Aerostat Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

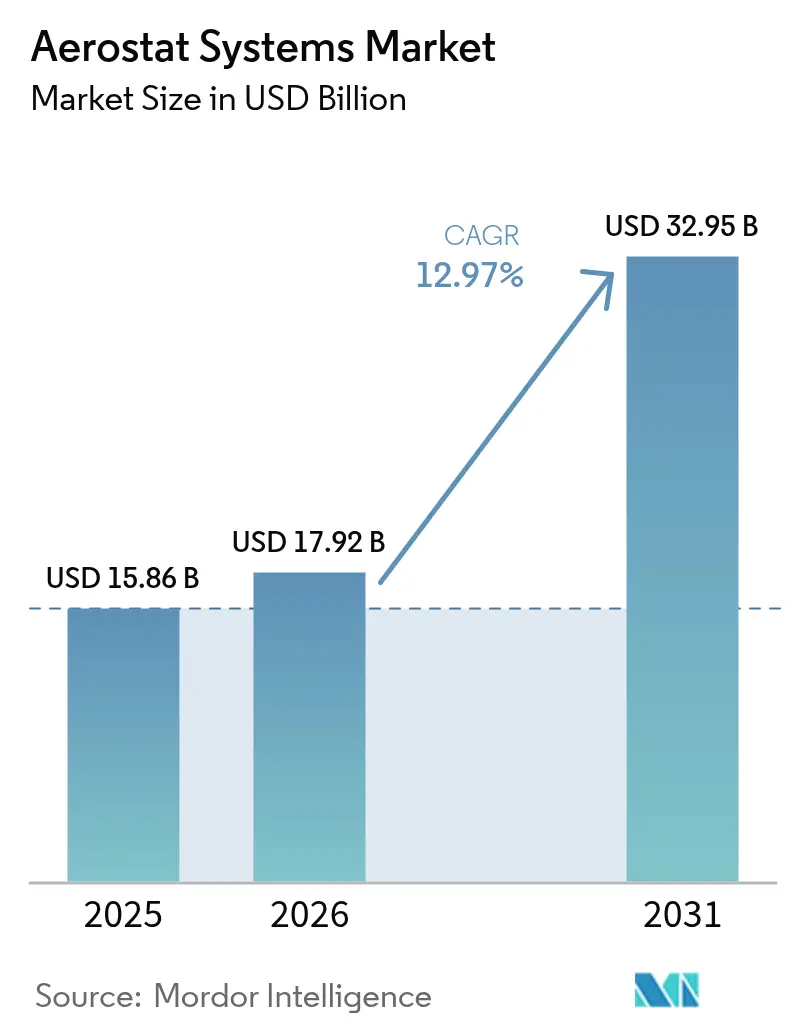

| Market Size (2026) | USD 17.92 Billion |

| Market Size (2031) | USD 32.95 Billion |

| Growth Rate (2026 - 2031) | 12.97% CAGR |

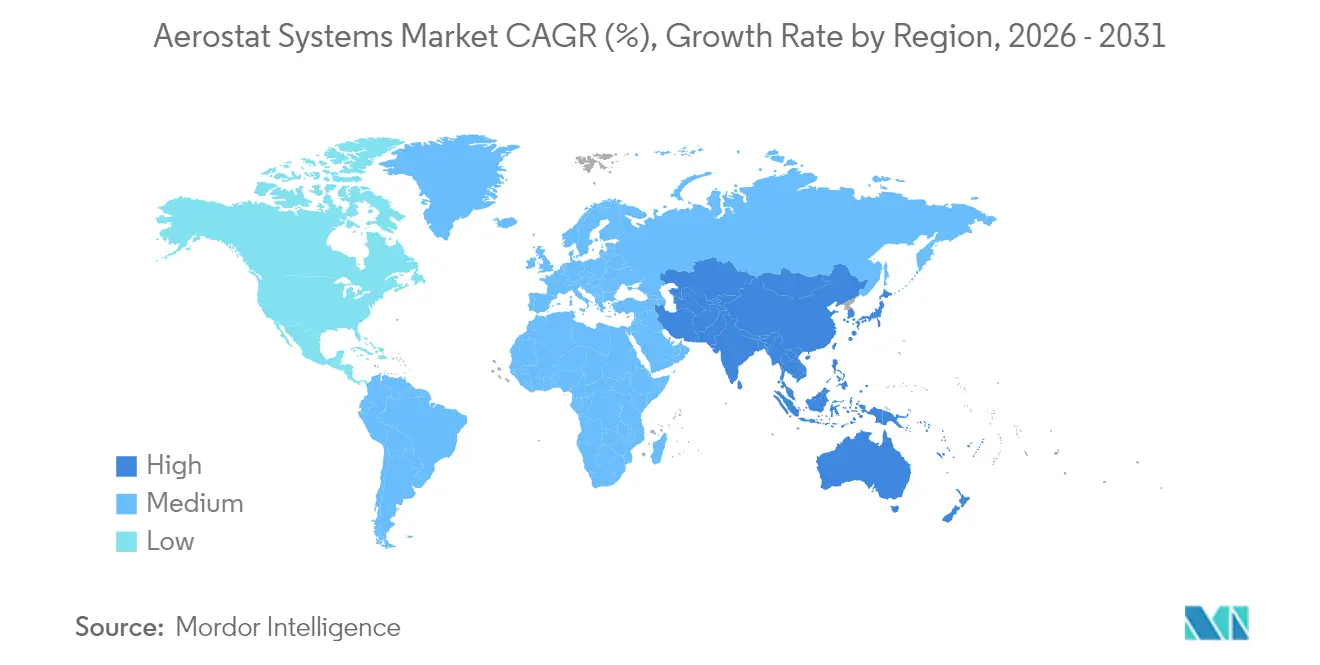

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerostat Systems Market Analysis by Mordor Intelligence

The aerostat systems market size is expected to grow from USD 15.86 billion in 2025 to USD 17.92 billion in 2026 and is forecast to reach USD 32.95 billion by 2031 at 12.97% CAGR over 2026-2031. Growing reliance on tethered platforms for persistent surveillance, border security, and temporary communications infrastructure has been the principal growth catalyst. Government procurement programs—such as the USD 170 million Tethered Aerostat Radar System (TARS) award covering eight southern-border sites—validated the technology’s value proposition and demonstrated budgetary commitment to long-endurance airborne sensors.[1]Source: QinetiQ Group plc, “QinetiQ Secures USD 170 Million TARS Border Surveillance Contract,” qinetiq.com Traditional balloon designs continued to dominate because they deliver 30-day endurance without fuel burn, while hybrid and powered variants gained traction by offering heavier payloads and limited station-keeping control. Helium-filled aerostats also found expanding roles in disaster-relief telecom backhaul and rural 5G pilots, drawing in commercial stakeholders seeking low-cost, quickly deployable coverage options. Even so, operators must budget for rising helium input prices, develop robust weather-risk procedures, and navigate evolving air-traffic regulations that govern tethered flights.

Key Report Takeaways

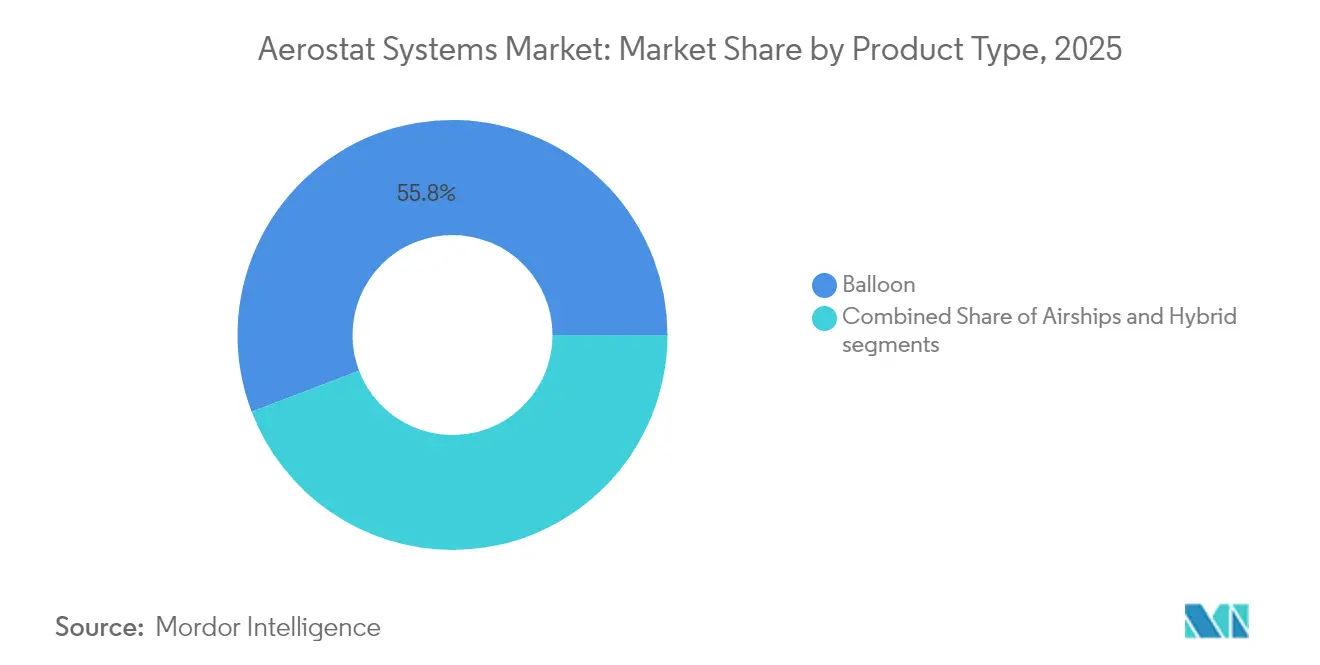

- By product type, balloon aerostats led with 55.80% revenue share in 2025; hybrid platforms are projected to grow at an 17.72% CAGR through 2031.

- By application, military ISR captured 48.10% of the aerostat systems market share in 2025, while telecom-relay activities are forecasted to expand at 15.98% CAGR to 2031.

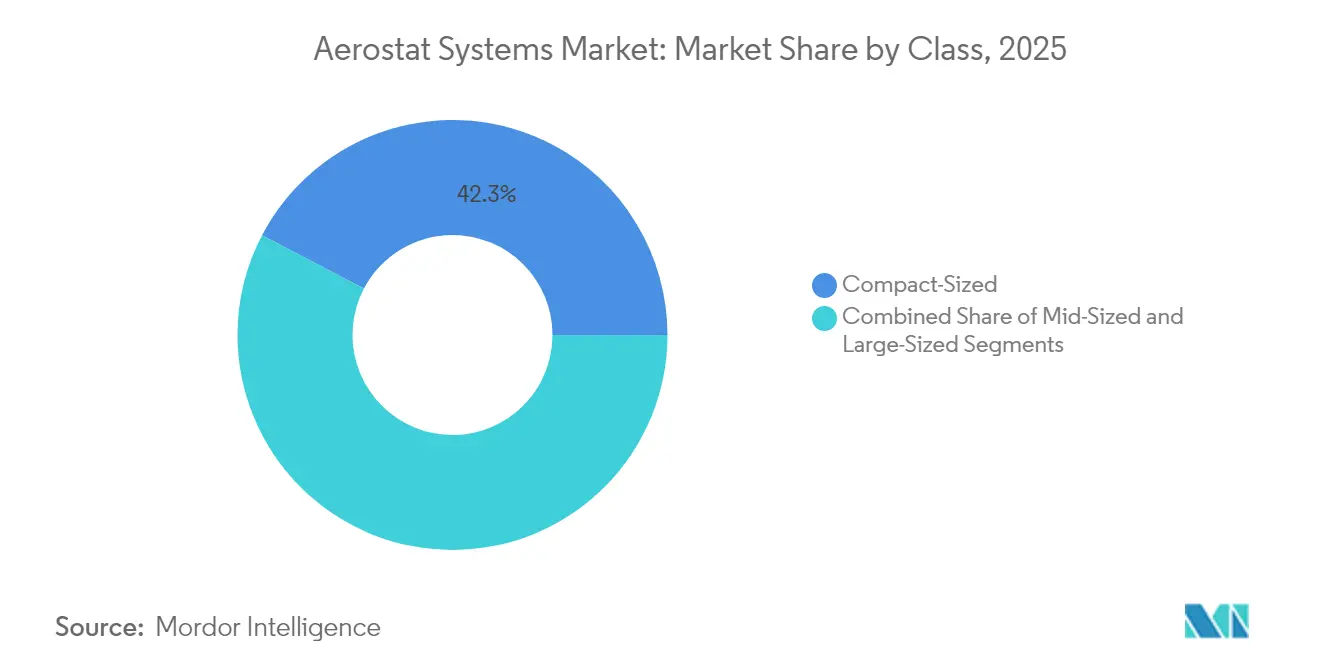

- By class, compact aerostats held a 42.32% share of the aerostat systems market in 2025; large platforms will advance at a 15.05% CAGR between 2026 and 2031.

- By end user, the defense sector had a 68.40% share in 2025; civil and commercial uptake will accelerate at a 14.92% CAGR to 2031.

- By propulsion system, unpowered lift accounted for 64.90% share of the aerostat systems market in 2025; powered aerostats will advance at a 17.12% CAGR between 2026 and 2031.

- By geography, North America accounted for 44.70% of 2025 revenue; Asia-Pacific is poised for the fastest 14.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerostat Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent demand for border-ISR platforms | +2.8% | North America and Europe, spill-over to MEA | Medium term (2-4 years) |

| Lower lifecycle costs than satellites and UAVs | +2.1% | Global | Long term (≥ 4 years) |

| Rising defense modernization budgets in Asia and MEA | +1.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expanding telecom-relay use-cases for rural 5G | +1.7% | Global, with early gains in remote regions | Short term (≤ 2 years) |

| Development of stratospheric pseudo-satellite aerostats | +1.4% | North America and EU | Long term (≥ 4 years) |

| ESG-driven environmental monitoring mandates | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Demand for Border-ISR Platforms

Southern-border surveillance contracts awarded to QinetiQ in 2025 cemented aerostats as indispensable for continuous wide-area radar and EO/IR coverage. Elevated to altitudes near 15,000 ft, tethered balloons monitored low-altitude incursions and relayed situational data to command nodes for 30 days without a crewed sortie. Israel’s Sky Dew program, built with Israel Aerospace Industries hardware and TCOM envelope expertise, provided another benchmark, enabling early warning against small UAVs and cruise missiles.[2]Source: TCOM LP, “Airspace & Surface Radar Reconnaissance (ASRR) Systems Overview,” tcomlp.com Increasing cross-border trafficking and unmanned air threats, therefore, sustained procurement pipelines as agencies sought persistent but budget-friendly sensing layers.

Lower Lifecycle Costs Than Satellites and UAVs

A single balloon aerostat operating a month between maintenance cycles delivered radar dwell times that no satellite or multirotor UAV could match at a comparable total cost of ownership. Operators avoided fuel, aircrew, and frequent overhaul expenses because tethered lift required only helium top-offs and small ground crews. QinetiQ’s TARS fleet documented predictable cost profiles that simplified multi-year budgeting. Rapid roll-out from trailers or modest pads minimized infrastructure outlays, making aerostats attractive for temporary events, emergency missions, or exploratory telecom coverage without tower builds.

Rising Defense Modernization Budgets in Asia and MEA

Defense ministries across East, South, and West Asia earmarked larger percentages of modernization funds for persistent ISR assets capable of policing vast land and maritime frontiers. Domestic integrators partnered with platform specialists to deliver country-specific variants suited to monsoon wind patterns, hot-high conditions, and maritime humidity. Hybrid configurations offering heavier radar loads and encrypted C2 links emerged as force multipliers inside layered sensing architectures, complementing patrol aircraft rather than replacing them. As joint-force doctrines embraced distributed sensors, tethered aerostats provided an immediate, lower-risk on-ramp to panoramic, multi-domain awareness.

Expanding Telecom-Relay Use-Cases for Rural 5G

Fixed-wing drones provide fleeting coverage; ground towers face right-of-way and cost hurdles. By contrast, a tethered balloon hoisting a small cell or phased-array antenna furnished line-of-sight links across 60–80 km, ideal for sparsely populated terrain. QinetiQ’s platform family shipped with modular telecom bays, letting operators snap in 5G radios or P25 public-safety gateways on demand. Disaster-response agencies also valued raising connectivity within hours after hurricanes or earthquakes. Commercial network operators consequently began pilot programs that could scale once national regulators issued tethered-balloon spectrum approvals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weather-related mission downtime | -1.8% | Global, particularly high-wind regions | Short term (≤ 2 years) |

| Stringent civil air-space regulations | -1.4% | Global, concentrated in developed aviation markets | Medium term (2-4 years) |

| Helium supply volatility and price spikes | -1.1% | Global | Long term (≥ 4 years) |

| Cyber-security vulnerabilities in data links | -0.9% | Global, heightened in contested environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Weather-Related Mission Downtime

Sustained winds above platform limits forced periodic reel-downs that interrupted coverage and raised ground-crew workload. Near-space wind studies showed seasonal velocity peaks that cut effective station time in certain latitudes, pressing operators to adopt stronger tethers, dynamic winches, or powered fins for limited vectoring. Icing and heavy rain added further risk by increasing envelope weight and degrading sensor clarity. Operators, therefore, invested in meteorological forecasting and automated mooring systems to shorten response cycles and protect expensive payloads.

Stringent Civil Air-Space Regulations

Tethered balloons intersect controlled airspace and thus require filings, NOTAMs, and altitude caps. The FAA’s Part 101 and case-by-case waivers govern obstacle lighting, radar reflectors, and vertical limits in the US.[3]Source: Federal Aviation Administration, “Part 101: Subpart D—Moored Balloons, Kites, Amateur Rockets, and Unmanned Free Balloons,” faa.gov Equivalent European frameworks under EASA’s UAS Regulatory Package mandate conspicuity beacons and integration plans with ATM systems. Compliance steps lengthen deployment lead times and may constrain altitude envelopes in densely trafficked corridors, especially near commercial airports. Civil operators planning telecom or event-security roles must maintain liaison teams and document risk mitigations before launch approval.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Balloon Systems Sustain Leadership

Balloon aerostats generated 55.80% of 2025 revenue as operators favored their mature design, straightforward ground gear, and stable lift characteristics. The aerostat systems market size for balloon platforms is projected to climb steadily, while hybrid architectures outpace in percentage growth. Agencies ran QinetiQ’s TARS balloons at 15,000 ft with EO/IR and L-band radar kits, achieving month-long sorties while incurring only helium and crew stipends.

Hybrid models, blending balloon envelopes with aerodynamic fins or semi-rigid frames, will post an 17.72% CAGR to 2031 by accommodating heavier AESA radars and multi-band telecom payloads without sacrificing tether endurance. TCOM’s maritime hybrids showed how detachable sea moorings let naval forces reposition sensors overnight without pier infrastructure. The trajectory suggests hybrid systems will capture incremental mission sets—particularly shipboard overwatch and mobile border caravans—while balloons remain the default for fixed-site, low-maintenance surveillance.

By Application: Military ISR Remains Core

Armed-forces users secured 48.10% of the aerostat systems market share in 2025, thanks to program-of-record spending on long-range airborne radar fences. Border-guard agencies leveraged the same airframes for human-tracking radars and counter-UAS receivers, producing scale economies that broadened sustainment pools. Sensitive missions valued persistent line-of-sight sensors that could not be jammed off-route like small drones or forced ablation like satellites.

Telecom-relay duties will be the fastest 15.98% CAGR niche through 2031. Public-safety departments already treat tethered balloons as pop-up LTE towers when hurricanes disable terrestrial networks. Commercial carriers began proof-of-concept deployments in remote valleys, where a single high-gain antenna under a balloon replaced dozens of microcells. As regulators clear spectrum and simplify operating rules, telecom payloads may become a mainstream revenue line for integrators formerly tied to defense contracts.

By Class: Compact Designs Dominate Tactical Use

Compact aerostats claimed 42.32% of 2025 global billings for the aerostat systems market. Ground teams could trailer these 8-11 m diameter balloons to forward bases and loft them within 90 minutes, making them popular for expeditionary brigades and coastal patrol cutters. Lower helium volumes and simplified mooring reduced lifecycle costs while supporting daylight EO imagery and Ku-band data links.

Demand for large aerostats will accelerate at 15.05% CAGR because integrated ISR architectures increasingly call for multi-sensor suites: wide-area GMTI radar, SIGINT antenna farms, and high-capacity microwave relays. Programs such as Sky Dew validated a heavier-lift approach, where a single unmanned envelope hosts phased-array radars able to cue interceptors hundreds of kilometers out. Operators balancing cost, lift, and deployment tempo continue positioning mid-sized variants as versatile compromises that can swap payload kits with minimal ground-crew retraining.

By End-User Industry: Defense Keeps Highest Adoption

The defense community represented 68.40% of 2025 spending. Long-term service contracts bundled flight operations, maintenance, and mission-analysis support, yielding predictable cash flows for prime contractors. International deals—such as Poland's procurement of Airspace and Surface Radar Reconnaissance balloons—illustrated NATO's interest in fixed-site sensor grids that interface seamlessly with ground air-defense radars.

Commercial operators should see 14.92% CAGR from a small base as energy utilities, port authorities, and smart-city planners test high-altitude monitoring. Environmental agencies deploy sensor pods to track atmospheric pollutants or methane leaks at industrial plants, leveraging persistent altitude to improve vertical sampling accuracy. Insurance underwriters and logistics firms also evaluate aerostats for real-time asset tracking over sparsely served regions.

By Propulsion System: Unpowered Platforms Prevail

Unpowered lift held 64.90% revenue in 2025, providing the lowest cost-per-flight-hour in the aerostat systems market. A winch, tether, and helium envelope form a simple mechanical loop with few failure points, allowing continuous multi-week missions that eclipse powered-airship loiter times. Simplified ground checks further reduce manpower requirements and ease training pipelines.

Powered aerostats, though they have a small volume share today, will climb at a 17.12% CAGR. Bow-mounted electric thrusters or tail rotors give station-keeping authority during gusty periods, cutting unplanned reel-downs and thus improving the duty cycle. Navy trials aboard littoral combat ships proved that small propulsion packs maintain angle-on-target even when apparent wind shifts with vessel heading. Continuing advances in lightweight batteries and hybrid gensets will make powered tethers viable for locations where wind roses previously ruled out balloons.

Geography Analysis

North America accounted for 44.70% of global revenue in 2025 as integrated border-security concepts promoted multi-sensor aerostat corridors from the Gulf of Mexico to the Pacific. QinetiQ’s USD 170 million renewal for TARS coverage underscored the US Government’s long-term sustainment posture. Canada adopted complementary tethered balloons for Arctic domain awareness, while Mexico weighed surveillance corridors over remote desert routes, extending value chains for ground stations, tethers, and helium logistics.

Asia-Pacific will post the steepest 14.01% CAGR through 2031. Maritime flashpoints and sprawling Exclusive Economic Zones require enduring radar pickets that do not overextend scarce patrol aircraft inventories. Local integrators in Japan, India, and Indonesia partnered with envelope specialists to localize manufacturing, mitigate import duties, and satisfy sovereign data directives. Hybrid balloons that withstand monsoon wind cycles and salt-laden air have found traction with coast guards and offshore energy operators intent on increasing awareness of the maritime domain.

Europe remained an influential buyer thanks to border-management pressures and NATO readiness mandates. Poland’s Airspace and Surface Radar Reconnaissance purchase illustrated Eastern-flank priorities for low-altitude cruise-missile defense. Western European states leveraged aerostats around major airports to host multilateration sensors that improve drone intrusion detection while freeing manned helicopters for other duties. Funding consortia under the European Defence Fund earmarked feasibility studies on high-altitude pseudo-satellite hijinks—projects likely to integrate tether innovations to limit launch-risk profiles.

Regulatory Landscape

Aerostat operations sit at the intersection of civil aviation rules and defense airworthiness expectations. In the United States, tethered balloon operations are governed by the FAA under 14 CFR Part 101, including requirements linked to size thresholds, operating limitations, and night lighting. Platform developers can also pursue airworthiness through standard pathways or Special Airworthiness Certificates under 14 CFR Part 21 Subpart H for experimental or non-standard configurations. For civil deployments such as telecom-relay and event-security missions, these steps can extend lead times because they require airspace coordination artifacts, including filings and NOTAMs, in controlled corridors.

In Europe, EASA provides certification specifications relevant to tethered gas balloons, such as CS-31TGB, and expects safety analyses for tether systems, including FMEA, along with integration planning with air traffic management. For military use, interoperability and airworthiness alignment are also shaped by common standards such as NATO STANAG 4671, which many nations use as a baseline for cross-border integration and acceptance within allied operating environments. This shapes how primes document safety cases and qualify systems for multinational procurement.

Value Chain Analysis

The aerostat systems value chain begins with upstream inputs such as helium and specialty materials, including coated composite fabrics for envelopes and high-strength fibers for tethers, along with components for winches and mooring systems. It then moves into platform fabrication and subsystem integration, covering the envelope, tether and ground-control segment, power options, and mission payloads. Payload providers, including radar, EO/IR, SIGINT, and communications relays, along with secure datalink suppliers, feed the midstream, while certification and airspace-approval work, using FAA/EASA routes for civil use and military airworthiness baselines, drives test, qualification, and documentation cycles before fielding.

On the downstream side, defense primes and integrators bundle aerostats into persistent surveillance architectures that include operations, maintenance, training, spares, and mission support, often under multi-year contracting vehicles. The April 2025 US Army Product Director Aerostats award, a 10-year, USD 4.19 billion IDIQ to multiple partners, illustrates how demand concentrates around long-term life-cycle support and refresh in addition to initial platform delivery. Supply-side pinch points also remain tied to helium price volatility and availability, as well as specialized engineering capacity for tether reliability, automation, and safety systems that reduce weather-related reel-downs and improve duty cycle.

Competitive Landscape

The aerostat systems market exhibited moderate concentration. Two incumbent primes—QinetiQ and TCOM—carried forward installed bases exceeding 20 persistent sites worldwide, giving them economies in helium procurement, training curricula, and spare-parts pooling. Eight TARS locations along the US southern border delivered recurring O&M fees under a performance-based logistics charter.

Competitive differentiation centered on payload modularity, automated reel-down safety systems, and global support footprints. QinetiQ’s open-architecture gondola lets agencies swap EO/IR balls, surface-search radars, or telecom repeaters without re-balancing the envelope, shortening reconfiguration windows to under four hours. TCOM answered with rapid-deflation valves and smart-winch algorithms that could dock a 30-m-diameter envelope within 12 minutes when gusts topped spec, enhancing fleet availability for navies operating in monsoon belts.

Emerging challengers pursued lighter composite envelopes, hydrogen-compatible gas cells, and AI-assisted sensor fusion that flags anomalies automatically. Strategic mergers mirrored wider defense-sector consolidation trends, such as Rheinmetall’s 2024 acquisition of Loc Performance to secure vehicle-borne mooring hardware capabilities. Suppliers of helium recycling skids and advanced fiber tethers forged alliances with primes to hedge against commodity volatility and extend integrated-solution portfolios.

Aerostat Systems Industry Leaders

TCOM, LP,

Israel Aerospace Industries Ltd.

Aerostar LLC

Lockheed Martin Corporation

RT LTA Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procurement vehicles that emphasize fleet modernization, sustainment, and rapid technology insertion create whitespace for suppliers that can shorten integration timelines for new payloads and counter-UAS capabilities. The US Army Product Director Aerostats IDIQ awarded in April 2025, totaling USD 4.19 billion across multiple vendors, signals demand for integration, fielding, and life-cycle support at scale, which favors vendors offering modular gondolas, secure communications, and automated launch-and-recovery systems that reduce personnel burden. In parallel, fixed-site early warning and low-altitude threat detection highlighted by large radar-fence programs, such as Poland's Barbara aerostat radar acquisition under a Foreign Military Sales framework, points to demand where terrain and curvature limit ground radar coverage.

A second opportunity area is higher-altitude lighter-than-air development that complements tethered systems with longer-duration communications and ISR coverage. India has publicized indigenous workstreams, including DRDO test activity at roughly 17 km altitude and an airship-based high-altitude pseudo-satellite (AS-HAPS) program under the Ministry of Defence (DAC) Make-I category, which supports demand for subsystems such as high-reliability envelopes, communications backhaul, and network integration. On the commercial and dual-use side, tethered platforms continue to fit rural connectivity and disaster-response communications use-cases, but scaling depends on operating approvals in controlled airspace and clear spectrum authorization pathways for balloon-hosted telecom payloads.

Recent Industry Developments

- July 2026: IIT Delhi and DRDO demonstrated an indigenous tactical aerostat concept aimed at carrying surveillance and communications payloads at altitudes up to 20 km. The activity reinforces domestic development momentum in India around lighter-than-air ISR and relay concepts, broadening the potential supplier base for subsystems, payload integration, and ground-segment tooling.

- October 2025: The US Department of Defense awarded TCOM a USD 624.9 million contract for airspace and surface radar reconnaissance aerostat systems and associated product support, with performance running through September 2030. The award supports the long-duration radar fence use-case and continues platform standardization and sustainment capacity across multi-year delivery schedules.

- May 2024: Poland's Ministry of National Defence signed a USD 1 billion agreement with the United States to acquire four aerostat-based early warning radar systems. This program expands European demand for persistent, low-altitude surveillance layers and drives follow-on needs for site infrastructure, training, and long-term maintenance support.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers aerostat systems that use lighter-than-air platforms for persistent observation or communications, including the platform and the key supporting equipment needed to operate it. We treat the market in value terms for systems delivered for defense, security, and selected civil missions.

Scope exclusions: We exclude tourist hot-air balloons, one-off advertising blimps, and experimental pseudo-satellite style vehicles that sit outside typical aerostat procurement and operating profiles.

Segmentation Overview

- By Product Type

- Balloon

- Airships

- Hybrid

- By Application

- Military ISR

- Border and Coastal Surveillance

- Telecom and Broadband Relay

- Environmental and Weather Monitoring

- Disaster Management and Public Safety

- Scientific Research and Academic

- By Class

- Compact-Sized

- Mid-Sized

- Large-Sized

- By End-User Industry

- Commercial

- Military

- By Propulsion System

- Powered

- Unpowered

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Israel

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model to visible defense and civil demand signals, and to keep country assumptions consistent across the time series. We referenced public sources such as national defense budget documents, government procurement portals and contract notices, oversight or audit publications, and regulator material from civil aviation and spectrum bodies.

To translate those signals into market inputs, we also reviewed company annual reports and investor presentations, product brochures, reputed press coverage, and technical papers in peer-reviewed journals that describe endurance, payload types, and operating constraints. A paid subscription focused on company financials, and another focused on patent activity, were used selectively to confirm exposure and technology direction. These desk sources are illustrative only, and many other references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on expert interviews and structured surveys with defense and homeland security stakeholders, system integrators, payload specialists, and operators involved in deployment and sustainment. Inputs were used to confirm what typically gets counted as a system sale, how upgrade cycles behave in practice, and which demand triggers (border surveillance needs, temporary telecom relay, and ISR persistence requirements) matter most across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 18% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 36% | EMEA: 33% |

| Smaller Players: 18% | Managers: 46% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using both top-down and bottom-up logic, so the totals stay realistic even when a single data series is incomplete. On the top-down side, defense and security spending patterns, program-level procurement signals, and the installed base need for persistent surveillance were used to reconstruct an addressable demand pool and then convert it into annual system value.

Those results were then checked with selective bottom-up approximations, such as sampling typical unit pricing for major aerostat classes, applying payload mix assumptions (ISR sensors vs communications relay), and validating the implied delivery volumes through channel checks. When gaps appeared, conservative substitution rules were applied, for example by carrying forward the last confirmed delivery cadence and adjusting only for known program shifts.

For forecasting, scenario analysis was used because this market is sensitive to contract timing and changes in security posture. Key inputs included border and coastal surveillance investments, upgrade and replacement cycles, operating altitude and endurance requirements that influence system selection, and the share of demand coming from temporary communications coverage during emergencies.

Data Validation & Update Cycle

Outputs were validated through triangulation across procurement signals, supplier discussions, and regional spending patterns, followed by variance checks against prior-year trajectories and known contract values. Where a country result looked out of range, assumptions were re-tested, and respondents were re-contacted if the gap could not be explained by a clear policy or procurement change.

Before sign-off, the model goes through multi-step analyst review so the logic, units, and currency handling are consistent across regions and years. Reports refresh annually, with interim updates for material events such as major awards or cancellations that can shift deliveries between years. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Aerostat Systems Market Sizing Compared With Other Published Estimates

Published market sizes for aerostat systems often do not match, even when the same segment names are used. The differences usually come from what each publisher counts inside a system, how it treats payload and ground equipment value, and how it handles contract timing and currency conversion.

Contract award values, observed procurement timing, and operator feedback on upgrade cycles are used as checks to keep Mordor Intelligence's estimate tied to delivered aerostat systems with their associated ground control and mission payloads, instead of mixing in adjacent lighter-than-air activity like tourist balloons or one-off advertising blimps.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.86 B (2025) | |

| Industry Publisher A | USD 18.32 B (2025) | Often builds a wider bill of materials that expands what is treated as a full system, especially around payload and ground support content, which lifts the average value per deployment. |

| Industry Publisher B | USD 13.01 B (2024) | Uses factory-gate framing and different recognition timing, and totals can be lower if integrator-led missionization and delivery-year shifts are not fully captured. |

The spread in the table is mainly explained by what gets counted within a system sale and by timing choices that can move revenue between years. By keeping inputs traceable to procurement signals and field validation, the resulting market value stays repeatable for planning and easy to audit back to the drivers.

Key Questions Answered in the Report

What is the current value of the aerostat systems market?

The aerostat systems market size stood at USD 17.92 billion in 2026 and is on track to reach USD 32.95 billion by 2031, witnessing a 12.97% CAGR.

Which application segment is growing the fastest?

Telecom-relay operations are projected to register the highest 15.98% CAGR as operators deploy tethered balloons for rural 5G backhaul and emergency communications.

Why do defense agencies favor aerostats over UAVs for border surveillance?

Tethered aerostats offer 30-day endurance without fuel costs, enabling constant wide-area coverage at lower lifecycle expense than multirotor or fixed-wing drones.

What are the main restraints on market growth?

Weather-induced downtime and stringent civil-airspace rules require additional investment in forecasting, automation, and regulatory compliance, tempering adoption rates.

Which region will contribute most to new revenue by 2031?

Asia-Pacific is expected to deliver the highest incremental growth, buoyed by territorial surveillance needs and rising defense modernization budgets.

How concentrated is the competitive landscape?

With the top five vendors controlling just around 45-55% of sales, the market shows moderate concentration, leaving opportunities for niche specialists and regional integrators.

Page last updated on: