Satellite Launch Vehicle Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 5.6 Billion |

| Market Size (2030) | USD 13.06 Billion |

| Growth Rate (2025 - 2030) | 18.44% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Launch Vehicle Market Analysis by Mordor Intelligence

The Satellite Launch Vehicle Market size is estimated at 5.6 billion USD in 2025, and is expected to reach 13.06 billion USD by 2030, growing at a CAGR of 18.44% during the forecast period (2025-2030).

The satellite launch vehicle market is experiencing a transformative shift driven by increasing commercialization and technological advancements in space exploration. Private companies are revolutionizing the industry through innovations in reusable launch vehicle technology and cost-effective space launch services. The emergence of new players has intensified competition, leading to reduced launch costs and increased accessibility to space. This democratization of space access has resulted in a surge of satellite deployments, with over 4,131 satellites being placed in Low Earth Orbit (LEO) for various applications, including communication and Earth observation.

The industry is witnessing a significant evolution in launch vehicle capabilities and mission complexity. Major space agencies and private companies are developing next-generation satellite launch vehicles with enhanced payload capacities and improved efficiency. In March 2023, ISRO demonstrated its growing capabilities by successfully launching 36 OneWeb communications satellites, marking a significant milestone in commercial space operations. The industry is also seeing a trend toward more ambitious projects, as evidenced by SpaceX's announcement in January 2023 to complete up to 100 orbital flights within the year, showcasing the increasing frequency and scale of launch operations.

Commercial partnerships and strategic collaborations are reshaping the space launch market landscape. Amazon's strategic agreement for 83 launches over five years for its Project Kuiper broadband internet constellation exemplifies the growing intersection of technology companies and space launch services. These partnerships are driving innovation in launch vehicle design and operations, leading to more specialized and efficient launch services. The industry is seeing increased participation from both traditional aerospace companies and new entrants, creating a diverse ecosystem of launch service providers.

The market is characterized by rapid technological advancements in launch vehicle design and manufacturing processes. Companies are investing in innovative technologies such as 3D printing for rocket components, advanced propulsion systems, and sophisticated flight control systems. These technological improvements are enabling more precise payload deployments and expanding the range of possible missions. Launch vehicles are becoming more versatile, capable of accommodating multiple payloads in single launches, and offering various orbit insertion capabilities. This technological evolution is supported by advancements in materials science, propulsion technology, and automation, leading to more reliable and cost-effective spacecraft launch solutions.

Global Satellite Launch Vehicle Market Trends and Insights

Growing demand and competition in the global satellite launch vehicle market

- North America has been a pioneer in space exploration, with many space missions having their origins in the region. SpaceX is a leading aerospace company in North America that manufactures and launches advanced reusable rockets and spacecraft. It is currently the leading provider of launch services in the region, with its launch vehicles including Falcon-9, Falcon Heavy, and Starship. During 2017-2022, SpaceX’s rockets launched approximately 2,744 satellites into orbit.

- In Europe, companies such as ArianeGroup are developing the Ariane Next rockets, which involve a reusable first stage for the Ariane rocket. Russia's Roscosmos is another key player in the market, with a long history of developing and deploying launch vehicles. The company is responsible for the development of the Soyuz and Proton rockets, which have been used to launch a range of satellites into space. During 2017-2022, the Soyuz rocket launched approximately 611 satellites into space for various satellite operators globally.

- In Asia-Pacific, CASC is responsible for developing and deploying a range of launch vehicles, including the Long March series, which has become one of the most reliable launch vehicles in the world. During 2017-2022, CASC's Long March rocket launched approximately 372 satellites into space for various satellite operators globally. During 2017-2022, JAXA launched approximately 25 satellites into space for various satellite operators globally using its H-IIA and H-IIB rockets. India's space program has also seen significant growth in recent years, with the ISRO playing a key role in the development of the country's launch vehicles. During 2017-2022, ISRO's rockets launched approximately 171 satellites into space for various satellite operators globally.

Investment opportunities in the global satellite launch vehicle market

- In North America, global government expenditure for space programs hit a record of approximately USD 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space in the world. In terms of funds allocated for launch vehicle development, under FY 2023 President's Budget Request Summary from FY 2022-FY 2027, NASA is expected to receive USD 13.8 billion.

- In November 2022, ESA announced that it had asked its 22 nations to back a budget of EUR 18.5 billion for 2023-2025, with Germany, France, and Italy being the major contributors. Developed at a cost of just under USD 3.9 billion and originally set for an inaugural launch in July 2020, the project has been hit by a series of delays. The governments of France, Germany, and Italy announced that they had signed an agreement on "the future of launcher exploitation in Europe" to enhance the competitiveness of European vehicles while ensuring independent European access to space.

- In February 2023, the Indian government announced that ISRO is expected to receive USD 2 billion for various space-related activities. Under the Outlay on Major Schemes, INR 9,441 crore has been allocated for launch activity, R&D on rockets, engines, satellites, etc. In March 2021, Japan announced its plan to spend USD 4.14 billion on space-related activities. In March 2023, South Korea announced that approximately USD 113.6 million would be used to develop a next-generation carrier rocket, the KSLV-2.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Rising demand for satellite miniaturization globally

Segment Analysis: Orbit Class

LEO Segment in Satellite Launch Vehicle Market

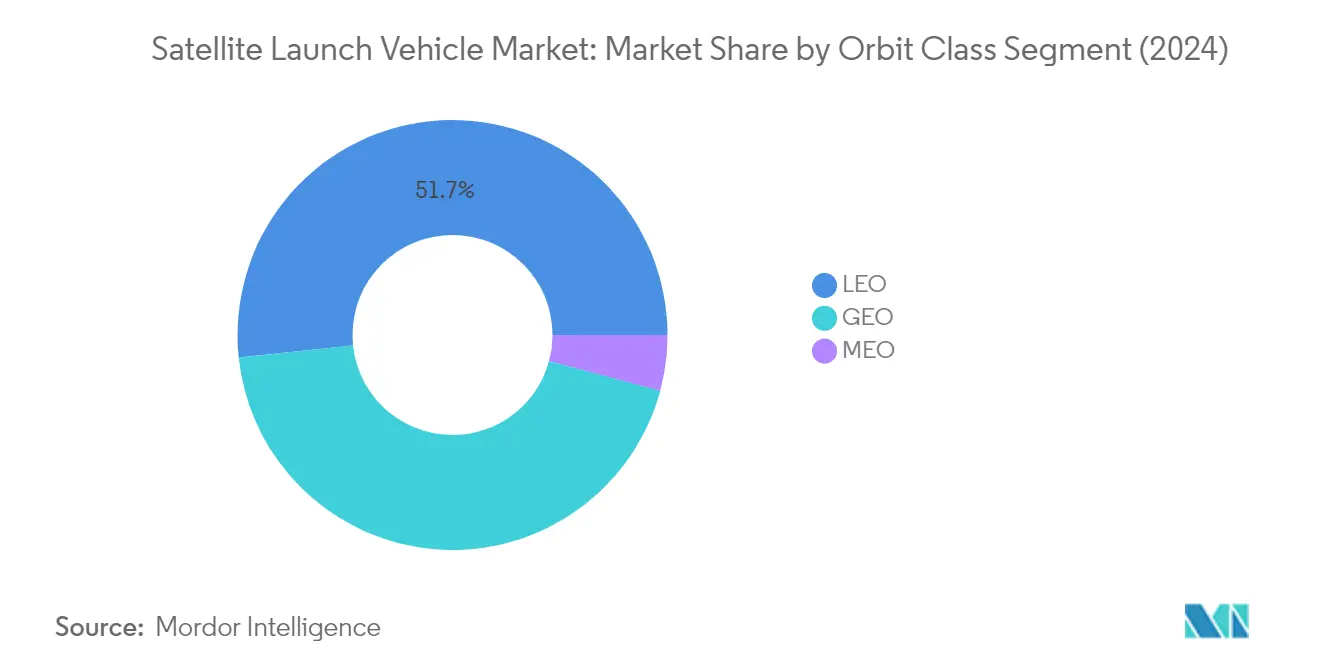

The Low Earth Orbit (LEO) segment dominates the satellite launch vehicle market, commanding approximately 52% market share in 2024. This significant market position is primarily driven by the increasing adoption of LEO satellites in modern communication technologies and their crucial role in Earth observation applications. The segment's dominance is further strengthened by the growing deployment of satellite constellations for global internet coverage and telecommunications. Government initiatives pertaining to LEO satellites and their diverse applications, including commercial communications, Earth observation, navigation, and military surveillance, have contributed substantially to the segment's market leadership. The cost-effectiveness and reduced latency of LEO satellites compared to other orbits have made them particularly attractive for commercial operators and government agencies alike.

LEO Segment Growth in Satellite Launch Vehicle Market

The Low Earth Orbit (LEO) segment is experiencing remarkable growth momentum, projected to expand at approximately 25% during 2024-2029. This exceptional growth rate is fueled by several factors, including the increasing demand for high-speed internet connectivity, Earth observation services, and the rising adoption of small satellite constellations. The segment's growth is further accelerated by technological advancements in satellite miniaturization and the development of more cost-effective launch vehicle solutions. Private space companies are increasingly focusing on LEO missions, developing reusable launch vehicles and innovative deployment systems specifically designed for LEO satellites. The segment is also benefiting from growing investments in space-based internet infrastructure and the increasing demand for real-time Earth observation data across various industries.

Remaining Segments in Orbit Class

The Geosynchronous Earth Orbit (GEO) and Medium Earth Orbit (MEO) segments continue to play vital roles in the satellite launch vehicle market. GEO remains crucial for telecommunications and weather monitoring applications, offering advantages in terms of coverage area and stability for long-term missions. MEO serves as an optimal choice for navigation satellites and specialized communication systems, providing a balance between coverage and latency. These segments are particularly important for specific applications where their unique orbital characteristics provide distinct advantages over LEO satellites. The continued development of advanced launch vehicles capable of reaching these higher orbits ensures their sustained relevance in the overall market landscape.

Segment Analysis: Launch Vehicle MTOW

Medium Segment in Satellite Launch Vehicle Market

The medium launch vehicle segment dominates the satellite launch vehicle market, accounting for approximately 51% of the total market value in 2024. Medium launch vehicles are critical for launching satellites, conducting scientific missions, and resupplying the International Space Station. These vehicles are designed to launch payloads weighing between 2,000 kg and 20,000 kg into geosynchronous orbit. The segment's dominance is driven by the increasing number of satellites being launched into orbit due to rising space activities. Companies like SpaceX and Amazon are actively utilizing medium launch vehicles for their satellite constellation deployments, with plans to launch thousands of satellites to provide high-speed internet access to remote and underserved areas. Blue Origin's development of New Glenn, an advanced medium-lift launch vehicle capable of delivering up to 45,000 kg to lower orbit, further strengthens this segment's position in the market.

Light Segment in Satellite Launch Vehicle Market

The small launch vehicle segment is experiencing the most rapid growth in the satellite launch vehicle market, with a projected growth rate of approximately 31% during 2024-2029. This remarkable growth is driven by the expansion of small satellite capabilities and their increasing strategic utility in the space industry. Programs such as the Aerial Launch Assisted Space Approach (ALASA) are focused on creating cost-effective methods for launching small satellites, with goals of achieving significant cost reductions compared to current military and commercial launch costs. The European Space Agency's initiatives to test new navigation satellites in lower Earth orbits are also contributing to the segment's growth. Light launch vehicles differ from conventional heavy-lift launchers in terms of performance and cost-effectiveness, making them particularly attractive for small satellite deployments.

Remaining Segments in Launch Vehicle MTOW

The heavy launch vehicle segment continues to play a crucial role in the satellite launch vehicle market, particularly for interplanetary missions and launching heavy payloads. These vehicles, capable of lifting between 20,000 kg and 50,000 kg to low Earth orbit, are essential for major resupply missions to the ISS and orbital insertions. NASA's collaboration with private players such as SpaceX and Blue Origin in developing heavy-lift launch vehicles demonstrates the segment's strategic importance. The development of advanced technologies and reusable launch systems is driving innovation in this segment, with companies focusing on improving performance, reducing costs, and increasing reliability for heavy payload launches.

Satellite Launch Vehicle Market Geography Segment Analysis

Satellite Launch Vehicle Market in Asia-Pacific

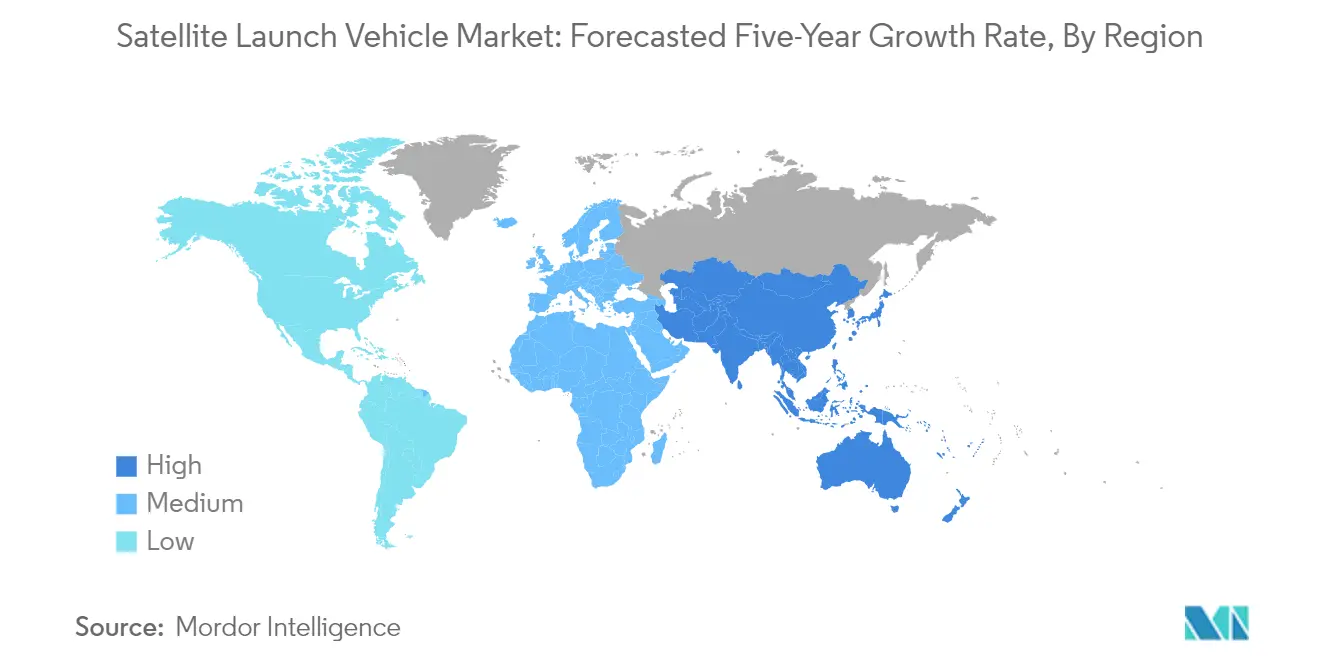

The Asia-Pacific region has emerged as a significant player in the satellite launch vehicle market, with countries like China, India, and New Zealand making substantial contributions. The region's growth is driven by increasing investments in space technology, the development of indigenous launch capabilities, and rising demand for satellite-based services. China has established itself as a dominant space power with ambitious moon missions, while India continues to advance its space program through ISRO's developments. New Zealand has positioned itself as an emerging player, particularly in the small satellite launch segment.

Satellite Launch Vehicle Market in India

India has established itself as the largest market in the Asia-Pacific region, with a market share of approximately 41% in 2024. The country's space agency, ISRO, has been actively developing and operating satellite launchers to cater to growing domestic and international demand. India's launch vehicle portfolio includes PSLV, GSLV Mk-II, and GSLV Mk-III, enabling the country to offer a wide range of launch capabilities. The nation has successfully positioned itself as a reliable and cost-effective launch service provider, attracting customers from various countries, including the UK, US, and Germany.

Satellite Launch Vehicle Market Growth in India

India is also leading the region's growth trajectory with a projected growth rate of approximately 28% during 2024-2029. The country's growth is driven by continuous technological advancements and the expansion of launch vehicle capabilities. ISRO is developing new vehicles like HRLV, SSLV, and RLV-TD for future missions, while NewSpace India Limited, the commercial arm of ISRO, is fostering collaboration with the private sector to enhance manufacturing capabilities. The country's focus on developing cost-effective launch solutions and expanding its launch vehicle portfolio continues to attract international customers, solidifying its position in the satellite launch vehicle market.

Satellite Launch Vehicle Market in Europe

The European satellite launch vehicle market represents a crucial segment of the global space industry, with Russia being a key player in the region. The launch equipment industry stands as the second-largest space manufacturing activity in Europe, following the development of commercial satellites. European launch vehicles have demonstrated significant capabilities in meeting both government requirements and commercial market demands, contributing to the region's socioeconomic benefits and space access capabilities.

Satellite Launch Vehicle Market in Russia

Russia maintains its position as the dominant force in the European market, holding approximately 17% market share in 2024. The country has committed substantial resources to its space programs and has successfully developed various launch vehicles, including the Proton space rocket. The Proton-M/Briz-M rocket, featuring a sophisticated six-first-stage RD-276 engine setup, demonstrates Russia's advanced technological capabilities in the satellite launch market. The country's space program encompasses both civilian and military applications, with significant investments in anti-access/area-denial capabilities and communication systems.

Satellite Launch Vehicle Market Growth in Russia

Russia is leading the European region's growth with an expected growth rate of approximately 21% during 2024-2029. The country's growth is supported by its continued focus on developing advanced launch vehicles and expanding its launch capabilities. Russia's commitment to enhancing its space infrastructure and developing new technologies for both civilian and military applications is driving this growth. The country's strategic approach to space activities and its emphasis on maintaining technological sovereignty contribute to its market expansion within the launch vehicle industry.

Satellite Launch Vehicle Market in North America

North America stands as a pioneer in space exploration, with the United States leading the region's activities. The SLV market is characterized by strong demand for low-cost launch systems capable of deploying heavy satellites into high-altitude orbits. The region has witnessed significant private sector participation, with companies like SpaceX and Blue Origin driving innovation in the industry. Space organizations such as NASA have established strategic partnerships with private players for satellite production and launches, fostering a collaborative ecosystem that enhances the region's capabilities in the space sector.

Satellite Launch Vehicle Market in Rest of World

The Rest of World region encompasses diverse markets, including Iran and other emerging space-faring nations. This region has shown increasing interest in developing indigenous space capabilities, with various countries investing in space launch services technology. Iran has emerged as both the largest and fastest-growing market in this region, focusing primarily on military applications and reconnaissance capabilities. The country's space agency is actively involved in designing and manufacturing research satellites while also establishing partnerships with other nations to further develop its space program. The region's growth is driven by increasing awareness of space technology's strategic importance and the desire to establish independent space access capabilities.

Competitive Landscape

Top Companies in Satellite Launch Vehicle Market

The satellite launch vehicle market is characterized by continuous innovation in reusable launch vehicle technology, advanced propulsion systems, and payload capacity optimization. Companies are focusing on developing cost-effective launch services through vertical integration of manufacturing processes and the implementation of cutting-edge technologies like autonomous flight control systems. Strategic partnerships with government space agencies, commercial satellite operators, and defense organizations have become crucial for securing long-term launch contracts. Operational agility is demonstrated through rapid launch turnaround times, flexible mission planning capabilities, and adaptable launch vehicle configurations to accommodate varying payload requirements. Market players are expanding their global footprint by establishing launch facilities in strategic locations, investing in ground infrastructure, and developing comprehensive launch service portfolios that include end-to-end mission support.

Market Dominated by Government-Backed Space Organizations

The satellite launch vehicle market exhibits a moderately consolidated structure with a mix of state-owned enterprises and private commercial launch providers. Traditional government-backed space organizations maintain significant market presence through established launch programs and extensive technological expertise, while private companies are increasingly gaining market share through innovative business models and cost-competitive solutions. The market is characterized by high entry barriers due to substantial capital requirements, complex technological capabilities, and stringent regulatory compliance needs.

The industry has witnessed strategic consolidations through joint ventures and partnerships, particularly between established aerospace companies and emerging space technology firms. These collaborations aim to combine traditional aerospace expertise with new-age innovation in launch system development. Regional markets are typically dominated by national space agencies and their commercial arms, which benefit from government support and established infrastructure. The competitive dynamics are evolving with the entry of private players who are challenging traditional cost structures and operational paradigms through disruptive technologies and business approaches.

Innovation and Cost Efficiency Drive Future Success

Success in the satellite launch vehicle market increasingly depends on developing cost-effective, reliable launch services while maintaining high safety standards. Incumbent players must focus on modernizing their launch vehicle fleet, improving operational efficiency through automation and advanced manufacturing techniques, and expanding their service offerings to include specialized launch solutions for different satellite categories. Building strong relationships with satellite manufacturers and operators, while maintaining flexibility in launch scheduling and payload integration, will be crucial for maintaining market position.

New entrants and challenger companies can gain market share by focusing on specific market segments, such as small satellite launches or specialized orbit deployments. Developing innovative launch technologies that reduce costs and improve reliability will be essential for competing with established players. Success will also depend on navigating complex regulatory environments across different jurisdictions, building robust safety track records, and establishing efficient supply chain networks. Companies must also consider environmental sustainability in their operations, as regulatory focus on space debris and environmental impact continues to increase.

Satellite Launch Vehicle Industry Leaders

Ariane Group

China Aerospace Science and Technology Corporation (CASC)

ROSCOSMOS

Space Exploration Technologies Corp.

United Launch Alliance, LLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: ISRO launched 36 communication satellites of Oneweb aboarding its LVM3 rocket into LEO.

- August 2022: United Launch Alliance's Atlas V rocket carried SBIRS GEO-6, built by Lockheed Martin for the US Air Force, was launched from the Cape Canaveral Space Force Station.

- April 2022: Northrop Grumman Corporation completed the expansion of the satellite manufacturing plant at its campus in Gilbert, Arizona. The expansion adds 120,000 square feet to the existing 135,000 square foot facility, nearly doubling the site's production capacity to accommodate the company's growing satellite backlog.

Global Satellite Launch Vehicle Market Report Scope

GEO, LEO, MEO are covered as segments by Orbit Class. Heavy, Light, Medium are covered as segments by Launch Vehicle Mtow. Asia-Pacific, Europe, North America are covered as segments by Region.| GEO |

| LEO |

| MEO |

| Heavy |

| Light |

| Medium |

| Asia-Pacific | By Country | China |

| India | ||

| New Zealand | ||

| Europe | By Country | Russia |

| North America | By Country | United States |

| Rest of World | By Country | Iran |

| Rest of World |

| Orbit Class | GEO | ||

| LEO | |||

| MEO | |||

| Launch Vehicle Mtow | Heavy | ||

| Light | |||

| Medium | |||

| Region | Asia-Pacific | By Country | China |

| India | |||

| New Zealand | |||

| Europe | By Country | Russia | |

| North America | By Country | United States | |

| Rest of World | By Country | Iran | |

| Rest of World | |||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.