Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

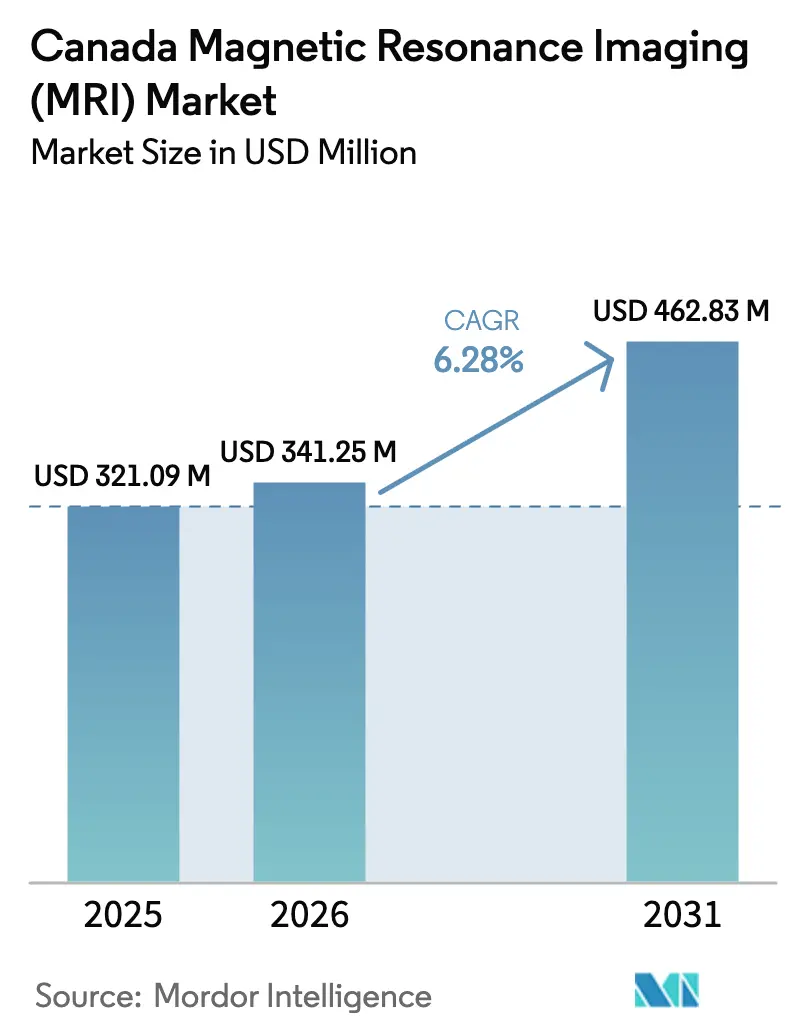

| Base Year Market Size (2025) | USD 321.09 Million |

| Market Size (2026) | USD 341.25 Million |

| Market Size (2031) | USD 462.83 Million |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Magnetic Resonance Imaging (MRI) Market Analysis by Mordor Intelligence

The Canada Magnetic Resonance Imaging (MRI) market size in 2026 is estimated at USD 341.25 million, growing from 2025 value of USD 321.09 million with 2031 projections showing USD 462.83 million, growing at 6.28% CAGR over 2026-2031. Consistent demand for high-field scanners, government programs that cut imaging backlogs, and rapid breakthroughs in portable, helium-free platforms are steering growth patterns. Vendors that integrate quantum-enhanced detectors and machine-learning reconstruction now differentiate on diagnostic speed rather than magnet power alone, while outpatient providers use these capabilities to win volumes once locked inside hospitals. Realignment of the supply base toward domestic magnet fabrication and alternative cooling technologies further reduces procurement risk and broadens geographic participation. Overall, investment in bedside imaging, ultra-high-field research scanners, and AI-enabled workflow tools collectively reinforce a healthy five-year expansion trajectory for the MRI systems market.

Key Report Takeaways

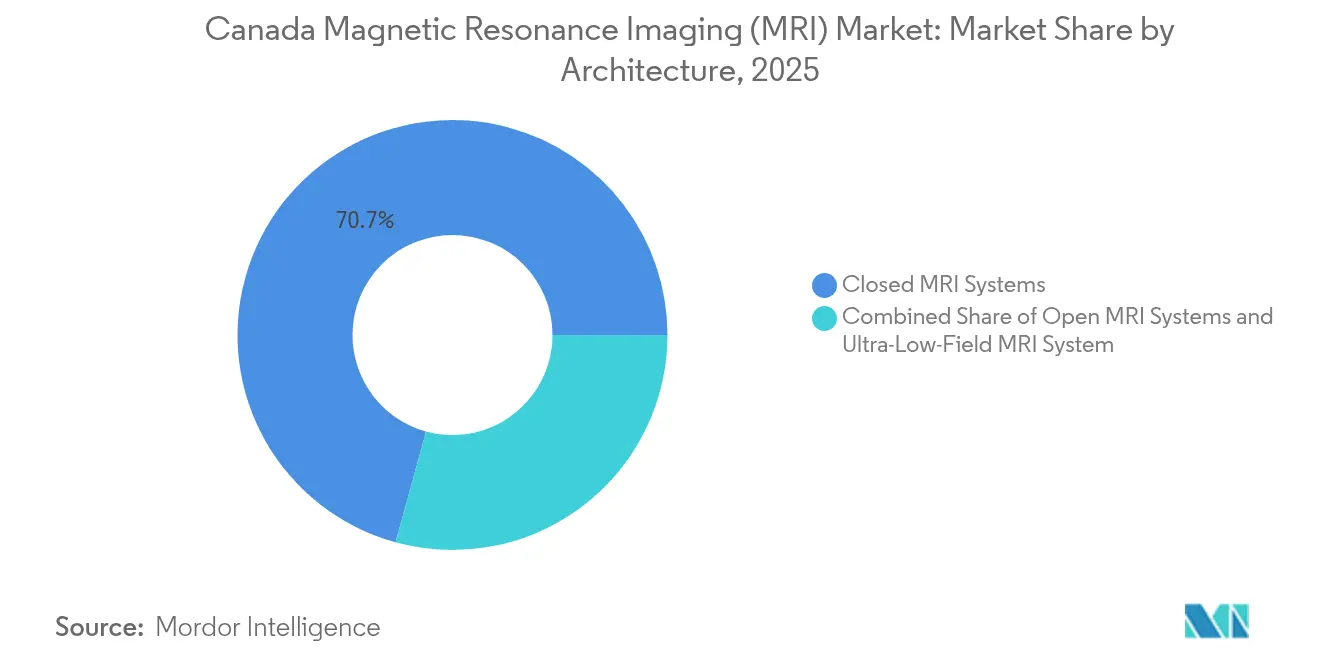

- By architecture, closed scanners held 70.74% of Canada Magnetic Resonance Imaging (MRI) market share in 2025, whereas portable and ultra-low-field devices are forecast to grow at 6.78% CAGR through 2031.

- By field strength, 1.5 T platforms retained 44.76% share of the Canada Magnetic Resonance Imaging (MRI) market size in 2025, while 7 T systems record the fastest 7.12% CAGR to 2031.

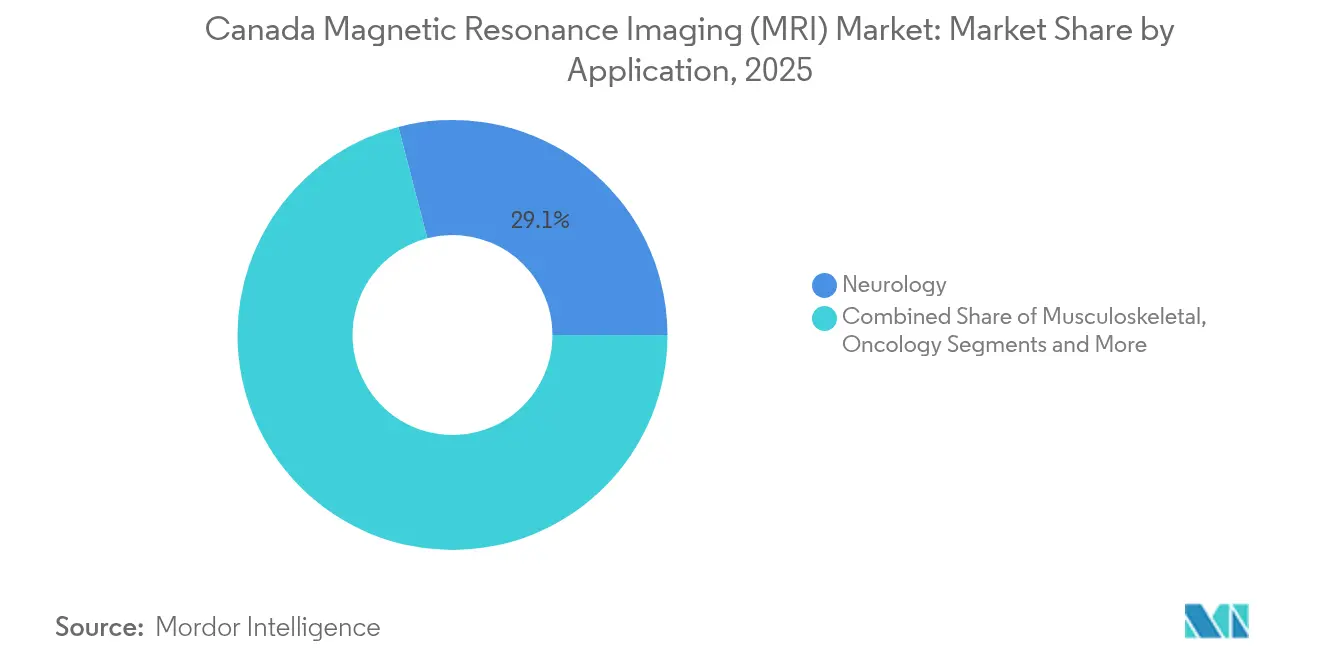

- By application, neurology contributed 29.05% revenue in 2025; oncology is poised for a 7.68% CAGR across the same horizon.

- By end user, hospitals controlled 61.72% share in 2025, yet diagnostic imaging centers expand at 7.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Magnetic Resonance Imaging (MRI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic diseases | +1.2% | Global; greatest in North America and Europe | Long term (≥ 4 years) |

| Aging population and rising imaging referrals | +0.9% | North America, Europe, Japan | Long term (≥ 4 years) |

| Government funding to cut MRI wait-times | +0.8% | Canada, United Kingdom, Australia, Nordics | Medium term (2–4 years) |

| Technological advancement of MRI systems | +1.1% | Global, led by North America and Europe | Medium term (2–4 years) |

| Adoption of ultra-low-field portable MRI | +0.7% | Global; early uptake in United States and Europe | Short term (≤ 2 years) |

| Expansion of privately funded imaging clinics | +0.6% | North America; emerging across Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Diseases

Quantum-hyperpolarized MRI amplifies metabolic signals by 100,000-fold, enabling clinicians to map tumor metabolism without radioactive tracers and detect malignancies that conventional imaging misses [1]Technical University of Munich, “Quantum Technology for Cancer Imaging,” EurekAlert, eurekalert.org. Uptake is strongest in oncology centers treating pancreatic and brain cancers, where early identification drives survival odds and reimbursement aligns with improved outcomes. Regulatory agencies in the United States and Europe are adapting approval pathways to accommodate these quantum-enhanced sequences. Hospitals that adopt the technology report higher referral capture, reinforcing long-run demand for premium scanners in the MRI systems market.

Aging Population & Rising Imaging Referrals

The median age in advanced economies surpasses 40 years, raising the incidence of stroke, osteoarthritis, and neurodegenerative diseases. Portable systems cleared for bedside neurological use shorten door-to-scan times, particularly for stroke triage in emergency units. Point-of-care imaging also supports geriatric care in long-term facilities that lack room for conventional suites. These access gains translate into higher annual scan volumes, a positive demand loop for the MRI systems market.

Government Funding to Cut MRI Wait-Times

Ontario allocated USD 70 million for helium-free systems, while British Columbia set a 50% wait-time reduction target through fresh installations and service contracts. These programs favor vendors offering low-maintenance magnets and long-term uptime guarantees. Framework tenders covering training and service escalate near-term order pipelines and create predictable revenue across the forecast period for the MRI systems market.

Technological Advancement of MRI Systems

Quantum diamond sensors demonstrated spatial resolution down to ten millionths of a meter, opening cellular-level imaging for pharmaceutical research [2]Dominik Bucher, “New Quantum Sensor Elevates Magnetic Resonance Imaging to the Microscopic Level,” Wiley Analytical Science, analyticalscience.wiley.com . At the same time, deep-learning reconstruction slashes scan durations from 45 minutes to five without losing diagnostic value. Vendors package these algorithms inside workflow dashboards that auto-route images to subspecialty radiologists, expanding throughput and boosting the economic case for premium models in the MRI systems market.

Adoption of Ultra-Low-Field Portable MRI

FDA-cleared bedside scanners eliminate magnetic shielding, three-phase power, and helium, lowering installed cost by nearly 70% versus fixed rooms. Clinical studies confirm equivalence for specific neuro exams, strengthening confidence among stroke neurologists and ICU teams. Early adopters cite faster throughput and new revenue streams from rural outreach programs, supporting accelerated penetration of portable devices.

Expansion of Privately Funded Imaging Clinics

Private equity–backed chains keep acquiring community centers and layering AI triage software that maximizes asset utilization. RadNet’s USD 103 million purchase of iCAD aligned mammography AI with its multi-state MRI network, enabling same-day scans and rapid reads for self-pay consumers. Growth of these outpatient networks lifts aggregate system demand and reshapes referral patterns within the MRI systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating cost of MRI suites | −1.8% | Global; most acute in emerging economies | Long term (≥ 4 years) |

| Helium supply constraints and price volatility | −1.1% | Global; variable regional access | Medium term (2–4 years) |

| Shortage of MRI technologists and radiologists | −0.9% | North America, Europe; spreading to Asia-Pacific | Long term (≥ 4 years) |

| Limited public reimbursement for advanced sequences | −0.7% | North America, selective European markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Cost of MRI Suites

Full-service installations exceed USD 1 million and require specialized shielding, uninterruptible power, and trained staff. Scanner density in low-income nations remained below 2 units per million population in 2024, underscoring affordability gaps. Leasing and shared-service models partially offset barriers, but life-cycle costs still deter small hospitals and dampen adoption within the MRI systems market.

Helium Supply Constraints & Price Volatility

Periodic shortages pushed helium prices up more than 50% between 2017 and 2025, creating unplanned downtime for facilities that lack recapture systems. Vendors now prioritize cryogen-light or helium-free magnets; however, premium list prices can delay procurement in budget-sensitive regions. Until supply stabilizes, uncertainty restrains capital allocation for new scanners and upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Reign While Portables Surge

Closed platforms delivered 70.74% revenue in 2025 because surgeons and oncologists rely on their high-signal-to-noise images for complex cases. Facilities appreciate the wide coil ecosystem and mature service networks that keep downtime minimal. Yet the portable wave is undeniable: ultra-low-field units post a 6.78% CAGR as emergency departments, trauma centers, and rural hospitals embrace bedside exams that circumvent transport and queuing delays. Vendors consult architects on shielding-lite rooms that streamline upgrades, helping maintain closed-system dominance in the MRI systems market.

The portable niche unlocks entirely new points of care. Hyperfine’s rolling cart design fits into tight spaces, operates on standard power, and never vents helium. Outcome studies document faster stroke decision-making, which feeds into favorable reimbursement and grants. As clinical evidence expands to musculoskeletal and pediatric use, the segment’s contribution to MRI systems market size will accelerate, though it is unlikely to overtake closed installations in the near term.

By Field Strength: Mid-Range Stability Meets Ultra-High Ambition

At 44.76% share, 1.5 T remains the workhorse because protocols, implants, and radiologist training center on this field. Hospital PACS and contrast media are optimized for its signal profile, preserving a stable installed base across regions. Meanwhile, 7 T delivers the highest growth at 7.12% CAGR, as FDA clearance for clinical neuro scans moves the magnet from research labs into tertiary centers. Price tags hover at USD 10 million, but grant funding and philanthropic gifts help absorb the premium.

3 T models address applications where higher resolution materially alters care pathways, notably epilepsy surgery planning and cardiac tissue characterization. Vendors that supply both mid- and ultra-high-field lines can upsell within their service contracts, ensuring annuity streams even as MRI systems market share remains weighted toward 1.5 T.

By Application: Neurology Leads; Oncology Climbs Fast

Neurology’s 29.05% slice stems from MRI’s unmatched ability to visualize gray-matter architecture, white-matter tracts, and perfusion patterns without ionizing radiation. Functional and diffusion sequences aid diagnosis of stroke, multiple sclerosis, and traumatic injury, sustaining routine use. Oncology, however, clocks a 7.68% CAGR as metabolic and quantitative imaging spread from academic trials to mainstream practice. Hyperpolarized agents now monitor tumor response days after therapy begins, allowing faster protocol adjustments.

Musculoskeletal exams gain momentum from sports injury surveillance, whereas cardiology scans benefit from newer compressed-sensing techniques that eliminate breath holds. Each subfield pushes vendors to refine coils, software, and table ergonomics, enlarging the collective MRI systems market size.

By End User: Hospitals Dominate but Outpatient Centers Accelerate

Hospitals still capture 61.72% spending because they manage trauma pathways, intensive care, and surgical staging that require immediate on-site imaging. Their budgets also absorb the capital and facility modifications necessary for high-field magnets. The MRI systems market nevertheless tilts toward outpatient chains, which post 7.02% CAGR by delivering same-day slots and transparent self-pay prices.

Investors consolidate stand-alone sites into regional brands equipped with standardized scanners and AI decision support. Shorter report turnarounds and patient-friendly scheduling draw referring physicians away from congested hospitals. Mobile fleets further extend reach to employer campuses and assisted-living facilities, broadening the end-user base.

Geography Analysis

Provincial health plans are pushing Canada’s MRI market forward by tying new funding to shorter patient queues. Ontario, for instance, set aside USD 70 million to add scanners, while British Columbia is expanding sites and staff in a bid to halve MRI wait-times by 2030. Because helium supplies are unpredictable, many tenders now specify “helium-free” magnets, a requirement that gives Siemens Magnetom Flow and GE Freelium an edge in competitive bids.

Canada’s publicly funded system creates steady replacement cycles, yet tight budgets mean vendors must prove lower lifetime costs, not just a low sticker price. Regional needs also differ: Ontario and Quebec host the highest scanner counts, whereas western provinces often rely on mobile or shared units to serve patients scattered across large rural areas.

Health Canada’s device rules mirror many FDA standards, so companies with U.S. clearances can enter quickly, though post-market reporting requirements remain uniquely Canadian. Hospitals looking to meet strict wait-time targets are choosing high-throughput models with built-in AI that speeds exams without adding staff. British Columbia, for example, is placing scanners where demand is highest and extending operating hours, favoring vendors that bundle strong service contracts and remote monitoring to keep machines running around the clock.

Competitive Landscape

The MRI systems market hosts a solid core of three multinationals—GE Healthcare, Siemens Healthineers, and Philips—who collectively oversee extensive manufacturing, software, and service engines. Their combined R&D spending tops USD 3 billion annually, fueling rapid iteration in coils, gradient amplifiers, and reconstruction AI. Each has introduced helium-light or zero-boil-off platforms to cushion against commodity swings and align with sustainability mandates. Market entrants such as Canon Medical, United Imaging, and Neusoft Medical Systems differentiate through aggressive pricing, local-language interfaces, and flexible financing.

Strategic cooperation now centers on software ecosystems. Siemens paid USD 150 million to extend U.S. magnet coil production and committed GBP 250 million to a U.K. AI hub, ensuring prompt firmware rollouts and regional service backing [3]Siemens Healthineers Press Office, “Siemens to Expand Oxford Facility,” siemens-healthineers.com . GE bundles its Edison AI platform across modalities, facilitating cross-learning between CT and MRI for unified reporting. Portable specialist Hyperfine leverages a cloud-hosted AI suite that automatically centers brain scans and uploads data for neurologist review, positioning it as a disruptor within the MRI systems market.

M&A remains active: RadNet’s acquisition of iCAD folded breast-imaging AI into its national center network, while Function Health absorbed Ezra to marry preventive screening subscriptions with rapid MRI access. Suppliers also pursue joint research agreements; Philips collaborates with the Technical University of Munich on hyperpolarized agents, accelerating translation to clinic. These maneuvers consolidate capability and lock in service revenues, yet room persists for niche innovators in coils, quiet gradient technology, and photon-counting detection to carve profitable segments.

Canada Magnetic Resonance Imaging (MRI) Industry Leaders

GE Healthcare

FUJIFILM Holdings Corporation

Koninklijke Philips N.V.

Canon (Canon Medical Systems)

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Subtle Medical’s SubtleHD received Health Canada clearance, enabling up to 80% faster MRI scans through image enhancement software.

- April 2023: Kelowna General Hospital (Canada) installed a new MRI scanner under a CAD 30 million (USD 22.6 million) investment to double annual scan capacity.

- February 2023: Georgian Bay General Hospital (Canada) secured CAD 800,000 (USD 604,663) in operating funds to launch onsite MRI services.

Canada Magnetic Resonance Imaging (MRI) Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique used in radiology to produce pictures of the anatomy and the body's physiological processes. These pictures are further used to diagnose and detect the presence of abnormalities in the body. The Canada Magnetic Resonance Imaging (MRI) Market is Segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, Very High Field MRI Systems, and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

| Portable / Ultra-Low-Field MRI Systems |

By Field Strength

| Low-Field (< 0.5 T) |

| Mid-Field (0.5–1.4 T) |

| High-Field (1.5 T) |

| Very-High-Field (3 T) |

| Ultra-High-Field (7 T) |

By Application

| Neurology |

| Oncology |

| Musculoskeletal |

| Cardiology |

| Gastroenterology & Hepatobiliary |

| Other Applications |

By End User

| Hospitals |

| Diagnostic Imaging Centres |

| Others |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| Portable / Ultra-Low-Field MRI Systems | |

| By Field Strength | Low-Field (< 0.5 T) |

| Mid-Field (0.5–1.4 T) | |

| High-Field (1.5 T) | |

| Very-High-Field (3 T) | |

| Ultra-High-Field (7 T) | |

| By Application | Neurology |

| Oncology | |

| Musculoskeletal | |

| Cardiology | |

| Gastroenterology & Hepatobiliary | |

| Other Applications | |

| By End User | Hospitals |

| Diagnostic Imaging Centres | |

| Others |

Key Questions Answered in the Report

What is the current Canada Magnetic Resonance Imaging (MRI) Market size?

The MRI systems market is estimated at USD 341.25 million in 2026 and is forecast to reach USD 462.83 million in 2031.

Who are the key players in Canada Magnetic Resonance Imaging (MRI) Market?

GE Healthcare, FUJIFILM Holdings Corporation, Koninklijke Philips N.V., Canon (Canon Medical Systems) and Siemens Healthineers are the major companies operating in the Canada Magnetic Resonance Imaging (MRI) Market.

Which MRI architecture is growing the fastest?

Portable and ultra-low-field devices are projected to grow at 6.78% CAGR through 2031.

Why are ultra-high-field 7 T scanners gaining attention?

7 T platforms deliver superior neuro-vascular resolution and are expanding from research settings into clinical use, driving a 7.12% CAGR.

Page last updated on: