E-bike Motor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

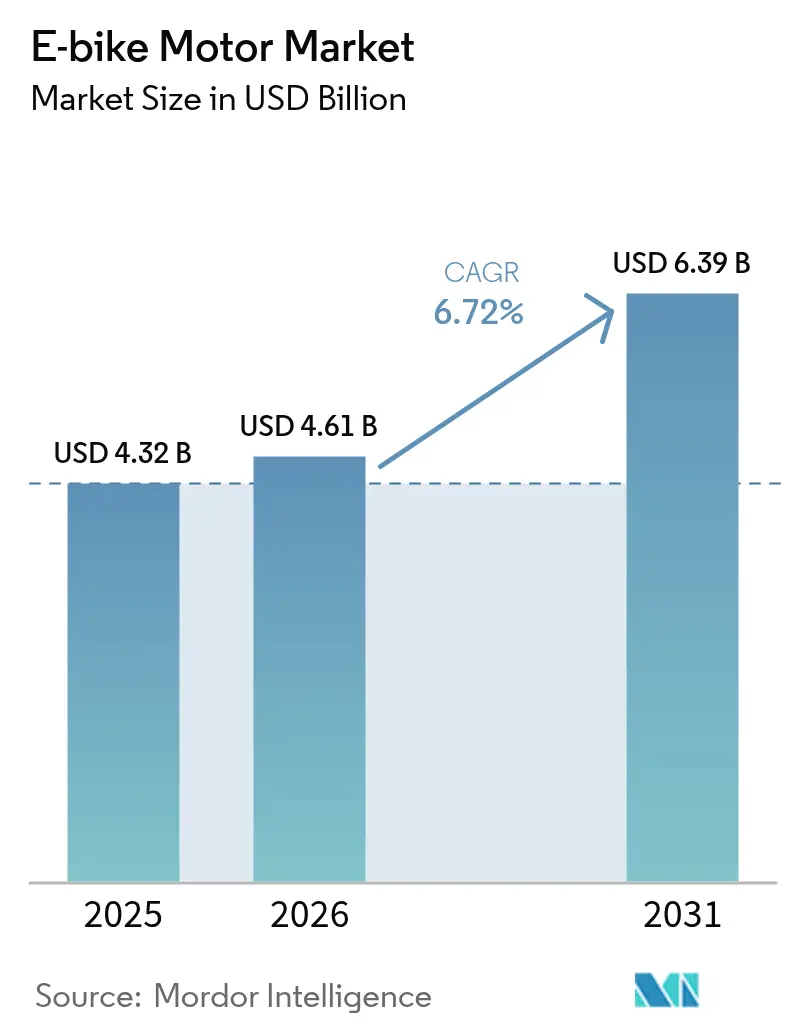

| Market Size (2026) | USD 4.61 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-bike Motor Market Analysis by Mordor Intelligence

The e-bike motor market size was valued at USD 4.32 billion in 2025 and estimated to grow from USD 4.61 billion in 2026 to reach USD 6.39 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). Demand accelerates as cities tighten carbon-reduction mandates, logistics firms electrify fleets, and OEMs roll out software-defined drive units. The e-bike motor market benefits from falling battery prices, yet faces margin pressure from rare-earth magnet volatility that prompts suppliers to explore iron-nitride and ferrite alternatives. Intensifying consolidation—the Yamaha-Brose deal and Bosch’s expanding smart-system portfolio—signals a shift toward vertically integrated offerings that blend hardware with over-the-air software. Asia-Pacific remains the primary production hub, but North America’s appetite for high-power, throttle-enabled models drives fresh investment in local assembly lines.

Key Report Takeaways

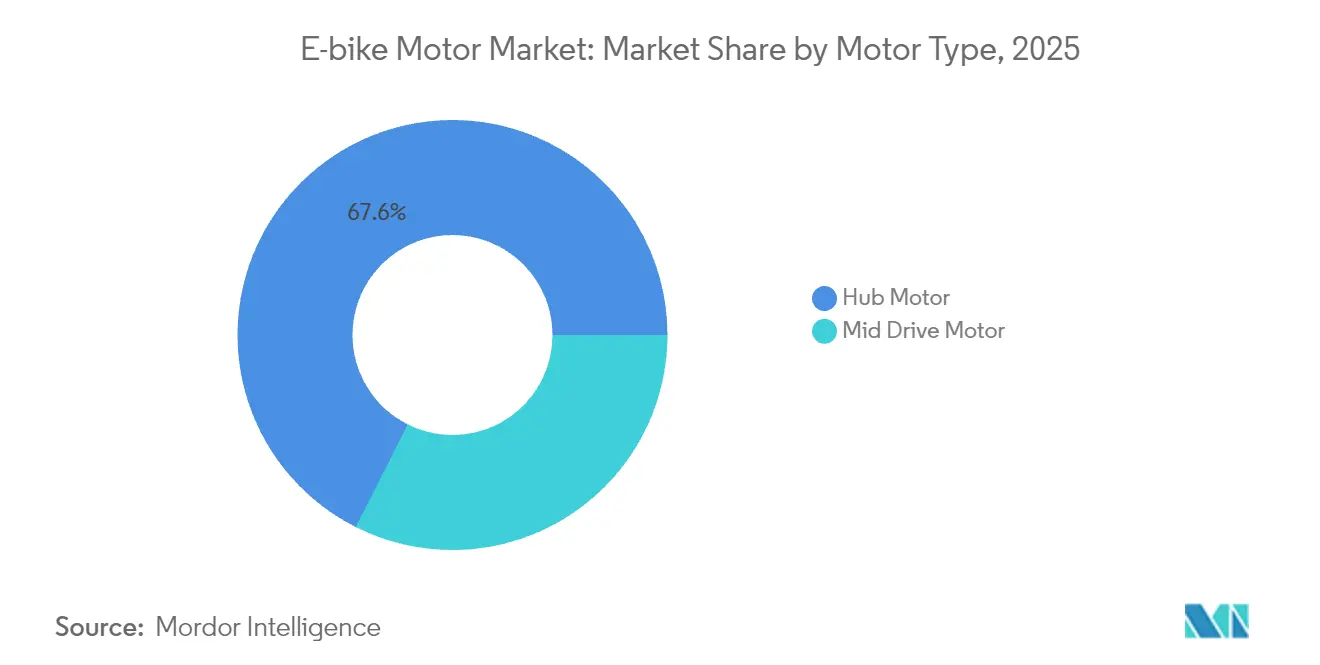

- By motor type, hub systems held 67.58% e-bike motor market share in 2025, whereas mid-drive systems are on track for an 8.36% CAGR through 2031.

- By e-bike category, urban models captured 42.86% of the e-bike motor market size in 2025, while e-mountain bikes are projected to post an 8.02% CAGR to 2031.

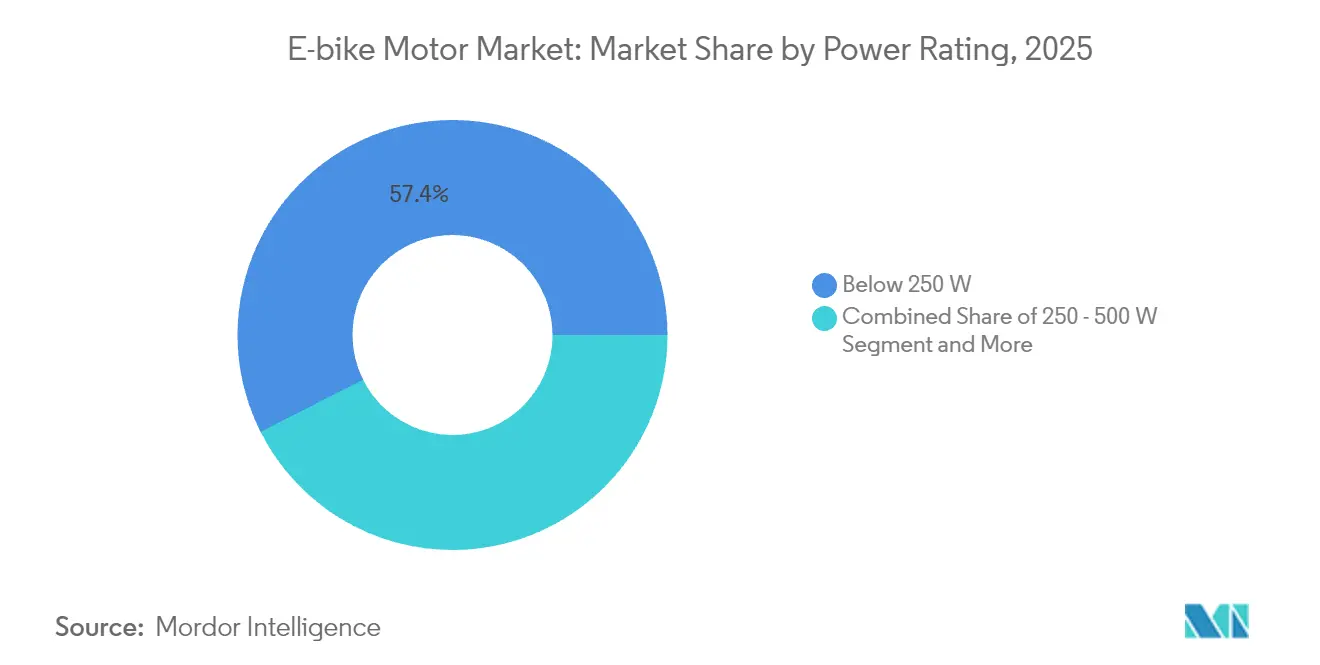

- By power rating, sub-250 W units commanded 57.42% share of the e-bike motor market size in 2025; in contrast, motors above 500 W are expanding at an 8.66% CAGR.

- By sales channel, OEM factory-fit installations represented 64.05% share in 2025, but the aftermarket is forecast to register a 9.18% CAGR over the outlook period.

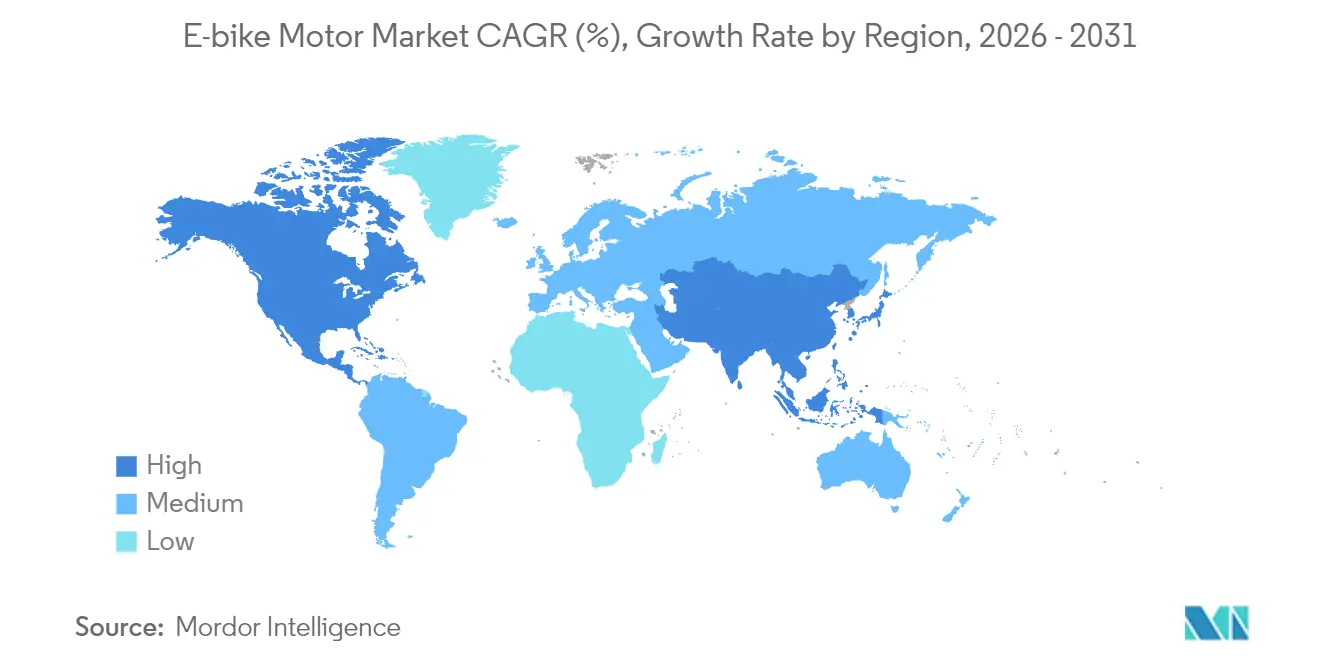

- By geography, Asia-Pacific dominated with a 78.05% share in 2025, whereas North America is expected to grow at a 9.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-bike Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring Urban-Commuter Uptake | +1.8% | North America, Europe | Medium term (2-4 years) |

| Stricter EU and China CO₂ Targets | +1.2% | Europe, China | Long term (≥ 4 years) |

| OEM Push for Smart Integrated Systems | +1.1% | North America, Europe | Medium term (2-4 years) |

| Electrification of Delivery Fleets | +0.9% | Global urban centers | Short term (≤ 2 years) |

| Venture Funding into Mid-Drive Specialists | +0.7% | North America, Europe | Short term (≤ 2 years) |

| Magnet-Material Breakthroughs | +0.6% | Global hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Urban-Commuter Uptake

Corporate bike-leasing programs fuel predictable, bulk demand that raises minimum quality thresholds for motor suppliers. Tax incentives lower end-user costs by up to 40%, channeling consumer preference toward premium drive units with onboard connectivity. As leasing spreads to France and the Nordics, the e-bike motor market secures an annuity-like volume stream anchored by fleet replacement cycles of three to four years. Motor makers leverage this stability to justify higher R&D outlays, especially for AI-based diagnostics that cut downtime. The growth of commuter e-bike lanes in major cities further reinforces baseline demand.

Stricter EU and China CO₂ Targets

Revised European vehicle-emission rules and China’s GB 17761-2024 standard press suppliers to maximize efficiency per kilogram, rather than peak wattage. Bosch’s magnesium-housing Performance Line CX Gen 5 trims 100 g in weight yet maintains 85 Nm torque[1]“Performance Line CX,”, Bosch eBike Systems, bosch-ebike.com. China now mandates embedded battery-management systems, anti-tamper hardware, and satellite positioning, rewarding firms with advanced software stacks and penalizing low-end assemblers. These rulebooks also accelerate the industry’s shift from lead-acid to lithium packs, cementing demand for compatible motor electronics. Compliance costs rise, but early movers gain a head start and access to high-regulation markets, reinforcing their brand equity in the e-bike motor market.

OEM Push for Smart Integrated Systems

Bike brands now specify drive units, batteries, displays, and firmware as a single package to streamline warranty and service. Bosch’s Smart System integrates over-the-air theft protection, auto-shift, and AI route planning, and its eShift interface now interoperates with Shimano and TRP drivetrains. Yamaha’s pending acquisition of Brose’s e-bike division deepens its European engineering bench, positioning it to deliver fully calibrated powertrains to OEM partners. Integration raises switching costs for brands, strengthening ecosystem lock-in and cementing recurring revenue streams from updates and digital services within the e-bike motor market.

Electrification of Delivery Fleets

Parcel and food-delivery operators adopt cargo e-bikes to skirt congestion charges and cut emissions. Fleet buyers value duty-cycle resilience, waterproof connectors, and quick-swap batteries, reshaping motor design priorities toward torque consistency and thermal management. Because commercial riders average six to eight charge cycles per week—triple that of commuters—motors must endure higher load spectra. Volume contracts from logistics firms create forward visibility that underwrites plant expansions in Poland, Vietnam, and Mexico, insulating global supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Motor–Battery Cost | -1.4% | Global | Short term (≤ 2 years) |

| Dependence on NdFeB Magnets | -0.8% | Global | Medium term (2-4 years) |

| Fire-Safety Recalls and Insurance Hikes | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Speed-Cap Policy Divergence | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dependence on NdFeB Magnets

China processes roughly 85% of global rare-earth output, leaving motor OEMs vulnerable to export restrictions and spot-price spikes[2]“Rare Earths Statistics and Information,”, U.S. Geological Survey, usgs.gov. Setting up processing facilities beyond China's borders demands years of capital investment and environmental approvals, extending the period of vulnerability. This challenge is compounded by the complexities of navigating regulatory frameworks and securing sustainable supply chains. As the e-bike motor market grapples with margin risks linked to magnet supply fluctuations, it awaits the scaling of iron-nitride or ferrite alternatives, which could provide a more stable and cost-effective solution in the long term.

Speed-Cap Policy Divergence

Global standards vary widely: the EU caps assistance at 25 km/h and 250 W continuous, while many U.S. states allow 750 W motors with a throttle up to 28 mph. Such fragmentation obliges brands to maintain multiple SKUs, complicating inventory and homologation. Platform launches slow as engineering teams juggle disparate firmware, connectors, and compliance paperwork, muting the otherwise bullish e-bike motor market trajectory in certain regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Mid-Drive Momentum

Hub motors retained a 67.58% e-bike motor market share in 2025, underpinned by low cost, plug-and-play installation, and widespread availability. Yet mid-drive units, projected to register an 8.36% CAGR, are reshaping premium categories through improved weight distribution and drivetrain synergy. Hub innovators answer back with features such as clutch-free coasting and sealed multi-speed gearboxes, prolonging their relevance in budget city bikes.

Shifts in component sourcing underscore the trajectory. Automotive-grade suppliers bring in IP-protected torque-sensor stacks and ASIC-based controllers that elevate mid-drive efficiency. Firmware updates enable user-selectable power maps, furthering personalization. While hub systems will dominate volume for entry-level and shared-mobility fleets, margin-rich mid-drive platforms will capture outsized profit pools, reinforcing the two-tier structure within the e-bike motor market.

By E-Bike Type: Urban Core and Mountain Surge

Urban commuting bikes accounted for 42.86% of sales in 2025 and remain the anchor of the e-bike motor market size through mid-decade. City authorities add protected lanes and extend employer tax perks, magnifying baseline demand. At the same time, e-MTB shipments exhibit the fastest 8.02% CAGR as high-traction torque and adaptive suspension merge with 29-inch chassis standards. Motors designed for mountain bikes integrate barometric sensors to modulate power based on gradient, improving battery utilization. Fleet urban models emphasize weather sealing and predictive maintenance alerts that cut downtime for couriers.

The two segments differ on price elasticity; e-MTBs command ASPs approximately 1.7 times that of commuter units, justifying richer motor features. Urban platforms drive scale production, pushing down per-unit electronics cost, which then trickles into performance-oriented e-MTBs. This virtuous loop helps sustain volume growth across both segments, reinforcing the the overall robustness of the e-bike motor market.

By Power Rating: Regulatory Logic

Sub-250 W motors led with 57.42% share in 2025 because they comply with EU pedelec rules that grant access to bike lanes without registration. The e-bike motor market size for this band is poised to grow steadily on the back of commuter adoption in dense cities. Conversely, motors exceeding 500 W will chart an 8.66% CAGR, fueled by North American demand for throttle-enabled Class 3 bikes. Mid-power (250–500 W) remains a bridging category favored in Asia-Pacific, where regional standards often mirror European wattage limits but allow brief peak outputs.

As policymakers revisit definitions of light-electric vehicles, suppliers develop modular controllers that let OEMs software-cap power for compliant export, lowering SKU proliferation. Battery pairing decisions revolve around duty cycle: high-power motors need larger packs, which in turn invite advanced thermal controls. Such cross-component optimization underscores the integrated nature of the e-bike motor market.

By Sales Channel: OEM First, Aftermarket Next

Factory-fit installations represented 64.05% of the market in 2025, reflecting brand strategies to build purpose-designed frames around compact mid-drive housings. Warranty bundling and telemetry-driven service plans enhance OEM stickiness. The aftermarket, while smaller, is projected for a 9.18% CAGR as consumers retrofit legacy frames. Conversion-kit suppliers introduce quick-mount torque arms and smartphone-calibrated controllers to simplify do-it-yourself projects.

Aftermarket traction is most substantial in developing markets where disposable incomes lag but repair culture thrives. Kits priced below USD 350 democratize electrification, though they often lack advanced safeguards in OEM units. Regulators may soon impose tighter safety checks, nudging kit vendors toward certified battery–motor bundles, effectively professionalizing the conversion niche within the e-bike motor market.

Geography Analysis

Asia-Pacific dominated with 78.05% share in 2025 due to China’s end-to-end supply chain that spans rare-earth mining to final assembly. Chinese electric two-wheeler exports exceeded CNY 40 billion (USD 5.5 billion) in 2024, underscoring regional capacity. Japan contributes premium drivetrain engineering, and India emerges as a fast-growing assembly node via joint ventures such as Musashi Seimitsu’s partnership for integrated powertrains. Regional incentives—reduced VAT and urban congestion levies—bolster domestic ownership and export competitiveness, solidifying Asia-Pacific as the cornerstone of the e-bike motor market.

North America exhibits the fastest 9.14% CAGR through 2031 as consumer preferences tilt toward high-power, throttle-enabled models. Federal stimulus for domestic manufacturing and state-level rebates spur capacity additions like eBliss Global’s New York plant. Regulatory heterogeneity across states creates niches for adaptable firmware and modular controller designs. Corporate fleet conversions and expanding trail access further diversify demand profiles, enhancing regional significance to the e-bike motor market.

Europe presents a mature but innovation-rich arena. Although unit sales tapered in 2024 amid macro headwinds, the continent remains technology-leading due to rigorous EN 15194 certification requirements. German leasing programs expand across the bloc, funneling steady orders for high-spec drive systems. Supply-chain localization efforts, notably battery-cell plants in Hungary and drive-unit factories in Poland, aim to offset Asian dependencies. As policymakers debate speed-cap harmonization, European OEMs refine motor efficiency within 250 W boundaries, reinforcing their premium brand cachet in the global e-bike motor market.

Competitive Landscape

The e-bike motor market features moderate concentration; Bosch, Shimano, Yamaha, Bafang, and Brose dominate through vertically integrated systems that bundle hardware with telematics. Yamaha’s acquisition of Brose’s drive unit arm intensifies competitive pressure by fusing Brose’s European OEM ties with Yamaha’s manufacturing reach. Bosch continues to strengthen ecosystem lock-in via over-the-air features, AI range predictors, and theft-tracking services, deepening customer lifetime value.

Automotive suppliers such as ZF and SEG Automotive enter with scale advantages in power electronics and drivetrain calibration, challenging incumbents on cost and reliability. DJI’s Avinox launch signals entry by consumer-electronics firms leveraging sensor know-how and UX design. These new contenders push incumbents to accelerate firmware roadmaps and upgrade post-purchase digital services. Meanwhile, mid-drive start-ups court niche segments—cargo logistics and high-end e-MTB—offering bespoke torque profiles and automatic gearboxes, further fragmenting the e-bike motor market.

Strategic partnerships permeate the landscape. Bosch aligns with Shimano and TRP for cross-brand eShift solutions, enhancing compatibility and expanding addressable OEM pools. ZF licenses motor IP to frame makers under private-label deals, while Bafang partners with Tier-1 bearing suppliers to improve durability. Consolidation is likely to continue as software becomes the chief differentiator and capital requirements rise, suggesting the e-bike motor market heads toward an oligopolistic equilibrium.

E-bike Motor Industry Leaders

Robert Bosch GmbH

Yamaha Motor Co., Ltd

Shimano Inc

Bafang Electric (Suzhou) Co., Ltd.

Mahle GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: With the backing of state tax credits, eBliss Global has invested USD 4.1 million to establish a manufacturing site in New York. This facility is designed to produce up to 15,000 units annually, aiming to enhance the company's production capabilities and meet growing market demand.

- June 2025: At Eurobike 2025, Bafang introduced the M430 Drive System, a professional-grade solution for cargo bikes, boasting a total payload capacity of 300kg. This innovative drive system is designed to meet the growing demand for efficient and reliable cargo transportation, catering to both commercial and personal use. The M430 Drive System combines advanced technology with robust engineering, ensuring optimal performance and durability under heavy loads.

Global E-bike Motor Market Report Scope

In an electric bicycle, the E-Bike Drive Unit combines key components to provide propulsion. Typically, this unit encompasses a motor, battery, controller, and sensors. Together, they deliver either pedal-assisted or fully electric power to the wheels, enhancing the rider's experience and promoting efficient, eco-friendly transportation. Additionally, the motor pack features a gear-reduction system. E-bike motors, available in various types like hub and mid-drive motors, are powered by rechargeable batteries.

The e-bike motor market is segmented by motor type, e-bike type, capacity type, and geography. By motor type, the market is segmented into Mid-drive and hub motor. By e-bike type, the market is segmented into urban, E-mountain/E-MTB, and E-cargo. By capacity/output type, the market is segmented into below 250W, 250W- 500W, and 500W and above. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The report offers the market size in value (USD) and forecasts for all the above segments.

| Hub Motor |

| Mid-drive Motor |

| Urban / City |

| E-Mountain / EMTB |

| E-Cargo |

| Below 250 W |

| 250 - 500 W |

| Above 500 W |

| OEM / Factory-fit |

| Aftermarket / Retrofit |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Motor Type | Hub Motor | |

| Mid-drive Motor | ||

| By E-Bike Type | Urban / City | |

| E-Mountain / EMTB | ||

| E-Cargo | ||

| By Power Rating | Below 250 W | |

| 250 - 500 W | ||

| Above 500 W | ||

| By Sales Channel | OEM / Factory-fit | |

| Aftermarket / Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the E-bike Motor Market?

The e-bike motor market size stands at USD 4.61 billion in 2026 and is forecast to reach USD 6.39 billion by 2031, translating into a 6.72% CAGR.

Which motor type is gaining share the fastest?

Mid-drive systems are projected to grow at an 8.36% CAGR through 2031.

Why are rare-earth magnets a risk factor?

China controls 85% of processing capacity, exposing manufacturers to price spikes and supply disruptions

Which region is expanding the quickest?

North America shows the highest regional CAGR at 9.14% due to demand for high-power, throttle-enabled models.

Page last updated on: