Electric Vehicles MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

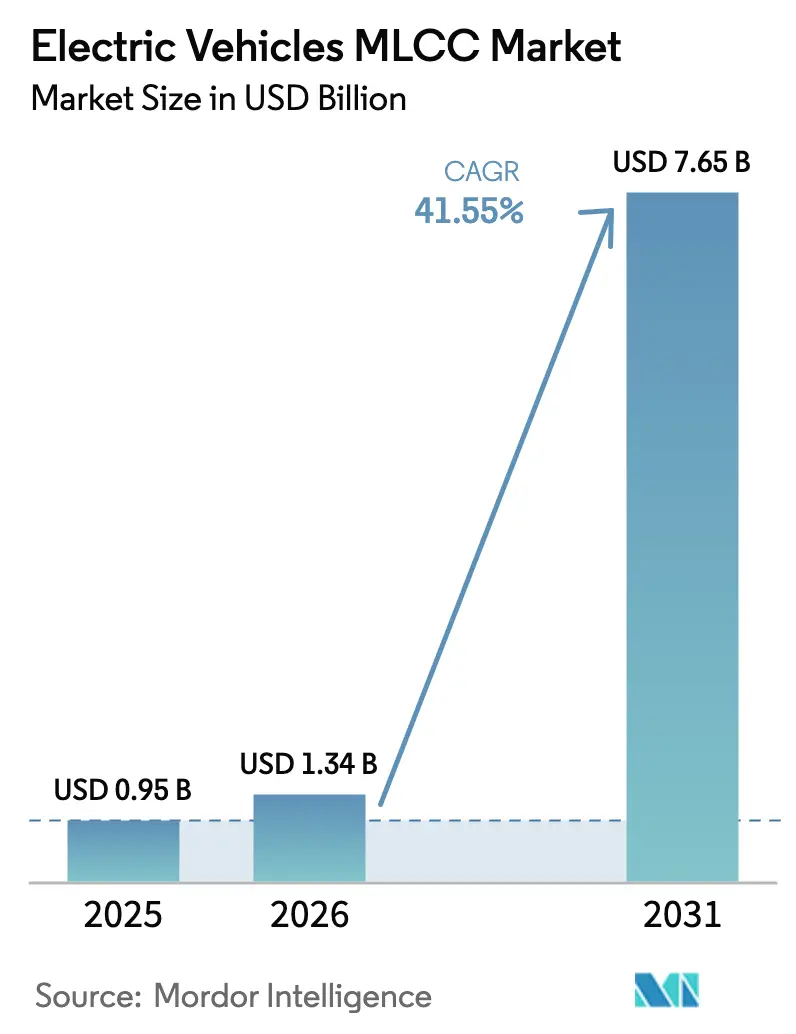

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 7.65 Billion |

| Growth Rate (2026 - 2031) | 41.55% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicles MLCC Market Analysis by Mordor Intelligence

Electric Vehicles MLCC market size in 2026 is estimated at USD 1.34 billion, growing from 2025 value of USD 0.95 billion with 2031 projections showing USD 7.65 billion, growing at 41.55% CAGR over 2026-2031. Adoption of 800 V–1,000 V vehicle architectures, the multiplication of on-board sensors, and the shift to silicon-carbide (SiC) inverters are lifting per-vehicle multilayer ceramic capacitor (MLCC) counts, while localization initiatives and capital-intensive capacity builds temper supply risks. Automakers increasingly design-in temperature-stable Class 1 capacitors for harsh power-electronics zones, and advanced driver-assistance systems (ADAS) are accelerating demand for high-capacitance density footprints. Meanwhile, government incentives under the CHIPS Act encourage regional production, and recycling pilots for end-of-life battery packs are emerging as a supplementary feedstock pathway. Although raw-material price swings and cyclical smartphone demand pose headwinds, sustained xEV output growth and stricter qualification regimes continue to anchor the long-term outlook for the Electric Vehicles MLCC market.

Key Report Takeaways

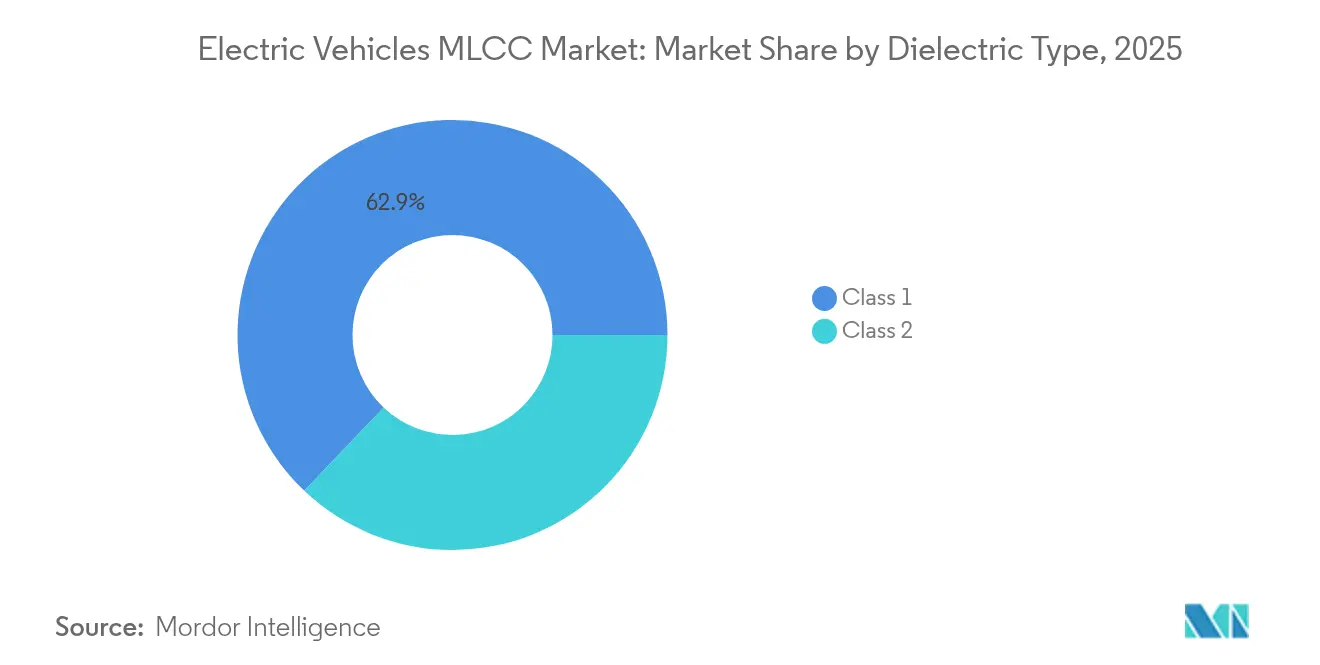

- By dielectric type, Class 1 capacitors led with 62.90% revenue share in 2025 in the Electric Vehicles MLCC market; Class 1 is also projected to advance at a 43.67% CAGR through 2031.

- By case size, the 201 format accounted for 55.90% of the Electric Vehicles MLCC market share in 2025, while the 402 size is projected to grow at a 43.12% CAGR through 2031.

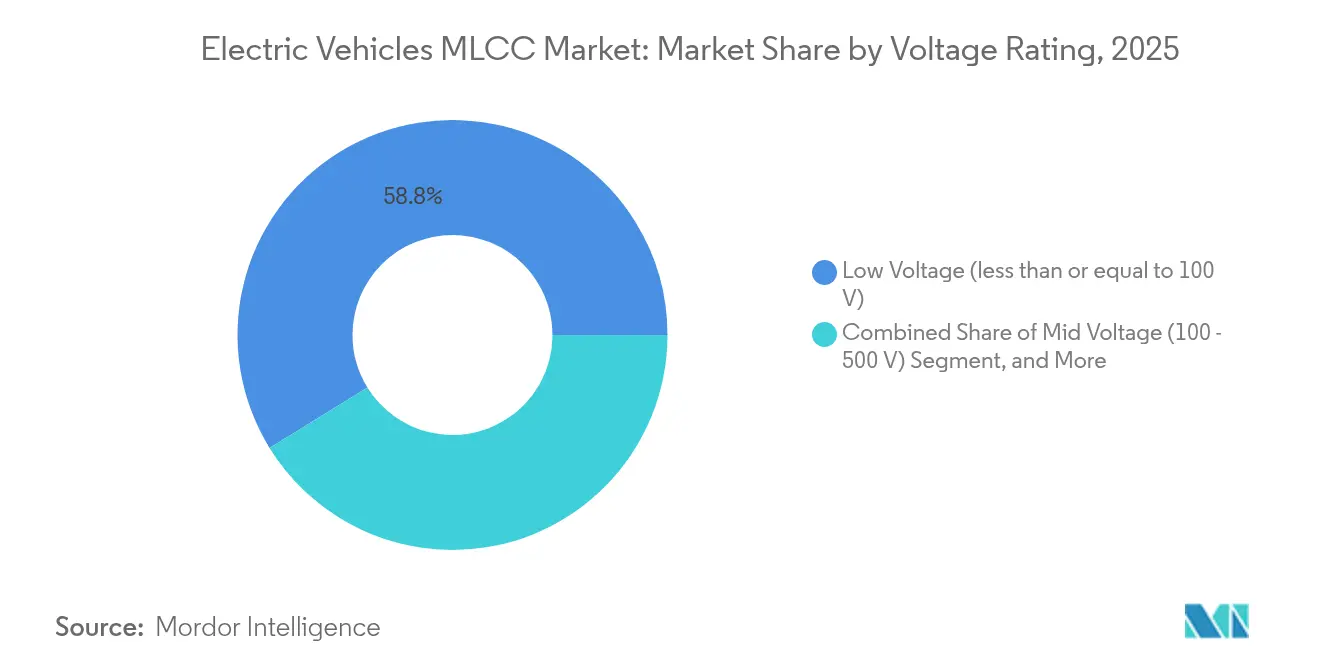

- By voltage rating, low-voltage (less than or equal to 100 V) devices held 58.80% share of the Electric Vehicles MLCC market size in 2025 and are poised to expand at a 42.65% CAGR during the forecast horizon.

- By mounting style, surface-mount devices commanded 41.10% share in 2025 in the Electric Vehicles MLCC market; metal-cap parts are forecast to log a 42.30% CAGR through 2031.

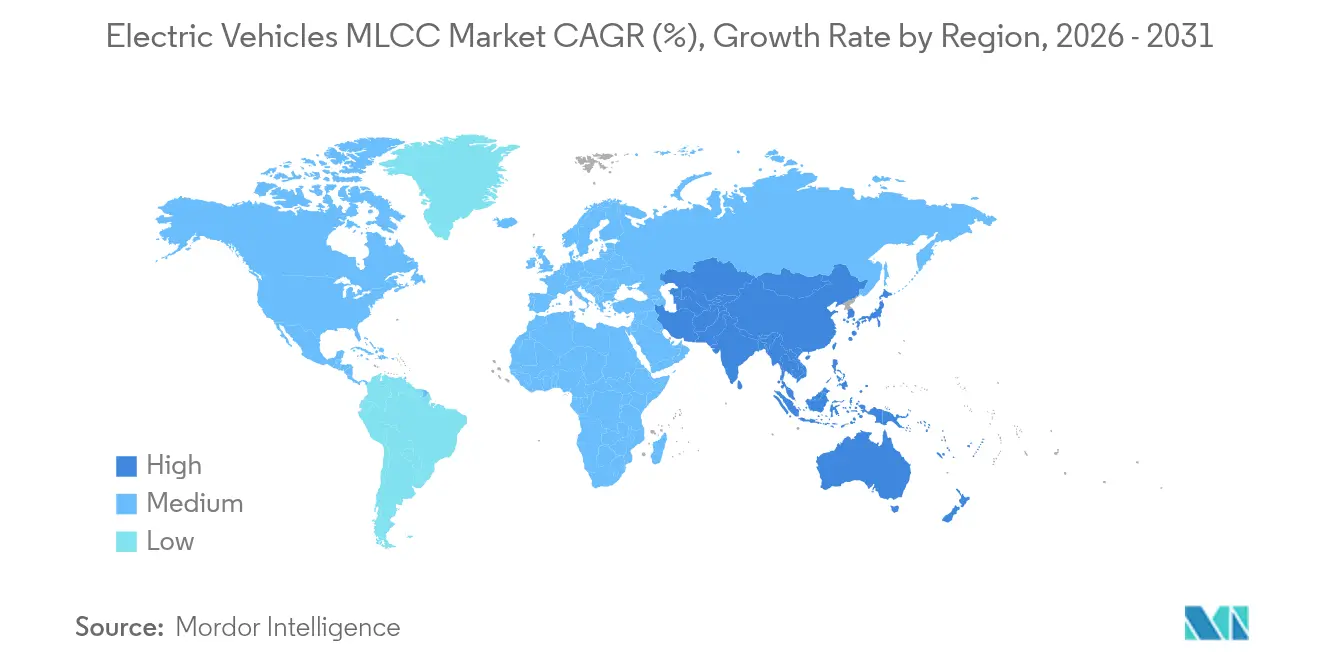

- By region, North America dominated the Electric Vehicles MLCC market with a 56.90% share in 2025, but the Asia-Pacific region is expected to record the highest CAGR of 43.05% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicles MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring EV Powertrain Voltage Platforms Elevate MLCC Demand | +8.2% | Global, with early adoption in Europe and China | Medium term (2-4 years) |

| Integration of Advanced ADAS/Autonomous Modules Requiring High Capacitance Density | +7.1% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift to SiC Inverters Raising Temperature-Stable Class-1 MLCC Uptake | +6.8% | Global, led by premium EV segments | Medium term (2-4 years) |

| OEM Localization Strategies Stimulating Regional MLCC Supply Chains | +6.5% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Capital Expenditure Race by Top-Tier MLCC Makers in EV-Specific Facilities | +5.4% | Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Recycling of MLCCs from End-of-Life EV Packs Creating Secondary Supply Loops | +4.2% | Europe and China, early regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring EV Power-Train Voltage Platforms Elevate MLCC Demand

Vehicle manufacturers are migrating from 400 V to 800 V and even 1,000 V systems to shorten fast-charge times and raise efficiency, which in turn lifts capacitor working voltage, insulation, and reliability requirements. An 800 V pack can replenish 10–80% state-of-charge in under 18 minutes, versus 30+ minutes for 400 V systems, driving installation of additional high-voltage decoupling networks. TDK links this voltage step-up to passive-component volume growth of 4–7% annually inside electric vehicles.[1]TDK Corporation, “Integrated Report 2024,” tdk.com Each battery-electric model now integrates roughly 10,000 MLCCs compared with 5,000 units in an internal-combustion car. Higher system voltages also heighten electromagnetic-compatibility thresholds, causing OEMs to specify more Class 1 parts that exhibit minimal capacitance drift over wide temperature swings. Samsung Electro-Mechanics’ goal of 1 trillion won automotive-MLCC revenue underscores the commercial scale of this demand shift.

Integration of Advanced ADAS/Autonomous Modules Requiring High Capacitance Density

Level 3 and higher autonomy stacks employ 20–30 sensors, LiDAR, radar, and high-resolution cameras, versus fewer than 10 in mainstream models, multiplying local power-filtering nodes. Capacitor counts per sensor module rise because each requires wideband noise suppression and microsecond response times. Research indicates that high-capacitance MLCCs between 1 µF and 100 µF dominate these circuits due to their form-factor advantage. Centralized domain controllers further compound demand, as single-board compute units can hold hundreds of decoupling capacitors to stabilize gigahertz-class processors. ISO 26262 functional-safety requirements call for redundant power rails, cementing MLCC volume increases across ADAS subsystems. As vehicle autonomy grows, the Electric Vehicles MLCC market gains a structural demand tailwind that offsets consumer-electronics cyclicality.

Shift to SiC Inverters Raising Temperature-Stable Class-1 MLCC Uptake

Silicon-carbide switches operate at junction temperatures above 200 °C and switching frequencies beyond 20 kHz, demanding MLCCs with low dielectric loss, tight tolerances, and exceptional thermal stability. Class 1 NPO/COG capacitors exhibit near-zero temperature coefficients and thus dominate these inverter filter positions. TDK has allocated roughly 30% of its three-year JPY 700 billion cap-ex program to expanding high-reliability automotive MLCC lines that address SiC inverter niches. Higher frequencies permit downsized passives, yet elevated dv/dt exacerbates electromagnetic interference, prompting designers to increase the quantity of small-case MLCCs around power modules. Consequently, the Electric Vehicles MLCC market benefits from both rising SiC penetration and stricter reliability specifications.

OEM Localization Strategies Stimulating Regional MLCC Supply Chains

Automakers prioritize sourcing within a 500 km radius to curb logistics risk and align with rules-of-origin under trade pacts such as USMCA. The U.S. Department of Commerce earmarked USD 2 billion in CHIPS Act grants for printed-circuit and component plants, creating incentives for domestic MLCC fabrication.[2]U.S. Department of Commerce, “CHIPS and Science Act Funding Opportunity,” commerce.gov Samsung’s newly expanded Philippines line illustrates a “China-plus-one” approach, servicing North American demand while staying proximate to ceramic-powder suppliers. Localized supply chains grant co-development access, shorten qualification cycles, and shield OEMs from Section 301 capacitor tariffs. These factors collectively inject 6.5% incremental uplift into the Electric Vehicles MLCC market CAGR forecast.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility for Rare-Earth Oxides in Class-2 Dielectrics | +3.8% | Global, with acute exposure in Asia-Pacific | Short term (≤ 2 years) |

| MLCC Shortage Risk Due to Smartphone-EV Demand Collision | +2.9% | Global, particularly affecting consumer electronics hubs | Medium term (2-4 years) |

| Stringent Automotive AEC-Q200 Qualification Cycles Delaying Design-Ins | +2.1% | Global, with extended timelines in North America and Europe | Medium term (2-4 years) |

| Thermal Runaway Failures in High-Voltage MLCCs Triggering Warranty Recalls | +1.4% | Global, concentrated in 800V+ platform deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility for Rare-Earth Oxides in Class-2 Dielectrics

Barium titanate and dopant oxides constitute up to 60% of MLCC manufacturing outlays, and spot prices spiked when mining shutdowns coincided with pandemic-era logistics disruptions. Automotive contracts typically fix prices long term, pushing manufacturers to absorb volatility or renegotiate at the cost of losing design wins. TDK disclosed that commodity swings trimmed JPY 24 billion from passive-component profits in FY 2024, highlighting sensitivity to input costs. As EV volumes climb, competition with consumer electronics for high-purity ceramic feedstock threatens lead-time stability, exerting a 3.8% drag on the Electric Vehicles MLCC market CAGR projection.

MLCC Shortage Risk Due to Smartphone–EV Demand Collision

Fourth-quarter smartphone launches require large batches of high-cap MLCCs, overlapping with automotive production peaks. Given higher margins and shorter qualification windows, suppliers often allocate constrained capacity to handset makers first. Murata’s 2025 earnings flagged price competition from Chinese entrants, even while Taiwan shipments stayed resilient. If similar cycles recur, automotive lines risk 26–32 week lead times, compared to the customary 12–16 weeks, which would delay EV builds and shave 2.9% off the forecast CAGR for the Electric Vehicles MLCC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Class 1 Capacitors Anchor High-Voltage Reliability

Class 1 products accounted for 62.90% of 2025 revenue, underscoring OEM reliance on temperature-stable ceramics for SiC inverters and on-board chargers. The Electric Vehicles MLCC market size for Class 1 is projected to reach USD 5.24 billion by 2031, mirroring a robust 43.67% CAGR. Superior coefficient stability across -55°C to +125°C safeguards capacitance in mission-critical applications. Future designs targeting switching frequencies above 1 MHz reinforce demand for low-loss NPO/COG stacks, securing long-term market share gains.

Class 2 retains niche relevance where volumetric efficiency outweighs thermal drift, particularly in the infotainment and body electronics domains. Yet its susceptibility to capacitance aging and DC-bias effects limits penetration in traction inverters. AEC-Q200 testing cycles of up to 24 months favor incumbent Class 1 suppliers, sheltering margins despite rising unit competition. Consequently, Class 1 dominance is expected to persist as SiC inverter penetration broadens, consolidating the Electric Vehicles MLCC market leadership of high-reliability formulations.

By Case Size: Miniaturization Spurs 402 Adoption

The 201 footprint held 55.90% revenue share in 2025, benefiting from mature process yields and wide-spread pick-and-place compatibility. Nonetheless, the 402 size is poised to make significant strides with a forecasted 43.12% CAGR to 2031 as designers compress electronics around battery packs. The Electric Vehicles MLCC market share leadership may transition once 402 pricing reaches parity with larger footprints in later forecast years.

Miniaturization yields weight and board-area savings essential to OEM range targets. Yet it imposes tighter placement tolerances, pushing suppliers to refine screen-printing and multilayer alignment accuracy. Leaders like Samsung leverage ultra-thin dielectric tape casting to maintain breakdown voltage while slimming form factors. Sustained R&D spending, therefore, underpins the migration to smaller cases without quality trade-offs, supporting the Electric Vehicles MLCC market expansion.

By Voltage Rating: Low-Voltage Devices Remain Volume Engine

Low-voltage MLCCs (less than or equal to 100 V) delivered 58.80% of 2025 sales and are forecast to climb at 42.65% CAGR. Their ubiquity spans body electronics, lighting, and user interfaces, translating into the highest unit volumes within the Electric Vehicles MLCC market size. Mid-voltage (100–500 V) recoups share as 400 V subsystems proliferate, whereas above 500 V parts, though premium-priced, remain a smaller slice tied to traction inverters.

Design-migration toward zonal architectures embeds multiple voltage domains, ensuring continued breadth for low-voltage inventories even as high-voltage rails expand. Suppliers differentiate on insulation-coordination expertise and failure-rate analytics, factors that influence total-cost-of-ownership calculations for OEMs. As ASP erosion in low-voltage classes accelerates, high-voltage SKUs offer margin relief, balancing the Electric Vehicles MLCC market revenue mix.

By MLCC Mounting Type: Metal-Cap Format Gains Traction for Harsh Environments

Surface-mount variants retained 41.10% share in 2025 due to automated line familiarity. Metal-cap devices, although representing a smaller base, will surge at a 42.30% CAGR as traction inverters and battery junction boxes demand enhanced vibration resilience. Once volumes scale, the Electric Vehicles MLCC market size for metal-cap formats could surpass USD 1.21 billion by 2031.

Through-hole radial parts persist for legacy powertrains but face a gradual sunset as OEMs rationalize board real estate. The shift underscores how mechanical reliability bottlenecks rather than pure dielectric performance increasingly guide capacitor selection. Vendors integrating design-for-vibration simulation tools alongside ceramic process know-how will capture this emergent niche.

Geography Analysis

North America commanded 56.90% of 2025 revenue, supported by entrenched Detroit and Silicon Valley EV programs and federal incentives favoring domestic content. Fast-growing charging networks and premium truck launches elevate per-vehicle capacitor counts, while CHIPS Act funding accelerates on-shore passive-component proposals. Although tariff-led cost pressures lifted BOM pricing, OEM localization strategies mitigate lead-time exposures, stabilizing Electric Vehicles MLCC market demand.

Asia-Pacific is projected to register a formidable 43.05% CAGR through 2031 as regional xEV volumes soar. Samsung Electro-Mechanics’ target of 1 trillion won automotive MLCC turnover and TDK capacity additions in Japan highlight the region’s production gravity. Chinese battery-electric output, coupled with Korean ceramic-materials expertise, positions Asia-Pacific as the nucleus for scale economics. De-risking moves such as Philippines line-ups and India pilot runs diversify geopolitical exposure while preserving proximity to raw-material sources, nurturing the Electric Vehicles MLCC market expansion.

Europe, though lagging on absolute scale, leverages stringent fleet-average CO₂ mandates to sustain capacitor demand growth. The Critical Raw Materials Act seeks to reduce dependency on Chinese barium-titanate supplies, creating venture opportunities in local powder synthesis and recycling. German OEM transitions to 800 V architectures amplify high-voltage capacitor use, whereas energy-price volatility motivates efficiency-driven electronic redesigns. The region’s adherence to ISO 26262 spurs extra redundancy layers, augmenting the Electric Vehicles MLCC market baseline.

Competitive Landscape

The Electric Vehicles MLCC market shows moderate concentration: Murata controls nearly 50% of automotive-grade shipments, and TDK holds 35–40% share in selected ceramic categories, forming a duopoly that approaches 85% of premium supply.[3]Murata Manufacturing Co., Ltd., “Murata Value Report 2024,” murata.com High cap-ex barriers and AEC-Q200 cycles exceeding 18 months shield incumbents. Samsung Electro-Mechanics acts as a fast follower, scaling advanced tape-casting lines to challenge leadership in high-voltage grades.

Strategic thrusts emphasize vertical integration. TDK’s Honjo facility will introduce proprietary dielectric-powder synthesis, reducing external sourcing risk and facilitating grade differentiation. Murata’s “layer-portfolio” management balances smartphone cyclicality against automotive backlog, enabling capacity allocation agility across segments. Chinese entrants advance cost-down strategies for body-electronics MLCCs but must still overcome perceptions about long-term reliability to penetrate traction-inverter sockets.

Partnership ecosystems are widening: OEMs co-locate engineers at supplier fabs for accelerated design validation, while Tier-1 power-electronics players stipulate dual-sourced capacitor footprints to avert single-vendor dependencies. Recycling consortia, notably within the European Battery Alliance, entice both ceramic suppliers and vehicle makers to pilot closed-loop ceramic recovery, reflecting emergent sustainability differentiation themes within the Electric Vehicles MLCC market.

Electric Vehicles MLCC Industry Leaders

Kyocera AVX Components Corporation (Kyocera Corporation)

TDK Corporation

Yageo Corporation

Murata Manufacturing Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Samsung Electro-Mechanics expanded automotive MLCC output in the Philippines to capitalize on USMCA regional demand and tariff-free access.

- February 2025: TDK reported JPY 24 billion passive-component profit headwind from inventory corrections but reiterated H2 2025 rebound expectations.

- January 2025: U.S. Department of Commerce granted USD 2 billion under the CHIPS Act to bolster domestic PCB and component ecosystems.

- October 2024: Murata released its “Murata Value Report 2024,” emphasizing automotive MLCC as a core growth pillar.

Global Electric Vehicles MLCC Market Report Scope

0 603, 0 805, 1 206, 1 210, 1 812, Others are covered as segments by Case Size. 50V to 200V, Less than 50V, More than 200V are covered as segments by Voltage. 10 µF to 1000 µF, Less than 10 µF, More than 1000µF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Class 1 |

| Class 2 |

| 201 |

| 402 |

| 603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 – 500 V) |

| High Voltage (above 500 V) |

| Metal Cap |

| Radial Lead |

| Surface Mount |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Dielectric Type | Class 1 | |

| Class 2 | ||

| By Case Size | 201 | |

| 402 | ||

| 603 | ||

| 1005 | ||

| 1210 | ||

| Other Case Sizes | ||

| By Voltage | Low Voltage (less than or equal to 100 V) | |

| Mid Voltage (100 – 500 V) | ||

| High Voltage (above 500 V) | ||

| By MLCC Mounting Type | Metal Cap | |

| Radial Lead | ||

| Surface Mount | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform