Managed Domain Name System (DNS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

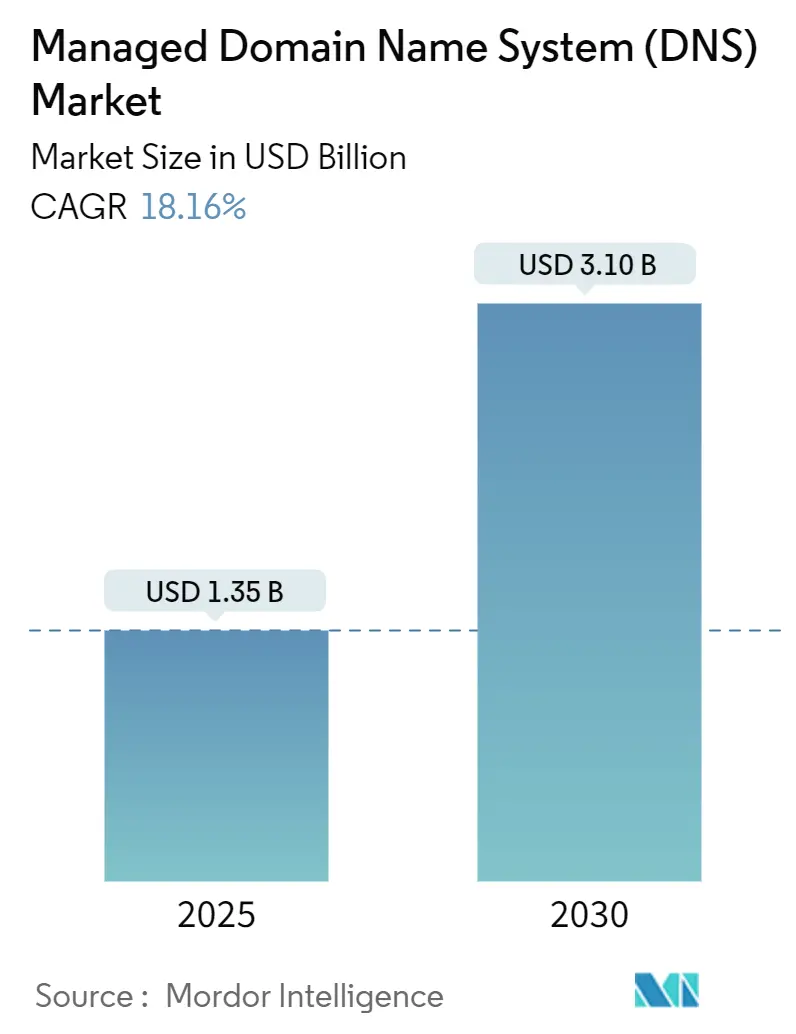

| Market Size (2025) | USD 1.35 Billion |

| Market Size (2030) | USD 3.10 Billion |

| Growth Rate (2025 - 2030) | 18.16% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Domain Name System (DNS) Market Analysis by Mordor Intelligence

The Managed Domain Name System market size reached USD 1.35 billion in 2025 and is expected to climb to USD 3.10 billion by 2030, expanding at an 18.16% CAGR over the forecast period. Rapid cloud migration, edge-computing adoption, the spread of IoT endpoints, and regulatory mandates requiring encrypted DNS collectively sustain double-digit growth. Vendors that once delivered basic authoritative resolution now position DNS as the first line of cyber defense, bundling DDoS mitigation, threat intelligence, and certificate automation into unified service portfolios. Enterprise buyers prefer globally distributed anycast networks with programmable APIs that fit infrastructure-as-code workflows, while small businesses adopt simplified managed offerings that erase on-premises complexity. The Managed Domain Name System market, therefore, serves as both a performance enabler and a security control, underpinning multi-cloud architectures and zero-trust frameworks alike.

Key Report Takeaways

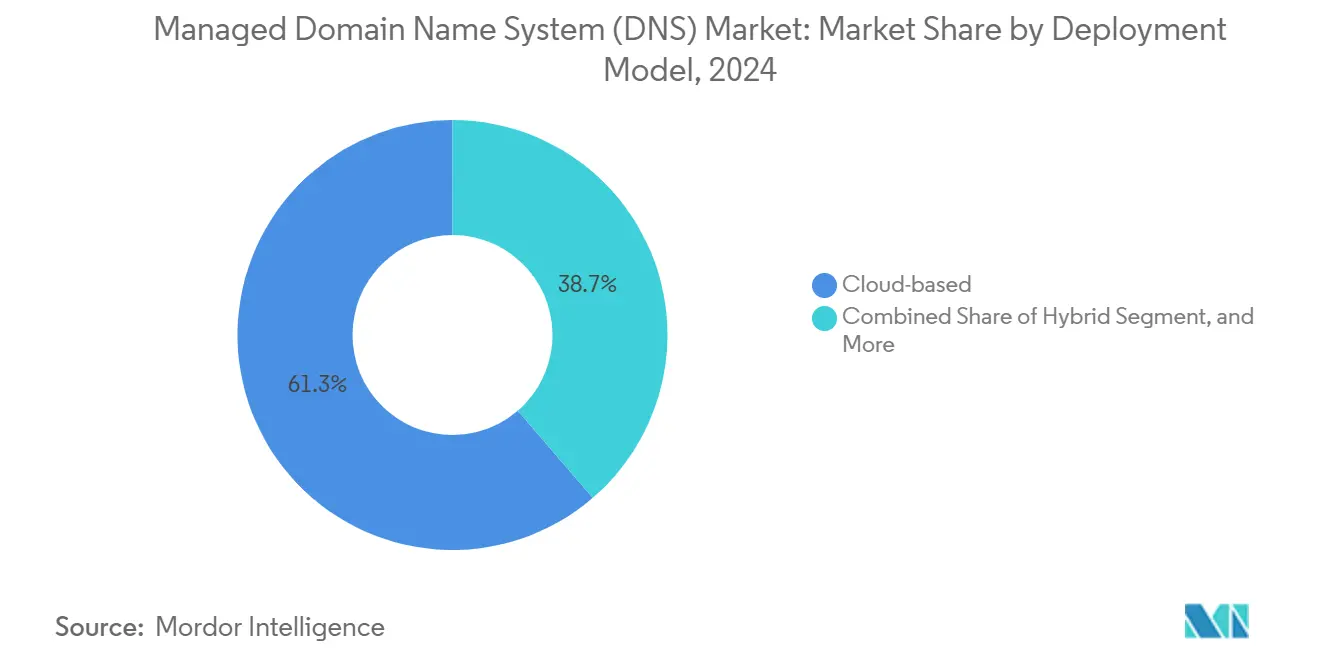

- By deployment model, cloud-based services led with 61.32% revenue share in 2024, whereas hybrid deployments are on track for the fastest 19.83% CAGR through 2030.

- By DNS service type, primary DNS accounted for 43.37% of 2024 revenue, while dynamic DNS is projected to advance at a 19.43% CAGR through 2030.

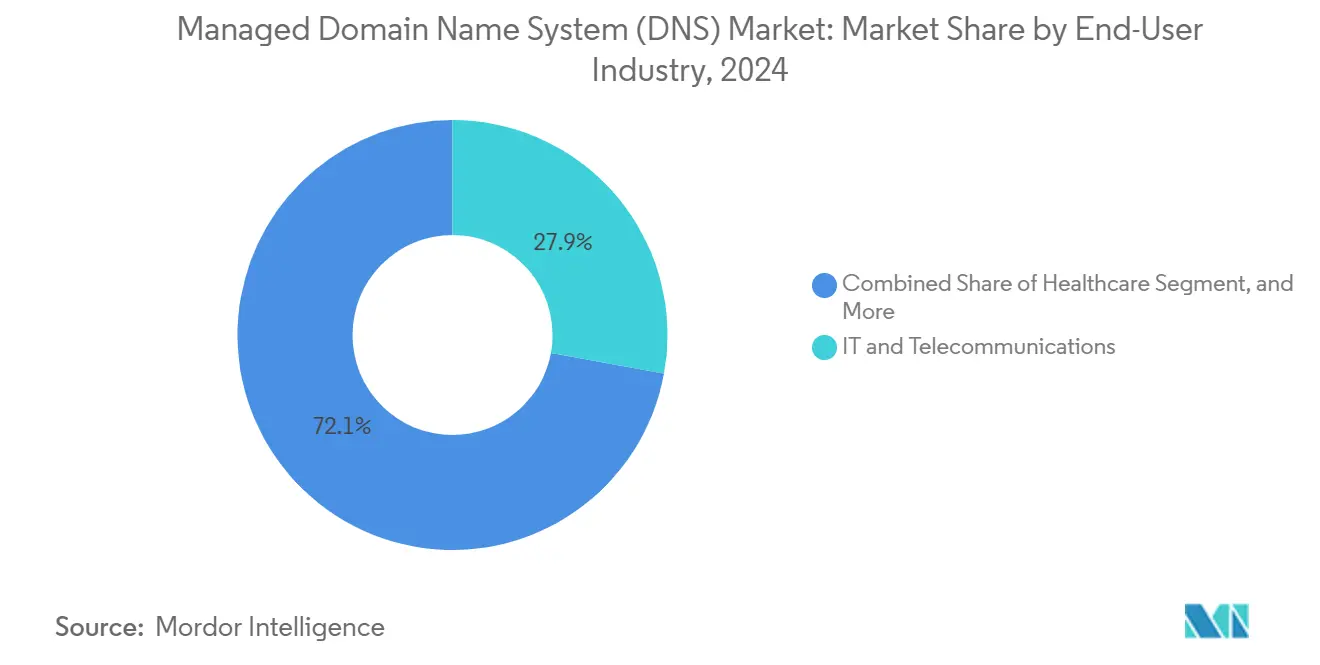

- By end-user industry, IT and telecommunications held 27.87% of 2024 demand, whereas healthcare will post the highest 18.67% CAGR through 2030.

- By organization size, large enterprises controlled 66.83% of 2024 spending, yet small and medium enterprises are poised for a 20.13% CAGR over the forecast horizon.

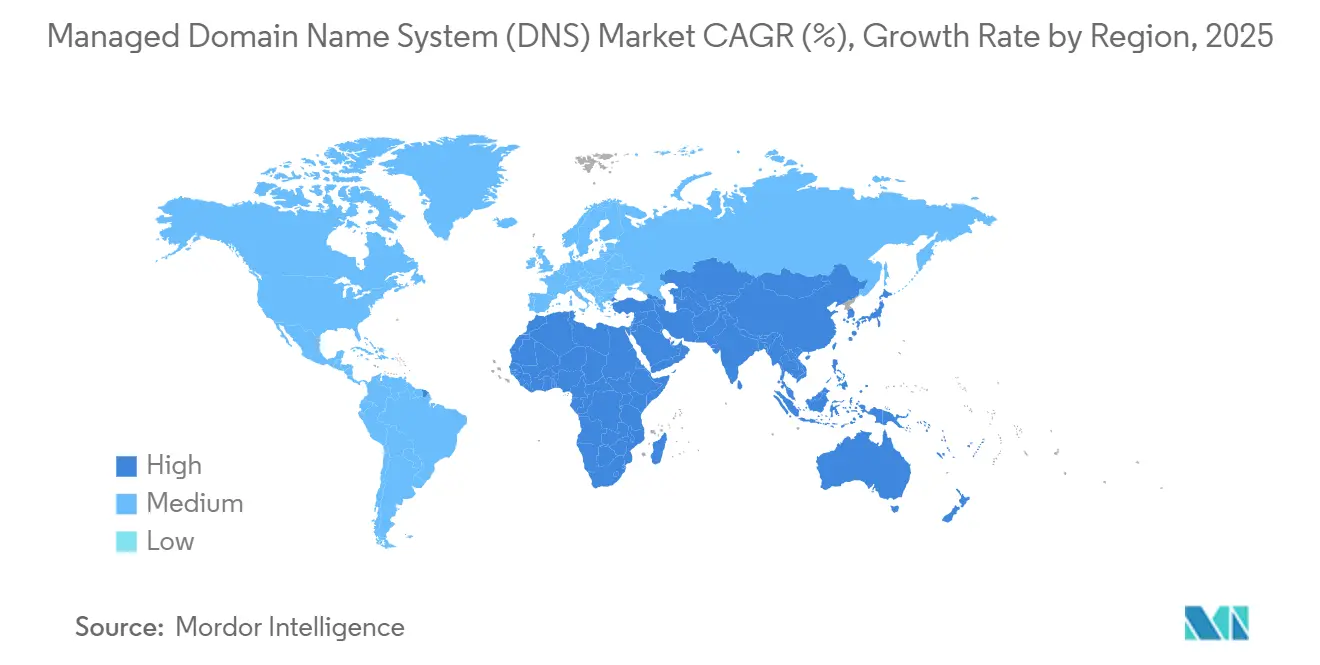

- By geography, North America contributed 39.32% of 2024 revenue, while Asia-Pacific is expected to register an 18.92% CAGR to 2030.

Global Managed Domain Name System (DNS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid proliferation of cloud-native applications | +4.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Increasing cyber-attacks (e.g., DDoS) demanding resilient DNS | +3.8% | Global, particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Growing adoption of CDN and multi-CDN strategies | +2.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of IoT endpoints requiring scalable DNS | +3.1% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| Edge-computing deployments needing ultra-low-latency DNS | +2.7% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Data-residency mandates creating demand for localized DNS nodes | +1.9% | EU, Asia-Pacific, with emerging requirements in MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Cloud-Native Applications

Containerized and serverless architectures multiply DNS query volumes as service discovery events spike during every pod spin-up or function cold-start. Kubernetes clusters often push millions of record updates per day, making manual zone management infeasible. Enterprises, therefore, favor managed services offering RESTful APIs, GitOps-style workflows, and SLA-backed anycast networks that minimize failover latency. Large SaaS providers embed DNS in continuous deployment pipelines to orchestrate blue-green releases without user disruption, reinforcing demand for programmable platforms.[1]Amazon Web Services, “What Are Route 53 Profiles?” aws.amazon.com

Increasing Cyber-Attacks Demanding Resilient DNS

Attackers now weaponize algorithmic complexity exploits like KeyTrap to exhaust resolver CPU cycles, bypassing volumetric rate filters. Financial institutions logged 350 DNS-centric DDoS events in October 2024, prompting protective DNS adoption that blocks malicious domains at query time. Federal agencies deploying CISA’s enterprise DNS shield prevented 1.86 billion outbound connections to known command-and-control hosts in 2025, underscoring DNS as a critical zero-trust enforcement point.[2]Cybersecurity & Infrastructure Security Agency, “Securing Federal Networks: Evolving to an Enterprise Approach,” cisa.gov

Growing Adoption of CDN and Multi-CDN Strategies

Video-on-demand services orchestrate traffic across multiple CDNs using weighted DNS records, achieving seamless viewer hand-offs during traffic bursts. Multi-CDN strategies eliminate single points of failure and optimize cost-to-performance ratios, turning DNS into the control plane for real-time traffic steering. Integration with application recovery controllers automates failover decisions in seconds, outpacing human intervention during outages.[3]Tubi Engineering, “Scaling Tubi for the Super Bowl: Implementing a Multi-CDN Strategy,” tubitv.com

Expansion of IoT Endpoints Requiring Scalable DNS

Manufacturing lines, smart campuses, and connected vehicles flood authoritative servers with telemetry look-ups and firmware update checks. Network protocols such as NB-IoT and 6LoWPAN rely on specialized relays that translate IPv6 or 6-byte addresses into legacy environments, amplifying the need for elastic DNS capacity. Managed providers respond by coupling dynamic DNS with auto-scaling anycast nodes hosted near major IoT rollouts in Asia-Pacific smart-city corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistence of legacy on-premises DNS infrastructure | -2.8% | Global, particularly in traditional enterprises | Medium term (2-4 years) |

| Cost sensitivity among SMEs in emerging markets | -1.9% | Asia-Pacific, MEA, Latin America | Short term (≤ 2 years) |

| IPv6 operational complexity for service providers | -1.4% | Global, with higher impact in Asia-Pacific | Long term (≥ 4 years) |

| Price commoditization in mature regions | -1.1% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistence of Legacy On-Premises DNS Infrastructure

Many organizations still operate self-hosted BIND servers because sunk costs and perceived control outweigh modernization benefits. Complex internal zone hierarchies and limited DNS automation skills deter migration, while downtime fears slow cut-over planning. Nevertheless, rising maintenance costs, staffing shortages, and mandatory encrypted DNS push holders of legacy estates toward phased hybrid adoption.

Cost Sensitivity Among SMEs in Emerging Markets

Small firms in price-conscious economies lean on registrar-bundled DNS even when feature gaps expose them to outage and phishing risk. Subscription models built for enterprise query volumes feel overpriced to businesses resolving tens of thousands of queries per day. Governments offer digitalization grants, yet uptake remains low due to limited cybersecurity awareness. Providers addressing this restraint introduce freemium tiers with usage-based scaling that upgrade seamlessly as traffic grows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Adoption Rises During Cloud Migration

Cloud-based solutions retained 61.32% of 2024 revenue, affirming their role as the backbone of the Managed Domain Name System market. The hybrid approach, however, is projected to exhibit a 19.83% CAGR through 2030, reflecting enterprises that keep sensitive zones on-premises while leveraging cloud points of presence for resilience. The Managed Domain Name System market size for cloud and hybrid combined will widen further as regulatory data-boundary solutions, such as Microsoft’s EU Data Boundary, remove sovereignty objections.

Ongoing integration of DNS with infrastructure-as-code accelerates cloud uptake. Platforms like Terraform codify zone files beside virtual machine manifests, allowing network teams to version-control every record change. On-premises deployments decline as operators struggle to maintain 24 × 7 DDoS scrubbing and redundancy. Consequently, managed vendors bundle seamless migration utilities that transfer millions of records without downtime, smoothing the path for late adopters.

By DNS Service Type: Dynamic DNS Underpins Real-Time Workloads

Authoritative primary DNS represented 43.37% revenue in 2024, anchoring web properties, SaaS endpoints, and enterprise mail gateways. Dynamic DNS, although smaller, is forecast to sprint at a 19.43% CAGR on the back of mobile edge, IoT, and disaster-recovery use cases. In 2024, dynamic services handled 1 trillion IP updates, indicating how real-time applications ignite query bursts that static models cannot address.

Secondary DNS adoption advances as high-profile outages spur redundancy investments, illustrating that the Managed Domain Name System market share commanded by dual-provider strategies is climbing. Meanwhile, reverse DNS and DNS over HTTPS emerge as niche categories for anti-fraud validation and privacy compliance. Providers differentiate by automating DNSSEC signing and offering post-quantum algorithms to future-proof integrity, further expanding the Managed Domain Name System market size attached to premium security tiers.

By End-User Industry: Healthcare Outpaces Traditional Leaders

IT and telecommunications sustained the largest slice at 27.87% in 2024 because carriers, ISPs, and cloud platforms require authoritative DNS for customer-facing and backbone services. Healthcare, although smaller, is set for an 18.67% CAGR through 2030 as telehealth, e-prescription, and connected medical devices necessitate encrypted DNS and HIPAA compliance. The Managed Domain Name System market share held by healthcare expands every year as hospital systems outsource critical infrastructure to security-centric DNS providers.

Banking, financial services, and insurance embrace protective DNS after a surge in Layer 7 DDoS attacks rattled customer trust. Media and entertainment leverages DNS-based traffic steering to guarantee low-latency streaming during international sporting events. Government adoption rises due to executive orders mandating encrypted DNS, confirming that a broad policy push elevates the Managed Domain Name System market across verticals.

By Organization Size: SME Growth Accelerates

Large enterprises controlled 66.83% of 2024 spending, benefiting from complex multi-cloud estates and compliance mandates. Yet SMEs record the swiftest 20.13% CAGR, propelled by cloud-first operating models and user-friendly managed dashboards. Self-service portals let small teams craft failover policies, block malware domains, and deploy DNSSEC without command-line expertise, broadening the Managed Domain Name System market to millions of previously underserved businesses.

For global corporations, integrated digital-trust suites that combine DNS, PKI, and certificate lifecycle automation drive vendor consolidation. DigiCert’s acquisition of Vercara typifies the pivot toward unified platforms that can auto-renew TLS certificates while updating corresponding DNS records in under a second, reducing outage risk and compliance overhead.

Geography Analysis

North America generated 39.32% of 2024 revenue, reflecting early managed DNS adoption across federal, financial, and hyperscale cloud sectors. The United States boosts demand through CISA’s Protective DNS program that filters billions of queries daily, and Canada plus Mexico follow as cross-border data flow rules tighten. Venture investment and a dense network of anycast nodes keep latency below 20 milliseconds for most regional users, solidifying the area’s current leadership.

Asia-Pacific is predicted to post an 18.92% CAGR through 2030, the fastest in the forecast, as digitization mandates, 5G rollouts, and smart-city programs multiply query loads. China’s municipal IoT networks and India’s expanding digital payments ecosystem depend on resilient authoritative services hosted within sovereign borders. Japan, South Korea, and Australia add momentum by demanding ultra-low-latency resolution for edge-AI inferencing, increasing the Managed Domain Name System market size attributable to Asia-Pacific deployments.

Europe grows steadily on the back of GDPR and the NIS 2 directive, which compel critical-infrastructure operators to audit and encrypt DNS traffic. The EU Data Boundary initiative accelerates cloud uptake by satisfying sovereignty concerns, while Germany and the United Kingdom deploy hybrid architectures to balance control with scale. Elsewhere, the Middle East and Africa and South America experience rising adoption tied to telecom modernization, though budget constraints and skills shortages moderate CAGR compared to Asia-Pacific.

Competitive Landscape

Incumbent providers race to bundle value-added security into core resolution services, shifting competition from price per zone to breadth of threat-mitigation features. DigiCert’s integration of Vercara’s UltraDNS plus DDoS scrubbing technologies creates a platform that automates certificate issuance and DNS record alignment, responding directly to enterprise downtime anxieties. Cloudflare processes more than 1 trillion daily queries across 310 cities, leveraging its scale to promote zero-trust network access and AI-driven attack detection as differentiators.

AWS Route 53 retains traction with infrastructure teams seeking tight coupling with EC2, S3, and load-balancing services, while Google Cloud DNS extends control-plane parity across multi-region deployments and sovereign cloud offerings. Smaller challengers such as DNSFilter and Infoblox carve niches by delivering security-first DNS that blocks phishing and malware without network re-architecture, a proposition resonating with mid-market buyers. Patent activity escalates around quantum-safe DNSSEC and machine-learning response heuristics, signaling sustained R&D investment in next-generation protection.

Market consolidation intensifies as buyers prefer single-pane management platforms that span PKI, DNS, and content delivery. Vendors therefore pursue mergers, alliances, and FedRAMP authorizations to penetrate regulated industries. Regional specialists with deep compliance know-how often become acquisition targets for global networks eager to localize points of presence and secure government contracts, reshaping the Managed Domain Name System market toward integrated digital-trust ecosystems.

Managed Domain Name System (DNS) Industry Leaders

Cloudflare, Inc.

Amazon Web Services, Inc.

Google LLC

Akamai Technologies, Inc.

International Business Machines Corporation (NS1)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cloudflare introduced Containers in public beta, delivering edge-deployed container services with built-in DNS routing.

- April 2025: DigiCert achieved record FY 2025 growth by expanding its quantum-ready digital-trust platform.

- March 2025: DigiCert launched DigiCert ONE, converging PKI and DNS to automate certificate renewal and zone updates.

- February 2025: Microsoft completed the EU Data Boundary to enhance regional data residency for DNS and other cloud services.

Global Managed Domain Name System (DNS) Market Report Scope

| Cloud-based |

| On-premises |

| Hybrid |

| Primary DNS |

| Secondary DNS |

| Dynamic DNS |

| Reverse DNS |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Media and Entertainment |

| Retail and E-commerce |

| Healthcare |

| Government and Public Sector |

| Other End-User Industry |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Model | Cloud-based | ||

| On-premises | |||

| Hybrid | |||

| By DNS Service Type | Primary DNS | ||

| Secondary DNS | |||

| Dynamic DNS | |||

| Reverse DNS | |||

| By End-User Industry | IT and Telecommunications | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Media and Entertainment | |||

| Retail and E-commerce | |||

| Healthcare | |||

| Government and Public Sector | |||

| Other End-User Industry | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the Managed Domain Name System (DNS) market?

The Managed Domain Name System (DNS) market is valued at USD 1.35 billion in 2025 and is projected to reach USD 3.10 billion by 2030.

How fast is the market growing?

It is expanding at an 18.16% CAGR over 2025-2030 as enterprises elevate DNS to a frontline security and performance layer.

Which deployment model leads revenue?

Cloud-based DNS holds 61.32% of 2024 revenue due to demand for globally distributed, scalable resolution services.

Which region shows the highest growth?

Asia-Pacific is forecast to post an 18.92% CAGR through 2030, driven by digital-transformation and data-residency mandates.

Why is healthcare adoption accelerating?

Telemedicine growth and HIPAA compliance rules require encrypted, resilient DNS, boosting healthcare’s forecast 18.67% CAGR.

Who are key vendors shaping competition?

Cloudflare, AWS, Google Cloud, DigiCert-Vercara, and DNSFilter lead through global anycast networks and integrated security suites.

Page last updated on: