Market Overview

| Study Period | 2020 - 2031 |

|---|---|

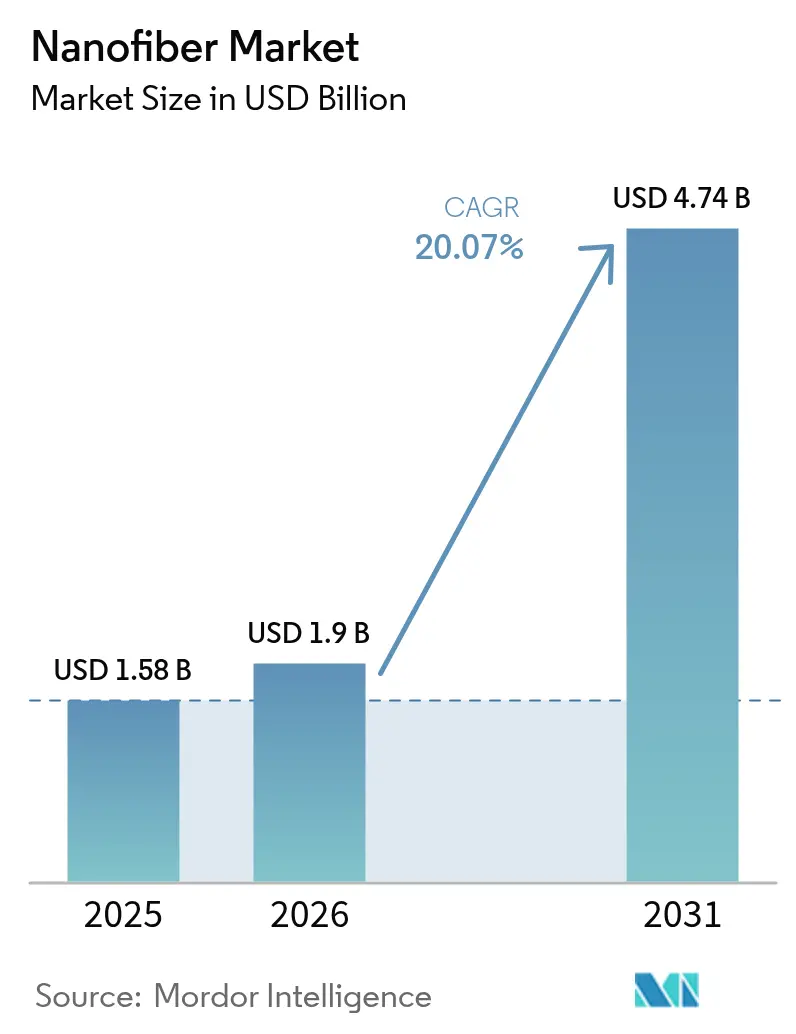

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 4.74 Billion |

| Growth Rate (2026 - 2031) | 20.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

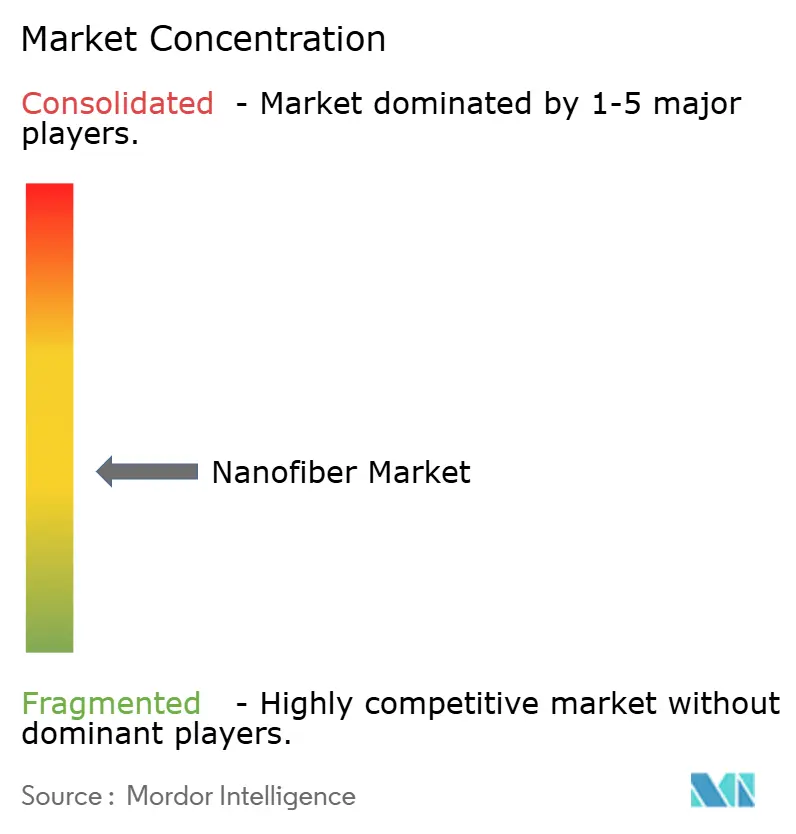

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nanofiber Market Analysis by Mordor Intelligence

The Nanofiber Market size was valued at USD 1.58 billion in 2025 and estimated to grow from USD 1.9 billion in 2026 to reach USD 4.74 billion by 2031, at a CAGR of 20.07% during the forecast period (2026-2031). Heightened demand for high-surface-area materials in medical, filtration, energy storage, and advanced textile applications anchors this outlook. Asia-Pacific, with an existing 38% revenue lead, benefits from strong manufacturing ecosystems and is expected to expand at 22% CAGR through 2030, reinforcing its dual role as both the largest and fastest-growing regional base. The polymeric product category holds 42% of 2024 revenue, supported by mature electrospinning capacity, while carbohydrate-based grades set the growth tempo at 27% CAGR, reflecting a wider sustainability shift. Global incumbents such as Toray Industries and DuPont maintain volume leadership while innovators like NanoLayr deploy proprietary manufacturing to capture high-margin medical and energy niches. Persistent scale-up hurdles for carbon nanofibers, coupled with price volatility in polyacrylonitrile (PAN) feedstock, temper the near-term supply outlook.

Key Report Takeaways

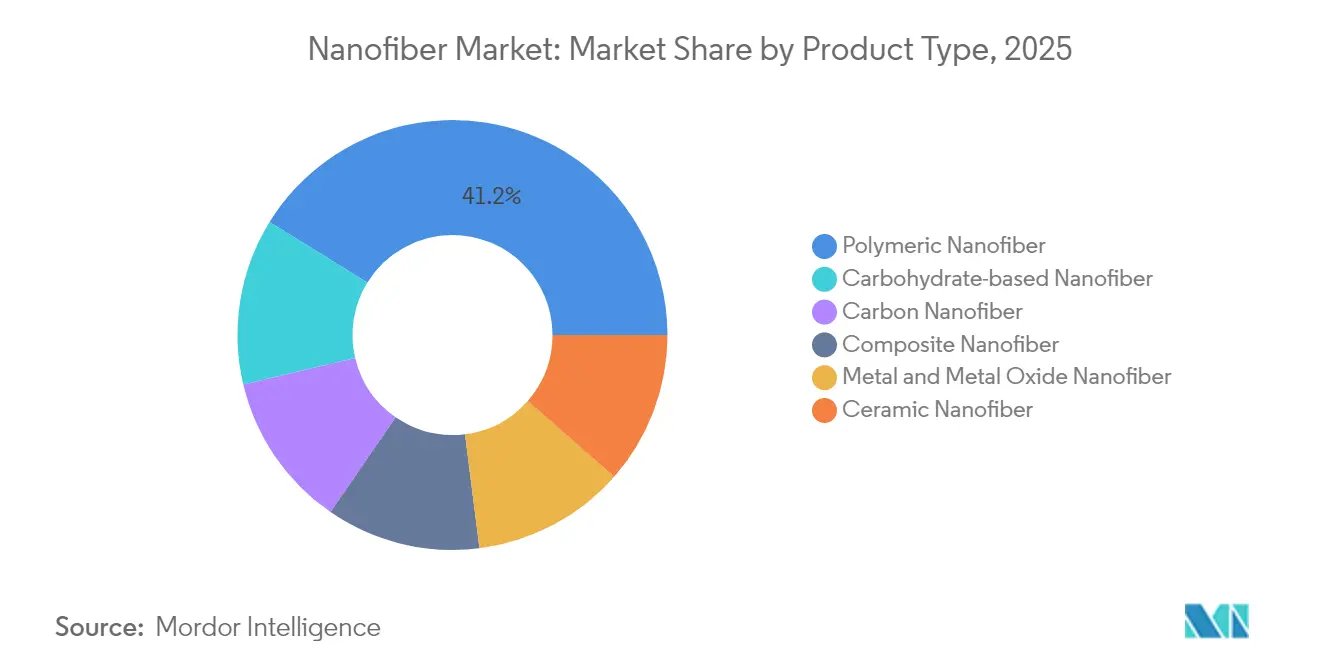

- By product type, polymeric grades led with 41.20% revenue share in 2025, whereas carbohydrate-based nanofibers are projected to clock a 26.2% CAGR to 2031 .

- By application, water and air filtration commanded 39.30% of the nanofiber market share in 2025; energy storage applications are expected to register the fastest growth at 27.1%-plus CAGR through 2031.

- By manufacturing technology, electrospinning retained a 57.20% revenue share in 2025, while forcespinning is forecast to expand at 22.1% CAGR to 2031.

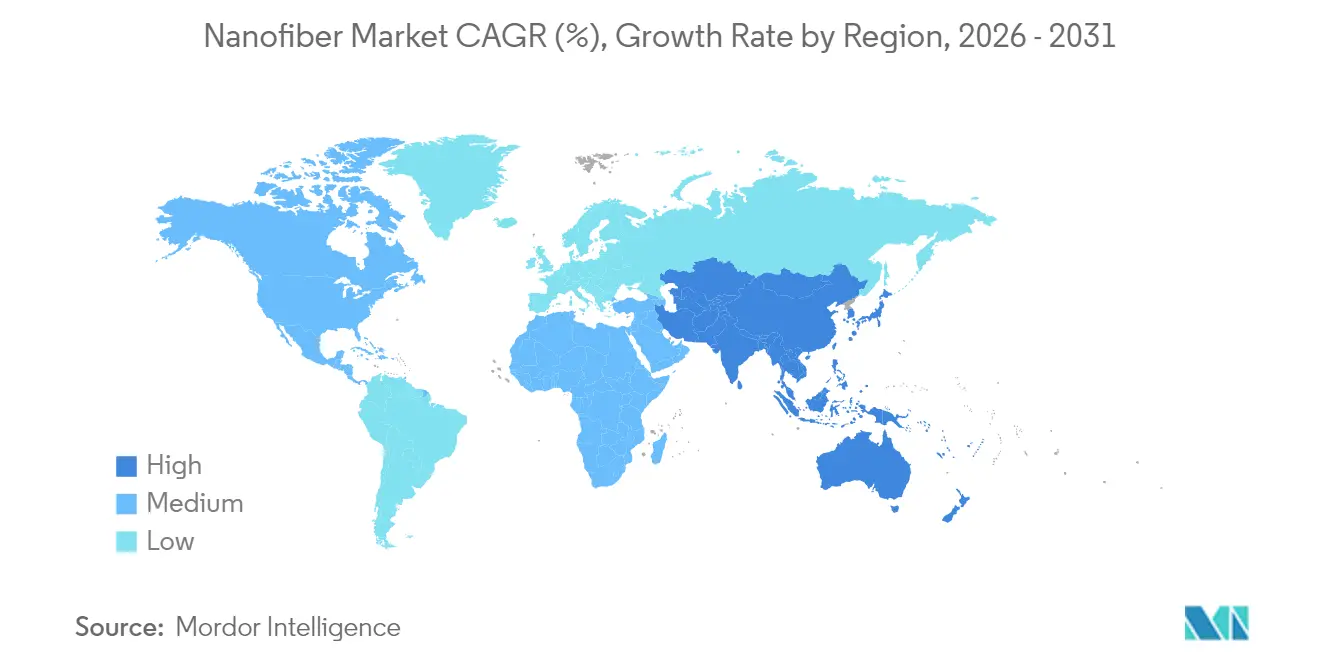

- By geography, Asia-Pacific captured 37.60% of 2025 revenue; the region is also set to post the highest regional CAGR of 21.4% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nanofiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand from the Medical and Pharmaceutical Industries | +5.20% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Demand for High-Surface-Area Battery Separators in EV Gigafactories | +4.80% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Demand for High-Efficiency Filtration Materials | +3.50% | Global, most acute in urban Asia-Pacific | Short term (≤ 2 years) |

| Growth in the Automotive Industry | +2.80% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Expansion in the Textile Industry | +2.40% | Asia-Pacific, with growth in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand from Medical and Pharmaceutical Industries

Nanofiber-based drug delivery platforms now achieve 85%-plus drug loading and sustained release for up to 96 hours, sharply improving therapeutic adherence and lowering systemic toxicity. Their extracellular-matrix-like architecture supports superior cell attachment, enabling next-generation tissue scaffolds that cut healing time and minimize scarring[1]Deepanjan Datta et al., “Cellulose-Based Nanofibers for Wound Healing,” pubs.acs.org . Hospitals adopting advanced wound dressings cite patient-turnover gains that translate to reduced care costs, strengthening procurement appetite. Regulatory pathways for nanofiber scaffolds in orthopedics continue to clarify, lowering time-to-market risk for developers. Collectively, these medical breakthroughs elevate reimbursement prospects and reinforce recurring demand across high-value healthcare channels.

Demand for High-Surface-Area Battery Separators in EV Gigafactories

Electrospun nanofiber separators now withstand 150 °C thermal excursions without dimensional loss, addressing critical EV safety standards. Enhancements in ion conductivity are extending fast-charge capability by up to 40% while preserving cycle life, a gain attracting procurement from Asian and US gigafactories. Automated roll-to-roll lines scale output beyond 3 million m² annually, narrowing cost gaps with conventional polyolefin films. Capital deployment by major cell producers is locking in multiyear supply contracts, providing predictable volume visibility for nanofiber vendors. National clean-mobility incentives in China and the United States further amplify separator adoption in new cell chemistries.

Demand for High-Efficiency Filtration Materials

Multilayer nanofiber media capture 0.3 µm particulates at more than 99% efficiency while keeping the pressure drop to 48 Pa, exceeding WHO indoor-air guidelines. HVAC system retrofits in dense Asian cities adopt these filters to curb smog-related morbidity. In automotive fuel systems, nanofiber layers remove 4 µm contaminants at 99.9% efficiency, lengthening injector life and lowering maintenance costs. Water-treatment plants integrate nanofibrous membranes to remove pathogens at the nanoscale without chlorine dosing, slashing disinfection by-products. Pandemic-era consumer awareness of air quality pushes adoption of high-end respirators, solidifying retail demand.

Growth in the Automotive Industry

Nanofiber-reinforced composites reduce vehicle component weight by up to 30%, driving fleet fuel-economy gains and emission compliance. Cabin-air filters integrating nanofiber layers achieve PM2.5 removal above 99.5%, enhancing occupant health metrics and adding premium features in mid-range models. Acoustic nanofiber mats offer broadband noise dampening, allowing automakers to lighten structural dampers and improve passenger comfort. In-situ functional nanofibers provide electromagnetic shielding for electric drivetrains, preventing signal interference. Collectively, these features raise material uptake per vehicle, reinforcing long-term demand from OEMs and Tier-1 suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile PAN Feedstock Prices | -3.60% | Global, highest exposure in emerging markets | Short term (≤ 2 years) |

| Difficulty in Shift of Carbon Nanofibers from Lab Scale to Plant Scale due to Small Size and Complexity | -4.20% | Global, acute in high-tech manufacturing hubs | Long term (≥ 4 years) |

| Health and Safety Concerns | -2.10% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile PAN Feedstock Prices

PAN constitutes about 90% of carbon nanofiber precursors, and its spot price fluctuates by up to 20% annually, eroding margin stability for downstream suppliers. Supply disruptions linked to acrylonitrile feed shortages intensify inventory risk, prompting producers to pursue petroleum-asphaltene or lignin alternatives that can cut raw-material cost below USD 9 per kg while raising sustainability credentials. Transition timeframes remain lengthy due to impurity management and variable mechanical performance, prolonging exposure to PAN volatility. Buyers hedge through index-linked contracts, but long-term pricing visibility is still limited, dampening aggressive capacity expansion.

Difficulty in Shifting Carbon Nanofibers from Lab to Plant Scale

Commercial lines must maintain fiber diameters within ±50 nm tolerance and crystallinity above 90% to meet electronic and battery specifications, yet lab-to-plant transfers often widen these ranges, degrading product performance. Capital-intensive spinneret arrays and stringent environmental controls lift project payback periods, curbing investor appetite. Regulatory scrutiny is tightening; Massachusetts proposes classifying carbon nanofibers as Higher Hazard Substances under TURA, adding compliance overhead[2]Massachusetts Government, “Draft Carbon Nanotube and Nanofiber Policy,” mass.gov . Modular production platforms under federal grants show promise, but broad rollout will hinge on demonstrated reliability and cost parity with established microfibers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Carbohydrate-Based Nanofibers Lead Sustainability Shift

The polymeric category anchors 41.20% of 2025 revenue, driven by well-established electrospinning lines and broad chemical versatility across packaging, filtration and biomedical devices. Carbohydrate-based grades, while smaller in volume, accelerate at a 26.2% CAGR as end-users pursue biodegradable, bio-sourced alternatives aligned with global circular-economy mandates. Cellulose nanofibers rival aramid tensile strength yet biodegrade under ambient conditions, compelling packaging suppliers to adopt them in single-use applications. Chitin nanofibers attract wound-care producers due to inherent antimicrobial traits, spurring investment in shellfish-waste valorization. Carbon nanofibers find significant use in specialty energy and electronics applications; however, production scale and cost challenges are restraining immediate growth.

Momentum for carbohydrate-based products is amplified by brand-owner commitments to cut fossil plastic use. Legislative bans on single-use synthetic fibers in several EU states compound this pull. Composite nanofibers, which blend polymer and ceramic phases, play a significant role in high-temperature filtration niches. Metal and metal-oxide grades serve catalytic and sensing applications where elevated conductivity or photocatalytic activity is critical. Ceramic nanofibers retain demand for thermal insulation in aerospace and furnace linings. As raw-material R&D migrates toward forestry and agricultural waste streams, cost curves are expected to converge, bolstering the broader nanofiber market.

By Application: Energy Storage Disrupts Traditional Dominance

Water and air filtration maintain a commanding 39.30% share in 2025 as urban air-quality mandates and safe-drinking-water regulations intensify. Nonetheless, battery components for EV and stationary storage are capturing disproportionate investor attention, with early-adopter cell manufacturers integrating nanofiber separators and electrodes to raise energy density and fast-charge capability. This sub-segment is projected to outpace others, expanding above 27.1% CAGR through 2031, and is set to elevate the nanofiber market size for energy storage from a mid-single-digit revenue slice today to a high-teen contribution by 2031.

Medical applications generate significant revenue, driven by electrospun scaffolds and premium-priced drug delivery patches. The automotive sector sees substantial contributions through composite weight reductions and enhanced interior filtration. Electronics play a key role with the integration of conductive nanofiber paths in flexible displays and micro-sensors. Advanced textile applications, though currently niche, are gaining traction with innovations in wearable health monitors and antimicrobial sportswear. Additionally, industrial and environmental sectors, including oil-water separation and food packaging, provide notable contributions. Performance advancements in one segment, such as moisture management in apparel, frequently inspire similar innovations in others, like thermal regulation in batteries.

By Manufacturing Technology: Innovations Beyond Traditional Electrospinning

Electrospinning still owns 57.20% of 2025 production thanks to proven scalability for polymeric feedstocks and the availability of turnkey pilot lines. Continuous upgrades, including tri-axial needle arrays, raise throughput to 1 kg/h, though energy intensity and high-voltage requirements remain cost concerns. Forcespinning accelerates throughput to 50-100 g/h without high voltage, advancing at 22.1% CAGR as automotive and filtration users pilot industrial runs.

Needle-less electrospinning eliminates clogging issues and produces uniform webs ideal for HEPA-grade filtration. Solution blow spinning enables rapid fiber formation for thermally sensitive polymers and supports aqueous spins, reducing solvent emissions. Melt blowing remains a preferred choice for mask and HVAC filter manufacturers due to the simplicity of thermoplastic extrusion. Advancements in instrumentation, such as laser-controlled jet monitoring and AI-driven quality assurance, are bridging the gap between laboratory research and industrial production, ensuring consistent fiber morphology critical for regulated applications. Additionally, advanced textiles and sectors like oil-water separation and food packaging contribute to market growth, with innovations in one area often driving advancements in others.

Geography Analysis

Asia-Pacific commands 37.60% of 2025 revenue, with China, Japan and South Korea benefitting from deep electronic supply chains and government-backed nanotech initiatives. Robust EV production bases in China elevate local demand for nanofiber separators, while strict environmental guidelines accelerate uptake in air-filtration retrofits. Regional stimulus funds earmarked for sustainable materials further de-risk investment in lignin-derived nanofiber plants. This ecosystem underpins a 21.4% regional CAGR, ensuring Asia-Pacific continues to anchor global volume growth.

North America, driven by the U.S. with its USD 2.2 billion FY-25 National Nanotechnology Initiative budget, which allocates grants to medical, defense, and energy sectors, plays a significant role in global revenue generation. High-value healthcare projects dominate demand; clinical trials for nanofiber-based regenerative implants secure FDA fast-track status, accelerating commercialization. Defense agencies sponsor filtration and protective-wear R&D, fortifying domestic supply chains. Canada’s clean-technology incentives and proximity to automotive hubs kindle cross-border collaboration in battery materials. Europe, driven by Germany and France's stringent sustainability frameworks, leads in the market for biodegradable nanofiber packaging and HVAC solutions. Horizon Europe grants foster university-industry clusters that fast-track scale-up and standardization, while REACH compliance guidelines supply regulatory certainty. Although growth rates trail Asia-Pacific, EU directives banning select single-use plastics are opening replacement opportunities in food-service and personal-care products. In South America, the Middle East, and Africa, where programs addressing potable-water scarcity and enhancing agricultural efficiency are gaining traction, revenue is driven by the early adoption of nanofiber membranes in desalination and controlled-release fertilizers.

Competitive Landscape

The nanofiber market features a moderately fragmented profile. Toray Industries fortifies its portfolio via steady capacity upgrades at its Japanese and Thai sites, focusing on high-temperature filtration grades. DuPont leverages extensive polymer chemistry know-how to introduce medical-grade electrospun scaffolds with validated biocompatibility. Teijin integrates nanofibers into carbon-fiber composites, capturing synergies in aerospace and sporting goods.

Specialist firms mount technology-led offensives. NanoLayr refines sonic-spinning techniques for sub-200 nm fibers that deliver enhanced barrier films to wound-care OEMs. Hollingsworth & Vose scales patented multiscale filtration media that balance pressure drop and efficiency, winning contracts for premium home-appliance filters. Start-ups in Europe champion lignin-based lines, aiming to disrupt the PAN cost base while advancing ESG credentials.

Strategic collaborations accelerate innovation. Asahi Kasei’s 2024 agreement with Aquafil merges cellulose nanofibers with ECONYL regenerated nylon for additive-manufactured components, highlighting cross-industry convergence. Chuetsu Pulp’s partnership with Marubeni introduces agricultural pest-control films made from cellulose nanofibers, validating new revenue channels. Intellectual-property activity intensifies: patents for non-woven nanofiber membranes in lateral-flow diagnostics forecast encroachment into point-of-care devices. Overall, differentiation hinges on production economics, functional performance and sustainability credentials.

Nanofiber Industry Leaders

Toray Industries Inc.

Donaldson Company Inc.

DuPont

Teijin Limited

Hollingsworth & Vose

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Rengo Co., Ltd.'s newly developed "FineNatura" cellulose nanofiber was chosen by TILEMENT CORPORATION as a curing accelerator for its exterior wall organic surface preparation materials.

- October 2024: Asahi Kasei and Aquafil have collaborated to harness cellulose nanofibers and regenerated ECONYL Polymer for 3D printing applications. This partnership is expected to drive innovation and expand the adoption of nanofiber-based materials, potentially boosting growth in the nanofiber market.

Global Nanofiber Market Report Scope

Nanofibers are defined as fibers with diameters of less than 1000 nanometers. They can be produced by interfacial polymerization, electrospinning, and force spinning. The market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into carbon nanofiber, composite nanofiber, metal, and metal oxide nanofiber, polymeric nanofiber, carbohydrate-based nanofiber, and ceramic nanofibers. By application, the market is segmented into water and air filtration, automotive and transportation, textiles, medical, electronics, energy storage, and other applications. The report also covers the size and forecasts for the nanofibers market in 11 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

By Product Type

| Polymeric Nanofiber |

| Carbon Nanofiber |

| Composite Nanofiber |

| Metal and Metal Oxide Nanofiber |

| Ceramic Nanofiber |

| Carbohydrate-based Nanofiber |

By Application

| Water and Air Filtration |

| Medical |

| Energy Storage |

| Automotive and Transportation |

| Electronics |

| Textiles |

| Other Applications |

By Manufacturing Technology

| Electrospinning (Needle-Based) |

| Needle-less Electrospinning |

| Solution Blow Spinning |

| ForceSpinning/Rotary Jet Spinning |

| Melt Blowing |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Polymeric Nanofiber | |

| Carbon Nanofiber | ||

| Composite Nanofiber | ||

| Metal and Metal Oxide Nanofiber | ||

| Ceramic Nanofiber | ||

| Carbohydrate-based Nanofiber | ||

| By Application | Water and Air Filtration | |

| Medical | ||

| Energy Storage | ||

| Automotive and Transportation | ||

| Electronics | ||

| Textiles | ||

| Other Applications | ||

| By Manufacturing Technology | Electrospinning (Needle-Based) | |

| Needle-less Electrospinning | ||

| Solution Blow Spinning | ||

| ForceSpinning/Rotary Jet Spinning | ||

| Melt Blowing | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global nanofiber market?

The nanofiber market is valued at USD 1.9 billion in 2026 and is projected to reach USD 4.74 billion by 2031.

Which region leads the nanofiber market, and how fast is it growing?

Asia-Pacific holds 37.60% of 2025 revenue and is projected to grow at 21.4% CAGR through 2031, maintaining leadership.

What drives nanofiber demand in electric vehicle batteries?

Nanofiber separators deliver superior thermal stability and faster ion transport, enabling 40% quicker charging without sacrificing safety, which is critical for EV gigafactories.

Why are carbohydrate-based nanofibers gaining popularity?

They offer biodegradability and strong mechanical performance, aligning with circular-economy goals and propelling a 26.2% CAGR in this segment.

What are the main hurdles to scaling carbon nanofiber production?

High capital requirements, strict quality tolerances and emerging regulatory scrutiny complicate the transition from lab to industrial scale, slowing commercial rollout.

Page last updated on: