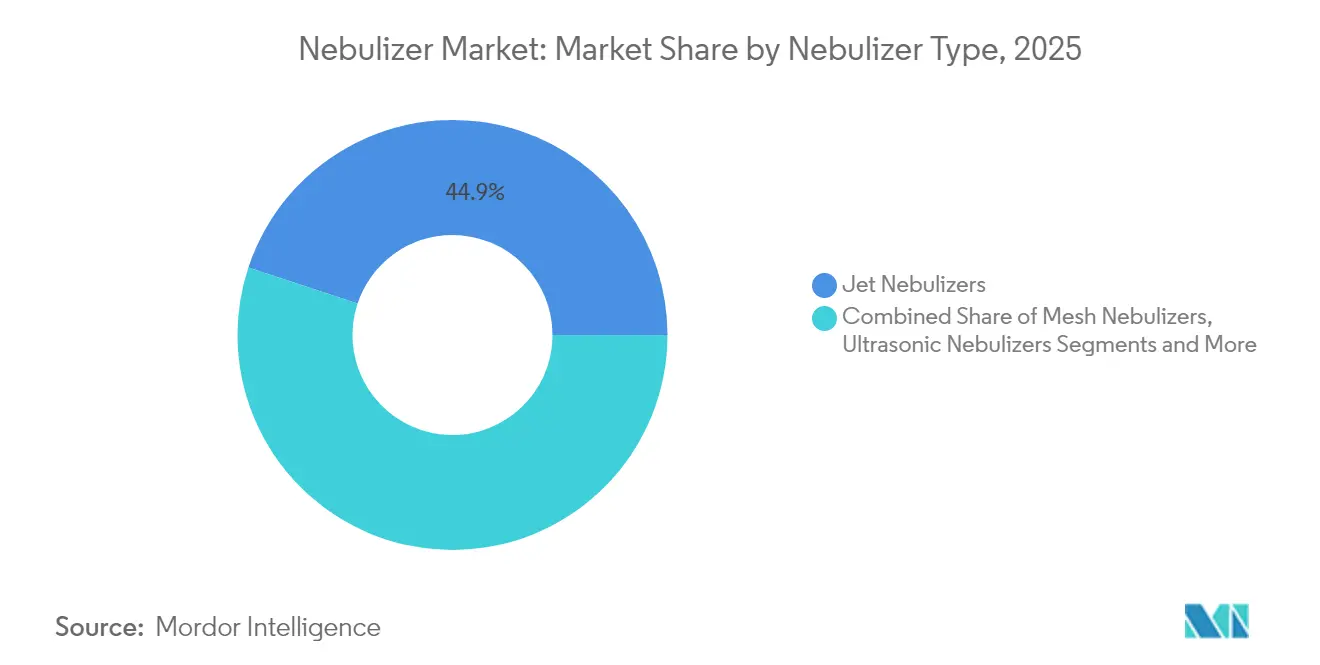

- By nebulizer type, jet nebulizers led with 44.92% of the nebulizer market share in 2025, while mesh nebulizers are projected to expand at an 11.02% CAGR through 2031.

- By portability, table-top units commanded 50.84% share of the nebulizer market size in 2025, whereas handheld and portable models are advancing at a 10.56% CAGR.

- By sales channel, direct institutional purchases accounted for 47.05% of the nebulizer market size in 2025; online retail exhibits the highest projected CAGR at 9.62% through 2031.

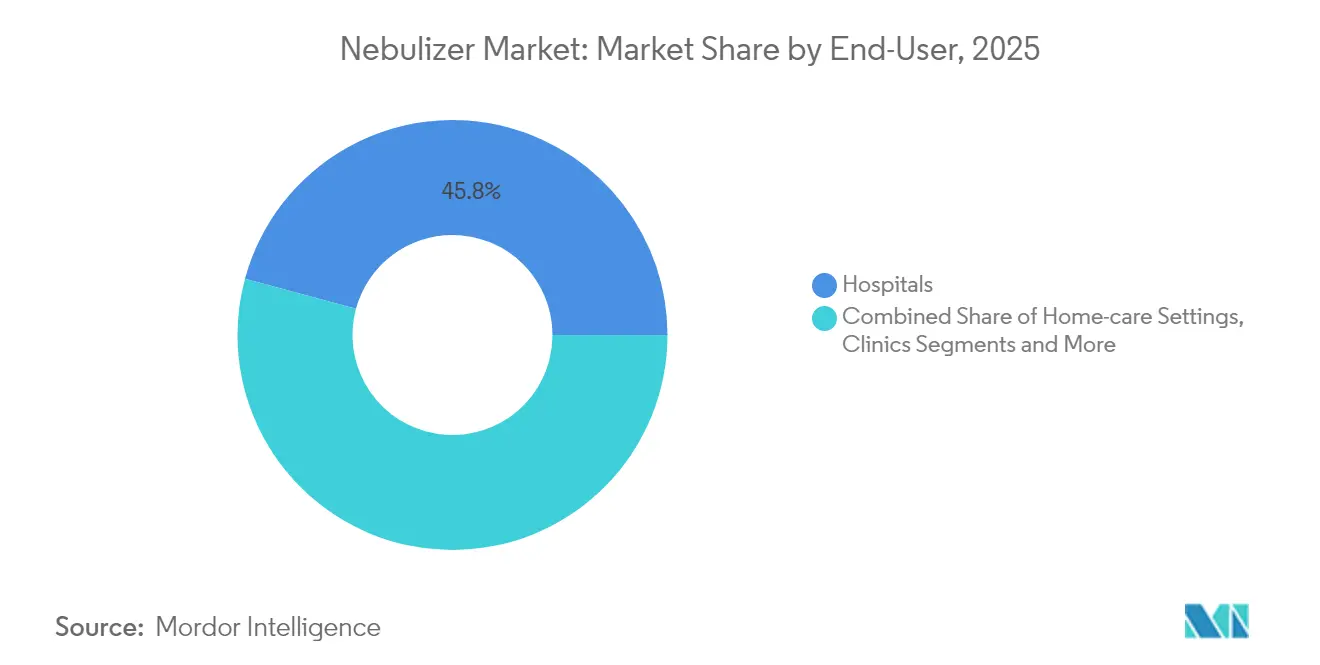

- By end-user, hospitals held 45.78% of the nebulizer market share in 2025 and home-care settings are forecast to expand at a 10.29% CAGR up to 2031.

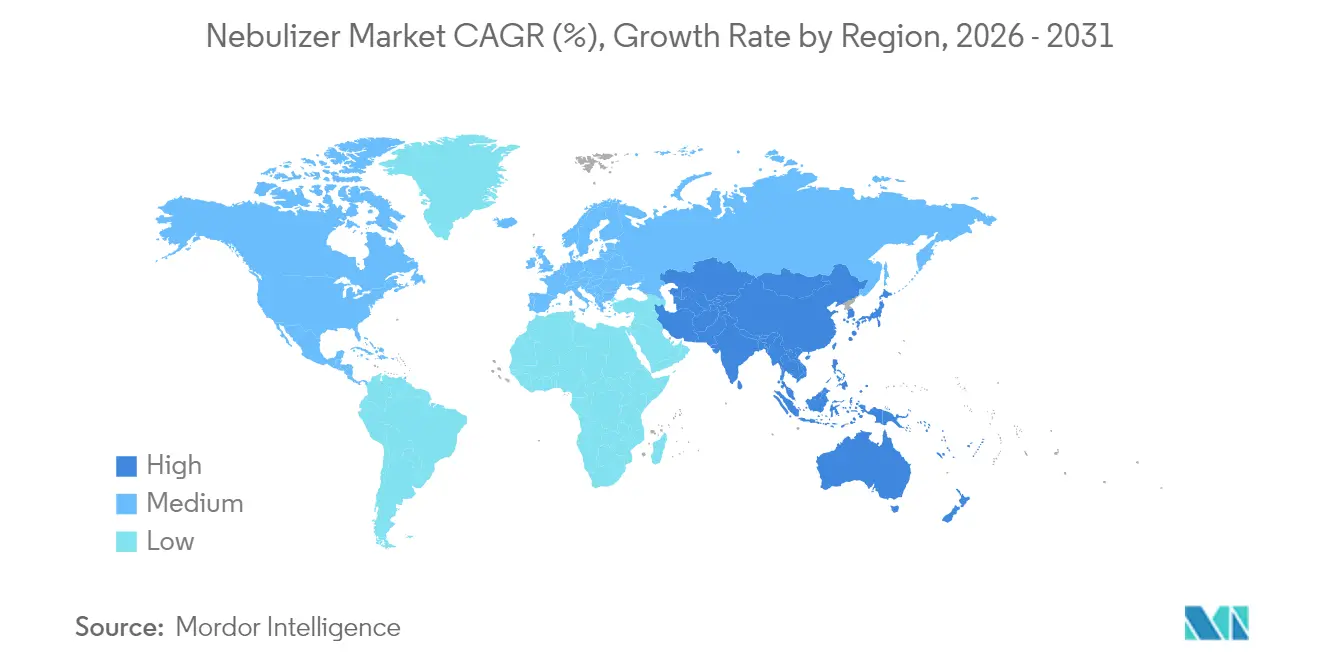

- By geography, North America captured 38.11% of the nebulizer market share in 2025, while Asia-Pacific is poised to post a 9.51% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Nebulizer Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic respiratory diseases | +2.1% | Global with focus on APAC urban clusters | Medium term (2-4 years) |

| Growing demand for home healthcare devices | +1.8% | North America and Europe, expanding into APAC | Short term (≤ 2 years) |

| Increasing geriatric population base | +1.4% | Global, notably Japan, Germany, Italy | Long term (≥ 4 years) |

| Technological advances in mesh nebulizers | +1.2% | North America and Europe with emerging APAC adoption | Medium term (2-4 years) |

| Integration with remote-patient-monitoring platforms | +0.9% | North America, selective European markets | Short term (≤ 2 years) |

| Adoption of biologics / liposomal drugs for inhalation | +0.7% | North America and Europe with limited APAC penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Respiratory Diseases

Chronic obstructive pulmonary disease affected 392 million people worldwide in 2024, and prevalence continues to climb in cities with high particulate pollution[1]World Health Organization, “Global Health Observatory Data Repository,” WHO, who.int. Rising symptom burden pushes patients to seek daily therapy that delivers fine aerosol particles efficiently, a clinical requirement that favors mesh and jet nebulizers over inhaler formats among older adults with low inspiratory force. In Asia-Pacific megacities, hospital pulmonology units report earlier onset of moderate COPD, driving public health campaigns that subsidize home-care respiratory kits. The persistent epidemiological trend underpins long-run demand visibility, encouraging device makers to scale production capacity in manufacturing hubs across China and Malaysia. Health ministries in India and Indonesia have already earmarked respiratory devices as priority imports within national procurement plans that emphasize community-level disease management.

Growing Demand for Home Healthcare Devices

North American and European payers intensified efforts to migrate chronic care out of hospitals, a shift solidified when the Centers for Medicare & Medicaid Services broadened reimbursement for durable respiratory equipment in 2024[2]Centers for Medicare & Medicaid Services, “Coverage Guidelines Update,” CMS, cms.gov. The updated rules classify nebulizers as essential home-use tools, which is helping cut emergency-room visits by up to 23% in COPD cohorts. Device vendors responded with Bluetooth-enabled models that upload dosage logs to provider dashboards, a feature that aligns with value-based payment contracts. Home-health agencies now bundle nebulizers with tele-nursing services, creating annuity-style revenue tied to remote monitoring. Similar programs are appearing in South Korea and Singapore, suggesting the model will diffuse across high-income APAC markets over the next two years.

Increasing Geriatric Population Base

Global population aged 65 years and above is expanding at 3% annually, and the cohort is projected to hit 1 billion by 2030, with deep concentrations in Japan, Germany, and Italy. Older adults live with diminished lung capacity, making them susceptible to bronchospasm and lower-airway infections that necessitate aerosolized bronchodilators. Hospitals in Italy reported a 17% rise in outpatient nebulizer prescriptions during 2024, while Japanese insurers have launched incentive programs that reimburse portable units to curtail repeat admissions. Device ergonomics now feature larger buttons, audible cues, and auto shut-off to cater to seniors who may battle dexterity or cognitive decline. The demographic swell thus primes long-duration growth for the nebulizer market by enlarging the therapy-eligible base.

Technological Advances in Mesh Nebulizers

The U.S. FDA cleared three MEMS-mesh platforms in 2024, each producing 1-5 micron droplets with up to 40% less medication loss than legacy jet systems. Omron and Philips quickly licensed the MEMS patterns, cutting treatment windows to under four minutes for 2.5 mL albuterol doses. Lower waste is pivotal in biologic inhalation where one vial can cost more than USD 1,000, prompting hospitals to run pharmacoeconomic analyses that overwhelmingly favor mesh delivery. Manufacturing yields are improving as suppliers refine sputter-deposition of stainless-steel meshes, trimming cost per unit by 12% over the past year. As economies of scale accrue, analysts foresee mesh devices seizing incremental share from ultrasonic models across North America and Western Europe.

Restraints Impact Analysis of Nebulizer Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Drug loss during aerosol delivery | -1.3% | Global, acute in cost-sensitive markets | Medium term (2-4 years) |

| Competition from MDIs & DPIs | -1.1% | Global, stronger in developed economies | Short term (≤ 2 years) |

| High QA/QC costs for MEMS-based mesh plates | -0.8% | Manufacturing hubs in Asia-Pacific | Medium term (2-4 years) |

| Limited reimbursement for smart nebulizers | -0.6% | Developing regions and selective developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Drug Loss During Aerosol Delivery

Traditional jet devices lose between 60% and 80% of medication to the surroundings, an inefficiency flagged by the European Medicines Agency in its 2024 guideline on inhalation products[3]European Medicines Agency, “Guideline on Inhalation Products,” EMA, ema.europa.eu. Payers in Latin America and parts of Southeast Asia consider that waste economically untenable when treating high-priced monoclonal antibodies. Hospitals thus restrict nebulizer use to fluticasone and bronchodilator solutions with lower per-dose cost, dampening unit sales. Manufacturers are tackling the issue with valved masks and breath-actuated flow sensors but must still prove these add-ons reduce waste without inflating acquisition price beyond payer comfort. Until quantifiable gains are demonstrated, reimbursement committees will continue to scrutinize device efficiency, constraining broader uptake.

Competition From MDIs & DPIs

Pharmaceutical majors launched dry-powder formulations of previously nebulized molecules in late 2024, touting pocket-size convenience that appeals to active patients. DPIs deliver metered doses with near-perfect content uniformity, a quality that resonates with pulmonologists who value dosing precision for biologics. Coupled with the absence of cleaning routines, inhalers win favor among younger COPD patients and asthmatics, siphoning potential sales from the nebulizer market. Jet and ultrasonic device makers attempt to counter by stressing efficacy in patients with compromised inspiratory flow, but this clinical message competes against relentless consumer marketing for DPIs. The ensuing product rivalry will temper nebulizer adoption rates in affluent economies over the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Nebulizer Market Segment Analysis

By Nebulizer Type:

Mesh Technology Drives Premium ShiftJet models retained 44.92% of the nebulizer market share in 2025, yet mesh units are registering the sharpest climb, propelling the segment at an 11.02% CAGR through 2031. The shift reflects payers’ readiness to pay more for devices that cut medication waste and shorten treatment sessions. Mesh plates fashioned from electro-formed nickel offer sub-micron tolerances, ensuring drug dispersion uniformity that elevates therapeutic value. Hospitals deploy mesh platforms to deliver antibiotics and biologics whose high-cost profile magnifies the economic upside of lower drug wastage. The widened clinical menu and incremental gains in battery life signal sustained traction for mesh across critical-care, outpatient, and home-care arenas.

Ultrasonic devices serve niche roles where silent operation matters, such as neonatal wards, but their global share is plateauing as production of jet kits remains cost-efficient for volume tenders in emerging markets. Market analysts anticipate that falling mesh component costs will push mesh systems into mid-price tiers by 2027, cementing their role as default technology for chronic therapy. Patent filings at the U.S. Patent and Trademark Office indicate active R&D, with firms refining mesh aperture geometry to accommodate liposomal suspensions without clogging. These iterative enhancements strengthen the competitive runway for mesh within the nebulizer market.

By Portability:

Mobile Solutions Gain TractionTable-top devices controlled 50.84% of global revenue in 2025 thanks to dominant use in in-patient wards, yet handheld and portable equipment is charging ahead at a 10.56% CAGR. Working-age adults prioritize treatments that fit into commutes and travel routines, a behavior that nudges procurement managers toward lightweight, battery-enabled designs. Manufacturers incorporate USB-C charging and antimicrobial polymer housings to address mobility and hygiene expectations. Hospitals still rely on mains-powered compressors for continuous bronchodilation therapies, but discharge planning teams now recommend portable alternatives to minimize readmission risk.

The nebulizer market size for portable units is expected to reach USD 1.11 billion by 2031, equal to nearly 45.12% of global revenue, as mesh modules become thinner and power-efficient. This convergence blurs historical distinctions between home and clinical devices, creating an ecosystem where patients transition between care settings without needing separate hardware. As a result, channel partners, including pharmacies and online retailers, are redesigning fulfillment processes for recurring accessory shipments tied to the growing installed base of portable systems.

By Sales Channel:

Digital Transformation Reshapes DistributionDirect institutional orders delivered 47.05% of the nebulizer market size in 2025 and remain crucial for early adoption of advanced devices. Hospital group-purchasing organizations negotiate three-year contracts that bundle device acquisitions with maintenance agreements, providing predictable revenue streams to incumbents. Nonetheless, e-commerce platforms recorded a 9.62% CAGR as consumers gained confidence in purchasing durable medical equipment online. Click-through rates climbed following pandemic-era telehealth expansion, prompting brands to invest in direct-to-consumer digital storefronts.

The online channel now cements loyalty through auto-ship programs for replacement mesh caps and filters, a profitability lever absent in traditional institutional contracts. Pharmacy chains preserve relevance by integrating curbside pickup and pharmacist counseling, aligning with patients who value in-person guidance. The sales-channel transformation spotlights data analytics as a competitive tool because order histories help vendors anticipate consumables demand and optimize supply-chain workflows.

By End-User:

Home Care Segment Drives GrowthHospitals represented 45.78% of total revenue in 2025, yet home-care adoption is accelerating at a 10.29% CAGR as payers pivot toward lower-cost care sites. Durable equipment suppliers now ship ready-to-use kits that pair nebulizers with Wi-Fi connectivity, permitting clinicians to adjust therapy remotely. This model aligns with new reimbursement codes that reward continuous monitoring rather than episodic interventions. Clinics and ambulatory surgical centers continue to play a bridging role by initiating therapy protocols before patients transition home.

The nebulizer market share for home users is forecast to approach 31.84% by 2031 as device ease-of-use improves. ISO 13485 guidelines, updated in 2024, emphasize risk mitigation for lay users, spurring manufacturers to redesign interfaces with intuitive symbols and automated cleaning prompts. Remote technical support hotlines further reduce barriers, assuring caregivers who may lack clinical training that they can troubleshoot minor issues without returning to hospital settings.

Geography Analysis

North America Nebulizer Market

North America dominated with 38.11% revenue share in 2025, supported by robust insurance coverage and early embrace of connected health platforms. The FDA’s clearer pathway for software-as-a-medical-device modules expedited mesh device clearances, enabling providers to bundle therapeutic hardware with digital adherence dashboards. Large integrated delivery networks now embed nebulizer data feeds into electronic health records, facilitating population-level analytics that identify non-compliant patients.

Europe Nebulizer Market

Europe follows with stable mid-single-digit growth anchored in Germany, France, and the United Kingdom, where hospital systems value mesh technology for pediatric and geriatric populations. The European Union’s Medical Device Regulation requires clinical efficacy proof and post-market surveillance, favoring established firms that possess sizable evidence portfolios. Southern Europe opts for cost-balanced jet devices but is introducing pilot projects that test portable mesh units in home-oxygen programs.

APAC Nebulizer Market

Asia-Pacific stands out with a 9.51% CAGR aided by urban smog and smoking prevalence that swell respiratory caseloads. China’s National Medical Products Administration approved 12 new nebulizer models in 2024, underscoring regulators’ support for domestic producers. Subsidies under the Healthy China 2030 blueprint boost community-level clinics, cultivating demand for low-cost jet kits alongside premium mesh exports. Japan and South Korea focus on portable lines that cater to aging cohorts demanding on-the-go therapy, thereby expanding the installed base for consumables. Emerging Southeast Asian economies remain price-sensitive yet represent latent upside once reimbursement schemes mature.

Regulatory Landscape

Nebulizers sold for direct patient interface in the United States fall under FDA medical device rules and are commonly regulated as Class II devices (21 CFR 868.5630), which brings 510(k) expectations around performance testing, labeling, and design controls. In parallel, some medicinal nonventilatory nebulizers (atomizers) are listed as Class I and can be exempt from premarket notification under 21 CFR 868.5640, shaping go-to-market planning and the depth of documentation across product lines.

Across major regions, compliance is increasingly anchored to harmonized standards and formal classification guidance. FDA recognizes ISO 27427:2023 for safety and performance testing of general-purpose nebulizing systems (including continuous and breath-actuated designs), which supports standardized verification packages for global submissions. In Europe, nebulizers and inhalation administration devices must align with the EU Medical Device Regulation (MDR 2017/745), with MDCG 2021-24 used as an applied reference for classification under Annex VIII and for setting expectations around clinical evidence and post-market surveillance.

Competitive Landscape

The nebulizer market shows moderate fragmentation with the top five vendors accounting for significant global sales. Philips builds scale on its strong patent library around mesh atomization while Omron leverages consumer brand equity to widen retail reach. Both firms emphasize ecosystem playbooks, bundling devices with cloud services and consumables subscriptions. Second-tier players such as PARI Pharma innovate in breath-actuated systems suited for cystic-fibrosis antibiotics, gaining traction in specialized hospital wings.

Acquisition activity intensified during 2024–2025 as multinationals sought niche capabilities. Philips assimilated BioTelemetry remote-monitoring assets to enhance data-driven interventions, and Molex expanded into combination inhalation platforms by acquiring Vectura’s technology in January 2025. Meanwhile, Chinese manufacturers Hong Ke and Mindray invest in automated assembly lines that lower compressor costs, aiming to undercut Western brands in tender bids across Africa and Latin America. Despite cost competition, premium mesh devices defend margins through clinical performance evidence and software differentiation, traits that resonate with hospitals under outcome-based payment contracts. Overall, success hinges on mastering both hardware reliability and digital companion services that motivate long-term patient engagement.

Nebulizer Industry Leaders

Omron Corporation

Koninklijke Philips N.V.

DeVilbiss Healthcare LLC

PARI Pharma GmbH

Vyaire Medical, Inc. (Asahi Kasei Corporation)

- *Disclaimer: Major Players sorted in no particular order

Nebulizer Market Companies Covered in this Report

- Aerogen Ltd.

- Air Liquide

- Allied Healthcare Products

- Beurer

- Briggs Healthcare

- Drive DeVilbiss Healthcare

- Fazzini srl

- GF Health Products, Inc.

- Invacare

- Koninklijke Philips

- MeDel S.p.A.

- Medline Industries

- Microlife

- OMRON

- PARI Pharma GmbH

- Rossmax

- Trudell Medical International

- Vyaire Medical, Inc. (Asahi Kasei Corporation)

- Yuyue Medical

Market Opportunities and Future Outlook

One whitespace is converting legacy installed bases, especially jet platforms, into lower-waste, more controllable delivery without forcing full device replacement. That focus is reinforced by ongoing research activity around synchronizing aerosol generation with inhalation phases and add-on approaches that reduce secondary exposure and drug wastage, addressing a core drawback of continuous-mode nebulization highlighted by payers and regulators. For manufacturers and distributors, this supports upgrade accessories, valved interfaces, and workflow-integrated consumables programs that fit hospital purchasing constraints while improving real-world efficiency.

A second opportunity is faster product iteration and portfolio segmentation enabled by active regulatory throughput and corporate portfolio moves. FDA 510(k) clearances for mesh nebulizers (for example, Qingdao Future Medical Technology Co., Ltd. clearance for an H6 mesh nebulizer in 2025) provide a visible pathway for new entrants and private-label programs to compete beyond compressor-based systems. On the supply side, Glenmark Pharmaceuticals' transfer of nebulizer brands and related intellectual property to Glenmark Healthcare Limited (June 2026) points to continued vertical integration and dedicated platform ownership, which can support region-specific SKUs, tighter control of component sourcing (including mesh plates), and quicker commercialization of connected or breath-synchronized features where reimbursement and clinical protocols support adoption.

Recent Industry Developments in Nebulizer Market

- April 2026: DeVilbiss Healthcare announced the commercial launch of the 555 Compact Oxygen Concentrator, positioned around a smaller footprint and lower energy consumption versus the prior model. While not a nebulizer, it strengthens DeVilbiss by Drive in respiratory home-care equipment, where bundled offerings and channel presence can influence nebulizer pull-through and account access across DME providers.

- November 2025: OMRON Healthcare reported cumulative global sales of its nebulizers surpassing 50 million units. The milestone reinforces OMRONs installed base advantage and provides leverage for retail, pharmacy, and online channels, where repeat consumables and replacement cycles support long-term category share.

- March 2024: Medline unveiled the Hudson RCI TurboMist small-volume nebulizer designed to complete medication delivery in as little as three minutes. Faster treatment cycles help throughput in clinical settings, and create a differentiation point for institutional purchasing where time-on-therapy and workflow fit can matter as much as device acquisition cost.

Nebulizer Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the value of nebulizer devices used to deliver inhaled medicines by turning liquids into a breathable mist for patients in clinical and home settings. It counts device sales across common technologies and form factors that are purchased through institutional and retail channels.

Scope exclusions: We exclude nebulized drug sales, replacement medicines, and non-nebulizer respiratory devices such as inhalers and CPAP machines.

Segments Covered in This Report

- By Nebulizer Type

- Jet Nebulizers

- Ultrasonic Nebulizers

- Mesh Nebulizers

- Smart/Connected Nebulizers

- By Portability

- Table-top

- Hand-held / Portable

- By Sales Channel

- Direct/Institutional Purchase

- Online Retail

- Pharmacies & Drug Stores

- By End-user

- Hospitals

- Clinics

- Home-care Settings

- Ambulatory Surgical Centres

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the basic market boundaries and to anchor the demand environment for respiratory care devices. We reviewed public health and disease burden signals from organizations such as the World Health Organization, US CDC, and Global Initiative for Asthma publications, and then matched them with country level population and age structure data from the World Bank and UN sources.

To keep the model realistic at a country level, we also used trade and production signals where they were visible, including customs statistics and import-export portals, along with regulatory and device listings from agencies such as the US FDA and similar national regulators. Company annual reports, investor presentations, press releases, and reputable healthcare news were used to track launches, pricing direction, and channel changes. In a limited way, we referenced paid subscriptions for company financials and intelligence, and for patent databases, to cross-check product pipelines. The desk sources listed above are illustrative only, and we also used other public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives device volumes and pricing in hospitals, clinics, and homecare, since those details are often not visible in public data. We spoke with a mix of device manufacturers, distributors, and clinical stakeholders across major regions to confirm technology mix shifts (jet to mesh), portable adoption, and typical replacement patterns, then used this input to tighten assumptions and close data gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 30% | EMEA: 33% |

| Smaller Players: 17% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

The core market value is built using a top-down approach where respiratory disease prevalence and treated patient pools are translated into device demand, then filtered through setting of care and technology adoption rates before a value is calculated. Because purchasing behavior varies by country, the demand pool is adjusted using indicators such as COPD and asthma burden, elderly population share, nebulization use in acute care, homecare penetration, and the mix of portable versus tabletop devices.

After the first pass, results are checked using selective bottom-up approximations that a junior analyst can reproduce, including channel checks on institutional procurement, sample price points for jet and mesh devices, and supplier and distributor revenue splits where they are disclosed. If a country lacks clear trade or pricing signals, we fill the gap with proxy pricing from similar markets and then correct it using interview-based discount assumptions and margin ranges. For forecasting, we mainly use scenario analysis, where the base case is guided by expected chronic respiratory disease trends, device replacement cycles, and the pace of mesh adoption, and then we stress-test using more conservative and more aggressive adoption paths.

Data Validation & Update Cycle

Validation happens in steps so that outliers do not carry into the final numbers. We compare computed totals against independent signals such as import intensity for device categories, health expenditure direction, and the implied device-per-treated-patient ratio, then rework any unusual jumps until the logic is consistent across countries and regions.

Before sign-off, the model is reviewed by another analyst for unit consistency, currency conversion timing, and the reasonableness of key assumptions. A final pass is then used to confirm that the latest public updates are reflected. Reports are refreshed annually, and interim updates are triggered when material events occur, such as large regulatory changes, major product launches, or sudden demand shocks.

Mordor Intelligence's Nebulizer Market Sizing Compared With Other Published Estimates

Published market sizes for nebulizers can look different even when they cover the same device types, since scope and the anchor year used for the time series are not always aligned. In practice, differences also come from how portable devices are counted, how online retail is treated, and whether smart or connected nebulizers are included as a separate pool.

Key gap drivers are usually linked to inclusion rules and the way prices are projected over time. Some estimates track a narrower set of jet, mesh, and ultrasonic types, and they may also anchor on a different base year. That shifts the USD value after currency timing and inflation adjustments. Others assume a slower price decline or a flatter mix shift, which can lower the stated current number even if the longer forecast horizon remains similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.75 B (2026) | |

| Global Research Publisher A | USD 1.22 B (2024) | Uses an earlier base year and presents a narrower device framing that focuses on jet, mesh, and ultrasonic types, which can undercount smart nebulizers and some channel-driven pricing effects in later years. |

| Healthcare Publisher B | USD 0.98 B (2025) | Anchors sizing to a different base year and applies a slower near-term growth and pricing path, which can reduce the stated current value even if the longer forecast horizon extends further. |

Import trends for respiratory devices and the observed shift toward portable and mesh technology are the checks that keep Mordor Intelligence tied to a device-demand pool that is consistent with how hospitals and homecare buyers replace and upgrade nebulizers. When the year anchor, included device set, and price mix logic are made explicit, the spread across published figures becomes easier to explain and easier to reconcile.

Key Questions Answered in the Report

What is the global value of nebulizer sales in 2026?

Revenue reaches USD 1.75 billion in 2026.

Which device technology is expanding fastest through 2031?

Mesh nebulizers lead, advancing at an 11.02% CAGR.

How quickly is demand growing in Asia-Pacific?

Sales in the region are projected to rise at a 9.51% CAGR.

Why are providers favoring mesh devices for biologic therapies?

Mesh platforms cut medication waste by up to 40% and shorten delivery time, improving cost-effectiveness for high-priced biologics.

Which distribution channel is seeing the steepest post-pandemic growth?

Online retail is climbing at a 9.62% CAGR as patients shift to e-commerce for equipment and consumables.

How is the rise of home care shaping nebulizer design priorities?

Manufacturers focus on portable, intuitive units with remote-monitoring features that meet ISO 13485 safety standards for non-professional users.

Page last updated on: