Aerospace And Defence MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

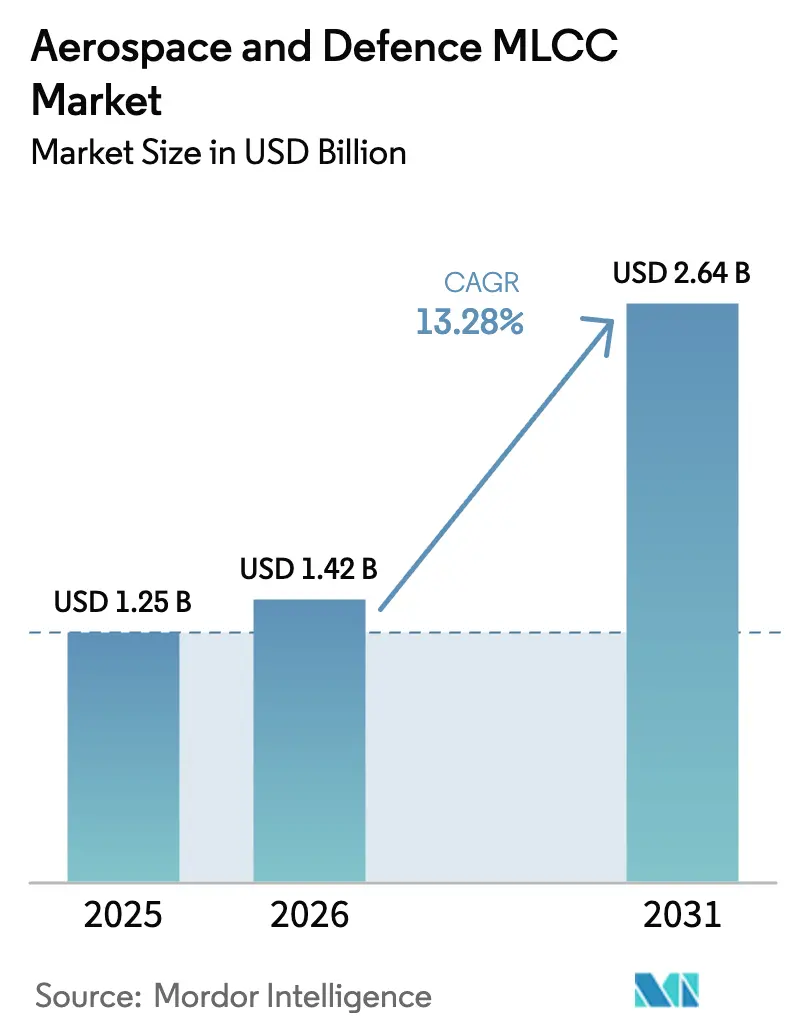

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 2.64 Billion |

| Growth Rate (2026 - 2031) | 13.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace And Defence MLCC Market Analysis by Mordor Intelligence

The Aerospace and defence MLCC market size is expected to grow from USD 1.25 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 2.64 billion by 2031 at 13.28% CAGR over 2026-2031. Robust investment in defense modernization programs, including the U.S. Army’s 35 initiatives aimed at Multi-Domain Operations readiness, intensifies requirements for high-reliability capacitors that comply with MIL-PRF-32535 testing thresholds.[1]Editor, “Northrop Grumman ATHENA Selected by US Army,” Joint Forces, joint-forces.com Asia-Pacific manufacturers leverage extensive ceramic know-how to supply more than half of global demand, while North American suppliers accelerate capacity expansion to capture defense spending backed by domestic-content mandates. Miniaturization trends, the shift toward wide-bandgap semiconductors, and persistent raw-material volatility create both growth headroom and supply-chain risk for the Aerospace and defence MLCC market. Defensive inventory policies adopted by Tier-1 avionics OEMs after the 2024 semiconductor crunch continue to influence near-term procurement patterns.

Key Report Takeaways

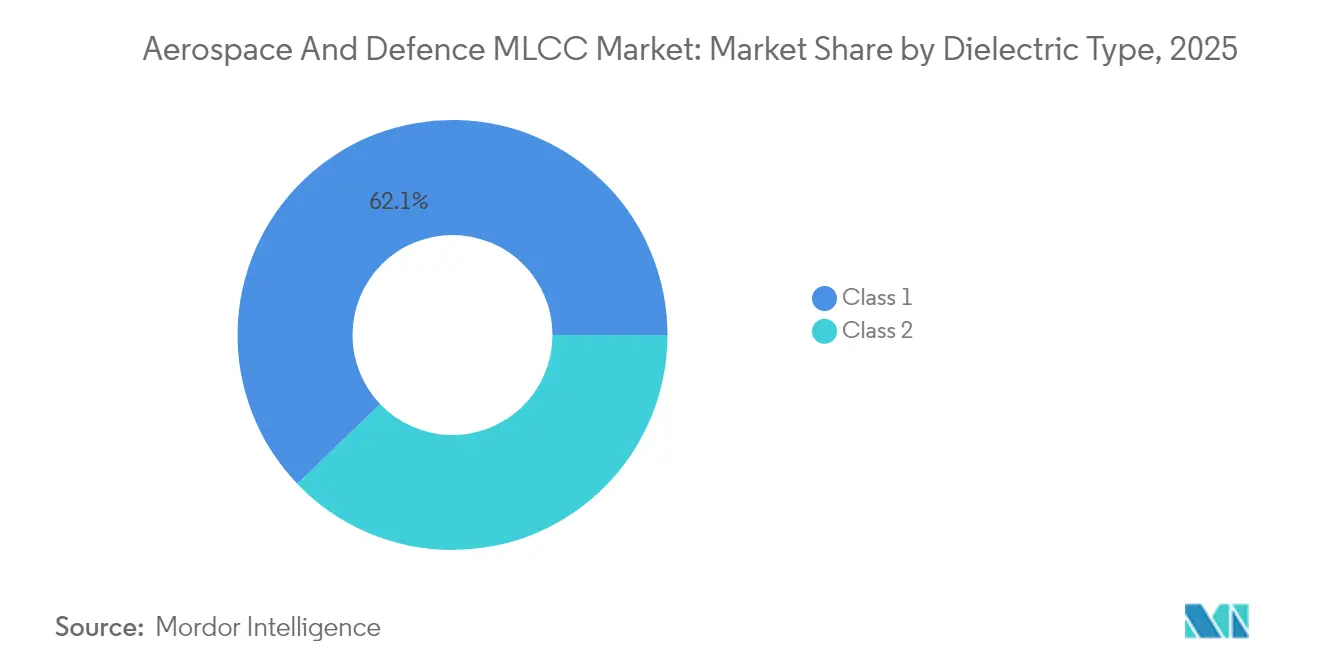

- By dielectric type, Class 1 components captured 62.15% of Aerospace and defence MLCC market share in 2025 and are expanding at a 14.62% CAGR to 2031.

- By case size, 0201 held 55.95% of the Aerospace and defence MLCC market size in 2025 in the Aerospace and defence MLCC market, while 0402 shows the fastest 14.35% CAGR through 2031.

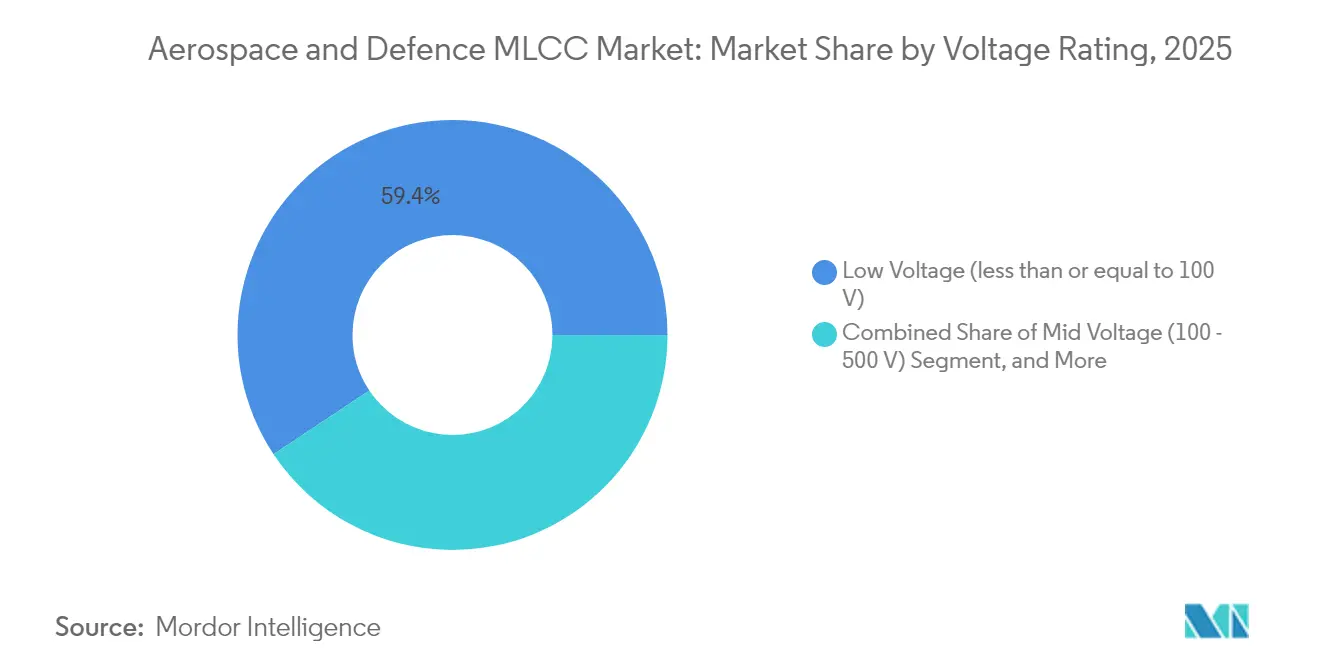

- By voltage rating, less than equal to 100 V MLCCs accounted for 59.35% of 2025 in the Aerospace and defence MLCC market revenue and post a 13.12% CAGR to 2031.

- By mounting type, surface-mount designs formed 41.25% of 2025 sales in the Aerospace and defence MLCC market; metal-cap variants register a 14.05% CAGR to 2031.

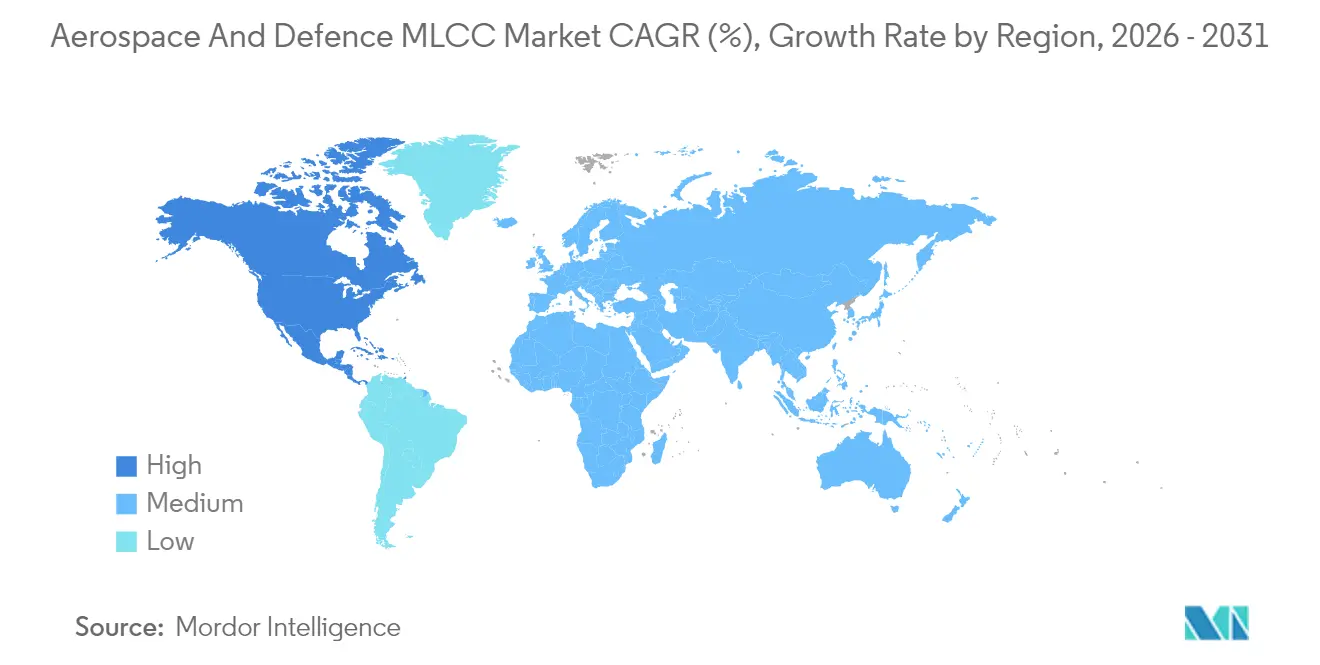

- By region, Asia-Pacific dominated with 57.10% share in 2025 in the Aerospace and defence MLCC market, whereas North America records the quickest 14.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerospace And Defence MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for radiation-hardened MLCCs in LEO satellite constellations | +3.2% | Global, with concentration in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Transition toward all-electric aircraft subsystems | +2.8% | North America, Europe, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Miniaturisation pressure in advanced phased-array radar modules | +2.1% | Global, led by North America and Asia-Pacific defense programs | Short term (≤ 2 years) |

| Design wins for wide-bandgap (SiC/GaN) power electronics in defence platforms | +1.9% | North America, Europe, with emerging adoption in Asia-Pacific | Medium term (2-4 years) |

| Active inventory build-up by Tier-1 avionics OEMs amid supply-chain shocks | +1.6% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Government offsets mandating local content in defence electronics | +1.4% | Regional focus: North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Radiation-Hardened MLCCs in LEO Satellite Constellations

Thousands of small satellites launched into 160 - 2 000 km orbits expose onboard electronics to severe radiation, prompting defense primes to specify MLCCs rated above 100 krad(Si) and hardened against single-event upsets. Programs such as the ATHENA missile-warning sensor rely on high-stability Class 1 devices to maintain 24/7 vigilance. Accelerated launch cadences through 2028 make this driver a medium-term pillar for the Aerospace and defence MLCC market.

Transition Toward All-Electric Aircraft Subsystems

The electrification of flight-control, environmental, and auxiliary systems increases operating voltages and thermal loads, driving demand for mid- and high-voltage MLCCs. Funding streams such as the USD 1.04 billion F-22 sensor upgrade and the Collins Aerospace UH-60M MOSA project underscore institutional commitment to electric architectures. Development and certification cycles extend influence into the next decade.

Miniaturization Pressure in Advanced Phased-Array Radar Modules

AESA platforms like the AN/TPS-80 G/ATOR consolidate multi-mission capability by packing thousands of T/R modules into compact apertures, favoring 0201 and 0402 MLCCs that tolerate tight pitch without sacrificing thermal stability. Demand spikes immediately as radar modernization budgets mature, benefiting suppliers with proven micro-package yields.

Design Wins for Wide-Bandgap (SiC/GaN) Power Electronics in Defense Platforms

Directed-energy weapons and advanced power supplies adopt SiC MOSFETs and GaN HEMTs that switch at high frequencies and temperatures, requiring low-ESR MLCCs that maintain capacitance across the thermal envelope. Vishay’s Gen 3 SiC diodes rated to 175 °C illustrate component benchmarks shaping MLCC specifications.[2]Vishay Intertechnology, “Gen 3 650 V and 1200 V SiC Schottky Diodes,” vishay.com Qualification cycles keep this driver in the medium-term window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-reliability qualification cost and time (MIL-PRF-32535) | -2.3% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Commodity MLCC capacity crowd-out in commercial lines | -1.8% | Asia-Pacific manufacturing centers, global supply impact | Medium term (2-4 years) |

| Long-tail raw-material criticality (palladium, ruthenium) | -1.5% | Global, with concentration risk in Russia and South Africa | Medium term (2-4 years) |

| Extended design-in cycles in safety-critical avionics | -1.2% | Global, particularly North America and Europe defense programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-Reliability Qualification Cost and Time (MIL-PRF-32535)

Achieving MIL-PRF-32535 compliance can exceed USD 5 million per product family and stretch across 18-24 months. Only well-capitalized incumbents such as KYOCERA AVX consistently finance full test regimes covering temperature cycling, mechanical shock, and extended burn-in, effectively limiting new entrants.[3]KYOCERA AVX, “MIL-PRF-123 Qualified Chip Capacitors,” kyocera-avx.com Lengthy validation suppresses innovation velocity and constrains the Aerospace and defence MLCC market’s supplier pool.

Commodity MLCC Capacity Crowd-Out in Commercial Lines

Explosive consumer demand for smartphones and EVs draws factory allocation away from low-volume, high-reliability military builds. Asia-Pacific makers prioritize commercial runs where economies of scale prevail, forcing defense buyers to compete for scarce production slots amid palladium and ruthenium price swings. Supply tightness persists through 2028 as capacity investments lag demand diversification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Reliability Keeps Class 1 in Front

Class 1 components controlled 62.15% of 2025 revenue, reflecting their low dielectric loss and capacitance stability indispensable for precision radar timing circuits. The Aerospace and defence MLCC market size tied to Class 1 is projected to widen at 14.62% CAGR as LEO satellite designs and GaN-based power modules require temperature-stable capacitors for mission assurance. Manufacturers enhance formulations to resist radiation levels above 100 krad(Si), reinforcing share dominance even as unit costs stay above Class 2 equivalents. The Aerospace and defence MLCC market benefits when defense primes lock long-term agreements to secure Class 1 supply continuity, limiting price erosion.

Class 2 parts appeal where volumetric efficiency outweighs accuracy, but piezoelectric noise and capacitance drift restrict adoption in flight-critical electronics. Continuous innovation narrows these performance gaps; however, the testing burden to qualify new Class 2 chemistries under MIL-PRF-32535 slows penetration. As a result, Class 1 devices should retain a leading Aerospace and defence MLCC market share through 2031, particularly inside AESA modules and spaceborne payloads.

By Case Size: 0201 Remains Sweet Spot While 0402 Accelerates

The 0201 format retained 55.95% share in 2025 due to balanced electrical rating, manufacturability, and assembly yield. OEM preference for smaller footprints in conformal phased-array panels has pushed suppliers to improve solder-joint robustness and reduce micro-cracking. Growing radar retrofit programs mean 0201 volumes rise in tandem with platform deliveries, keeping this size at the core of the Aerospace and defence MLCC market.

0402 units led growth at 14.35% CAGR, riding the drive for extreme channel counts in GaN-based AESA radars and electronic-warfare pods. As pick-and-place accuracy improves and X-ray inspection becomes standard, acceptance of 0402 packages increases. Larger 0603 and 0805 formats survive in power conversion and energy-storage rails where capacitance per device offsets board real estate. Suppliers that balance micro-package scale and military-grade reliability remain best positioned inside the Aerospace and defence MLCC market.

By Voltage Rating: Low-Voltage Parts Dominate Digital Architectures

MLCCs rated less than or equal to 100 V generated 59.35% of 2025 sales, aligning with 28 V aircraft buses and low-power RF front-ends. Design migrations toward 48 V or higher DC rails to cut cabling weight will lift mid-voltage demand, but entrenched digital avionics keep low-voltage MLCCs central to the Aerospace and defence MLCC market.

Mid-voltage (100-500 V) devices expand alongside electric actuators and SiC-based converters, claiming the fastest 14.11% CAGR. High-voltage (above 500 V) selections remain niche, servicing directed-energy weapons and pulse-power modules where energy density overshadows board area. Effective derating policies and DO-160 compliance testing dictate final voltage picks across defense fleets.

By Mounting Type: Surface Mount Efficiency Versus Metal-Cap Robustness

Surface-mount devices accounted for 41.25% revenue in 2025 because automated reflow lines minimize assembly cost while achieving fine-pitch density. Vibration-prone land-based mobile radars, however, push buyers toward metal-cap variants showing 14.05% CAGR thanks to their higher mechanical compliance and thermal-cycle endurance.

Radial leaded parts endure in legacy systems where field reparability and socket compatibility matter. Balancing cost-effective SMT throughput with field-level durability will dictate mounting-type mix in the evolving Aerospace and defence MLCC market.

Geography Analysis

Asia-Pacific retained 57.10% share in 2025, underpinned by Japan’s ceramic expertise and Korea’s high-volume fabrication lines that together meet stringent MIL-PRF-32535 requirements. Regional suppliers leverage vertically integrated powder production and long-running government support for electronic-materials research. Yet export-control measures and growing demand for sovereign supply chains prompt Western primes to reassess sole-source dependencies within the Aerospace and defence MLCC market. Expansion of Chinese defense-electronics capacity adds competitive pressure but remains subject to restricted technology flows.

North America advances at a 14.22% CAGR through 2031, buoyed by elevated Pentagon outlays and offset mandates such as the USD 24.5 billion NORAD upgrade that prioritize domestic content. Prime integrators lock multi-year MLCC agreements to de-risk programs like F-22 sensor enhancement and M-SHORAD laser weapon systems. Capacity additions, reshoring incentives, and ITAR-driven ecosystem clustering strengthen the region’s position inside the Aerospace and defence MLCC market size forecast.

Europe presents steady yet slower growth as collaborative programs such as FCAS and Tempest concentrate on sovereign electronics supply. Fragmented national certification protocols extend qualification cycles, but funding pools tied to digital-sovereignty objectives encourage local MLCC development. Outside core regions, the Middle East and Indo-Pacific defense spenders continue importing high-reliability capacitors while exploring licensed production partnerships to fulfill localization clauses.

Competitive Landscape

The Aerospace and defence MLCC market demonstrates moderate concentration, with Murata, Samsung Electro-Mechanics, TDK, Vishay, and KYOCERA AVX collectively controlling the majority of qualified capacity. Decades of ceramic material R&D, proprietary dielectric recipes, and in-house powder synthesis furnish these firms with defensible technological moats. Multi-million-dollar military test suites and extensive documentation repositories create additional entry hurdles.

Strategic moves emphasize technology broadening and vertical integration. Vishay’s 2025 rollout of Gen 4.5 650 V MOSFETs and follow-on SiC diode launches position the firm to deliver turnkey passive-and-active solutions to power-electronics designers. Samsung Electro-Mechanics channels capital toward high-frequency C0G lines that align with GaN radar drivers, while Murata pursues radiation-hardened part families for space contracts.

Supply-chain resilience tactics include dual-site manufacturing, regional warehousing, and advance-purchase agreements brokered with primes to lock wafer starts. Smaller specialty houses targeting niche dielectric chemistries focus on directed-energy and hypersonic projects but wrestle with qualification economics. Over the forecast horizon technological differentiation around radiation tolerance, thermal stability, and sub-0402 packaging will dictate competitive gains within the Aerospace and defence MLCC market.

Aerospace And Defence MLCC Industry Leaders

Taiyo Yuden Co., Ltd

Walsin Technology Corporation

Yageo Corporation

Samsung Electro-Mechanics Co., Ltd.

Murata Manufacturing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vishay Intertechnology introduced Gen 4.5 650 V E-Series MOSFETs featuring record low RDS(on)·Qg, aimed at high-density aerospace converters.

- March 2025: Collins Aerospace won a USD 80.2 million U.S. Army contract to develop a modular open-systems avionics backbone for UH-60M Black Hawk helicopters.

- September 2024: Raytheon secured up to USD 1.04 billion to upgrade F-22 sensors, integrating advanced processing hardware through 2029.

- September 2024: Vishay initiated its “Vishay 3.0” restructuring to streamline production and accelerate defense-market growth.

Global Aerospace And Defence MLCC Market Report Scope

Manned Aerial Vehicle, Unmanned Aerial Vehicle are covered as segments by Vehicle Type. 0 201, 0 402, 0 603, 1 005, 1 210, Others are covered as segments by Case Size. 600V to 1100V, Less than 600V, More than 1100V are covered as segments by Voltage. 10 μF to 100 μF, Less than 10 μF, More than 100 μF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Class 1 |

| Class 2 |

| 201 |

| 402 |

| 603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 – 500 V) |

| High Voltage (above 500 V) |

| Metal Cap |

| Radial Lead |

| Surface-Mount |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Dielectric Type | Class 1 | |

| Class 2 | ||

| By Case Size | 201 | |

| 402 | ||

| 603 | ||

| 1005 | ||

| 1210 | ||

| Other Case Sizes | ||

| By Voltage | Low Voltage (less than or equal to 100 V) | |

| Mid Voltage (100 – 500 V) | ||

| High Voltage (above 500 V) | ||

| By MLCC Mounting Type | Metal Cap | |

| Radial Lead | ||

| Surface-Mount | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform