Clinical Chemistry Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.93 Billion |

| Market Size (2031) | USD 18.37 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

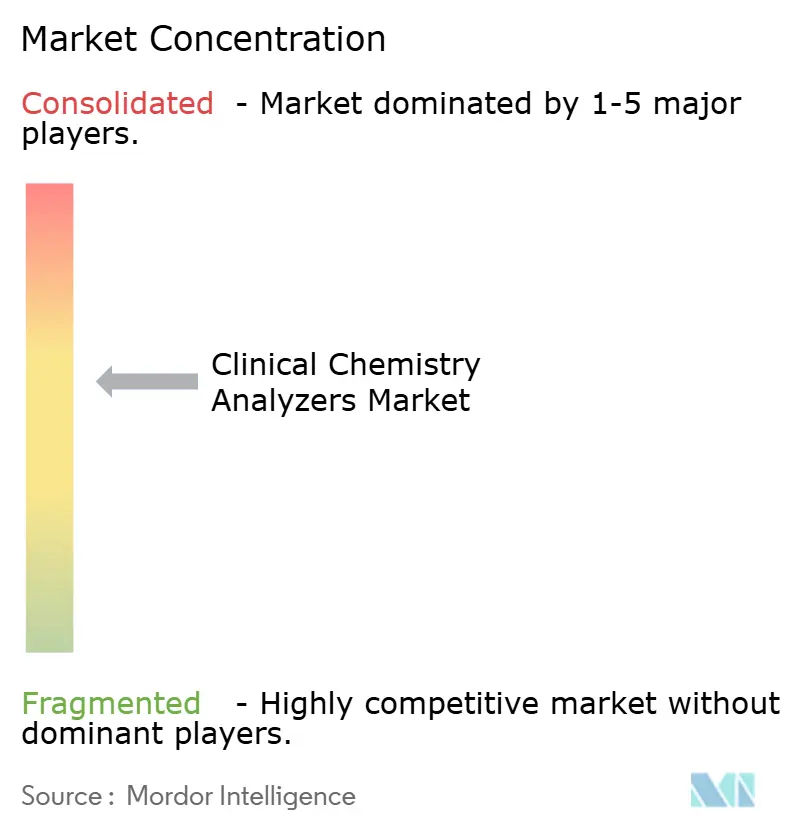

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Chemistry Analyzers Market Analysis by Mordor Intelligence

The clinical chemistry analyzers market size was valued at USD 14.32 billion in 2025 and estimated to grow from USD 14.93 billion in 2026 to reach USD 18.37 billion by 2031, at a CAGR of 4.24% during the forecast period (2026-2031). The steady expansion reflects a maturing yet resilient space where automation, artificial intelligence, and data-centric workflows increasingly define value creation. Heightened demand for high-throughput instruments, combined with a pivot toward integrated informatics, is reshaping procurement decisions and softening the historic reliance on sheer test-volume growth. Vendors now differentiate by uptime, predictive maintenance, and middleware interoperability rather than reagent bundling alone. Hospital consolidation, point-of-care expansion, and chronic-disease surveillance continue to anchor daily test volumes, while capital investment cycles favor modular analyzers that can be field-upgraded as assay menus widen. Price pressures in emerging regions and stricter cybersecurity mandates remain headwinds, but the medium-term outlook is buoyed by demographic shifts and the migration of specialty biomarkers onto routine chemistry platforms, ensuring persistent demand for the clinical chemistry analyzers market.

Key report takeaways

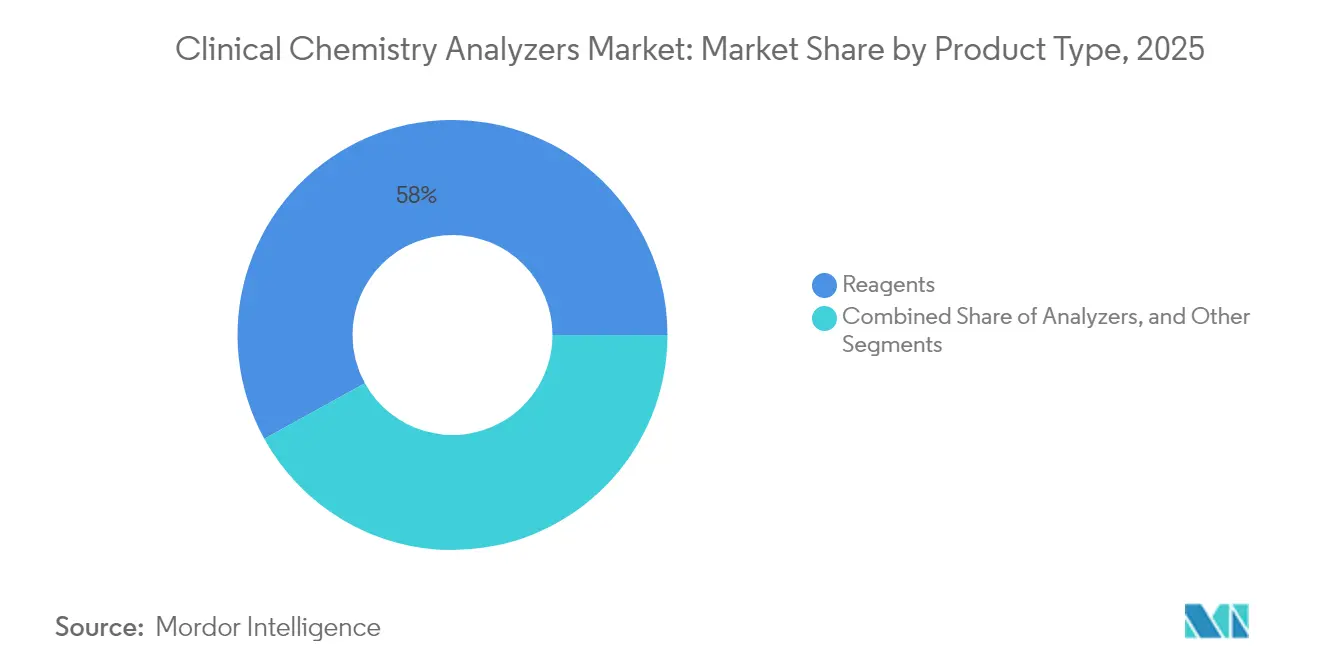

- By product category, reagents commanded a dominant 58.02% share of the clinical chemistry analyzers market in 2025, ensuring a steady revenue stream from consumables. Analyzers will experience the industry's swiftest growth, registering an 8.12% CAGR through 2031, as laboratories ramp up their automation investments.

- By types of test, cardiac markers are set to outpace basic metabolic panels, expanding at an 8.72% CAGR, fueled by the rising adoption of high-sensitivity troponin.

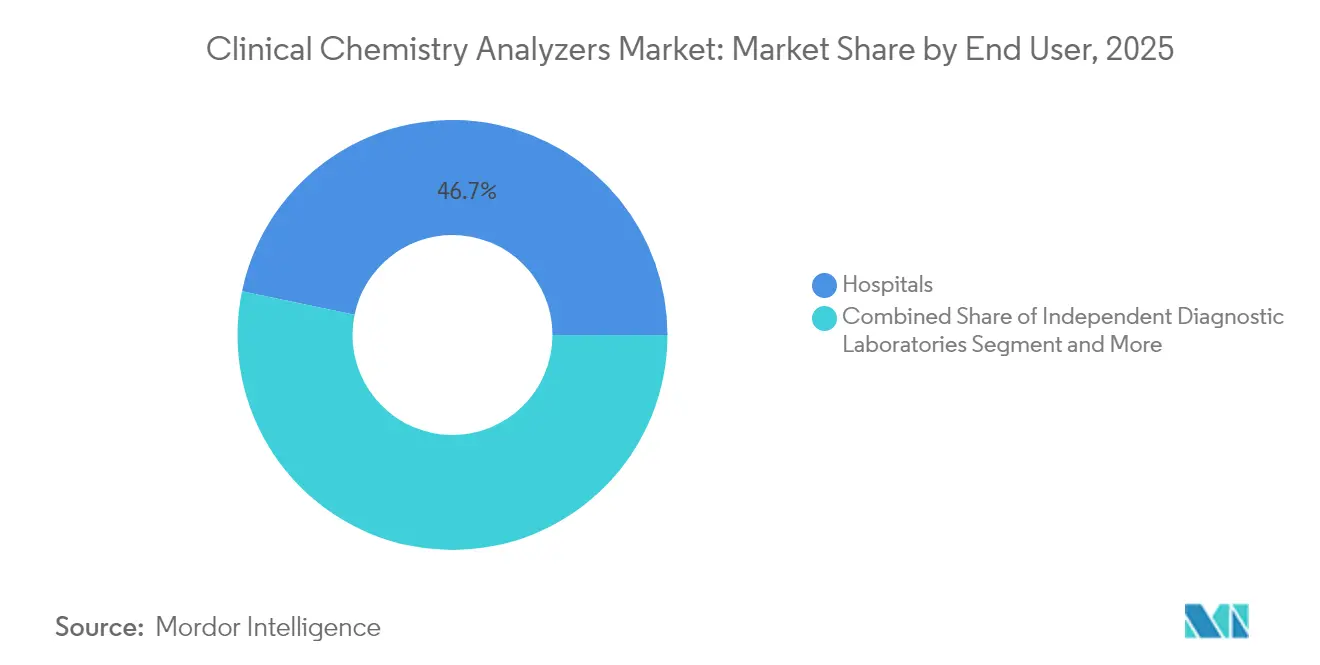

- By end user, point-of-care centers, driven by urgent critical-care needs, are projected to lead with a robust 9.02% CAGR.

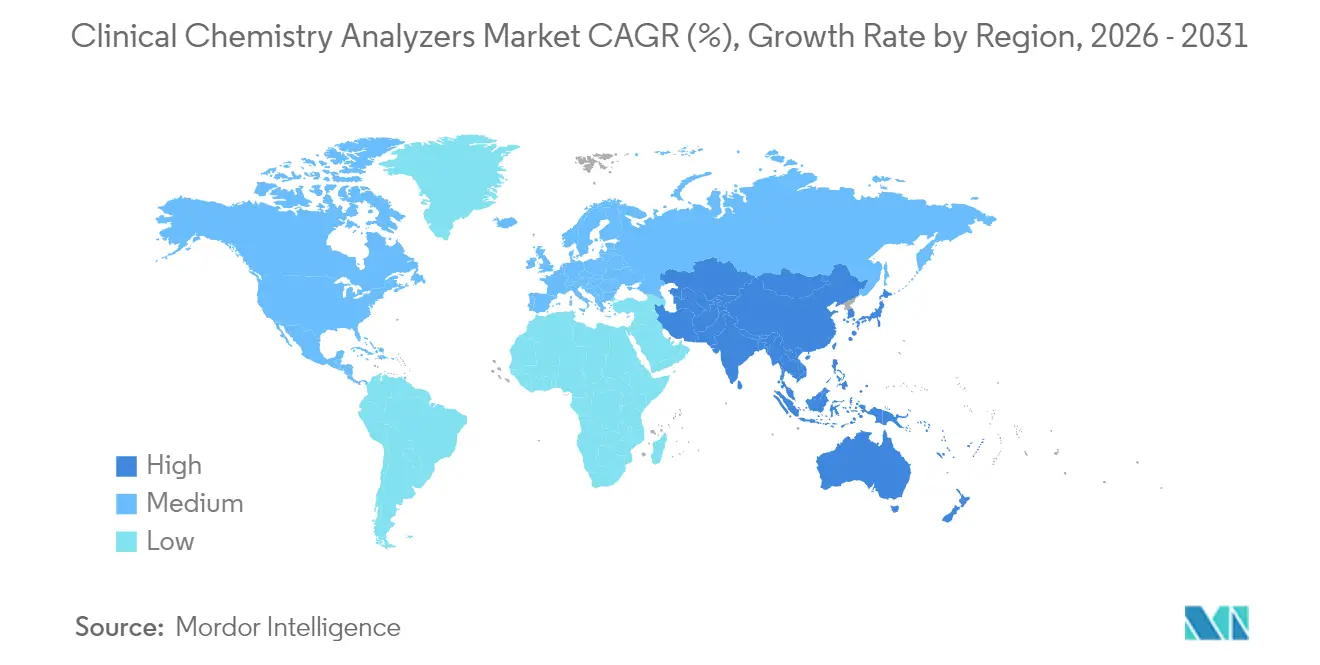

- By geography, while North America led with a substantial 33.78% revenue share in 2025, the Asia-Pacific region is emerging as the dominant growth engine, eyeing a commendable 7.56% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clinical Chemistry Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & chronic-disease burden | +1.5% | North America, Europe; growing global influence | Long term (≥ 4 years) |

| Point-of-care adoption in critical care | +0.8% | North America, Europe; Asia-Pacific emerging | Medium term (2-4 years) |

| AI-enabled high-throughput automation | +0.7% | Early uptake in developed markets; global diffusion | Medium term (2-4 years) |

| Broader metabolic/specialty test menu | +0.6% | Worldwide, aligned with precision-medicine strategies | Long term (≥ 4 years) |

| Sustainability push for energy-efficient HW | +0.4% | Europe leading, North America following | Long term (≥ 4 years) |

| Monetization of analyzer-generated data | +0.3% | North America, Europe; roll-out to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic-Disease Burden

Rapid demographic aging is intensifying chronic-disease testing needs, lifting daily demand for metabolic panels, cardiac markers, and renal function assays. Screening and monitoring protocols for diabetes, cardiovascular disorders, and chronic kidney disease have grown more stringent, producing test-volume curves that rise faster than population growth. High-throughput analyzers with auto-repeat and reflex testing options deliver the scalability required to keep pace with this influx, enabling laboratories to future-proof capacity without proportionate staffing increases. Instrument vendors that package workflow simulators and predictive analytics enjoy a competitive edge in capital tenders. In mature healthcare systems, pay-for-outcome reimbursement further cements the clinical chemistry analyzers market as a frontline resource for preventive care programs. Long term, demographic momentum ensures durable test volumes even amid episodic spending slowdowns.

Point-of-Care Adoption in Critical Care Settings

Emergency departments and intensive care units increasingly depend on near-patient chemistry panels that return results within minutes rather than hours. High-sensitivity cardiac troponin, lactate, and metabolic assessments now guide rapid triage, reducing door-to-needle times in myocardial infarction and sepsis pathways. bioMérieux’s EUR 111 million move for SpinChip Diagnostics typifies strategic investment aimed at 10-minute cardiac marker turnaround. As device miniaturization narrows the analytical gap with central labs, decentralised workflows slash specimen transport delays and hospital length-of-stay, amplifying value for payers and providers. The resulting demand updraft positions benchtop systems and disposable microfluidic cartridges as high-growth niches within the clinical chemistry analyzers market.

AI-Enabled High-Throughput Automation

Machine-learning algorithms embedded in flagship analyzers now forecast instrument drift, optimize reagent usage, and trigger maintenance cycles autonomously. Roche’s cobas c 703 processes up to 2,000 tests per hour while auto-calibrating reagent packs, replacing manual QC checks with rule-based statistical monitoring[1]Roche Diagnostics, “cobas c 703 Analytical Unit,” roche.com. Vendors that couple remote performance dashboards with cloud-delivered expert diagnostics help laboratories shrink downtime, a crucial differentiator amid persistent technologist shortages. Over the medium term, AI-orchestrated workflows pave the way for “dark labs” that run 24/7 under lights-out conditions, a frontier that reshapes staffing models and strengthens the clinical chemistry analyzers market’s appeal to hospital CFOs.

Broader Metabolic/Specialty Chemistry Test Menu

Routine chemistry platforms increasingly incorporate high-sensitivity troponin, pro-BNP, inflammatory markers, and emerging peptides such as DPP3 or adrenomedullin, enabling a one-stop analytical hub for acute-care diagnostics. Consolidating specialized assays onto core instruments raises revenue per test and curtails sample splitting, a boon for workflow efficiency. Expanded menus also unlock participation in precision-medicine initiatives where longitudinal biomarker panels inform therapy selection. Manufacturers that balance assay range with throughput can capture share from niche specialty systems and reinforce installed-base stickiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled lab technologists | –0.9% | North America, Europe; widening elsewhere | Short term (≤ 2 years) |

| High capital & maintenance costs | –0.5% | Global; sharper in low-resource markets | Medium term (2-4 years) |

| Rare-earth-dependent reagent supply risk | –0.4% | Asia-Pacific most exposed | Medium term (2-4 years) |

| Rising cybersecurity & compliance overhead | –0.3% | North America, Europe; expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Lab Technologists

Vacancy rates of 17.3% in U.S. chemistry departments and 46% across total laboratory positions underline a widening skills gap. Recruitment lags stem from retiring baby-boom cohorts, limited training program capacity, and muted public visibility of the profession. While middleware automation eases manual workloads, oversight of quality-control flags and complex result interpretation still demands licensed staff. Laboratories respond with cross-training, relaxed credential prerequisites, and salary premiums, yet the supply-demand mismatch endures. For manufacturers, intuitive user interfaces, auto-verification algorithms, and remote diagnostics become product imperatives to counter workforce scarcity, reinforcing value propositions inside the clinical chemistry analyzers industry.

High Capital & Maintenance Costs

Sophisticated analyzers command list prices north of USD 300,000, with annual service contracts adding 10-12% of purchase cost. Budget-constrained hospitals in Latin America and parts of Southeast Asia often defer upgrades, prolonging the lifecycle of legacy instruments. Deferred capex slows adoption of newer reagent chemistries and AI modules that underpin differentiated offerings. Vendors combat sticker shock through reagent-rental agreements, pay-per-test models, and multi-year financing, yet the upfront cost hurdle continues to moderate near-term uptake in developing economies, tempering overall growth in the clinical chemistry analyzers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reagents Sustain Revenue While Analyzers Drive Innovation

The reagents segment accounted for 58.02% of clinical chemistry analyzers market size in 2025, reflecting the entrenched consumable model that underwrites laboratory cash flow. Revenues remain predictable as recurrent test volumes anchor demand for calibrators, controls, and enzyme substrates. Yet capital investments are tilting toward fully automated analyzer platforms that promise faster throughput, AI-backed maintenance, and consolidated assay menus, resulting in an 8.12% CAGR forecast for analyzers through 2031. Instrument purchases increasingly include middleware licenses and cloud dashboards bundled into total-solution contracts, signaling a shift from component pricing to outcome-based procurement.

Benchtop analyzers are outpacing floor-standing units in shipment growth, powered by point-of-care expansion and the repatriation of acute panels into emergency wards. Vendors differentiate via cartridge ergonomics, sample traceability, and rapid QC unlock times that maximize uptime. Reagent innovation centers on liquid-stable formulations with extended onboard stability, trimmed plastic volume per test, and barcoded pack tracking that feeds inventory analytics. Specialty chemicals for high-sensitivity cardiac troponin and emerging sepsis markers deliver premium margins, partially offsetting price erosion in basic metabolic reagents. The combined effect is a balanced ecosystem where consumables guarantee baseline revenue while hardware upgrades unlock step-change efficiency, fortifying long-term demand for the clinical chemistry analyzers market.

By Types of Test: Cardiac Markers Accelerate While Metabolic Panels Anchor Growth

Basic metabolic panels contributed 22.41% of 2025 revenue, cementing their role as cornerstone assays across primary care, inpatient monitoring, and chronic-disease management. Their volume stability shields laboratories from elective-procedure volatility and underpins reagent pull-through. Cardiac marker assays, notably high-sensitivity troponin I/T, are projected to log an 8.72% CAGR, the fastest among test categories, on rising chest-pain presentations and guideline-mandated serial testing. With throughput-optimized analyzers now completing first results in under 10 minutes, clinicians can discharge low-risk patients sooner, translating to measurable bed-day savings.

Renal and liver function panels exhibit mid-single-digit growth, supported by CKD surveillance programs and hepatitis screening, respectively. Lipid profiles face substitution pressure from apolipoprotein and emerging lipoprotein-particle assays. Specialty chemistries encompassing DPP3 and adrenomedullin are nascent yet promise double-digit expansion once clinical-utility evidence matures. Integrating automated rule engines that reflex to confirmatory tests elevates clinical utility and elevates service line contribution per sample, reinforcing the premium trajectory of the clinical chemistry analyzers market.

By End User: Point-of-Care Centers Disrupt Traditional Laboratory Models

Hospitals retained 46.74% share of the clinical chemistry analyzers market in 2025, leveraging central labs that run high-volume instruments round-the-clock. Yet the fastest growth emanates from point-of-care centers at a projected 9.02% CAGR as emergency medicine and critical-care clinicians pursue immediate result turnaround. Plug-and-play benchtop analyzers with cartridge-based reagents reclaim analytic territory historically reserved for stat labs, enabling bedside management and reducing interdepartmental sample-transfer latency.

Independent diagnostic laboratories contend with reimbursement compression and automation races that erode traditional cost advantages. Academic research hubs represent a specialized niche, commanding premium, open-channel systems for assay development, but account for a modest revenue share. The rise of “dark labs,” fully automated facilities staffed by minimal technologists, heralds an efficiency revolution: early adopters report 20% lower operating costs and superior QC pass rates. Vendors that supply turnkey service bundles—encompassing instrument rental, reagent logistics, and compliance documentation—stand to outcompete fragmented offerings in this evolving end-user landscape.

Geography Analysis

North America generated 33.78% of 2025 revenue, anchored by robust reimbursement, rapid AI adoption, and a dense installed base of next-generation analyzers. The FDA’s LDT Final Rule, while elevating compliance costs, cements a high regulatory bar that entrenches incumbent suppliers who can furnish validated systems and documentation at scale, bolstering overall sales momentum within the region. Europe follows with steady replacement demand but must navigate IVDR-driven re-certification workloads that tax manufacturer resources.

Asia-Pacific is forecast to post a vigorous 7.56% CAGR, driving outsized contribution to future global clinical chemistry analyzers market size. China leads volume growth, propelled by provincial hospital consolidation and chronic-disease screening mandates, even as volume-based-procurement schemes challenge vendor pricing power. India and Southeast Asian nations accelerate rural diagnostic outreach via public–private partnerships, boosting benchtop and semi-automated analyzer adoption. Latin America and the Middle East & Africa present mid-single-digit trajectories tied to health-insurance expansion and laboratory infrastructure modernization, albeit vulnerable to currency volatility. Vendors that tailor reagent pack sizes, financing terms, and field-service footprints to local realities capture disproportionate share, underscoring geography-specific execution as a decisive success factor in the clinical chemistry analyzers market.

Regulatory Landscape

Clinical chemistry analyzers and associated IVD systems face tightening quality and evidence requirements across major markets. In the United States, FDA regulation of medical devices and IVDs is reinforced by the phaseout of enforcement discretion for laboratory developed tests (LDTs), which became effective in July 2024 and raises the compliance bar for tests historically run under laboratory frameworks. In February 2026, the FDA Quality Management System Regulation (QMSR) became effective, requiring manufacturers and contract manufacturers to align device quality systems with updated requirements and documentation practices.

In Europe, IVDR-driven conformity assessment capacity remains a defining constraint, with TEAM-NB reporting 3,102 total IVDR applications and 2,500 certificates issued by end-2025, a key indicator of the workload facing Notified Bodies and manufacturers. The IVDR transition calendar also affects chemistry test portfolios, including May 2026 milestones tied to transitional arrangements for Class C devices and related submission timing to maintain market continuity. These shifts increase the strategic value of regulatory-ready menu expansion, post-market surveillance capabilities, and cybersecurity-aware software lifecycle controls for connected analyzers and middleware.

Competitive Landscape

Moderate consolidation typifies the clinical chemistry analyzers industry, with Abbott, Roche, Siemens Healthineers, and Thermo Fisher Scientific collectively holding a majority revenue share. Their global service networks, vertically integrated reagent lines, and ongoing AI-feature rollouts form high barriers to entry. Nevertheless, agile entrants focusing on microfluidic cartridges, cloud-native middleware, or point-of-care cardiac panels disrupt established segments. bioMérieux’s EUR 111 million purchase of SpinChip Diagnostics exemplifies targeted M&A to secure rapid immunoassay IP and tighten time-to-result metrics.

Strategic thrusts increasingly revolve around cloud orchestration, cybersecurity hardening, and sustainability branding rather than incremental throughput gains alone. Siemens Healthineers’ Atellica® ecosystem advertises secure remote monitoring and energy-optimized idle states, while Abbott’s Alinity platform leverages common reagent packs across chemistry and immunoassay modules for inventory rationalization. Thermo Fisher Scientific channels biopharma client relationships into quality-control material cross-selling, further blurring boundaries between clinical and research diagnostics.

Price competition persists in reagents, yet differentiation through data analytics subscriptions and uptime guarantees can outweigh per-test cost considerations for high-complexity labs. Outsourced managed-service contracts now bundle instrument leases, reagent supplies, staffing, and compliance documentation into multi-year service-level agreements, locking in share and elevating switching costs. Looking ahead, scale-driven cost advantages coexist with niche innovation, preserving a dynamic yet disciplined competitive equilibrium within the clinical chemistry analyzers market.

Clinical Chemistry Analyzers Industry Leaders

Abbott Laboratories

Thermo Fisher Scientific Inc.

Danaher Corp. (Beckman Coulter)

Mindray Medical

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity centers on replacing legacy chemistry capacity with modular, high-throughput platforms that address workforce and space constraints in consolidated hospital and reference-lab networks. FDA 510(k) clearance in March 2026 for Roche cobas c 703 and cobas ISE neo analytical units, designed for integration into the cobas pro platform, creates a concrete procurement trigger for laboratories seeking scalable throughput without proportional footprint expansion. Similar momentum appears in integrated chemistry-immunoassay systems, where FDA clearance of Beckman Coulter DxC 500i (March 2025) supports a workflow consolidation play for mid-volume settings that want fewer instruments, fewer interfaces, and simplified training.

Whitespace is also emerging where chemistry platforms, informatics, and adjacent high-precision modalities converge. Published validations of fully automated, random-access mass spectrometry systems (for example, routine-focused platforms with 24-hour capability and minimal operator intervention) suggest a pathway to expand operations for select high-value analytes, complementing routine chemistry rather than replacing it. Product-safety actions also point to where vendors still need tighter operational controls, with Siemens Healthineers recall activity for certain Dimension Creatinine Flex reagent cartridge lots (March 2026) highlighting an unmet need for tighter lot-to-lot control, automated QC intelligence, and vendor-led quality assurance software that reduces manual oversight across multisite labs.

Recent Industry Developments

- June 2026: Thermo Fisher Scientific launched Thermo Scientific LabLink 360 Quality Assurance software for clinical laboratory workflow management. The release expands the company's footprint in lab informatics and quality oversight, supporting networked labs that need standardized QA processes across instruments and sites. It also reinforces procurement decisions that bundle software with analyzer ecosystems rather than standalone hardware.

- March 2025: Beckman Coulter (Danaher) received FDA 510(k) clearance for the DxC 500i Clinical Analyzer, an integrated clinical chemistry and immunoassay system. The clearance enables broader US commercialization for a consolidated testing workflow, which can reduce instrument count and floor space in laboratories balancing chemistry and immunoassay demand. It strengthens competitive positioning in the integrated analyzer segment where automation and menu breadth support replacement decisions.

- July 2024: Beckman Coulter (Danaher) introduced the DxC 500i Clinical Analyzer and made it available in CE mark-accepting countries. The launch supported earlier adoption in international markets and created an installed-base lever for follow-on reagent pull-through and service contracts. It also increased competitive pressure on incumbent systems by emphasizing integration and throughput in a smaller laboratory footprint.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers clinical chemistry analyzers and the related products used to run routine biochemistry tests on patient samples in lab settings. Revenues are tracked across instrument systems and recurring consumables tied to these routine chemistry assays.

Scope exclusions: It does not count broader lab automation that is not used for clinical chemistry testing, or general hospital IT that is not directly tied to analyzer operation.

Segmentation Overview

- By Product Type

- Analyzers

- Floor-standing High-Throughput

- Modular/Integrated Systems

- Benchtop

- Semi-automated

- Reagents

- Calibrators & Controls

- Consumables

- Others (QC Materials, Software Licenses)

- Analyzers

- By Types of Test

- Basic Metabolic Panel

- Electrolyte Panel

- Liver Panel

- Lipid Profile

- Thyroid Function Panel

- Renal Function Panel

- Cardiac Markers

- Specialty Chemistries

- By End User

- Hospitals

- Independent Diagnostic Laboratories

- Academic & Research Institutes

- Point-of-Care Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and build the initial demand map by country and care setting. We used public health statistics and lab diagnostics context from sources such as the World Health Organization, the US Centers for Disease Control and Prevention, the World Bank, and the OECD, since these indicators help explain testing demand and healthcare capacity.

On the supply side, we reviewed manufacturer annual reports, investor presentations, and product literature to understand how systems are positioned and how reagent pull-through works in routine chemistry workflows. Trade association pages and peer-reviewed clinical chemistry journals were used to cross-check the test panels typically run and how instrument throughput is discussed in practice. Where needed, a paid subscription database was used only for company financials and patent checking when public disclosures were limited. The sources listed above are not exhaustive, and other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done to pressure-test assumptions that are hard to confirm from public material, including average reagent attachment rates, replacement cycles, and how testing activity splits between hospital labs and independent diagnostic labs. Interviews included lab managers, procurement and operations leaders, and product and commercial roles across major regions, so adoption patterns in mature markets and fast-growing lab networks could be reflected in one consistent model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | APAC: 39% |

| Mid tier: 46% | Functional/Unit leaders: 41% | EMEA: 37% |

| Smaller Players: 16% | Managers: 44% | Americas: 24% |

Market-Sizing & Forecasting

The core build uses a top-down approach where healthcare activity signals are translated into an addressable testing pool, and then converted into analyzer and reagent revenue using typical utilization patterns. Country totals are first constructed using inputs such as clinical lab testing volumes, the share of routine panels performed on chemistry platforms, installed base and replacement timing, average tests per analyzer per day (utilization), and reagent spend per test across common panels (BMP, electrolyte, liver, lipid, renal, and thyroid).

To keep the totals realistic, we corroborate them with selective bottom-up approximations such as sampled ASP times unit demand for analyzer placements in major care settings, and channel checks on reagent pull-through for high-volume sites where automation is common. When a country has limited disclosure, we close the gap with proxy indicators like hospital bed capacity, diagnostics spend trends, and import patterns for IVD instruments, and then adjust based on what interviewees described for local lab network maturity.

For forecasting, scenario analysis is used so the model can reflect different pathways for routine test growth and automation uptake without forcing a single straight-line curve. Scenarios are anchored on variables such as chronic disease screening intensity, outpatient testing migration, staffing shortages driving automation, public reimbursement stability, and budget cycles that influence instrument replacement, and then aligned to the range of expectations shared by primary respondents.

Data Validation & Update Cycle

Validation is done by checking whether the model outputs line up with independent signals, such as reagent-to-instrument revenue balance, typical replacement cycles, and regional splits that match known lab capacity patterns. We also run variance checks at country and regional levels to identify jumps that do not fit the demand indicators, and those cases are reviewed again with the underlying assumptions before sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur, including major regulatory changes, sharp currency moves, or large shifts in healthcare funding. Before delivery, an analyst performs a fresh pass on the key inputs and calculations so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Clinical Chemistry Analyzers Market Size Compared Against Other Published Estimates

Published numbers for clinical chemistry analyzers rarely match perfectly because authors do not always count the same revenue streams, and they also select different base years and currency timing. Variations in whether reagents and adjacent consumables are included, and how fast test demand is assumed to grow, usually explain most of the spread.

The biggest gap drivers tend to be scope and the way recurring revenues are treated over the forecast window. Some estimates place more weight on instrument shipments and higher ASP assumptions, while others emphasize recurring reagent consumption and apply more conservative utilization per analyzer. Both approaches can still look reasonable unless they are cross-checked against lab workload signals and replacement cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.32 B (2025) | |

| Global Consultancy A | USD 19.61 B (2024) | Uses an earlier base year with a larger stated total, which can happen when instrument and reagent scope is bundled with adjacent lab categories and when currency conversion timing differs across regions. |

| Industry Publisher B | USD 14.93 B (2024) | Often starts from product-level splits that emphasize analyzer classes and broad reagent buckets, but does not always show how utilization, replacement timing, and test-panel mix were used to reconcile country totals. |

The table shows a wide range for the same market window, and in Mordor Intelligence's model the total is tied to routine chemistry testing demand and then translated into analyzer and reagent revenue using explicit utilization and replacement assumptions. When the scope boundary and the linking variables are stated clearly, the result becomes easier to repeat and to stress-test when conditions change.

Key Questions Answered in the Report

What is the current clinical chemistry analyzers market size and growth outlook?

The clinical chemistry analyzers market size is USD 14.93 billion in 2026 and is expected to reach USD 18.37 billion by 2031, reflecting a 4.24% CAGR.

Which product category leads the market today?

Reagents remain the largest revenue contributor with 58.02% share in 2025, driven by stable consumable demand.

Why are cardiac marker assays growing faster than other test panels?

High-sensitivity troponin assays enable rapid myocardial infarction diagnosis, pushing cardiac marker revenues to an 8.72% CAGR through 2031.

How is point-of-care testing influencing the market structure?

Point-of-care centers are growing at 9.02% CAGR, as emergency and critical-care units adopt benchtop analyzers for immediate decision-making.

Which region offers the highest growth potential?

Asia-Pacific is forecast to expand at 7.56% CAGR, propelled by healthcare infrastructure investment and chronic-disease screening programs.

Page last updated on: