Market Overview

| Study Period | 2019 - 2031 |

|---|---|

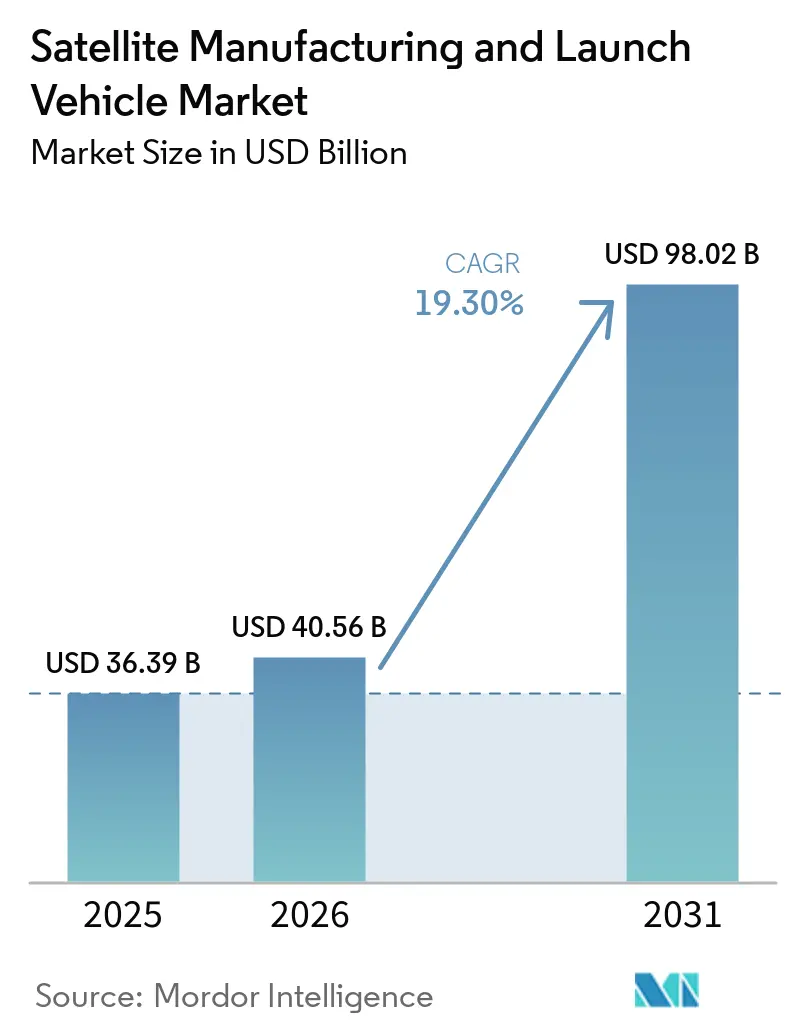

| Market Size (2026) | USD 40.56 Billion |

| Market Size (2031) | USD 98.02 Billion |

| Growth Rate (2026 - 2031) | 19.30% CAGR |

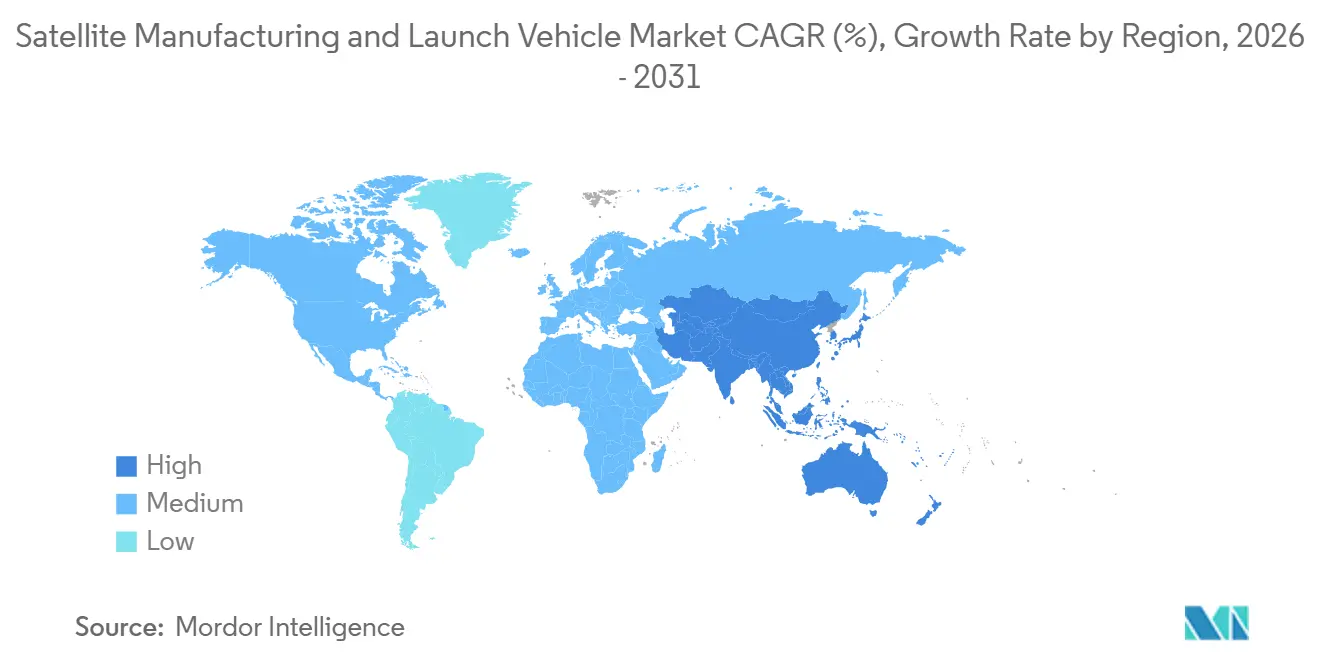

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Manufacturing And Launch Vehicle Market Analysis by Mordor Intelligence

The satellite manufacturing and launch vehicle market size is expected to grow from USD 36.39 billion in 2025 to USD 40.56 billion in 2026 and is projected to reach USD 98.02 billion by 2031, at a 19.30% CAGR over 2026-2031. This expansion reflects a pivot toward large-scale LEO deployments, widening the gap with legacy geostationary missions as constellation operators compress build cycles and secure rapid launch cadence. China’s multi-constellation filings for 203,000 satellites underscore an orbital land grab that raises the bar on frequency coordination and launch throughput planning. Launch reusability is now a structural cost lever in the satellite manufacturing and launch vehicle market as licensing modernization and rapid reuse operations raise flight rates while improving reliability learning curves. Capital flows, defense procurement, and commercial broadband uptake align around proliferated architectures, which are pulling subsystem, component, and software supply chains toward vertical integration at scale.

Key Report Takeaways

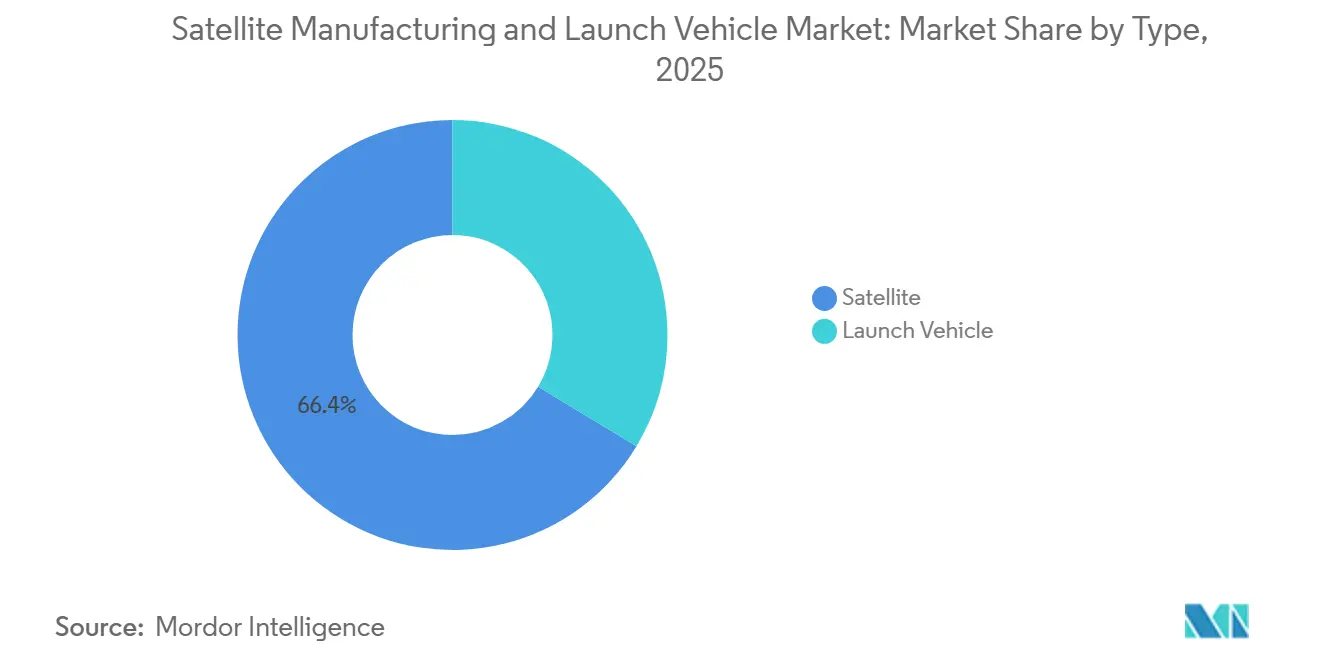

- By type, satellite led the satellite manufacturing and launch vehicle market with a 66.35% share in 2025 and is the fastest-growing segment, with a 23.00% CAGR through 2031.

- By orbit, LEO accounted for a 39.00% share of the satellite manufacturing and launch vehicle market in 2025 and is projected to record the highest growth at a 19.90% CAGR through 2031.

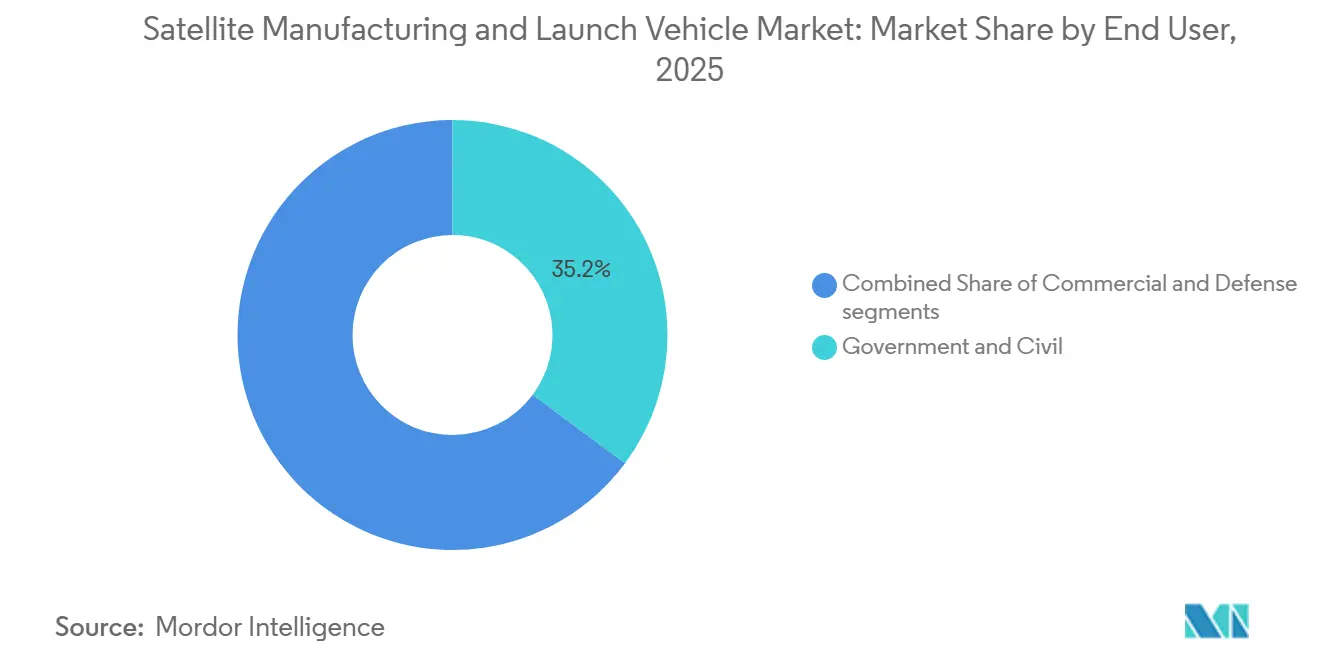

- By end user, the government and civil segment captured a 35.17% share of the satellite manufacturing and launch vehicle market in 2025, while the commercial segment is forecast to grow at the highest CAGR of 20.81% through 2031.

- By application, communication services accounted for 55.00% market share in 2025, while national security and surveillance is the fastest-growing segment at a 19.89% CAGR through 2031.

- By subsystem, satellite buses accounted for 24.55% of the satellite manufacturing and launch vehicle market in 2025. Satellite payload is the fastest-growing at a 23.81% CAGR through 2031.

- By geography, North America retained a 60.76% share of the satellite manufacturing and launch vehicle market in 2025. Asia-Pacific is the fastest-growing region, with a 29.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Satellite Manufacturing And Launch Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reusable launch systems reducing access costs | +2.5% | North America, China, broader Asia-Pacific | Medium term (2-4 years) |

| LEO constellation expansion boosting launch demand | +2.1% | Global, led by North America and China | Short term (≤ 2 years) |

| Defense shift towards distributed space architecture | +1.8% | North America, Europe, Asia-Pacific including India, Japan, South Korea | Medium term (2-4 years) |

| Private capital accelerating commercial space deployment | +1.4% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising dependence on satellite-based infrastructure services | +1.3% | Global, critical infrastructure in the UK, US, India | Long term (≥ 4 years) |

| Propulsion and manufacturing technology efficiency gains | +0.9% | Global innovation hubs in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LEO Constellation Expansion Boosting Launch Demand

SpaceX’s deployment of over 9,350 Starlink satellites into orbit by December 2025, and the planned increase in launches during 2026, underscore that the scale of satellite constellations is driving demand for reliable, high-frequency launch capacity in the satellite manufacturing and launch vehicle markets. Amazon’s Project Kuiper advanced its 3,236‑satellite plan and aligned multi‑provider launch procurement to secure service milestones beginning in early 2026.[1]Amazon Staff, “Project Kuiper Deployment Update,” Amazon, aboutamazon.com China accelerated the GW and Qianfan constellations and signaled even higher launch activity for 2026 as filing activity and domestic industrial capacity expand. India cleared spectrum pathways for satellite broadband services in late 2025, positioning future mega-constellation deployments for Asia-Pacific coverage as the market pivots to underserved regions. ITU filing obligations that require rapid partial deployment to retain spectrum rights are compressing program timelines, which amplifies launch cadence as a gating factor across multi-orbit networks.[2]International Telecommunication Union, “Radio Regulations,” ITU, itu.int

Defense Shift Towards Distributed Space Architecture

Defense procurement is moving to proliferated LEO networks that improve resilience and responsiveness for missile warning, tracking, and secure communications across the satellite manufacturing and launch vehicle market. The US Space Development Agency's tranches have expanded award momentum into 2025 as tracking and transport layers add coverage and redundancy with a growing combined satellite count. Budget priorities in FY2025 reinforce this direction and sustain investment in protected tactical communications and resilient sensing layers. The National Reconnaissance Office's Silent Barker constellation, launched in 2023, became operational in early 2025. It enhances space-domain awareness in geosynchronous orbit by supporting the detection and characterization of objects in GEO. European programs continued to emphasize sovereign secure connectivity, adding to multi-region momentum for distributed architectures that complement national defense strategies. This transition is embedding dual-use capabilities that serve defense and commercial users through common buses, payloads, and data transport layers.

Reusable Launch Systems Reducing Access Costs

First-stage reusability has shifted launch-market economics by enabling higher flight cadence with shorter refurbishment intervals, compressing marginal costs, and stabilizing schedules. In 2025, Falcon 9 Block 5 first stages exceeded 20 flights in operational service, enhancing confidence in booster lifecycle planning and fleet utilization. Blue Origin's New Glenn, following two launches in 2025, is scheduled to commence regular operations in 2026, providing a high-capacity reusable platform that broadens heavy-lift capabilities for multi-satellite deployments. China's LandSpace achieved significant progress toward reusability with the Zhuque-3 launch in late 2025. The vertical recovery test successfully demonstrated closed-loop guidance performance for stage return. Streamlined licensing frameworks facilitate a higher launch tempo and enable rapid refurbishment schedules, thereby reducing bottlenecks in the constellation buildout. As flight-proven hardware becomes standard, competitive pressure encourages multi-manifest optimizations that improve payload economics in the satellite manufacturing and launch vehicle market.

Private Capital Accelerating Commercial Space Deployment

Large private rounds and strategic investments sustained constellation and launch development in 2024 and 2025, reinforcing the market's growth profile. Operators advancing direct-to-device architectures secured multiyear capital support to back larger spacecraft and advanced payloads, with program milestones tied to demonstrated service links. India's private launch ecosystem has outlined capacity expansion plans for 2026 and beyond, with production capabilities designed to meet monthly launch objectives. Meanwhile, China's commercial space sector has introduced new funding mechanisms to advance reusable launch systems and satellite-IoT initiatives, with some rocket manufacturers progressing toward public listings. The net effect is a deeper pipeline of flight hardware and services that integrates upstream manufacturing and downstream service models across the satellite manufacturing and launch vehicle market. Operators that align financing with manufacturing scale and rideshare access are best positioned to sustain deployment momentum into 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital requirements and financial risk exposure | -1.7% | Global, acute in emerging markets including India and Brazil | Medium term (2-4 years) |

| Regulatory barriers and spectrum allocation constraints | -1.3% | Global, with bottlenecks in the US, EU, and India | Long term (≥ 4 years) |

| Critical component supply chain bottlenecks | -1.1% | North America and Asia-Pacific for semiconductors, Europe for optics | Short term (≤ 2 years) |

| Orbital congestion and space debris risk growth | -0.9% | LEO critical, GEO moderate, global concern | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Requirements and Financial Risk Exposure

Long development cycles and significant non-recurring engineering outlays create financing risk for new entrants, especially when flight heritage is required to unlock commercial demand. Program-level financing commitments for LEO broadband networks in 2024 highlighted the need for multi-billion-dollar support before service activation. Heavy-lift contracts for large spacecraft continue to price at nine-figure levels, as seen in late 2025, which concentrates risk in fewer missions. Private companies that do not diversify revenue around launch and downstream services often face extended timelines to close commercial backlogs. Capital intensity also extends beyond vehicles to manufacturing infrastructure and regulatory compliance, which can delay breakeven schedules. As project debt and equity commitments increase, program execution risks may lead to higher financing costs and contingencies.

Regulatory Barriers and Spectrum Allocation Constraints

US licensing for large constellations requires multi-agency coordination and environmental review, which can extend approval timelines and delay initial deployments. Power flux density protections for incumbents can constrain usable capacity for certain non-geostationary systems, thereby affecting regional service economics. Global coordination under ITU procedures requires bilateral engagement with many administrations, and large orbital filings add complexity to securing interference-free operations. China’s late-2025 filings increased Ku- and Ka-band contention and elevated planning uncertainty for overlapping constellations. The FCC’s ongoing modernization effort seeks to consolidate licensing regimes while introducing new mechanisms for underused spectrum, but industry feedback warns of potential allocation volatility. These factors combine to raise schedule risk across multi-orbit programs in the satellite manufacturing and launch vehicle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Launch Bottlenecks Drive Vehicle Segment Outperformance

Satellite led with 66.35% of the market share in 2025, while the launch vehicles segment grew with an 9.89% CAGR expected through 2031. The market experienced growth in 2025 due to a high launch cadence, which aligned capacity with constellation backlogs and improved throughput efficiency. US commercial revenue in 2025 was dominated by Falcon 9 as reuse drove mission economics and opened more rideshare slots.[3]Federal Aviation Administration, “2025 Annual Compendium of Commercial Space Transportation,” FAA, faa.gov The launch supply picture broadened in Asia-Pacific as China increased flight rates and diversified commercial providers, adding resilience to manifest planning. Rideshare missions improved price-access for small satellites but introduced trade-offs in insertion altitude and schedule certainty. As reuse matures and heavy-lift vehicles enter service, launch capacity becomes a differentiating asset for rapid LEO deployment.

The market incorporated additional vertical offerings at launch, such as mission integration and rapid manifest swaps, which maintained the cadence through 2025. Competitive pressure encouraged entrants to prioritize reusability and avionics commonality to lower the marginal cost per flight. China’s private launch firms advanced reusability pilots and signaled increased flight counts in 2026, which should support constellation buildouts in the region. Small satellite operators used rideshare to manage cost but often accepted delays to access preferred orbital planes, which kept dedicated missions in demand for time-sensitive deployments.

By Orbit: LEO Dominance Masks MEO’s Latency-Driven Resurgence

LEO maintained a 39.00% share in 2025 and grew at the highest CAGR of 19.90% through 2031, driven by dense broadband constellations. The market has allocated additional resources to LEO replenishment and second-generation designs as operators work to expand capacity and enhance reliability. MEO capacity meets specific coverage and service-level needs, including maritime and aviation routes where stable beams and service availability take priority over minimum latency.

The MEO is projected to expand at a 17.87% CAGR through 2031 as service-quality requirements push differentiated routing and backhaul paths. In parallel, GEO platforms continued to serve broadcast and fixed-satellite links, while operators rationalized their fleets in line with IP-based video trends. Multi-orbit service portfolios gained traction as enterprise users blended LEO, MEO, and terrestrial solutions to ensure continuity and coverage. Program designs increasingly incorporate crosslinks and flexible payloads that shift capacity to where demand peaks in the satellite manufacturing and launch vehicle market.

By End User: Commercial Segment Eclipses Government as Private Capital Floods Market

Government and civil captured a 35.17% share in 2025, while the commercial segment experienced a 20.81% CAGR through 2031. The market experienced growing subscription and enterprise demand for direct-to-device services, broadband backhaul, and maritime connectivity, which is expected to continue through 2025. Private financing supported ongoing production and service activation, including capital raises by leading operators and direct network investments by MNO partners. Government and civil budgets were steady in 2025, while defense continued to prioritize proliferated architectures for resilient sensing and transport.

Public-sector spending in Europe decreased due to budget rationalization, impacting long-term programs planned for 2025. Meanwhile, commercial demand grew, driven by flexible capacity and reduced terminal costs, which supported the adoption of fixed wireless access and maritime applications. Vertically integrated operators used subscriber revenue to maintain launch schedules, thereby strengthening their market position.

By Application: Communication Dominance Masks Earth Observation’s Intelligence-Driven Surge

Communication services held 55.00% share in 2025, anchored by proliferated broadband and evolving direct-to-device links, while National security and surveillance is the fastest-growing at a 19.89% CAGR. SAR and optical constellations advanced resolution and tasking timelines, extending use cases across defense, agriculture, and infrastructure. Enterprise platforms have integrated Earth Observation feeds with analytics workflows, providing added value for customers managing distributed assets.

The market encompasses diverse applications that utilize hybrid connectivity and monitoring stacks to serve logistics, energy, and government customers with customized SLAs. Earth Observation providers increased capacity and coverage while expanding tasking windows to shorten time-to-insight. Navigation systems sustained cross-industry roles in timing and positioning, which underpins economic activity and emergency response.

By Subsystem: Payload Dominance Erodes as GNC Complexity Escalates

Satellite buses are projected to hold the highest market share in the satellite subsystem segment, accounting for 24.55% by 2025, underscoring their significant role in the industry. The Guidance, Navigation, and Control System (GNC) segment experienced the fastest growth in the launch vehicle subsystem market, with a 11.30% CAGR. Regulatory modernization and rapid reusability encouraged advanced autonomous flight termination and precision guidance, raising the sophistication of launch vehicle avionics. Operators shifted spending toward flexible payloads and software-defined capabilities to match capacity with evolving demand. The growing flight heritage of high-cycle boosters has validated the investment in robust IMUs and control systems to maintain recovery margins at a higher cadence.

Satellite payloads are experiencing growing demand for high-throughput antennas, optical sensors, and SAR apertures, driven by advancements in communication, imaging, and remote sensing technologies. At the same time, factory-style satellite bus production compressed schedules and reduced unit costs, thereby shifting more value to the payload and GNC subsystems. Precision landing control surfaces, navigation receivers, and onboard compute received increased investment to support frequent reuse. Industrialized manufacturing in China and India added supply capacity for smallsat buses, feeding constellations across communications and Earth Observation.

Geography Analysis

North America retained a 60.76% share in 2025 as high launch cadence and defense programs anchored demand and investment in the satellite manufacturing and launch vehicle market. US operators leveraged vertical integration to sustain monthly flight targets and coordinate constellation deployments. Defense budgets prioritized proliferated LEO architectures for sensing and secure communications in 2025. Licensing modernization enabled reusability and rapid turnaround, contributing to throughput gains across the region.

Asia-Pacific is the fastest-growing region, with a 29.35% CAGR, as China's commercial launch activity and industrial scaling intensify capacity across vehicles and satellites. The National Commercial Aerospace Development Fund added multi-year financing support for reusable launch and satellite networking ventures. India's advanced heavy-lift missions secured international payload contracts, with LVM3 enhancing the regional commercial presence in late 2025. In November 2025, South Korea completed a private-led orbital mission, expanding its capacity and highlighting the rise of additional regional suppliers.

Europe is driven by the transition of Ariane 6 toward commercial service, while regional operators continue to adopt multi-orbit strategies. New manufacturing investments supported software-defined payloads and flexible capacity models for enterprise and government customers. Public programs prioritized sovereignty and resilience, supporting secure communications and situational awareness. Cross-regional procurement and rideshare access helped European users maintain deployment schedules during the transition period.

Competitive Landscape

The satellite manufacturing and launch vehicle market is moderately concentrated, with major players such as The Boeing Company, Airbus SE, Northrop Grumman Corporation, and Space Exploration Technologies Corp. handling the majority of high-value contracts. The launch services market is highly concentrated, with a single provider expected to hold the majority of US commercial launches in 2025 through extensive vertical integration and the use of reusable first stages. The cost efficiencies enabled by reusability have supported competitive pricing, intensifying pressure on expendable or delayed vehicles. New heavy-lift capacity is scheduled to enter the market in 2026, expanding options for large payloads and multi-satellite missions. Meanwhile, mid-lift providers are continuing to invest in next-generation vehicles, including reusable designs tailored for frequent constellation deployments.

Chinese manufacturers scaled industrial lines for 100-1,000 kg classes, focusing on short cycle times and standardized buses. European and US primes advanced software-defined payloads and flexible designs that suit multi-orbit portfolios. Vertical integration extended into terminals and inter-satellite links as operators sought to safeguard against supply bottlenecks and control costs.

Strategic initiatives in 2024 and 2025 focused on significant customer-financed programs for LEO communications and milestone-based funding aimed at achieving manufacturing scale. In lunar logistics, commercial providers secured multiyear contracts to deliver surface transportation services at lower unit costs compared to historical programs. On the regulatory side, licensing modernization facilitated the integration of launch operations with reusability certifications, supporting a high quarterly launch frequency. Facility investments in Europe enhanced capacity for next-generation, software-configurable satellites.

Satellite Manufacturing And Launch Vehicle Industry Leaders

Airbus SE

Northrop Grumman Corporation

China Aerospace Science and Technology Corporation

The Boeing Company

Space Exploration Technologies Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: IN-SPACe announced the selection of three private firms, Astrome Technologies, Azista Industries, and Dhruva Space, to develop indigenous small satellite bus platforms under its ‘Satellite Bus as a Service’ initiative. Each company will receive INR 5 crore (USD 0.55 million) to design scalable, modular satellite buses, which are essential for payload support and mission functionality.

- July 2025: Airbus Defence and Space was selected as the prime contractor for the development and production of two new PAZ-2 radar satellites, ensuring the continuity of the existing Earth observation PAZ satellite, which has been operational since 2018.

Global Satellite Manufacturing And Launch Vehicle Market Report Scope

The satellite manufacturing and launch vehicle market encompasses the design, production, integration, and deployment of spacecraft across various size classes, as well as the vehicles used to transport them into Earth and deep-space orbits. This includes satellite platforms, payload systems, propulsion units, subsystems, and end-of-life deorbit solutions, along with light, medium, and heavy launch vehicles supporting commercial, civil, and defense missions.

The satellite manufacturing and launch vehicle market is segmented by type, orbit, end user, application, subsystem, and geography. By type, the market is segmented into satellite and launch vehicles. By orbit, the market is segmented into LEO, MEO, and GEO. By end user, the market is segmented into commercial, government and civil, and defense. By application, the market is segmented into communication, earth observation, navigation, science and exploration, and national security and surveillance. By subsystem, the market is segmented into satellite subsystems and launch vehicle subsystems. The report also covers the market sizes and forecasts for the satellite manufacturing and launch vehicle market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

By Type

| Satellite | Small Satellites |

| Medium Satellites | |

| Large Satellites | |

| Launch Vehicle | Light |

| Medium | |

| Heavy |

By Orbit

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

By End User

| Commercial |

| Government and Civil |

| Defense |

By Application

| Communication |

| Earth Observation |

| Navigation |

| Science and Exploration |

| National Security and Surveillance |

By Subsystem

| Satellite Subsystems | Propuslion System |

| Satellite Buses | |

| Satellite Payload | |

| Satellite Antenna | |

| Others | |

| Launch Vehicle Subsystems | Structure |

| Propulsion Systems | |

| Electrical Power Systems | |

| Guidance, Navigation, and Control System (GNC) | |

| Others |

By Geography

| North America | United States | |

| Canada | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Satellite | Small Satellites | |

| Medium Satellites | |||

| Large Satellites | |||

| Launch Vehicle | Light | ||

| Medium | |||

| Heavy | |||

| By Orbit | Low Earth Orbit (LEO) | ||

| Medium Earth Orbit (MEO) | |||

| Geostationary Orbit (GEO) | |||

| By End User | Commercial | ||

| Government and Civil | |||

| Defense | |||

| By Application | Communication | ||

| Earth Observation | |||

| Navigation | |||

| Science and Exploration | |||

| National Security and Surveillance | |||

| By Subsystem | Satellite Subsystems | Propuslion System | |

| Satellite Buses | |||

| Satellite Payload | |||

| Satellite Antenna | |||

| Others | |||

| Launch Vehicle Subsystems | Structure | ||

| Propulsion Systems | |||

| Electrical Power Systems | |||

| Guidance, Navigation, and Control System (GNC) | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.