Molecular Biosensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

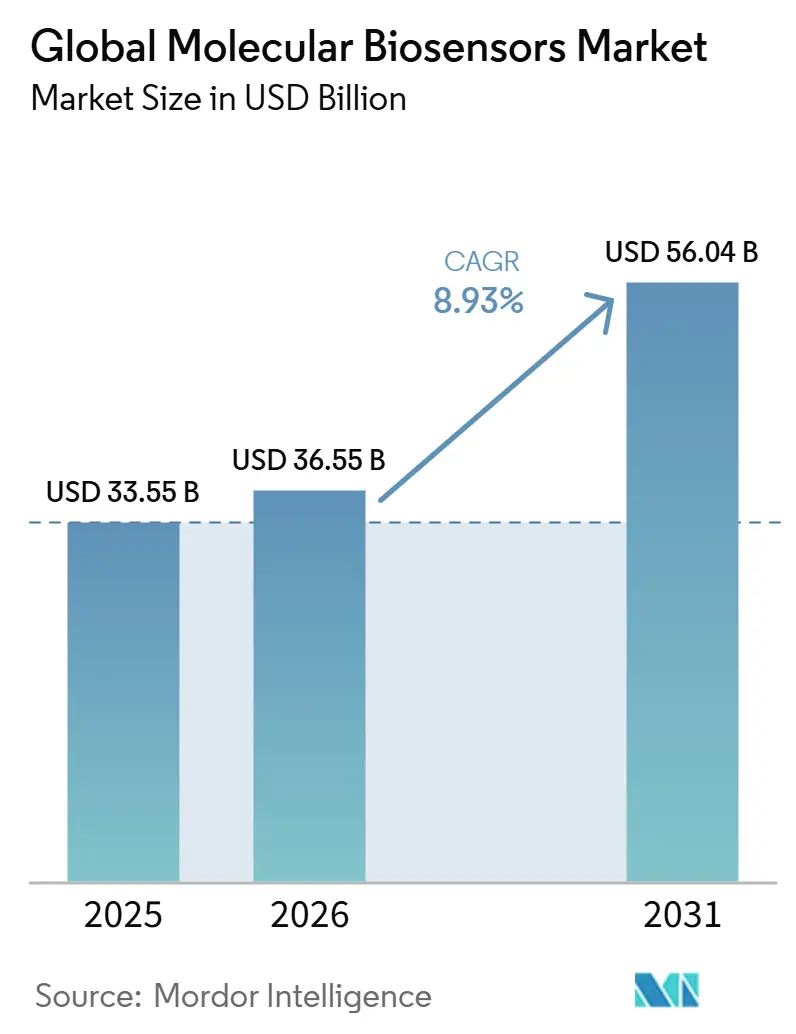

| Market Size (2026) | USD 36.55 Billion |

| Market Size (2031) | USD 56.04 Billion |

| Growth Rate (2026 - 2031) | 8.93 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Molecular Biosensors Market Analysis by Mordor Intelligence

The molecule biosensor market size was valued at USD 33.55 billion in 2025 and estimated to grow from USD 36.55 billion in 2026 to reach USD 56.04 billion by 2031, at a CAGR of 8.93% during the forecast period (2026-2031). Momentum stems from healthcare digitization mandates, stricter environmental-quality laws, and public investment in point-of-care diagnostics that accelerated after the COVID-19 pandemic. Regulatory sentiment supports broader consumer access; the US FDA cleared an over-the-counter continuous glucose monitor in March 2024[1]Source: US Food & Drug Administration, “Enforcement Policy for Over-the-Counter Continuous Glucose Monitoring Devices,” fda.gov , a landmark decision that removes prescription barriers for millions of diabetes patients. Molecule biosensor deployment cuts the time between specimen collection and clinical decision, creating measurable savings for providers while enabling real-time pollutant surveillance for utilities complying with the EPA’s 2024 PFAS thresholds. Competitive intensity is rising as incumbents and venture-backed entrants race to integrate nanomaterials, wireless connectivity, and AI analytics, signalling a pivot toward full-stack sensing ecosystems that address clinical, industrial, and public-sector needs.

Key Report Takeaways

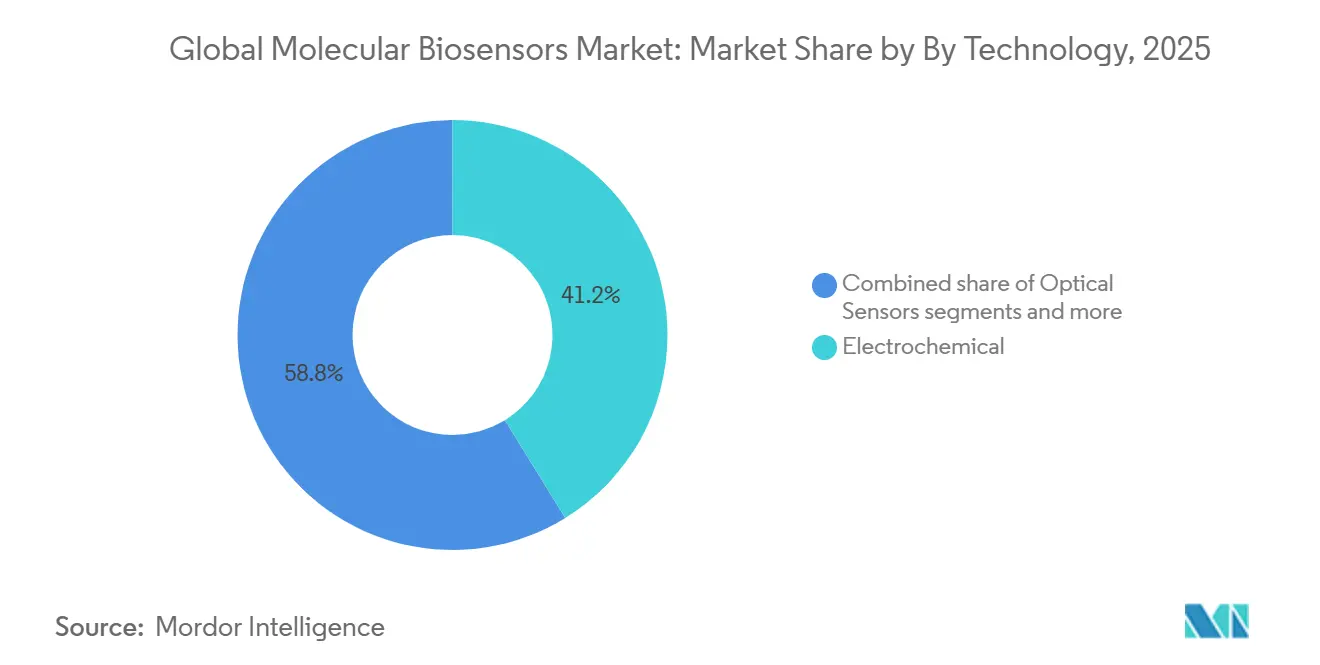

- By technology, electrochemical sensors led with 41.22% of the molecule biosensor market share in 2025, while optical sensors are forecast to post the fastest 9.88% CAGR through 2031.

- By product type, disposable formats commanded 37.71% share of the molecule biosensor market size in 2025, whereas wearable sensors are expected to record an 11.05% CAGR to 2031.

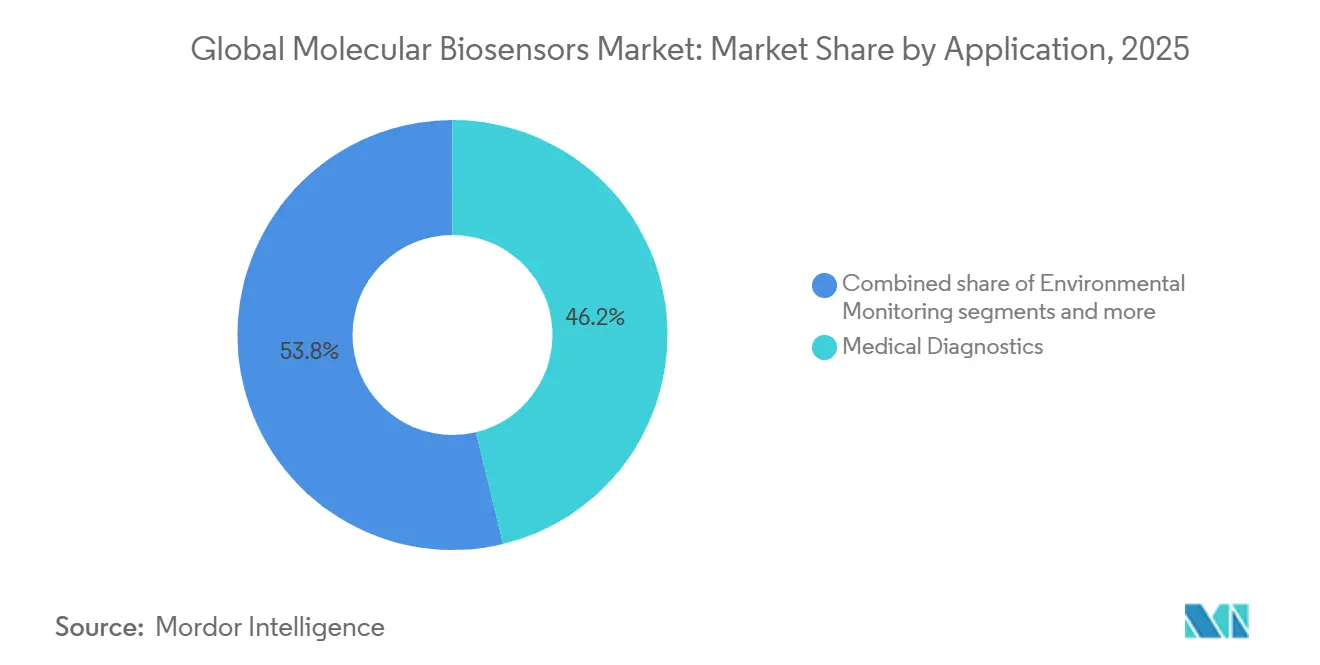

- By application, medical diagnostics captured 46.22% of the molecule biosensor market share in 2025; defense and security applications are projected to expand at a 10.65% CAGR through 2031.

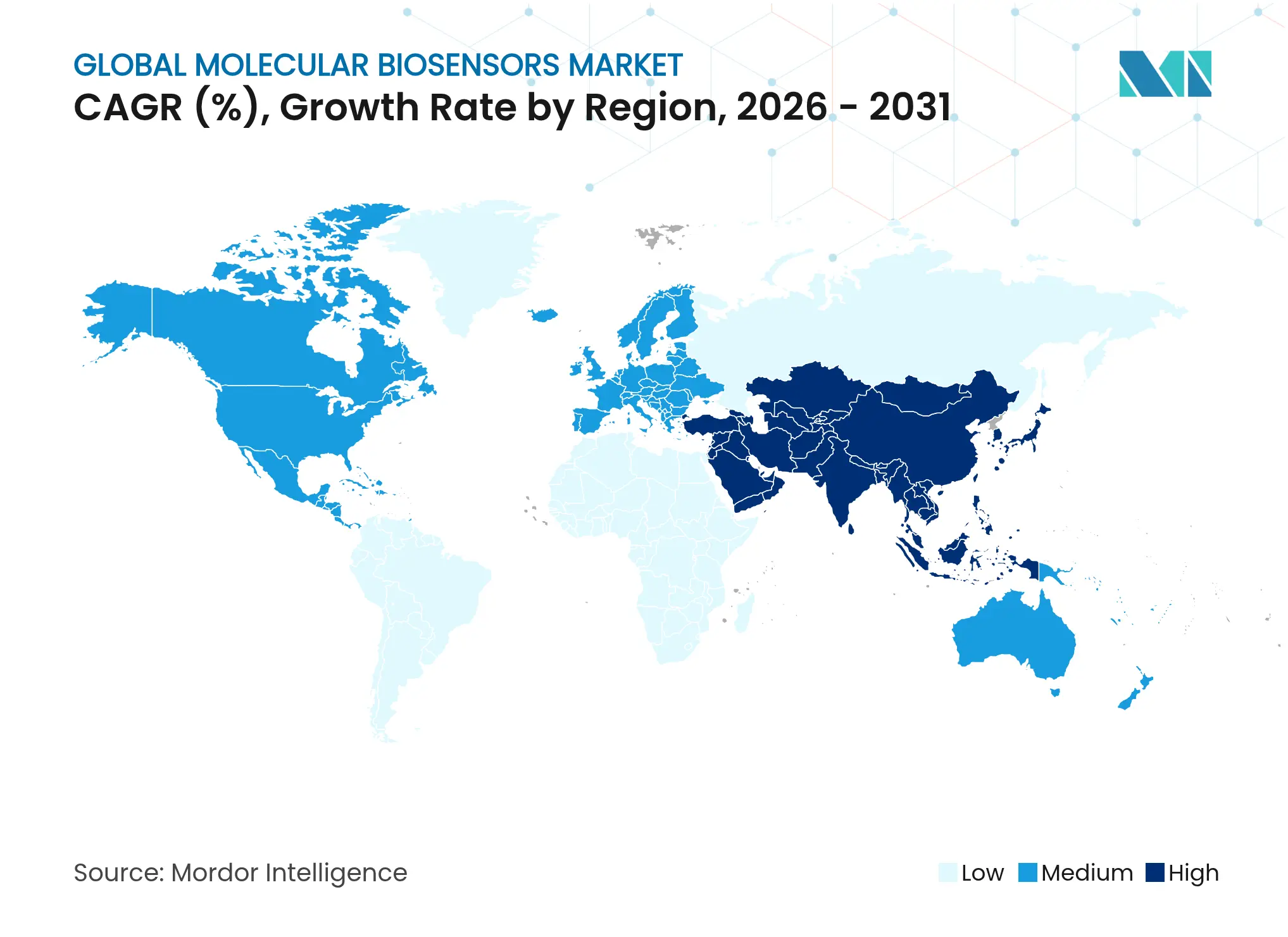

- By geography, North America retained 34.08% revenue leadership in 2025, while Asia-Pacific is set to advance at the highest regional 11.62% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Molecular Biosensors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid adoption of point-of-care diagnostics Rapid adoption of point-of-care diagnostics | +2.1% | Global, with acceleration in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Global, with acceleration in North America & EU | Impact Timeline:Medium term (2-4 years) |

Integration of IoT & AI for real-time sensing Integration of IoT & AI for real-time sensing | +1.8% | APAC core, spill-over to North America | Long term (≥ 4 years) | |||

Nanomaterials boosting detection sensitivity Nanomaterials boosting detection sensitivity | +1.4% | Global, led by research hubs in US, EU, Asia | Long term (≥ 4 years) | |||

Stricter environmental monitoring mandates Stricter environmental monitoring mandates | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Wearable continuous-monitoring biosensors Wearable continuous-monitoring biosensors | +1.0% | Global, consumer-driven in developed markets | Short term (≤ 2 years) | |||

Government pandemic-preparedness funding Government pandemic-preparedness funding | +0.8% | Global, concentrated in developed economies | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Adoption of Point-of-Care Diagnostics

Healthcare networks are rebuilding testing models around immediate answers at the bedside. The 2024 FDA clearance of an over-the-counter glucose monitor opened a consumer pathway for self-directed diabetes management. Molecule biosensors that deliver pathogen, cardiac-marker, or metabolic data within minutes reduce admission-to-treatment intervals in emergency departments and rural clinics. Smartphone-linked readers transfer encrypted results to electronic records, strengthening telemedicine programs and lowering follow-up costs. These efficiencies slash laboratory outsourcing expenses and create surplus capacity in overstretched central labs.

Integration of IoT & AI for Real-Time Sensing

Edge analytics transforms molecule biosensors from passive detectors into predictive sentinels. Researchers at Hokkaido University demonstrated a wearable patch that achieved more than 80% early-event prediction accuracy for arrhythmia, coughs, and falls by processing data locally on the device. Machine-learning models trained on continuous biosignal streams detect deterioration hours before symptoms appear, enabling proactive care that lowers readmissions. On-board calibration routines extend sensor lifespans, while secure cloud dashboards aggregate anonymized data for epidemiological surveillance.

Nanomaterials Boosting Detection Sensitivity

Graphene, carbon nanotubes, and plasmonic nanoparticles elevate signal-to-noise ratios and cut detection limits to femtomolar ranges. Graphene oxide chips reported three-fold sensitivity gains versus conventional substrates, allowing early cancer or HIV biomarker identification without fluorescent labels. Carbon-nanotube electrodes tuned by chirality control detect hormone fluctuations at parts-per-trillion levels, accelerating drug-development assays and personalized therapy adjustments. Multiplexed optical waveguides read multiple analytes on one disposable card, shrinking equipment footprints in space-constrained clinics.

Stricter Environmental Monitoring Mandates

The EPA’s 2024 PFAS regulation sets a 4 ng/L ceiling for specific contaminants, pushing utilities toward continuous, in-pipe molecule biosensing arrays. Wireless sensor meshes provide block-level pollution heat maps, enabling targeted remediation that saves millions in blanket treatment costs. Enzyme-stabilized probes endure high salinity and pH swings, making them ideal for coastal discharges and chemical-plant effluents. European water authorities are adopting similar models, creating a trans-Atlantic market pull for rugged, low-maintenance platforms.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost & complexity of miniaturization High cost & complexity of miniaturization | -1.5% | Global, more pronounced in cost-sensitive markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.5% | Geographic Relevance:Global, more pronounced in cost-sensitive markets | Impact Timeline:Medium term (2-4 years) |

Regulatory hurdles for clinical validation Regulatory hurdles for clinical validation | -2.2% | Global, strictest in North America & EU | Long term (≥ 4 years) | |||

Bioreceptor instability & shelf-life issues Bioreceptor instability & shelf-life issues | -1.1% | Global, critical for distributed applications | Short term (≤ 2 years) | |||

Data-privacy concerns around biosensing Data-privacy concerns around biosensing | -0.8% | Global, heightened in privacy-conscious regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost & Complexity of Miniaturization

Shrinking multi-parameter analyzers onto postage-stamp substrates requires sub-micron lithography and exotic polymers. Production yields fall when microfluidic channels clog during wafer bonding, raising scrap rates and pushing per-unit costs beyond the reach of budget-constrained clinics. Limited global foundry capacity with bio-compatible encapsulation creates year-long queue times, delaying commercial launches and extending breakeven horizons for investors.

Regulatory Hurdles for Clinical Validation

In-vitro diagnostic molecule biosensors must clear exhaustive analytical and clinical evaluations. The US FDA pathway often spans three years and costs double-digit millions, especially for multimarker devices without predicate comparators. EU IVDR rules add separate dossiers for every new biomarker, multiplying documentation workloads. Start-ups lacking dedicated regulatory teams face steep learning curves that erode first-mover advantages.

Segment Analysis

By Technology – Electrochemical Platforms Hold Cost Edge While Optical Systems Accelerate

Electrochemical sensors captured 41.22% of the 2025 molecule biosensor market share thanks to mature screen-printed electrode lines that churn out billions of glucose strips each year. Low operating voltage, rapid response times, and standardized reimbursement codes underpin continued demand across primary-care settings. Optical sensors, however, are set to log a 9.88% CAGR through 2031, driven by nanophotonic waveguides that register biomolecular binding without electrochemical interference. A Korean research team reported 99% accuracy in colorectal-cancer detection using an AI-enhanced optical chip, underscoring clinical potential for early-stage oncology screening. Thermal, piezoelectric, and nanomechanical modalities serve niche requirements such as label-free kinetics and temperature-indexed reactions, but they collectively account for a modest slice of the molecule biosensor market.

Electrochemical formats remain the preference for resource-limited clinics because they pair with existing readers and disposable strip logistics. Precision oncology centers and pharmaceutical QA labs favor surface-plasmon resonance benches that multiplex cytokines, hormones, and viral antigens on one slide. The divergence hints at a future where cost-sensitive mass-market testing and precision-critical specialty assays coexist rather than converge. Suppliers are therefore expanding catalogues into dual-platform offerings to hedge demand shifts.

Note: Segment shares of all individual segments available upon report purchase

By Product Type – Disposable Dominance Meets Wearable Upswing

Disposable cartridges held 37.71% of 2025 revenue within the molecule biosensor market size, reflecting infection-control protocols that soared after the pandemic. Single-use workflows wipe out sterilization overhead and streamline supply-chain audits for hospital procurement managers. Wearable devices are forecast to grow at an 11.05% CAGR, catalyzed by payer support for remote-patient monitoring programs and consumer demand for real-time metabolic feedback. Patches now achieve seven-day operational lifespans without calibration, cutting patient burden and strengthening adherence. Implantables serve neurological and cardiac indications, benefiting from bio-stable coatings that maintain signal fidelity beyond 30 days in vivo. Benchtop analyzers still anchor research labs that need high-throughput panels for drug discovery and environmental assays.

Adoption patterns suggest a shift from episodic testing toward continuous insight loops. Hospitals deploy disposable sensors for acute triage, while outpatient programs rely on wearables to stream longitudinal data into population-health dashboards. The molecule biosensor market is thus widening, not cannibalizing, as each format maps to a discrete clinical or industrial job-to-be-done.

By Application – Diagnostics Core While Security Surges

Medical diagnostics delivered 46.22% of 2025 sales, anchored by glucose, cardiac-marker, and infectious-disease panels integral to chronic-care guidelines. Robust reimbursement and clinician familiarity keep growth steady. Defense and security applications are projected to rise at a 10.65% CAGR through 2031 because military planners prioritize rapid biological-threat detection at borders and field hospitals. Environmental monitoring demand escalates in response to new pollutant thresholds that require continuous, in-situ measurement.

Food-safety authorities now deploy handheld molecule biosensors to screen incoming batches for Salmonella and Listeria, trimming costly warehouse quarantines. Precision-farming initiatives integrate soil-nutrient and livestock-health probes that feed agronomic AI engines, while industrial bioreactors use inline biosensors to detect contamination events before product loss. The versatility of molecule biosensor platforms unlocks stacked revenue streams across healthcare, agriculture, and manufacturing, broadening the total molecule biosensor market beyond its clinical roots.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 34.08% of molecule biosensor market revenue in 2025, propelled by established clinical trial infrastructure, extensive payer coverage for continuous glucose monitoring, and sustained federal procurement of pandemic-preparedness kits. Academic-industry clusters in Boston, Minneapolis, and San Diego channel National Institutes of Health grants into spin-outs that commercialize nanomaterial electrodes and AI calibration software. Partnerships between device majors and cloud vendors accelerate hospital adoption of end-to-end monitoring solutions that integrate smoothly with electronic medical records.

Asia-Pacific is forecast to post the fastest 11.62% CAGR through 2031 as national health systems pivot from manufacturing hubs to innovation epicenters. Japan’s digital-health market is tracking a 7.29% CAGR through 2028 on the back of government incentives for personal health record integration and AI diagnostics. South Korea’s AI health sector is projected to reach USD 6.67 billion by 2030, reflecting 50.8% CAGR powered by ubiquitous 5G coverage and more than 90% electronic medical record penetration. China and India channel sizable funds into domestic sensor fabs to secure supply chains and lower import reliance, positioning the region to generate high-volume exports of low-cost electrochemical strips within the decade. Europe sustains mid-single-digit growth through environmental monitoring directives under the Green Deal, which mandate real-time water-quality assessments across member states. Germany and the Nordics pilot smart wastewater grids that stream molecule biosensor data to municipal dashboards for pollutant hot-spot mapping. South American and Middle-East governments deploy molecule biosensors in food-export supply chains and mass-gathering health surveillance, creating foundational demand even where per-capita healthcare spending remains modest. The geographic mosaic underscores that the molecule biosensor market is no longer a transatlantic duopoly; it is a multi-polarity landscape with localized drivers and differentiated regulatory tempos.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The molecule biosensor market is moderately fragmented, with the top five suppliers controlling just over half of revenue. Abbott, Dexcom, Roche, Siemens Healthineers, and bioMérieux leverage scale manufacturing, global sales teams, and regulatory expertise to secure hospital contracts. bioMérieux acquired Norway-based SpinChip Diagnostics in January 2025[2]Source: LabMedica International, “bioMérieux Acquires Norwegian Immunoassay Start-Up SpinChip Diagnostics,” labmedica.com , adding ten-minute whole-blood immunoassays to its point-of-care portfolio.

Venture-backed challengers target unmet needs with fresh architectures. Biolinq’s intradermal sensor promises multi-analyte coverage in a coin-sized patch and attracted USD 100 million in Series C funding in April 2025. Spin-outs from Stanford, MIT, and Seoul National University explore graphene and photonic crystal structures that lower detection limits to picomolar ranges, appealing to oncology and neurology specialists. Partnerships between semiconductor foundries and bio-foundries provide design toolkits that shorten development cycles for start-ups, yet scale production remains a hurdle until pilot volumes justify dedicated lines.

Competitive strategy is tilting toward services. Device makers bundle consumable cartridges with subscription analytics that visualize trends and deliver clinical decision support, converting razor-razorblade models into sticky software-as-a-service revenue. Hospitals favor integrated vendors that shoulder cybersecurity compliance and data-integration overhead, squeezing smaller firms that offer only hardware. Nevertheless, white-space segments—such as rare-earth detection, personalized nutrition, and industrial bioprocess monitoring—remain wide open for niche innovators, preserving a balanced competitive environment.

Molecular Biosensors Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stanford University unveiled SENSBIT, an implantable platform that tracks molecular profiles for a full week in live subjects, marking a breakthrough in sensor durability

- April 2025: Biolinq closed a USD 100 million Series C to commercialize a precision multi-analyte wearable after successful US pivotal trials

Table of Contents for Molecular Biosensors Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid adoption of point-of-care diagnostics

- 4.2.2Integration of IoT & AI for real-time sensing

- 4.2.3Nanomaterials boosting detection sensitivity

- 4.2.4Stricter environmental monitoring mandates

- 4.2.5Wearable continuous-monitoring biosensors

- 4.2.6Government pandemic-preparedness funding

- 4.3Market Restraints

- 4.3.1High cost & complexity of miniaturization

- 4.3.2Regulatory hurdles for clinical validation

- 4.3.3Bioreceptor instability & shelf-life issues

- 4.3.4Data-privacy concerns around biosensing

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts

- 5.1By Technology (Value)

- 5.1.1Electrochemical Sensors

- 5.1.2Optical Sensors

- 5.1.3Piezoelectric & Acoustic Sensors

- 5.1.4Thermal & Calorimetric Sensors

- 5.1.5Nanomechanical & Cantilever Sensors

- 5.2By Product Type (Value)

- 5.2.1Wearable Sensors

- 5.2.2Implantable Sensors

- 5.2.3Disposable Sensors

- 5.2.4Benchtop / Stand-alone Sensors

- 5.3By Application (Value)

- 5.3.1Medical Diagnostics

- 5.3.2Environmental Monitoring

- 5.3.3Food & Beverage Safety

- 5.3.4Industrial Process Control

- 5.3.5Agriculture & Livestock

- 5.3.6Defense & Security

- 5.4By Geography (Value)

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1GCC

- 5.4.5.2South Africa

- 5.4.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Abbott Laboratories

- 6.3.2F. Hoffmann-La Roche AG

- 6.3.3Thermo Fisher Scientific

- 6.3.4Siemens Healthineers

- 6.3.5Honeywell International

- 6.3.6Medtronic plc

- 6.3.7Sensirion AG

- 6.3.8TDK Corporation

- 6.3.9QIAGEN N.V.

- 6.3.10Danaher Corporation (Cepheid etc.)

- 6.3.11Bio-Rad Laboratories

- 6.3.12Agilent Technologies

- 6.3.13Teledyne FLIR

- 6.3.14Hologic Inc.

- 6.3.15Yokogawa Electric Corporation

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Molecular Biosensors Market Report Scope

As per the scope of the report, a molecular biosensor is a device that uses specific biochemical reactions mediated by isolated enzymes, immunosystems, tissues, organelles, or whole cells to detect chemical compounds usually by electrical, thermal, or optical signals and is, thus, able to facilitate rapid detection and diagnosis at the Point-of-Care (POC), which make them particularly useful for an early and unequivocal diagnosis. The Molecular Biosensors market is segmented by Technology (Electrochemical Biosensors, Optical Biosensors, Thermal Biosensors, Piezoelectric Biosensors), Application (Medical Diagnostics, Food and Beverages, Environment Safety, Defense and Security and Others, and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.