Telecommunication MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

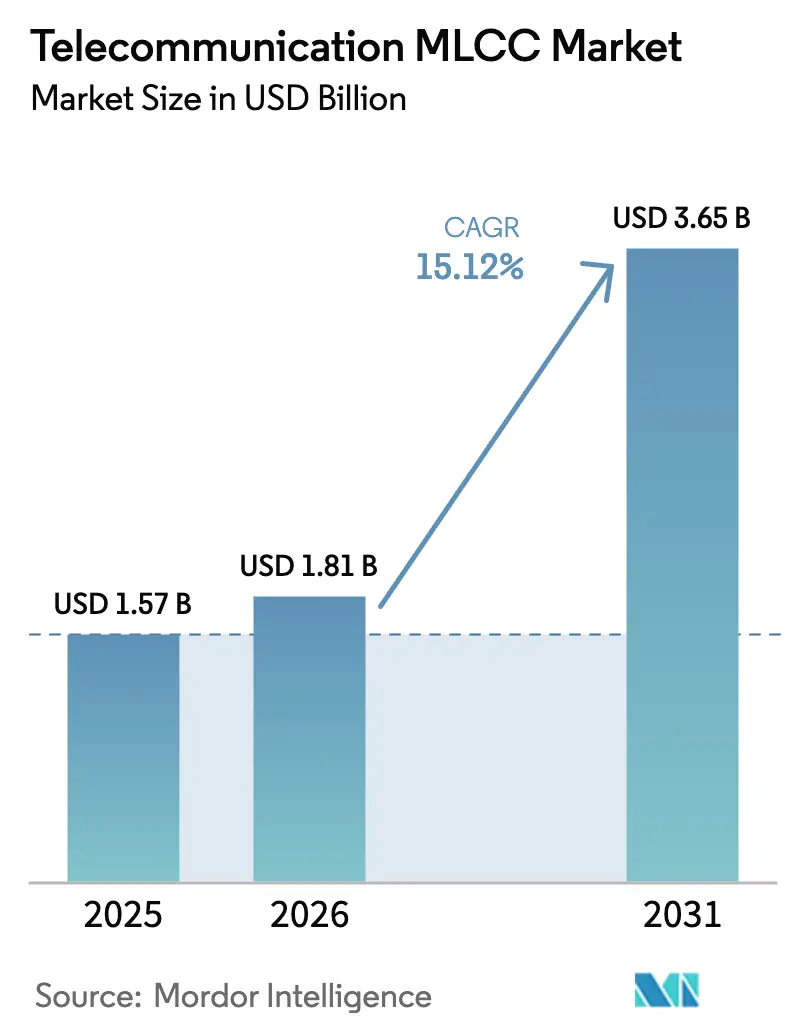

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 3.65 Billion |

| Growth Rate (2026 - 2031) | 15.12% CAGR |

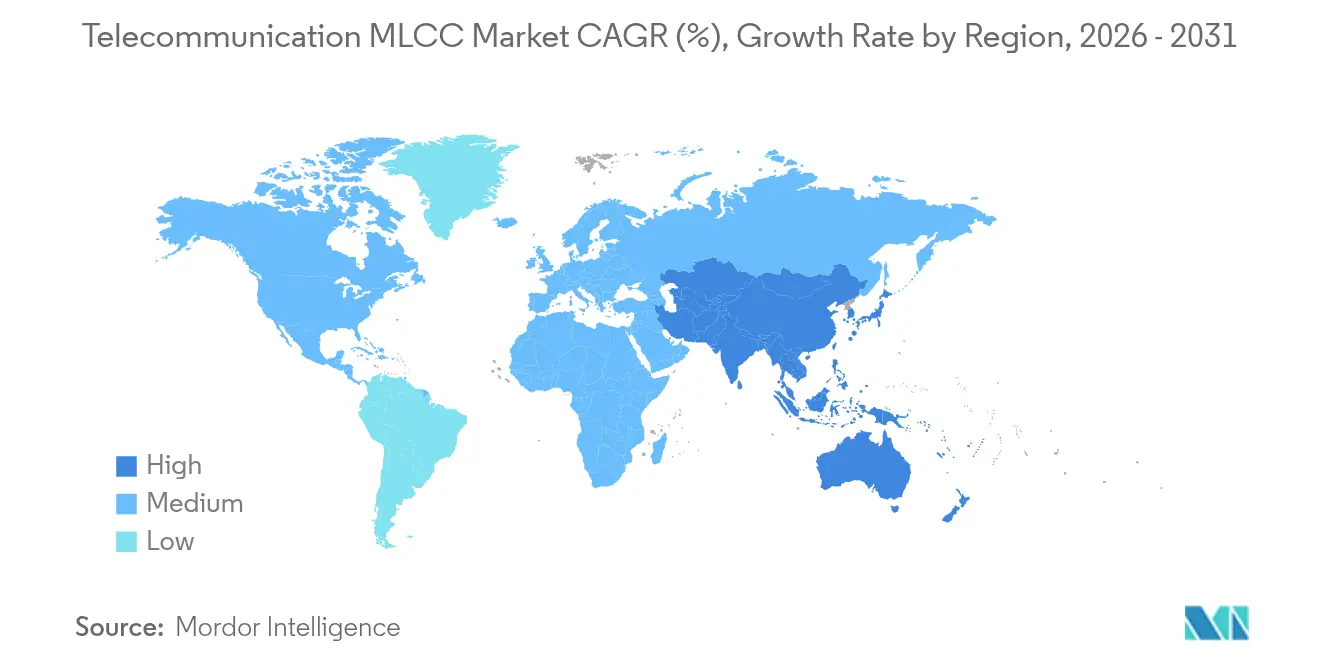

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecommunication MLCC Market Analysis by Mordor Intelligence

The telecommunication MLCC market size was valued at USD 1.57 billion in 2025 and estimated to grow from USD 1.81 billion in 2026 to reach USD 3.65 billion by 2031, at a CAGR of 15.12% during the forecast period (2026-2031). Continued 5G macro-cell rollouts, massive MIMO antenna density, and the widening use of high-capacitance ceramic dielectrics in RF front-ends anchor this momentum. Government-funded rural broadband schemes in Australia and the United States result in sizable fixed-wireless access equipment orders, with each unit carrying more than 20 MLCCs on average. Class 1 dielectrics lead demand because their temperature stability keeps mmWave links within design tolerances, while the shift to smaller 402 packages signals sustained miniaturization.[1]Kyocera-AVX, “MLCC Delivering Industry-Highest 47µF Capacitance in 0402,” kyocera-avx.com North America’s early investment in 5G and defense programs shapes current regional dominance, yet Asia-Pacific’s proximity to ceramic fabrication plants positions it for the quickest capacity ramp-ups.[2]Murata Manufacturing Co., Ltd., “Company News – General,” murata.com Pricing uncertainty tied to barium-titanate inputs and concentrated East-Asian output remains the principal risk, prompting OEMs to dual-source for supply continuity.[3]TDK Corporation, “Press Release,” tdk.com

Key Report Takeaways

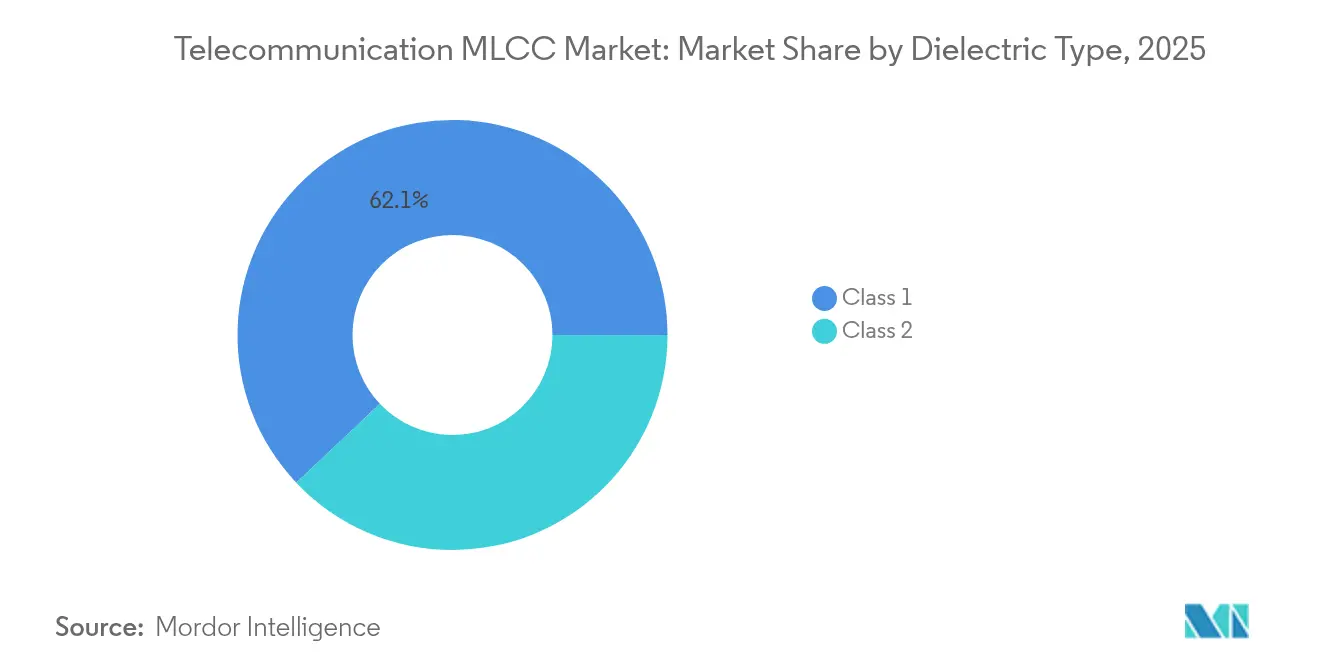

- By dielectric type, Class 1 devices held 62.05% of the telecommunication MLCC market share in 2025 and are advancing at a 16.55% CAGR through 2031.

- By case size, the 201 format accounted for 55.72% of the telecommunication MLCC market size in 2025, while the 402 package is projected to climb at a 16.4% CAGR by 2031.

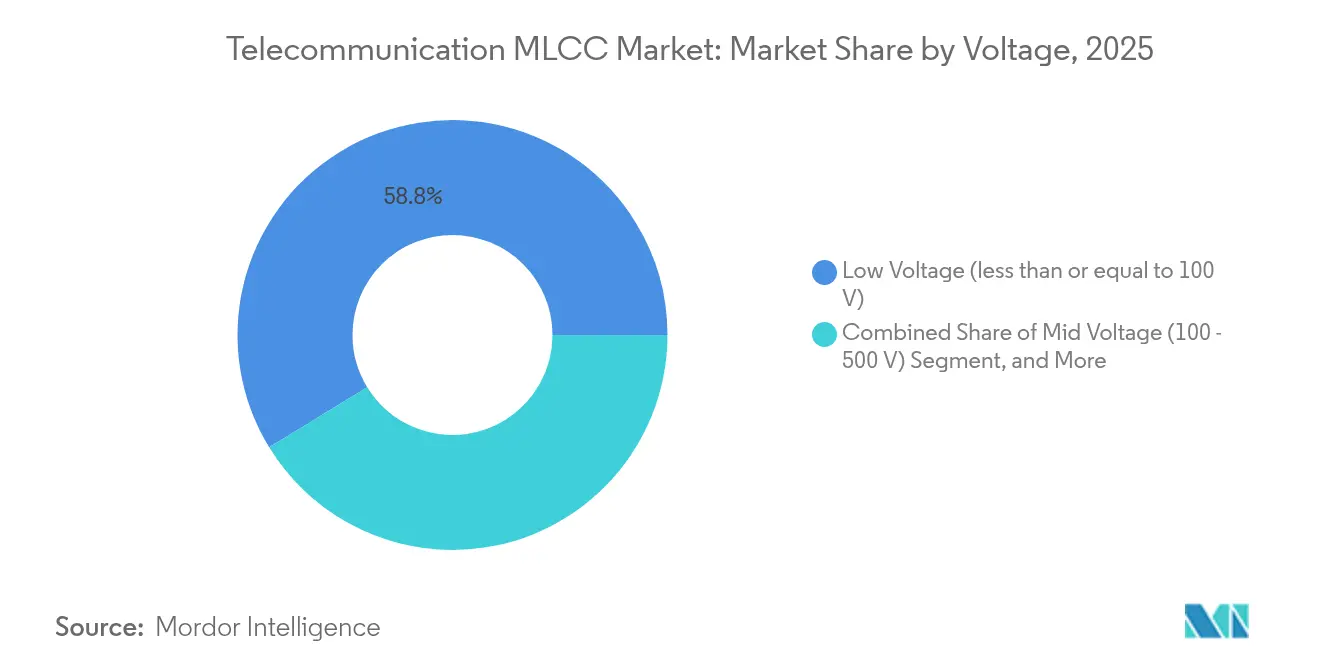

- By voltage, parts with a rating of less than or equal to 100 V captured 58.75% of the revenue in 2025 in the telecommunication MLCC market and are projected to scale at a 16.22% CAGR to 2031.

- By mounting style, surface-mount units generated 41.15% sales in 2025 in the telecommunication MLCC market, yet metal-cap designs register the fastest 15.96% CAGR through 2031.

- By geography, North America accounted for 57.05% of the 2025 revenue in the telecommunication MLCC market, and the Asia-Pacific region is forecast to record a 16.66% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telecommunication MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G / massive-MIMO base-stations | +4.2% | Global, with concentration in North America, China, South Korea | Medium term (2-4 years) |

| Adoption of high-capacitance MLCCs in smartphone RF front-ends | +3.8% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Growth in broadband CPE and set-top-box shipments | +2.9% | North America, Europe, emerging APAC markets | Medium term (2-4 years) |

| Expansion of IoT and LPWAN networks | +2.1% | Global, with early deployment in urban centers | Long term (≥ 4 years) |

| Advanced ceramic dielectrics enabling mmWave reliability | +1.8% | North America, Japan, South Korea | Long term (≥ 4 years) |

| Government-subsidised rural broadband / FWA roll-outs | +1.6% | Australia, United States, Canada, rural Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G / Massive-MIMO Base-Stations

Base-station upgrades from 4G to massive-MIMO escalate MLCC demand eightfold as each 64-256 element array integrates discrete RF chains that rely on Class 1 capacitors for temperature-invariant filtering.[4]Ericsson, “Mobility Report – 5G Massive MIMO Deployment,” ericsson.com China alone spent more than USD 50 billion on 5G infrastructure in 2024, with every site embedding up to 400 MLCCs. The shift toward centralized radio units concentrates procurement volumes, presenting vendors with batch-size economies. Higher site counts also magnify supply-chain strain for mmWave-fit parts, where dielectric losses above 24 GHz need ultra-low dissipation factors. Consequently, suppliers with proprietary ceramic chemistries capable of sustaining ±30 ppm/°C drift see preferential design wins.

Adoption of High-Capacitance MLCCs in Smartphone RF Front-Ends

Premium handsets now feature 40% more MLCCs than sub-6 GHz models, as envelope-tracking amplifiers require rapid voltage swings across multiple bands. Kyocera-AVX’s 47 µF, 0402 release underscores the leap in capacitance density, tripling the previous ceiling while retaining a 402-footprint height profile. Samsung’s DDR5-ready series illustrates the convergence of RF and high-speed memory needs, demanding low ESR and low ESL in a single device. Such advances cut board real estate, freeing space for additional antennas and sensors. Integration roadmaps anticipate further capacitance scaling via thinner dielectric layers and stacked electrode counts, benefiting power-delivery efficiency in energy-constrained devices.

Growth in Broadband CPE and Set-Top-Box Shipments

Australia’s Better Connectivity Plan earmarked AUD 2.4 billion (USD 1.6 billion) for rural broadband, while the U.S. ReConnect Program added USD 1.15 billion in 2024 grants. Each outdoor CPE enclosure deploys 15-25 MLCCs tolerant of wide temperature and humidity swings. Set-top boxes migrating to 8K decoding add roughly 30% more capacitors because higher GPU frequencies invite stiffer decoupling. Vendors meeting IEC 60068 moisture-resistance ratings are gaining traction in public-funded procurements that stipulate multi-year service lifetimes.

Expansion of IoT and LPWAN Networks

Cellular IoT endpoints are projected to top 5.1 billion by 2030, each embedding 2-8 MLCCs, mostly in 0201 footprints for NB-IoT and Cat-M1 radios. RedCap specification releases drive a cost-optimized bill of materials, but RF integrity cannot dip below operator thresholds, keeping ceramic capacitors central to design. Industrial IoT mandates automotive-grade reliability, pushing AEC-Q200-qualified MLCCs into smart-factory gateways. Continuous low-voltage sleep modes heighten leakage-current scrutiny, favoring Class 1 chemistries for their sub-10 nA figures at room temperature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile MLCC pricing cycles | -2.3% | Global, with acute impact in cost-sensitive segments | Short term (≤ 2 years) |

| Supply-chain concentration risk in East Asia | -1.9% | Global supply chains, critical for North America and Europe | Medium term (2-4 years) |

| Competition from polymer capacitors in sub-6 GHz filters | -1.4% | Global, particularly in consumer and automotive segments | Medium term (2-4 years) |

| Environmental rules on barium-titanate recycling | -0.8% | Europe, North America, with expanding influence in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile MLCC Pricing Cycles

Capacitor price swings exceeded 300% during the last shortage, upsetting fixed-price telecom contracts. Although 2024 saw normalization, new ceramic kilns require up to 24 months to commission, keeping forward visibility narrow. Because requalifying an MLCC tier can delay a radio design by six months, OEMs seldom switch suppliers mid-cycle, amplifying exposure. Precious-metal electrode pricing and geopolitical events, such as export curbs on Japanese barium-titanate, layer extra volatility on sourcing budgets.

Supply-Chain Concentration Risk in East Asia

Roughly 75% of global MLCC volume originates in Japan, South Korea, and China. A 2024 earthquake in Japan’s Ishikawa prefecture temporarily shut multiple ceramic lines, triggering week-long spot-market shortages. Western OEMs assess dual-sourcing or near-shoring, yet greenfield fabs outside East Asia typically require three to five years to achieve yield parity and often necessitate licensed powder technology. Escalating trade-policy uncertainty around advanced communication gear deepens this vulnerability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Class 1 Dominance Drives mmWave Adoption

Class 1 devices represented 62.05% of 2025 revenue, reflecting strict phase-stability demands in base-station radio units. That share is widening as telecommunication MLCC market size for Class 1 parts expands at 16.55% CAGR to 2031. These capacitors maintain capacitance within ±30 ppm/°C, even when duty cycles exceed 85 °C, ensuring signal phase alignment in 64T64R arrays. Superior Q-factors above 1000 also make Class 1 indispensable in band-edge filters and PA bias tees operating near 28 GHz. Emerging 6G trials exceeding 40 GHz reinforce their runway, with rare-earth-doped NPO blends sustaining low loss tangents. Tooling investments for ultra-thin dielectric tapes allow suppliers to pair stability with respectable volumetric efficiency, blunting historic cost objections.

Class 2 parts, X7R and X5R, remain vital for bulk energy storage and EMI suppression. Their higher k-values deliver above 10 µF in a 402 footprint, a capability Class 1 cannot match. Hybrid stacks that colocate Class 1 atop Class 2 layers in a single body have begun sampling, targeting small-cell radios that juggle RF accuracy with size constraints. In the longer term, IEC 60068 durability norms and outdoor moisture-resistance tests may shift some Class 2 volume toward polymer hybrids; however, overall telecommunication MLCC market demand retains a two-tier dielectric hierarchy, grounded in cost-performance trade-offs.

By Case Size: Miniaturization Accelerates 402 Growth

The 201 outline controlled 55.72% of 2025 shipments due to the presence of entrenched SMT lines in CPE and mid-tier handset boards. Nonetheless, the telecommunication MLCC market size for 402 parts is projected to track a 16.4% CAGR as designers seek board real estate savings. Kyocera-AVX’s 47 µF, 402 achievement validates the cost-per-capacitance advantage, effectively doubling energy density relative to last-gen 603 units. Tighter placement tolerances achievable with modern pick-and-place heads lower tombstoning risk, once a deterrent for 402 adoption.

Larger 603 and 805 bodies remain in high-voltage nodes and lightning-surge suppression modules, segments unlikely to miniaturize until GaN power stages gain broader commercial use. Radial or 1210 footprints find pockets in tower-top amplifiers where creepage distances trump board savings. Simultaneously, research into embedded MLCC technology, dice laminated inside the PCB, threatens to redraw the external case-size taxonomy altogether, though volume production remains at the proof-of-concept stage.

By Voltage Rating: Sub-100 V Units Lead Efficiency Push

Low-voltage MLCCs (less than or eqaul to 100 V) generated 58.75% of 2025 receipts and are forecast to rise at a 16.22% CAGR. Shrinking semiconductor node voltages invite matching supply rails, so decoupling capacitors proportionally down-rate. Envelope-tracking PAs toggle between 0.8 V and 3.4 V supplies within microseconds, necessitating ceramic capacitors that hold capacitance across sharp transients. Their compact dielectric thickness accelerates sintering throughput, feeding cost competitiveness.

Mid-band (100–500 V) parts retain relevance in power-factor-correction and PA gate-bias circuits. They rely on thicker dielectric stacks and silver-palladium electrodes, inflating average selling prices. High-voltage devices (above 500 V) stay niche, but GaN DC-DC converters in radio heads have begun to specify 600 V MLCCs for transient mitigation, hinting at incremental demand. Over time, the telecommunication MLCC market share for low-voltage grades will lift as integrated power-management ICs proliferate.

By MLCC Mounting Type: Metal-Cap Units Find Reliability Niches

Surface-mount variants produced 41.15% of 2025 income and hold lead status for automated assembly yield. Even so, metal-cap designs are securing a 15.96% CAGR, solving vibration-induced cracking in tower-top radios that face wind-load flexing. Their copper caps spread thermal hotspots, raising power-handling headroom, critical for PA bias rails that dissipate tens of watts.

Radial lead configurations persist in retrofit deployments and maintenance stock because through-hole solder lets field technicians replace a single failed part without hot-air rework. SMT’s cost edge keeps it the default, yet hybrid packages, where metal caps are laser-welded onto an SMT body, emerge as a best-of-both architecture. Over time, telecommunication MLCC industry discussions may center on whether these hybrids can hit IPC 9701 fatigue benchmarks at consumer-electronic cost points.

Geography Analysis

North America accounted for 57.05% of 2025 revenue, underpinned by more than USD 100 billion in 5G capex commitments and defense radio refresh cycles that stipulate -55 °C to +125 °C reliability. The region also benefits from Buy American incentives steering rural broadband CPE builders toward domestic sourcing. U.S. semiconductor fabs collaborate with MLCC suppliers on 6G frequencies above 90 GHz, potentially birthing a localized supply chain for leading-edge dielectrics.

Asia-Pacific is on track for a 16.66% CAGR, the fastest worldwide, courtesy of co-located handset, base-station, and passive-component factories. China’s ongoing 5G densification absorbs high volumes domestically, while South Korea’s memory fabs reap cross-supply benefits from ceramic powders. Japanese producers maintain technological leadership, investing in R&D to develop rare-earth-doped compositions that sustain high Q-factors at mmWave frequencies. Regional governments offer tax rebates for new kilns, compressing payback periods and encouraging further capacity build-outs.

Europe maintains moderate growth fueled by industrial automation and EV charging infrastructure, albeit with lower telecommunication MLCC market share due to limited local output. Stringent REACH and RoHS directives push European OEMs to specify halogen-free dielectric binders, affecting supplier qualification hurdles. The EU Chips Act aspires to seed domestic capacitor fabs, yet high capital intensity and licensing complexities suggest a gradual timeline. Nevertheless, European design centers influence global spec sheets, particularly for automotive-grade variants that later transfer to telecom SKUs.

Competitive Landscape

Murata, Samsung Electro-Mechanics, and TDK together control nearly 60% of global capacity, commanding economies of scale from powder synthesis through plating. Their vertically integrated operations shorten R&D feedback loops, allowing them to introduce specialized Class 1 offerings months ahead of their smaller rivals. High entry costs, often USD 400 million per kiln cluster, and 18-month customer qualification windows deter new entrants, cementing an oligopolistic telecommunication MLCC market structure.

Mid-tier vendors, such as Kyocera-AVX and Yageo, differentiate themselves through application-specific engineering, co-designing filters and decoupling networks with OEMs. Kyocera-AVX’s record-setting 47 µF, 0402 product highlights how process innovation can secure board positions without volume leadership. Yageo’s pending acquisition of Shibaura Electronics signals a push to bundle sensors with passives, widening its appeal to telecom gear makers pursuing integrated thermal monitoring.

Pricing remains volatile because a small number of plants determine the supply. Lead-time extensions encourage double-ordering, exaggerating demand signals, and sparking short-term price spikes. To hedge, large OEMs adopt dual-sourcing frameworks and pre-pay capacity reservations. In parallel, some defense-oriented customers stock two-year safety inventories, supporting niche ceramic houses that focus on ultra-ruggedized, low-volume runs.

Telecommunication MLCC Industry Leaders

Taiyo Yuden Co., Ltd

Walsin Technology Corporation

Yageo Corporation

Murata Manufacturing Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kyocera-AVX unveiled the first 47 µF MLCC in a 0402 outline, tripling capacitance density for space-constrained 5G radios.

- January 2025: Yageo Corporation received final METI clearance for its JPY 94.55 billion purchase of Shibaura Electronics, expanding its sensor and MLCC portfolio.

- October 2024: TDK confirmed a multi-year capacity expansion program focused on advanced MLCC lines for mmWave and automotive applications.

- October 2024: Murata reported above-plan earnings, attributing growth to robust 5G base-station MLCC demand.

Global Telecommunication MLCC Market Report Scope

Base Stations, Set Top Boxes, Others are covered as segments by Device Type. 0 201, 0 402, 0 603, 1 005, 1 210, Others are covered as segments by Case Size. 50V to 200V, Less than 50V, More than 200V are covered as segments by Voltage. 10 μF to 100 μF, Less than 10 μF, More than 100 μF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Class 1 |

| Class 2 |

| 201 |

| 402 |

| 603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 – 500 V) |

| High Voltage (above 500 V) |

| Metal-Cap |

| Radial-Lead |

| Surface-Mount |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Dielectric Type | Class 1 | |

| Class 2 | ||

| By Case Size | 201 | |

| 402 | ||

| 603 | ||

| 1005 | ||

| 1210 | ||

| Other Case Sizes | ||

| By Voltage | Low Voltage (less than or equal to 100 V) | |

| Mid Voltage (100 – 500 V) | ||

| High Voltage (above 500 V) | ||

| By MLCC Mounting Type | Metal-Cap | |

| Radial-Lead | ||

| Surface-Mount | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform