Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

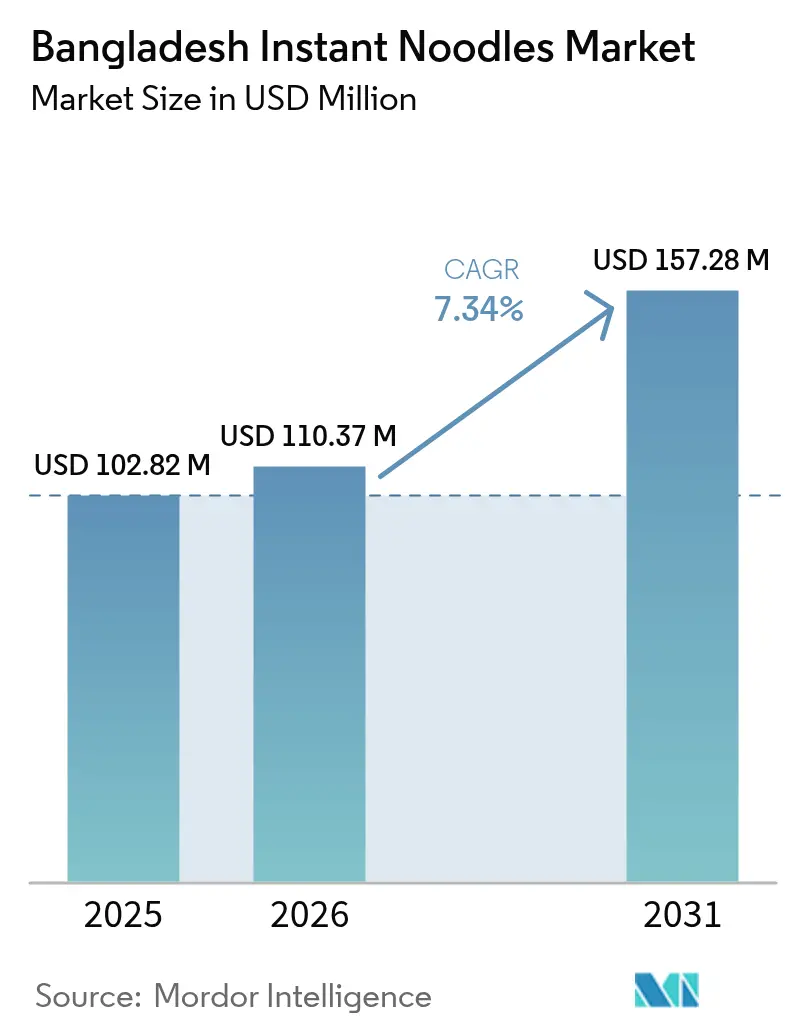

| Base Year Market Size (2025) | USD 102.82 Million |

| Market Size (2026) | USD 110.37 Million |

| Market Size (2031) | USD 157.28 Million |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bangladesh Instant Noodles Market Analysis by Mordor Intelligence

The Bangladesh instant noodles market was valued at USD 102.82 million in 2025 and estimated to grow from USD 110.37 million in 2026 to reach USD 157.28 million by 2031, at a CAGR of 7.34% during the forecast period (2026-2031). This upward trajectory is fueled by rising urban incomes, the evolution of retail formats, and a notable shift towards online grocery shopping, making instant noodles more accessible to diverse demographics. For context, the World Bank reported in 2023 that 35.27% of Bangladesh's workforce was in agriculture, 20.88% in industry, and a significant 43.85% in services[1]Source: World Bank, "Distribution of employment by economic sector, Bangladesh", databank.worldbank.org. Companies are not just fortifying products and experimenting with flavors, but also introducing premium cup formats. These moves are a direct response to growing health concerns and evolving taste preferences, underscoring brand differentiation. Furthermore, corporations are channeling investments into automated production lines and rigorous internal testing, ensuring they meet regulatory standards while simultaneously driving down unit costs. The competitive landscape is intensifying, with multinational players rolling out value-added offerings. In response, local producers are innovating with pricing strategies and regional flavors, ensuring both visibility and trial for the category.

Key Report Takeaways

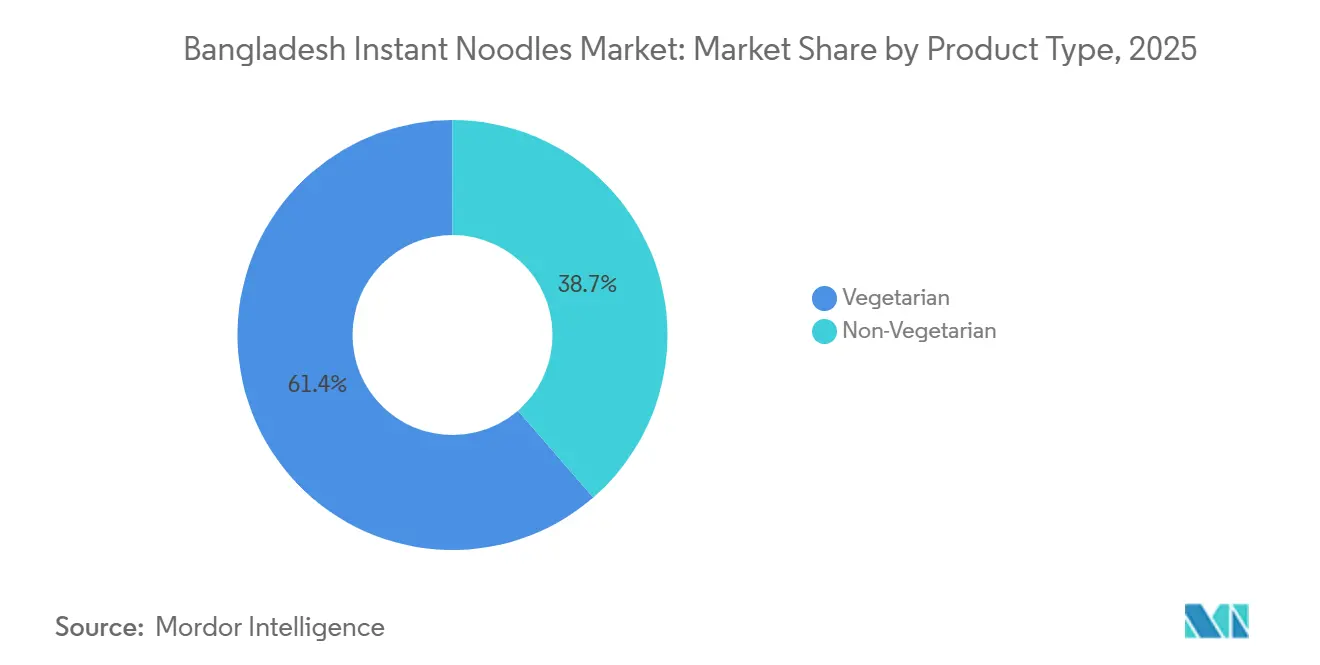

- By product type, vegetarian variants led with 61.35% of Bangladesh's instant noodles market share in 2025, yet non-vegetarian options are expanding at an 8.54% CAGR through 2031.

- By serving size, single-serve packs commanded 64.10% share of the Bangladesh instant noodles market size in 2025, whereas multi-serve formats are climbing at an 8.33% CAGR to 2031.

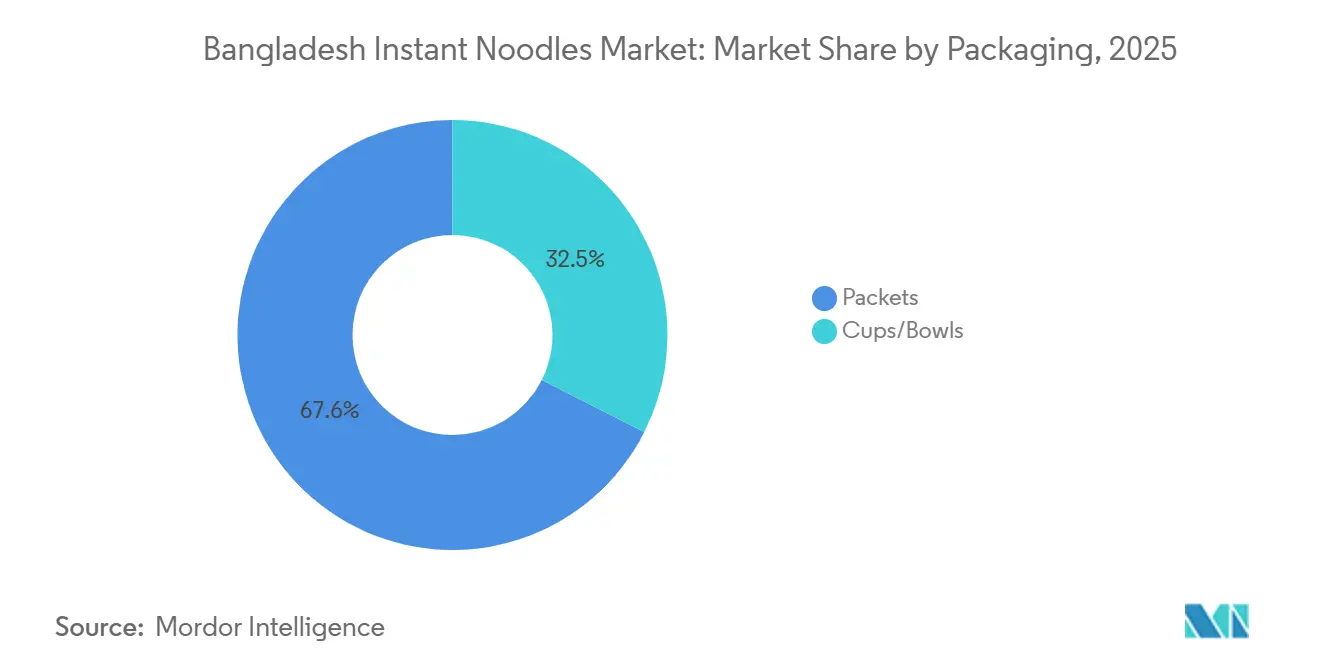

- By packaging, packets held 67.55% revenue share in 2025; cups and bowls are forecast to grow at an 7.86% CAGR through 2031.

- By flavor, chicken claimed 59.10% share in 2025, while masala/spicy variants are advancing at a 9.18% CAGR to 2031.

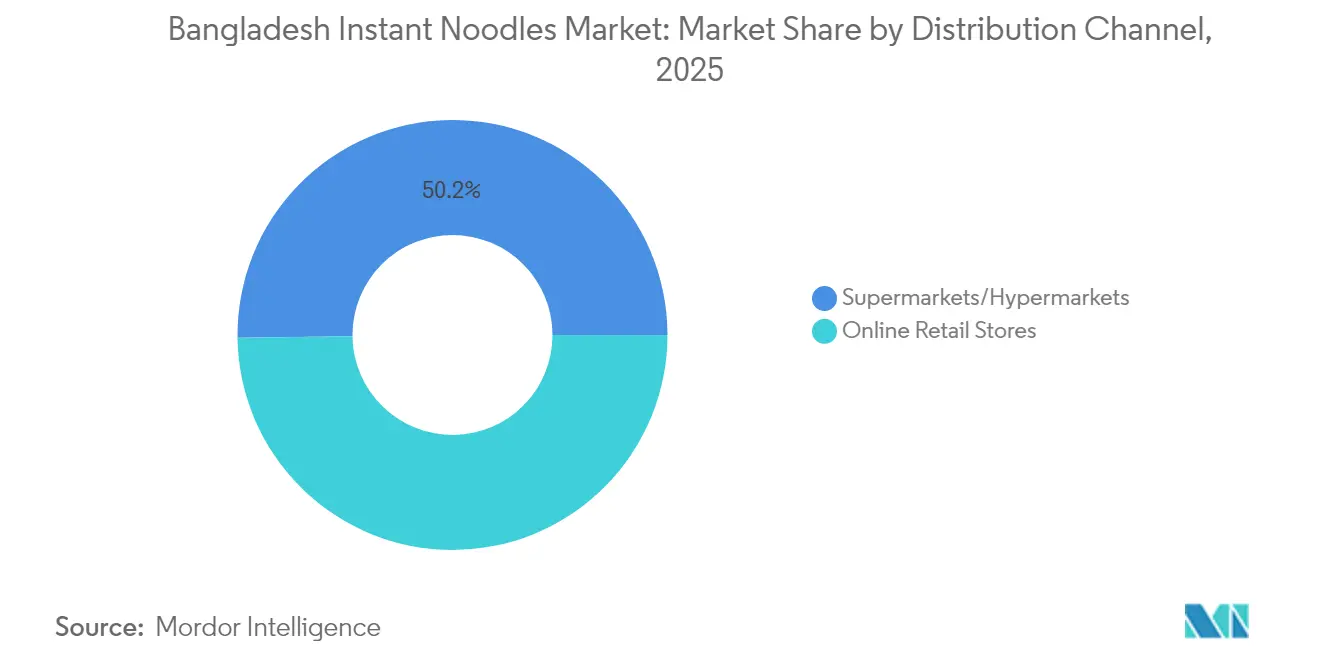

- By distribution channel, supermarkets and hypermarkets accounted for 50.20% of the 2025 value; online retail is rising at a 10.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Instant Noodles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product innovation and variety | +1.8% | National, concentrated in Dhaka, Chattogram | Medium term (2-4 years) |

| Growing preference for snacking and fast food | +2.1% | Urban centers with spillover to rural areas | Short term (≤ 2 years) |

| Expansion of retail and e-commerce | +1.5% | National, led by major cities | Long term (≥ 4 years) |

| Influence of digital marketing and social media | +1.2% | National, youth-focused demographics | Medium term (2-4 years) |

| Convenience and minimal cooking | +0.9% | Urban areas, working population segments | Short term (≤ 2 years) |

| Taste and sensory appeal | +0.5% | National, culturally driven preferences | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Innovation and Variety

Meghna Group's Fresh brand is taking the lead in fortification strategies, adding Vitamins B2, C, D, and Zinc to its instant variants. Meanwhile, its cup noodles now boast added Calcium and Iodine, directly targeting nutritional deficiencies. This proactive approach tackles the pressing issue of micronutrient malnutrition in Bangladesh, where, as highlighted by the World Bank, anaemia rates are notably high among children and non-pregnant, non-lactating women. Local manufacturers are not just stopping at fortification; they're elevating product quality by harnessing European technology and sourcing raw materials from Ireland and India. Their export-driven focus, reaching markets in Italy, the UK, France, and Japan, underscores a commitment to international quality benchmarks. With a staggering 93.7% of consumers aware of food adulteration, as reported by the Bangladesh Food Safety Authority, there's a pronounced push for transparent ingredient sourcing and nutritional enhancements.

Growing Preference for Snacking and Fast Food

According to ICDDR, B research, fast food consumption among adolescents has doubled, driven by an urban lifestyle transformation that accelerates snacking adoption. This shift, in tandem with Bangladesh's urbanization and rising disposable income, especially among the youth, has fostered a sustained demand for convenient meal solutions. The World Bank reported that in 2023, 40.47% of Bangladesh's population resided in urban areas, marking a 35.33% point increase since 1960[2]Source: World Bank, "Share of urban population in Bangladesh", www.databank.worldbank.org. Youth, influenced by global food trends on social media, are at the forefront of this change. Snacking preferences have evolved; instant noodles are now favored not just as meal replacements but also as between-meal snacks and late-night treats. The evolution of street food in Bangladesh, transitioning from traditional offerings like piyaju and singara to global favorites such as pizza, momos, and burgers, underscores a cultural openness to diverse flavors. This shift has expanded the variety of instant noodles in the market. Yet, this trend brings competitive pressure: street vendors, earning a monthly USD 350-400 (Tk 30,000-35,000), provide affordable alternatives, challenging the position of convenience foods against these culturally ingrained informal food systems.

Expansion of Retail and E-commerce

In June 2024, foodpanda unveiled its private label 'bright', boasting over 200 SKUs, underscoring its dedication to expanding in the food sector. While e-commerce currently accounts for just 3.8% of total retail, platforms like Chaldal, Shwapno, and Daraz are poised to capitalize on this growth, broadening their grocery selections and enhancing delivery services. In 2024, ShopUp, with a revenue of USD 129 million, and Priyoshop, boasting a GMV of USD 436 million, are spearheading B2B digitization. Their efforts empower small retailers to swiftly procure instant noodles, overcoming traditional distribution hurdles in rural areas. Facebook merchants dominate social commerce, accounting for 40% of online transactions, offering instant noodle brands a fresh avenue to engage younger consumers. The retail landscape is further buoyed by a surge in digital payment adoption and the rise of mobile financial services, which have diminished the cash reliance that once hampered online food purchases.

Influence of Digital Marketing and Social Media

With millions of users, social media has become a potent platform for brand engagement. A significant portion of these users encounters environmental campaigns online, suggesting they are receptive to brand messaging and product positioning. DataReportal highlights that, as of February 2025, Bangladesh boasts over 59.95 million Facebook users. Influencers like Iftekhar Rafsan, with their millions of followers, offer instant noodle brands authentic endorsements that resonate deeply with their target audience. Thanks to AI-driven personalization and data analytics, digital marketing has become more sophisticated, allowing brands to target consumer segments based on their purchasing behaviors and taste preferences. Social media not only accelerates the dissemination of food trends but also speeds up flavor innovation cycles. These platforms provide swift consumer feedback on new product launches and variant preferences. Furthermore, the digital realm influences recipe sharing and preparation techniques, elevating instant noodles from mere standalone products to versatile ingredients. This shift broadens their consumption occasions and increases their frequency of use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative convenient foods | -1.4% | National, strongest in urban areas | Short term (≤ 2 years) |

| Sustainability and packaging waste | -0.8% | Urban centers, environmentally conscious segments | Medium term (2-4 years) |

| Regulatory compliance and food safety concerns | -0.6% | National, manufacturing and import focused | Long term (≥ 4 years) |

| Growing consumer health consciousness | -1.1% | Urban educated demographics, spreading rural | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Convenient Foods

In Dhaka, street food vendors cater to 2 million customers daily, exerting significant competitive pressure. They offer fresh, culturally authentic dishes at prices that rival those of instant noodles. Meanwhile, live bakeries sprouting across Dhaka neighborhoods sell fresh bread and savory items for Tk 20-30 (USD 0.17-0.26). These bakeries not only compete on convenience and affordability but also ensure transparency by showcasing their production processes. Companies like Paragon Agro are rapidly expanding their frozen food offerings, which include chicken nuggets (500g priced at Tk 332) and vegetable spring rolls. These products provide protein-rich, convenient alternatives, addressing the nutritional concerns often associated with instant noodles. The competitive landscape intensifies as traditional wet markets continue to dominate food retail. At the same time, services offering home-cooked meals and ready-to-eat local products capitalize on cultural preferences and perceived health benefits. Furthermore, regulatory oversights in licensing street food vendors grant informal competitors a pricing edge, allowing them to sidestep compliance costs that formal manufacturers inevitably shoulder.

Growing Consumer Health Consciousness

In Bangladesh, rising diabetes rates are prompting a closer look at processed food consumption, with instant noodles facing the brunt of this scrutiny from health-conscious consumers, as highlighted by the Bangladesh Food Safety Authority. The International Diabetes Federation reports that in 2024, Bangladesh allocated an average of USD 74 per diabetic patient[3]Source: International Diabetes Federation, "IDF Diabetes Atlas - Eleventh Edition (2025)", diabetesatlas.org. With 30% of the population grappling with obesity and metabolic syndrome, there's a pressing medical push for dietary changes. Consequently, healthcare professionals are increasingly advocating for a reduction in processed food consumption. As consumers become more aware of food adulteration and the presence of harmful chemicals in foods, there's a marked shift towards natural ingredients and transparent labeling. However, instant noodles often fall short in these areas. Studies on front-of-package labeling reveal a growing consumer interest in nutritional information. This trend is pressuring manufacturers to either reformulate their products or risk losing market share to healthier alternatives. While urban, educated demographics are at the forefront of this health consciousness trend, its reach is extending to rural areas, thanks to digital media and healthcare awareness campaigns. This shift poses significant challenges for traditional instant noodle formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetarian Dominance Faces Protein Transition

In 2025, the vegetarian segment commands a dominant 61.35% market share in Bangladesh, underscoring the nation's cultural and economic leanings towards plant-based diets. These preferences resonate with traditional values and economic considerations. Yet, the non-vegetarian segment is on the rise, boasting an impressive 8.54% CAGR projected through 2031. This surge indicates a pivotal shift in protein consumption, largely fueled by increasing disposable incomes and urbanization. For manufacturers, this evolving landscape presents a challenge: they must navigate the entrenched vegetarian demand while catering to the burgeoning appetite for diverse protein options, especially among the younger, urban demographic.

While vegetarian products enjoy a stronghold due to cultural acceptance and religious mandates, non-vegetarian offerings are carving out their niche through innovative flavors and premium branding. Given the pronounced growth in the non-vegetarian sector, it's imperative for manufacturers to channel their development and marketing efforts towards this segment, all while safeguarding their leadership in the vegetarian domain. Both segments face equal scrutiny from regulatory bodies, with the Bangladesh Food Safety Authority mandating uniform testing protocols for glutamic acid, preservatives, and contaminants, irrespective of the protein source.

By Serving: Single Serve Convenience Meets Family Economy

As of 2025, single-serve packs command a dominant 64.10% market share, but multi-serve packs are on a trajectory, boasting an impressive 8.33% CAGR growth projected through 2031. This shift underscores a transformation in household purchasing behaviors, with economic optimization and a tilt towards bulk buying coming to the fore. Such dynamics are emblematic of Bangladesh's price-sensitive consumers, who are increasingly seeking value, especially in the face of inflationary pressures. As household budgets tighten, families are becoming more discerning, emphasizing cost-per-serving efficiency. Furthermore, the evolving serving sizes hint at a broader shift in consumption patterns: instant noodles are no longer just a quick snack but are increasingly being embraced as family meal solutions.

Single-serve packs, while holding the market's reins, owe their leadership to a strategic focus on convenience and the allure of portion control. This appeal resonates strongly with office workers and students, both of whom are often in search of swift meal solutions. The choice of packaging format plays a pivotal role in shaping distribution strategies. Single-serve packs find their niche in convenience stores and street vendors, whereas multi-serve packs are more at home in supermarkets and bulk retail channels. For manufacturers, the challenge lies in optimizing production lines to cater to both formats, all while navigating the complexities of inventory management across a spectrum of retail partnerships. This segmentation in serving sizes not only carves out avenues for premium pricing in single serves but also paves the way for volume-driven margins in multi-serve formats.

By Packaging: Traditional Packets Yield to Cup Innovation

By 2031, cups and bowls are projected to grow at an 7.86% CAGR, challenging the 67.55% market dominance held by packets in 2025. This shift underscores a changing consumer preference, leaning towards convenience and premium offerings. As urbanization rises, consumers increasingly value easy preparation and consumption, especially in offices and during commutes where traditional cooking isn't an option. Given the growth of the cup format, manufacturers are urged to boost production and distribution in this segment to meet the surging demand.

While packet formats benefit from cost advantages and cultural familiarity, ensuring their market leadership among price-sensitive and tradition-oriented consumers, cups and bowls present distinct advantages. They offer enhanced branding opportunities, better portion control, and a convenience factor that supports premium pricing. This shift in packaging not only reshapes market dynamics but also has supply chain ramifications. The specialized equipment and material sourcing needed for cup formats may give larger manufacturers, who benefit from economies of scale, a competitive edge. Furthermore, as consumer awareness of packaging waste intensifies, environmental considerations are taking center stage in packaging decisions, with sustainable materials emerging as key differentiators.

By Flavor Profile: Chicken Leadership Faces Spicy Disruption

Bangladesh's shifting taste preferences are evident as masala and spicy variants project a robust 9.18% CAGR growth through 2031. In contrast, chicken commands a dominant 59.10% market share in 2025. This evolution underscores the nation's cultural affinity for spiced foods and a younger demographic eager to explore bold flavors. Such dynamics present manufacturers with a chance to stand out, leveraging regional spice blends and varying heat intensities. The spicy segment's rapid ascent not only highlights adept market positioning but also hints at a lucrative premium pricing strategy.

Chicken flavoring, with its universal appeal and protein association, continues to lead the market. This dominance not only justifies ongoing investments in the chicken segment but also nudges manufacturers to tap into the burgeoning spicy variants. Meanwhile, beef and seafood flavors cater to niche markets, driven by distinct cultural and regional preferences. Vegetarian options, on the other hand, resonate with the rising trends of dietary restrictions and health consciousness. This intricate flavor segmentation poses challenges in inventory management, compelling manufacturers to strike a balance between established offerings and emerging taste trends. To innovate successfully, a deep understanding of regional spice preferences and heat tolerance across Bangladesh's varied demographics is essential.

By Distribution Channel: Traditional Retail Meets Digital Acceleration

Bangladesh's retail landscape is undergoing a notable transformation. While online retail stores are projected to grow at a remarkable CAGR of 10.35% through 2031, supermarkets and hypermarkets command a significant 50.20% market share in 2025. This shift indicates that digital channels are increasingly capturing demand, yet traditional formats continue to lead in volume. As this distribution landscape evolves, manufacturers face strategic imperatives: they must cultivate omnichannel capabilities and fine-tune inventory allocation across varied retail partnerships. The surge in online retailing is bolstered by advancements in logistics infrastructure and a growing acceptance of digital payments. This progress has empowered instant noodle brands to penetrate rural markets that were once overlooked.

Supermarkets and hypermarkets maintain their dominance in distribution, thanks to ingrained consumer shopping habits and the perks of bulk purchasing. Meanwhile, convenience and grocery stores excel in offering accessibility and catering to impulse buys. This diversification in channels compels manufacturers to tailor their packaging, pricing, and promotional strategies to fit each distribution format. However, they must also navigate potential channel conflicts and strive for margin optimization. Online platforms present a distinct advantage: they provide richer consumer data insights and more precise marketing capabilities than traditional retail avenues. This edge underscores the competitive advantage for brands that adeptly harness digital channels. As the distribution landscape shifts, it's clear that manufacturers aiming for success must strike a balance: nurturing traditional retail ties while investing in digital channels to harness both present volumes and future growth prospects.

Geography Analysis

Urban centers, especially Dhaka and Chattogram, dominate Bangladesh's instant noodle consumption, fueled by rising disposable incomes, shifting lifestyles, and robust retail networks. However, as urbanization surges and rural connectivity improves, the once-concentrated demand is now reaching deeper into rural areas. This urban-centric consumption not only drives economies of scale in distribution and marketing but also offers manufacturers a focused audience for premium product launches and targeted promotions.

With platforms like Chaldal and foodpanda pushing delivery services into rural territories, the expansion is further bolstered by a youthful demographic. Rural youth, influenced by social media and newfound economic prospects, are mirroring urban consumption habits. Instant noodles, once a city staple, are now being embraced in rural areas as a quick, affordable protein source, bridging the rural-urban consumption divide.

Regional taste nuances present segmentation avenues: northern districts lean towards spicier variants, while coastal regions gravitate to seafood flavors, echoing local culinary customs. This regional diversity compels manufacturers to tailor flavor profiles and marketing strategies, yet they strive for production efficiency with standardized base formulations. While remote areas pose distribution hurdles, they also open doors for local collaborations and creative last-mile delivery methods, tapping into previously overlooked segments. Across the board, regulatory standards remain steadfast, with the Bangladesh Food Safety Authority ensuring uniformity in testing and compliance, irrespective of the region.

Competitive Landscape

The Bangladesh instant noodles market remains moderately fragmented, characterized by the presence of both established domestic manufacturers and multinational brands competing across multiple price segments. PRAN-RFL Group continues to lead the market through its integrated manufacturing capabilities, extensive nationwide distribution network, and strong retail penetration, enabling widespread product availability. Nestlé leverages its global research and development expertise to introduce premium cup noodles and value-added offerings targeted at urban professionals and convenience-seeking consumers. At the same time, Unilever benefits from its well-established distribution infrastructure, utilizing synergies with its beverages and condiments businesses to secure a strong shelf presence across modern trade and traditional retail channels.

Regional and international competitors continue to strengthen their market positions through differentiated strategies. IFAD Multi Products, one of the leading local players, enhances its competitiveness by sourcing wheat domestically, improving cost efficiency, and maintaining flexible manufacturing lines that allow rapid introduction of new flavors aligned with changing consumer preferences. Meanwhile, Samyang Foods focuses on premium and spicy Korean-style noodles, relying primarily on e-commerce platforms, specialty stores, and modern retail outlets rather than competing directly in the mainstream mass-market segment. This targeted approach enables the company to appeal to younger consumers and early adopters seeking international flavors and premium eating experiences.

Competition is increasingly shaped by evolving consumer preferences, retail requirements, and digital engagement. Modern retail chains and distributors now expect stringent quality assurance, food safety certifications, and accredited laboratory documentation from manufacturers, making regulatory compliance an important competitive differentiator. At the same time, brands are investing heavily in digital marketing through platforms such as TikTok and Facebook Reels, where recipe challenges, food influencers, and snack trends significantly influence purchasing behavior among Gen Z consumers. Looking ahead, companies are prioritizing fortified formulations, recyclable packaging materials, sustainable production practices, and digital supply chain optimization to enhance operational efficiency, strengthen brand loyalty, and maintain profitability in Bangladesh's highly price-sensitive yet increasingly aspirational instant noodles market.

Bangladesh Instant Noodles Industry Leaders

-

Unilever PLC

-

Nestle SA

-

PRAN-RFL Group Ltd.

-

IFAD Multi Products Ltd.

-

Kallol Thai President Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Wai Wai Noodles, one of the major players in Bangladesh, introduced three bold and irresistible instant noodle flavors, setting the stage for an exciting culinary journey. This underlined its position as a major market player in the highly competitive instant noodle segment. Known for its innovative approach and commitment to satisfying diverse taste preferences, Wai Wai is redefining the instant noodle experience again.

- December 2023: SQUARE Food and Beverage's instant noodle brand, Chopstick, ran a Mother's Day campaign titled "Ma Manei Sob Bhalo" (Mother means everything). This campaign and the related events reinforce the brand's marketing efforts and focus on engaging with its consumer base.

- July 2023: Mr. Noodles, a leading brand under the PRAN Group, launched a Korean Kimchi Ramen Noodles product in Bangladesh. The launch was part of the company's strategy to introduce popular international flavors to the local market. The product, available in an eight-piece family pack, was distributed through various retail channels, including supermarkets and the e-commerce site Othoba.com.

- July 2023: Square Food and Beverage Limited launched its instant noodles brand "Chopstick" in Bangladesh, which was asserted to be conscious about the physical and mental development of children. As part of these efforts, Chopstick organized a campaign on Mother's Day titled "Ma Manei Sob Bhalo" (Mother means everything).

Bangladesh Instant Noodles Market Report Scope

Instant noodles are precooked and dried, packed with different flavored seasonings and oils. The seasonings can be available in a separate sachet or loose in the pack itself.

The Bangladesh instant noodles market is segmented by product type and distribution channel. By product type, the market is segmented into cups/bowls and packets. By distribution channel, the market is segmented into supermarkets/hypermarkets, grocery stores, online retail stores, and other distribution channels.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Vegetarian |

| Non-Vegetarian |

By Serving

| Single Serve Packs |

| Multi Serve Packs |

By Packaging

| Packets |

| Cups/Bowls |

By Flavor Profile

| Chicken |

| Masala/Spicy |

| Beef |

| Seafood |

| Vegetarian |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Vegetarian |

| Non-Vegetarian | |

| By Serving | Single Serve Packs |

| Multi Serve Packs | |

| By Packaging | Packets |

| Cups/Bowls | |

| By Flavor Profile | Chicken |

| Masala/Spicy | |

| Beef | |

| Seafood | |

| Vegetarian | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the forecast value for the Bangladesh instant noodles market by 2031?

The category is projected to reach USD 157.28 million by 2031, reflecting a 7.34% CAGR.

Which segment currently holds the largest market share?

Vegetarian variants led with 61.35% share in 2025.

How fast is online retail growing in this category?

Online sales are expected to record a 10.35% CAGR through 2031.

Which packaging type is expanding the fastest?

Cup and bowl formats are increasing at an 7.86% CAGR thanks to portability benefits.

Who are the top three players in the market?

PRAN-RFL Group, Nestlé, and Unilever occupy the leading positions.

What is the major restraint facing manufacturers?

Rising health consciousness, linked to diabetes and metabolic syndrome concerns, is dampening repeat purchases among urban consumers.

Page last updated on: