Multilayer Ceramic Capacitor (MLCC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

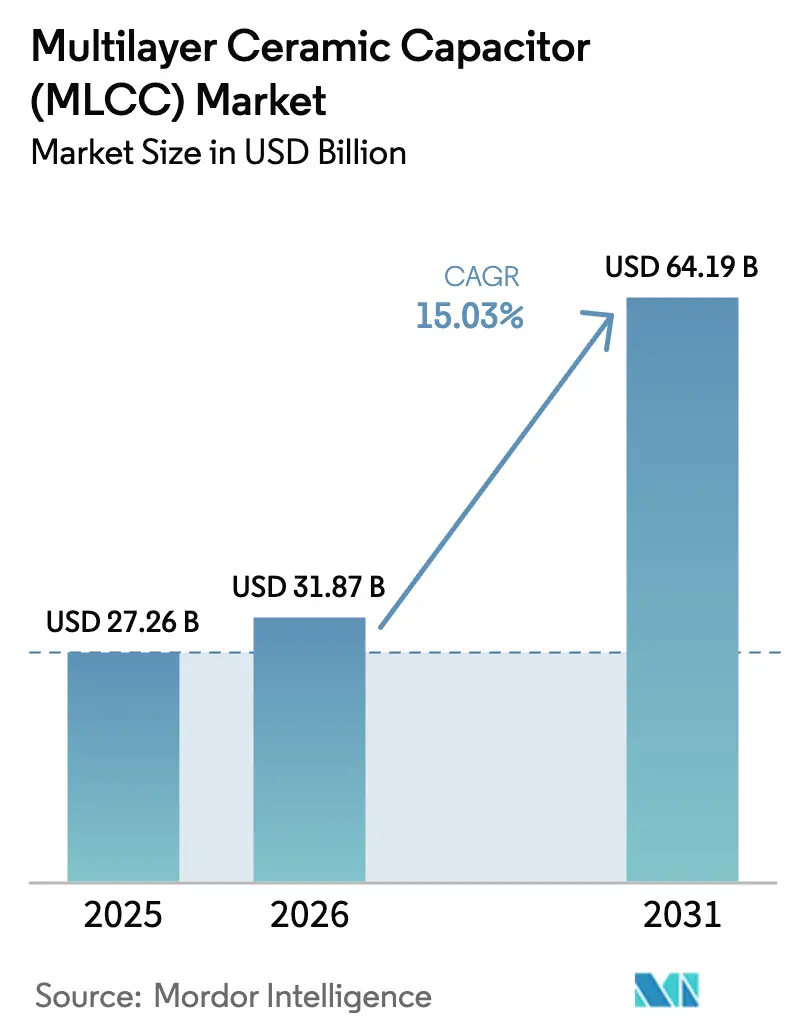

| Market Size (2026) | USD 31.87 Billion |

| Market Size (2031) | USD 64.19 Billion |

| Growth Rate (2026 - 2031) | 15.03% CAGR |

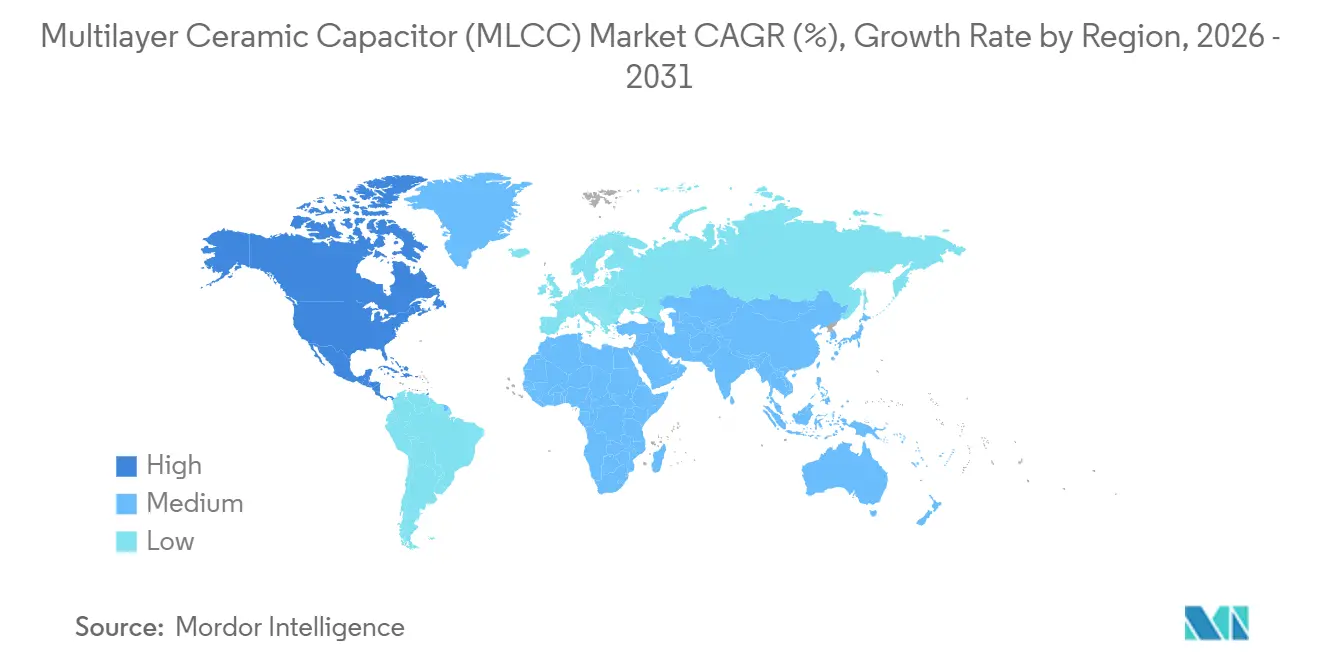

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multilayer Ceramic Capacitor (MLCC) Market Analysis by Mordor Intelligence

The multilayer ceramic capacitor (MLCC) market size is projected to expand from USD 27.26 billion in 2025 and USD 31.87 billion in 2026 to USD 64.19 billion by 2031, registering a 15.03% CAGR between 2026 and 2031. The growth trajectory reflects surging demand for passive components as vehicle electrification, artificial-intelligence infrastructure, and edge computing converge, placing sustained pressure on legacy supply chains. Class 1 temperature-stable dielectrics continue to gain traction in safety-critical designs, while 0402 packages are becoming the preferred form factor for high-performance servers that prize ultra-low equivalent series inductance over absolute footprint savings. Geo-diversified friend-shoring is unlocking incremental capacity in India and Southeast Asia, yet long qualification cycles for AEC-Q200 parts keep near-term supply tight. Competitive dynamics favor vertically integrated leaders that control barium-titanate powders and nickel electrode metallurgy, especially as volatility in nickel and palladium prices raises cost risk across the multilayer ceramic capacitor market.

Key Report Takeaways

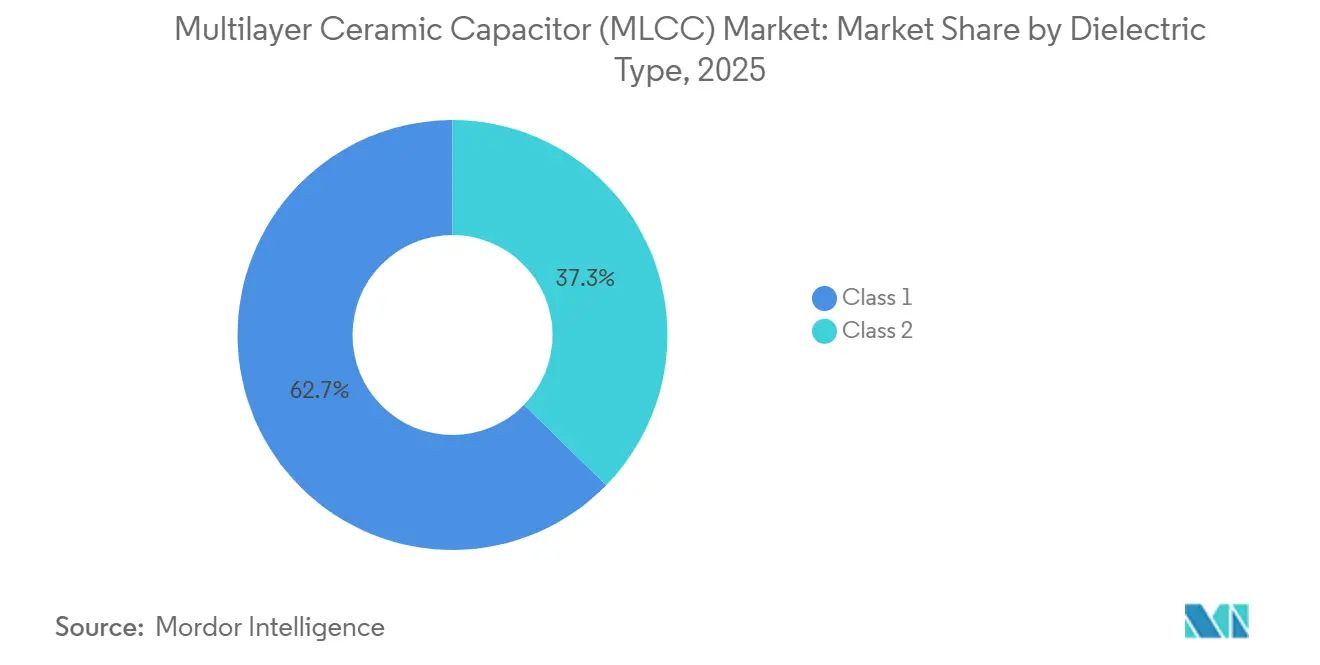

- By dielectric type, Class 1 MLCCs led with 62.69% revenue share revenue of the multilayer ceramic capacitor (MLCC) market in 2025. Class 1 MLCCs also recorded the highest growth outlook within this segmentation, advancing at a 15.83% CAGR through 2031.

- By case size, the 0201 format captured 56.48% share of 2025 revenue of the multilayer ceramic capacitor (MLCC) market. The 0402 format is the fastest-growing case size, expanding at a 16.02% CAGR to 2031.

- By voltage rating, low-voltage parts below 500 V represented 59.34% of revenue of the MLCC market in 2025. Mid-voltage parts between 500 V and 1,000 V post the strongest momentum, rising at a 15.46% CAGR through 2031.

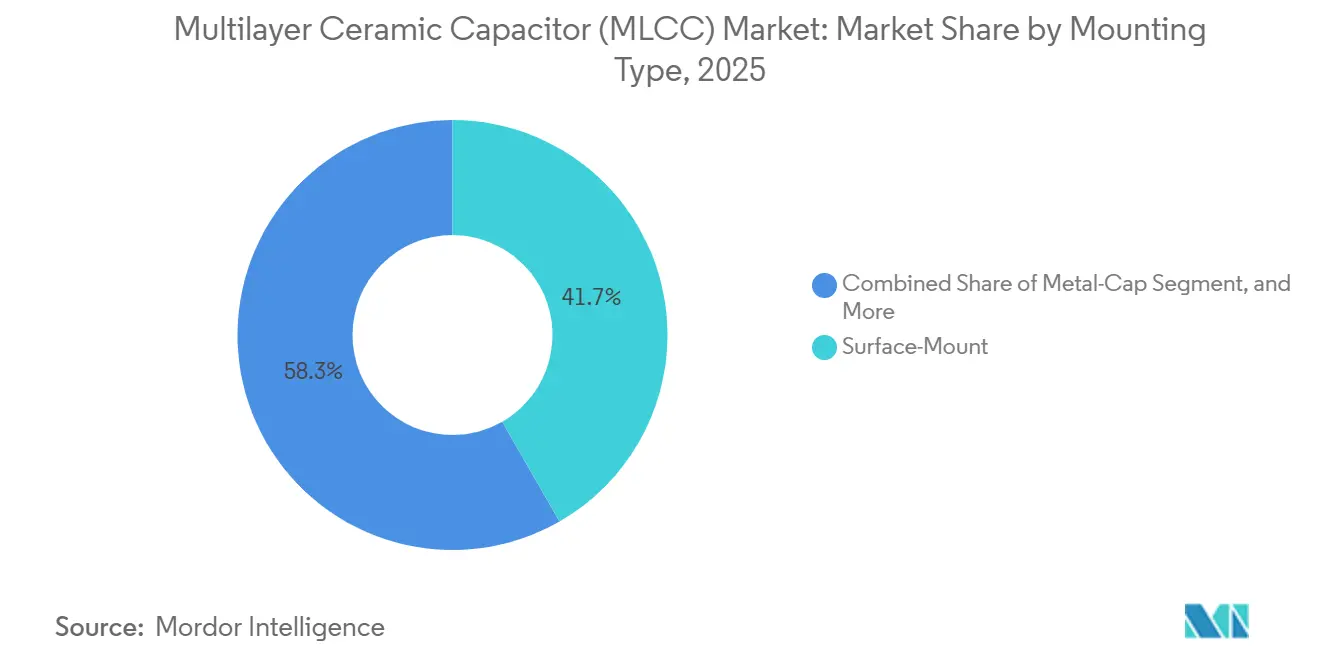

- By mounting type, surface-mount technology held 41.71% share in 2025. Metal-cap variants show the sharpest climb, moving at an 15.67% CAGR to 2031.

- By end-use application, consumer electronics accounted for 51.46% of revenue in 2025. Automotive applications are growing the quickest, registering a 19.63% CAGR during 2026-2031.

- By geography, Asia-Pacific dominated with 57.69% of worldwide revenue of the MLCC market in 2025. North America is the fastest-advancing region, expanding at a 16.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multilayer Ceramic Capacitor (MLCC) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 800 V EV architectures accelerate demand for high-voltage MLCCs | +3.2% | Global with emphasis in China, Europe, North America | Medium term (2-4 years) |

| Gen-AI server build-out spurs ultra-low-ESL, high-CV MLCC adoption | +2.8% | North America and Asia-Pacific data-center hubs | Short term (≤ 2 years) |

| On-device AI and advanced wearables require sub-1005 miniature MLCCs | +2.1% | Global, led by Asia-Pacific consumer-electronics manufacturing | Medium term (2-4 years) |

| Geo-diversified friend-shoring of passive-component supply chains | +1.9% | North America, Europe, India, Southeast Asia | Long term (≥ 4 years) |

| Sustainability mandates favor lead-free and recycled-ceramic MLCCs | +1.4% | Europe and North America with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Semiconductor-subsystem co-design embeds MLCCs inside chiplets | +1.2% | Global, centered in advanced-packaging ecosystems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

800 V EV Architectures Accelerate Demand for High-Voltage MLCCs

Automakers shifting to 800 V battery platforms need MLCCs that withstand ≥1,000 V operating margins, prompting suppliers to thicken nickel-palladium electrodes and refine sub-micrometer dielectric deposition. Samsung Electro-Mechanics released a 2,000 V X7R family in 2025 for silicon-carbide inverters, while Murata’s GCM32 series pairs 1,000 V ratings with 100 nH equivalent series inductance for noise suppression.[1]Product Newsroom, “2,000 V X7R MLCC Series Targets SiC Inverters,” Samsung Electro-Mechanics, samsungsem.com, Product Release, “GCM32 High-Voltage MLCCs Reach 1,000 V,” Murata Manufacturing, murata.com IDTechEx expects 800 V vehicles to represent 40% of production by 2028, lifting MLCC content per car by roughly one-quarter.[2]Research Note, “800-V Battery Architectures 2024-2030,” IDTechEx, idtechex.com Qualification bottlenecks persist because automotive-grade life testing still spans 1,000 hours at 150 °C, yet suppliers mastering these hurdles enjoy premium pricing in the multilayer ceramic capacitor (MLCC) market.

Gen-AI Server Build-Out Spurs Ultra-Low-ESL, High-CV MLCC Adoption

Inference accelerators drawing 700 W per socket create voltage transients that demand 0402 MLCCs positioned within 2 mm of the die. Murata began shipping a 47 µF 4 V 0402 device in July 2025 that stacks 800 layers only 0.6 µm thick.[3]Technical Brief, “0402 47 µF MLCC Achieves 800 Layers,” Murata Manufacturing, murata.com KYOCERA AVX doubled capacity for its low-ESL server portfolio because each GPU board now carries up to 3,000 capacitors, far above CPU systems. TrendForce reported 35% MLCC unit growth in servers during 2025, well ahead of server shipment growth.[4]Market Bulletin, “AI Server MLCC Demand Surged 35% YoY in 2025,” TrendForce, trendforce.com Japanese precision houses therefore widen their lead as defect rates climb when active layers exceed 600.

On-Device AI and Advanced Wearables Require Sub-1005 Miniature MLCCs

Smartphones integrating neural engines and wearables housing health sensors need 0201 and even 01005 sizes, but shrinking below 0402 compresses electrode spacing, elevating dielectric breakdown risk. Murata introduced a 0.22 µF 6.3 V 0201 MLCC in 2025 whose barium-titanate grains measure under 50 nm. KYOCERA AVX followed with a 10 µF 0402 line for fitness trackers. Only a handful of suppliers possess the photolithography-grade clean rooms necessary for such geometries, concentrating production and extending lead times across the multilayer ceramic capacitor (MLCC) market.

Geo-Diversified Friend-Shoring of Passive-Component Supply Chains

Manufacturers now mandate at least one non-China source, steering investment to India, the Philippines, and Eastern Europe. Murata committed USD 340 million to a Krishnagiri, India, plant that entered volume production in 2025. Samsung Electro-Mechanics allocated USD 150 million to its Bulacan, Philippines, campus, and TDK consolidated Southeast Asian logistics to meet regional-content rules. Although new fabs raise near-term costs by up to 30%, they hedge geopolitical risk and qualify for incentives in the United States CHIPS and Science Act and the European Union Chips Act.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile nickel and palladium prices inflate BOM costs | -2.4% | Global with acute impact in automotive and industrial segments | Short term (≤ 2 years) |

| Persistent capacity mismatch for automotive-grade MLCCs | -1.8% | North America, Europe, China automotive corridors | Medium term (2-4 years) |

| China price-led offensive in commodity MLCCs erodes global margins | -1.3% | Global, centered in consumer electronics | Medium term (2-4 years) |

| Physical limits on dielectric-layer thickness stall capacitance gains | -0.9% | Global, affecting high-capacitance and miniaturized segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Nickel and Palladium Prices Inflate BOM Costs

Nickel spiked 42% in early 2024 after Indonesian export curbs, then swung 18% lower by late 2025, while palladium fluctuated between USD 900 and USD 1,400 per troy ounce amid Russian supply uncertainty.[5]Metals Data, “Nickel and Palladium Spot Prices,” London Metal Exchange, lme.com A 10% rise in electrode-metal cost lifts finished MLCC bills by 3-5%, squeezing suppliers in consumer tiers where annual price erosion already approaches 8%. TDK said raw-material inflation trimmed its passive-component margin by 120 bps in fiscal 2026, accelerating copper electrode substitution.[6]Financial Results FY 2026, “Raw-Material Inflation Update,” TDK Corporation, tdk.com Murata is renegotiating quarterly price clauses tied to nickel futures, passing some risk to data-center clients. Smaller Asian suppliers without hedging programs cut automotive output in late 2025, deepening shortage conditions.

Persistent Capacity Mismatch for Automotive-Grade MLCCs

AEC-Q200 qualification still demands 1,000-hour high-temperature life and extreme thermal shock, extending ramp schedules to 18-24 months. Samsung Electro-Mechanics reported 26-week lead times in early 2025 even at full utilisation, prioritising electric-vehicle orders over legacy platforms. Murata’s Shimane expansion will add 25% capacity but will not complete qualification until late 2027. Automakers therefore pay 30-50% premiums or freeze designs early, while agile suppliers that co-locate test labs enjoy a competitive edge. The imbalance keeps the multilayer ceramic capacitor (MLCC) market for automotive parts structurally tight despite headline capacity announcements.

Segment Analysis

By Dielectric Type: Temperature Stability Drives Class 1 Resurgence

Class 1 devices accounted for 62.69% multilayer ceramic capacitor (MLCC) market share in 2025, reflecting automakers' need for drift-free performance over 15-year vehicle lifespans. The segment is set to grow at a 15.83% CAGR, faster than the broader multilayer ceramic capacitor market size, as wide-bandgap inverters and medical electronics migrate to zero-temp-coefficient ceramics. Murata’s 1,250 V C0G series exemplifies the shift toward thicker electrodes that combat electromigration while maintaining sub-ppm temperature tracking. In contrast, Class 2 barium-titanate parts still dominate smartphones because their higher volumetric efficiency offsets aging losses, yet they lose share in safety-critical designs.

The trade-off between board real estate and stability remains central. Class 1 capacitors occupy up to five times the footprint of Class 2 equivalents, yet predictable capacitance eliminates costly design margins, which matters in ISO 26262-compliant powertrain control units. Regulatory bodies do not explicitly mandate dielectric selection, but AEC-Q200 life testing implicitly steers designs toward Class 1 formulations. Consequently, the MLCC market continues to bifurcate: high-value automotive and industrial nodes lean on Class 1 stability, while consumer electronics retain Class 2 density.

By Case Size: Miniaturization Meets Power Density in 0402 Surge

The 0201 footprint captured 56.48% of the multilayer ceramic capacitor (MLCC) market in 2025, driven by smartphones and wearables chasing sub-millimetre components. Yet 0402 units are rising 16.02% annually, supported by AI servers that need 47 µF decoupling capacitors contiguous to 700 W GPUs. Murata’s July 2025 release of an 800-layer 0402 part doubled capacitance density over its previous generation. KYOCERA AVX followed with a 10 µF 0402 range for smart-watch modules.

Manufacturing complexity scales sharply below 0402, requiring photolithography-grade clean rooms and laser trim. This concentrates capacity among three Japanese and Korean leaders, extending lead times to 20 weeks in early 2026, while Chinese entrants compete in commoditised 0603 and 0805 lines. As GPU boards swell to 3,000 MLCCs each, supply tightness in 0402 parts is likely to persist, underpinning premium price realisation across the multilayer ceramic capacitor market.

By Voltage Rating: Mid-Voltage Segment Captures 800 V EV Wave

Low-voltage MLCCs below 500 V retained 59.34% share in 2025 thanks to phones, laptops, and servers. Mid-voltage types between 500 V and 1,000 V exhibit a 15.46% CAGR, lifting their multilayer ceramic capacitor market size as 800 V drivetrains and renewable-energy inverters scale. Samsung Electro-Mechanics’ 2,000 V X7R launch in 2025 answers silicon-carbide traction inverter needs; TDK’s 1,250 V C0G series addresses on-board chargers. High-voltage i.e., above 1,000 V parts remain niche in X-ray and photovoltaic systems yet command high margins.

Automakers see 800 V buses halving charging time and trimming copper wiring mass by up to 30%, yielding greater MLCC dollar content per vehicle. IDTechEx forecasts 40% 800 V penetration by 2028, underscoring mid-voltage momentum. Above 1,500 V, film capacitors still compete on energy density, but ceramics win where space and ESR drive architectural choice.

By Mounting Type: Metal-Cap Variants Gain in Data-Center Power Delivery

Surface-mount MLCCs delivered 41.71% of revenue in 2025 and stay dominant in consumer and automotive boards. Metal-cap designs grow 15.67% annually as data-center power planes adopt direct-attach capacitors that cut parasitic inductance by up to 60%. Murata’s 0402 metal-cap offering premiered in 2025 with 47 µF capacitance, serving Gen-AI nodes. KYOCERA AVX noted a capacity pivot toward these SKUs after orders doubled in 2025.

The metal-cap premium rests on mechanical robustness during thermal cycling and the ability to sit within 2 mm of high-amp silicon. Radial-lead parts decline as through-hole assembly wanes, though industrial retrofits keep a residual niche. The multilayer ceramic capacitor market therefore segments by assembly environment: high-speed pick-and-place favours surface mount, while high-current rails inside GPUs justify the costlier metal-cap topology.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Application: Automotive Electrification Outpaces Consumer Electronics

Consumer electronics still led at 51.46% of 2025 revenue, yet automotive MLCC demand rises 19.63% annually as electric vehicles multiply component counts. Battery-electric cars already house 8,000-12,000 capacitors and gain 2,000-3,000 more when moving from 400 V to 800 V buses. Samsung Electro-Mechanics began shipping to BYD’s 800 V platforms in early 2026. Telecommunications sits in the low-mid-single digits, while industrial automation enjoys steady growth tied to robotics and renewables.

Medical, aerospace, and defense remain small but price-rich because they need radiation-hard or traceable lots. Power utilities deploy high-voltage MLCCs in grid inverters, albeit in modest volumes relative to automotive. As a result, car electrification pulls capital investments toward AEC-Q200 fabs, realigning the multilayer ceramic capacitor (MLCC) market around long-lifecycle, high-reliability sectors.

Geography Analysis

Asia-Pacific generated 57.69% of multilayer ceramic capacitor revenue in 2025, reflecting Japan’s mastery of precision ceramics, South Korea’s high-mix production, and China’s vast consumer-electronics export engine. Chinese factories supplied up to 75% of global MLCC output, yet geopolitical tension spurred OEMs to dual-source through Japanese, Korean, and Indian sites. Murata, TDK, and Taiyo Yuden all ran full utilisation in early 2026 and expanded capacity in the Philippines and India to satisfy friend-shoring mandates. Samsung Electro-Mechanics, likewise running at capacity, channelled parts to BYD’s 800 V vehicles while fortifying its Philippine campus.

North America is growing at 16.07% through 2031, buoyed by CHIPS and Science Act incentives that pull semiconductor and passive-component supply back onshore. Hyperscalers such as Microsoft and Amazon doubled server-grade MLCC orders during 2025, chasing ultra-low-ESL decoupling for AI accelerators. Proposed U.S. fabs remain delayed by labour cost and lengthy AEC-Q200 qualification cycles, so Mexican sites pick up overflow assembly under USMCA trade terms. Canada’s piece is small but may rise as critical-mineral policies support domestic nickel and palladium supply.

Europe held a mid-teens share in 2025, tied to Germany’s automotive corridor and Nordic renewable-energy projects. The European Union Chips Act encourages localisation, though strict RoHS and REACH standards extend qualification and inflate costs by up to 15% versus Asia. Würth Elektronik is scaling automotive-grade output, yet still imports sub-micron dielectric powders from Japan. Elsewhere, South America, the Middle East, and Africa represent a low-single-digit slice, with growth centring on Brazil’s electric-vehicle rollout and Gulf data-center builds that value low-inductance MLCCs.

Competitive Landscape

The multilayer ceramic capacitor market remains highly concentrated: Murata Manufacturing, Samsung Electro-Mechanics, and TDK Corporation controlled an estimated 60-65% of revenue in 2025. Vertical integration into barium-titanate synthesis and nickel electrode plating shields their margins from raw-material swings, while proprietary co-firing ovens enable sub-0.6 µm dielectric layers. Murata patented a copper-electrode stack under 0.5 µm in 2025 that could double capacitance density and cut electrode cost by up to 40%. Samsung Electro-Mechanics combines capacity expansion in the Philippines and Vietnam with AI-enabled defect analytics that trimmed scrap by 18% in 2025.

Mid-tier players such as Yageo and Walsin pursue M and A for automotive qualification, exemplified by Yageo’s 2024 KEMET acquisition, yet still trail in ultra-miniature nodes. Chinese entrants Sunlord and Fenghua move aggressively on price in commodity smartphones, underbidding Japanese peers by 15-25%, but remain excluded from automotive and data-center sockets that demand AEC-Q200 compliance and low-ESL metrics. As semiconductor firms embed capacitors inside chiplet substrates, a small yet growing share of demand shifts into integrated passives, presenting both a challenge and an opportunity for discrete MLCC vendors.

Barriers to entry stay formidable because AEC-Q200 and IEC 60384 protocols require component stress tests, lot traceability, and co-located life-test ovens that only capital-rich suppliers can afford. Sustainability regulation in Europe further raises hurdles, favouring companies that can certify recycled ceramic powders and lead-free terminations. Overall, scale, materials science, and qualification speed define competitive advantage across the multilayer ceramic capacitor market.

Multilayer Ceramic Capacitor (MLCC) Industry Leaders

Murata Manufacturing Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

Taiyo Yuden Co., Ltd.

Yageo Corporation

TDK Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Murata Manufacturing announced a JPY 12 billion (USD 80 million) expansion at its Shimane plant to lift automotive-grade capacity by 25% by 2H 2027, including dedicated AEC-Q200 lines.

- February 2026: Murata Manufacturing completed a capacity lift at Wuxi, China, adding 15% output focused on 800 V EV inverters and on-board chargers.

- February 2026: TDK Corporation revised fiscal 2026 earnings guidance, citing an 18% rise in nickel and palladium costs that compressed passive-component margins by 120 bps and accelerated copper electrode substitution.

- January 2026: Murata Manufacturing opened its Philippines fab, boosting Southeast Asia MLCC output 20% and achieving full AEC-Q200 qualification.

Global Multilayer Ceramic Capacitor (MLCC) Market Report Scope

The Multilayer Ceramic Capacitor (MLCC) Market Report is Segmented by Dielectric Type (Class 1, Class 2), Case Size (0 201, 0 402, 0 603, 1 005, 1 210, Other Case Sizes), Voltage Rating (Low Voltage, Mid Voltage, High Voltage), Mounting Type (Surface-Mount, Metal-Cap, Radial-Lead), End-Use Application (Aerospace and Defense, Automotive, Consumer Electronics, Industrial, Medical Devices, Power and Utilities, Telecommunications, Rest of End-Use Applications), and Geography (North America, Europe, Asia-Pacific, Rest of the World). The Market Forecasts are Provided in Terms of Value (USD).

| Class 1 |

| Class 2 |

| 0 201 |

| 0 402 |

| 0 603 |

| 1 005 |

| 1 210 |

| Other Case Sizes |

| Low Voltage (Less than 500 V) |

| Mid Voltage (500 - 1000 V) |

| High Voltage (Above 1000 V) |

| Surface-Mount |

| Metal-Cap |

| Radial-Lead |

| Aerospace and Defense |

| Automotive |

| Consumer Electronics |

| Industrial |

| Medical Devices |

| Power and Utilities |

| Telecommunications |

| Rest of End-Use Applications |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Dielectric Type | Class 1 | |

| Class 2 | ||

| By Case Size | 0 201 | |

| 0 402 | ||

| 0 603 | ||

| 1 005 | ||

| 1 210 | ||

| Other Case Sizes | ||

| By Voltage Rating | Low Voltage (Less than 500 V) | |

| Mid Voltage (500 - 1000 V) | ||

| High Voltage (Above 1000 V) | ||

| By Mounting Type | Surface-Mount | |

| Metal-Cap | ||

| Radial-Lead | ||

| By End-Use Application | Aerospace and Defense | |

| Automotive | ||

| Consumer Electronics | ||

| Industrial | ||

| Medical Devices | ||

| Power and Utilities | ||

| Telecommunications | ||

| Rest of End-Use Applications | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform