Multi-Mode Chipset Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 22.22 Billion |

| Market Size (2030) | USD 46.70 Billion |

| Growth Rate (2025 - 2030) | 16.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Mode Chipset Market Analysis by Mordor Intelligence

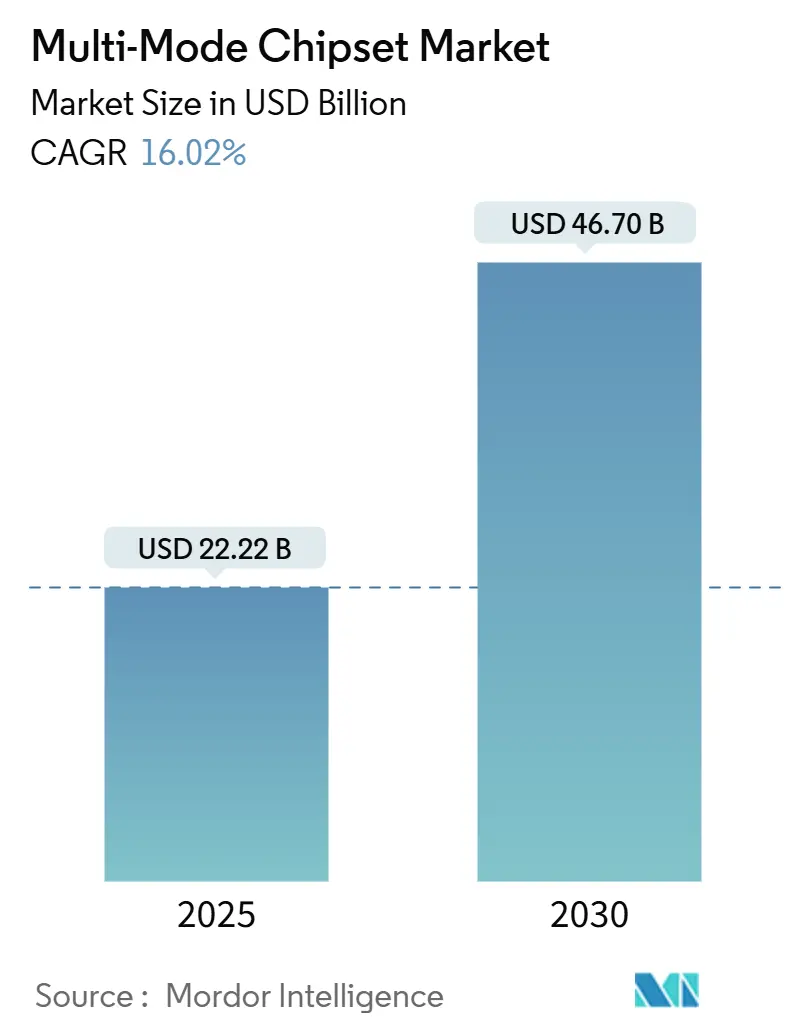

The multi-mode chipset market size stands at USD 22.22 billion in 2025 and is projected to reach USD 46.70 billion by 2030, expanding at a 16.02% CAGR. This momentum reflects the semiconductor sector’s rapid shift toward heterogeneous integration that combines cellular modems, AI accelerators, and edge-computing blocks within a single die or package. Demand tailwinds include the migration of 5G into sub-USD 250 smartphones, regulatory mandates for connected vehicles, and the steady rise of industrial IoT deployments. At the same time, the transition to 3 nm and 5 nm nodes unlocks higher transistor density for advanced on-device AI, enabling chipset suppliers to charge premium prices while lowering power envelopes. Supply-side vulnerabilities chiefly export controls and thermal limits in 3D stacks temper near-term upside but do not derail the broader growth trajectory.

Key Report Takeaways

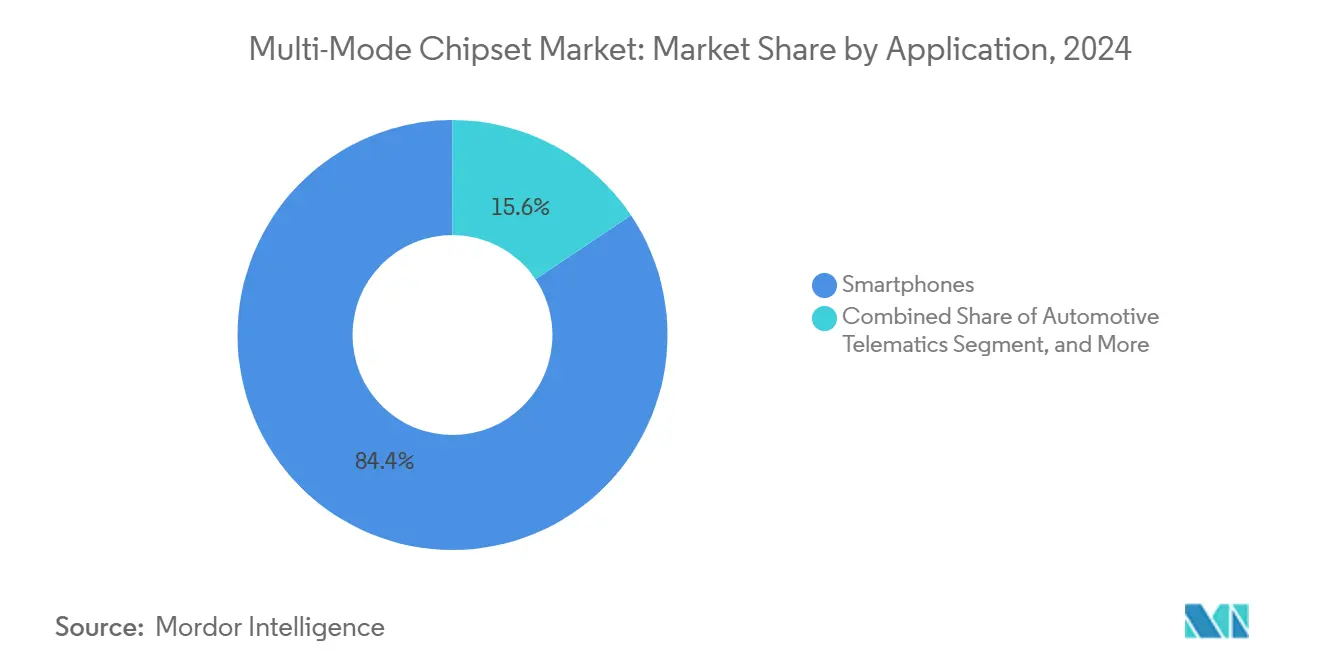

- By application, smartphones led with an 84.40% revenue share in 2024; automotive telematics is forecast to expand at a 17.21% CAGR through 2030.

- By integration type, system-on-chip architectures held 72.30% of the multi-mode chipset market share in 2024, while embedded communication modules are poised for the fastest CAGR at 19.56% to 2030.

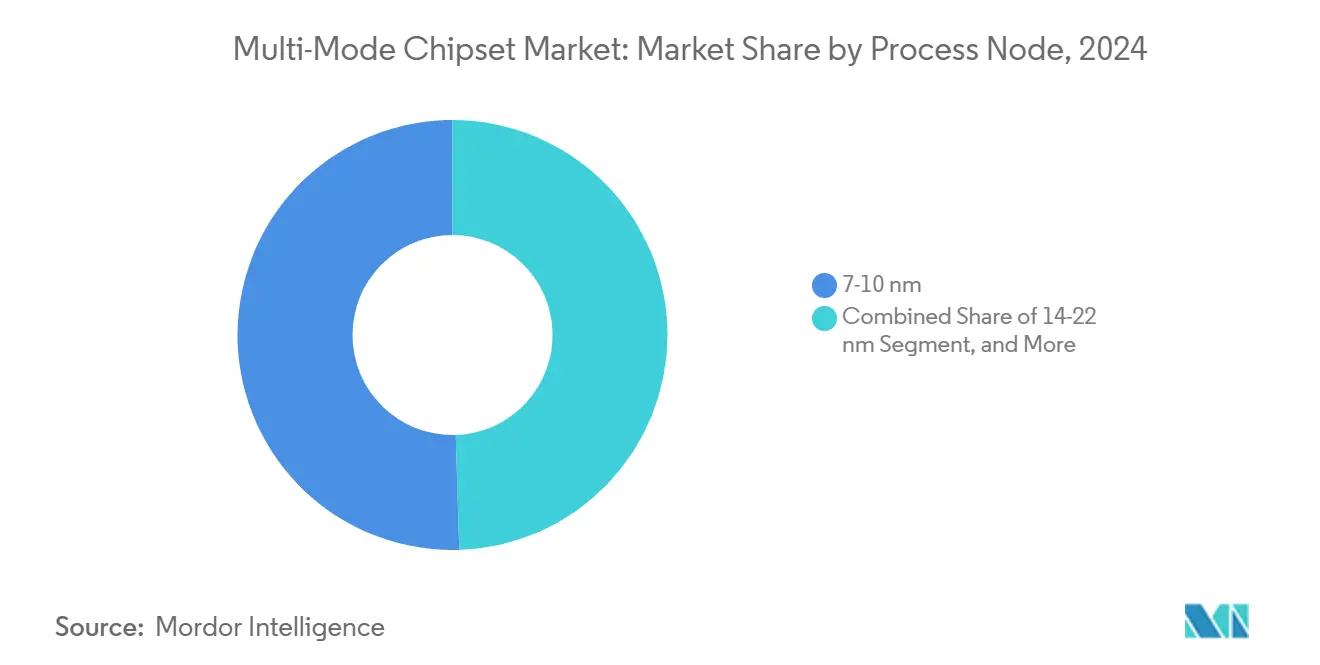

- By process node, the 7-10 nm class accounted for 50.50% share of the multi-mode chipset market size in 2024, whereas ≤5 nm nodes are projected to grow at a 17.80% CAGR during 2025-2030.

- By frequency band support, Sub-6 GHz solutions captured 68.22% share in 2024, and dual-band Sub-6 GHz plus mmWave chipsets are advancing at an 18.44% CAGR to 2030.

- By end-use industry, consumer electronics commanded 79.89% of 2024 revenue, but industrial IoT applications are set to post the highest 18.77% CAGR through 2030.

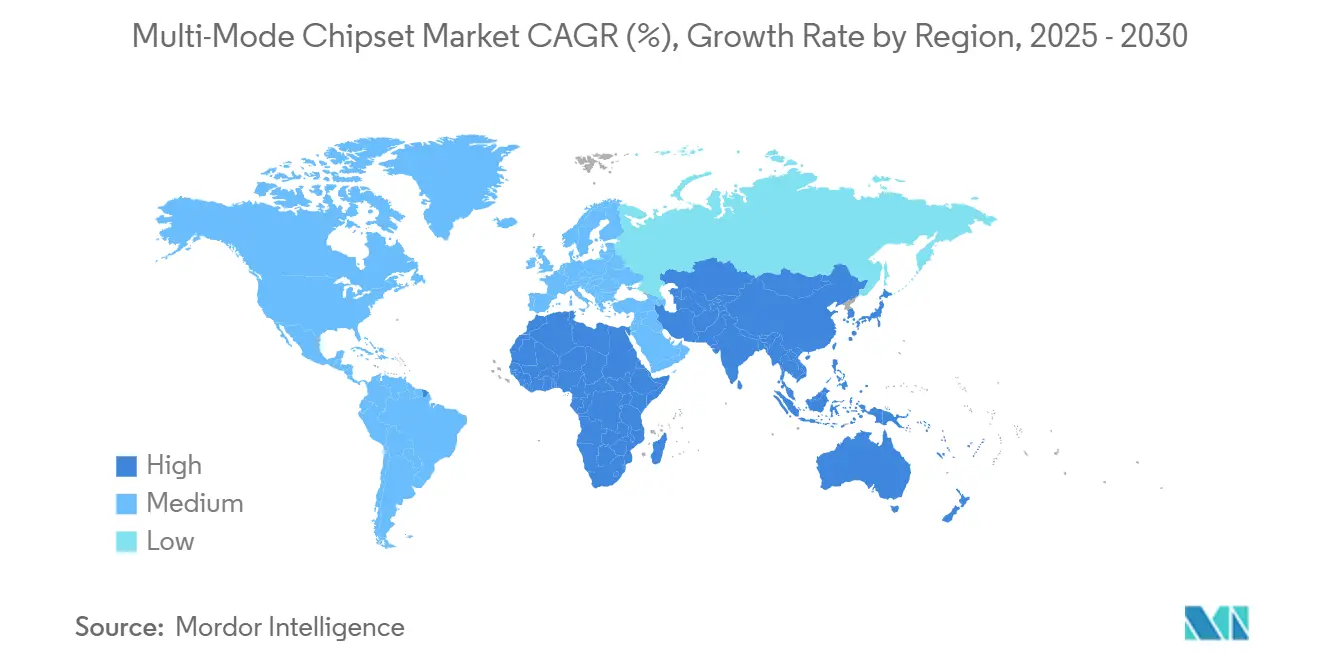

- By geography, Asia-Pacific Asia Pacific maintains market leadership with 57.77% share in 2024 and accelerates at 20.21% CAGR through 2030.

Global Multi-Mode Chipset Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Efficient Integrated SoCs for Sub-USD 250 5G Phones | +3.2% | Global, with concentration in APAC and emerging markets | Medium term (2-4 years) |

| Rapid Adoption of On-Device AI Accelerators | +4.1% | North America, APAC core markets, spill-over to Europe | Short term (≤ 2 years) |

| Expansion of RedCap and NB-NTN Standards in IoT Devices | +2.8% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Transition to 3 nm and 5 nm Nodes in Flagship Smartphones | +3.5% | APAC manufacturing hubs, North America design centers | Medium term (2-4 years) |

| Localization of Chip Supply Chains in India and Southeast Asia | +1.9% | APAC region, with strategic implications for global supply | Long term (≥ 4 years) |

| Government Incentives for Mature-Node Capacity (22-28 nm) | +1.8% | North America, Europe, select APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficient Integrated SoCs for Sub-USD 250 5G Phones

Energy-optimized SoCs reduce external components by 30%, enabling 5G connectivity in budget devices without breaching thermal envelopes. MediaTek’s Dimensity 6300 and Qualcomm’s Snapdragon 4s Gen 2 exemplify the strategy, opening large addressable bases in price-sensitive markets.

Rapid Adoption of On-Device AI Accelerators

Dedicated neural engines now define mainstream product roadmaps. Apple’s A18 Pro reaches 35 TOPS, while MediaTek’s APU 790 pushes 45 TOPS, cutting cloud inference costs by 40-60% for typical smartphone AI workloads.On-device AI acceleration has evolved from premium smartphone differentiator to essential functionality across consumer and industrial applications, fundamentally altering chipset architecture requirements.

Expansion of RedCap and NB-NTN Standards in IoT Devices

RedCap (Reduced Capability) and NB-NTN (Narrowband Non-Terrestrial Network) standards emergence creates new market categories for multi-mode chipsets optimized for IoT applications requiring extended battery life and global connectivity. 3GPP Release 18 enables 10-year battery life and satellite backhaul, catalyzing asset-tracking and remote-sensor use cases. Qualcomm’s X35 and MediaTek’s T830 achieve 70% lower power draw than legacy 5G modems.[1]“Release 18 Specifications,” 3GPP, 3gpp.org

Transition to 3 nm and 5 nm Nodes in Flagship Smartphones

Advanced process node adoption accelerates as smartphone manufacturers pursue performance differentiation and AI capability enhancement, despite significant cost premiums and yield challenges. TTSMC’s 3 nm node delivers 35% power savings and 15% performance gains over 5 nm, justifying 20-25% cost premiums and creating a two-tier device landscape

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TCPA Compliance and Regulatory Complexity | -1.8% | North America primarily, with spillover to global operations | Short term (≤ 2 years) |

| Data Privacy and Security Concerns | -1.5% | Global, with acute impact in Europe (GDPR) and North America | Medium term (2-4 years) |

| Integration Complexity with Legacy Systems | -1.2% | Global, particularly affecting large enterprises | Medium term (2-4 years) |

| High Implementation and Training Costs | -0.9% | Global, with higher impact in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Geopolitical Export Controls on 5G IP

Export control restrictions on 5G intellectual property create market fragmentation and development delays, particularly affecting Chinese chipset vendors' access to advanced radio frequency designs and standards-essential patents. Entity-List restrictions lengthen Chinese vendors’ time-to-market by up to 18 months and inflate R&D outlays, reshuffling share toward suppliers with unrestricted access.[2]“Entity List,” U.S. Department of Commerce, doc.gov

Thermal-Management Limits in Heterogeneous 3D Stacks

Heterogeneous 3D integration creates thermal density challenges that constrain performance scaling in advanced multi-mode chipsets, particularly as AI accelerators and 5G modems operate simultaneously within compact form factors. Junction temperatures above 85 °C force performance throttling, keeping sustained AI processing at 60-70% of peak. Advanced interface materials add USD 3-5 per unit and prolong design cycles

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Smartphones Dominate Volume While Automotive Accelerates Value

The multi-mode chipset market size for smartphones equaled USD 18.76 billion in 2025, accounting for 84.40% of total revenue. Flagship handsets depend on integrated modems and AI engines to differentiate user experience, whereas mid-tier models balance cost with 5G capability. Automotive telematics, though smaller in units, is advancing at a 17.21% CAGR as regulators mandate eCall, over-the-air updates, and advanced driver-assistance connectivity. Premium pricing—three to four times smartphone average selling prices—stems from extended temperature ranges, functional safety certifications, and decade-long supply guarantees. Tablets and fixed wireless CPE sustain demand where 5G replaces fiber, while wearables pursue extreme integration to fit space-constrained enclosures.

Smartphone supremacy remains important for economies of scale, but the revenue mix is tilting toward high-value vehicular, industrial, and CPE segments that demand durable, secure, and mission-critical performance. Telematics control units increasingly embed multi-band 5G plus GNSS and V2X radios, providing future-proof designs for autonomous driving. Meanwhile, industrial IoT deployments integrate chipsets with deterministic networking to support time-sensitive manufacturing processes. This demand diversity reduces reliance on cyclical handset volumes and stabilizes long-term supplier margins.

By Frequency Band Support: Sub-6 GHz Leads While Dual-Band Integration Gains Speed

In 2024, Sub-6 GHz-only solutions held 68.22% of the multi-mode chipset market share, thanks to widespread 5G non-stand-alone rollouts that prioritize coverage. Enterprises deploying private 5G emphasize low-band performance for wide-area reach, reinforcing Sub-6 GHz demand. Yet dual-band Sub-6 GHz plus mmWave devices are expected to grow at an 18.44% CAGR because ultra-low latency is essential for AR/VR streaming, industrial robotics, and fixed wireless fiber-substitution. Dual-band designs must contend with increased RF front-end complexity that raises bill-of-materials by up to USD 12 per device.

Operators worldwide refarm 2G/3G spectrum to expand 5G coverage, encouraging chipset vendors to provide software-defined radios for backward compatibility. In parallel, the United States Federal Communications Commission allocates additional 6 GHz and 7 GHz bands, prompting future-proof architectures that can quickly adapt to new allocations. Vendors investing in flexible RFICs secure long-term design wins as customers seek to minimize platform churn.

By Integration Type: SoCs Lead While Modules Surge in IoT

System-on-chip designs captured 72.30% revenue in 2024 because fully integrated platforms slash power consumption and board area. Smartphone OEMs favor SoCs to consolidate modem, CPU, GPU, and NPU blocks, simplifying thermal design and lowering printed circuit board layers. However, embedded communication modules are climbing at a 19.56% CAGR, driven by industrial IoT devices that prize rapid certification and low development overhead. Pre-approved modules cut global regulatory approval cycles from 12-18 months to as little as 3 months, substantially improving time-to-revenue.

Module adoption aligns with the rise of original design manufacturers serving niche verticals such as smart logistics, connected agriculture, and environmental monitoring. Many of these end products ship in modest volumes, so module reuse across projects lowers unit economics. Stand-alone modems remain relevant in network equipment requiring flexible RF paths and in legacy devices migrating from 3G to 5G.

By Process Node: 7-10 nm Remains Mainstream as Sub-5 nm Ramps Fast

The 7-10 nm bracket retained 50.50% of 2024 revenue, balancing power and cost for high-volume mid-range handsets. Foundry wafer pricing in this node range offers favorable yields and mature equipment amortization, making it the sweet spot for OEMs targeting USD 350-500 retail tiers. Conversely, ≤5 nm nodes are accelerating at a 17.80% CAGR because AI-rich flagships and premium tablets require higher transistor density and lower leakage. TSMC’s 3 nm process delivers 35% lower power than its 5 nm predecessor, critical for sustaining on-device AI yet staying within smartphone thermal budgets.

Mature nodes 22 nm and 28 nm planar continue to serve cost-sensitive IoT sensors and narrowband modules, especially where longevity and wide voltage tolerance outweigh sheer performance. Government incentives in the United States and Europe encourage fabrication at these larger geometries to strengthen supply resilience, making them a stable profit center for foundries.

By End-Use Industry: Consumer Electronics Prevails While Industrial IoT Gains Momentum

Consumer electronics delivered 79.89% of 2024 revenue, sustained by relentless smartphone refresh cycles and the increasing attach rate of 5G modems in tablets, wearables, and premium laptops. Nonetheless, industrial IoT deployments are rising at an 18.77% CAGR, supported by Industry 4.0 initiatives that require robust, secure, and long-life communication links. Predictive maintenance, digital twins, and real-time analytics demand chipsets that integrate secure boot, deterministic networking, and low-power AI.

Automotive OEMs extend the service window for over-the-air updates, intensifying the need for multi-mode chipsets with 10-year supply commitments. Telecom infrastructure vendors also seek highly reliable multi-mode solutions for small cells and fixed wireless access gateways where concurrent Sub-6 GHz and mmWave links must coexist within tight thermal limits.

Geography Analysis

Asia Pacific held 57.77% of 2024 revenue for the multi-mode chipset market and is set to grow at a 20.21% CAGR to 2030. China’s smartphone production scale and 5G roll-outs, South Korea’s memory and packaging prowess, and India’s assembly incentives combine to form an integrated supply chain that lowers cost and speeds innovation. India’s Production Linked Incentive scheme aims to add USD 10 billion in assembly capacity by 2028. Southeast Asian nations such as Vietnam, Malaysia, and Thailand attract diversification from “China-plus-one” strategies, creating regional manufacturing nodes for OEMs.

North America contributes substantial design value through advanced SoC architecture, AI IP, and millimeter-wave RF expertise. The CHIPS and Science Act earmarks USD 52 billion in grants for domestic fabs and packaging plants, encouraging local production of high-margin, security-sensitive chipsets.[3] “CHIPS and Science Act Implementation,” National Institute of Standards and Technology, nist.gov Europe’s emphasis on automotive safety and industrial automation sustains demand for long-lifecycle, functionally safe chipsets. Regional policies under the European Chips Act seek to double Europe’s global semiconductor share by 2030, further diversifying supply.

Across all regions, governments align semiconductor funding with national security and competitiveness goals. As technology sovereignty rises on policy agendas, chipset vendors must partition supply chains, adopt secure-by-design frameworks, and comply with varying data-localization laws, complicating global product strategies but also creating localized growth pockets for partners and suppliers.

Competitive Landscape

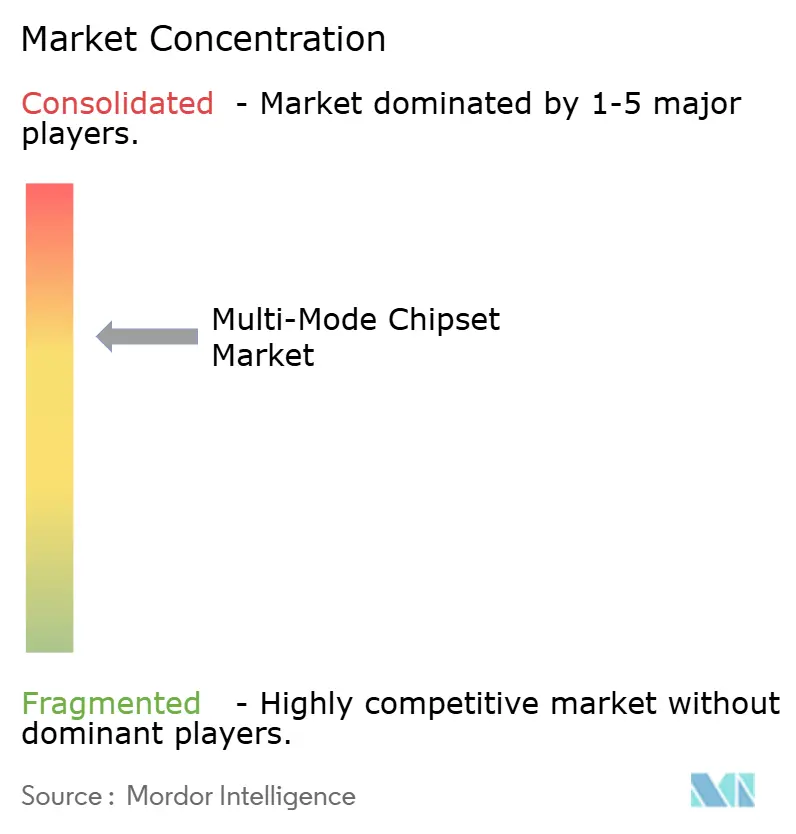

The multi-mode chipset market is moderately concentrated. Qualcomm leverages an extensive patent library and comprehensive modem-RF systems to retain leadership in premium and high-volume tiers. MediaTek competes aggressively in mainstream price bands through fast iteration and competitive pricing, narrowing performance gaps each design cycle. Apple’s vertically integrated silicon captures premium device margins while reducing external dependency, although the merchant chipset segment remains out of reach.

Emerging challengers address niche requirements. NXP and Renesas focus on automotive connectivity with ISO 26262 compliance. Unisoc targets budget Android handsets and low-cost IoT modules. Specialized players such as SatixFy and AST SpaceMobile develop non-terrestrial network solutions, extending connectivity beyond terrestrial cell grids. Barriers to entry remain high owing to modem patent pools, radio frequency front-end complexity, and the capital intensity of cutting-edge node R&D.

Strategically, incumbents pursue multi-chiplet packaging, AI core expansion, and greater software differentiation. The acquisition of VMware by Broadcom extends reach into software-defined networking, complementing enterprise-focused wireless chipsets. Intel’s USD 15 billion packaging investment aims to win automotive and industrial accounts looking for heterogeneous compute. Competitive dynamics now hinge on securing foundry capacity, navigating export controls, and delivering sustained AI performance within strict thermal budgets.

Multi-Mode Chipset Industry Leaders

MediaTek Inc.

Qualcomm Technologies Inc.

Apple Inc.

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Five9 launched its AI-powered Predictive Engagement Platform with advanced machine learning algorithms that optimize dialing patterns based on real-time customer behavior analytics. The platform integrates with Salesforce Service Cloud and Microsoft Dynamics 365, enabling contact centers to achieve up to 35% higher connection rates while maintaining TCPA compliance through intelligent call timing predictions.

- September 2025: Genesys completed its USD 2.1 billion acquisition of Nuance's enterprise communications division, expanding its predictive dialer capabilities with advanced speech analytics and natural language processing. The integration creates the industry's most comprehensive omnichannel customer experience platform, combining predictive dialing with real-time sentiment analysis and automated conversation intelligence.

- August 2025: Nice inContact announced a USD 150 million investment in its CXone platform to develop next-generation predictive dialer technology powered by generative AI. The enhanced system uses large language models to predict optimal contact strategies and automatically adjust dialing algorithms based on campaign performance, regulatory changes, and customer preference patterns.

- July 2025: RingCentral partnered with Microsoft to integrate predictive dialer functionality directly into Teams Phone, creating a unified communication solution for enterprise customers. The collaboration enables seamless transition between predictive dialing campaigns and collaborative work environments, targeting the USD 12 billion market for integrated business communications platforms.

Global Multi-Mode Chipset Market Report Scope

| Smartphones |

| Tablets |

| IoT Devices |

| Automotive Telematics |

| Fixed Wireless CPE |

| Wearables |

| Sub-6 GHz Only |

| Sub-6 GHz and mmWave |

| Legacy (≤4G) Multi-Mode |

| Stand-Alone Modem |

| Integrated SoC (Modem + Application Processor) |

| Embedded Communication Module |

| ≥28 nm |

| 14-22 nm |

| 7-10 nm |

| ≤5 nm |

| Consumer Electronics |

| Automotive |

| Industrial IoT |

| Telecom Infrastructure Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Application | Smartphones | |

| Tablets | ||

| IoT Devices | ||

| Automotive Telematics | ||

| Fixed Wireless CPE | ||

| Wearables | ||

| By Frequency Band Support | Sub-6 GHz Only | |

| Sub-6 GHz and mmWave | ||

| Legacy (≤4G) Multi-Mode | ||

| By Integration Type | Stand-Alone Modem | |

| Integrated SoC (Modem + Application Processor) | ||

| Embedded Communication Module | ||

| By Process Node | ≥28 nm | |

| 14-22 nm | ||

| 7-10 nm | ||

| ≤5 nm | ||

| By End-Use Industry | Consumer Electronics | |

| Automotive | ||

| Industrial IoT | ||

| Telecom Infrastructure Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for the multi-mode chipset market in 2030?

The market is projected to reach USD 46.70 billion by 2030, growing at a 16.02% CAGR.

Which application category is expected to grow fastest through 2030?

Automotive telematics chipsets are forecast to post a 17.21% CAGR thanks to regulatory mandates for connected vehicles.

Why are dual-band Sub-6 GHz plus mmWave chipsets gaining traction?

Enterprises need ultra-low latency and multi-gigabit speeds for AR/VR, industrial robotics, and fixed wireless access, driving an 18.44% CAGR for dual-band devices.

How do export controls influence chipset supply?

Restrictions on 5G IP prolong Chinese vendors’ development cycles by up to 18 months, shifting share toward suppliers with unrestricted access.

What process node leads mainstream production today?

The 7-10 nm node class dominates, holding 50.50% revenue share due to its cost-performance balance for high-volume smartphones.

Which region holds the largest market share?

Asia Pacific leads with 57.77% of 2024 revenue, bolstered by integrated manufacturing ecosystems in China, South Korea, and India.

Page last updated on: