North America Instant Ramen Noodles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

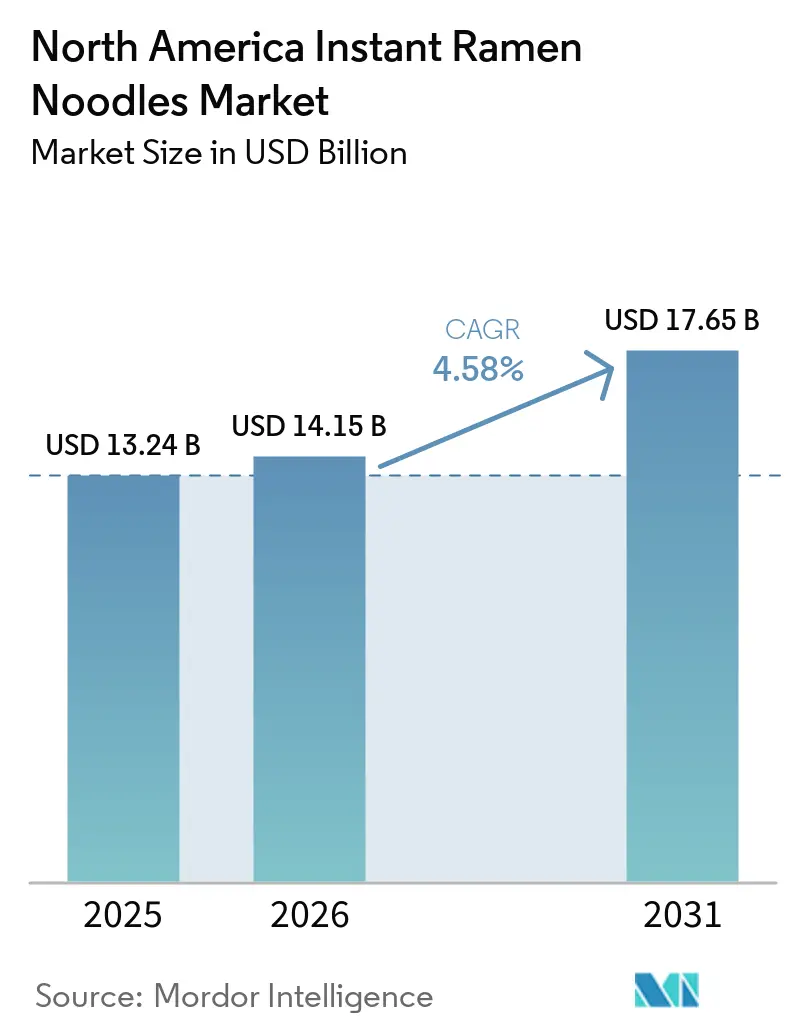

| Base Year Market Size (2025) | USD 13.24 Billion |

| Market Size (2026) | USD 14.15 Billion |

| Market Size (2031) | USD 17.65 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

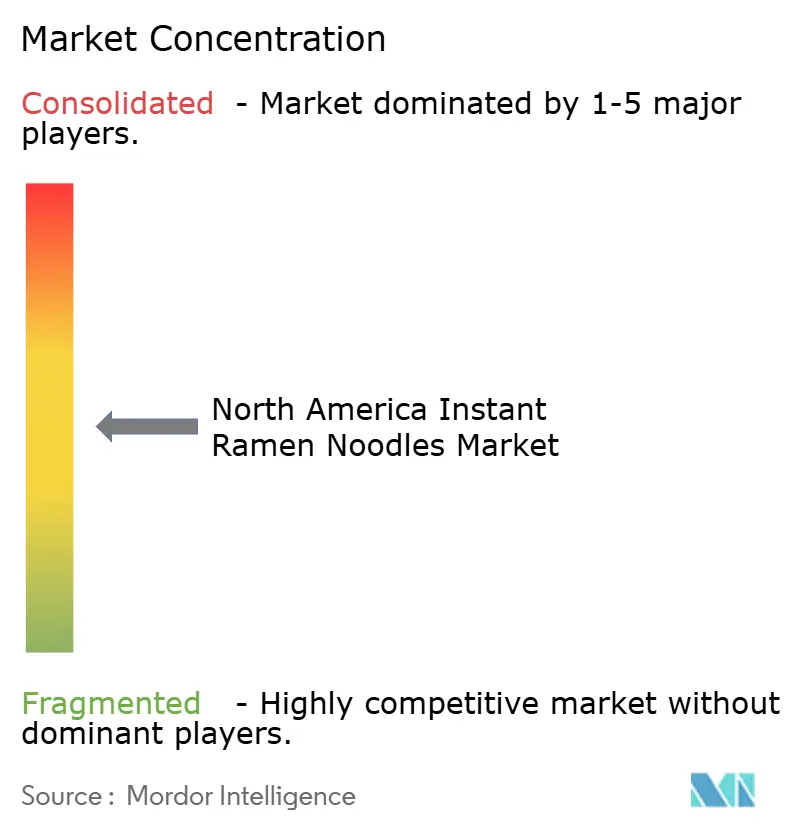

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Instant Ramen Noodles Market Analysis by Mordor Intelligence

The North America instant ramen noodles market size is projected to expand from USD 13.24 billion in 2025 and USD 14.15 billion in 2026 to USD 17.65 billion by 2031, registering a CAGR of 4.6% between 2026 and 2031. The North American instant noodles market is moving beyond its older image as a low-cost pantry staple because shoppers are now paying more for products that add protein, stronger flavor identity, and better convenience. Growth is also being supported by faster launch cycles, where brands use new flavors, limited editions, and platform-led discovery to keep the category visible in both stores and digital channels. The competitive field is becoming harder to read through a single value lens because legacy brands still hold wide distribution, while Korean and premium-focused brands are raising price ceilings and changing shopper expectations. Regulatory pressure around sodium and labeling is adding reformulation costs, but it is also creating a clearer opening for low-sodium, protein-fortified, and cleaner-label products across the North American instant noodles market. That combination of demand resilience, premium mix improvement, and product renovation keeps the North America instant noodles market on a steady path even as manufacturers adjust sourcing, labeling, and domestic production priorities.

Key Report Takeaways

- By product type, non-vegetarian noodles held 52.38% of the North America instant noodles market share in 2025, while vegetarian noodles recorded the highest projected CAGR at 6.25% through 2031.

- By serving type, single-serve packs accounted for 65.48% of the North American instant noodles market in 2025, while multi-serve packs are projected to grow at a 6.42% CAGR through 2031.

- By packaging type, cup and bowl products captured 72.17% of the North America instant noodles market share in 2025, while packets are forecast to expand at a 6.78% CAGR through 2031.

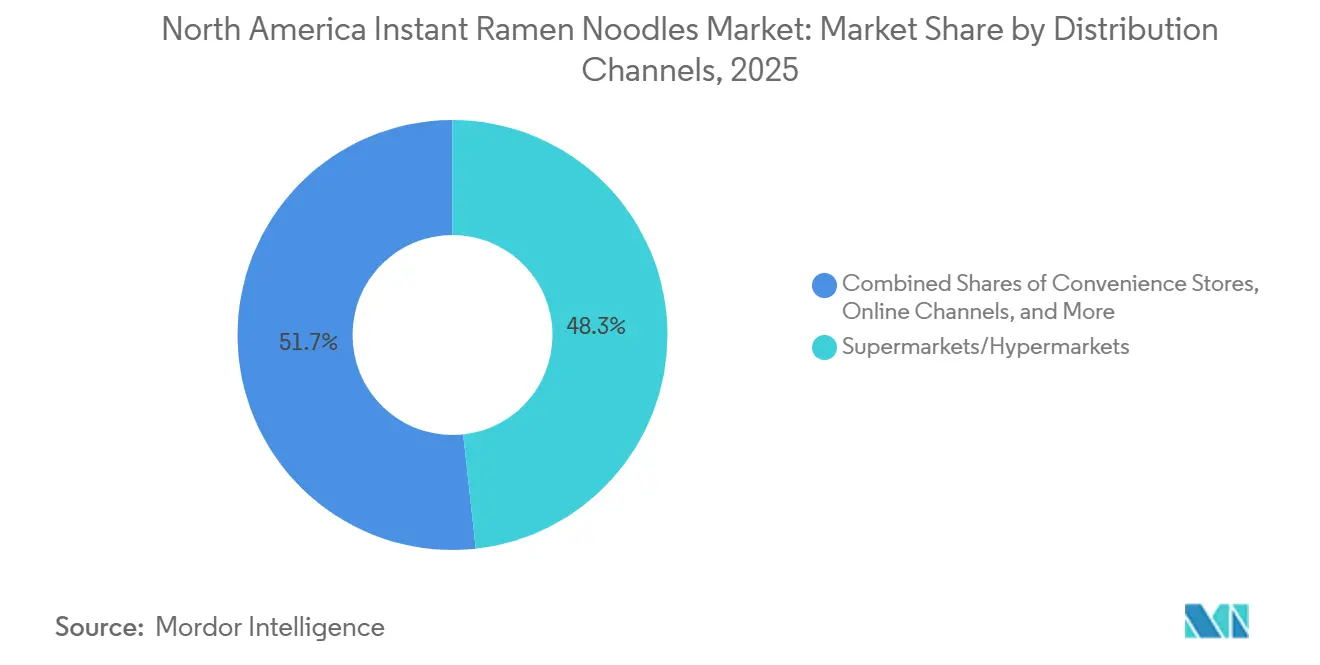

- By distribution channel, supermarkets and hypermarkets accounted for 48.27% of the North American instant noodles market in 2025, while online retail is expected to grow at a 6.57% CAGR through 2031.

- By geography, the United States contributed 58.62% of regional revenue in 2025, while Canada is set to post the fastest CAGR at 7.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Instant Ramen Noodles Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Convenient and Quick Meals | +1.0% | Global, with concentration in US urban metros | Short term (≤ 2 years) |

| Rising Popularity of Asian Cuisine | +0.8% | US (Pacific Coast, Northeast, South), Canada (BC, Ontario) | Medium term (2–4 years) |

| Affordable Meal Alternative During Economic Uncertainty | +0.7% | US (broad), Mexico (nationwide) | Short term (≤ 2 years) |

| Premiumization and Product Innovation | +0.6% | US (all major metros), Canada (urban) | Medium term (2–4 years) |

| Growth of Cup and Ready-to-Eat Formats | +0.5% | North America, with spillover in Mexico | Medium term (2–4 years) |

| Increasing Ethnic Diversity in North America | +0.4% | US (Southwest, West Coast, Southeast), Canada (GTA, Vancouver) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenient and Quick Meals

Time compression is the market's most durable structural engine, and instant noodles are benefiting from a demand pattern that goes well beyond college-dorm stereotypes. The US Bureau of Labor Statistics reports that Americans spend an average of just 37 minutes per day on food preparation and cleanup, the lowest figure since the survey's modern baseline, a statistic that mechanically favours shelf-stable, 3-minute meals. Nissin Foods addressed this directly in February 2026 by launching Cup Noodles Protein nationwide, delivering 16 grams of protein per cup via bone broth at USD 1.33 per unit, a price point that beats most protein bars while matching the two-minute prep window consumers already expect. Critically, the protein-fortified format reframes instant noodles as functional food for busy professionals, not just an austerity staple, which supports a higher average selling price without requiring a full premiumisation jump.

Rising Popularity of Asian Cuisine

The North American instant ramen noodles market is also benefiting from the broader mainstreaming of Asian flavors across grocery retail and digital food culture. Korean, Japanese, and pan-Asian flavor profiles are no longer limited to specialty aisles because large chains now treat them as repeat-purchase packaged food items with national appeal. This matters for category growth because flavor-led discovery often brings first-time buyers into instant noodles before price or habit turns them into repeat buyers. Samyang America reported USD 419 million in revenue for 2025, and the brand’s Buldak line was available in 30,000 US retail doors, which shows how quickly culturally resonant brands can expand once demand becomes visible to mainstream retailers. The result is a market where taste novelty, social visibility, and emotional brand pull are working together to raise velocity for spicy, creamy, and fusion variants across the North American instant noodles market. This also puts pressure on established players because the flavor bar is higher, and legacy products built around milder profiles now need faster renovation cycles to stay relevant.

Affordable Meal Alternative During Economic Uncertainty

Instant ramen noodles remain a textbook countercyclical product, yet the dynamics of that resilience are more nuanced in North America than in Asia. Toyo Suisan's Maruchan brand recorded approximately 3x growth in Mexico's bag-noodle sales over several years as peso inflation sharpened price sensitivity, while in the United States, the company highlighted strong student demand and resumed campus sampling in the post-pandemic period. A counter-signal worth noting: Bank of America data cited in the Japanese financial press indicates that while higher-income households remain steady instant-noodle buyers, lower-income consumers, historically the category's core, have trimmed purchases in 2025 in favour of raw ingredient cooking, pointing to a real floor on the affordability-driven demand base. The implication for manufacturers is that volume support from economic stress is not guaranteed; brands relying solely on value messaging face a ceiling that only product differentiation can lift.

Premiumization and Product Innovation

Premiumization is becoming a deeper structural theme in the North American instant ramen noodles market because brands are no longer treating premium lines as niche experiments. Manufacturers are introducing products that ask consumers to pay materially more in exchange for better nutrition, stronger flavor cues, more modern branding, or a format that stretches beyond the classic cup. Nissin Foods moved in that direction in June 2025 when it launched Kanzen Meal in the United States, a single-serve frozen range with up to 23 grams of protein, 10 grams of fiber, and broad micronutrient content at USD 7.0 to USD 8.0 per unit. Even though this line sits adjacent to standard instant noodles, the strategic effect is important because it raises the acceptable price band for branded noodle-based convenience meals. That helps the North American instant ramen noodles market widen its revenue mix even when pack volumes rise more slowly than value. It also encourages retailers to see noodles as a category with room for premium shelf architecture, not only as a low-margin traffic builder.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Related to High Sodium Content | -0.5% | United States (nationwide), Canada | Short to medium term (≤ 4 years) |

| Competition from Healthier Convenience Foods | -0.4% | United States urban metros, Canada | Medium term (2–4 years) |

| Supply Chain Disruptions | -0.3% | United States, Canada (import-reliant geographies) | Short term (≤ 2 years) |

| Consumer Shift Toward Low-Carb and High-Protein Diets | -0.3% | United States (nationwide) | Medium to long term (2–5 years) |

| Source: Mordor Intelligence | |||

Health Concerns Related to High Sodium Content

Sodium remains the category's most persistent vulnerability, and the regulatory environment in 2026 intensifies the pressure. The FDA's draft Phase II guidance, published in August 2024, sets new three-year voluntary targets for 163 processed-food categories; sodium content in standard instant noodle packs averages 830–1,720 mg per serving, well above the FDA's target ceiling, making the category among the most exposed in the packaged-foods aisle[1]Source: U.S. Food and Drug Administration, “FDA Announces Milestone in Sodium Reduction Efforts, Issues Draft Guidance with Lower Target Levels,”, fda.gov. The proposed front-of-package rule announced in January 2025 would label products with sodium at or above a medium Daily Value threshold with a visible "Med" or "High" flag, directly influencing shelf-browsing decisions for sodium-aware shoppers. Manufacturers who reformulate to lower-sodium profiles before the rule is finalised will be positioned to capture the "Low" designation as a differentiating claim, a compliance cost that doubles as a marketing asset, narrowing the competitive advantage of reformulation latecomers.

Competition from Healthier Convenience Foods

The competitive threat to instant noodles does not come from restaurant-quality competitors; it comes from the expanding universe of "good-enough" healthy convenience formats occupying the same 3-minute prep window. According to the International Food Information Council's study from 2024, 62% of consumers in America consumed healthy food products[2]Source: International Food Information Council, "2024 IFIC, Food & Health Survey", ific.org. Ready-to-eat grain bowls, protein-packed microwaveable rice cups, and high-protein lentil soups have proliferated across major US grocery chains since 2024, targeting the same meal occasion that instant noodles dominate on price alone. Danone-owned Huel launched Lite Ramen in 2026 with 25 grams of plant protein, 3.8 grams of fibre, and 26 essential vitamins, a product that directly competes on the functional-food positioning that premium instant-noodle makers are trying to establish. The substitution pressure is sharpest in the USD 4–8 single-serve segment, where the price gap between an enhanced instant noodle and a competitive healthy-convenience product has narrowed to the point where brand equity and format habit, rather than price, become the decisive variables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Vegetarian Volume Anchors a Vegetarian Uplift

Non-vegetarian noodles accounted for 52.38% of the North America instant ramen noodles market size in 2025, which kept them as the segment’s value anchor. Chicken and seafood-led flavor familiarity still supports strong repeat purchases because these products remain easy to place in mainstream retail and wide price bands. Their performance also reflects the fact that many legacy portfolios in the North American instant noodles market were built first around non-vegetarian profiles, which gives them better shelf density and faster consumer recognition. Even so, the fastest momentum is shifting toward vegetarian lines, which are forecast to expand at 6.25% CAGR through 2031. That growth rate stands above the total category because vegetarian products are now serving more than one consumer need at the same time. They appeal to plant-forward buyers, they travel better across dietary restrictions, and they often fit halal and kosher needs without the complexity of separate meat-based formulations.

Vegetarian formulations often make it easier to support non-MSG, clean-label, or better-for-you positioning, which matters more as sodium and nutrient scrutiny intensifies. Samyang Foods’ Tangle protein pasta line won the Superior Taste Award in 2026 across several SKUs, which signals that better-for-you formulations are improving their sensory credibility. That matters because the North America instant noodles market can add value faster when vegetarian lines are seen as desirable products rather than compromise products. Over time, the segment is likely to gain from both demand-side inclusion and supply-side flexibility, while non-vegetarian noodles continue to support base volumes and familiar flavor demand.

By Serving Type: Single-Serve Formats Stay Dominant, Multi-Pack Momentum Builds

Single-serve packs held 65.48% of the North America instant ramen noodles market size in 2025, which shows how strongly the category still depends on individual convenience occasions. This lead reflects the product’s fit with students, office workers, smaller households, and consumers who want a quick meal without leftovers or extra preparation. Single-serve formats are also easier to trial because the upfront spend is low and retailers can support a wide assortment without creating a major household inventory burden. These advantages keep single-serve packs central to the North American instant ramen noodles market even as purchasing behavior becomes more digitally influenced. At the same time, multi-serving packs are forecast to grow at 6.42% CAGR through 2031, which makes them the fastest-growing format. That faster growth suggests households are not only using instant noodles for emergency pantry stock but also increasingly for repeat family use, customization, and planned value shopping.

The shift matters because it changes where growth comes from inside the North American instant ramen noodles industry. Multi-pack demand benefits from economic logic because consumers can lower per-unit cost, but it also benefits from social behavior where people use noodles as a cooking base for add-ins, sauces, and viral recipes. That makes multi-packs more relevant for at-home experimentation, while single-serve packs remain stronger for direct, no-friction consumption. Maruchan’s Saucy Noods launch in January 2026 through Amazon, TikTok Shop, and selected retailers reflected that shift toward digital-first household demand and flavor-led repeat buying. The regulatory environment may add extra packaging and disclosure complexity to multi-packs because both outer-pack and serving-level information must be clear if front-of-pack rules move ahead. Even so, the serving mix in the North America instant noodles market is unlikely to become a zero-sum contest because single-serve packs and multi-packs meet different buying occasions, and both now contribute to category expansion in distinct ways.

By Packaging Type: Cups and Bowls Lead While Packets Recover Ground

Cup and bowl products represented 72.17% of the North American instant ramen noodles market size in 2025, which confirms that self-contained convenience remains the dominant packaging logic. Cups and bowls solve preparation, portability, and cleanup in one format, and that simplicity supports both mass retail velocity and premium price realization. They also match the category’s current move toward premium toppings, stronger flavor claims, and on-the-go positioning, which is why leading brands continue to invest in cup-based line extensions. That dominance gives cups and bowls a central role in the North American instant ramen noodles market, especially where shoppers treat the product as a substitute for quick-service meals rather than as a pantry ingredient. However, packets are forecast to expand at 6.78% CAGR through 2031, which makes them the fastest-growing packaging segment. This faster pace shows that packet noodles are regaining relevance as households use them for customization, meal stretching, and creator-inspired cooking.

Packets also have strategic advantages that are becoming more visible as the category evolves. They tend to support better value perception in multi-pack settings, and they are well suited to consumers who want control over broth, toppings, or cooking style. Maruchan’s April 2026 launch of Instant Lunch Flamin’ Hot Flavored Chicken translated a viral ramen-hack behavior into a mass retail SKU, showing how digital food culture can create commercial demand from format experimentation. Sustainability also shapes this segment comparison because cup manufacturers face more pressure to rethink materials under evolving single-use plastics policies in the United States and Canada. That means packets may gain incremental support not only from household cooking behavior, but also from packaging economics and a lighter compliance burden over time.

By Distribution Channel: Physical Retail Anchors Volume, Digital Commerce Redefines Discovery

Supermarkets and hypermarkets accounted for 48.27% of the North American instant ramen noodles market size in 2025, which kept physical retail as the main volume anchor. Large-format stores still matter because instant noodles are often purchased as impulse add-ons, fill-in items, or part of broader grocery trips rather than as planned category missions. They also remain the main location for trial because shoppers can see packaging, compare flavors, and respond to promotional placement in real time. This store-led visibility continues to shape the North American instant ramen noodles market even as online discovery becomes more important. Online retail, however, is projected to grow at 6.57% CAGR through 2031, which makes it the fastest-growing distribution channel. That growth reflects the category’s good fit with e-commerce because the products are shelf-stable, light to ship, and often bought in repeat or multi-unit orders.

Digital commerce is changing not only where instant noodles are purchased, but also how demand forms in the first place. Social platforms shorten the path from recipe inspiration or creator endorsement to actual purchase, which gives newer brands a way to build traction without first winning every mainstream shelf. That is especially useful for premium, spicy, or experimental products that benefit from visual storytelling and consumer reaction content. Nissin’s Top Ramen x Bachan’s collaboration launched exclusively at Walmart in March 2026, and that move showed how brands are now blending physical scale with social narrative to support launch momentum. Convenience stores also remain relevant because cup-based products fit immediate consumption and smaller basket missions, even though the channel trails larger grocery in total value. The overall result is a distribution structure where traditional retail still protects the category’s base, while digital channels increasingly shape new-product awareness, repeat buying, and premium flavor discovery across the North America instant noodles market.

Geography Analysis

The United States generated 58.62% of regional revenue in 2025, which made it the largest country market by a wide margin in the North American instant ramen noodles market. As the expat population in the United States is increasing, the consumption of ramen noodles is also growing. According to the American Immigration Council data from 2025, 4.6% of the population in the country was from China and 6.1% were from India[3]Source: American Immigration Council, "Expat Population in the United States", map.americanimmigrationcouncil.org.. That scale rests on broad retail penetration, deep brand familiarity, and the ability of the category to reach almost every major grocery format from dollar stores to warehouse clubs. The United States also has the deepest brand ladder, where value, mainstream, spicy premium, and better-for-you noodle lines can all coexist with meaningful shelf presence. Even so, the growth profile is becoming more quality-driven because future gains are likely to come more from premium mix and innovation than from simple entry-tier volume expansion. This makes the US portion of the North America instant noodles market especially important for product testing, retail exclusives, and flavor innovation that can later move across the rest of the region.

Canada is forecast to expand at 7.02% CAGR through 2031, which gives it the fastest growth rate among the geographic markets covered in the North America instant noodles market. Urban demand, particularly in cities influenced by Korean, Filipino, and other Asian food traditions, is driving this momentum. This urban blend accelerates the acceptance of bolder spice levels, diverse regional flavor profiles, and premium imported brands. Canadian retailers have also shown a greater willingness to dedicate shelf space to ethnic and cross-cultural packaged foods, which supports assortment breadth and repeat discovery. Together, those conditions create a market where demand builds quickly once assortment reaches a visible threshold. Canada therefore acts as an important regional growth engine because its consumer base can absorb both mainstream and specialty noodle lines without forcing brands to choose only one side of the value chain.

Mexico adds a different demand pattern because value-led bag noodles remain highly relevant, and that keeps the category tied closely to affordability and household usage. Toyo Suisan said Maruchan’s bag-noodle sales in Mexico grew around 3x over several years, which underlines the role of price sensitivity and strong brand equity in supporting consumption. Rest of North America remains smaller in revenue terms, but it reflects demand pockets linked to diaspora tastes and cross-border product familiarity. Across the region, the North America instant noodles market shows a clear split where the United States sets the revenue base, Canada raises the growth ceiling, and Mexico reinforces the category’s value resilience. That geography mix is commercially useful because it lets manufacturers balance premium innovation with scale and price-led demand within one regional framework.

Competitive Landscape

North America instant ramen noodles market shows moderate concentration. Nissin Foods and Maruchan remain the most established names in the North American instant noodles market because they still benefit from broad retail reach, strong household recognition, and long-standing value-tier presence. Their position gives them the widest coverage across price points, but it does not guarantee that newer demand pools will stay loyal to legacy formats. Korean brands, led by Samyang and Nongshim, are changing competitive expectations by pushing stronger flavor identity, faster launch cadence, and more emotionally resonant branding. This has made the North American instant ramen noodles market more fluid because attention now moves quickly toward brands that can pair shelf visibility with social relevance. The competitive picture is therefore no longer defined only by distribution muscle, since product storytelling, format innovation, and cultural pull now influence revenue capture more directly.

Several strategic moves in 2025 and 2026 show how leading companies are responding to this change. Nissin widened its innovation range with Cup Noodles Protein in February 2026 and had already moved into nutrient-dense frozen meals through Kanzen Meal in 2025, which shows a deliberate effort to capture healthier convenience occasions before they move outside noodles altogether. Maruchan used a different route by translating a viral consumer behavior into the Flamin’ Hot launch in April 2026, which showed a faster and more culture-led product cycle than the category once had. Borealis Foods pursued a domestic production and premium nutrition angle, and its April 2026 refinancing supported operations for several branded lines manufactured in South Carolina. These examples show that competition in the North America instant noodles market is now being shaped by both innovation speed and supply-side positioning, not only by legacy brand scale.

White space remains clearest in mid-tier premium products that are domestically produced, higher in protein, and more responsive to sodium concerns. That opening exists because the market still has a visible gap between entry-value staples and imported premium spicy noodles, with fewer options positioned cleanly in the middle. Samyang’s product recognition for its Tangle line suggests that texture and formulation can support premium pricing when brands solve the quality hurdle rather than relying only on heat or novelty. At the same time, the FDA’s sodium targets are likely to shape shelf planning, retailer discussions, and product renovation priorities across the North America instant noodles market over the next several years. Companies that align flavor renovation, nutrition claims, and domestic manufacturing with that regulatory backdrop are likely to hold the strongest bargaining position with retailers. That is why the competitive field remains moderately concentrated, yet increasingly open to brands that can connect product quality, compliance readiness, and cultural relevance in one offer.

North America Instant Ramen Noodles Industry Leaders

-

Nissin Foods Holdings Co., Ltd.

-

Nongshim Co., Ltd.

-

Samyang Foods Co., Ltd.

-

Toyo Suisan Kaisha, Ltd.

-

Ajinomoto Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Maruchan introduced its first-ever Flamin' Hot® flavored instant ramen product, launching the new Instant Lunch Flamin' Hot® Flavored Chicken Flavor in collaboration with PepsiCo's Flamin' Hot® brand. The product was developed in response to the viral "Maruchan Loca" social media trend, where consumers customized Maruchan noodle cups with Flamin' Hot® snacks and seasonings.

- March 2026: Nissin Foods announced a strategic collaboration between its Top Ramen brand and Bachan’s, a leading Japanese barbecue sauce company, to introduce a limited-edition range of instant ramen products inspired by Japanese barbecue flavors. The new lineup features three beef-flavored variants incorporating Bachan’s signature sauces: Original Japanese Barbecue, Sweet & Spicy Japanese Barbecue, and Roasted Garlic Japanese Barbecue.

- February 2026: Nissin Foods expanded its instant ramen portfolio with the nationwide launch of Cup Noodles Protein, the brand’s first high-protein product line featuring 16 grams of protein per serving, more than double the protein content of standard Cup Noodles.

North America Instant Ramen Noodles Market Report Scope

| Vegetarian Noodles |

| Non-Vegetarian Noodles |

| Single-Serve Packs |

| Multi-Serving Packs |

| Packets |

| Cups/Bowl Packaging |

| Supermarket/Hypermarkets |

| Convenience Stores |

| Online Retail Channels |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Product Type | Vegetarian Noodles |

| Non-Vegetarian Noodles | |

| Serving Type | Single-Serve Packs |

| Multi-Serving Packs | |

| Packaging Type | Packets |

| Cups/Bowl Packaging | |

| Distribution Channels | Supermarket/Hypermarkets |

| Convenience Stores | |

| Online Retail Channels | |

| Other Distribution Channels | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current size of the North America instant ramen noodles market?

The North America instant ramen noodles market was valued at USD 13.24 billion in 2025 and is estimated at USD 14.15 billion in 2026, with projected value reaching USD 17.65 billion by 2031.

What is driving growth in instant ramen noodles across North America?

The main growth factors are faster meal needs, stronger interest in Asian flavors, premium product launches, and rising online discovery that converts social content into purchases.

Which product type leads sales in North America?

Non-vegetarian noodles led with 52.4% of value in 2025, but vegetarian noodles are forecast to grow faster at a 6.3% CAGR through 2031.

Which packaging format is growing the fastest?

Packets are forecast to grow fastest at a 6.8% CAGR through 2031, even though cups and bowls still held the largest 72.2% share in 2025.

Page last updated on: