MRI - Compatible IV Infusion Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

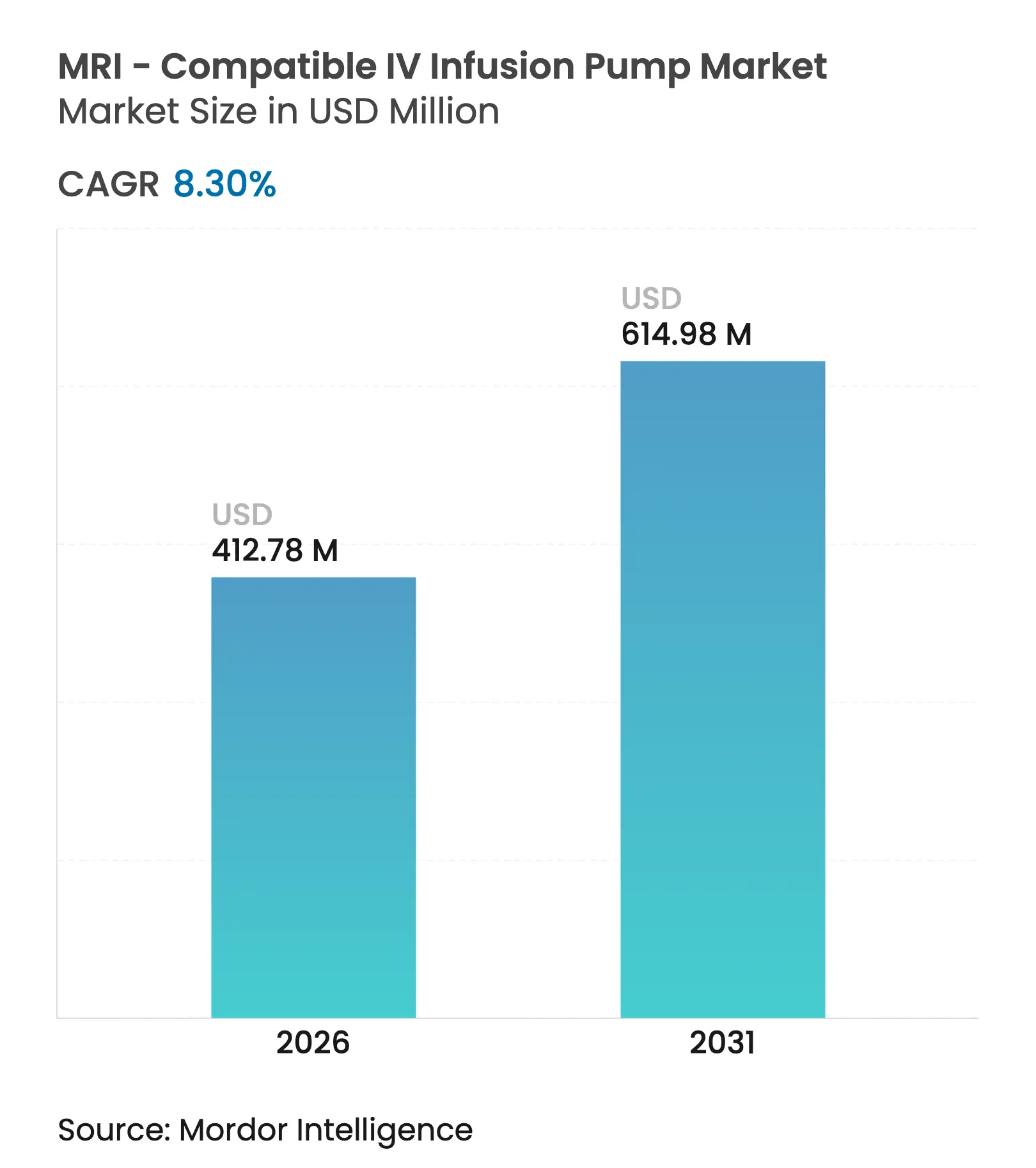

| Market Size (2026) | USD 412.78 Million |

| Market Size (2031) | USD 614.98 Million |

| Growth Rate (2026 - 2031) | 8.30 % CAGR |

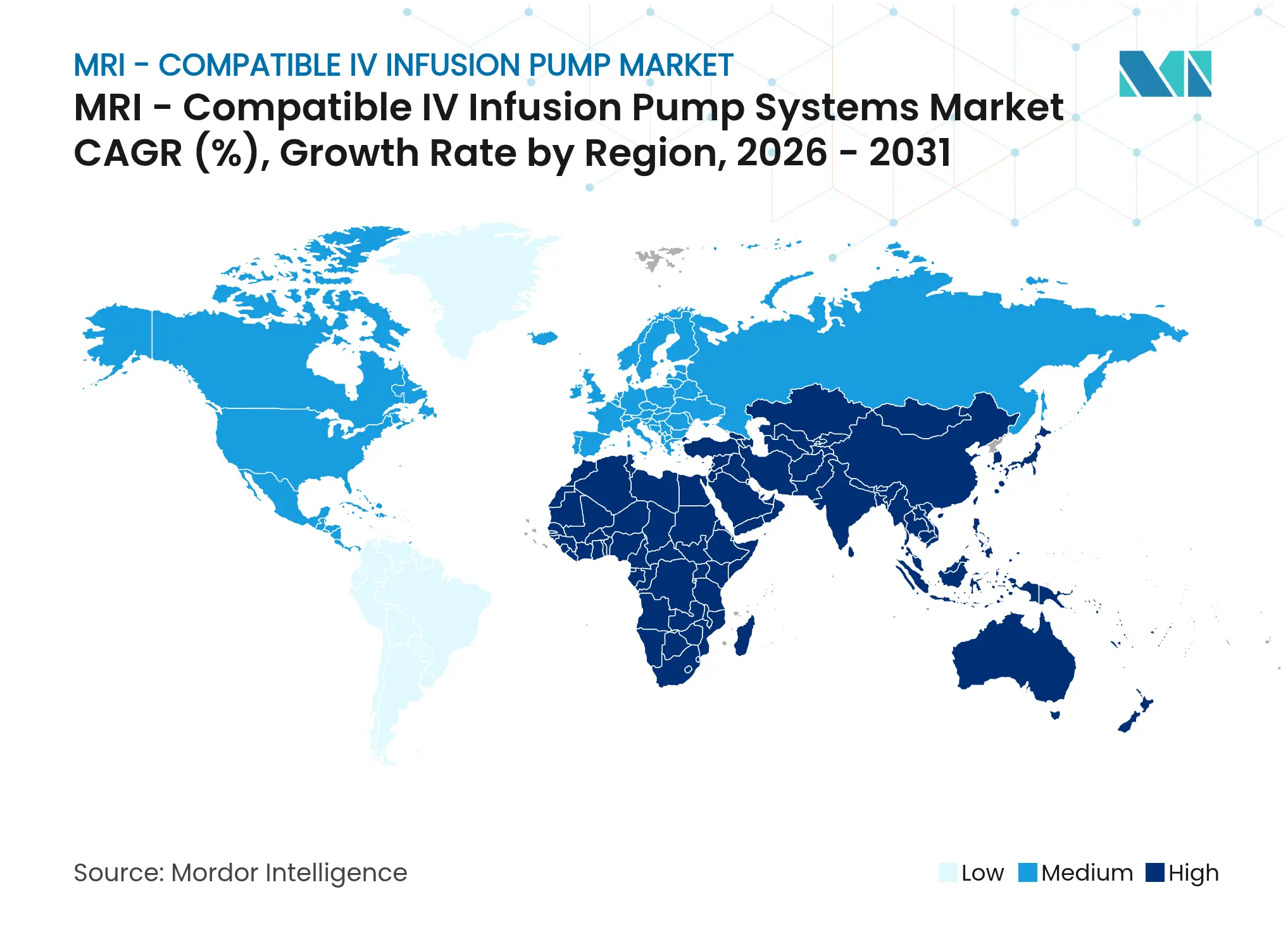

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

MRI - Compatible IV Infusion Pump Market Analysis by Mordor Intelligence

Growth is propelled by widening adoption of high-field MRI suites, the shift toward MRI-guided minimally invasive surgery, and hospitals’ push to standardize precision medication delivery during imaging. Non-magnetic systems currently dominate placements, but magnetic-shielded models are scaling fastest as device makers compress shielding costs. Portability trends, especially bedside units, align with flexible care pathways in intensive care and day-surgery settings. Hospitals remain the largest buyers, yet ambulatory surgical centers (ASCs) now account for most incremental unit demand because favorable reimbursement under the NOPAIN Act rewards non-opioid post-procedure pain management. Regionally, North America leads owing to legacy installed bases and early regulatory clearances, while Asia-Pacific is the principal expansion arena as indigenous MRI manufacturing reduces price barriers.

Key Report Takeaways

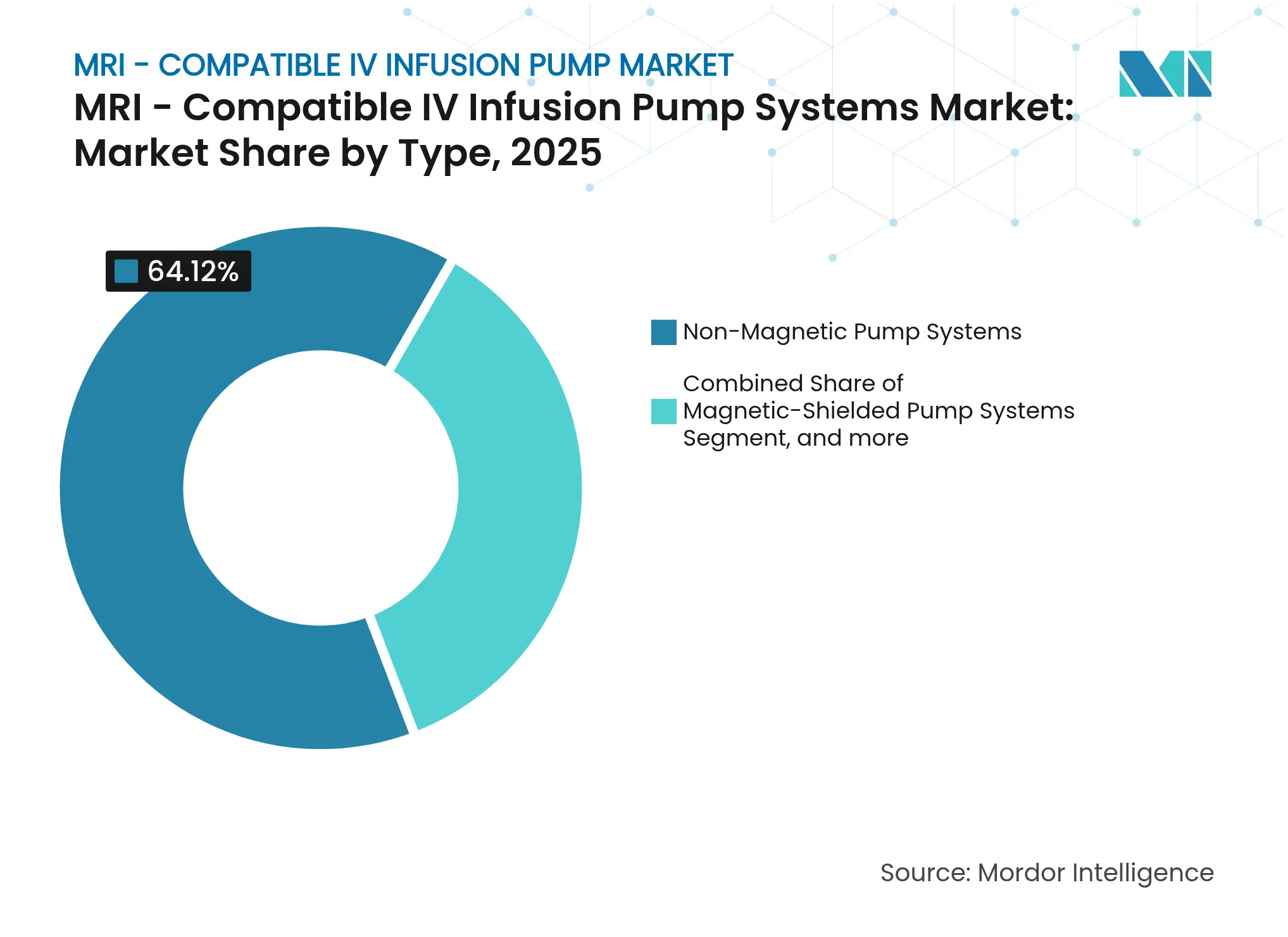

- By type, non-magnetic systems held 64.12% of the MRI-compatible IV infusion pump market share in 2025, while magnetic-shielded systems are projected to advance at a 10.96% CAGR through 2031.

- By magnetic-field compatibility, ≤1.5 T systems captured 42.75% of the MRI-compatible IV infusion pump market share in 2025; ultra-high-field systems are projected to grow at a 11.35% CAGR through 2031.

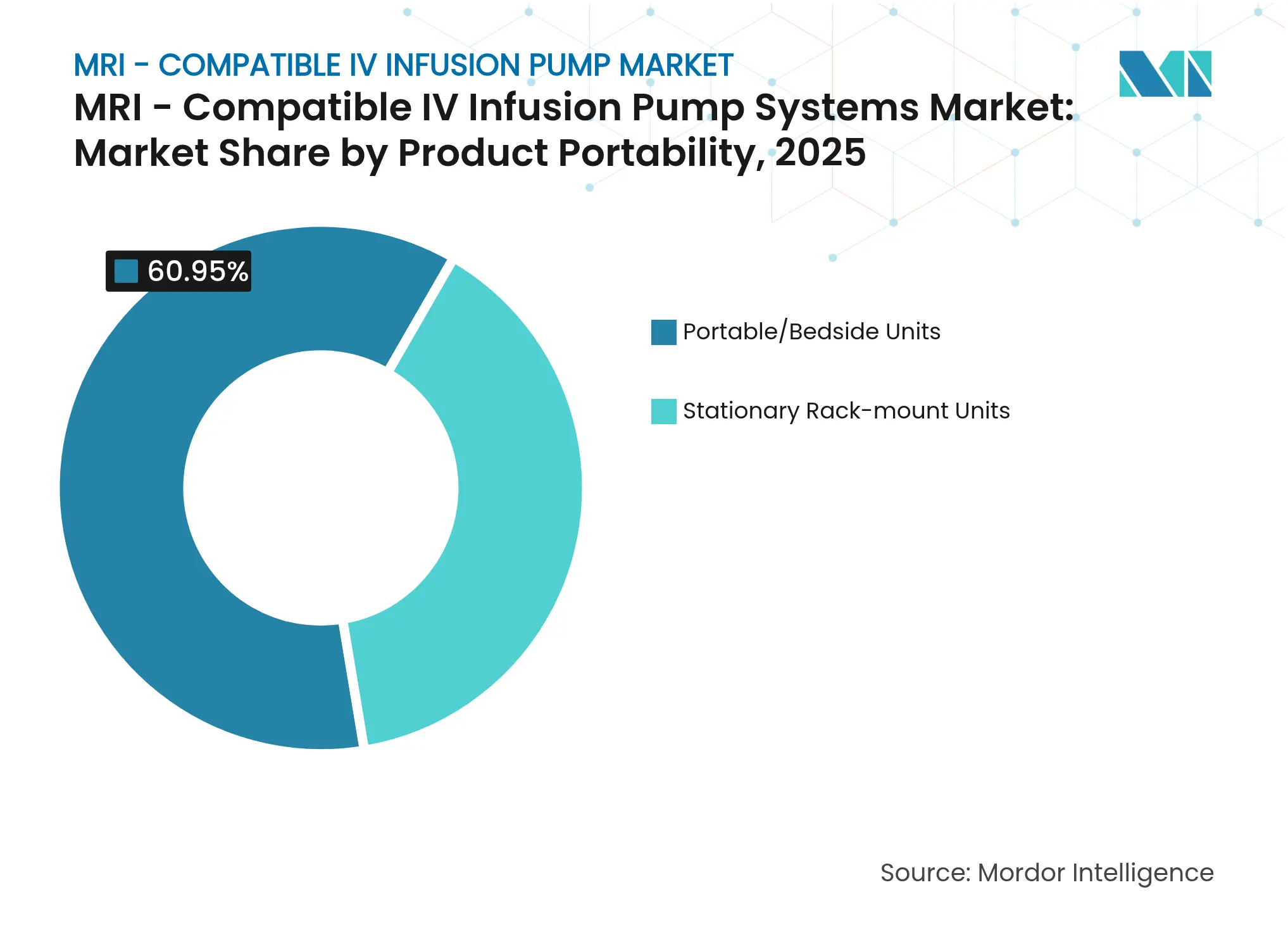

- By product portability, bedside units accounted for a 60.95% share of the MRI-compatible IV infusion pump market size in 2025 and are projected to rise at a 11.62% CAGR.

- By end user, hospitals commanded 68.74% of the MRI-compatible IV infusion pump market size in 2025, while ASCs are expanding fastest at a 12.79% CAGR.

- By geography, North America led the MRI-compatible IV infusion pump market with a 44.10% share in 2025; the Asia-Pacific region is projected to grow at a 12.98% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global MRI - Compatible IV Infusion Pump Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising burden

of chronic diseases & MRI scan volumes

Rising burden

of chronic diseases & MRI scan volumes

| +2.1% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+2.1%

|

Geographic

Relevance

:

Global,

concentrated in North America & Europe

|

Impact

Timeline

:

Long term (≥

4 years)

|

Growing

MRI-guided minimally invasive surgeries

Growing

MRI-guided minimally invasive surgeries

| +1.8% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Advances in

wireless non-magnetic pump platforms

Advances in

wireless non-magnetic pump platforms

| +1.5% | Global, led by US, Germany, Japan | Short term (≤ 2 years) | |||

IoT-enabled

closed-loop MRI infusion ecosystems

IoT-enabled

closed-loop MRI infusion ecosystems

| +1.3% | APAC core, spill-over to North America | Medium term (2-4 years) | |||

Expansion of

intra-operative MRI suites

Expansion of

intra-operative MRI suites

| +1.0% | North America & EU; selective APAC adoption | Medium term (2-4 years) | |||

Hospital

policies eliminating long IV-line workarounds

Hospital

policies eliminating long IV-line workarounds

| +0.8% | Global, faster in developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Burden of Chronic Diseases & MRI Scan Volumes

Higher prevalence of cardiovascular, neurological, and oncological disorders raises the number of MRI studies that require uninterrupted drug infusion. The FDA’s updated MRI-device safety guidance gives manufacturers clearer routes to clearance, accelerating product launches.[1]U.S. Food and Drug Administration, “Guidance for Industry and FDA Staff: MRI Safety and Compatibility,” fda.gov Tertiary hospitals are aggregating integrated MRI suites so that complex infusion regimens proceed without patient relocation. The aging demographic intensifies this demand, as multimorbidity often necessitates simultaneous imaging and therapy.

Growing MRI-Guided Minimally Invasive Surgeries

Real-time neuro, cardiac, and focused-ultrasound procedures need pumps that function inside 1.5 T, 3 T, and emerging 7 T magnets. GE HealthCare’s SIGNA MAGNUS 3.0 T head-only scanner exemplifies the ecosystem pulling infusion makers toward higher-field compatibility.[2]GE HealthCare, “SIGNA MAGNUS 3 T MRI System Cleared by FDA,” gehealthcare.com Hospital capital budgets increasingly pair MRI upgrades with pump purchases because better image guidance shortens length of stay and lowers readmission risk.

Advances in Wireless Non-Magnetic Pump Platforms

IRadimed’s MRidium 3870, cleared by the FDA in May 2025, runs an ultrasonic motor that eliminates ferromagnetic parts and minimizes RF emissions.[3]IRadimed Corporation, “MRidium 3870 Infusion Pump Clearance,” iradimed.com New BioDur 108 stainless alloy reduces nickel and cobalt, improving biocompatibility without compromising structural integrity. Touchscreen interfaces mirror consumer electronics, boosting nurse acceptance and reducing training hours.

IoT-Enabled Closed-Loop MRI Infusion Ecosystems

Connected pumps feed vitals into analytics engines that auto-adjust dosage. Baxter already tracks more than 1.5 million networked devices in hospitals worldwide, a scale that speeds software iteration. Research prototypes demonstrate 94% heart-rate detection accuracy and 98% drip-rate control, signaling imminent commercial translation. Multi-hop sensor networks extend monitoring beyond the magnet suite, linking radiology, ICU, and post-anesthesia units.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital

& maintenance costs

High capital

& maintenance costs

| -1.4% | Global; sharper for smaller facilities | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

-1.4%

|

Geographic

Relevance

:

Global;

sharper for smaller facilities

|

Impact

Timeline

:

Long term (≥

4 years)

|

Limited

reimbursement for MRI disposables

Limited

reimbursement for MRI disposables

| -1.1% | North America & EU | Medium term (2-4 years) | |||

Non-ferrous

component supply bottlenecks

Non-ferrous

component supply bottlenecks

| -0.9% | Global; acute in APAC manufacturing hubs | Short term (≤ 2 years) | |||

MRI-safety

workforce training gaps

MRI-safety

workforce training gaps

| -0.7% | Global; pronounced in emerging markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital & Maintenance Costs

Specialized engineering spikes unit prices, and smaller centers often delay upgrades. India’s public-sector MRI program illustrates cost-containment pressure by promising scanners at half prevailing import prices. Total ownership cost also includes maintenance contracts and magnet-room validation, prolonging payback periods.

Limited Reimbursement for MRI Disposables

Current Medicare rules reimburse external infusion pumps but not necessarily MRI-specific tubing, leaving providers to absorb the incremental cost. The NOPAIN Act’s carve-out for non-opioid pain pumps helps ASCs, yet omits many radiology indications. Payers demand data proving procedure-level savings before widening coverage.

Segment Analysis

By Type: Non-Magnetic Systems Lead Innovation Wave

Non-magnetic pumps accounted for 64.12% of the MRI-compatible IV infusion pump market share in 2025, as their ferrous-free architecture eliminates shielding constraints. This segment anchors the current MRI-compatible IV infusion pump market as large centers prioritize unrestricted patient positioning and workflow simplicity. The MRI-compatible IV infusion pump market size tied to non-magnetic units is forecasted to expand in parallel with the installation of new high-field scanners. Magnetic-shielded pumps are gaining traction, advancing at a 10.96% CAGR as compact shielding materials reduce cabinet bulk. B. Braun’s Space MRI Station features eight conventional pumps housed within a mu-metal cloak, appealing to hospitals that have already standardized on B. Braun software. Disposable tubing manufacturers are experimenting with BioDur 108 alloy to reduce the per-procedure cost while meeting sterility standards.

Achieving ultra-quiet operation inside the magnet bore is a core non-magnetic selling point. Clinicians report fewer alarms, reducing scan interruptions. Meanwhile, shielded models utilize familiar pump interfaces, thereby flattening the learning curve for staff who rotate between MRI and standard infusion rooms. Some tertiary centers mix both types: shielded racks for long oncology infusions and non-magnetic portables for anesthesia and contrast bolus work.

Note: Segment shares of all individual segments available upon report purchase

By Magnetic-Field Compatibility: Ultra-High Field Drives Future Growth

Scanners at ≤1.5 T currently account for 42.75% of the MRI-compatible IV infusion pump market share, mirroring installed base realities. However, ultra-high-field systems exhibit the fastest 11.35% CAGR because neuroscience and cardiac research institutes adopt 7 T magnets. The MRI-compatible IV infusion pump market size in this ultra-high-field niche is expected to grow as head-only and extremity scanners transition from research to clinical settings, leading to increased billing codes. Engineering challenges include eliminating eddy-current noise and ensuring Bluetooth telemetry survives intense gradients. Manufacturers collaborate with coil vendors to co-validate pump placement zones, shortening procurement cycles.

Mid-range 3 T machines remain radiology workhorses, sustaining steady replacement demand. Hospitals upgrading from 1.5 T to 3 T often bundle pump refreshes in the same capital cycle, a pattern vendors exploit by packaging service contracts. Payers in Europe are increasingly reimbursing 7T neuro scans for refractory epilepsy diagnostics, a policy catalyst that will nudge more centers toward ultra-high-field compatible pumps.

By Product Portability: Bedside Flexibility Dominates Preferences

Bedside units captured 60.95% of the MRI-compatible IV infusion pump market share in 2025, as radiology teams value devices that accompany the patient from pre-scan preparation through post-scan observation. Battery life and a lightweight chassis enable seamless handoffs without repriming lines. The MRI-compatible IV infusion pump market continues to tilt toward portability as ASCs and hybrid ORs schedule same-day discharges. Stationary rack systems remain relevant for lengthy neurovascular procedures that utilize multiple drug channels simultaneously. IRadimed’s newest model weighs under 4 kg, one-third lighter than first-generation designs, and incorporates four-channel capability in a single shell.

Technicians cite faster room turnover when pumps clip directly onto detachable poles rather than large gantry mounts. Meanwhile, rack systems integrate with anesthesia workstations, giving anesthesiologists centralized control. Makers respond by offering modular carts, allowing facilities to start with portables and later add docking bays to expand the channel count without requiring new pump purchases.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Lead While ASCs Accelerate Growth

Hospitals accounted for 68.74% of the MRI-compatible IV infusion pump market size in 2025. Teaching facilities emphasize research versatility, so they specify pumps operable at multiple field strengths. Multi-campus health networks negotiate enterprise deals, bundling disposables at fixed margins, driving repeat revenue for manufacturers. ASCs post the fastest 12.79% CAGR because payer policies shift elective spine and joint interventions to outpatient settings. Pump vendors target ASCs with leasing programs that minimize the upfront cash requirement.

Specialty clinics—such as pain, neurology, and oncology—seek portable pumps that integrate with electronic medical record systems for automatic charting. Diagnostic imaging centers, once observers, are piloting on-site sedated pediatrics programs and therefore buying a small fleet of non-magnetic pumps. Research institutes procure the earliest prototypes, providing real-world feedback that informs the development of broader commercial versions.

Geography Analysis

North America retained 44.10% of the MRI-compatible IV infusion pump market size in 2025. The United States drives most placements thanks to early FDA clearances and a concentration of magnet-stocked academic medical centers. Canada’s provincial health systems fund capital grants for intra-operative MRI suites, sustaining replacement cycles. Mexico’s private hospital chains invest in turnkey surgical imaging theaters to attract medical tourists, creating incremental pump demand.Europe remains a mature adopter with stringent, predictable CE-mark pathways. Germany, France, and the United Kingdom favor network-ready pumps that comply with GDPR for device data. Scandinavian countries pilot closed-loop infusion protocols inside 3 T neurosurgical theaters, a model under review by EU health technology assessment bodies. Russia’s neuroscience institutes continue to import ultra-high-field capable pumps despite broader equipment sanctions, sustaining a small but resilient niche.

Asia-Pacific posts the strongest 12.98% CAGR. China’s National Health Commission earmarked funds for county-level MRI expansion, spurring local contract manufacturers to license Western pump IP and reduce import tariffs. India’s government-backed 1.5 T scanner line aspires to halve magnet pricing, indirectly lifting pump affordability. Japan pioneers IoT integration, linking infusion pumps with radiology scheduling systems to auto-populate drug libraries. Southeast Asian markets, led by Thailand and Indonesia, see private hospital groups differentiate premium packages with MRI-guided pain ablation services, fueling pump uptake.

The Middle East invests in flagship transplant centers where high-field MRI supports intra-op vascular mapping. Saudi Arabia’s Vision 2030 hospital projects include hybrid suites pre-wired for non-magnetic pumps. South America advances more slowly; however, Brazil’s top oncology institutes trial AI-assisted 3 T therapy workflows that require pump interoperability, hinting at future scale.

Competitive Landscape

Market Concentration

The MRI-compatible IV infusion pump market shows consolidation. IRadimed retains first-mover credibility by iterating on non-magnetic architecture every two to three years; most recently, the MRidium 3870 cleared in 2025. Baxter leverages its Novum IQ software stack—already managing 1.5 million connected devices—to integrate MRI profiles without requiring the rewriting of hospital formularies. B. Braun competes through its broad portfolio, bundling consumables to secure long-term accounts.

Strategic moves trend toward vertical integration. Fresenius Kabi’s USD 240 million Ivenix acquisition combined IV solutions and intelligent pumps, creating an end-to-end loop of consumables, hardware, and software. ICU Medical partnered with Otsuka in a USD 200 million joint venture to expand bag capacity and secure parenteral nutrition components, insulating against PVC resin shortages. Patent activity rises around sensor-enabled dose confirmation: Conncons secured claims on networked infusion systems that self-verify drug identity before start-of-scan.

Supply chain resilience is a fresh battleground. Component shortages during the pandemic forced several pump lines off the market; vendors now dual-source ASICs and lithium cells. Adoption of nickel-free alloys aims to de-risk raw material price spikes. Vendors extend service intervals and remote diagnostics to lower lifecycle costs, a selling point for budget-constrained ASCs.

MRI - Compatible IV Infusion Pump Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ICU Medical and Otsuka Pharmaceutical Factory announced formation of a USD 200 million joint venture to create one of the largest global IV solutions manufacturing networks. The partnership combines ICU Medical's commercial expertise with Otsuka's manufacturing capabilities to enhance supply chain resilience and accelerate new product development, including PVC-free technologies relevant to MRI applications.

- May 2025: IRadimed Corporation received FDA 510(k) clearance for its MRidium 3870 IV Infusion Pump System, featuring non-magnetic ultrasonic pump motor technology and four-channel capability. The system represents a significant advancement in MRI-compatible infusion technology with enhanced safety features and intuitive touchscreen interface, positioning IRadimed for expanded market penetration when commercial distribution begins in 2026.

- April 2025: ICU Medical announced FDA clearances for its new Plum Solo and Plum Duo precision IV pumps, introducing a new category of infusion devices with advanced safety features. These systems incorporate sophisticated dose error reduction capabilities and represent ICU Medical's strategic focus on precision infusion therapy following the company's portfolio expansion through acquisitions.

- November 2024: GE HealthCare received FDA 510(k) clearance for its SIGNA MAGNUS 3.0T head-only MRI system, featuring innovative asymmetrical gradient coil design for enhanced neuroimaging capabilities. The system's advanced imaging capabilities create new requirements for compatible infusion equipment in neurosurgical and research applications.

Table of Contents for MRI - Compatible IV Infusion Pump Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Burden of Chronic Diseases & MRI Scan Volumes

- 4.2.2Growing MRI-Guided Minimally-Invasive Surgeries

- 4.2.3Advances in Wireless Non-Magnetic Pump Platforms

- 4.2.4Iot-Enabled Closed-Loop MRI Infusion Ecosystems

- 4.2.5Expansion of Intra-Operative MRI Suites

- 4.2.6Hospital Policies Eliminating Long IV-Line Workarounds

- 4.3Market Restraints

- 4.3.1High Capital & Maintenance Costs

- 4.3.2Limited Reimbursement for MRI Disposables

- 4.3.3Non-Ferrous Component Supply Bottlenecks

- 4.3.4MRI-Safety Workforce Training Gaps

- 4.4Technological Outlook

- 4.5Porter’s Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Type

- 5.1.1Non-Magnetic Pump Systems

- 5.1.2Magnetic-Shielded Pump Systems

- 5.1.3Tubing & Disposables

- 5.2By Magnetic-Field Compatibility

- 5.2.1≤1.5 T Systems

- 5.2.23 T Systems

- 5.2.3Ultra-High-Field Systems

- 5.3By Product Portability

- 5.3.1Portable/Bedside Units

- 5.3.2Stationary Rack-mount Units

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Specialty Clinics

- 5.4.3Ambulatory Surgical Centers

- 5.4.4Diagnostic & Imaging Centers

- 5.4.5Research Institutes

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1IRadimed Corp.

- 6.3.2B. Braun SE

- 6.3.3Baxter International Inc.

- 6.3.4Fresenius SE & Co. KGaA

- 6.3.5Becton Dickinson & Co.

- 6.3.6Medtronic plc

- 6.3.7ICU Medical Inc.

- 6.3.8Eitan Medical Ltd.

- 6.3.9Arcomed AG

- 6.3.10Flowonix Medical Inc.

- 6.3.11Smiths Medical (ICU)

- 6.3.12Avanos Medical

- 6.3.13Moog Inc. (Curlin)

- 6.3.14Terumo Corp.

- 6.3.15Nipro Corp.

- 6.3.16Zyno Medical

- 6.3.17Shenzhen Mindray Bio-Medical

- 6.3.18CME-McKinley

- 6.3.19Bayer AG (MEDRAD)

- 6.3.20InfuSystem Holdings

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Type

- Non-Magnetic Pump Systems

- Magnetic-Shielded Pump Systems

- Tubing & Disposables

- Non-Magnetic Pump Systems

- By Magnetic-Field Compatibility

- ≤1.5 T Systems

- 3 T Systems

- Ultra-High-Field Systems

- ≤1.5 T Systems

- By Product Portability

- Portable/Bedside Units

- Stationary Rack-mount Units

- Portable/Bedside Units

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Diagnostic & Imaging Centers

- Research Institutes

- Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's MRI Compatible IV Infusion Pump Systems Baseline Commands Trust

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 381.2 Mn (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 258.0 Mn (2023) | Global Consultancy A | Excludes disposables and uses hardware-only scope with shorter forecast horizon | ||

USD 166.0 Mn (2024) | Trade Journal B | Uses shipment volume x ex-factory prices, omits Asia-Pacific refurb sales, constant-USD conversion absent | ||

USD 500.0 Mn (2023) | Regional Consultancy C | Blends smart pumps for CT/PET and assumes aggressive ASP escalation |