Domain Name System Tools Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

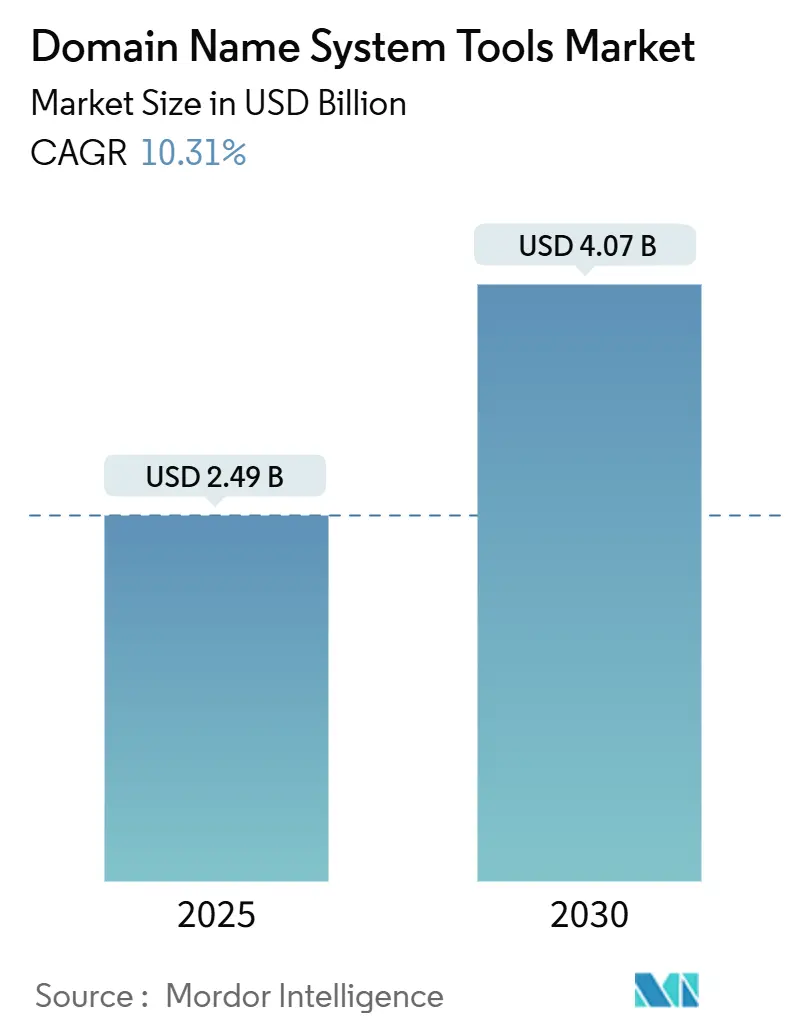

| Market Size (2025) | USD 2.49 Billion |

| Market Size (2030) | USD 4.07 Billion |

| Growth Rate (2025 - 2030) | 10.31% CAGR |

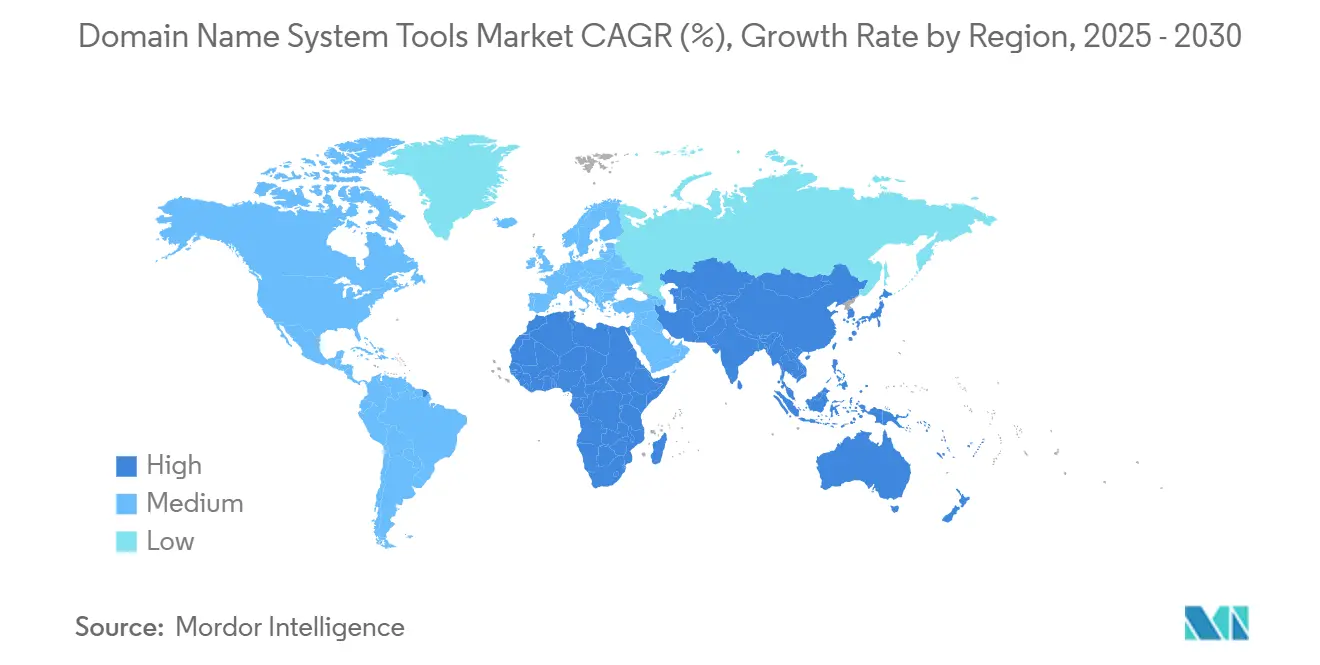

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

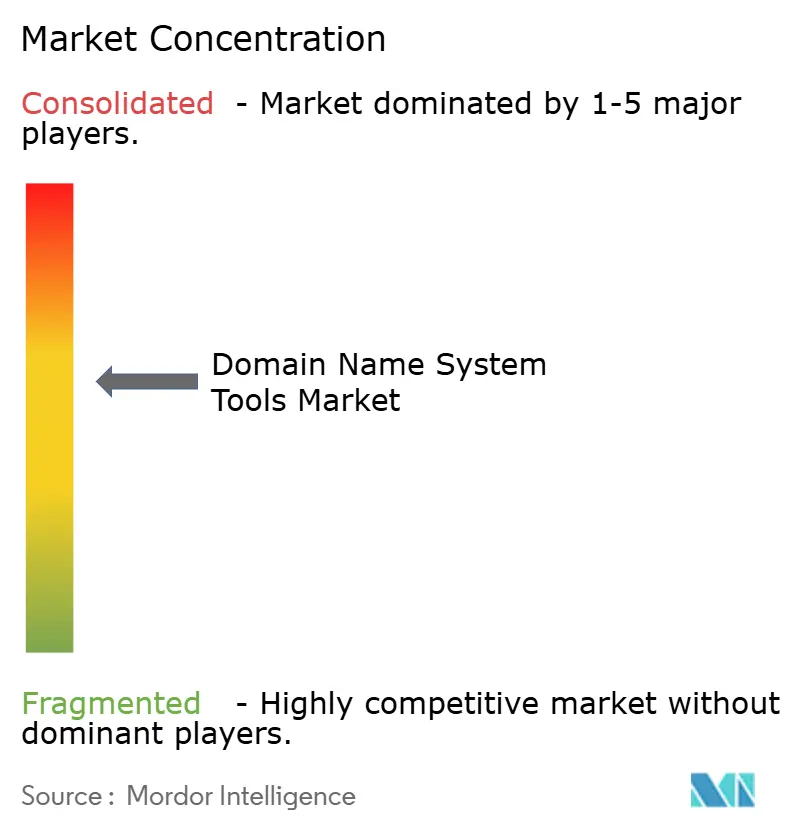

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Domain Name System Tools Market Analysis by Mordor Intelligence

The Domain Name System Tools market size stood at USD 2.49 billion in 2025 and is forecast to reach USD 4.07 billion by 2030, reflecting a 10.31% CAGR over the period. This expansion underscores how vital DNS orchestration has become as enterprises modernize applications, adopt Zero Trust security, and push workloads to multiple clouds. The Domain Name System Tools market is benefiting from rapid 5G private-network build-outs that demand sub-millisecond resolution, increasing IoT footprints that place DNS servers at the edge, and rising board-level attention to DNS-layer cyber risk. Competitive intensity is rising as cloud-native security vendors embed DNS controls into platform offerings, while legacy specialists respond with AI-driven analytics and more granular policy engines. Pricing dynamics are shifting as managed services outpace on-premises licenses and free recursive DNS providers challenge premium tiers, compelling vendors to differentiate through uptime guarantees, analytics depth, and compliance tooling.

Key Report Takeaways

- By deployment type, cloud platforms held 52% of the Domain Name System Tools market share in 2024, while hybrid architectures are set to expand at a 12.63% CAGR through 2030.

- By component, software and platform solutions accounted for 59% share of the Domain Name System Tools market size in 2024; the services segment is advancing at an 11.84% CAGR to 2030.

- By organization size, large enterprises commanded 61% of the Domain Name System Tools market size in 2024, whereas SMEs are forecast to progress at a 12.29% CAGR over 2025-2030.

- By vertical, IT and telecom captured 27% of the Domain Name System Tools market size in 2024, while BFSI is projected to grow at a 10.67% CAGR to 2030.

- By geography, North America led with 36% revenue share in 2024; Asia-Pacific is anticipated to rise at an 11.23% CAGR during the forecast horizon.

Global Domain Name System Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-cloud and hybrid-cloud proliferation | +2.1% | Global, North America and EU lead | Medium term (2-4 years) |

| DDoS, cache-poisoning and DNS-tunneling surge | +1.8% | Global, Asia-Pacific volumes highest | Short term (≤ 2 years) |

| Edge-computing and IoT footprint expansion | +2.3% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| DNS-over-HTTPS/TLS adoption for privacy | +1.4% | EU and North America | Medium term (2-4 years) |

| 5G private-network roll-outs | +1.9% | Asia-Pacific leads, followed by North America and EU | Long term (≥ 4 years) |

| SaaS bundling of managed DNS | +1.2% | Global, SME uptake fastest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Multi-Cloud and Hybrid-Cloud Architectures

Hybrid designs are growing at a 12.63% CAGR because enterprises need synchronized policies across AWS, Azure, and Google Cloud while keeping latency low for users. Case studies show page-load improvements nearing 10 times when dynamic DNS routing pushes traffic to the nearest edge PoP. Unified DDI platforms that automate failover and IPAM are now replacing siloed, on-premises tools, particularly in retail and media workloads that swing sharply with traffic spikes. [1]“Introducing Our Revolutionary DDI Services for the Hybrid, Multi-Cloud Era,” Infoblox, infoblox.com Vendor roadmaps increasingly integrate IaC templates so DevOps teams can declare DNS state alongside application code, easing governance and rollback. Compliance controls aligned with NIS2 and similar rules intensify demand for audit-ready DNS logs, further accelerating platform refresh cycles.

Surge in DDoS, Cache-Poisoning and DNS-Tunneling Attacks

DNS-layer threats rose markedly in 2024 as adversaries used AI models to spawn algorithmically generated domains that evade blocklists. Financial DDoS campaigns targeting authoritative servers can spike operating costs by tens of thousands of dollars within hours. [2]“The Cost Impact of DDoS Attacks on DNS Services,” Nexusguard, nexusguard.com Enterprises are deploying inline ML analytics that profile query patterns in real time; one global bank now blocks 374,000 malicious requests daily through advanced DNS security subscriptions. Insurers are tightening underwriting standards around DNS resilience, making monitored, redundant anycast footprints a prerequisite for favorable cyber-risk premiums.

Expansion of Edge-Computing and IoT Device Footprints

Latency-sensitive manufacturing, telemedicine, and autonomous-vehicle applications demand DNS resolution at or near the device, slashing round-trip trips to centralized data centers. Studies document a 92.5% drop in anomaly-detection lag when compute and DNS reside at the edge rather than in the core cloud. [3]“Edge Computing and Analytics for IoT Devices: Enhancing Real-Time Decision Making in Smart Environments,” SSRN, ssrn.com Vendors now offer lightweight authoritative nodes deployable on Kubernetes clusters inside factory floors, with policy synchronization back to centralized orchestrators. 5G network slicing amplifies this need by spawning isolated DNS zones per slice, forcing providers to manage thousands of ephemeral records without downtime.

Adoption of DNS-over-HTTPS/TLS for Privacy Compliance

GDPR and comparable statutes push enterprises toward encrypted queries to keep user metadata confidential. DoH and DoT deployments jumped throughout 2024, yet security teams worry about losing visibility for threat hunting. Solutions emerging from Microsoft and others enforce domain-allow lists within the endpoint’s DNS stub, enabling privacy without blind spots. Hardware appliance makers now embed on-box decryption capabilities that mirror queries to SIEM tools, seeking a middle ground between confidentiality and observability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outage-induced switching barriers and vendor lock-in | -1.3% | Global, enterprises hardest hit | Medium term (2-4 years) |

| Free recursive public DNS reducing paid adoption | -0.9% | Global, SME impact strongest | Short term (≤ 2 years) |

| DNSSEC skill-set shortages | -0.7% | Global, developing regions | Long term (≥ 4 years) |

| Sovereign-cloud and data-residency regulations | -1.1% | EU and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Outage-Induced Switching Barriers and Vendor Lock-In Concerns

Large enterprises report monthly outage losses exceeding USD 1 million when DNS fails, making even planned migrations risky. Complex hybrid architectures include thousands of static and dynamic records tied to application firewalls, making replication labor-intensive. Many firms keep the incumbent platform live in read-only mode after cutover, paying double fees to hedge against propagation errors. Vendors leverage this inertia with multi-year contracts bundled to IPAM and DHCP add-ons, which further raise exit costs and suppress churn.

Free Recursive Public DNS Lowering Paid-Service Adoption

Google Public DNS and Cloudflare’s 1.1.1.1 offer enterprise-grade response times at zero cost, causing smaller businesses to defer premium subscriptions. Commercial providers respond by layering threat-intelligence feeds, compliance auditing, and per-record analytics to justify pricing. Yet feature bloat can overwhelm lean IT teams, slowing decision cycles and elongating proof-of-concept phases. Subscription hikes, exemplified by DNS Made Easy’s move from USD 5 to USD 45 monthly, spark debate on value perception even as functionality grows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Models Drive Infrastructure Evolution

Hybrid deployments accounted for 12.63% CAGR through 2030, outpacing cloud-only and on-premises models, as firms kept authoritative zones in-house for sovereignty while leveraging global anycast in the cloud for peak traffic. The Domain Name System Tools market size for hybrid deployments is forecast to hit USD 1.87 billion by 2030, reflecting stronger compliance alignment in finance and healthcare. Hybrid environments also enable selective encryption, such as DoH for external queries while retaining DoT internally to accommodate existing packet inspection workflows. Edge gateways now incorporate DNS micro-services that synchronize to the same hybrid controllers, easing route-policy coordination across industrial IoT estates.

Cloud remains crucial with a 52% share in 2024 because SaaS platforms reduce capex and supply integrated SLAs spanning authoritative, recursive, and security layers. On-premises deployments persist in industries bound by air-gap mandates or sovereign-cloud statutes. Vendors offer turnkey hardware clusters with hot-swap drives and automated signer-key rotation to satisfy these niche needs while simplifying maintenance windows.

By Component: Services Surge as Complexity Increases

Managed DNS, consulting, and support contracts are expanding at an 11.84% CAGR, reflecting skills shortages in DNSSEC signing and policy automation. Enterprises opt for lifecycle engagements that include 24×7 SOC monitoring, quarterly risk assessments, and automatic failover testing. The Domain Name System Tools market size for services is projected to cross USD 1.71 billion by 2030, as AI-driven threat feeds require continual tuning by specialist analysts.

Software and platforms still dominate with 59% revenue share because authoritative and recursive engines underpin every other value-added layer. Vendors ship containerized images ready for Helm chart deployment, letting DevOps teams iterate without manual package upgrades. Licensing is shifting from perpetual nodes to traffic-based tiers that scale elastically with CDN-induced demand surges.

By End-User Organization Size: SME Adoption Accelerates Through Cloud Access

Large enterprises controlled a 61% share in 2024, given their expansive namespace inventories and global branch footprints. They demand granular RBAC, SOC-2 attestation, and 99.999% uptime guarantees. However, SMEs are projected to grow at a 12.29% CAGR as cloud APIs lower entry barriers. Subscription bundles priced below USD 100 per month now include DoH, RPZ filtering, and optional SOC alerting, replacing basic ISP resolvers. The Domain Name System Tools market share commanded by SMEs is forecast to climb to 43% by 2030 as feature parity with enterprise tiers narrows.

Vendor portals now expose low-code policy builders that abstract BIND syntax, enabling small IT teams to craft conditional forwarding and split-DNS views. Training programs delivered via online academies accelerate SME onboarding while creating new revenue streams for providers.

By Industry Vertical: Financial Services Lead Digital Transformation

IT and telecom retained a 27% share because carriers integrate DNS caching into subscriber access networks to optimize latency and filter malware in real time. BFSI will log the fastest growth at 10.67% CAGR due to real-time payments and trading systems that penalize millisecond delays. One top-10 bank cut DNS failover from minutes to seconds after deploying anycast-based authoritative clusters, translating to a documented USD 2 million annual OPEX reduction.

Healthcare is accelerating encryption adoption to protect electronic health records, while education institutions expand capacity for e-learning, surging in the use of SaaS-based DNS security. Government agencies in the United States now require encrypted DNS for all executive-branch domains, spurring agency-wide migrations to compliant platforms.

Geography Analysis

North America generated 36% of 2024 revenue owing to mature cloud adoption, strong cyber regulations, and the presence of leading vendors. Federal mandates such as CISA’s encrypted DNS directive push even mid-market firms toward managed recursion with integrated logging. U.S. spending remains buoyant, with Cloudflare earning USD 849.5 million domestically in 2024. Canada mirrors this trend through its Secure Smart Cities initiatives, encouraging edge-ready DNS architectures.

Asia-Pacific is the fastest-growing region at 11.23% CAGR, thanks to 5G roll-outs and IoT manufacturing hubs. China alone may reach USD 266.1 million by 2030, aided by industrial automation priorities in the 14th Five-Year Plan. Singapore’s data-center boom and the Asia-Pacific DNS Forum’s focus on DNSSEC training catalyze security upgrades for regional enterprises. India’s public-sector digital-ID platforms also stimulate demand for sovereign, compliant DNS hierarchies.

Europe remains a pivotal compliance-driven market. GDPR and the incoming NIS2 Directive call for accurate registration data and breach notification within 24 hours, sparking platform refreshes that embed audit trails and encrypted query handling. DNS4EU, backed by the European Commission, underwrites regional providers like ClouDNS and EuroDNS to deliver sovereign resolution services. Nordic countries push for carbon-neutral data centers, prompting the adoption of energy-efficient authoritative clusters cooled by renewable sources.

Competitive Landscape

The Domain Name System Tools market is moderately consolidated. Leaders such as Cloudflare, Infoblox, and Akamai advance AI-based detection that classifies domains at query time, shrinking dwell periods for DNS-tunneling malware. DigiCert’s 2024 purchase of Vercara folded authoritative services into a broad digital-trust portfolio, handling one-fifth of global queries and illustrating escalating scale economics.

Platform convergence is unmistakable. Palo Alto Networks now offers Advanced DNS Security as a cloud subscription that plugs into its broader firewall ecosystem, giving customers unified policy planes across ports and protocols. Microsoft’s Zero Trust DNS, in private preview, brings domain-name allow-listing to Windows endpoints, closing gaps between endpoint detection and network filtering.

Emerging competitors carve niches in industrial IoT, healthcare compliance, and automated certificate-bound records. Some innovators pair DNS telemetry with SIEM correlation engines, enriching threat context for SOC analysts. Price competition intensifies as free recursive services match enterprise latencies, pushing vendors to tie SLAs to query integrity, not just uptime.

Domain Name System Tools Industry Leaders

Cloudflare, Inc.

Infoblox Inc.

Akamai Technologies, Inc.

NS1 Inc.

BlueCat Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Microsoft announced Zero Trust DNS private preview integrating domain-based lockdown and DoH/DoT support.

- January 2025: Akamai released Infrastructure Security Analytics for Edge DNS with SIEM connectors.

- September 2024: DigiCert completed Vercara acquisition, forming a unified trust platform.

- September 2024: Infoblox launched Universal DDI suite unifying DNS, DHCP, and IPAM.

Global Domain Name System Tools Market Report Scope

| Cloud |

| On-premises |

| Hybrid |

| Software / Platform | |

| Services | Managed DNS |

| Consulting and Integration | |

| Support and Maintenance |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Media and Entertainment |

| Retail and eCommerce |

| Healthcare and Life Sciences |

| Education |

| Government and Public Sector |

| Other Industry Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Type | Cloud | ||

| On-premises | |||

| Hybrid | |||

| By Component | Software / Platform | ||

| Services | Managed DNS | ||

| Consulting and Integration | |||

| Support and Maintenance | |||

| By End-User Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | IT and Telecom | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Media and Entertainment | |||

| Retail and eCommerce | |||

| Healthcare and Life Sciences | |||

| Education | |||

| Government and Public Sector | |||

| Other Industry Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What CAGR is expected for the Domain Name System Tools market during 2025-2030?

The market is projected to expand at a 10.31% CAGR through 2030, rising from USD 2.49 billion to USD 4.07 billion.

Which deployment model is growing fastest within Domain Name System Tools?

Hybrid architectures are forecast to grow at a 12.63% CAGR because they balance on-premises control with cloud scalability.

Why are financial institutions investing heavily in DNS platforms?

BFSI firms need millisecond-level performance and strict compliance; optimized DNS can cut annual operating costs by millions while meeting regulatory mandates.

Which region will add the most incremental revenue by 2030?

Asia-Pacific, fueled by 5G roll-outs and IoT manufacturing, is expected to deliver the highest incremental gains at an 11.23% CAGR.

How are vendors differentiating against free public DNS services?

Providers bundle AI-driven threat detection, compliance audit trails, and SLA-backed uptime guarantees that free resolvers do not offer.

What role does DNS-over-HTTPS play in enterprise adoption decisions?

Encrypted queries help organizations meet privacy regulations while new tools maintain visibility, driving wider adoption without sacrificing security monitoring.

Page last updated on: