Molecular Quality Controls Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

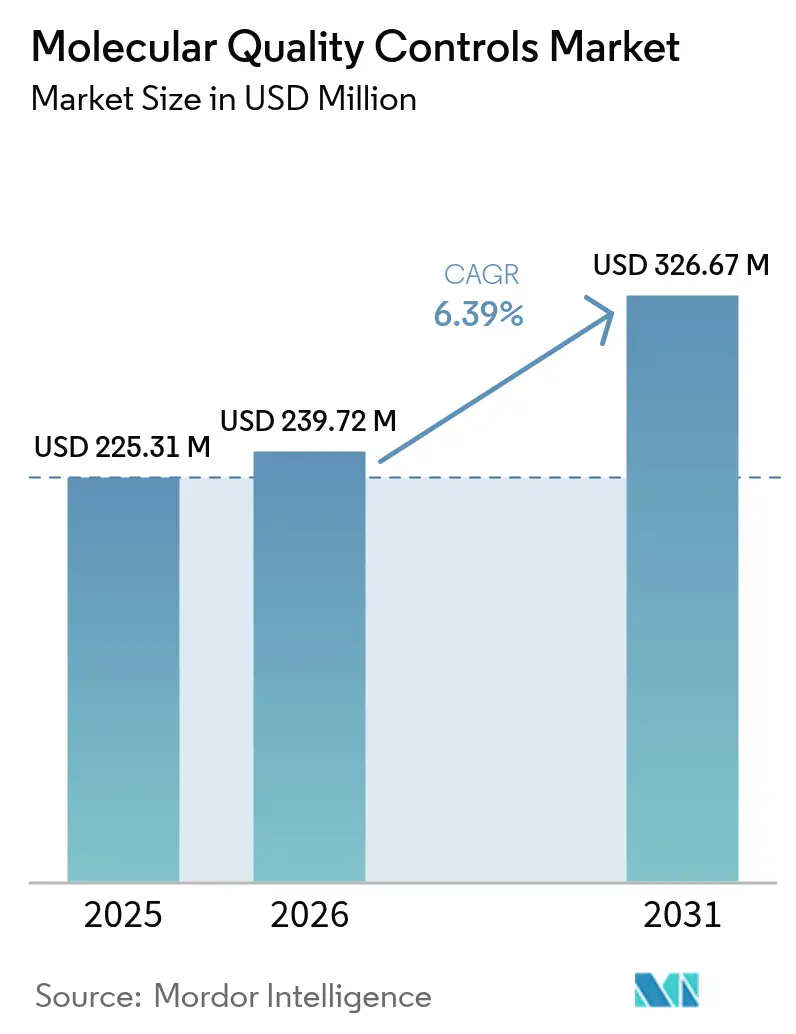

| Market Size (2026) | USD 239.72 Million |

| Market Size (2031) | USD 326.67 Million |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

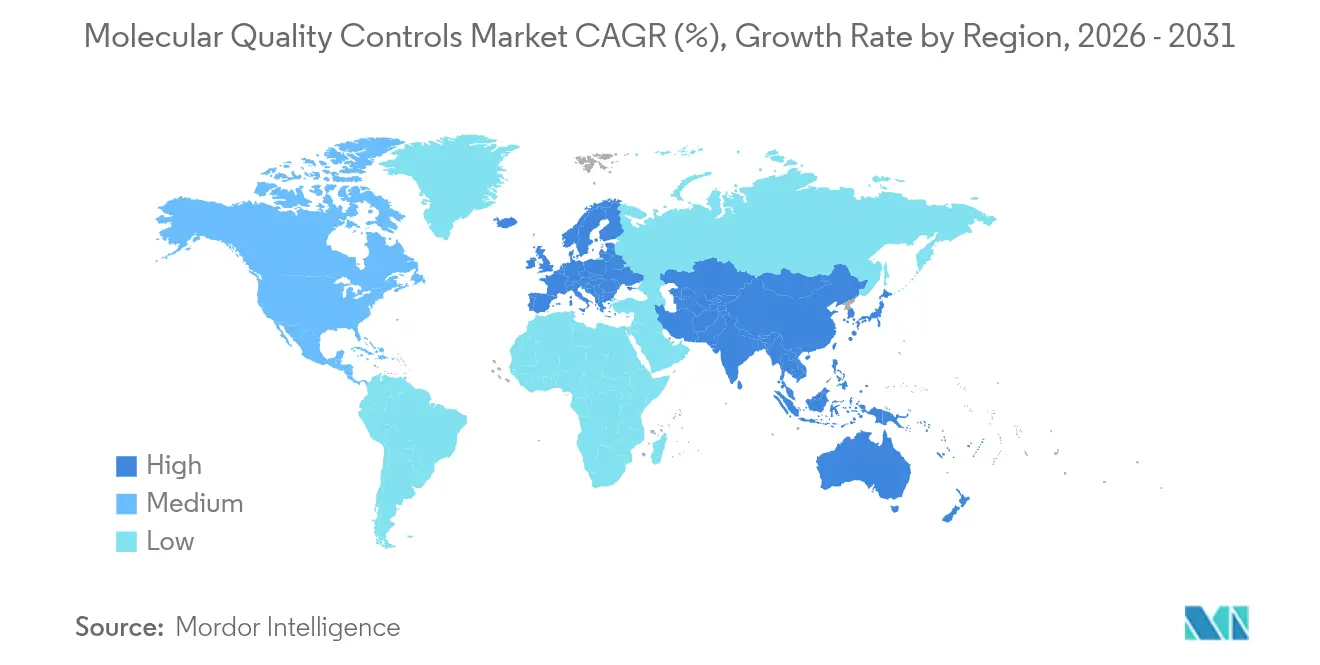

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

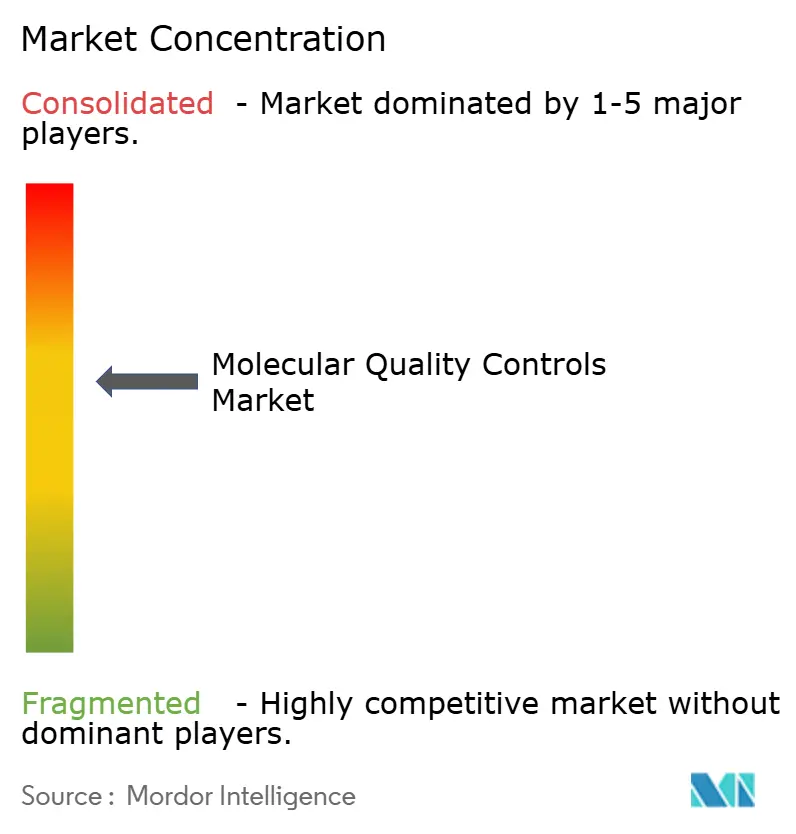

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Molecular Quality Controls Market Analysis by Mordor Intelligence

Molecular Quality Controls Market size in 2026 is estimated at USD 239.72 million, growing from 2025 value of USD 225.31 million with 2031 projections showing USD 326.67 million, growing at 6.39% CAGR over 2026-2031. Robust growth rests on three forces: the United States Food and Drug Administration’s (FDA) Laboratory Developed Tests (LDT) Final Rule, the global push for ISO 15189:2022 accreditation, and laboratories’ rapid shift from single-analyte to multiplex and next-generation sequencing (NGS) testing. Independent, third-party controls remain the default tool for demonstrating analytic accuracy, while instrument-specific controls gain momentum as laboratories integrate automation and middleware.[1]Source: U.S. Food and Drug Administration, “FDA Takes Action Aimed at Helping to Ensure the Safety and Effectiveness of Laboratory Developed Tests,” fda.gov Demand is reinforced by oncology’s expanding need for comprehensive genomic profiling, rising external-quality assessment (EQA) mandates, and the clinical move toward point-of-care molecular platforms that must still meet centralized quality standards. Conversely, high per-run control costs, supply bottlenecks for rare pathogen reference materials, and overlapping regulatory pathways temper near-term spending.

Key Report Takeaways

- By product type, independent controls led with 57.52% of molecular quality controls market share in 2025; instrument-specific controls are projected to post the fastest 7.12% CAGR through 2031.

- By technology, PCR-based controls retained 69.05% revenue share in 2025, while NGS-based controls expand at a 6.89% CAGR to 2031.

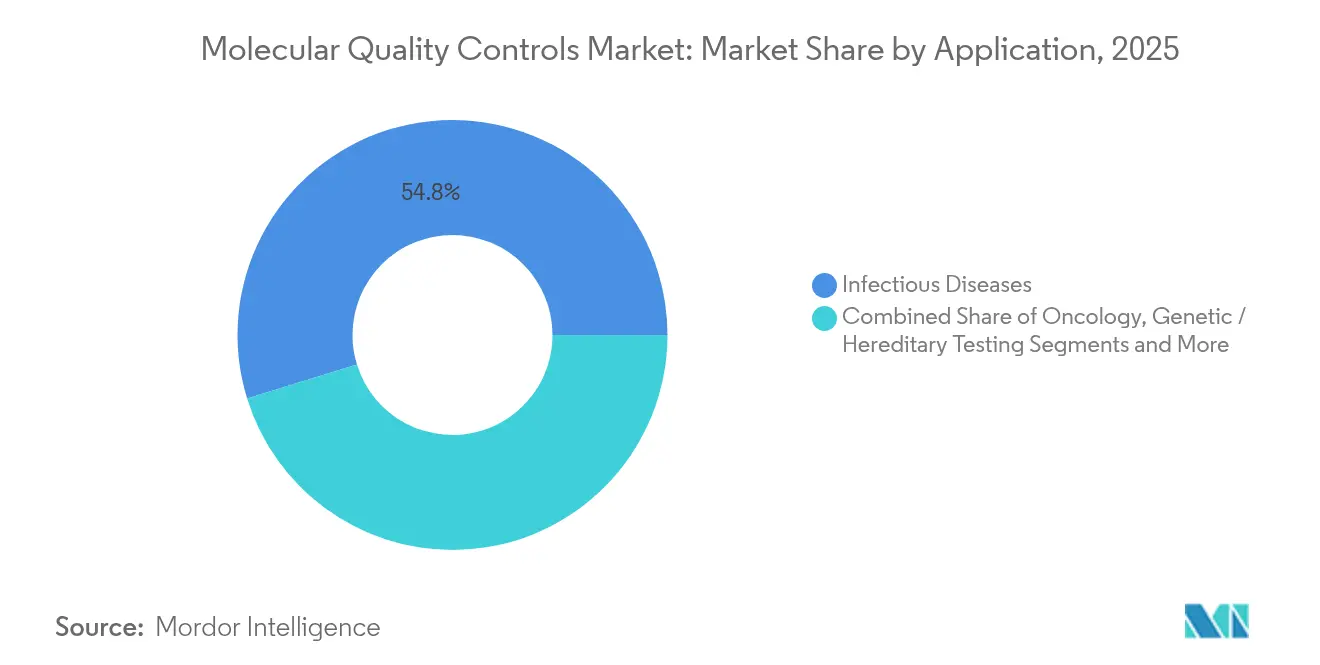

- By application, infectious diseases accounted for 54.78% of the molecular quality controls market size in 2025; oncology testing is advancing at an 7.56% CAGR through 2031.

- By end user, clinical laboratories held 45.86% of demand in 2025; IVD manufacturers and CROs record the highest 7.31% CAGR to 2031.

- By geography, North America captured 37.82% revenue in 2025; Asia-Pacific is the fastest-growing region at an 7.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Molecular Quality Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Test-Volume in Molecular Diagnostics | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing Adoption of 3rd-Party QC For ISO 15189 Accreditation | +1.5% | Global, particularly emerging markets in APAC | Long term (≥ 4 years) |

| Growing Incidence of Cancer and Genetic Disorders | +1.2% | Global, with higher impact in developed regions | Long term (≥ 4 years) |

| Stricter External-Quality Assessment (EQA) Mandates | +1.0% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Shift To Digital Multiplex QC Panels | +0.8% | North America & Europe, early adoption in APAC | Medium term (2-4 years) |

| Consolidation of Labs Driving Enterprise QC Data-Integration | +0.5% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Test-Volume in Molecular Diagnostics

Diagnostic laboratories processed unprecedented volumes during the COVID-19 public-health emergency, with the FDA authorizing 291 molecular assays, demonstrating the scalability of high-throughput platforms.[2]Source: U.S. Department of Health and Human Services, “Testing & Diagnostics,” hhs.gov Post-pandemic, volume remains elevated as labs extend molecular testing to pharmacogenomics, antimicrobial resistance surveillance, and hereditary cancer panels. Each multiplex target adds validation layers, compelling laboratories to rely on robust third-party controls to avoid analytical drift. Digital QC dashboards integrated with laboratory information systems have trimmed manual verification steps by 62.5%, underscoring technology’s role in managing rising workloads.

Increasing Adoption of Third-Party QC for ISO 15189 Accreditation

ISO 15189:2022 raises the bar for risk management and for point-of-care integration, pushing laboratories toward externally sourced controls that demonstrate traceability and independence. The first U.S. accreditation under the new version signaled an early inflection toward global compliance momentum. Laboratories have three years to transition, anchoring sustained demand for molecular quality controls market products.

Growing Incidence of Cancer and Genetic Disorders

Cancer incidence rates continue rising globally, with molecular testing becoming essential for precision oncology treatment decisions. NGS oncology panels interrogate hundreds of genes, copy-number events, and fusions, each demanding stringent controls for variant detection accuracy. Liquid-biopsy assays amplify complexity by requiring ultra-low-frequency variant detection, escalating the need for high-sensitivity synthetic controls. Similarly, hereditary disease panels covering 100 plus actionable genes require variant-specific controls to support correct clinical reporting.

Stricter External-Quality Assessment Mandates

The 2024 CLIA update introduced 23 new molecular proficiency tests and narrowed allowable error margins by 33.3%, compelling U.S. laboratories to upgrade QC procedures. The longitudinal analysis of 20 years of EQA schemes for PCR/NAAT-based bacterial detection reveals declining in-house assay usage and increased adoption of commercial quality controls. Parallel schemes in Europe under IVDR and ISO 15189 require regular proficiency participation, cementing a compliance-driven spending channel within the molecular quality controls market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Run Cost of Molecular QC Materials | -1.2% | Global, particularly cost-sensitive emerging markets | Short term (≤ 2 years) |

| Complex Multi-Agency Regulatory Pathway | -0.8% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Unfavourable Reimbursement for Confirmatory Molecular Tests | -0.6% | North America & Europe | Long term (≥ 4 years) |

| Supply-Chain Fragility for Rare Pathogen Reference Materials | -0.4% | Global, with acute impact during outbreaks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Per-Run Cost of Molecular QC Materials

The economics of molecular quality controls present significant challenges for laboratories operating under constrained budgets, particularly as test complexity increases. NGS assays cut the overall cost of patient care compared with sequential PCR yet still demand expensive multi-analyte controls that can account for 4–7% of per-sample cost, a margin non-trivial to small laboratories. Fixed control costs scale poorly when test volumes are modest, prompting labs to stretch replacement intervals and potentially compromise analytical robustness.

Complex Multi-Agency Regulatory Pathway

The regulatory landscape for molecular quality controls involves multiple agencies with overlapping jurisdictions, creating compliance complexity that extends product development timelines and increases costs. The FDA’s four-year phase-in of the LDT Final Rule requires device-like quality systems, medical-device reporting, and in many cases premarket review.[3]Source: U.S. Food and Drug Administration, “Medical Devices; Laboratory Developed Tests,” fda.gov Parallel IVDR conformity assessments in Europe oblige manufacturers to address multiple audit bodies, lengthening product launches and raising compliance costs, especially for small suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Independent Controls Drive Market Leadership

Independent controls dominated with a 57.52% molecular quality controls market share in 2025, reflecting laboratories’ preference for vendor-neutral verification tools that satisfy ISO 15189 documentation requirements and mitigate platform bias. Bio-Rad’s Unity Data Management network, active in 38,000 labs, illustrates how third-party controls aggregate peer comparisons to detect systemic deviations quickly. Independent products span multi-analyte panels for respiratory pathogens to custom oncology variants, allowing labs to standardize across diverse instruments.

Instrument-specific controls, though smaller, are projected to post a 7.12% CAGR through 2031 as automation and integrated sample-to-answer platforms expand. Manufacturer-tuned stability and lot-to-lot consistency save validation time, a decisive advantage in high-throughput environments. Yet vendor-lock fears linger, keeping independent controls the reference option for proficiency schemes. The molecular quality controls market therefore gravitates toward a dual-sourcing model in which labs deploy independent controls for accreditation while relying on instrument-specific materials for daily workflow continuity.

By Technology: PCR Dominance Faces NGS Disruption

PCR-based products retained 69.05% revenue in 2025, anchored by high-volume infectious disease testing where turnaround time and cost trump breadth. These controls typically contain stabilized viral or bacterial nucleic acids encapsulated in non-infectious particles for biosafety.

NGS-based controls, however, are advancing at a 6.89% CAGR, reflecting oncology’s shift toward multi-gene panels and the rising use of comprehensive genomic profiling in hereditary disorders. Sample-preparation QC kits assess library complexity, fragment size, and adapter ligation efficiency before sequencing, reducing costly reruns. The molecular quality controls market size for NGS panels is poised to expand as reimbursement improves and sequencing costs continue to decline. Isothermal amplification controls occupy niche use cases such as point-of-care STI testing, where rapid qualitative answers suffice.

By Application: Infectious Diseases Leadership Under Oncology Pressure

Infectious-disease testing held 54.78% of the molecular quality controls market size in 2025, supported by continuous respiratory virus surveillance and mandated EQA participation for notifiable pathogens. Multi-target panels covering influenza, RSV, and SARS-CoV-2 remain baseline requirements for clinical labs.

Oncology, forecast to grow at an 7.56% CAGR, is narrowing the gap. Liquid-biopsy innovation and adaptive cancer trials necessitate quantitative controls capable of detecting variants at allele frequencies below 0.5%. Laboratories also bundle QC data into electronic submission packages for U.S. FDA companion-diagnostic approvals, a procedural reality lifting control volumes per assay. Genetic and hereditary disease testing gains momentum through expanded carrier screens and pharmacogenomic guidance, propelling broader adoption of multiplex controls with calibrated variant distributions.

By End-User: IVD Manufacturers Accelerate Enterprise Integration

Clinical laboratories commanded 45.86% revenue in 2025, yet purchasing dynamics increasingly shift upstream. IVD manufacturers and CROs, growing at 7.31% CAGR, bundle controls into assay development pipelines to streamline FDA or CE marking dossiers. Control consumption spikes during validation, bridging analytical sensitivity, specificity, and limit-of-detection studies.

Enterprise consolidation also moves QC selection to central corporate teams, prioritizing platforms offering data-integration APIs and automated lot-tracking. For hospital networks, middleware linking QC metrics with inventory data curtails wastage, giving suppliers that provide cloud dashboards a competitive edge. Academic medical centers remain important adopters, particularly where translational research creates novel assay designs demanding bespoke QC materials.

Geography Analysis

North America led with 37.82% revenue in 2025, buoyed by strong reimbursement, high test volume, and the FDA’s framework that elevates third-party controls from best practice to regulatory necessity. CLIA’s stricter performance thresholds compound demand as laboratories widen QC frequency to retain accreditation. Canada’s modernization of medical-device regulations supports accelerated pathways for innovative quality controls, sustaining steady regional growth.

Asia-Pacific is the fastest-growing geography with an 7.74% CAGR, propelled by government genomics programs and expanding private diagnostic chains. Japan’s reimbursement of NGS oncology panels and South Korea’s investment in cell-and-gene therapy manufacturing both translate to higher QC consumption for NGS workflows. China’s domestic instrument makers increasingly embed QC lot-tracking software, amplifying local demand. Despite fragmented regulations, the molecular quality controls market benefits from APAC’s push to harmonize quality standards with ISO 15189 and IVDR principles, fostering cross-border product adoption.

Europe exhibits consistent mid-single-digit growth as IVDR implementation compels laboratories and manufacturers to upgrade quality documentation. The United Kingdom’s National Health Service awards central laboratory contracts that require ISO 15189:2022 compliance, embedding QC use in procurement templates. Middle East & Africa and South America remain nascent but show double-digit incremental gains where new reference laboratories open. In these regions, infectious-disease surveillance projects funded by multilateral agencies often stipulate third-party controls, giving suppliers an early foothold.

Regulatory Landscape

Regulation affecting molecular quality controls is tightening alongside expanded oversight of molecular diagnostics. In the United States, CLIA requirements for control procedures for molecular tests (including use of multiple control materials and inhibition checks where applicable) establish baseline expectations for routine QC. FDA guidance for infectious-disease NGS diagnostics further reinforces the need for positive, negative, and internal controls to monitor process performance. FDA quality system expectations also rise as the Quality Management System Regulation (QMSR) takes effect in February 2026, increasing the emphasis on harmonized quality-system documentation and postmarket controls across IVD-related suppliers.

In Europe, EU Regulation 2017/746 (IVDR) shapes how control materials are handled within the conformity assessment ecosystem, including risk-based classification that links certain control materials to the risk class of the associated IVD. Companion diagnostics under IVDR add consultation steps with the EMA or national competent authorities, raising the level of documentation rigor around analytical performance and suitability claims. Transitional timelines under IVDR (including a May 26, 2026 milestone for certain Class C devices) and the global transition toward ISO 15189:2022 accreditation together reinforce demand for traceable, independently sourced molecular QC materials that support risk management across the testing lifecycle.

Competitive Landscape

The molecular quality controls market is moderately concentrated. Bio-Rad, Roche, and Thermo Fisher anchor the top tier, leveraging broad assay portfolios and informatics layers to create high switching costs. Bio-Rad’s pending purchase of Stilla Technologies will blend digital PCR expertise with its independent control catalogue, expanding quantitative options for gene-therapy vector assays. Roche embeds sample-quality metrics into its NGS sample-prep kits, aligning control materials with workflow automation.

Mid-sized specialists such as ZeptoMetrix and Microbiologics focus on niche pathogen lines, often launching reference materials within weeks of emerging threats, a capability valued during outbreaks. Barriers to entry sit chiefly in regulatory proficiency and bio-manufacturing scale; newcomers typically partner with contract manufacturers to bridge gaps. Competitive differentiation is increasingly data-centric: platforms that stream QC results to cloud dashboards offer near-real-time performance analytics, a feature laboratories use to shorten troubleshooting windows from days to hours.

Opportunities abound in point-of-care and decentralised testing, where lateral-flow and microfluidic systems still lack robust third-party controls. Suppliers able to miniaturize controls for cartridge formats stand to capture incremental volume. Likewise, the rise of AI-powered quality-management software generates pull-through for control providers offering machine-readable certificates and barcode integration, reinforcing ecosystem lock-in beyond mere reagent sales.

Molecular Quality Controls Industry Leaders

Bio-Rad Laboratories Inc

F. Hoffmann-La Roche AG

ZeptoMetrix Corporation

bioMérieux SA

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A core opportunity lies in translating compliance requirements into scalable QC formats for multiplex, syndromic, and NGS workflows, where control burdens increase as assay complexity rises. CLIA control-procedure obligations for molecular tests and the limited applicability of IQCP for more complex molecular assays create whitespace for suppliers offering full-process controls (including inhibition-sensitive materials) and machine-readable documentation aligned to laboratory quality systems. As laboratories formalize ISO 15189:2022 risk management and traceability practices, control providers that pair third-party materials with data-management capabilities can differentiate by easing audit readiness and supporting cross-instrument comparability across consolidated lab networks.

Decentralization and automation also create whitespace for control designs that operate reliably outside traditional cold-chain, high-infrastructure settings. Development work around lyophilized and other stabilized control materials (including plasma-based controls designed for broader temperature stability) supports the need for QC suited to point-of-care and distributed testing models, while still meeting centralized quality expectations. Materials innovation, such as pseudovirus-based reference materials for nucleic acid testing, aligns with automated sample-to-answer systems, where controls that mimic clinical specimens and remain stable through extraction and amplification steps can support uptake across infectious disease, oncology, and emerging applications like cell and gene therapy quality control.

Recent Industry Developments

- July 2026: Bio-Rad launched Vericheck ddPCR kits for cell and gene therapy quality control applications. The launch extends molecular QC beyond clinical diagnostics into manufacturing-oriented workflows where quantitative verification is central to lot release and process monitoring. It also broadens Bio-Rad's addressable QC use cases alongside its existing molecular control portfolio.

- June 2025: ZeptoMetrix launched NATtrol Influenza A H5N1 Quantitative Stock using phage-like particle technology to support avian-influenza assay validation. The product targets high-consequence infectious disease testing where quantitative benchmarking and rapid verification are priorities. It strengthens ZeptoMetrix's positioning in outbreak-relevant reference materials that laboratories and developers use for method verification.

- November 2024: Microbiologics acquired SensID, expanding its diagnostic quality control portfolio into oncology and precision medicine. The deal adds capabilities aligned with complex molecular testing content, including controls suited to higher-plex and variant-driven assays. It also supports portfolio expansion beyond infectious disease into growth areas that demand more specialized QC designs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the molecular quality controls market covers third party and instrument linked control materials used to check, calibrate, and validate molecular test runs, so labs can confirm results for PCR, NAAT, and sequencing based workflows.

Scope exclusions: This sizing does not count broader lab consumables, generic reagents, or external proficiency testing fees unless they are sold specifically as molecular quality control materials.

Segmentation Overview

- By Product Type

- Independent Controls

- Instrument-specific Controls

- By Technology

- PCR-based

- NGS-based

- Isothermal/Other NAAT

- By Application

- Infectious Diseases

- Oncology

- Genetic / Hereditary Testing

- Reproductive and Prenatal Health

- Others

- By End-user

- Clinical Laboratories

- Hospitals and Academic Medical Centres

- IVD Manufacturers and CROs

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- South Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and keep definitions consistent across molecular control products and end users. We relied on public health and regulatory signals that affect routine QC use, including FDA guidance updates, CLIA CMS resources, and accreditation references like ISO 15189.

To quantify inputs, we also reviewed public sources such as CDC laboratory guidance, WHO and ECDC infectious disease surveillance updates, and peer reviewed publications on molecular diagnostics error rates, control frequency, and assay drift. In parallel, company annual reports, investor decks, press releases, and distributor catalogs were reviewed to map product positioning and typical pack formats. Select paid subscriptions were used for company financials and intelligence, patent databases, and news and financials to cross check product launches and revenue context. The sources named here are illustrative only, and many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on lab decision makers and QC specialists who can describe how often controls are run, what formats are preferred, and what drives switching between independent and instrument specific controls. We also interviewed quality managers at diagnostic labs, reference labs, and test manufacturers, then covered major geographies so adoption patterns in North America, Europe, and fast growing APAC markets were reflected in the assumptions used.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 50% |

| Mid tier: 56% | Functional/Unit leaders: 25% | EMEA: 30% |

| Smaller Players: 16% | Managers: 60% | Americas: 20% |

Market-Sizing & Forecasting

The sizing model starts with a top-down build that reconstructs demand from the molecular testing pool, and then applies realistic control usage rates and replacement cycles by technology type. Because labs do not run controls the same way across workflows, we adjusted assumptions using inputs on control frequency per batch, average tests per instrument per day, and the mix shift between PCR panels and NGS based assays.

To keep totals practical, we corroborated the model with selective bottom-up checks, such as rolling up sampled supplier revenues, channel checks on typical ASP by control format, and sanity checks on volumes tied to the installed instrument base. Where data gaps appeared, for example for smaller labs that primarily buy through distributors, we used conservative penetration ranges and then refined them during calls. Forecasting relied mainly on scenario analysis that combines expected molecular test volume growth, regulatory and accreditation pull, and price progression patterns, then cross checked the curve using expert views on how quickly multiplexing and automation are changing routine QC needs.

Data Validation & Update Cycle

Model outputs were checked against independent signals including molecular diagnostics testing trends, accreditation adoption, and the pace of instrument placements, then reviewed for spikes that did not fit known market activity. If an assumption created an unusual regional share or an unrealistic ASP movement, the logic was revisited and targeted follow ups were triggered with respondents.

We also ran a multi step internal review before sign off, including a separate analyst pass to confirm units, currency timing, and year to year continuity. Reports are refreshed annually, with interim updates when material events occur, such as major regulatory changes, supply disruptions for reference materials, or step changes in testing volumes. Before delivery, a final refresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Molecular Quality Controls Market Size Compared Against Other Published Estimates

Published market sizes for molecular quality controls can vary even when they appear to cover the same topic, since different studies set different product inclusions, base years, and pricing logic. Variation also comes from how each study treats instrument linked controls versus independent controls, and whether forecasts assume steady pricing or a faster shift toward higher value multiplex and NGS workflows.

Some external estimates appear to include adjacent laboratory QC and broader QA spend that sits outside molecular controls, which can pull the value upward. In the Mordor Intelligence model, the count is limited to control materials specifically used to validate molecular assay performance, and it is kept aligned to testing volumes and control run frequency, with annual refresh checks on ASP and mix by technology.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 239.72 M (2026) | |

| Global Consultancy A | USD 220.00 M (2024) | Uses an earlier base year and a different timing for currency and pricing, and the write up does not clearly separate molecular control materials from other lab QC line items, which can shift totals down or up depending on what is bundled. |

| Industry Publisher B | USD 215.20 M (2024) | Sets a narrower definition around selected product categories and relies more on supplier side reporting without clearly tying demand to test volumes and control run frequency, so adoption and utilization assumptions may not fully reflect lab practice. |

Taken together, the spread is mainly explained by base year choice and how closely each model stays to an observable demand pool. By keeping the steps traceable to test volumes, control usage patterns, and realistic pricing checks, the estimate becomes easier to reproduce and to adjust when the market mix changes.

Key Questions Answered in the Report

Why is the molecular quality controls market growing faster after 2026?

Demand accelerates as the FDA’s LDT Final Rule tightens quality-system requirements, compelling laboratories worldwide to adopt third-party controls and driving a 6.39% CAGR through 2031.

Which product category holds the largest molecular quality controls market share today?

Independent, vendor-neutral controls dominate with 57.52% share because they satisfy ISO 15189 documentation and cross-platform comparability needs.

How quickly are NGS-based quality controls expanding?

NGS-based controls are projected to rise at a 6.89% CAGR, reflecting oncology’s shift toward comprehensive genomic profiling and multi-gene hereditary panels.

Which region will contribute the most incremental revenue by 2031?

Asia-Pacific, poised for an 7.74% CAGR, will add the largest new revenue due to genomic-medicine initiatives and rising laboratory infrastructure investments.

What are the main cost pressures facing laboratories?

High per-run QC material costs and supply constraints for rare pathogen references can raise operational expenses by up to 7% of assay cost, especially in low-volume settings.

Page last updated on: